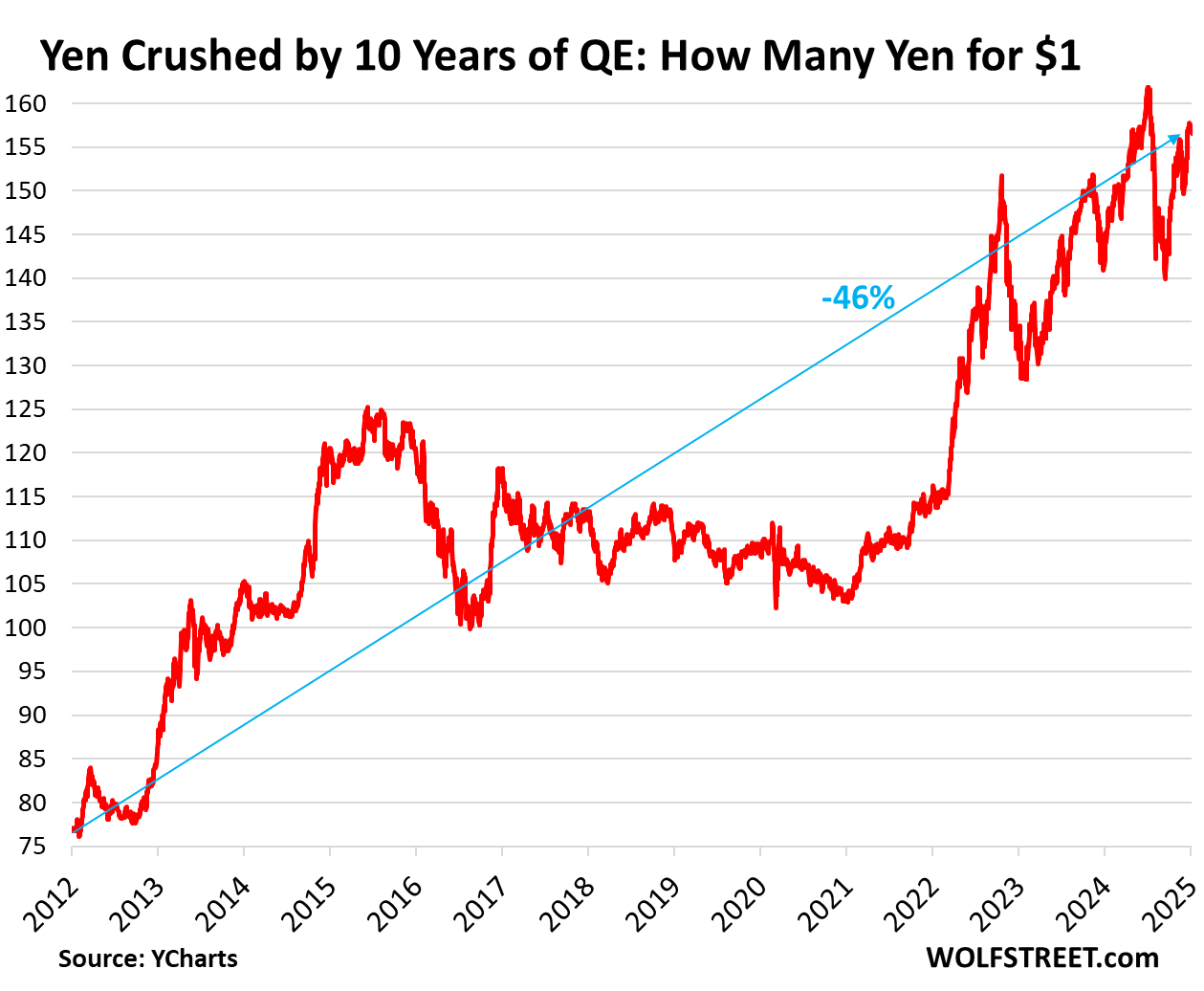

Too little too late to help the yen that got mauled by 10 years of rampant QE.

By Wolf Richter for WOLF STREET.

