Categories that helped power the cooling of CPI are U-Turning – used & new vehicles, food, energy – just as housing seems to be coming in line.

By Wolf Richter for WOLF STREET.

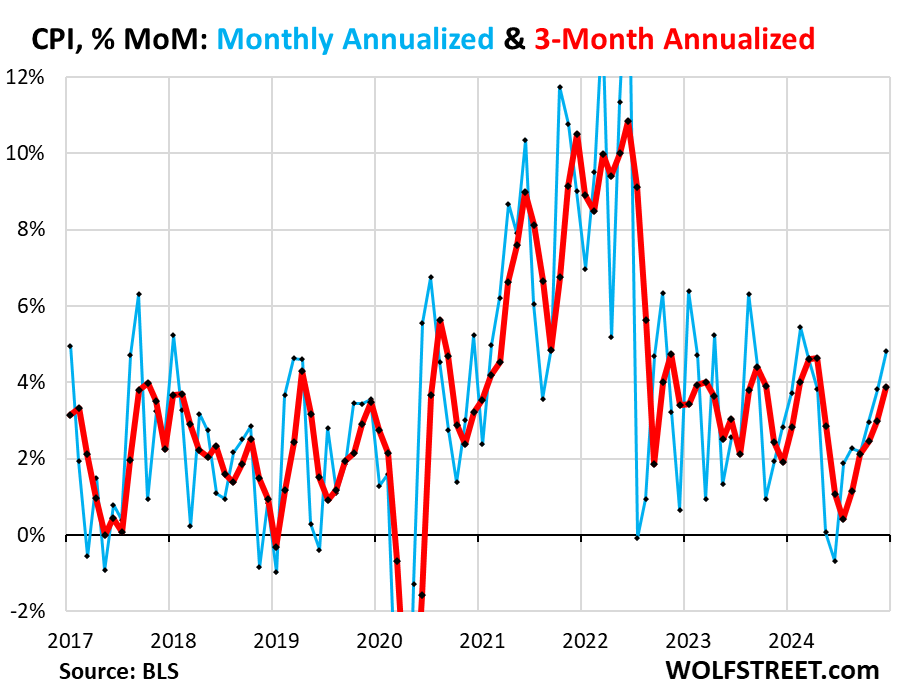

The overall Consumer Price Index rose by 0.39% (+4.8% annualized) in December from November, the sharpest increase since February 2024. It has been accelerating since the low point in June (blue).

The three-month CPI, which irons out some of the month-to-month squiggles. jumped by 3.9% annualized, the sharpest increase since April, and the fifth month-to-month acceleration in a row.

The year-over-year CPI rose by 2.89%, the sharpest increase since July, and the third month in a row of acceleration.

Categories that helped power the cooling of CPI are U-Turning.

Food price inflation, after a lull at very high levels, has been accelerating for months and now started to push the year-over-year needle higher. Energy prices surged for the month, which whittled down the year-over-year drop to just a hair. Used vehicle prices, which had plunged off the historic spike, jumped in December for the fourth month in a row, a sign that the plunge has ended, and further whittled down the erstwhile double-digit year-over-year plunge. New-vehicle prices also jumped for the second month in a row.

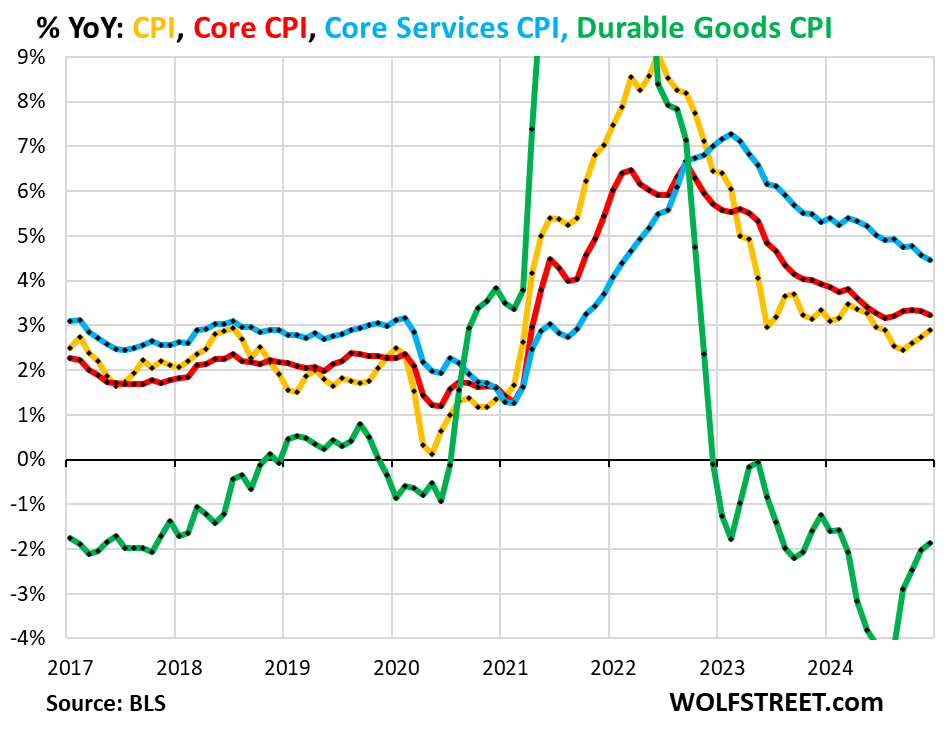

The Core CPI, which excludes food and energy components to track underlying inflation, rose by 3.24% year-over-year, a deceleration from the prior month (+3.32%), but a faster rise than in July and August. It has been stuck in the same 3.1% to 3.3% range for the seventh month in a row.

The major components, year-over-year:

- Overall CPI: +2.89% (yellow).

- Core CPI +3.24% (red).

- Core Services CPI: +4.46% (blue).

- Durable goods CPI: -1.87% (green).

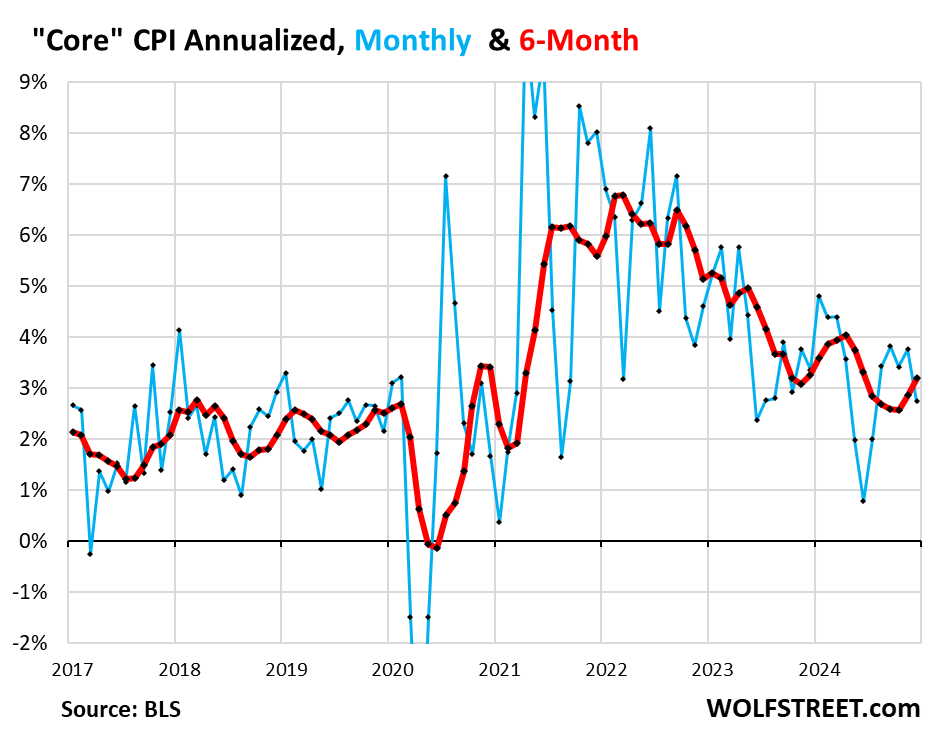

Month-to-month “Core” CPI rose by 0.23% (+2.7% annualized) in December from November, the smallest increase since July, following four months of the biggest increases since March (blue in the chart below).

The 6-month average “core” CPI accelerated to +3.2% annualized, the second month in a row of acceleration and the worst since June (red).

