Inflation is festering and accelerating in services (two-thirds of overall PPI), not in goods.

By Wolf Richter for WOLF STREET.

As has been the case for many months, today’s Producer Price Index for January included big up-revisions of the prior month, driven by a whopper up-revision for services which account for two-thirds of the overall PPI. On top of these upwardly revised December figures, the PPI rose further in January.

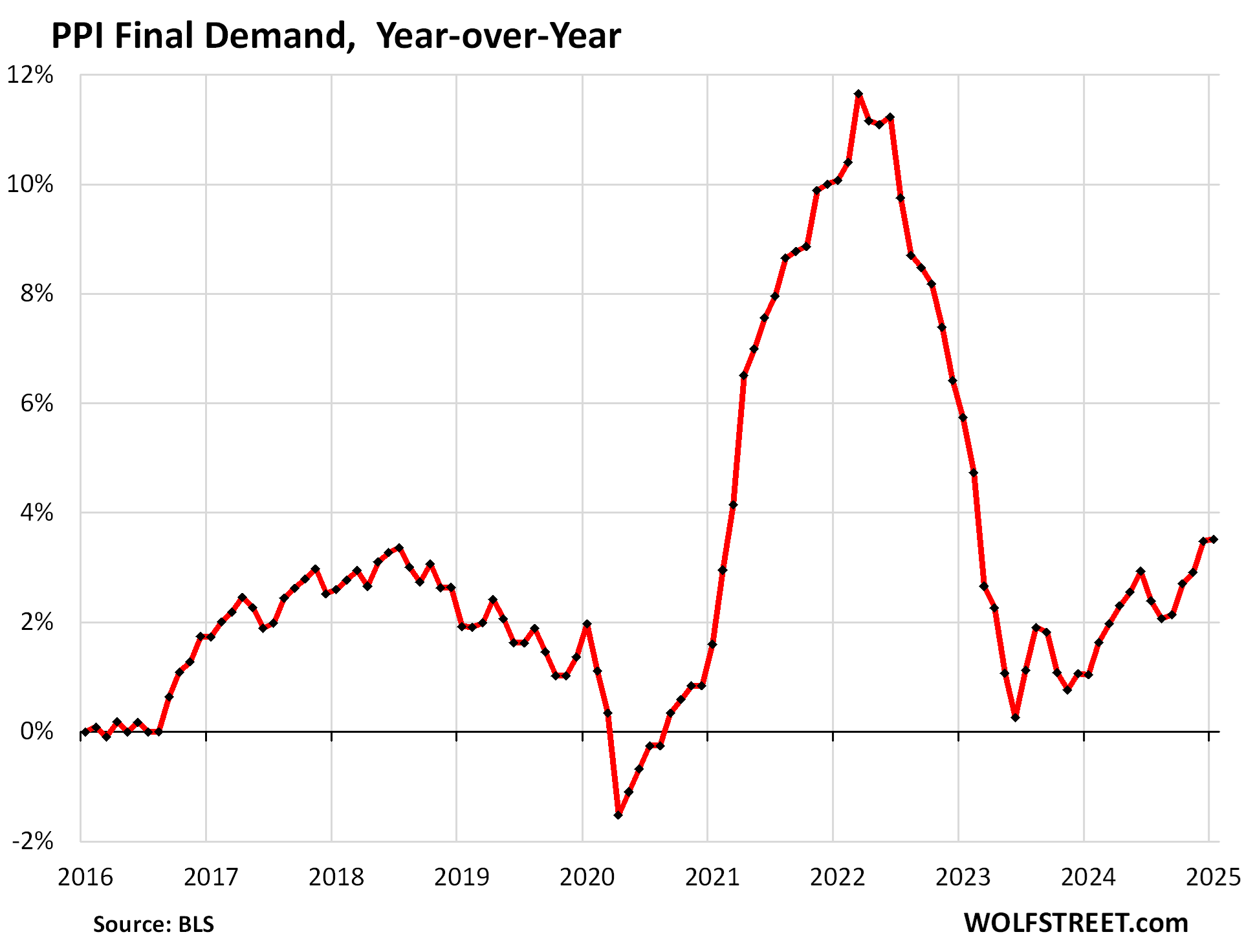

In January, the overall PPI accelerated to an increase of 3.51% year-over-year, the worst increase since February 2023, following a persistent zigzag line higher from the low point of near 0% in June 2023, driven largely by the services PPI.

And December was revised up to an increase of 3.48%, from 3.31% as reported a month ago. This up-revision was powered by a massive up-revision in services.

The PPI tracks inflation in goods and services that companies buy and whose higher costs they ultimately try to pass on to their customers.