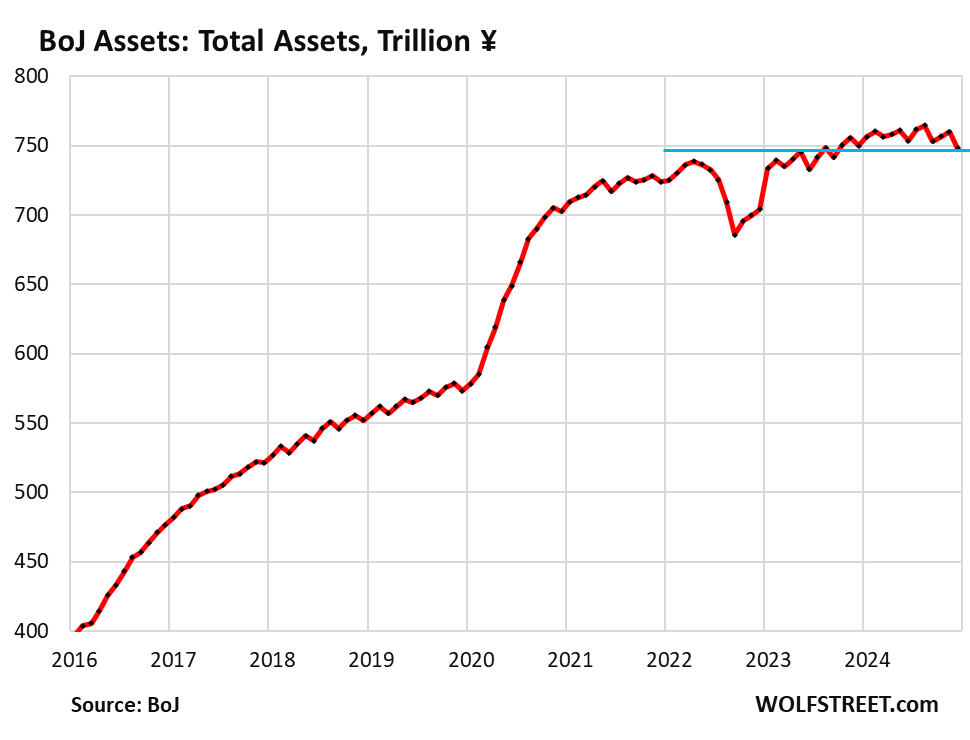

The Bank of Japan had announced at its meeting on July 31, 2024, that it would start QT, and it’s showing up on the balance sheet. It started shedding its holdings of corporate bonds and commercial paper in mid-2022, and a big portion is now gone. Its huge government bond holdings peaked in February 2024, and have zigzagged lower ever since. It also has a loan portfolio, and those loans had risen, which had caused its overall assets to inch up through August 2024, despite the decline in its bond holdings. But for the past five months, even the loans have been declining, and the overall balance sheet has been shrinking.

