The CRE meltdown just doesn’t let up.

By Wolf Richter for WOLF STREET.

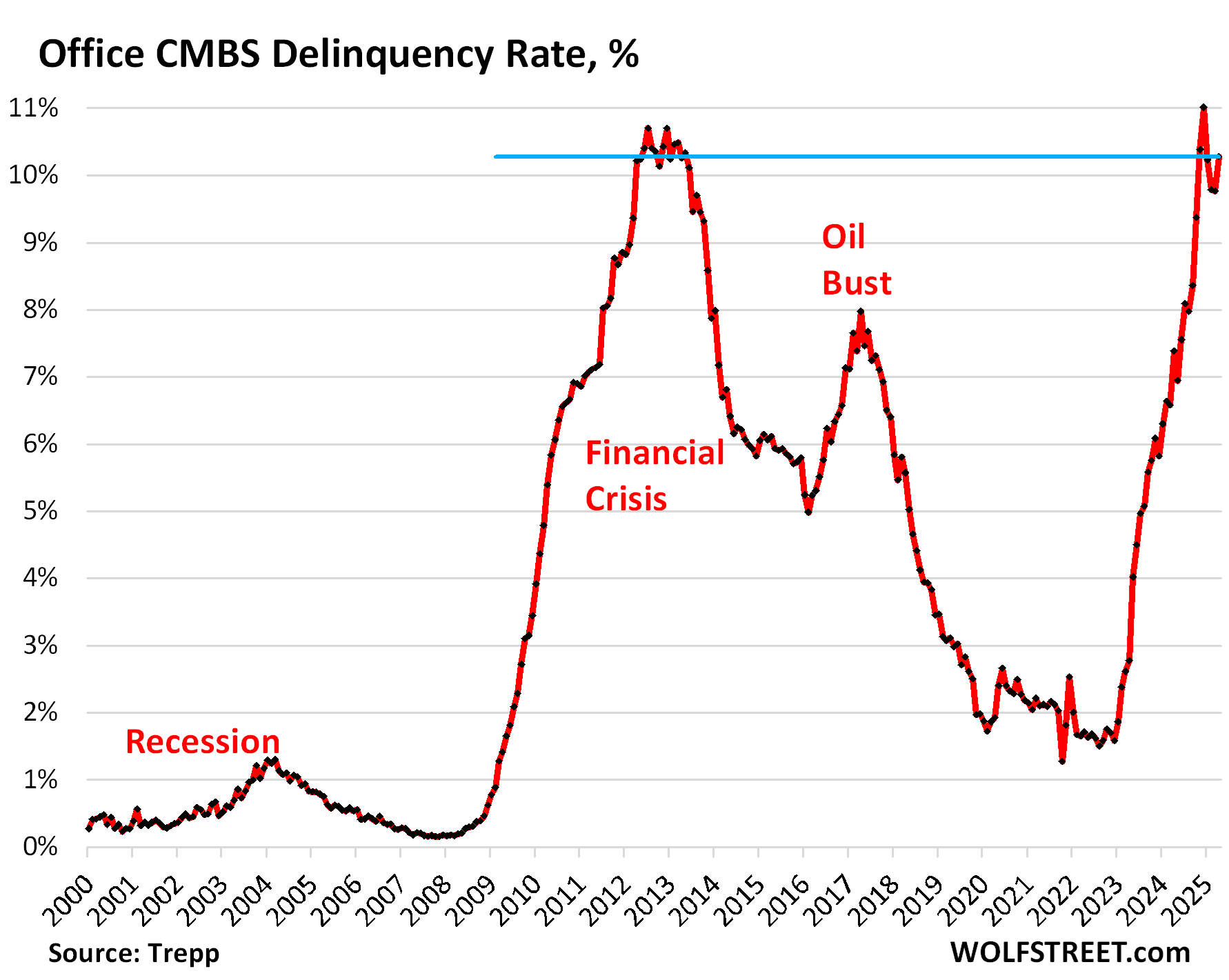

Delinquencies of office mortgages that were securitized into commercial mortgage-backed securities (CMBS) have been in the red-hot zone since mid-2023 and in December 2024 hit 11.0%, surpassing even the debt-meltdown during the Financial Crisis. Then, during the first three months of 2025, the delinquency rate backed off some, but in April re-spiked by 52 basis points to 10.3%, according to data by Trepp today, which tracks and analyzes CMBS.