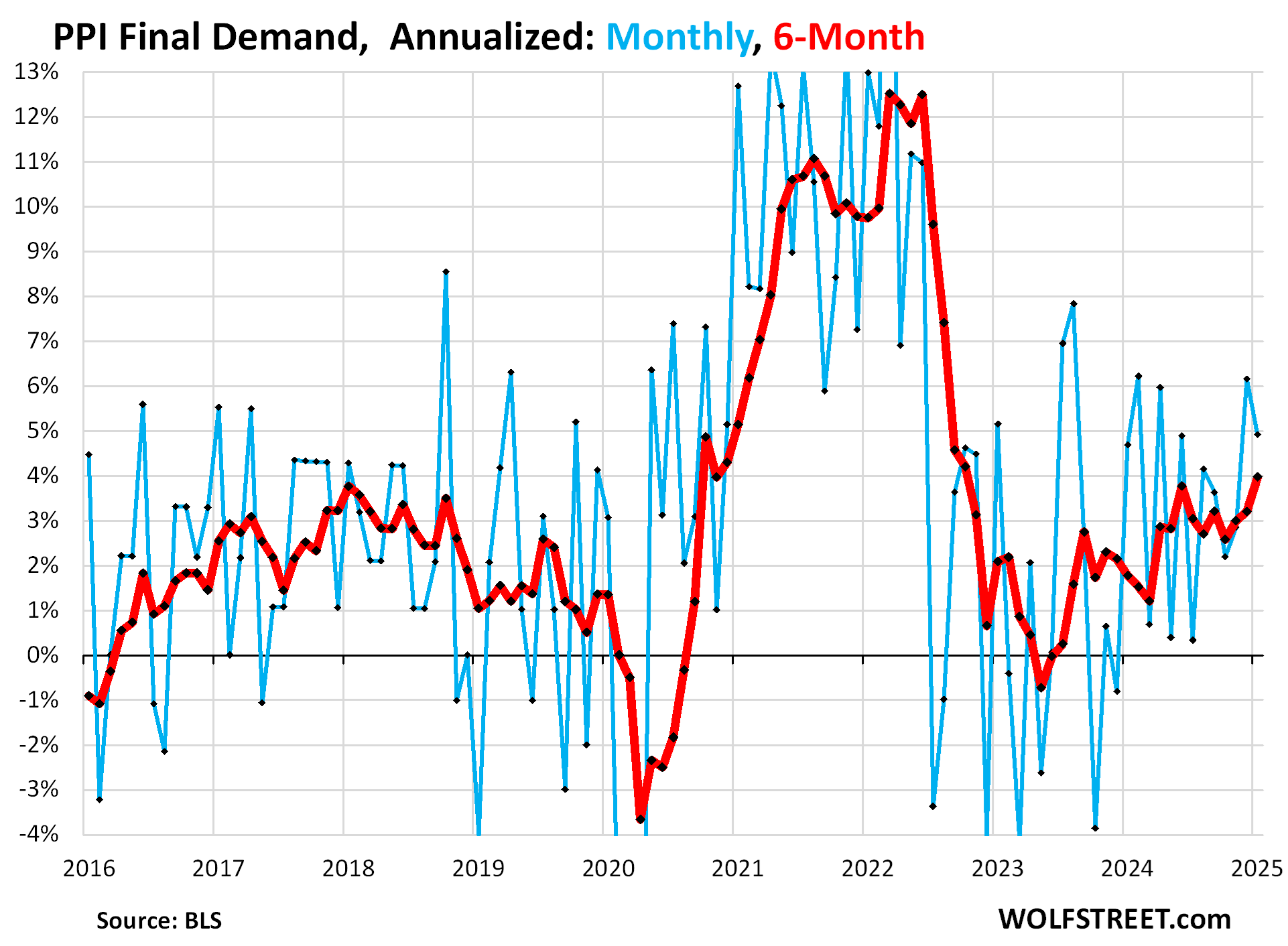

On a month-to-month basis, the PPI for final demand jumped by 0.40% (4.9% annualized) in January from December, seasonally adjusted.

And December’s increase was revised up to +0.50% (+6.2% annualized) from the previously reported +0.22% (+2.7% annualized). The up-revision more than doubled the increase! This was driven by the whopper up-revision of the Services PPI.

The up-revision for December plus January’s increase caused the 6-month PPI to surge to +4.0% annualized, the worst increase since October 2022 (red).

The plunge in energy prices from mid-2022 through September 2024 had cooled the overall PPI increases into the pre-pandemic range, and papered over the inflationary forces in services. But since October, energy prices stopped dropping and flipped to increases. In January, energy prices jumped by 1.7% from December, which wiped out the remainder of the year-over-year drop, and the index was unchanged year-over-year.

Food prices jumped by 1.1% in January from December and by 5.5% year-over-year. The avian flu’s impact on egg production had some impact here.