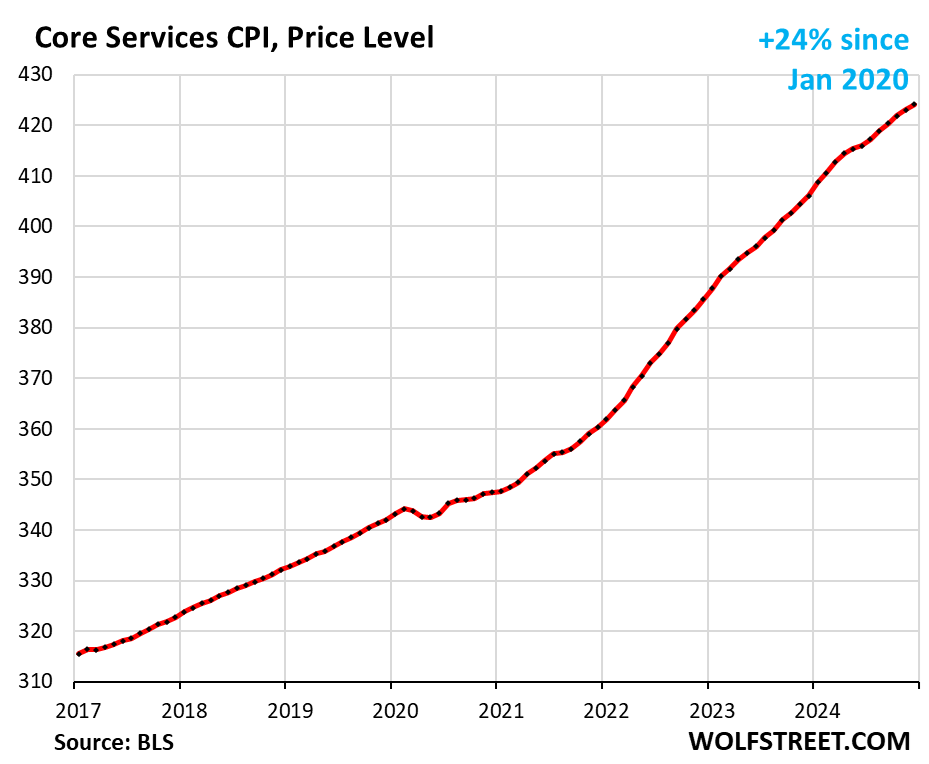

“Core services” CPI.

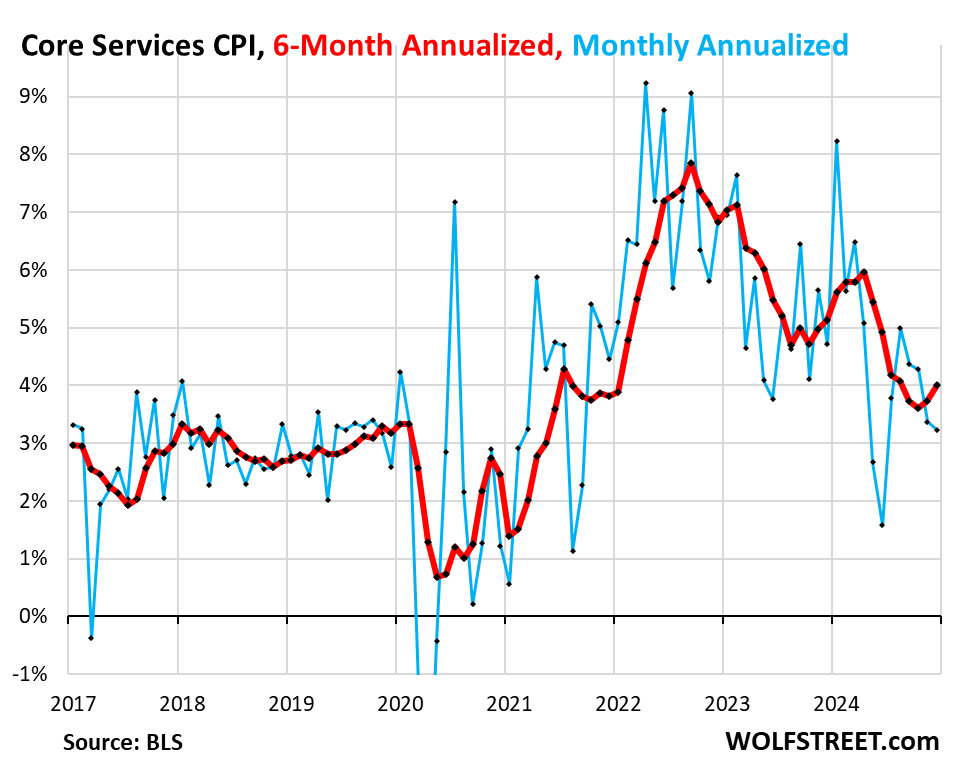

Month-to-month, the core services CPI, which are all services less energy services, decelerated to +3.2% annualized in December from November (blue line in the chart below).

The three-month core services CPI decelerated to +3.6%, but remained substantially higher than the 3.1% to 3.3% range over the summer.

The 6-month core services CPI, which irons out a lot of the month-to-month squiggles, accelerated to 4.0% annualized, the worst since August (red).

The housing components of core services.

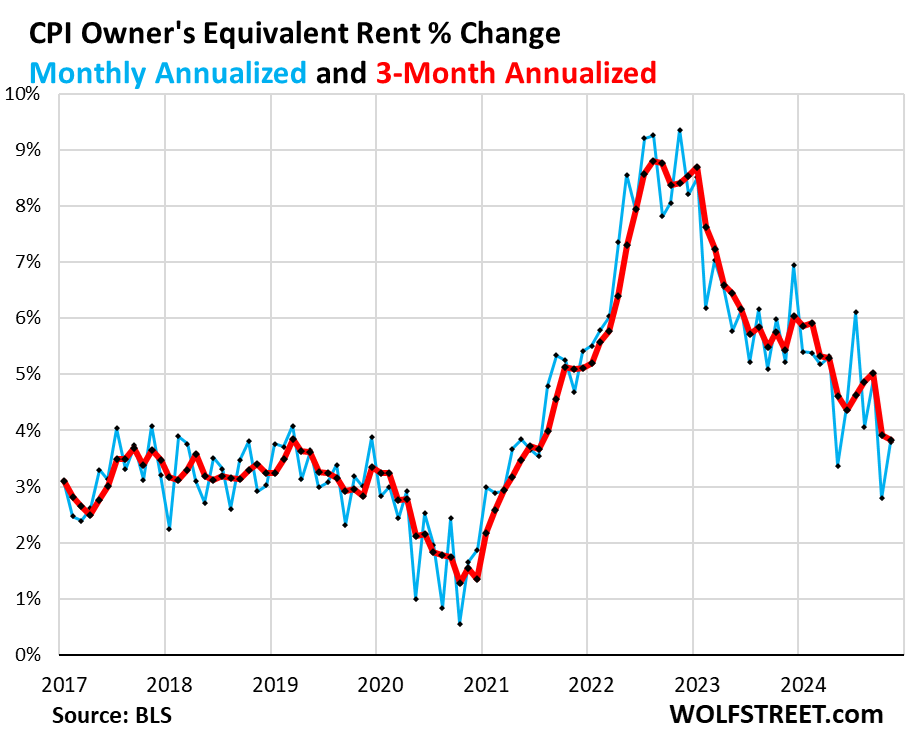

The Owners’ Equivalent of Rent CPI accelerated sharply to +3.8% annualized in December from November (+0.31% not annualized). The three-month average decelerated a hair to +3.8% annualized.

OER indirectly reflects the expenses of homeownership: homeowners’ insurance, HOA fees, property taxes, and maintenance. It’s the only measure for those expenses in the CPI. It is based on what a large group of homeowners estimates their home would rent for, with the assumption that a homeowner would want to recoup their cost increases by raising the rent.

As a stand-in for homeowners’ insurance, HOA fees, property taxes, and maintenance costs, OER accounts for 27% of overall CPI and estimates inflation of shelter as a service for homeowners.

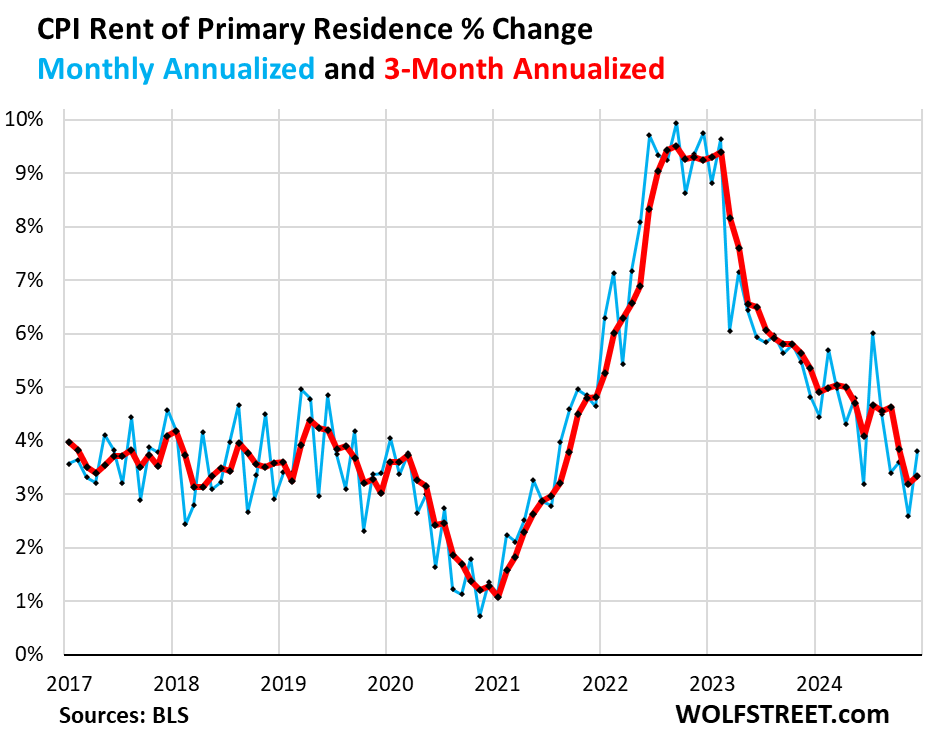

Rent of Primary Residence CPI also accelerated sharply to +3.8% annualized in December from November. The 3-month rate accelerated to +3.3%. The rent CPI is back roughly where it had been before the pandemic.