The 52-basis-point increase of the delinquency rate represented a U-Turn from the feeble signs of hope earlier this year and put the delinquency rate right back into the peak of the Financial Crisis meltdown.

A flight to quality has divided the office market into two: Amid much reduced demand for office space, vacancies in the latest and greatest buildings allow companies to move from older office towers into new fancy offices, while downsizing space at the same time. But landlords of older properties have trouble finding new tenants to replace them, and their vacancy rates have soared. It’s those older office towers that are on the problem list, not the latest and greatest towers.

The office sector of commercial real estate (CRE) has been in a depression for two years, and the office vacancy rates in the US worsened to a record 22.6% in Q1. But it’s now multifamily CRE (rental apartments) that is chasing after it.

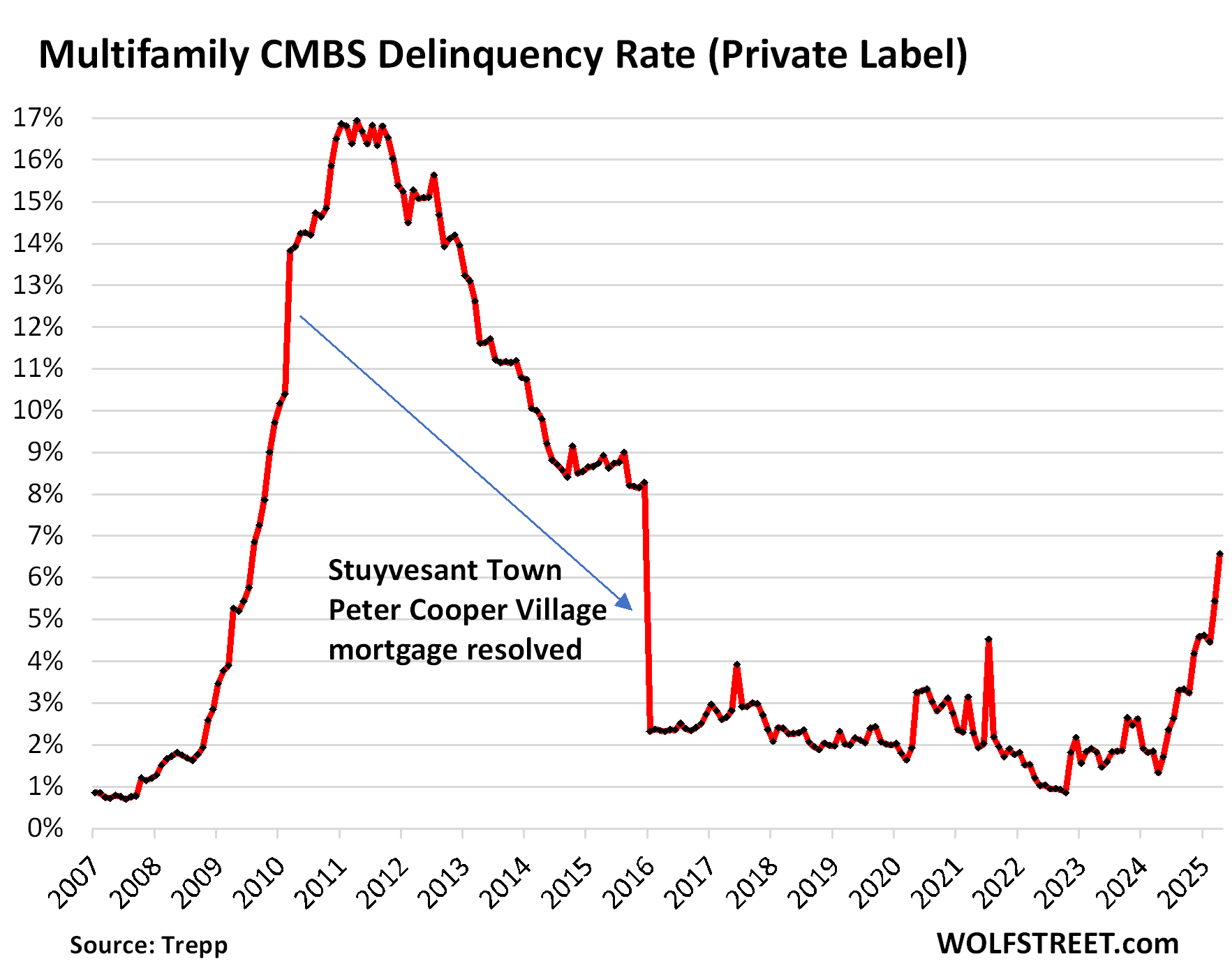

Multifamily is huge and delinquencies are turning ugly.

The multifamily CMBS delinquency rate in April spiked by 113 basis points, after spiking by 98 basis points in March, for 2.11 percentage points in two months, to 6.57%, having nearly quintupled year-over-year from 1.3% in April 2024.

These multifamily CMBS are “private label” — the mortgages in their mortgage pools are not backed by the government. More on government-backed multifamily mortgages in a moment.

The spike in delinquencies in April was triggered by over $1 billion in debt becoming newly delinquent, with the top three mortgages in that group amounting to $831 million, according to Trepp.

The plunge in January 2016 reflects a $3-billion delinquent mortgage on Stuyvesant Town–Peter Cooper Village in Manhattan (11,250 apartments spread over 110 buildings on 80 acres) that was paid off when Blackstone and Ivanhoe Cambridge purchased the complex. That mortgage had become delinquent in March 2009 and had contributed substantially to the Financial Crisis spike. The arrow connects the month of delinquency and the month when the delinquency was resolved.

Overall multifamily debt (not just CMBS) is the largest category of CRE debt, with $2.2 trillion in mortgages outstanding at the end of 2024, accounting for 45% of the $4.8 trillion in total CRE debt, according to the Mortgage Bankers Association.

