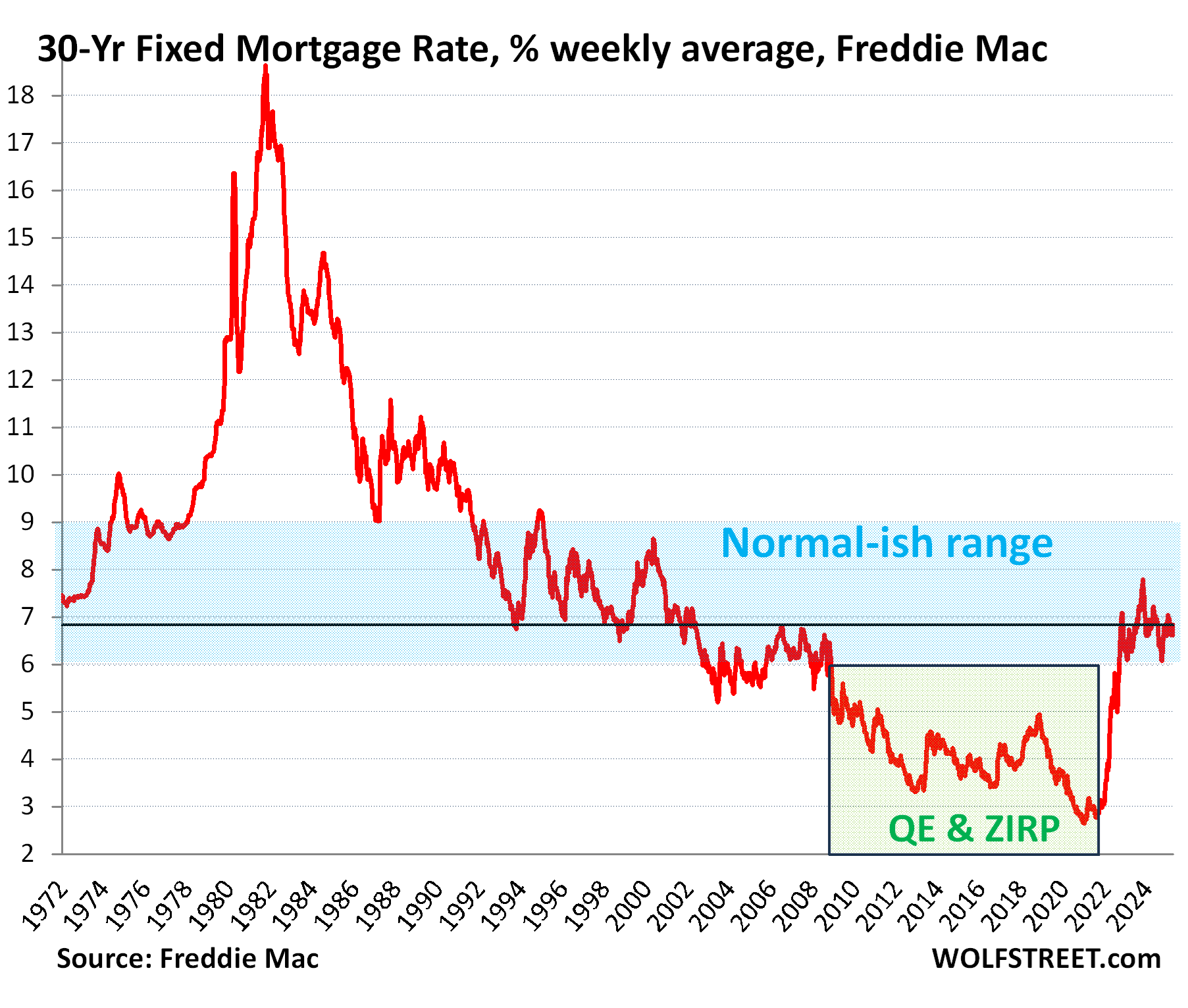

The 3-year 50% price explosion has caused epic demand destruction. Prices are way too high. But mortgage rates are back in the historically normal range above 6%.

By Wolf Richter for WOLF STREET.

The feverishly anticipated spring selling season is starting out as a dud. Sales of existing homes – single-family houses, townhouses, condos, and co-ops – that closed in March fell by 3.1% from the already frozen volume a year ago to 315,000 deals, not seasonally adjusted, down by 31% from March 2022, which was when home sales began to plunge after prices had spiked in many markets by 50% or more in just three years, to ridiculous levels, thereby destroying demand.

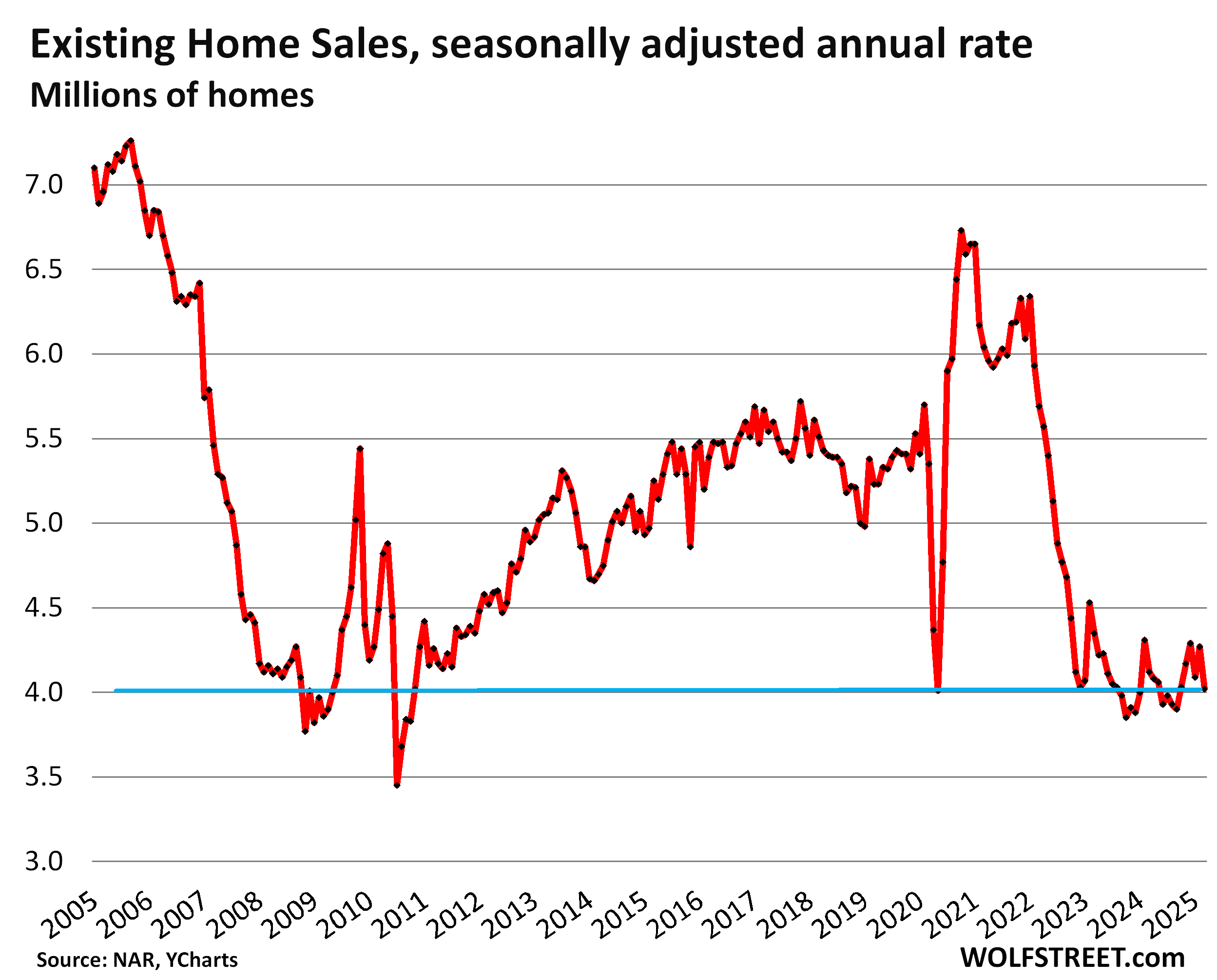

Demand destruction on display: The seasonally adjusted annual rate of sales of existing homes fell by 5.9% in March from February, and by 2.4% year-over-year, to a rate of 4.02 million, the worst March since 2009, according to the National Association of Realtors today. From the Marches in prior years (historical data from YCharts):