Rent CPI accounts for 7.7% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised vacant units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, paid in rent for these units.

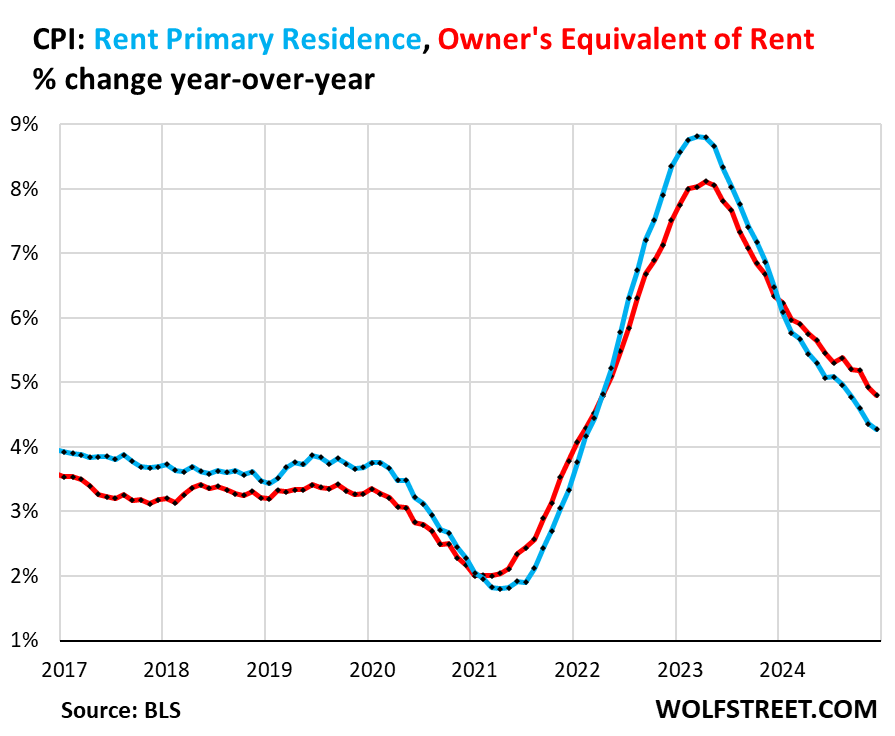

Year-over-year, both continued to decelerate: OER CPI +4.8% (red), Rent CPI +4.3% (blue), but both remain well above the range before the pandemic.

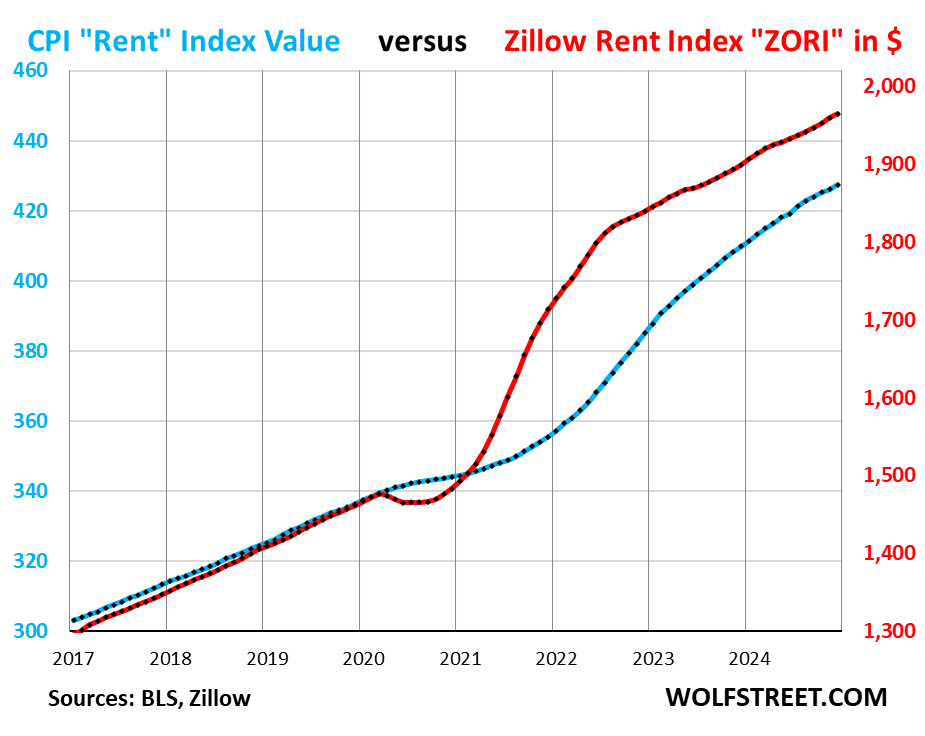

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market for rent. Because rentals don’t turn over that much, the spike in asking rents through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those jacked-up asking rents.

For December, the ZORI (seasonally adjusted) rose by 0.28% month-to-month and by 3.4% year-over-year.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 55% from January 2017:

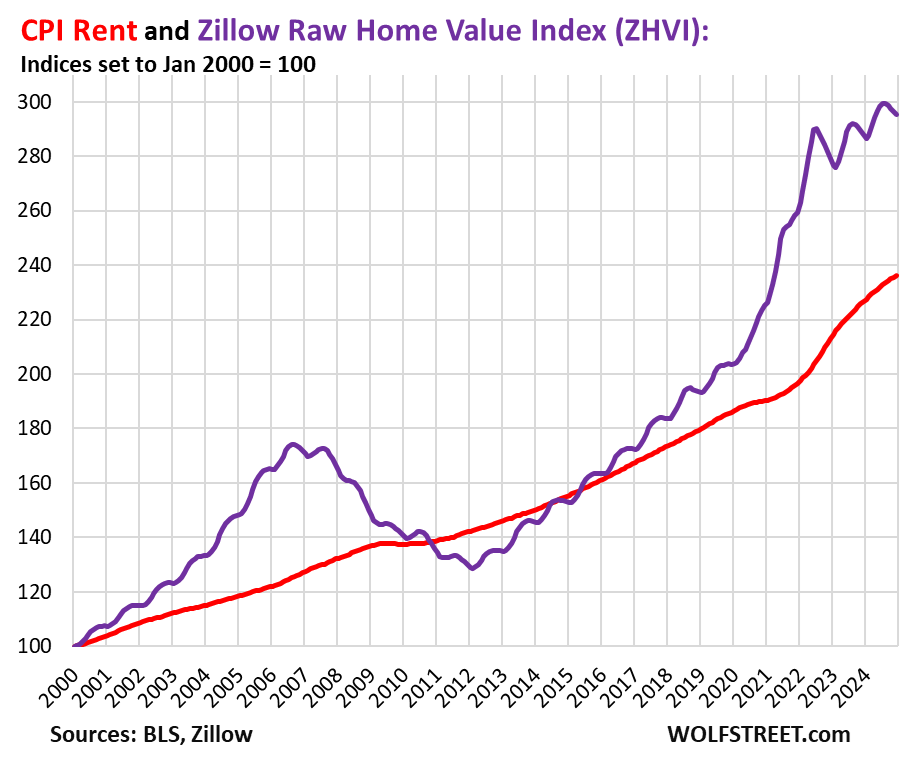

- Since January 2017: ZORI +52%, CPI Rent +41%.

- Since January 2020: ZORI +34%, CPI Rent +27%.