That $4.8 trillion in CRE debt excludes loans for acquisition, development, and construction; and loans collateralized by owner-occupied commercial properties, in order to reflect the performance of properties that rely on rents and leases to make mortgage payments.

Governments are on the hook for over half of multifamily debt:

- Federal, state, and local governments: $1.17 trillion (54%), many of them securitized into government-backed CMBS:

- Federal government: $1.07 trillion (49.8%), mostly Fannie Mae and Freddie Mac, which have tripled their exposure over the past 10 years.

- State & local governments: $92 billion (4.2%)

- Banks and thrifts: $628 billion (29.2%)

- Life insurers: $255 billion (11.8%)

- private label CMBS, CDOs, and other Asset Backed Securities (ABS) issues: $68 billion (3.2%)

Multifamily debt securitized into CMBS accounts for only a small portion of the total multifamily debt. In general, CMBS make up only a small portion of CRE debt. The rest of CRE debt is spread across other investors, governments, and banks.

But CMBS delinquency rates shed some light on the tough situation CRE is in overall.

Mortgages count as delinquent when the landlord fails to make the interest payment after the 30-day grace period. A mortgage doesn’t count as delinquent if the landlord continues to make the interest payment but fails to pay off the mortgage when it matures, which constitutes a repayment default. If repayment defaults by a borrower who is current on interest were included, the delinquency rate would be higher still.

Loans are pulled off the delinquency list when the interest gets paid, or when the loan is resolved through a foreclosure sale of the property, or a sale of the loan, generally involving big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended – the infamous extend-and-pretend.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Keep your powder dry.

Over the past 10 years, Loopnet has had limited to no offerings for multifamily in my area in the Great Lakes region. Over the past 6 months, I am seeing more and more pop up. There is still no buying opportunity IMO, but seeing some hit the market is a start. Commercial/Industrial space has been available and matches exactly what Wolf writes. Older buildings are tough to fill, while newer buildings are still performing well.