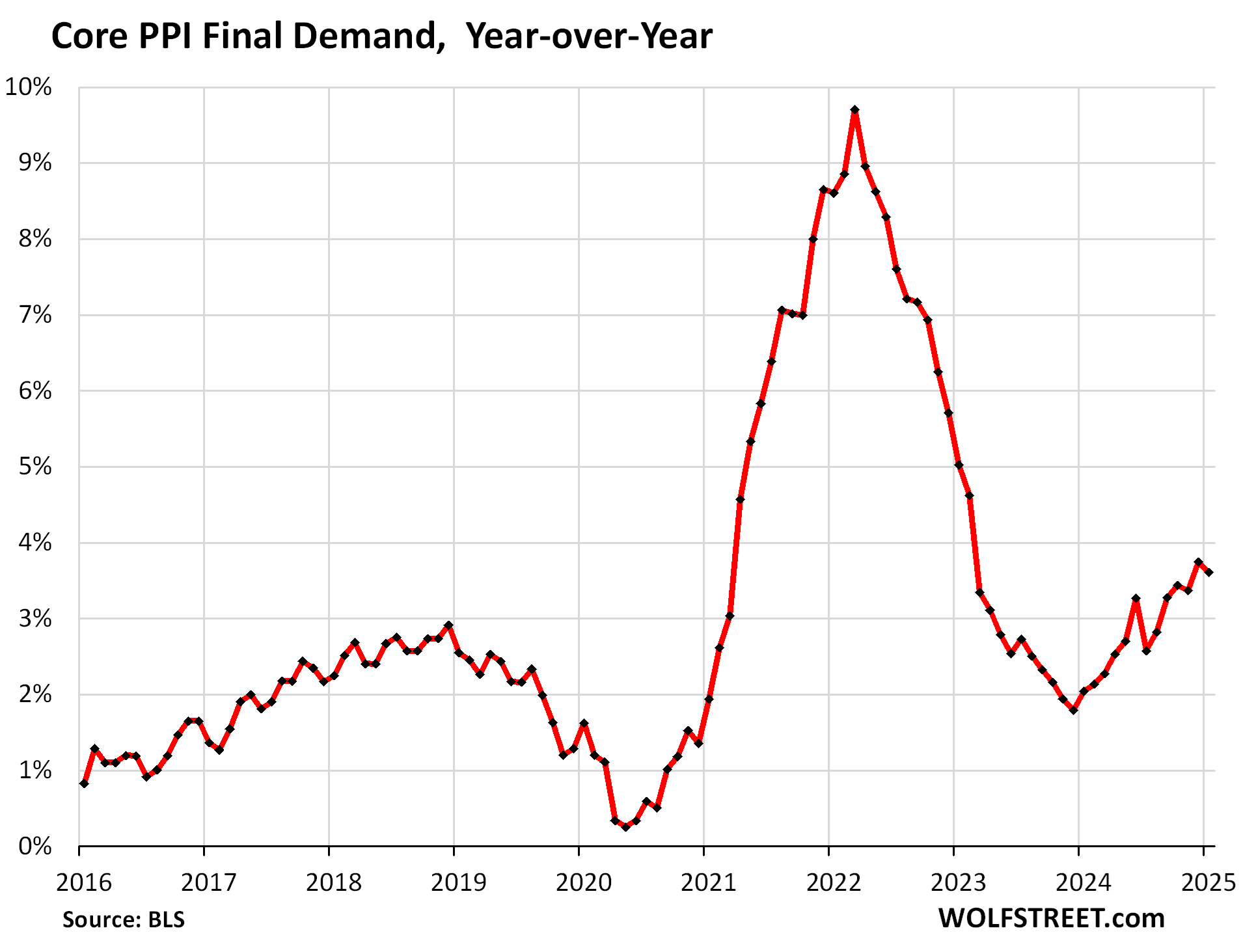

Without food, energy, and eggs: “Core” PPI, which excludes food and energy, was revised up massively for December.

The month-to-month increase for December had originally been reported as +0.04% (0.5% annualized). Today it was revised up by 36 basis points to an increase of +0.40% (4.9% annualized). All seasonally adjusted.

On top of the up-revised December rates came January’s increase of 0.28% (3.4% annualized), which accelerated the 6-month PPI to 3.8% annualized, the worst since September.

Year-over-year, core PPI for December was revised up by 20 basis points, from the previously reported +3.55% to today’s December figure of +3.75%.

Year-over-year data are not seasonally adjusted since they cover 12 months and wash out any seasonal effects. Not seasonally adjusted, the January core PPI jumped by 0.49% (not annualized). But the January 2023 increase of +0.63% fell out of the 12-month window. So year-over-year in January 2025, the index rose by 3.61%, a notch slower than the upwardly revised increase of 3.75% in December (originally reported at 3.55%).