- 2024: -2.4%

- 2023: -7.6%

- 2022: -29.3%

- 2019: -23.1%

- 2018: -27.0%

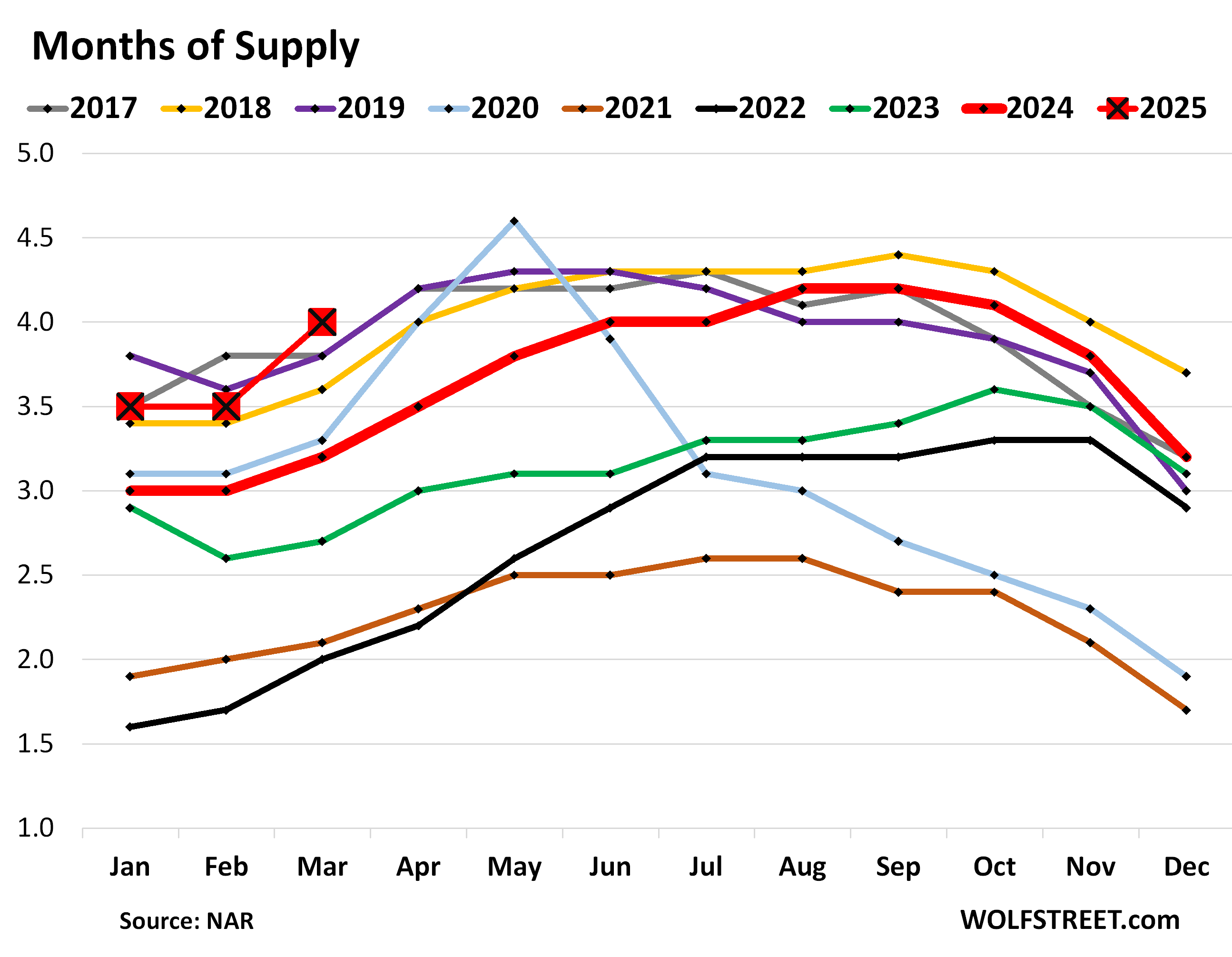

Highest supply for March since 2016.

Inventory of homes listed for sale jumped by 100,000 homes, or by 8.1%, in March from February, and by 20% year-over-year, to 1.33 million listings. This increase in inventory occurred even as buyers were on strike because prices are too high.

Supply of unsold homes on the market, amid these inventory levels and demand destruction, jumped to 4.0 months at the March rate of sales, the highest supply for any March since 2016. The months of 2025 are shown as the red squares:

Demand destruction by region.

The charts below show the seasonally adjusted annual rate of sales (SAAR) in the four Census Regions of the US. A map of the four regions is in the comments below the article.

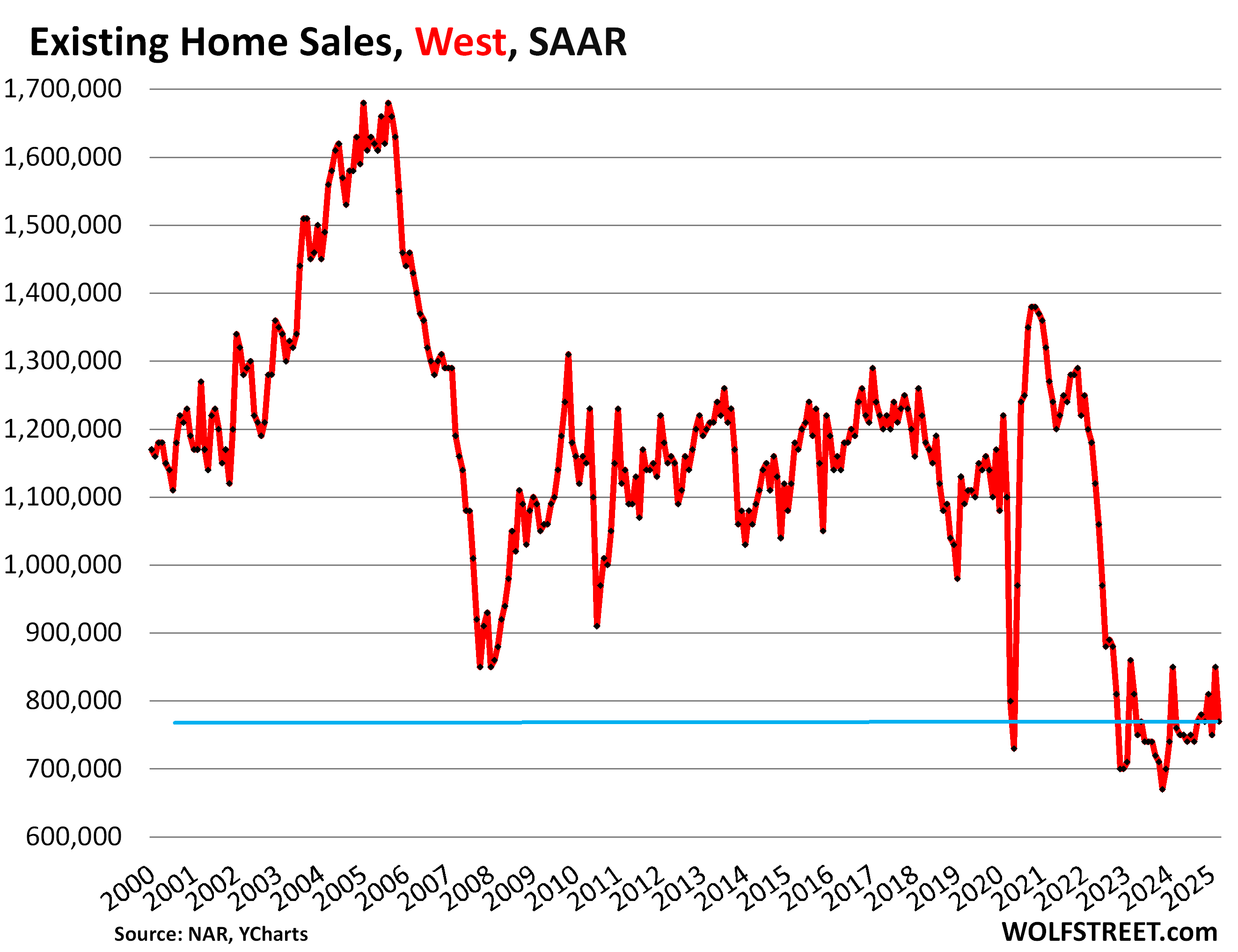

In the West, the seasonally adjusted annual rate of sales fell to 770,000 homes in March from 850,000 in February. But that was still up by 1.3% from the abysmal sales in March last year, and both were the worst Marches in the data going back to the 1990s. Compared to prior years:

| West, compared to March: | |

| 2024 | 1.3% |

| 2023 | -4.9% |

| 2022 | -34.7% |

| 2019 | -29.4% |

| 2018 | -36.9% |

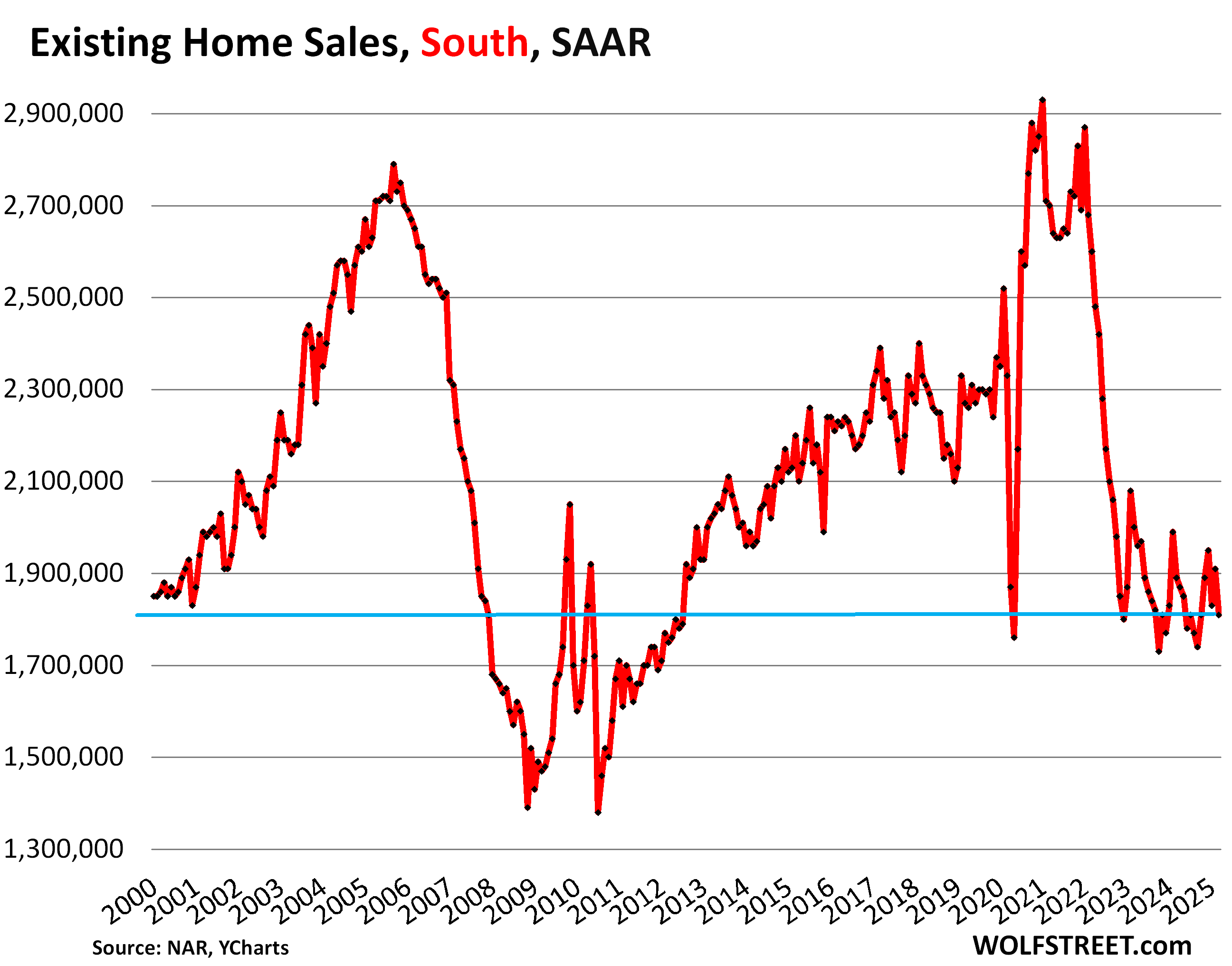

In the South, the seasonally adjusted annual rate of sales fell to 1.81 million in March, from 1.91 million in February, the worst March since 2012. Compared to prior years:

| South, compared to March: | |

| 2024 | -4.2% |

| 2023 | -9.5% |

| 2022 | -30.4% |

| 2019 | -20.3% |

| 2018 | -22.3% |

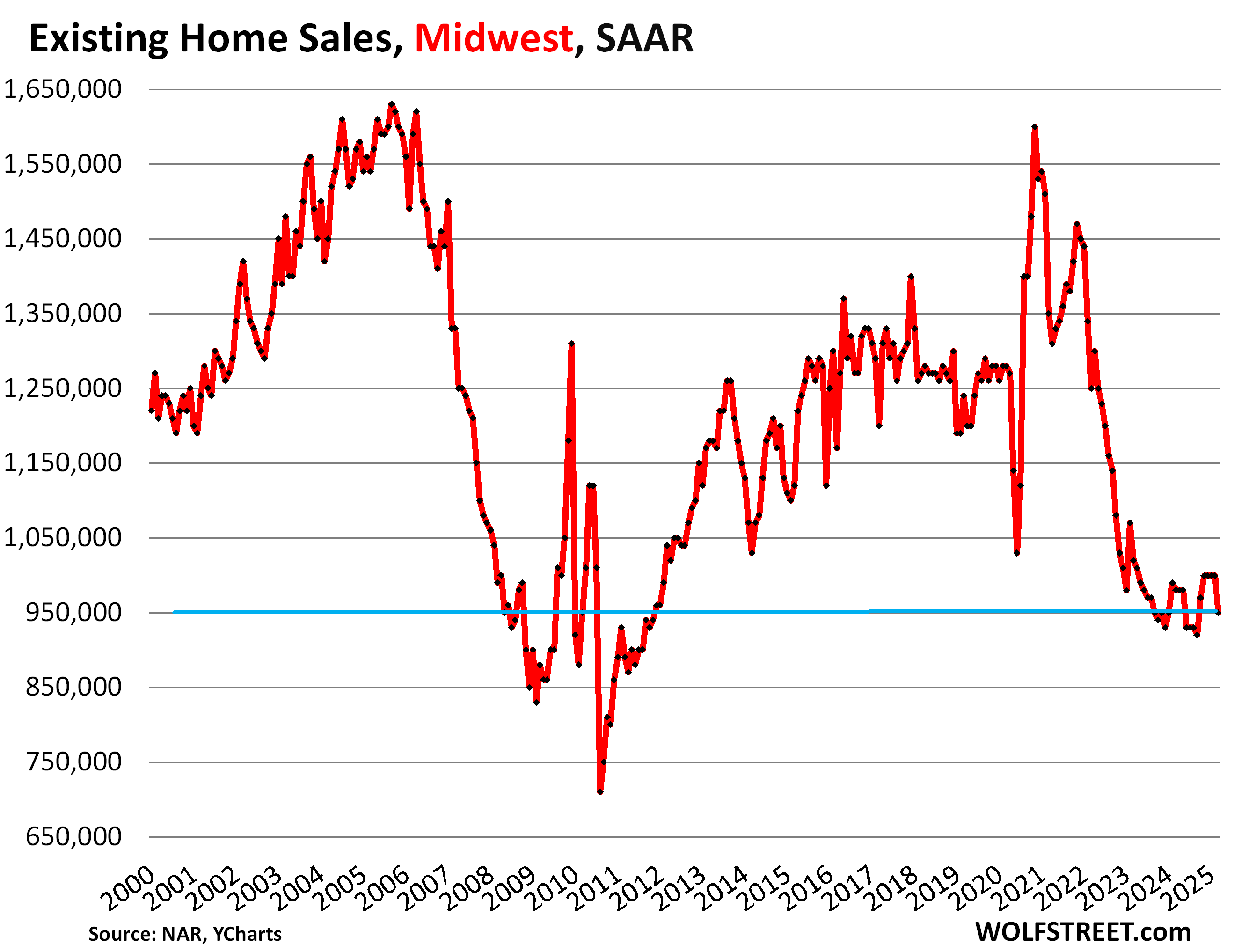

In the Midwest, the seasonally adjusted annual rate of sales fell to 950,000 in March, from 1.0 million homes in February, the worst March since 2011. Compared to prior years:

| Midwest, compared to March: | |

| 2024 | -3.1% |

| 2023 | -6.9% |

| 2022 | -24.0% |

| 2019 | -23.4% |

| 2018 | -25.2% |

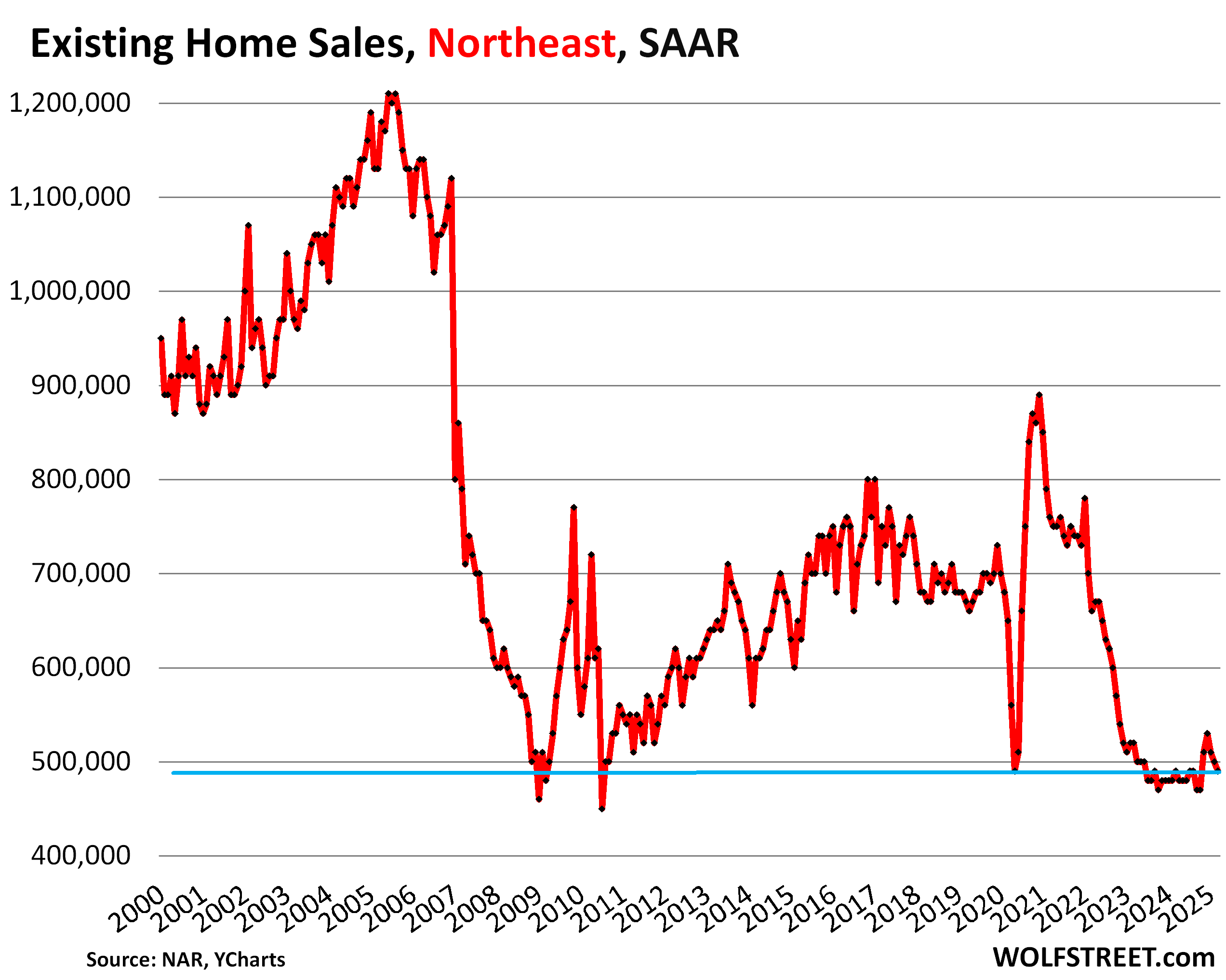

In the Northeast, the seasonally adjusted annual rate of sales fell to 490,000 homes in March, from 500,000 in February, and was the same as the abysmal March 2024 sales rate, and both were the worst Marches since 2009. Compared to prior years:

| Northeast, compared to March: | |

| 2024 | 0.0% |

| 2023 | -5.8% |

| 2022 | -25.8% |

| 2019 | -26.9% |

| 2018 | -27.9% |

But mortgage rates are in the historically normal-ish range.

While home prices that spiked by 50% triggered this massive demand destruction, mortgage rates have returned to the historically normal-ish range that prevailed in the decades before the Fed commenced its interest-rate-repression schemes in 2008, via its 0% interest rate policy (ZIRP) and two massive waves of QE, including the purchases of trillions of dollars of mortgage-backed securities.

Before this interest rate repression began in 2008, mortgage rates were always above 5%, and with the exception of the first three years (2003-2005) of Housing Bubble 1, above 6%, and much of the time above 7% and 8%.

But QT shaved $2.24 trillion off the Fed’s balance sheet so far, and the Fed keeps shedding its MBS holdings, and the spread between the 10-year Treasury yield and 30-year mortgage rates has widened to reflect that, and mortgage rates have remained near 7%, on either side of it.

The entire housing industry obviously loves ridiculously inflated prices and hates historically normal mortgage rates, and so it condemns the historically normal mortgage rates and praises the ridiculously high prices, which the NAR did today again.