Great article here and love to see this analysis!

I look at what is happening in this space and am so glad I sold off my office building in late 2023. I don’t think I would fetch the same price today.

Here in Tucson, apartment market still

WAY OVERPRICED

$100,000+++ for units

4 unit for $550k in so-so area

when I did my 1031 in 2022 I ended up buying 3 houses instead of multi-unit

very glad I did

It’s not an old building problem, but rather where they are located. In higher income areas, you most likely have to charge less for rent than “luxury” apartments, but filling up vacancy isn’t an issue otherwise.

Echoing Nathan – excellent and useful stats, Wolf.

The breakdowns/breakouts of who owns which kind of loans and aggregate market size data are all very useful.

I’ll post more, later, after I’ve had more time to reflect – but one immediate thought.

Mortgages (and not just apt complex mortgages) held by publicly traded CMBS may be the junkiest and therefore have the worst delinquency/default rates.

Maybe.

Basically because professional institutional investors (banks/insurers/etc) will only buy the better underwritten mortgages with the best protections – whereas the invt banks peddling the crapola mortgages (aggressively over-valued collateral, pathetic lender protections, etc.) are not shy about shoveling, ahem, shinola into the public markets (reputational effects now being a long dead and by now fully decayed corpse).

And make government guarantees available for the crapola mortgages CMBS?

You are immediately talking about barbarian hordes (invt banks) eyeballing Vestal virgins (taxpayers/USD holders).

I got laid off from this industry in November. I was doing acquisitions and yes a bloodbath in this could be coming. The smart people didn’t get 3% loans and overbid for properties.

Even the smart people make mistakes, sometimes. It’s easy to get caught up in market exuberance and think this time is different. I admit, though, that the EXCEPTIONALLY smart people, like Warren Buffett and George Soros, don’t fall for routine mistakes very often, if ever…

I work in class C market and huge increase in prices has been great for occupancy and rental rates

ex. 1 Bed class A over $1,000 easy all day

me $650 – nice remodeled units

cash flow is name game

Be interesting to know how many small US banks have most of their capital in one or two CRE assets. It is not easy to get AI to tell how many US banks currently have less than a hundred million in assets. Most precise data I found is from 2020:

‘Nearly a fifth of banks hold less than $100 million in assets, and the industry median is about $300 million.’

When these micro-banks collapse and are taken over by the FDIC, no one outside of the small towns they’re in even notices. There was one earlier this year, and a couple last year.

I noticed the one in January and the one from October. Both a few months after the fed started to cut rates. I looked back at the failed bank history back to 2007-2008 and noticed the majority started to fail after the fed began to cut the rates (faster than they are now of course)

So should we see the banks start failing once the fed gets on the roll with cutting rates (earning reports propped up due to high interest rates currently)

When multiple regional banks collaborate to provide a large loan, it’s typically referred to as a syndicated loan or a loan syndicate. A syndicated loan is a financial arrangement where a group of lenders (in this case, regional banks) pool their resources to finance a single borrower. This approach allows for larger loans to be made possible and also distributes risk among the lending institutions

Worked at a regional in Georgia and we were part of larger loans. Our leadership gave us the high level to show how we were part of the big picture

AI is not a search engine.

All gen AI does is predict what word should come after a word. It is not a reliable way to find information.

Taking it a little deeper, it builds responses by predicting the next word or phrase (called tokens) out of potentially trillions using what’s called an “attention mechanism” (a little piece of software), and constantly attempts to score each budding response against the others. The response with the highest score wins. Whether it is reliable or not is based on the number of available tokens and the number of links between them as well as the quality of the attention mechanism. If it has all the right information and right relationships, it can be very reliable.

When rents and values were going up fast many people overpaid in bidding wars. There are a LOT of ownership groups out there in trouble since expenses are going up faster than rents (and many of the properties can’t even pay the loans I/O portion). Insurance is the biggest expense outpacing inflation but maintenance numbers have been skyrocketing as more and more “can fix anything” baby boomer maintenane guys are retiring and the younger guys seem to be having a harder time than in the past actually fixing problems (even using spartphones and watching YouTube videos).