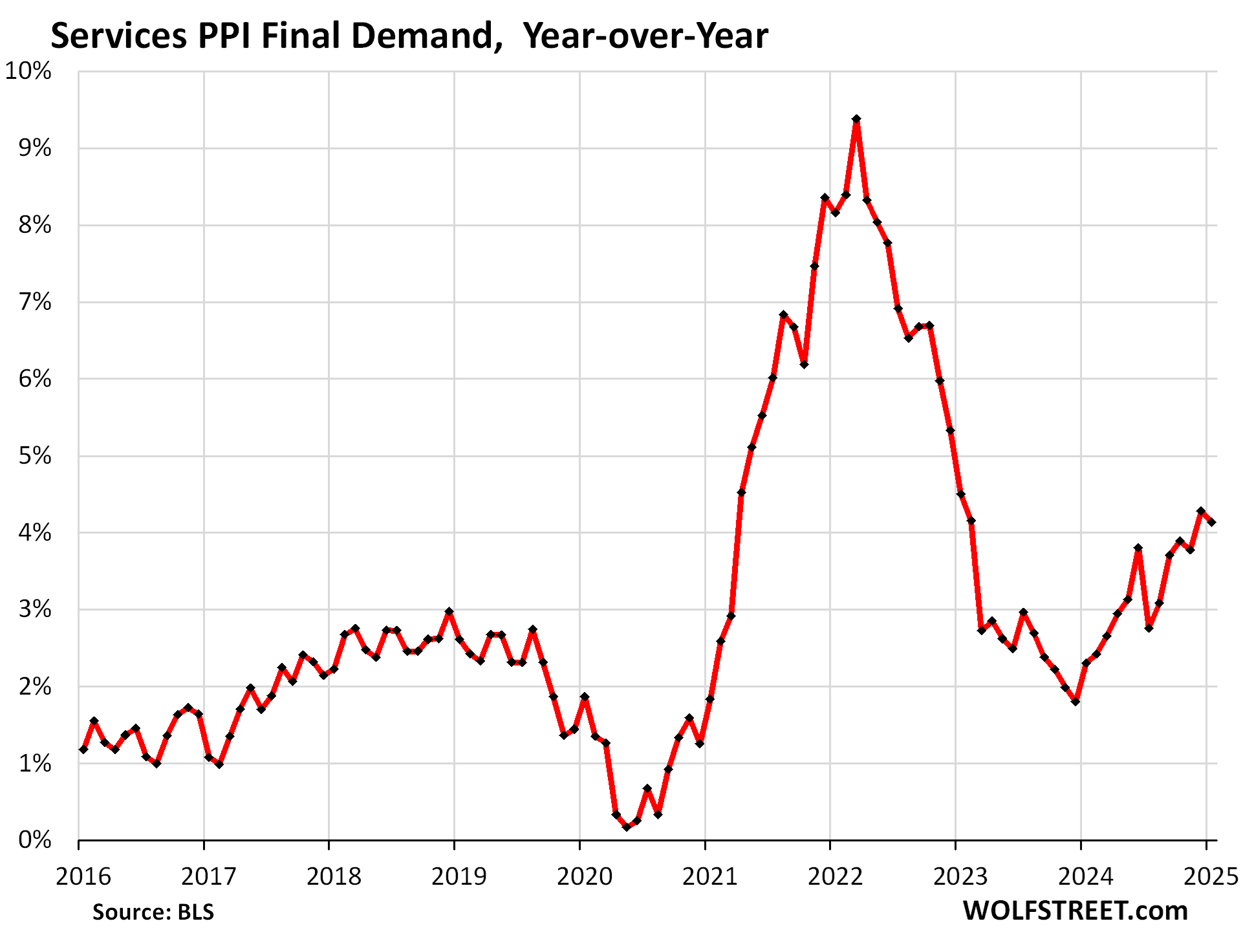

The services PPI, which accounts for two-thirds of the overall PPI but excludes energy services, had the whopper 47-basis-point up-revision for December, from the originally reported month-to-month increase of 0.04% (not annualized), so from nearly no change, to +0.51% as revised today.

On top of this upwardly revised 0.51% surge in December (+6.2% annualized), the services PPI rose another 0.32% in January (3.9% annualized).

This pushed the six-month services PPI to +4.5% annualized, the worst since September.

The year-over-year December increase was revised up by 25 basis points, to +4.28%, from the previously reported +4.03%.

With the January 2023 reading of +0.71% (not seasonally adjusted) dropping out of the 12-month window, and the January 2025 reading of +0.54% (not seasonally adjusted) moving into the 12-month window, the year-over-year increase in January cooled a hair to +4.14% from December’s up-revised 4.28% (originally reported as 4.03%).

These up-revisions have the effect that the entire zigzag line keeps shifting higher:

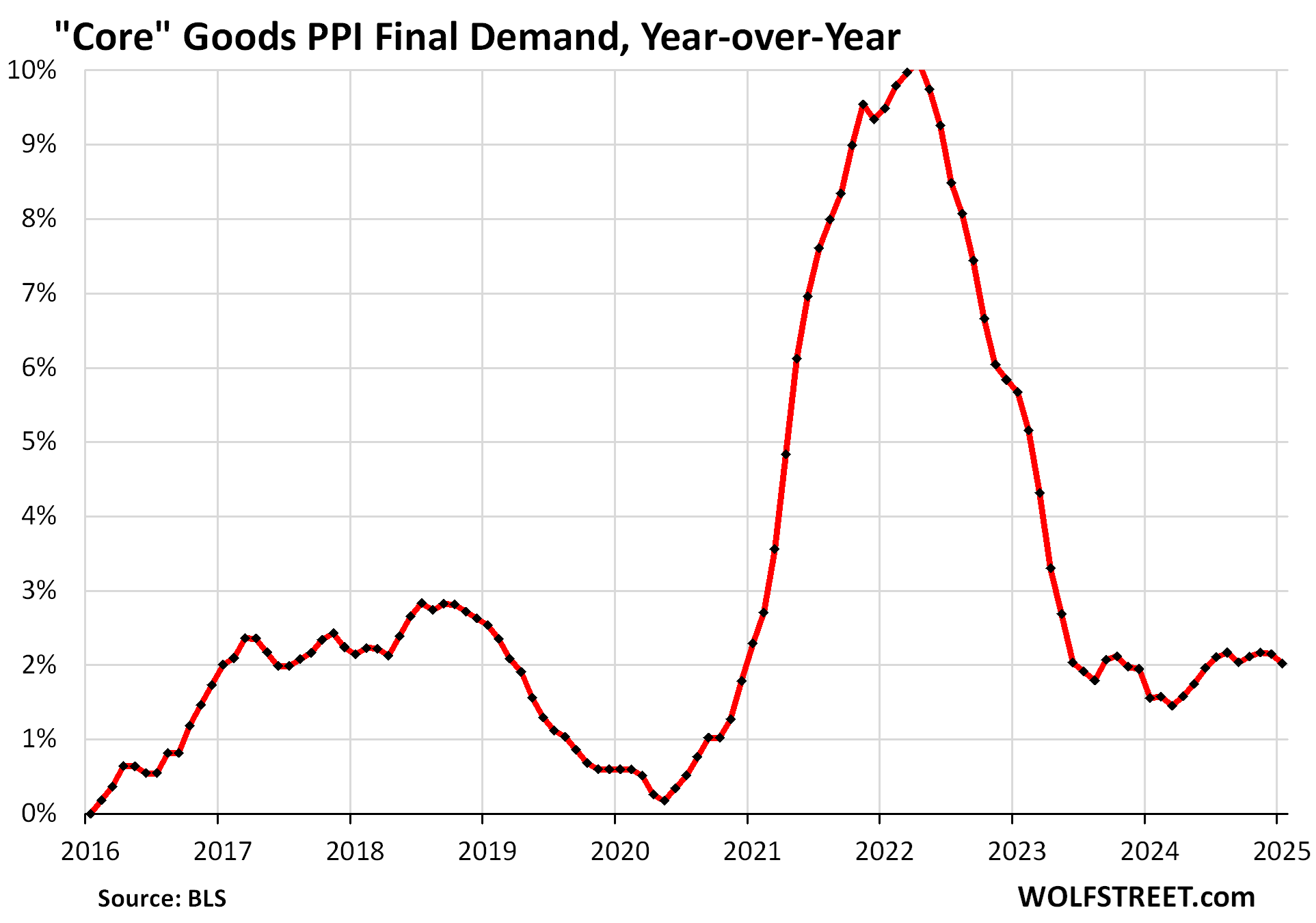

The “core goods” PPI was only minimally revised up. In January, it rose by 0.13% (+.5% annualized) from December.