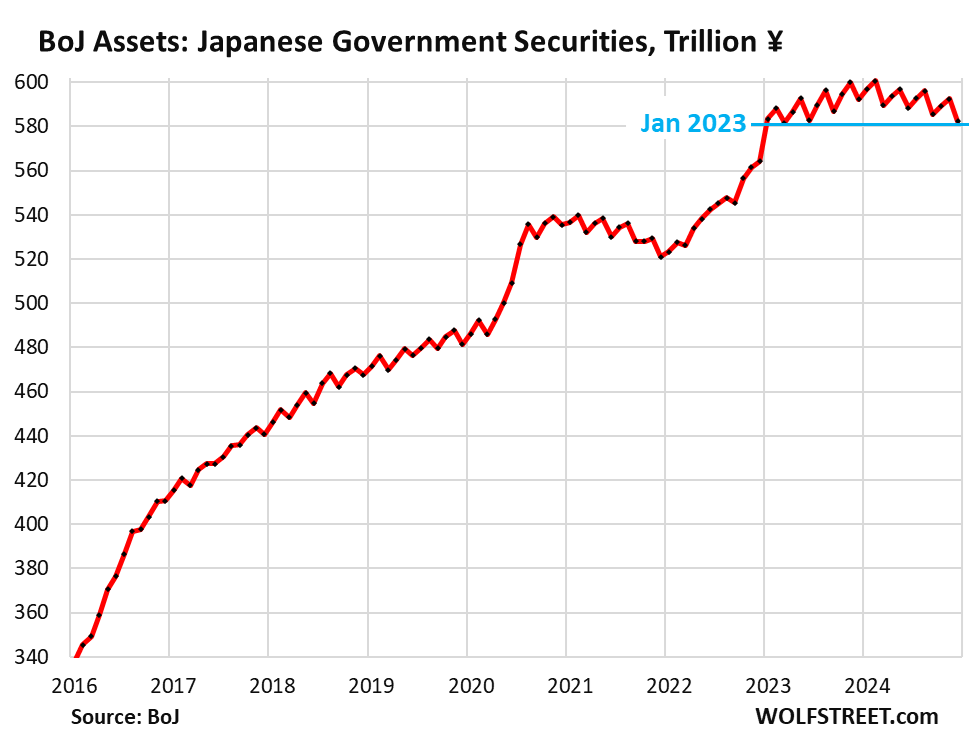

Japanese government securities: -¥18 trillion (-$114 billion), or -3.1%, from the peak in February 2024, to ¥582 trillion ($3.68 trillion) on the balance sheet at the end of December, released today. They’re now below where they’d first been in January 2023.

They account for 78% of total assets and have been zigzagging lower since their peak in February 2024. The BOJ’s JGB holdings run on a three-month cycle: One month, a pile of long-term bonds mature and come off the balance sheet, then over the next two months, as the BOJ purchases replacement bonds, its holdings rise in smaller increments.

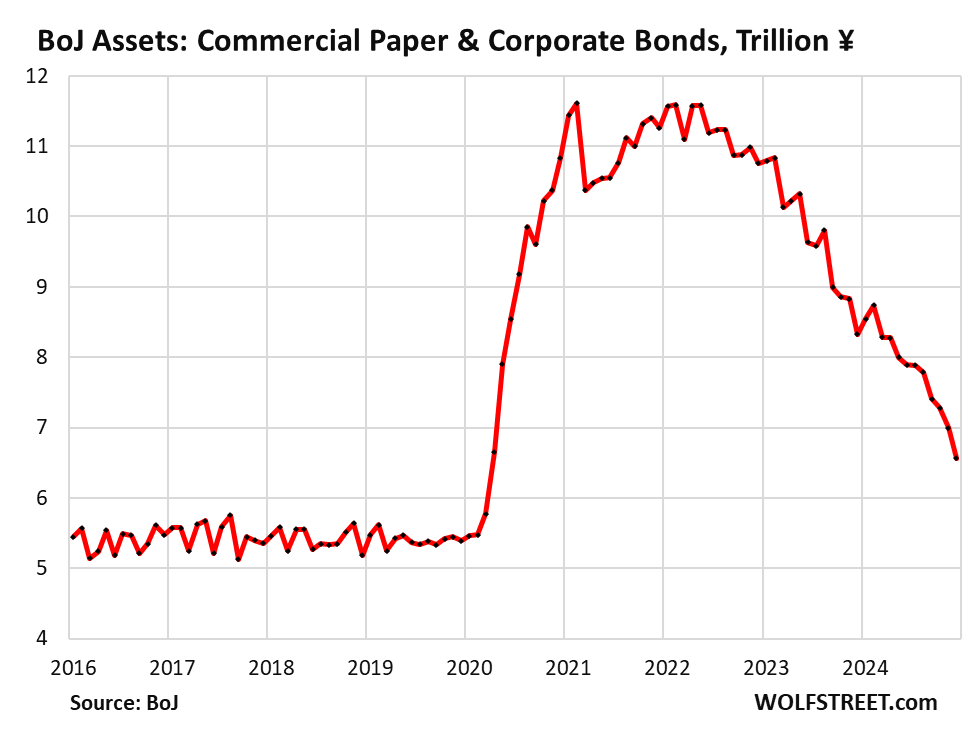

Commercial paper and corporate bonds: -¥5.0 trillion from the peak in May 2022, to ¥6.6 trillion ($42 billion). The BOJ stopped buying commercial paper and corporate bonds in early 2022. And its holdings have been running off the balance sheet as they mature. They now account for less than 1% of the total.