No Boomer, but a maintenance guy here:

A difficulty in maintenance and repair is certainly related to quality. Both the original items and certain materials used to repair/ replace are often in decline. (I do concede that so is knowledge/ ability in this field too).

This seems to have been accentuated by the “post-pandemic economy.” It was notable that production lacked quality control immediately during/ after pandemic, many reasons were cited: idling of production, shuffle of personnel, lack of supply for the “first choice” parts/ materials.

This is a culmination of the 4+ decades of the “China effect” that had already decimated product quality.

I have found that even some basic materials: adhesives, fasteners, chemicals/ compounds have suffered a decline in quality in recent years.

Finally: especially for an older building/ facility, parts availability and systems support is disappearing for much “outdated technology,” which can vary greatly from only 5-10 years old (computer/ electronics equipment including lighting) to considerably older for some things (basic plumbing from decades ago is similar).

“Basic materials “ I personally would not use the word basic because adhesive fasteners and chemicals all have been very selective in their origins and purpose and can’t be replaced with off the shelf products as u say quality and specs deteriorate

I’m on the very small-scale end of this, but still seeing insane closing prices of existing multis in my neck of the woods. The last one we purchased closed in March of 2020. Since then there has been nothing reasonable (reasonable to me is the rents have to cover all expenses and provide a profit, and I’m not going into a deal needing to double the rents to make the numbers work). The last one was a 1970s build priced at close to parity with what a new build would cost. I’ve been moving slowly in the direction of a new build (prefer existing multis but can’t wait for ever…I’m in a building trade and I have my hands full with that work as it is, not a huge desire to take on additional projects). My commercial loans on our existing multis all have 5-year fixed rates then start floating in 21 months (we refinanced them all in January 2022 and got in front of all the rate increases, because I read this website). If prices start coming down, great. It’s about time.

So, does the rise in delinquencies have more to do with the inability make higher post-refinancing loan payments than with tenants not being able to pay their rent?

You don’t understand. Did you miss it here? There is an office glut. Record amounts of vacant office space, see article. Many of these older office buildings have huge vacancy rates. If 50% of the building is vacant with no tenants, the cash flow gets cut in half, and even payments on an existing fixed-rate interest-only mortgage with a low 2021 interest rate cannot be made from cash flow, and then the landlords stops making the payments instead of plowing new money into the building to fund the interest payments. So that’s a “term default.”

Then there is the issue of a landlord not being able to refinance a maturing mortgage because of high vacancy rate in the building and a higher interest rate on the mortgage, that guarantee that cash flow from the building will not be enough to make the future mortgage payments, and then no lender will offer financing. When the maturing mortgage cannot be refinanced with a new mortgage, you have a “maturity default.”

So what is your estimated timetable on regional banks to start failing? Opinion obviously I will not hold you to it.

They’re not going to fall because of CRE. They’re just going to lose some money on their CRE loans, that’s it. But they’re hugely profitable, so if they have to write off some stuff, they’re just going to make less money, or have some losses. That’s part of being a bank. And their stocks will get hit, but so what. They might fall for other reasons. Three already fell for other reasons. US banks are not big holders of CRE, as I point out in the article. For example, all 4,000 US banks combined only hold 29% of the multifamily debt. In the article, “banks” = all banks, including foreign banks, and foreign piled heavily into US CRE. So US banks hold even less than 29% of multifamily debt.

I’m wondering if the question was more related to the increase in multi- family delinquencies?

Especially with the perpetual “housing shortage” every realtor advertises and the used house market frozen.

Are people not paying rent, or moving out (back to mom’s basement or into an incentivized new home ?) Or is it just overbuilt in certain markets?

I know you’re struggling, but “You don’t understand. Did you miss it here? There is an office glut. Record amounts of vacant office space, see article. Many of these older office buildings have huge vacancy rates.”

Wolf, a thought – maybe you should consider do these explanations at the top of the article? Yes, we need them; sorry. Yes, you can think we are dumb; I claim no expertise.