Year-over-year, it rose by 2.0%, in the same 2%-plus range of increases for the seventh month in a row. The goods sector is not where inflation is a big issue at the moment. The issue with inflation is in services.

The PPI for “core goods” covers goods that companies buy but excludes food and energy products.

With these underlying trends, as shown by the PPI, it’s no surprise that consumer price inflation, as tracked by CPI, continues to accelerate, and that there too, inflation is festering in services, and in January it was non-housing services where inflation accelerated sharply.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And yet, “rally on Garth”.

Interesting all the attention on eggs, shortages, etc. But no movement on actual chicken prices (at least none I’ve noticed).

Yes… Beef and pork prices have risen sharply, poultry prices are unchanged month-to-month and year-over-year – per CPI, see my article yesterday:

https://wolfstreet.com/2025/02/12/beneath-the-skin-of-cpi-inflation-worst-month-to-month-acceleration-of-cpi-since-aug-2023-on-spikes-in-used-vehicles-non-housing-services-food-energy/#comment-626136

The USDA says chickens with bird flu are perfectly safe to eat, though you probably won’t see them in your grocery store meat case. I imagine they’re flooding the processed food stream.

It would seem prudent to apply the precautionary principle in this situation.

Yeah, that’s not accurate at all.

👎

per USDA:

Q. Can I get avian influenza from eating poultry or eggs?

A. No. Poultry and eggs that are properly prepared and cooked are safe to eat. Proper food

safety practices are important every day. In addition to proper processing, proper handling and

cooking of poultry provides protection from viruses and bacteria, including avian influenza. As

we remind consumers each and everyday, there are four basic food safety steps to follow:

CLEAN, SEPARATE, COOK, and CHILL.

https://www.usda.gov/sites/default/files/documents/avian-influenza-food-safety-qa.pdf

It’s your use of “With” that is in question.

If they detect it in birds, they are destroyed. Not used secretly

That’s why eggs are so expensive, they come from clean flocks of chickens.

The Brits said the same thing about beef infected with mad cows disease in the 1980s.

Brad,

BSE wasn’t caused by a virus that you can destroy with high temperature (cooking), but by a “prion,” a misfolded protein.

From the omniscient Wikipedia:

Prions are a type of intrinsically disordered protein that continuously changes conformation unless bound to a specific partner, such as another protein. Once a prion binds to another in the same conformation, it stabilizes and can form a fibril, leading to abnormal protein aggregates called amyloids. These amyloids accumulate in infected tissue, causing damage and cell death.[13] The structural stability of prions makes them resistant to denaturation by chemical or physical agents, complicating disposal and containment, and raising concerns about iatrogenic spread through medical instruments.

Who’s secretary of the USDA these days? Kid Rock or Hulk Hogan?

The number of beef cattle in the US is at low levels not seen since 1950’s. Finally the cattle producers, ranchers, are seeing good prices due to competition at auctions (and contracted cattle). And those still in ranching are currently not keeping replacement heifers exacerbating the cattle number growth.

Great post, thanks. Small cow town sentiment from where I’m from. The bedrock of our society, the every day people.

Maybe everyone is becoming a chicken farmer, increasing supply, to reap the rewards of the golden eggs!

Not an advertisement for Safeway, but legs and thighs are 69 cents per pound this week with a digital coupon. I haven’t seen prices that low in about a decade.

Pork shoulder blades were $1.79/lb last week. BBQ smoked pulled pork was what was for dinner.

Maybe that’s a good sign?

Yet the markets react favorably.

Let’s hope it hits new All Time High so the Fed can cut rates again at absolute peak instanity. And they will.

Facts are only weakly correlated with vibes.

It will take a lot more bad news to get it the way of a tech bubble. The Tesla shorts got the stuffing kicked out of them for betting against a company with a bigger market cap than the auto industry. Meta is still called Meta. And so on.

Yet the USA tech exceptionalism trade grinds on, even though the cheerleaders are looking a bit long in the tooth.

Call me a skeptic but I don’t see the layoffs being AI related. Instead, it may be more like the beginning of something else.

The continued SP 500 overvaluation, driven by the Nifty Fifty (er, Magnificent 7) is a puzzle.

My off-hand guess is that auto-401k contributions (a good thing) during peak Boomer retirement prep, married with SP 500 allocations (agnostic diversification a good thing, cap weighting a bad thing) is what is driving the 8 year craziness.

The Boomers learned to respect saving (good), diversification (good), tax efficiency (good)…but have been pretty slow to learn about the pathologies of index construction.

How the SP 500 is actually put together matters – and its cap weighting has led to allocation distortions that work against its diversification mandate. I know there are some cap weighting caps…but only at fairly high levels.

In other words, if the Nifty Fifty can turn to tears (taken out and shot one by one) the “Magnificent 7” definitely can…fewer to shoot.

(Particularly if they persist in their religious zeal for spending *hundreds of billions* for AI data centers…mere weeks after being beat over the head by the amazingly obvious insight that clever software makes massive hardware investment very obsolete, very quickly (a lesson learned many, many times in IT history).