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence as index value. The purple line represents Zillow’s “raw” Home Value Index for the US. Both indexes are set to 100 for January 2000 [here are the largest, most expensive 33 metros: The Most Splendid Housing Bubbles in America ]:

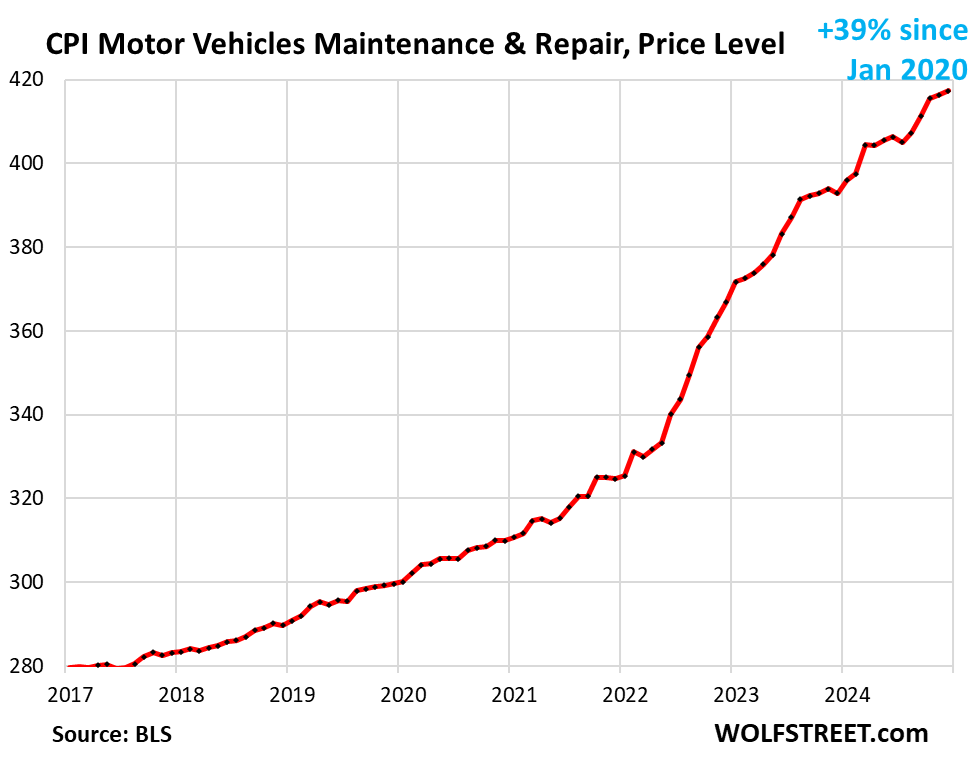

The CPI for motor-vehicle maintenance & repair rose by 2.2% annualized in December from November, after having spiked by 13% and 12% annualized in August and September.

Year-over-year, the index rose by 6.2%, the worst increase since May.

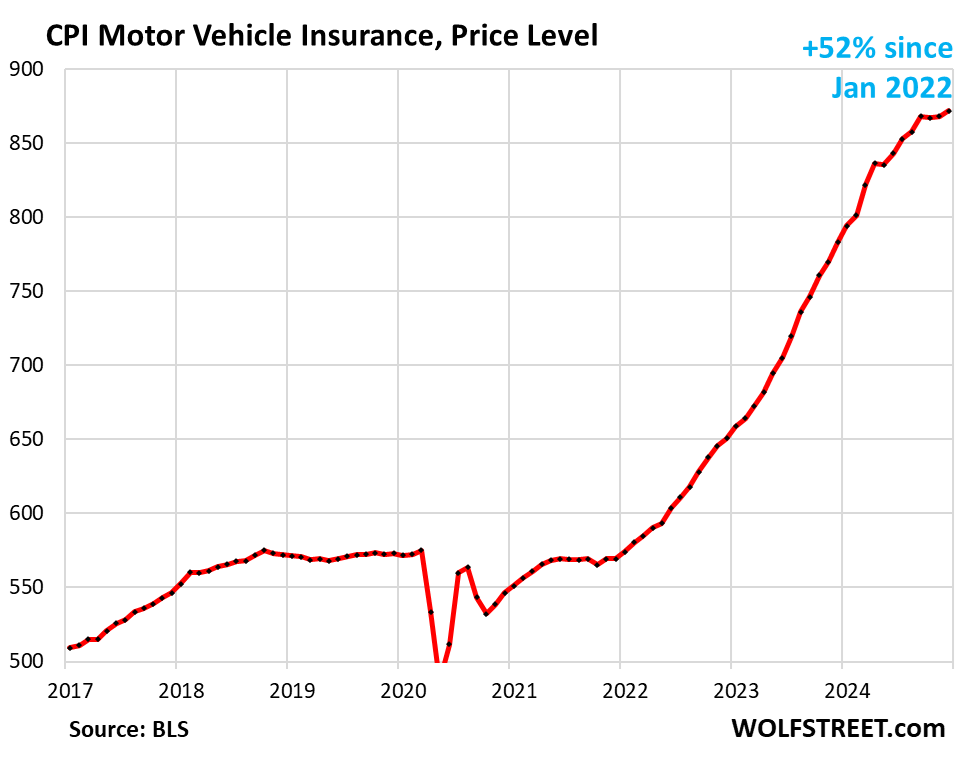

The CPI for motor vehicle insurance rose by 4.9% annualized in December from November, and by 11.3% year-over-year.

Since January 2022, it exploded by 52%, driven the historic spike in used vehicle prices, and therefore replacement costs for insurance companies, and by surging repair costs.

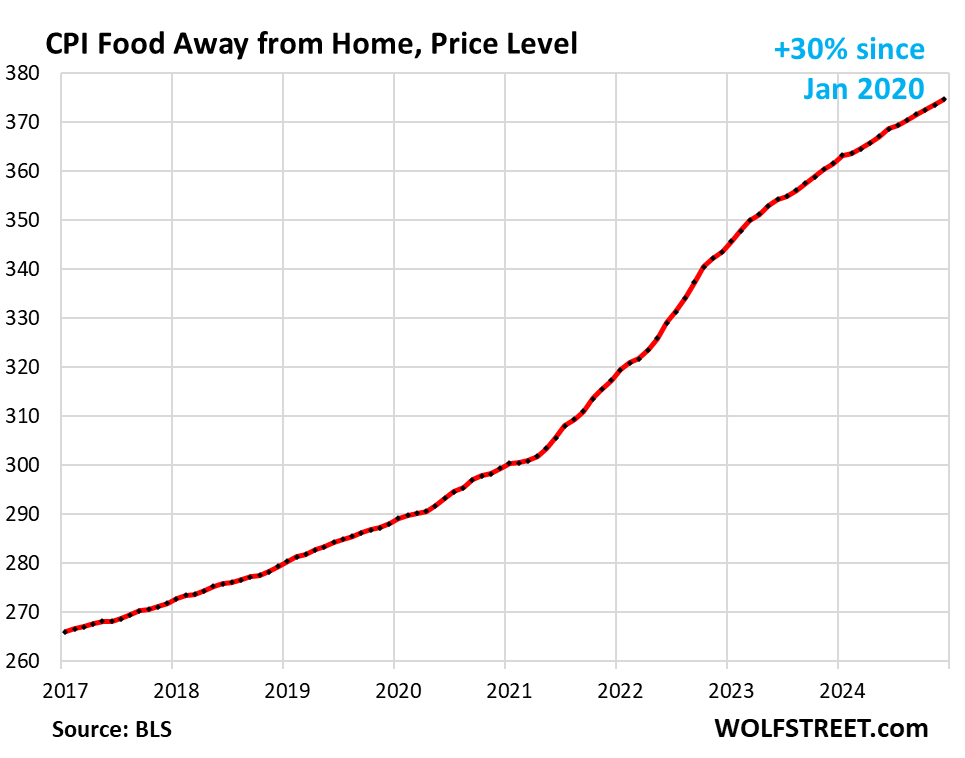

Food away from Home CPI rose by 3.6% annualized (+0.30% not annualized) in December from November, and by 3.6% year-over-year, same as in the prior month, and the smallest increase since August 2020.

Often called food services, the category includes full-service and limited-service meals and snacks served away from home, such as in restaurants, cafeterias, at stalls, etc.

| Major Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 65% | 0.3% | 4.8% |

| Owner’s equivalent of rent | 27.2% | 0.3% | 4.8% |

| Rent of primary residence | 7.8% | 0.3% | 4.3% |

| Medical care services & insurance | 6.5% | 0.2% | 3.4% |

| Food services (food away from home) | 5.4% | 0.3% | 3.6% |

| Education and communication services | 5.0% | -0.2% | 1.8% |

| Motor vehicle insurance | 3.0% | 0.4% | 11.3% |

| Admission, movies, concerts, sports events, club memberships | 1.9% | 0.3% | 2.8% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | -0.3% | 3.7% |

| Lodging away from home, incl Hotels, motels | 1.4% | -1.0% | 2.6% |

| Motor vehicle maintenance & repair | 1.3% | 0.2% | 6.2% |

| Public transportation (airline fares, etc.) | 1.1% | 2.7% | 5.7% |

| Water, sewer, trash collection services | 1.1% | 0.1% | 5.2% |

| Video and audio services, cable, streaming | 0.9% | 0.8% | 1.5% |

| Pet services, including veterinary | 0.4% | 0.1% | 6.2% |

| Tenants’ & Household insurance | 0.4% | 0.0% | 1.7% |

| Car and truck rental | 0.1% | 0.6% | -6.2% |

| Postage & delivery services | 0.1% | 0.4% | 10.1% |

The Core services CPI overall has risen by 24% since January 2020.

Prices of Goods.