People sometimes only read the top, on occasion the bottom.

Anywho – interesting article! My guess is a bit of tight-belting here, a bit of overhead cutting there for the smaller guys (who would be the customer profile for old office space), and, perhaps, a bit of small businesses becoming collateral damaged if their model was based on the China trade. Still early days.

Nate, are you suggesting that Wolf should lead with a headline such as

“Multi family delinquencies increase, due to massive glut in office space”?

I don’t follow CRE much, though it seems to be virtually dying, starting with malls/ brick n mortar 20+ years ago, now offices of all types. It’s reminiscent of a commodity boom/bust cycle.

One defining characteristic of this site is data, as opposed to opinion. Also, this is the comment section, not the Q&A. Though I rephrased another person’s comment and inserted a bit of personal opinion.

If you’re asking about MF loans then yes, it’s much more about the cost of debt, plus a bit about rising costs for asset owners, than it is about tenants not paying rents. There has also been a rise in vacancy in some overbuilt Sunbelt markets.

Any breakdown by geography for the multifamily delinquency? Sunbelt is famous for boom/bust cycles in multifamily rental.

In San Francisco, “multifamily” might be more accurately termed “multicoder,” as the residential trouble spots up and down Market and across SOMA are mostly studio and 1Br apartments and condos heavily targeted to well-paid, young coder singles, and almost none of it is family housing of any income cohort.

How are NEMA, Trinity, Serif, et al, doing wrt outstanding loans? Based on the direction of the majority of moving vans and the slow uptake of vacant office space, hiring in the AI hotspot doesn’t seem to be keeping pace with the ongoing downsizing in most of the rest of the software sector: slowdown in new non-AI startups, consolidation in large firms, and still slow-paced return-to-office for those companies not downsizing.

NEMA was facing foreclosure in 2023, but the landlord held a gun to the lenders’ head — something like “either make me a deal I can’t refuse or take the effing building” — and they made a deal and modified the mortgage, and it seems to be fine now. Lenders will do nearly anything these days to not end up with an apartment or office tower.

I wonder if it is cheaper to renovate (upgrade) an older office building, or simply tear it down and start over. Or maybe turn it into upscale apartments, as was done in some office buildings in NYC. I suppose it depends a lot on local factors (nobody wants to locate in a downtown ghetto scene) and the general state of the older office building. I dislike seeing nice old buildings torn down, usually replaced by super-ugly modernist (as in cheap) architecture.

Mmm…I would say that would be a nice dilemma to have from the delinquent landlords. They can’t pay their debt already, so I’m guessing either a tear-down or a renovation is not in the cards.

Sometimes, a distressed property is an opportunity. Other times, it has a reason that a cheap investment will not solve.

This concept has been discussed here at length previously — it’s just not practical to create residential space out of office building floors. The outer perimeter, with windows, could work, but the inner core of the building would be difficult to utilize. That’s ignoring the costs of plumbing, electrical, HVAC, and all the other changes… The value in some of these older towers is purely in its footprint.

Dirty work, In fact there was just an article this last week about an office building that was converted into upscale apartments in New York City, and about how the Flat Iron Building in New York City will undergo a similar transformation. As I mentioned, it depends a lot on the location. I imagine for most old office buildings, a tear-down is their likely future, sadly.

Here is some AI stuff. It is probably correct.

“In 2025, New York City is witnessing a significant trend of converting office buildings into apartments. One notable project involves the former global headquarters of the pharmaceutical company Pfizer, located at 219 E. 42nd St. in Manhattan. This conversion is expected to create 536 rental units, contributing to the growing number of office-to-apartment conversions in the city.

The New York metropolitan area has over 305.4 million square feet of office space suitable for conversion into residential space, accounting for nearly 46% of the area’s total office inventory.

The number of planned office-to-apartment conversions has nearly doubled from 2022 to 2025, rising from 23,100 to 70,700 units.

The Pfizer headquarters conversion is part of a larger trend where developers are converting underutilized office buildings into residential spaces. Metro Loft, along with David Werner Real Estate, is converting the Pfizer buildings into around 1,600 rental apartments. The first tenants are expected to move in at the end of the following year.”