The slavish devotion to AI burn rates in the face of these well-known facts makes me wonder what the Mag 7 are really doing/thinking about.

“clever software makes massive hardware investment very obsolete,”

The revelation from the 90s movie “hackers” and every other apocalyptic tech/AI story.

We all have a mass of hardware. “Old/ obsolete” laptops and smartphones can be used to rival the big boys… but only in Unity.

The strategy is always divide and conquer. Confusion is a form of division.

Also, I see in many headlines and in the comments here, people are eager for self extermination. The “wonders” of A”I” are a holy grail: filled with poison.

The way to drive the last nail is to convince the divided, confused masses that they are obsolete.

We used to believe that our creativity couldn’t be replaced, now we’re met with a charge to “expedite” for profit and efficiency. It’s in realms of cut n’ paste music and art.

High speed plagiarism has only begun.

There are multiple asset bubbles. Stocks are being priced at the greater fools hypothesis as opposed to a discounted cash flow analysis.

Well we do live in the stupid and ridiculous version of the many multiverse theory so this is par for course.

Next move, lower short term and hope long term rate will magically come down too. Better yet since we are re-writing or pulling rabbits out of the hat when it comes to rules, maybe we can have an executive order to have Fed set the 10yr yield moving forward or EO to not measure PPI.. That’ll show inflation who’s the boss

Phoenix Ikki, You live in a dream world if you think lowering short term rates will lower long term rates. As much discussed in Wolf Street, the Fed lowered short term rates 100 bp, and long term rates then went up 100 bp. Long term bonds worry about inflation and apparently have little confidence in the Fed being able to deal with inflation. Recent data suggest the long term bond guys are right. The really interesting question is if the Fed raises short term rates, i.e., is really serious about attacking inflation, will long term rates drop.

You really need to read my post before chiming in. This is not what I think will happen, I actually read Wolf’s article, my point is about magical thinking by people currently in charge.

For some reason, you like to direct your not so welcome comment at me like in the RTO article. This is the only time I’ll bite but you are more than welcome to reply to my comment

Phoenix Ikki, If you are being sarcastic, you have to indicate so, maybe with a “/sarc” tag. Otherwise how are we to know? People write the most ridiculous things and really believe what they write.

Phoenix_Ikki was clear to me.

I believe he was being facetious and questioning the logic of those in power (or lack thereof).

I think that there is proof of the physicists conjecture that reality depends on which dimension one is experiencing as normal.

Then, I proposed that my dog lives in a different dimension than I.

AI is mathematically destined to be stupid.

The thing about inflation is so many people have received higher wages and you can’t take those wages away so inflation is here to stay it’s great if you have assets like real estate or stocks that have gone up I feel bad for the younger generation who has to rely on only their wages

Why wouldn’t they?

The last 15 years has shown that the gov’t will always step in and bail people out. So be as irresponsible as you want because you can’t lose.

This bad behavior and speculation will continues until something bad happens and the gov’t lets the private sector really suffer the consequences.

There’s an awful lot of talk about stock bubbles in these comments. I tend to believe we are in a massive bubble myself. However, the total return of the S&P 500 with dividends reinvested for the period Jan 1999 to Dec 2024 was 8.180%. Nothing unusual here.

No. This is the biggest bubble agglomeration in human history. A crash is not desireable from the point of view of the asset holders.

Markets do what they do because they do it, that’s my ground rule.

Markets do what they do because the FED intervenes at the very slightest hint of a dent to valuations. They have told and shown the world that they will never allow stocks to correct. They will print money and destroy the currency to support them. That’s my ground rule.

i don’t know if this is true or not, but i do know that the silicon valley bank btfp program is what set the current mania in motion.

the fed hasn’t really been tested now in two years. we won’t know until a correction starts and they either start printing or hold off and do nothing

Agree 100%. If the Fed does an emergency rate hike tomorrow, market will crash on an epic proportion. Powell’s job is to never surprise the market.

“They will print money and destroy the currency to support them”

The historical evidence does show this to be mostly true.

Stocks fall 40% and Tim Geithner looks like he is close to suicide on TV and money printing has its biggest vogue since Weimar.

Housing costs zoom up 30% and the Fed is all about “measured, incremental responses”.

That does seem to betray a policy bias.

@FranzG

Yes. Soon as the fed stepped in and bailed out investors in SVB then it became a mania to keep the party going.

We must acknowledge that the Fed has certainly surprised many by raising rates aggressively and keeping them high for over 14 months. But that’s only part of the story. When one weak labor report came in, they quickly backpedaled with a 50-basis-point rate cut. Why didn’t they implement these cuts gradually, especially considering their previous approach?

As for QT, Powell has stated repeatedly that there has been no significant dent in reserves since the QT program began. Yet, they slowed down QT much sooner than expected. After only 8 months of a more cautious QT approach, overnight reverse repo (ON RRP) balances dropped to below $100 billion.

In his recent testimony before Congress, Powell didn’t outright dismiss the possibility of future QE. He indicated that the Fed would consider using it again if rates reached zero and there was a need to further support the economy. However, it would have been helpful if he had clarified that QE would not be coming back soon or easily.

To quote Adam Smith, “Some people don’t think the market be like it is, but it do.”

Stock Market Roulette: “Place your bets everybody. Round and round she goes, where she stops nobody knows. Good luck, everybody.” But unlike a legitimate roulette wheel, the guys with really big money know where she stops, because they can make her stop any time, anywhere.

Well, as Joseph Kennedy thought to himself, this seems like a good time to sell.

i’ve come to believe that there will never be a reasonable entry point for the purchase of assets again, at least not until the west’s financial system completely collapses, and something new takes its place.

the buy assets at all costs mantra is too ingrained for anyone, including the fed, to break it.