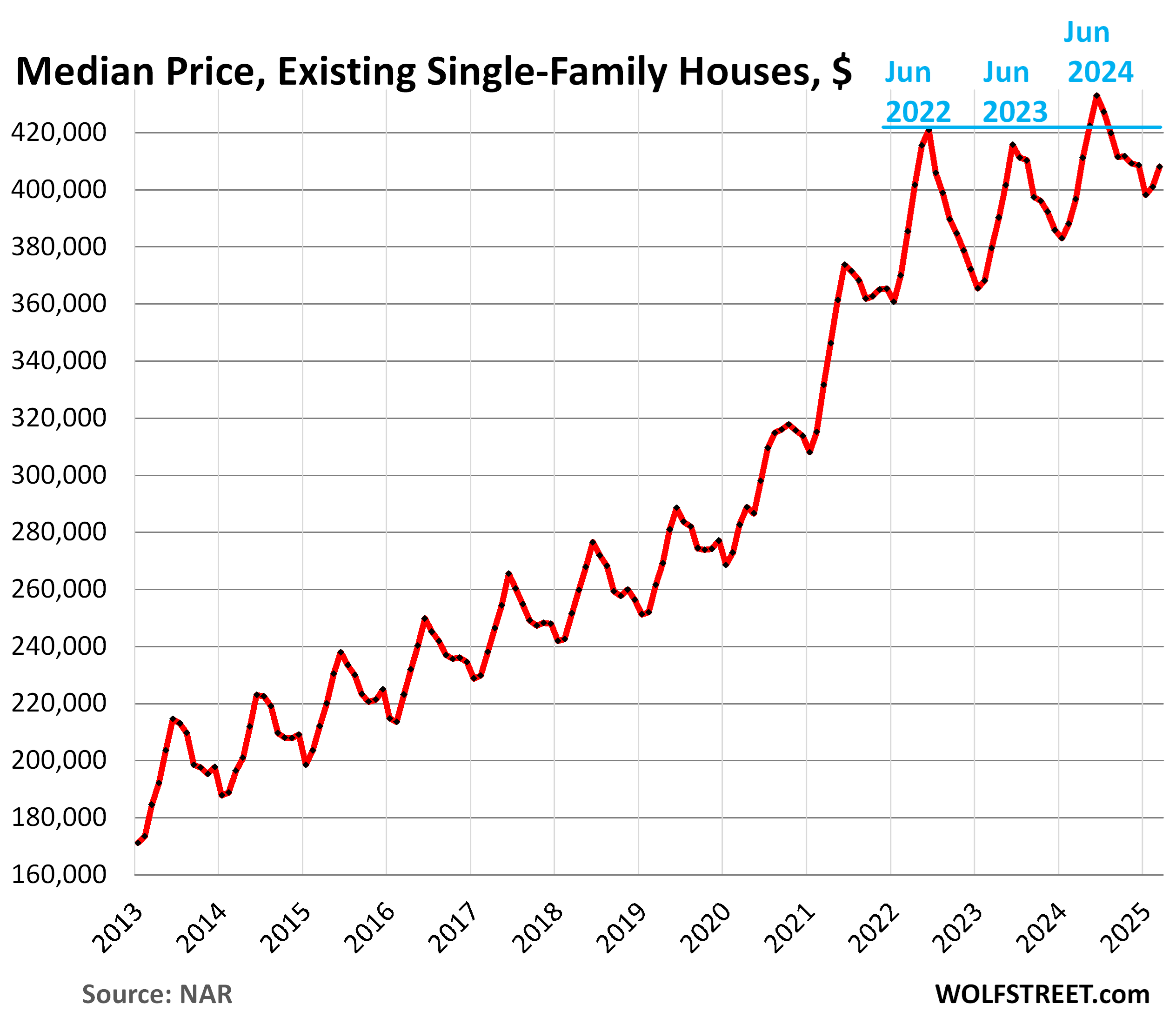

Median price for single-family houses and condos.

The median price is heavily skewed by changes in the mix of homes that sold. In the spring, nationally, more higher-end homes come on the market and sell, which changes the mix of what sold and skews the median price higher. It does the reverse in the fall and winter and skews the median price lower. These seasonal ups and downs in median prices are at least in part due to this shift in the mix.

Single-family houses: The national median price rose to $408,000 in March, from $400,900 in February.

This month-to-month gain of $7,100 was smaller than the gain in March last year, and so the year-over-year gain narrowed further to +2.9%, with year-over-year gains having now narrowed for the third month in a row (from +5.3% in December).

The 50% price explosion over the three years between June 2019 and June 2022, on top of the large price gains in the prior 10 years, was driven by the Fed’s interest-rate repression and money-printing schemes which have created the #1 problem in the housing market today, and it has destroyed demand: Prices are simply way too high, don’t make economic sense, and are not economically sustainable. Textbook demand destruction is the result.

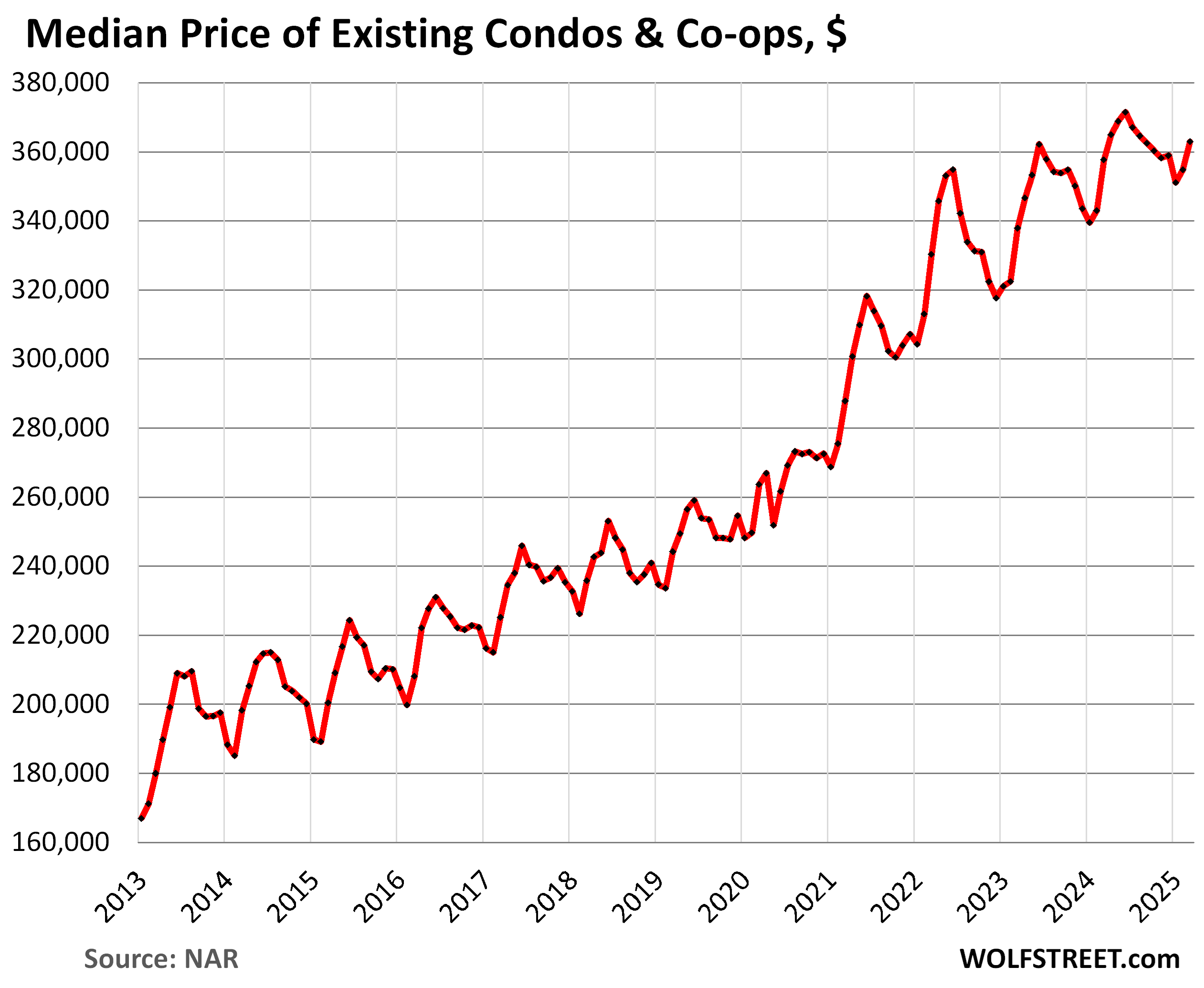

Condos and co-ops. The national median price rose to $363,000 in March, from $354,800 in February.

The month-to-month gain of $8,200 was far smaller (by almost half) than the gain in March last year, which slashed the year-over-year gain to just 1.5%, from 3.4% in February, the third month in a row of narrowing year-over-year gains (from +4.5% in December).

But every market dances to its own drummer. I track home prices (single-family and condos combined) in the largest most expensive 33 markets, in my long-running series, The Most Splendid Housing Bubbles in America, March 2025: The Price Drops & Gains in 33 of the Largest Housing Markets. In quite a few of them, prices have dropped substantially from their peaks in mid-2022.