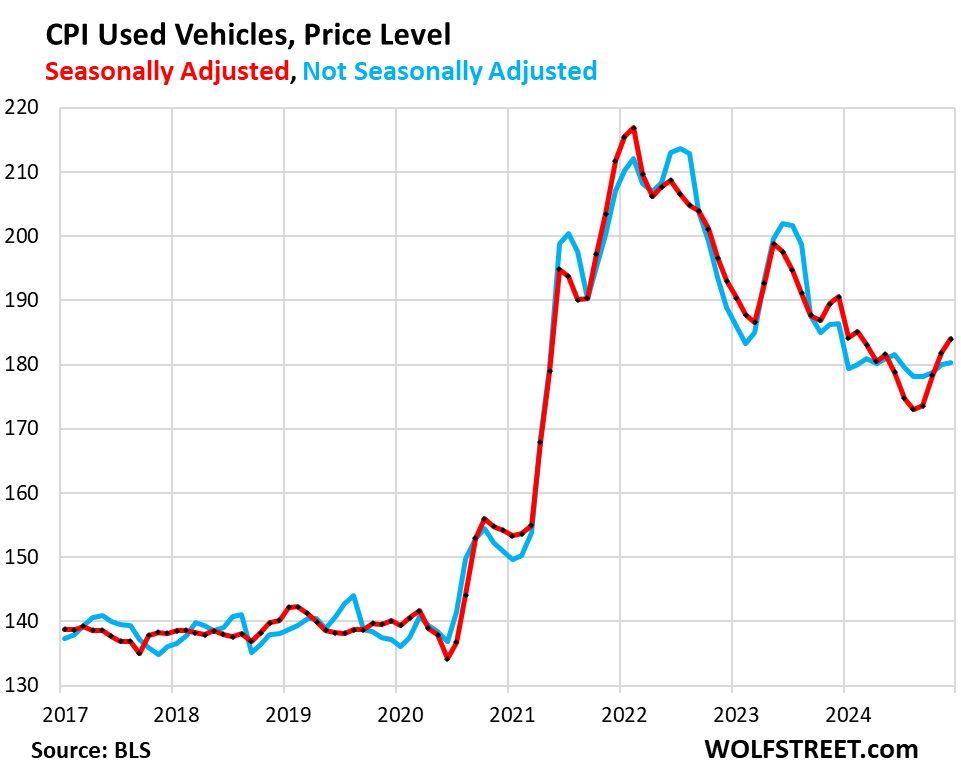

The used vehicle CPI jumped by 1.2% not annualized (15.5% annualized) in December from November, seasonally adjusted, the fourth month-to-month increase in a row (red).

Not seasonally adjusted, the index also increased though it would normally fall in December (blue).

The recent surge has whittled down the year-over-year decline to 3.2%, from the year-over-year plunge of over 10% last summer.

The 20% plunge of used vehicle retail prices from early 2022 through August 2024, seasonally adjusted, was a powerful factor in the cooling of CPI inflation. But that has ended. This U-turn in used vehicle retail prices has occurred amid very tight retail inventories, strong demand, and rising wholesale prices.

Prices are still up 32% from January 2020, and there are now substantial doubts they will give up more of the pandemic price spike.

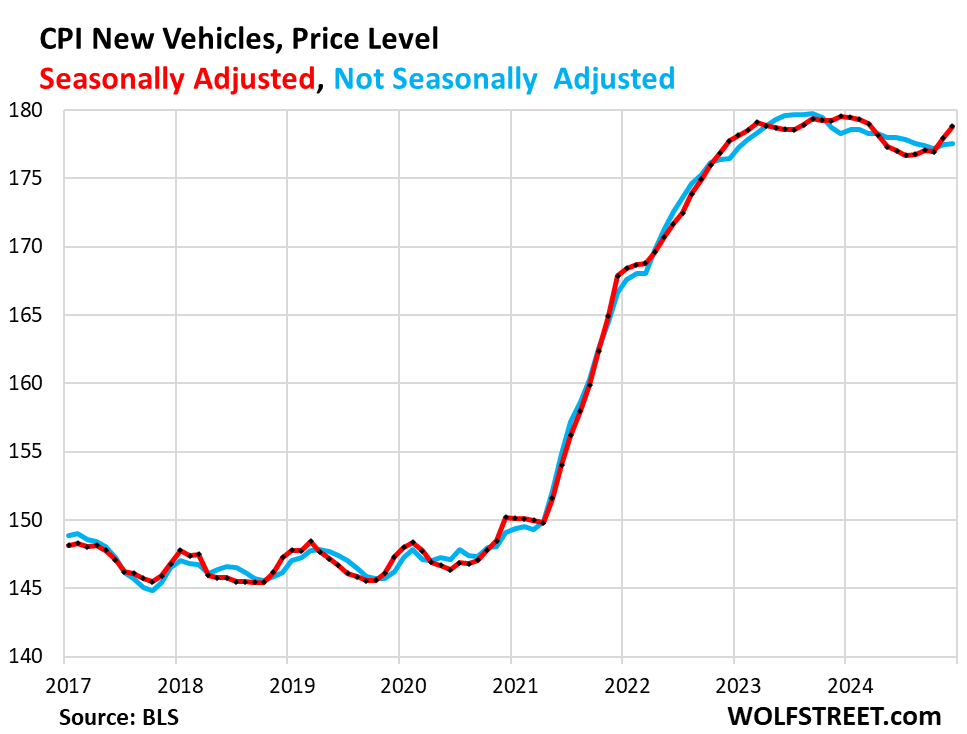

New vehicles CPI jumped by 0.47% not annualized (+5.8% annualized) in December from November, seasonally adjusted, the fourth month of increases over the past five months.

This whittled down the year-over-year drop to 0.4%. Since January 2020, the index is up 20%. At this rate, new vehicle CPI may carve out a new all-time high in a month or two; it’s now just 0.4% below its prior all-time high.

New-vehicle prices have been very sticky, unlike used-vehicle prices, despite the glut of new vehicles now on many lots, as automakers are trying to preserve their profit margins. The big incentives and discounts in recent months mostly just undid part of the increases in MSRPs.

But EVs experienced a lot of demand, and EVs sales surged toward the end of the year, and were up about 10% for all of 2024, despite the decline in Tesla sales, even as ICE vehicle sales edged up by less than 2%, and this demand for EVs may have contributed to the surprising rise of the CPI for new vehicles over the past two months.

New and used vehicles dominate Durable Goods. All major durable goods categories experienced often dramatic price declines starting in mid- to late 2022, after the price spike during the pandemic. But the month-to-month price drops in motor vehicles ended in September, and prices have risen since then. The other major categories of durable goods prices continue to decline:

| Major durable goods categories | MoM | YoY |

| Durable goods overall | 0.2% | -1.9% |

| New vehicles | 0.5% | -0.4% |

| Used vehicles | 1.2% | -3.3% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.2% | -0.9% |

| Sporting goods (bicycles, equipment, etc.) | -0.4% | -2.0% |

| Information technology (computers, smartphones, etc.) | -1.0% | -7.6% |

Food Inflation.

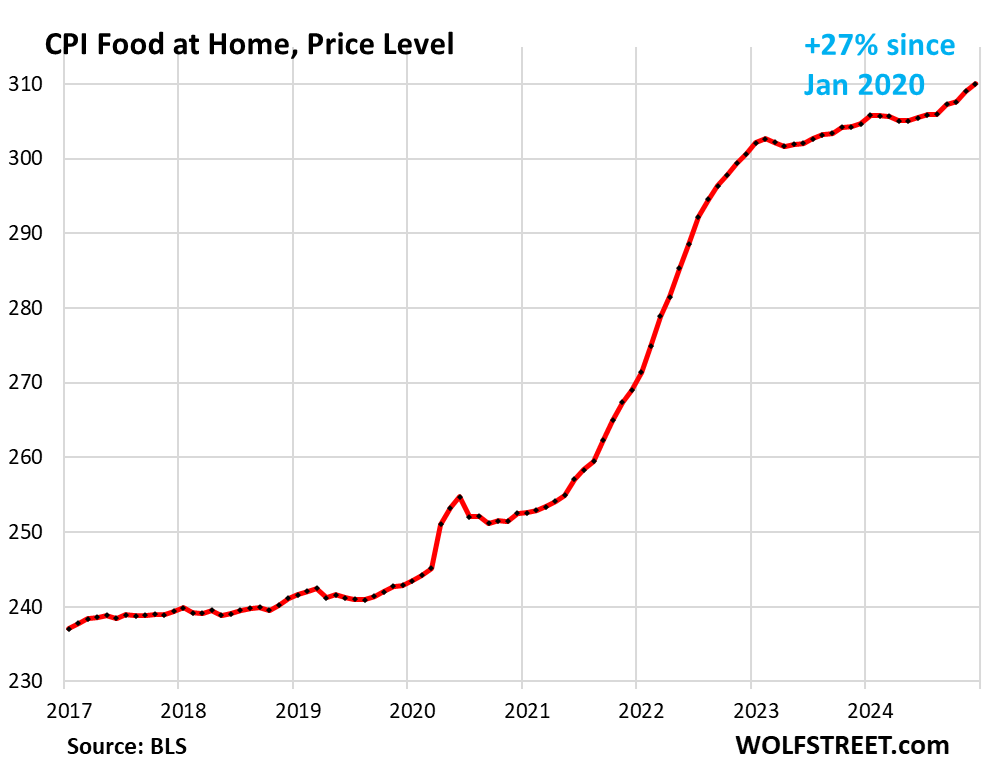

The CPI for “Food at home” – purchased at stores and markets and eaten off premises – jumped by 3.9% annualized in December from November (+0.32% not annualized). After a lull at painfully high levels, food prices have been increasing for the past six months, visible in the steepening slope of the chart below.