Agreed. RIP to buying and holding indefinitely, and especially to blindly buying indexes. Value investing and taking your modest gains is where it’s at- there still seems to be some decently valued companies out there. Oh, and T bills, lots of T bills.

isn’t it the opposite? it’s because people are buying and holding indefinitely, no matter the price, that the prices are so stupid.

Exactly. Everyone else is, so I’ll do the opposite, thank you!

We forget that 3 years ago, Italy was selling 100 year bonds at a negative interest rate.

In this eternal bull market, all news is good news. FED lost the battle against inflation. Markets won. The rich will thrive more, the poor will suffer more.

So the theory is just to give this more time. In other words – it’s transitory.

Obviously what is being done is not working. History repeating.

Like somebody said before: “This 4% inflation is not acceptable. There’s just no way we’d allow the 5% inflation to become entrenched, because this 6% inflation is not something we will tolerate for any length of time. The 7% inflation could really make things difficult due to this 8% inflation. We definitely don’t want to wait around long at 9% inflation, because this 10% inflation is becoming quite a bear. The 11% inflation is starting to eat away at people’s budgets, so we must arrest this 12% inflation soon, so that this 13% inflation doesn’t take off.”

Nice.

So DC will enpanel a 14% commission to make sure 15% inflation doesn’t shrink to 16%, the optimal growth model indicating that 17% is ideal, even though the American people really want 18%.

Absolutely.

Three shall be the number of the counting and the number of the counting shall be three. Four shalt thou not count, neither shalt thou count two, excepting that thou then proceedeth to three. Five is right out.

So sayeth the Fed members who say “Ni!”

Get ready for the bloodbath when the Fed lobbeth the Holy Hand Grenade of a rate increase to try to stop the killer rabbit of inflation.

Bring out your dead, bring out your dead

The sad thing is that if the markets and real estate dropped 30% overnight… It’s only a flesh wound!

We are now known as the FOMC who say:

Ekcy ekcy ekcy ekcy kabong…

Penny is too expensive to mint anymore. Can’t we ask China to do it for half a penny? Then we can tariff it at 100%. Win win.

This makes a lot of cents

It would make very little cents, literally.

Pennies are just sitting around in people’s change jars. No reason to make new pennies for 3 cents. Instead just institute a penny buy-back program, where the government buys pennies for 1.5 cents each. Genius!

US 1-MO

4.335

US 2-MO

4.318

US 3-MO

4.327

US 4-MO

4.337

US 6-MO

4.363

US 1-YR

4.267

US 2-YR

4.309

US 3-YR

4.324

US 5-YR

4.388

US 7-YR

4.456

US 10-YR

4.527

US 20-YR

4.792

US 30-YR

4.733

You can choose any yield you want, as long as it’s close to 4.5%.

Has the curve ever been this flat before? Only by letting the short end tick up a bit does the long end come down. Like a teeter totter.

My Bird food that I buy every week just went up 15%. Some of it comes from China.

Don’t buy Chinese bird food, LOL. That’s the whole point.

In addition, any news tariffs haven’t even been applied to the product you bought. This stuff takes a awhile. And the big de-minimus loophole closure has been rescinded for now. So what you paid was just a regular run-of-the-mill price hike, like gas prices going up, nothing to do with tariffs. A retailer just decided to rip you off and got away with it.

“This stuff takes a awhile.”

Wolf, you wouldn’t believe how many people were trying to buy things “before the price goes up on January 20th” at my little e-comm operation. I know because they would always bring it up when inquiring about backorder status/ETA of a popular product.

Meanwhile I’m like uhhh this stuff is already warehoused domestically…

Short:

Thereby making a price increase “entrenched.”

Inflation expectations for prices, assets or whatever are entrenched.

The people “know” prices only go up. The system tells us. As the Fed goes: 2%=flat

As the market goes (see above) 8% is flat.

Housing? Never had a down year (ignore the data).

US? Never defaulted (ignore Nixon, inflation and QE).

Crypto? Sound money

Got it? I don’t.

It is not surprising that PPI continues to push higher. Especially as regards services: To my knowledge, those with the last access to capital get their wage raises late in the economic cycle. The services portion of the economy is catching up to the massive price increases that have decimated wage earners and service providers buying power. Meanwhile corporate profits and margins remain high enough to support record highs in the financial markets.

andy,

Countries exporting to us do not pay the tariffs. It is the importer that pays the tariff. How is it that anyone does not understand this?

They lose market share if not pricing competitively, so they may

indeed take a hit in revenue.

What do you call a 25% hit to their GDP?

ONLY if they can’t sell to somebody else for any loss of sales

Frosty,

It’s ok because we will pay it to ourselves.

I should have been a central banker.

So odd that tea party Republicans are now tariff Republicans. I thought they were all about “remember the founders”! But, in their defense, some of the founders loved them some tariffs, like Madison and Hamilton.

Tariffs were prevalent in early America, before our government went nuts under FDR

Seems to me that if you are in Services (I am in software) that now is a good time to raise prices and also charge extra for CC payments while you are at it. The fast rising Tariff effects plus so many Foods Prices rising will hide all. And do not forget the upcoming Mid-West Farmers being shorted by the end of global food aid, not to mention that Ukraine (one of the biggest world food suppliers) is still being blocked from full production. And our new government may call ‘Drill baby drill’ from the highest rooftops, but the oil companies are not heeding the call at all. And are interest rates coming down anytime soon ?? I see a lot of storm clouds just off our coast and the winds are blowing our way.

“And our new government may call ‘Drill baby drill’ from the highest rooftops, but the oil companies are not heeding the call at all.”