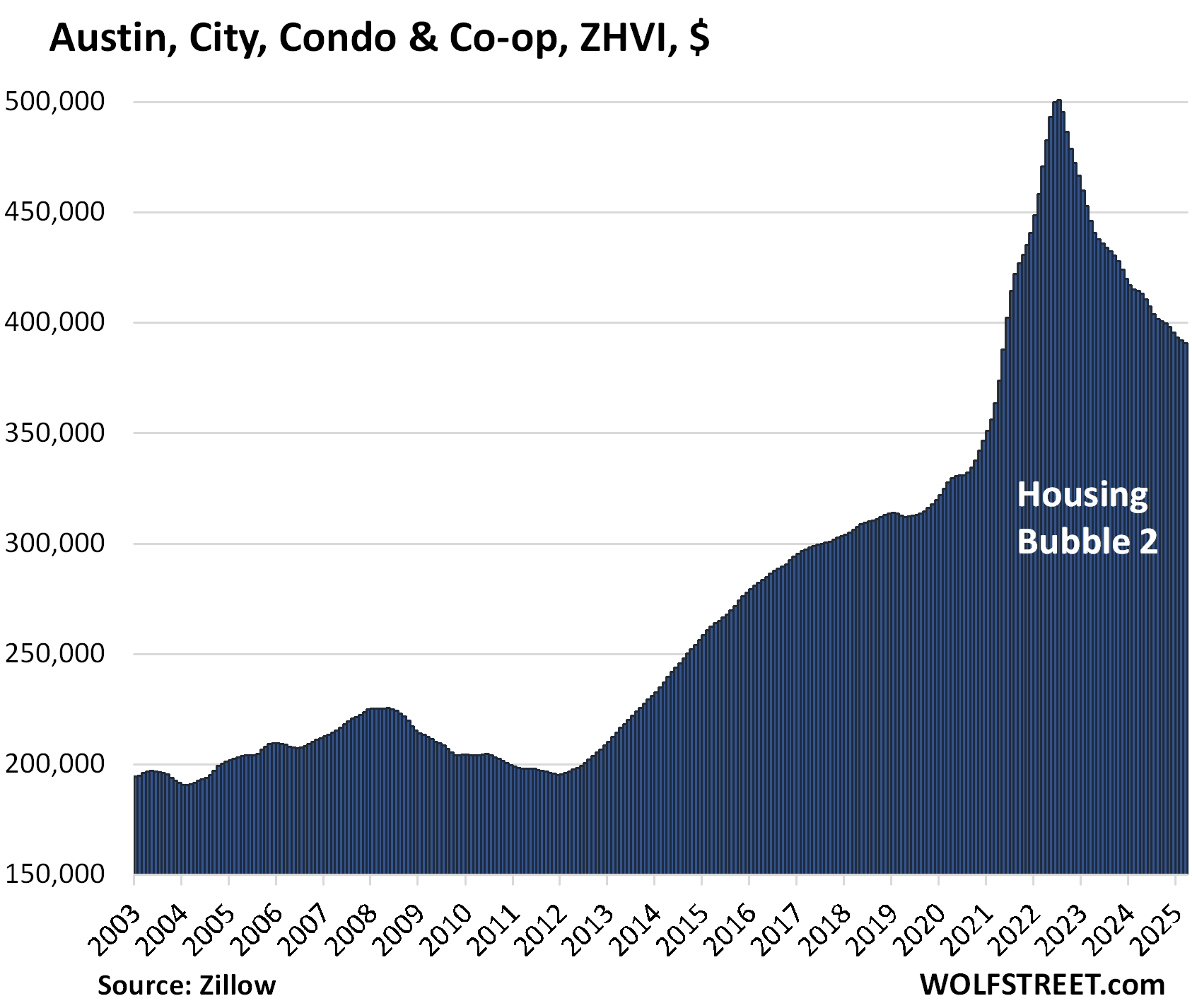

But condos are on the forefront, on the way up, and on the way down, and price drops in many cities have been substantial: In 15 Bigger Cities, Condo Prices Already -10% to -22%, 5 Are in Florida with Accelerating Drops. Absurdity Comes Unglued. Here are four of the 15:

Condo prices in Austin, TX: -22% from peak in July 2022:

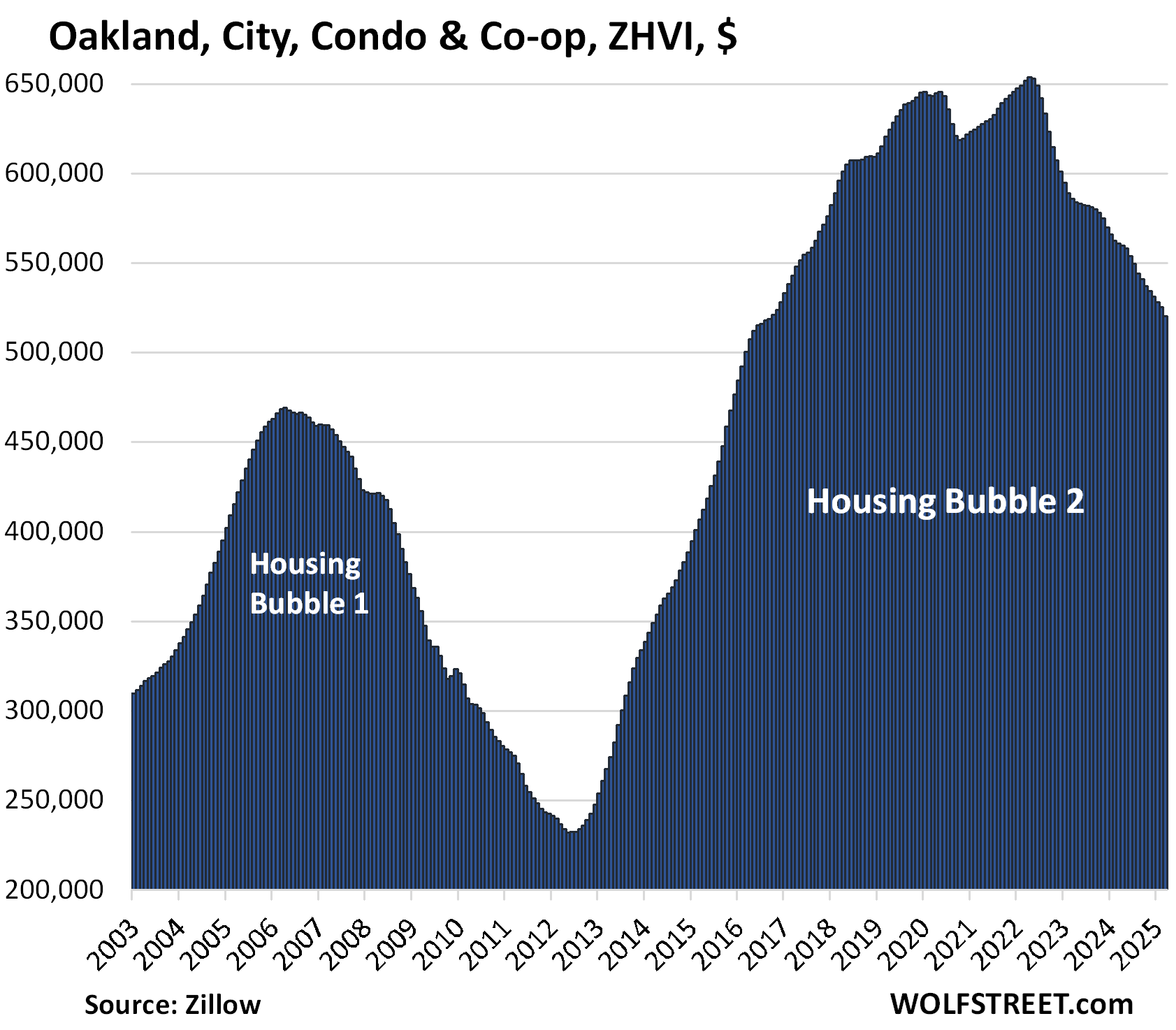

Condo prices in Oakland, CA: -20% from peak in May 2022:

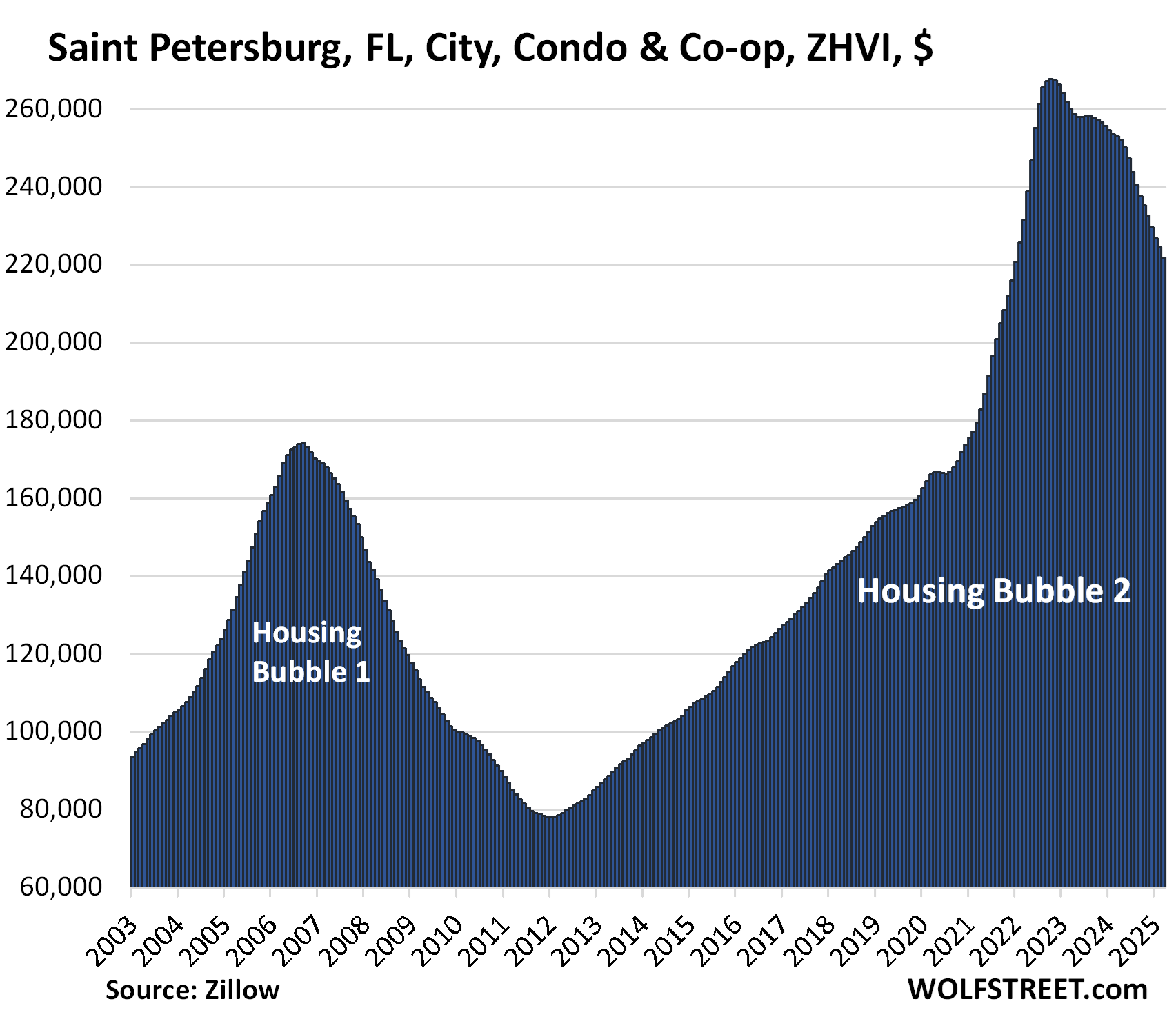

Condo prices in St. Petersburg, FL: -17% from peak in Oct 2022:

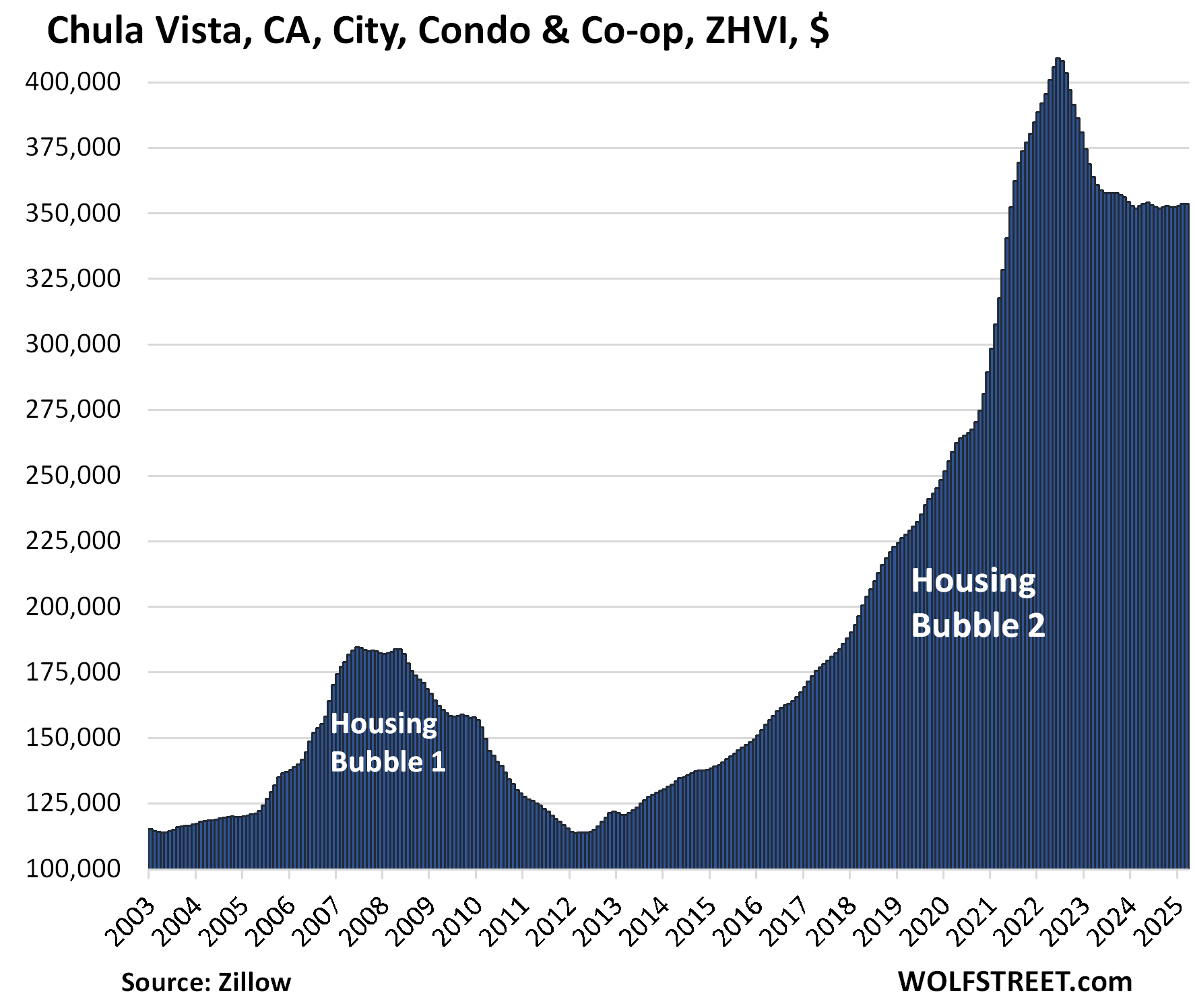

Condo prices in Chula Vista, San Diego County, CA: -14% from peak in June 2022:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

Great to see West is trending down…just need the west of west special bubble SoCal to follow the same pattern as general west to trend down and continue to trend down for a while because the way things are existing sellers still out to lunch with price and completely miss the memo…many still think if they hold on just a little longer, they will either rescue by rate decrease, any round of FOMO ramp up or some other BS reasons they gaslight themselves into believing..

Really sick of seeing any crapshack setting floor of $1M as some magical minimum asking price regardless of the area, house condition, size..