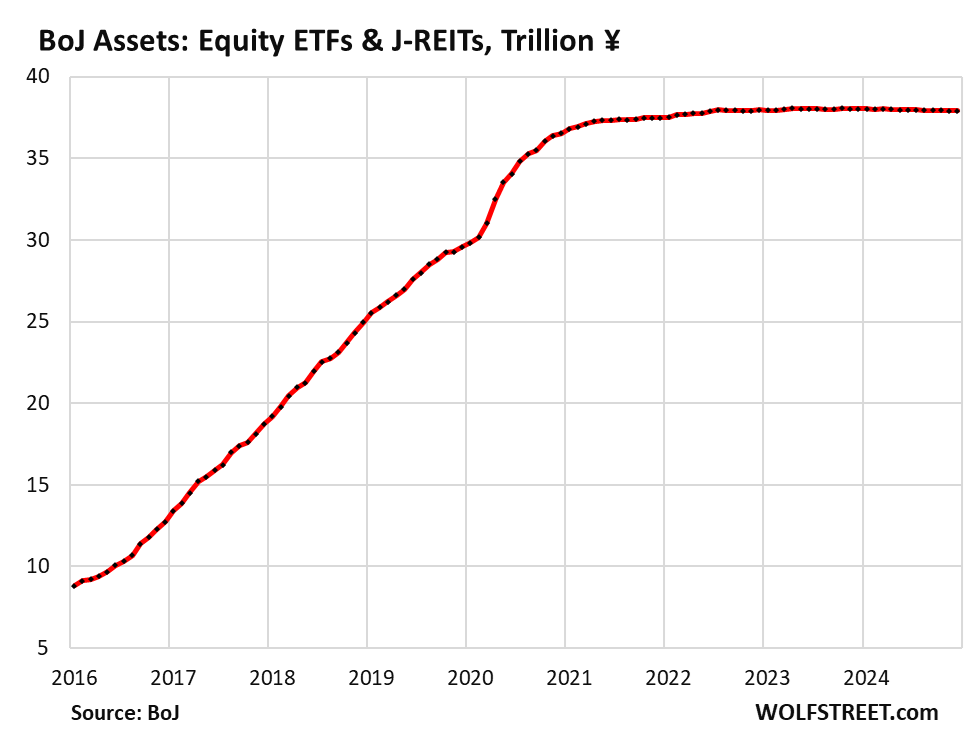

Equity ETFs and Japanese REITs: The BOJ stopped buying equity ETFs and J-REITs in 2021, when they’d reached about ¥38 trillion ($240 billion), and have remained essentially unchanged since then.

The BOJ carries them at cost, not at market value. It would have to sell them outright to get rid of them because they don’t mature and come off the balance sheet automatically, like bonds do. And it obviously has no appetite for hammering the Japanese stock market by telling everyone that it’s selling its ETFs and REITs.

During QE, the US financial media hyped those ETF purchases as if they were a huge deal, though they were always just a small part of its assets, currently 5% of the total.