Wells in the permain co-produce too much natural gas and NGLs which can’t be pipelined out quickly enough (and can no longer be flared off). This is currently the rate-limiting factor in oil production, and the reason natgas prices in the permian were negative for much of last year.

Rest assured, oil producers will consistently oversupply the market and drill themselves into bankruptcy given the chance.

Market action and bonds are indicting that these inflation reads are a blip and not a problem.

Are they? Or is that just your rationality to force sense into something that can’t be so easily explained

Can you provide a breakdown of services to show what is hot? Is it just a few services driving things up or everything?

I do that for CPI, I don’t do it for PPI, not worth it. Here is CPI, all major services detailed, a bunch of them with charts, and yes, it’s very broad:

https://wolfstreet.com/2025/02/12/beneath-the-skin-of-cpi-inflation-worst-month-to-month-acceleration-of-cpi-since-aug-2023-on-spikes-in-used-vehicles-non-housing-services-food-energy/

And this is before tariffs hit. The expectation of tariffs alone without implementation is cause for sellers of goods to pass on higher places under the guise of rising expenses. If this keeps going we will be back to 5% inflation by end of the year

MoM CPI is already at or above 5%

The biggest services increase for us has been insurance(house and cars) and property taxes. Blame the housing bubble, costs of labor for repairs/improvements, or global warming? Probably all of them.

Minimum wage also went up in many areas. I agree with this since rents are still high but it does cause inflation in construction, cleaning, ditch digging, landscaping, etc. Since many of the workers that did this work are likely immigrants, wages will continue to rise if they are no longer available.

I wonder how was it before 2022, before the influx of millions of immigrants or Pre 2020, when we have no inflation, no large number of extra immigrants to come here to work

“The biggest services increase for us has been insurance(house and cars) and property taxes.”

Same.

Difficult to tighten one’s belt and buy fewer of those things.

Good thing Powell put the brakes on QT in June eh???

Wouldn’t want to break anything like say… the inflation trend line.

/S

The US is just on a path of self destruction. Input costs are increasing even without tariffs because of wage increases. It’s a death spiral. We don’t need job losses, but we need people to tighten their belts a little bit to cool the economy by creating less demand. Unfortunately, sacrifice is not part of modern vocabulary. In fact, excess is the norm.

Trump just fired 200,000 government workers who had been employed less than one year. That should tighten some belts. That’s one way to cool the employment numbers.

Wouldn’t it make more sense to target positions strategically? The most recent hires are likely the positions that had the most need to be filled, thus the recent hiring. If the roles were necessary, they’ll be rehired. Recruitments and training are expensive, the payoff comes afterwards. These are also likely lower paying jobs (less experienced in their roles) in these departments, on average. This approach was lazy and lacked vision and strategy, a continuing trend.

So what you’re saying is we need a recession… Agreed!

Howdy Youngins. Have no fear. 50 / 50 chance this whole thing goes one of two ways. They Balance the Federal Budget and we will get a

1000 year Republic.

If they dont Balance the Federal Budget?

Its over baby.

Watch the debt clock and Doge clock and place your bets….

Was reading Ray Dalio’s latest tome today – all it takes is 4% in taxes, 4% cut in spending and 1% fall in real interest rates. Simple right? 😂🇺🇸💵

I’m starting to think that Real Estate in Washington D.C. may get hit hard by the government firings. Musk is going for broke. He is issuing mass firings via e-mail, just like he did at Twitter. Some of these people who just bought homes may find themselves SOL. (S$it out of luck). There are a shortage of listings anywhere in DC. This will change soon. We just appraised an 8 unit Condo that was bank owned, as the developer went out of business, before completing the conversion. The place looked like a trash dump on the outside, and the unit we appraised went for $50,000 below the $500,000 original listing price.

I’m not sure many government workers can even afford to buy in that market, prices have continued to rise in that city. Maybe the mass layoffs will affect landlords.

Real Estate agents here in the Swamp are finding it more and more to earn a living. There are few if any listings, and those that due come up are sold fairly rapidly, some without an agent, for whatever the demand price allows. Some are going for 10% to 20% below the price just 3 years ago. People just want to get rid of their property and get the hell out of here. This has been happening even before the mass firings of government workers and the contractors who support the government functions. It’s going to get ugly.

Economically and monetarily, it is 1979 again, and the next wave of inflation is just starting. Two BIG differences; 1) DEBT (cannot go “full Volcker”) and 2) we are moving from a uni-polar world to a multi-polar world.

The world needs much higher rates of interest, but the debt saturation creates a problem…

Interesting times.

It’s much worse than 1979. The Federal government is trying to do way too much. Spending is increasing massively since 2019. Nothing short of a massive cut to Federal spending can curb the coming inflation.

HHS Secretary RFK is saying he’s going to “Make America Healthy Again” he has exposed the total corruption of the food industry in the US today, which feeds off and begins with the lack of nutritional education in the public schools and elsewhere. I personally have given up shopping in my local chain grocery store, as the quality of the food has dropped dramatically. Now I go to a more expensive chain which sells high quality produce, seafood and salad bars etc, Example: Fresh unfrozen Icelandic Cod is now 21.99/lb. I pay the extra 30% because it is better for my health, and the food quality and selection is much better. Those without the ability to pay this extra 30% get to shop in bargain basement chain groceries that are more like junk food distribution centers. They wind up with future health issues as a result of eating that crap.

We are moving into a two America society. To former Presidential candidate, John Edwards I say, “where are you now that we need you”. He’s the one who said “There is one America for those with the means and another for the rest of Americans who don’t have it”.