This pushed the year-over-year price gain to 1.8%, the biggest increase since October 2023.

The avian flu outbreak that started months ago has by now created egg shortages, with many stores in January showing empty shelves, and what is available is marked up a lot. The CPI here is for December and doesn’t yet reflect the prices in January.

Also note how price increases are creeping back into other categories, including beef, from already very high levels.

| MoM | YoY | |

| Food at home | 0.3% | 1.8% |

| Cereals, breads, bakery products | 1.2% | 0.8% |

| Beef and veal | 0.5% | 4.9% |

| Pork | 0.3% | 1.8% |

| Poultry | 0.1% | 1.0% |

| Fish and seafood | 0.8% | -0.7% |

| Eggs | 3.2% | 36.8% |

| Dairy and related products | 0.2% | 1.3% |

| Fresh fruits | -1.1% | -0.2% |

| Fresh vegetables | 0.8% | 3.1% |

| Juices and nonalcoholic drinks | -0.8% | 1.8% |

| Coffee, tea, etc. | 0.8% | 3.5% |

| Fats and oils | -0.6% | 0.4% |

| Baby food & formula | 0.4% | 2.1% |

| Alcoholic beverages at home | 0.1% | 1.0% |

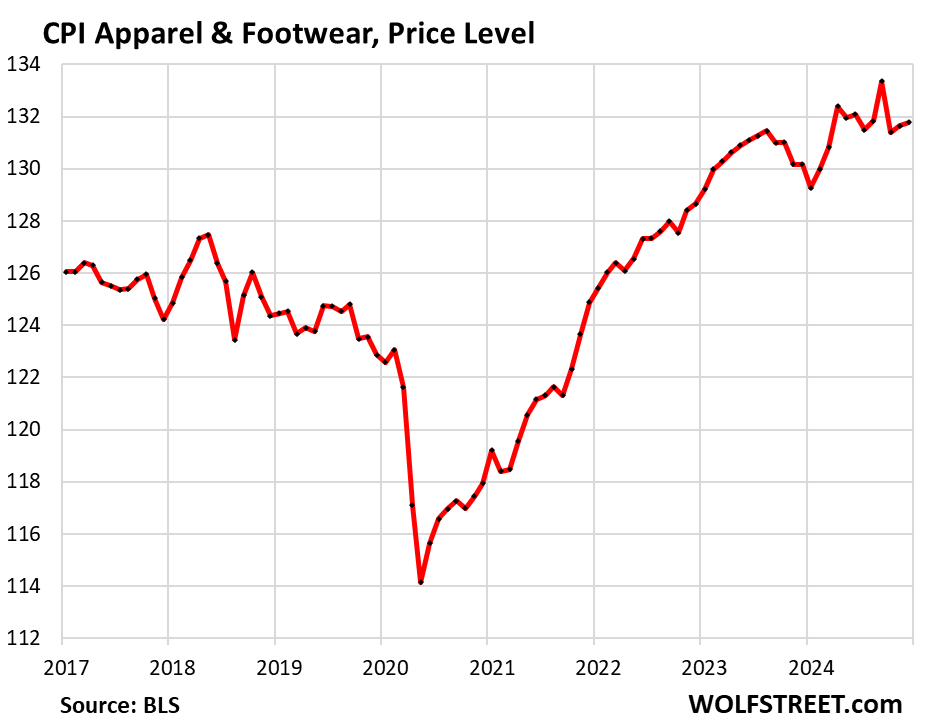

Apparel and footwear.

The CPI for apparel and footwear inched up by 0.1% in December from November and by 1.2% year-over-year.

Apparel and footwear are components of nondurable goods, along with food, gasoline, household supplies, personal care items, etc.

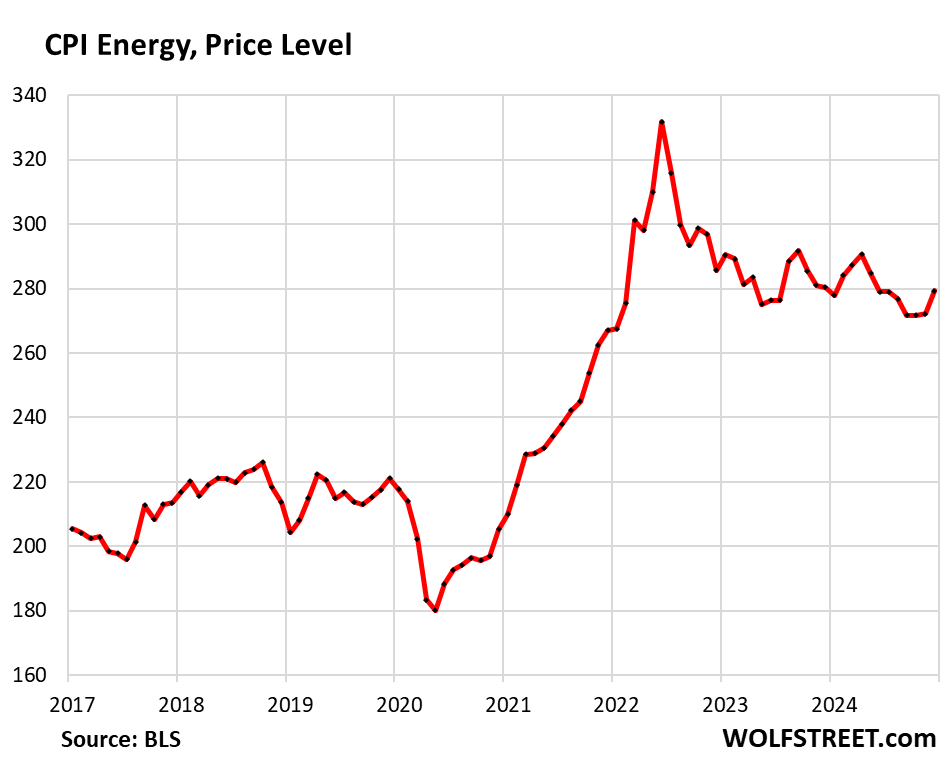

Energy.

The CPI for energy, which covers energy products and services that consumers buy and pay for directly, jumped by 2.6% in December from November, which further whittled down the year-over-year decline to just 0.5%.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 2.6% | -0.5% |

| Gasoline | 4.4% | -3.4% |

| Electricity service | 0.3% | 2.8% |

| Utility natural gas to home | 2.4% | 4.9% |

| Heating oil, propane, kerosene, firewood | 2.6% | -6.0% |

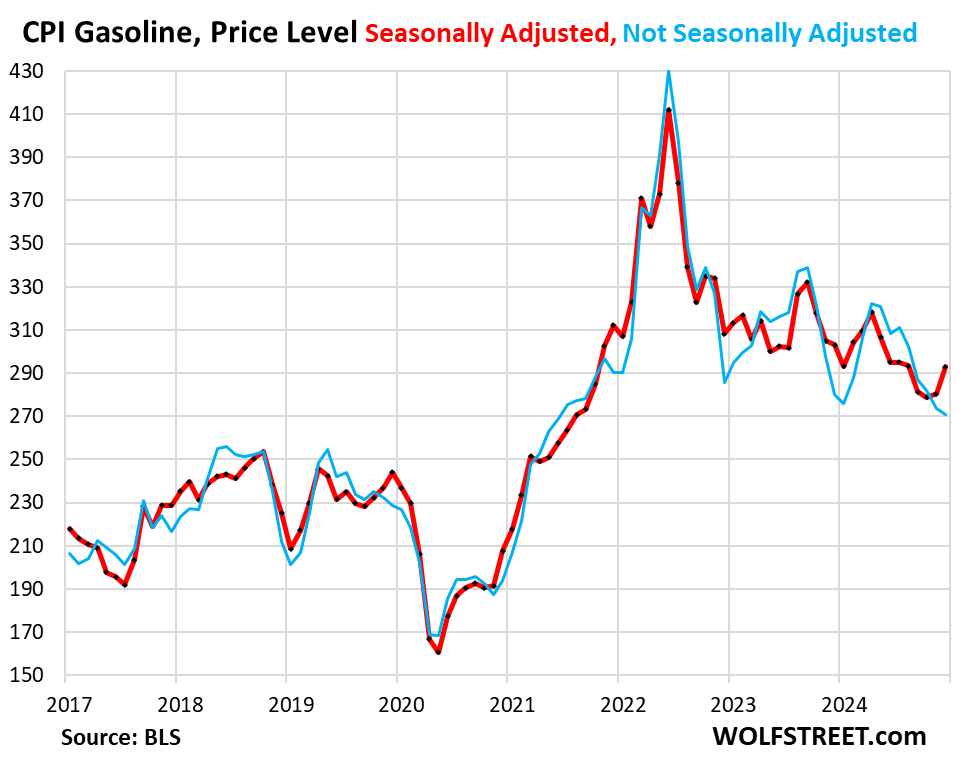

The CPI for gasoline makes up about half of the energy CPI. It jumped 4.4% in December from November, seasonally adjusted, which whittled down the year-over-year decline to 3.4%.