AI can’t do math:

“ doubled from 2022 to 2025, rising from 23,100 to 70,700 units.”

t2 – this isn’t NYC’s first building-conversion rodeo, where the ’60’s-’70’s affordable-‘lofting’ movement among the old factory structures of the SOHO-area by artists and bohemians, eventually morphed into trendy, high-cost residential real estate. (The floor-architecture of what was converted, and the determination of the new urban pioneers to work with/around/dodge code restrictions doubtlessly differed from the current zeitgeist and architecture of the real estate now coming into play…).

Funny how little attention MSM has even mentioned this….their entire attention span is on the residential side and how everything on that end is still hunky dory..

Presumably, because that is how much of MSM’s audience has a huge chunk, if not almost all of their positive net worth. Or they are looking to own a home as it was an American birthright?

Media reports what their audience finds interesting to sell advertising space.

yup agreed and I like your question about homeownership as a birthright….call it birthright, rite of passage, American dream, “you made it” narrative. One only has to look at /mortgage to see how many people pay through the nose to obtain this rite of passage instead of seeing it as an expense item that can provide some stability and shelter

Maybe MSM will paying more attention to this if this end up triggering something bigger in the tune of GFC, if not, then it will likely remain forever a nothing burger in general population’s zeitgeist

Honestly not like home ownership is all that high in this country. Stable yes. High, not so much. Not a good or bad thing as some can’t afford to buy and of course some don’t choose to buy. There is also the subjective conversation of what constitutes home ownership but that is something else entirely.

Msm in usa is what gets flushed down the toilet….

i really hope that the fed and congress bail out cmbs soon. there’s no reason any investor should ever have to take a loss on anything. it’s basically un-american.

Agreed.

“The CRE meltdown just doesn’t let up.”

(Not really just about CBRE but so many American macro imbalances…)

Not when governmental policy (interest rate and otherwise) is almost entirely hewn to obscure market signals until the farce cannot be hidden/obscured anymore and true economic fundamentals (long building, long disguised at greater cost) reveal themselves in an explosion.

That is why so many of Wolf’s graphs show incredibly steep increases in (almost always bad) metrics – the G continually says “No problem” while desperately, behind the scenes, trying to find a miracle fix/bagholder.

Out here in the Central Valley of California, the same old junk apartments I lived in 45 years ago are still sitting there like I used a time machine.

That stuff will be there depreciated, and maybe 1031 exchanged if that works, for the next couple of centuries.

With future MBS quantitative easing (QE) by the Federal Reserve and California residential building restrictions, those apartments are guaranteed to have a steady stream of unfortunates (California upper middle class and below).

In my area, apartments went up everywhere and are still being built. It worked once, twice, three times, keep doing it cuz that all we know… and now there’s too many, unable to command rents, 3-year interest only ARMs are due… numbers no longer work.

Yeah Wolfman, as far as multifamily housing, Hathaway Apartments (about 0.5 miles west of Hathaway Bridge in Panama City Beach) stopped construction after breaking ground last spring.

Hathaway Luxury Apartment LLC is owned or managed by Marvin Setness a Controller – RD Offutt Company.

I wonder why a major potato / agriculture company (RD Offutt Company) is an apartment developer in Panama City Beach :-/

Major agriculture also means major real estate owner. And building just about anything can be more profitable than using the land for agriculture. The history of Florida is rounding up wild spanish cattle on your government grant land, to breeding proper English breeds, to converting the land from cattle to citrus, from citrus to other fruits and vegetables, and finally to office, retail and housing. Almost all of the great developers in Florida started 150 years ago as land grant people. Bill Nelson, ex-Florida Senator and NASA head made his fortune developing his family land in the Melbourne, Palm Bay area.

Multi family net yields are lower than T-bills across the country. Prices will come down.

When @Kent wrote:

“Almost all of the great developers in Florida started 150 years ago as land grant people.:

It reminded me of the quote: “The children of California Farmers usually stop farming and get into real estate development”…