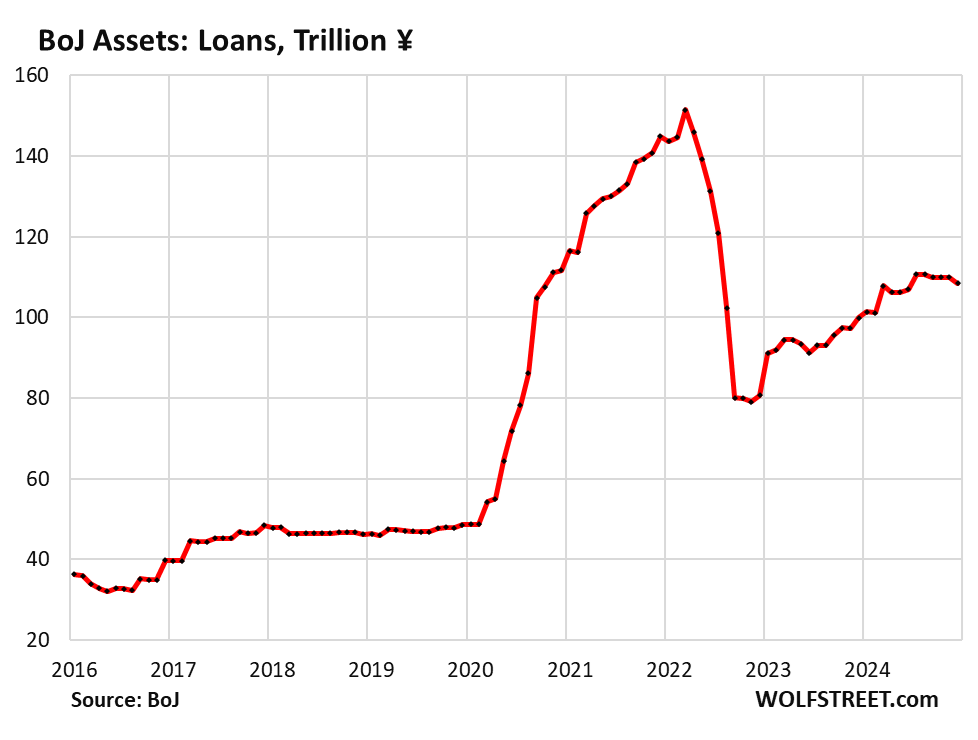

Loans: ¥109 trillion ($690 billion), lowest since June. They account for 14% of total assets. The BOJ handed out loans to banks and other entities under several programs, including the massive pandemic-era loans, a big part of which has been unwound. The total amount of loans outstanding had more than tripled from ¥49 trillion in February 2020 to ¥152 trillion at the peak in March 2022:

Total assets: -¥17 trillion (-$108 billion) from the peak, to ¥748 trillion ($4.73 trillion), the lowest since September 2023.

In addition to the QE-related assets above, they include gold, coins held for circulation, and foreign currency.

The yen paid the price for QE in 2012-2022.

The BOJ’s grand money-printing era started in 2012 under the doctrine of Abenomics and lasted into 2024. During this period, the yen plunged by 46% against the USD, from 85 YEN to the USD in 2012, to 157 now. The exchange rate is where the free money came home to roost.

The minuscule QT so far and the hair-thin rate hikes so far have not changed the equation for the yen. Japan’s annual CPI inflation was back to 2.9% in November, the highest since August, and the second highest since October 2023.

Due to persistent trade deficits, the crushed yen is not good for Japan.

Japan has run annual trade deficits every year since 2010 except in 2016 and 2017. In other words, it has imported more than exported. And the crushed yen has made these imports more expensive, has widened the trade deficit, and has added to inflation.

In addition, all major Japanese manufacturers have offshored a portion of their production. For example, most of the Japanese vehicles Americans can buy are made in North America, and many components are made in North America, China, Thailand, and other countries, and a weak yen doesn’t make them more competitive. The weak yen only helps when Japanese companies translate their foreign revenues and earnings into yen for their yen-denominated financial statements. But that’s only a paper benefit.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Another interesting post…

Is a portion of the “Equity ETF” positioned in US ETFs, and if so, could it pose any significant threat to US equity markets — or is the current liquidation value relatively insignificant?

Thanks

Wolf can correct me, but I suspect that the dumping of Japanese-owned ETFs or equities would have a negligible impact. The dumping of Japanese-owned US debt might be more impactful, but still not a threat.

John H.,

No, these ETFs that the BOJ bought are tracking Japanese stocks only. Same with its J-REITs, they strictly hold Japanese real estate.

WB,

It’s hard to say what impact selling the ETFs and J-REITs would have. The Japanese stock market is small compared to the US stock market. ETFs and J-REITs are a small portion of that. The BOJ holds $240 billion of them valued at cost. But it bought those many years ago and stopped buying in 2021. Japanese stocks have surged 370% over those years. So its pile of ETFs might be trading at around $700 billion now, just guessing. And selling those, just announcing that it would sell them, will have some impact. If it sells them at all, it would likely announce well in advance that it would trickle them out at such an unnoticeably minuscule pace that it would take forever to get rid of them. The BOJ is in no mood to dent Japanese stocks.

Thanks Wolf. I presume that Japan is still the largest foreign holder of U.S. government debt, but even then it is just over one trillion, so pretty minor.

my heloc just went up 25 basis points to 8.25%

didn’t prime drop??

joedidee

How did this end up here?

Longer-term US yields have been rising, and US mortgage rates have been rising. Not sure how banks price HELOCs, but it would make sense that their rates would rise as well.

Arigatou gozaimasu Richter san! :)

The plan is to slowly increase the run off, right?

Correct. And we should see it accelerate this year.

At the July meeting, it said that it would start running off its holdings of JGBs at a rate that increases every quarter, until the monthly runoff reaches its full speed of about ¥3 trillion per month ($19 billion per month at today’s exchange rate) in January-March 2026. And it would then continue at that pace.

https://wolfstreet.com/2024/07/31/bank-of-japan-hikes-by-25-basis-points-and-starts-qt-too-little-too-late-but-in-right-direction-to-put-a-floor-under-plunging-yen/

I have to admit ignorance that Japan has had a trade deficit for that long. If they still had a surplus they could devalue the Yen to 200 and it wouldn’t matter as “hard currency” continued to pour in. I’m assuming the majority of Japan’s imports are energy and food?