Compared to the peak in the summer of 2022, gasoline prices plunged by 29% seasonally adjusted (red), and by 37% not seasonally adjusted (blue).

The plunge in gasoline prices off the mid-2022 peak had been a big factor in the deceleration of the overall CPI.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks WR for this report.

Your reports/opinions are exactly opposite of MSM and I truly appreciate it.

I go into town & its packed with California aristocrats in the wine country blowing money.

I don’t think carry out pizza should cost $90.00 but here they do.

Has everyone lost their mind?

I have cut my costs down to the bone.

The stocks/real estate/crypto people are sh!tting in tall cotton, spending like there’s no tomorrow. The people with no assets are in a financial depression due to inflation.

yes. the capital class is driving inflation, which is why so many people have remarked to me lately that the costs of hotels, car rentals and other things are through the stratosphere. the fed created a mania and the wealth effect spending is on full display among the top few percent.

as long as they have their perceived wealth, inflation will continue at 3-5%

Bond market had a nice little celebration of the “good” news today.

Unbelievable right? How can the PPI and CPI readings be anything but acceleration in the wrong direction?

And they partied even harder today (Thursday 1/16).

Repos are 94 billion today, first time under 100. They should continue to go down.

“Reverse repos” or rather reverse overnight repos, or ON RRPs

The cold air all the way down to Texas will certainly not help keep energy prices down for this month

Not sure how much of flyover country has residential natty gas, but those prices are rising from historically low levels.

Gasoline/oil are still extremely expensive relative to natural gas on an energy-equivalent basis.

Those heating with firewood are getting a nice surprise this winter. My wood pellets actually cost less per bag than they did last winter.

ShortTLT – The only thing I use wood pellets is to smoke meat!

Not Wolf – True – I Need to fire up the generator to make sure it’s ready to go.

I suggest doing that on a regular schedule. I test run my backup genny for 10 minutes once a month. Engines don’t like to sit for long periods of time.

Wall Street latched on to the CPI report today like it was better news than it could have dreamed of. Cant wait to see how this plays out…..

Deep inside the Federal Reserve a group of PhD Economists calculate high the CPI can go before they get a real live French Revolution.

I’m confused. Wall St. liked the CPI report so bond yields are down because they think the Fed will cut rates. Except every time they’ve cut rates recently, longer dated yields have gone up.

not to mention that there was nothing in this cpi report that would lead the fed to change its recent statements that they’re at neutral.

Wolf has showed us accurate picture for CPI.

As usual MSM twisted the articles and headlines. But they are NOT alone.

Today FED Governor Waller called latest CPI report “very good” on CNBC interview. Come on. Not once but twice in same interview. Calling latest CPI report Good Report is pure Stupidity and being irresponsible.

Then he goes on to say IF and BIG IF if we continue to get this kind of reports, there will be cuts in even in first half of 2025.

I can understand IF part disclaimer. He can say anything with IF disclaimer. But then calling higher inflation read as Good or Acceptable reading makes that IF very subjective/low bar. He said even March rate cut is not off the table. Even give hints for 3-4 cuts this year. What a shame..

10 year dropped by 15 BP and 30 years too.

“Then he goes on to say IF and BIG IF if we continue to get this kind of reports, there will be cuts in even in first half of 2025.”

This is really funny. IF month-to-month CPI inflation continues on the same track as over the past three months, year-over-year CPI might hit 5% at the end of the first half of 2025.

Wolf,

Those are Waller’s words from CNBC interview.

I was just pointing out even FED Governor is also talking irresponsibly along with Paid Wall St media/MSM.

Media saying vs FED Governor saying is diff.

I was calling out that kind of talk by FED as shameful/irresponsible. Do you agree?

It’s not correlated. Long-term yields rose because of renewed expectations around inflation, higher for longer, etc., not because the FED cut rates.

Agree, it’s not directly causal, but the fed lowering rates indicated a lack of seriousness to taming inflation to the market. Bonds had been rising until September then pivoted almost exactly at the rate cuts and have essentially gone the opposite direction since.

That was just the scared money going back home to equities (where it belongs). They took 7-10 days worth of yield gains off the table. Let’s check back in a week and see where it’s sitting then.

scared money belongs in equities at stupid high valuations?

FOMO is a hell of a drug

If they saw something in today’s numbers that prompted a move out of treasuries that’s exactly where they belong.

What was the dump, 12 bp at close? We’ll have that back in 2 weeks. There’s gonna be lots of resistance at 5% from surging demand, but once the dam breaks watch out…

Fear – Vanguard embraced the mentality. They actually set up a fund for those individuals, VFMO.

Thanks Wolf,

Listening to Bloomberg while driving today and they made it sound like all is great- 10 year down 15 basis points, The Fed will cut cut cut blah blah blah

The 10 year had to take a breather at some point – going up 5-10bps every day wasn’t sustainable.

Still a lot more room for coupon yields to keep rising.

Which CPI reading is the most important, overall, core, services, other? The lowest one, of course!

Yep, that’s the point of all these different measures – they will always take the lowest and spin it as good. We will see if the media does a 180 once trump is in.

Good thing no one has a car in this country anymore, lol.

The spin depends on who the audience is and what sorts of revenue can be extracted from them.

This is pretty nerdy stuff, not for general consumption. Regular folks just want to know what egg prices are and gas prices, they’ll complain about both until they are back at 1993 levels.

Another excellent WR analysis. I really like the two decimal places. Interesting that the usual psychotic stock market and the normally staid long bond market both way over-reacted to a mere one month’s set of data. Very skittish, very frightened. The Fed set the standard for over-reaction when it dropped 50 bp based on data that turned out to be erroneous. Way to go, Jerry!

not to mention that the inflation report wasn’t “tame” the way the cnbc and bloomberg boys are describing it.

goebbels would be proud!

He learned everything from Eddie….

“The conscious and intelligent manipulation of the organized habits and opinions of the masses is an important element in democratic society. Those who manipulate this unseen mechanism of society constitute an invisible government which is the true ruling power of our country.”

-Edward Bernays

There is no excuse for the BLS to not publish these numbers out to two decimal places. When something moves 0.3% there is a 33% move in the rate of change to the next headline number. Unless of course there is a bias to get a result of say 0.34% so it can get initially rounded down and then get buried in revisions up in the next month to the actual say 0.36%.

Nah they wouldn’t do that…would they?

CuriousZiggy, It is one of my pet peeves. Say an indicator changes .3%, which is a rounded number. The actual number could be anywhere from .25% to .34%. That’s a heck of a range. And yes the government could easily do it. I wonder why they are fixated on publishing amost all indicators to one decimal place. It is so stupid. They publish the I-bond six month inflation component to five decimal places, as I recall.

The reason for rounding is to not create a false sense of 100% accuracy. All economic data are estimates, nothing is 100% accurate, and rounding the numbers and saying “about 0.3%” makes that clear.

But the problem is the media and the markets that make a huge deal out of something rising 0.2% (0.249%) when 0.3% was expected, and if it had risen by 0.251% instead of 0.249% it would have hit the mark. What the media/markets do with these rounded numbers drives me nuts.

Markets got overcomplacent since SVB bailout and are constantly fueling the inflation. QT is too slow to frighten the markets. Fiscal policy is a complete joke – ever increasing budget deficits do not help either. It seems the inflation has bottomed already. It will probably go up from here. This may cause trouble for the Reps in the midterm elections unless they focus on the budget discipline (which I don’t have any hope for).

1:04 PM 1/15/2025

Dow 43,221.55 703.27 1.65%

S&P 500 5,949.91 107.00 1.83%

Nasdaq 19,511.23 466.84 2.45%

VIX 16.12 -2.59 -13.84%

Gold 2,720.00 37.70 1.41%

Oil 80.40 2.90 3.74%

But notice how with all that surge the S&P did not retake the 50-day MA? Bull trap

MW: Dow ends up 700 points as U.S. stocks surge on bullish CPI inflation report

Don’t you love those headlines!? Worst YoY CPI readings since July, worst MoM CPI reading since February, and we get those silly headlines. Obviously, a lot of this stuff is produced by AI, or maybe by English-major interns.

but that of course means that the algos are trading on the headlines, so it’s not like the lies are contained to the media.

Whoever sets “Wall Street expectations” must set them high so even a tiny improvement is seen as reason to “cut, cut, cut”. It would be appropriate from someone from the Fed to just say, “Y’all must be pretty stupid, what about 2% don’t you understand?” Sorry, unreasonable dream.

Its the same for company earnings. The analysts all low ball estimates so that companies can hop over them and create the short term rallies on “beats expecations” and “beats on top and bottom line”. Its all by design.

Thank you Wolf! My trust in main stream media, which was already low just got knocked down even lower. If a juror knows all those “silly headlines” are false it’s difficult to believe any headlines. This is much bigger than Wolf Richter! I hope you will expand your mission a bit to go so far as to call out the major media outlets with misleading headlines and reports.