If you look at the inventory number or for sale in Irvine, LA, San Diego, etc it’s crazy. It’s almost like every other house is for sale. It reminds me of late 2007

With those overly inflated prices out there (I’m in Texas), it’s no wonder people are trying to cash out. I said trying….

i posted in the other thread, the paradox that if everyone tries to “cash out,” then the inventory is no longer “low” and they won’t be able to cash out.

Phoenix_Ikki,

With the LA Olympics a few years out and likely billions needing to be spent to get ready should be interesting. One has to assume lots of homeless shelters will be built or remarket homes people as “living with nature”. Unlikely any of the housing market mess will sort itself out by then as even if rate cuts there is no guarantee mortgage rates will move in same direction.

Is there a way to correlate time from downturn in sales to price correction and overlay with current conditions? I vaguely remember that some markets pulled back quickly so there were abundant deals in 2008/2009 but in others sellers held out hope and prices bottomed in 2011-12

As I said in the other thread, nothing is going to stop the tidal wave of supply coming, with or without foreclosures. 1 year from now, supply is going to be ALOT higher nationally than right now. ALOT higher.

A paltry 20% decrease in price is not going to fix this issue. Not with the cost of home ownership skyrocketing like maintaining or repairs needed, home owners insurance skyrocketing, and mortgage rates likely headed higher if not much higher from here.

There is serious pain coming to the price of homes. And people will be forced to sell at much, much lower prices in time. Divorce, death, job relocation, or simple cost to maintain, people will be forced to sell.

Yep, the youtuber Orlando Miner does a lot of videos on airbnbs failing along with hoa fees and housing payments in general skyrocketing. Everyone nowadays has to emote on tiktok about it apparently which is odd to me but nevertheless is quite revealing.

And there has to be a lot of leverage out there that is going to get absolutely destroyed, like private equity and pensions.

Every moron thinks their 50+ year old shack is worth a million and is probably driving a 70K truck because of that.

hopefully the private equity funds and pensions get bailed out by congress and the fed. there’s no reason they should have to take any losses.

to paraphrase leona helmsley, losses are for the little guy.

Really depends on when you bought. If you owned during the period to refinance to a sub 3% mortgage, you face much lower selling pressure than in normal times because your cost on that home is as free as financed housing ever gets.

So in the past we would see a lot of people sell, but instead some of those people will maintain ownership and rent the place out.

Rents can remain inflated because they are tied to perceptions of home values, and demand for rentals can stay elevated because house prices stay high.

The root of the problem is of course millions of people having 3% mortgages that will never increase.

rents are not tied to perceptions of home values. they’re tied to what people in the area can afford to pay. period.

The canary in the coal mine(in my opinion) is replacement cost.

Labor and materials are still crazy high. We looked at downsizing(building a second home on our property) and letting out kids have our house. Financially ridiculous…unless we move to a dying town in flyover country.

You do live on an island after all…

Yeah but Wolf, in defense of the entire housing industry I also sort of like ridiculously inflated prices and hate historically normal mortgage rates.

lol jk

Superb analysis thanks.

Free money is the best money, LOL. We all love it. After us the deluge?

Wait a minute this ain’t me

One of you Erics please add some alphanumeric symbols to your screen name, such as Eric01, Eric IV, or whatever.

Maybe it is just the time scale of the charts but it doesn’t seem like there has been any significant stretch where home sales stay within some average range, they either seem to be going up, up, up or down, down, down. It’s hard to say what would be an average year would be for home sales.

Tiny bubbles (tiny bubbles)

In the wine (in the wine)

Make me happy (make me happy)

Make me feel fine (make me feel fine)

Tiny bubbles (tiny bubbles)

Make me warm all over

With a feeling that I’m gonna

Love you till the end of time

Imagine what a normal EKG looks like. Now imagine what it looks like when the heart stops completely – FLAT LINE. Soon the housing market

‘EKG’ will look like that – a flat line – distress, anguish, despair, demise. You get the idea. 💡

We better start making funeral arrangements.

Wolf, I appreciate your research and read every email as I have for sometime. Regarding the housing market, we run PE investment banking fund and deal quite regularly in the luxury housing market. So far, the Florida coastal market is holding up quite well. Above $3.MM up to 22.MM has been resilient. Strong spec building in this market range.

We simply redefine all house building related companies as tax free, give them zero interest loans, and tell them to pass that along to consumers. New houses will be so cheap it will force existing house prices down.

There is a conceptual flaw in your thinking: For builders, as for any business: they’re always charging the maximum price that they can get and still achieve their unit sales goals. Their costs do NOT change the selling price, but only change their profit margins. By bringing down their costs, you would just increase their profit margins, which is exactly what happened during the interest rate repression era when we had 0% policy rates, and below 3% borrowing rates and free money everywhere.

Why not phase out the $500k home gain exclusion over ten years. That would activate supply and raise government revenue to boot. It would be a high class problem no one could legitimately complain about.

Another tax break for homeowners? You pay capital gains taxes on your stocks when you sell them, and you should pay capital gains taxes on ALL your assets when you sell them. RE is the most tax-coddled sector ever. I need to give Trump a call and let him know to write up and sign an executive order to that effect. You can sue him, if you don’t like it, LOL

Tell him I said hi. And, by the way, kill carried interest. And 1031….

Bobber,

Wouldn’t phasing out the 500K deduction cause a panic with homeowners trying to sell and cash in? The supply would increase drastically.

I don’t think lack of supply is the issue. Price is the issue as Wolf has pointed out.

Creating a huge supply shock might be enough to expedite a huge price crash like 2008.

I’d prefer the supply problem take care of itself gradually without any government caused black swan shock.

It is still a seller’s market here in the Midwest. I am having a tough time buying a house. Here is the synopsis of the past two weeks for me:

Made an offer 3% under asking due to their 15 year old roof. Outbid, 3 total offers

Tried to set up showings for 3 houses for a Friday on Thursday afternoon. They all three were on the market about 24 hours and were all under contract on Thursday afternoon, so I wasn’t even fast enough to see them.

Made another offer 1% under asking due to rot on siding and windows: Outbid, 3 total offers

Made another offer at list on a good house: Outbid with 2 total offers

Made another offer today, 4% over list. We’ll see if that one goes through.

If you’re looking to buy a house now, and are overbidding, don’t complain about the market because by trying to buy and by overbidding, you become part of the problem you’re complaining about. Buy it, pay whatever it takes, understand that you helped drive up prices, and understand that a house is an expense, and make sure you can make the mortgage payments for the next two decades, and that you don’t have to move for those two decades, and you’ll be fine no matter what happens to the housing market. Enjoy your life in your house, but don’t count on your house to make you rich. And if you lose money on your house, fine; and if you make money on your house, finer. But don’t complain about the market as you yourself are contributing to the problems.

“Made an offer 3% under asking due to their 15 year old roof. Outbid, 3 total offers”

“Made another offer 1% under asking due to rot on siding and windows: Outbid, 3 total offers”

Holy cow…try buyer protest for once, especially considering what you’re getting for the money…I promise you, renting is not the end of the world and yes you can rent a house and do something else with your down payment in the meantime. The delta you save compare to comparable mortgage payment you can also use to invest, T-bill and get some return.

Like Wolf said, if you’re still buying now then you’re part of the problem and probably shouldn’t be complaining and suck it up and overbid just like all the suckers that overbid and paid wayyy over sticker when C8 Z06 was going bonker, sure none of those people regret it now…

“I promise you, renting is not the end of the world”

Your posts suggest you feel like it has been, for you. :-)

I sat it out a long time (age 30) before underbuying, then sat for another 10+ waiting to upgrade, bitching the whole time about the idiots overpaying and ruining the market. When our perfect dream home came up right at the bottom of the 2011 market, we were too embroiled in another project to confidently swing it. We’ve wasted a lot of the last 30 years obsessed about this. Don’t be me.

What did you do from 2011 to 2019? Prices were steady and money was cheap?

I’m convinced the go-bar-mint and the banks must have a covert/invisible ‘Let’s Keep Housing Prices High Department’. Its mission…well, its mission is in its name. 🥸

So far so good in the Swamp. The price of existing homes and even condos are holding up well in DC. The end of WFH has al lot to do with it. People need to be close to their jobs.