With a shrinking population and an increasing national debt, at some point it seems like “the last Japanese person will own the whole island”. Seriously though, since they mostly own their own debt and owe it to themselves, couldn’t the BOJ just one day forgive the loans, tank the Yen to nothingness, then balance imports/exports and start over? Sixty or seventy million (and falling) Japanese citizens using the New Yen and exporting just enough high value manufactured goods to keep it stable?

1. “couldn’t the BOJ just one day forgive the loans, tank the Yen to nothingness”

You’re forgetting about the people who live there. They’re already quietly furious about having been impoverished by the collapsed yen when it comes to foreign travel and imports. Japanese people used to be big foreign travelers. They’d go on short trips overseas and blow a lot of money. Traveling overseas has gotten to be 50% more expensive for them just based on the yen, on top of the higher prices due to inflation in the destination countries. Buying imports – purses, beef, clothing, appliances, energy products, raw materials, etc. — has gotten a lot more expensive, even though the government subsidized energy products at the wholesale level to lessen the impact on consumers and businesses.

A currency is nothing to be trifled with.

2. “Sixty or seventy million (and falling) Japanese citizens using the New Yen…”

You should at least get your facts right. The population of Japan is twice that, 124.5 million, it’s declining, but not that fast, at a rate of about 460,000 per year currently. At this rate, it would take 20 years to bring the population down to 115 million. Projections are all over the place. But Japan’s urban areas are incredibly crowded with small living spaces and long arduous commutes. So as space opens up, housing gets bigger and more comfortable for families, and commutes get shorter, people’s behavior will change in response. That’s why projections about human beings are always wrong because humans react to changing conditions.

when i was in my 20s, i worked an internship at a large casino and hotel in las vegas. the amount of money rich japanese men dropped at the card tables literally shocked me.

i wonder whether those people are gone from the las vegas casinos with the much weaker yen.

It’s a big turnaround. Japanese used to flock to Hawaii and were known as the biggest spenders because their currency was so strong.

There was an anecdote from the late 80s about a Japanese woman being driven around Honolulu to view a dozen high-end houses, not saying much until she announced, “That’s enough. I’ll take them.”

Today, Japan is overcrowded with foreign visitors as a cheap travel destination. Japanese are adept at keeping their feelings to themselves but I imagine it feels like a national humiliation.

Ok, my population drop was exaggerated, but I’ve seen projections of ~80M by 2100. Japan seems to be a very closed society with most property and financial assets held internally, so they do seem most likely to at some point forgive themselves and start over. I’ll need to look into how much debt in Japan is issued in US dollars or other currencies.

Wolf – good points from a permanent resident of Japan. I’m not saying it won’t be painful but if Japan deleverages and population comes down to 115M or the “experts” citing 70M in 30-40 years, will be better for Japan in the long run..more sustainable. Just wondering if I should relocate to Japan (as I’m in the U.S now) or wait.

If you buy a home in Japan now with your US-earned dollars, you may be getting the deal of a lifetime, since the yen has collapsed. Japan has become shockingly cheap for USians.

MW: 30-year Treasury yield inches closer to 5% after November quits rate declines

ShortTLT must be having a fiesta.

TLT is down over 15% from its September 16, 2024 high of $101.64. Current price: $85.91.

This fellow bear is happy for ShortTLT. Cheers.

So your dumass is shorting bonds at all time high interest rates in last 205 years? Good luck.

All time high? LOL! Fucking kids. The 70’s/80’s weren’t that long ago.

Current interest rates on government debt are no where near a long term high. We are closer to a long term average for flagship benchmarks like the 10 or 30 year Treasury.

DarthTrader, I assume that you had a typo, and meant all time high in the last 25 years. Not 205 years. Is my assumption correct?

If you meant 25 years, then yes, interest rates are at a high between 25 years ago and present. But as others have commented, interest rates are no where near an all time high in the USA.

I’m not shorting bonds. I was complimenting the sagacity of another frequent commenter, ShortTLT. Rates on long term bonds have increased over the last year. So in this way, shorting TLT long would’ve been a prudent short position.

I’ll let your ad hominem slide because idgaf.