They’re produced FOR AI and algorithms. Who knows “what” publications are used to fed them. Who chooses them and how they are weighted. BIG $$$$$$ leading the corruption, collusion, and control. WR obviously isn’t on their list!

Def English major interns (I was an English major 😉). The bots are smarter.

Wolf gives us the unvarnished version and we thank you WR.

Thought you would get a good laugh out of that one today!

Excellent data and analysis.

Higher inflation should indicate no rate cuts so why is the Market saying otherwise?

I remember the infamous Black Monday crash of 87′, supposedly caused by computer driven trading and human panic. I would not be surprised if some bozo decision or statement might cause a similar event. Even though there is a time-out halt process, things are just too volatile these days.

With budget deficits everywhere, how can there be stability? A steady LOW inflation rate target just doesn’t seem possible with enormous budget deficits and no way to tame them. There are limits to growth.

I don’t think the market is indicating any more rate cuts. 1 year treasury is 4.2%.

No, Black Monday was caused by the sharpest decline in legal reserves since 1913 coupled with contemporaneous reserve requirements.

Not great, not terrible. Services coming down slowly. Feels like we would stick at this rate level for a while if it wasn’t for the coming Trump reforms. Rates are likely to increase at that point, but difficult to tell right now. He has already dropped some of his previous promises, so who knows what policies he will bring in and what he won’t. And there are still some republicans who care about the deficit, even if they are a diminishing number themselves. Hard to see through politics but it seems to be the deciding factor going forwards.

Well, after the disappointment from no Santa Rally, and the steady climb in long rates chipping away the foundation of any remaining Bull market, they basically needed something to latch onto to get a nice pop – which should mostly hold through the weekend. Of course Monday the markets are closed, and when they open on Tuesday – well, don’t be surprised if everything including the CPI is suddenly seen and interpreted far differently than it is right now.

I begin to wonder if the Wall Street headlines are the big money manager class “playing” the retail investor class.

Totally. It’s all manipulation. If I read one more NAR spin headline on how 2025 is going to be fantastic for housing price gains I may throw something at my screen. All that stuff does is encourage the six people left who can still afford to buy a house that they need to buy *right now* before prices go up. And it convinces sellers they should tack on a extra $100k so as to not leave money on the table.

Massive con, all of it.

Yes, they will suck us dry and then laugh about it. I quit reading msm. It is just so stupid. Best source for analysis is wolf street.

Likely

LOL! Ya think? It’s been this way for a while. In fact, quite often pension funds are loaded up with bullshit “financial products” that wall street bank know are bogus (hello MSB/CMBS)…

History repeats/rhythms and nothing changes until there’s a genuine world war or people in powerful positions start losing their heads. History is very clear on this, it’s human nature.

Same as it ever was!

This is all so crazy to me.

Inflation starts going down and the Market goes up, then the FED cuts rates and the Market goes up again, then the FED says it won’t cut for a while, or maybe not at all in 2025, and the Market still goes up. Then, today, inflation takes off again and the market goes up again. Whether inflation goes up or down, the Market goes up?

What, if anything, will make this market go down and stay down low enough to remove the hot air that’s in it? Is there ever going to be a “normal” Market? Or normal anything?

Maybe I am dreaming all this….

Could it be just too much liquidity? Yes $2T off Fed balance sheet, but reverse repo still has gas in the tank…maybe that ends in the next few months…and I thought the reverse repo is essentially “excess reserves” so even though $2T lower, its still lower excess…meaning excess remains.. Maybe until bank reserves start draining we won’t see markets go down?

Well, Jerry has been working on it and will continue to work in it.

His recipe for not blowing up the markets:

A little easing of the interest rates here

A very, very, very slow QT there

A sprinkling of fairy dust everywhere

Voila, someday we will normalize…

Unfortunately, it will be well after all the little people are crushed by inflation.

Little People? You must mean us Taxing Units?

Yes, the ones who haven’t reached enough of a wealth level to hire CPAs, financial/investment advisors, and tax lawyers who make sure that their clients pay the absolute minimum tax or nothing at all by using all the loopholes and tricks.

Bloomberg reported the core CPI rose 0.2% after rising 0.3% for the four preceding months. It annoys me that the data are rounded to one decimal place. There’s a big difference between 0.15% and 0.24%, but both numbers would be rounded to 0.2%.

The very definition of “Irrational exuberance” in the stock market. Watch out!!!

It doesn’t matter what actually happened. It only matters that it came in below Wall Street expectations. That’s what everyone here fails to see. Now, time to play for opex.

Could the shelter disinflation kill other inflationary items next year!

Shelter disinflation (lower inflation) will end/stabilize just like disinflation in new and used cars, energy, food, etc. ended. Disinflation runs out of steam sooner or later. It’s not something that just keeps going.

Not usually.

However, I think we can all agree that Swans are circling

Good news all around.

There are few investors left, everything is a trade.

Not many can say they have held an individual stock for years and they are small potatoes if they can.

Can many remember when it took 1 to 3 days to buy or sell a stock?

Nothing wrong with the speed except it adds volitility and costs to the business who issued the stock.

The winners are the dealers, insiders, and banks who use the churn.

The issue of liquidity only matters to the traders. Would a few hours even matter to an individual?

Today is an excellent reason not to own stocks and choose options, if you must play a rigged game.

Sigh, I guess it’s time for rate cuts.

No. It’s time for significant rate increases immediately.

Not so sure on cuts…The one word to describe this report to me was:

BROAD

Every category positive mom… Looking at the BLS CPI summary… Eyes on energy in addition to food and cars.

I think we’ll see cuts but it’ll be because of the job market not inflation or maybe no cuts at all if jobs starts strong….IF

Just to be clear, I am very much opposed to rate cuts at this juncture and I think that QT is going at much too slow a pace. They shouldn’t just be running off the MBS, but outright sales. I made that prior comment in a sad disgust of how the current FOMC board is making disastrous decision after disastrous decision just to bail out the banks and billionaires at the expense of the rest of us.

FI was oversold in the short term and due for a bounce. Note however that the curve didn’t flatten in the rally. If anything it steepened slightly. If traders and portfolio managers thought the PPI and CPI prints reflected declining inflation 30 years would lift off like a scalded cat. They didn’t. Everyone expects Powell to cut by 25 regardless of inflation because the banks have a carry trade unwind funding problem. Japan likely to increase rates by 25 bps at 10 pm on the 23rd. That represents a doubling of front end rates there. Kind of explains why Germany ,UK, Austria, France and US yields all taking off in the last 60-90 days. Add to that the obvious fact that the Fed seems to want inflation up around 3-4% you have a yield curve that has at least another 100 bps of steepening to run. If the Fed didn’t want inflation to be stubbornly high he would be cutting money supply not growing it. Still have to wonder why anyone would want to hold anything anywhere longer than 2 years given the above rant. At 4 percent inflation you lose half your principle in 17 years so what yield do you need for that?

I agree, hence many actual investors (not speculator/gamblers) are switching their mentality from one of return ON capital to one of a return OF capital.

Lot’s of promises for this new CONgress and president to keep…

Hedge accordingly.

The corporate and financial media sure came to a completely different conclusion regarding the inflation report. Not only that, but a bunch of huge accounts ran US equities through the roof today.

With that said, Wolf has it right and they are wrong.

Wall Street and Main Street are completely disconnected. While it has always been this way, the level of disconnect can vary, and I’d say we are in uncharted territory. I appreciate the unbiased data here as it helps me position my portfolio and tease out what the real costs/risks are. I am amazed by how long this disconnect has continued. Personally I see the world governments continuing to move away from constitutional governance as hyperinflation eventually sets in. Interesting times.

the markets are at this point just rich people trading stocks and bonds back and forth with each other. that’s really all it is at the core.

in terms of constitutional governance, i agree. the rule of law is a great sound bite, but it ultimately assumes some general level of prosperity. once you get an economic decline, the rule of law indubitably follows.

In five days the blizzard of executive orders starts, and some of them are likely to be tariffs, so whatever inflation looks like right now is, I think, soon to be last year’s news.

Read this, especially the 10 “Basics” of tariffs. You need it.

https://wolfstreet.com/2025/01/13/some-basics-about-u-s-tariffs-and-what-trumps-new-economic-team-said-about-tariffs/

Wolf has showed us accurate picture for CPI.

As usual MSM twisted the articles and headlines. But they are NOT alone.

Today FED Governor Waller called latest CPI report “very good” on CNBC interview. Come on. Not once but twice in same interview. Calling latest CPI report Good Report is pure Stupidity and being irresponsible.

Then he goes on to say IF and BIG IF if we continue to get this kind of reports, there will be cuts in even in first half of 2025.

I can understand IF part disclaimer. He can say anything with IF disclaimer. But then calling higher inflation read as Good or Acceptable reading makes that IF very subjective/low bar. He said even March rate cut is not off the table. Even give hints for 3-4 cuts this year. What a shame..

It’s odd how LT rates didn’t spike over 5% when CPI was sitting at 8-9% just a few years ago.

Now, let’s see what happens when corporations face a $1-2 trillion wave of rollover refinance debt.

And remember, inflation is a lagging indicator.