MC Bear,

You’re too kind. Even in the last 25 years DarthTrader is wrong. Rates on 10 yr and 30 yr bonds were often higher than the current cycle peaks between 2000 and 2007. Even if it was a typo, Darthtrader is still clueless unless the typo included both the 2 and the 0. Five years would be accurate.

Most sources I’ve read and heard (in English and Japanese) lead me to believe the falling exchange rate is mostly a result of the delta between Fed and BOJ rates and the carry reading that results. The Fed is staying higher for longer, and the BOJ wants to raise its rates but, in true Japanese prudent fashion, is taking its sweet, sweet time, and even then will only get up to 1% or so anyway. After 3 decades they actually want inflation.

Your data is interesting as a different take. I think you’re being a little selective with your starting point on that 46% drop, although your point still stands. Extend the graph a few more years and it goes back within its normal range of 100-110 JPY/USD. It actually got down below 80 at one point, maybe 78. You’re also right that near 160 is not helping anyone and could kill the economy if it gets much higher.

In your mind, what do you think it takes to see the exchange rate get back down to at least semi-normal, say below 130, and what do you think is most likely to happen over what period? Is it all in the hands of the BOJ or will it be more driven by the Fed?

I don’t see Japanese interest rates ever getting up in the US ranges of 5% or higher. The average Tanaka is already scared of what 1% will mean for personal loan rates. I don’t know how much affect QT has or how quickly they’ll unwind, other than to note they’re overly cautious.

The semi-normal exchange rate since at least the early 1990s was about 100 to 110, with 120 being the old upper limit when authorities started taking action. In increments, this upper limit has been moved to 160 now before authorities start to take action. And it might be moved up further at the next test.

The yen started sagging in 2012 with Abenomics. At the time, there was very little rate differential between the BOJ and the Fed. When the rate differential became a thing in 2022, the yen had already weakened dramatically, as you can see in the yen chart.

I chose 2012 as starting point because that’s when Abenomics started, which was based on money-printing and deficit spending, and we have warned about the effects of Abenomics from the beginning. You cannot get away with that forever, not even Japan, which has put the JGB market into a vice, but which cannot control the global currency markets. And that’s what we’ve seen since 2012.

Last time I was in Japan, on the way back from VN, the rate was 305 yen/USD.

Did not follow the obviously great delta to 85, but now see the clear possibility ,if Japan does not get it right, that we will see vastly increasing ratio again.

However, and it’s definitely a big IF,,, If the inflation/degradation of USD continues apace, the very opposite may and likely will proceed, as the charts above indicate so clearly….

Inflation Inflation Inflation may very well become the New location location location for ALL, and not just the RE folx.

Delineating the era at Abenomics makes sense, but for context readers should know that was an unheard of low at the time and a direct result of the GFC fallout in 2008-9. It first dropped into the 90s in 2008 from the normal 100-110 range. I was in Tokyo at the time: 2011 felt as low as today feels high.

I don’t normally follow the Japanese balance sheet though, so that input from someone who tracks it is valuable. Indeed, I started hearing about carry trading being a thing about 2022. I’m guessing it’s unlikely to wind down until the rate differential lessens, so the combined policy of the Fed and BOJ. That could take a while, maybe 2026 or later. Traders are having a field day at the expense of the public right now, but it’ll all come crashing back at some point. It always does… until it doesn’t.

I see yen weakness as forex differentials as well, however, Japanese saving rate is still high around 30% (compared to UK at 10%) so I personally doubt that average Tanaka concerns themselves about the risks of higher inflation although certainly they are there. Probably more likely to be chortling by Mrs.Watanabe.

If you go there, and I am about to relocate back to Japan coincidentally, something is very very wrong about a weak yen. Infrastructure is top notch, government debt when netted against liabilities is really only at a high western level, government state pensions are stingy, people work in retirement, they aren’t crippled by high housing costs (quite the opposite), they have more rail/road per citizen than e.g. the UK, and the high food costs they could fix by abandoning the protectionism of domestic production (i.e. don’t have all your farm units consisting of one 85 year old with 2 acres and a sickle).

I look at the difference gbp and yen, and the difference is that you have to be paid to hold gbp because of risk, and the cost of that is a heavy burden on the UK, whereas you don’t get any sweets for holding yen, the whole population is trying to do so.

Put it like this, in Japan, the UK’s minimum wage gives you a flat and a good lifestyle, you can visit restaurants etc so there is this HUGE imbalance somehow stuck there and whats weird is the weak yen. Even BigMac index they are half-priced.

btw an excellent summary of all the data Wolf great.

At these prices Japan can’t afford oil and that’s all that matters. The BoJ is too stupid to realize that by NOT raising rates they have ended up causing the very thing they feared.

Japan spent its borrowed money on infrastructure and useful stuff, while the US (and UK) (over)spent it on defense and all kinds of garbage pork.

There are also the infamous bridges to nowhere, totally underused Shinkansen lines, big subsidies for farmers, subsidies for energy… pork-barrel spending is ingrained in Japan, just like it is in the US. Their defense budget as a percent of GDP (1.4%) is smaller than that the US, but it’s not nothing.

Agreed on your last point- very glad to see Wolf’s summary.

The Tanakas are feeling that inflation especially with everyday imports like cheese and meat. Keep in mind that they haven’t experienced inflation in more than a generation at this point, so mental impact on the ground is outsized. No one 35 or under has ever seen this.

In the end they’ll survive, largely because of the savings rates you reference. Like Brits, the Japanese are used to rainy days- they get just about every disaster under the rising sun.

“Put it like this, in Japan, the UK’s minimum wage gives you a flat and a good lifestyle, you can visit restaurants etc so there is this HUGE imbalance somehow stuck there and whats weird is the weak yen. Even BigMac index they are half-priced.”

Perhaps the exchange rate is more determined by global investment prospects as opposed to local consumer spending. With wealth concentration at all-time highs, savings are very high and global investors are looking for highest return. Japan looks weak from an investment standpoint. With low or negative population growth, a lot of investment potential is removed relative to other countries. A lot of that problem is undoubtedly priced in now.

Bolhuis has an interesting paper on “Fiscal R-star” (the real interest rate required to stabilize debt levels when the primary balance is set exogenously) and the tensions that can happen when there is a large gap between Fiscal and Monetary R-star. It seemed like Japan would be an example of a country where monetary policy has become less independent because the country would have trouble if higher interest rates are applied to government debt. Do you think this is an issue that might be slowing the BoJ from raising rates? https://www.imf.org/en/Publications/WP/Issues/2024/08/09/Fiscal-R-Star-Fiscal-Monetary-Tensions-and-Implications-for-Policy-552877

Let me put it another way, the UK recently has basically redefined the minimum wage. OK to do in a fiat currency. They redefined the arbitrary cash number for base pay. This is not from demand for labour or productivity, its just by edict.

Except this would mean the currency is worth less, because the value of labour didn’t increase. So in an attempt to square the circle interest rates have been forced to go up i.e. the error is compounded because its gone up in real terms twice.

So now there is a situation where the minimum wage in the UK is above in many cases mid-career skilled Japanese jobs.

So. Going wrong is relative. So when I say something is wrong with the yen, its comparative. I could also say something is seriously wrong with the UK pound and now I re-arrange my perspective, its easier to see Japan as normal but the UK momentarily suspended in the air with mandatory minimum relative pay levels that exceed the underlying production of the worker.

In the end its the same thing though, the yen is hugely undervalued, the pound is hugely overvalued and to come back to the point, its OBVIOUSLY so if you were to go there and look at prices. Is this the case for the USA, I imagine to some lesser extent but I don’t know. There is the same dynamic, you have a federal minimum wage and a high base rate.

Japanese wages are weird… minimum wage just increased to a whopping 1050 yen. That’s $6.63/hr, or £5.37. Can you live on that? Sure, but you’re not saving 30%, or probably anything.

In terms of career wages, there’s a big middle class and not too much to either side of it. Most office jobs make close to median salary; it’s really hard to break out and make the equivalent of a six-figure salary outside a handful of professions.

On both the JPY and GBP, I feel like it’s at the whim of the Fed. Policymakers worldwide tune into Fed meetings and make their adjustments accordingly. The US has inflation, and as the leading global currency they’re sharing it with everyone.

Thanks for sharing…I estimate 1 percent of the American public would understand your article…how do I know this…because I’m a product of public schools, public college, born to commonors….I learned this on my own after 9,11,01, housing debacle, corona, bridge collapse and learning all sports on tv are scripted nonsense….Henry Ford was wrong about his revolution theory on the monetary system and americans….