Housing Bust 2 reverses part of the “Housing Crisis” when people with good incomes could no longer afford to live in the City.

By Wolf Richter for WOLF STREET.

The big decline in tech employment in San Francisco and the northern part of Silicon Valley that we’ll get to in a moment has put its stamp on home prices in the city of San Francisco.

Unsustainable home-price spikes are, well, unsustainable.

Single-family house prices: -15.4% from the peak. In the city of San Francisco, prices of mid-tier single-family houses in November have dropped by 15.4% from the peak in May 2022, to $1.39 million, seasonally adjusted, and are back where they’d first been in 2019. October and November were down a tad from the prior three months.

“Mid-tier” to reduce the effects of shifts in the mix; “seasonally adjusted” to reduce the effects of seasonality; and “smoothed” (three-month average) to reduce monthly zigzags, as per data from the Zillow Home Value Index (ZHVI).

Slowly undoing the “Housing Crisis.” In the decade from 2012 to May 2022, ZHVI for single-family houses had spiked by 160%, triggering what was locally called the “Housing Crisis,” where middleclass employees with good incomes could no longer afford to live in the City.

Since May 2022, prices have now reversed about 25% (-$253,000) of the 10-year price spike (+$1.013 million), thereby beginning to alleviate the “Housing Crisis” that has caused so much damage to the City’s economic fabric.

This spike in house prices from 2012 to 2022 made San Francisco too expensive, forced employers in the City to pay huge salaries, driving up their primary costs, which pushed many of them to places where housing costs and wages were a lot lower.

And the City lost people, and it lost jobs, especially jobs in tech and finance. And home prices began to careen down, but it’s a slow bumpy process.

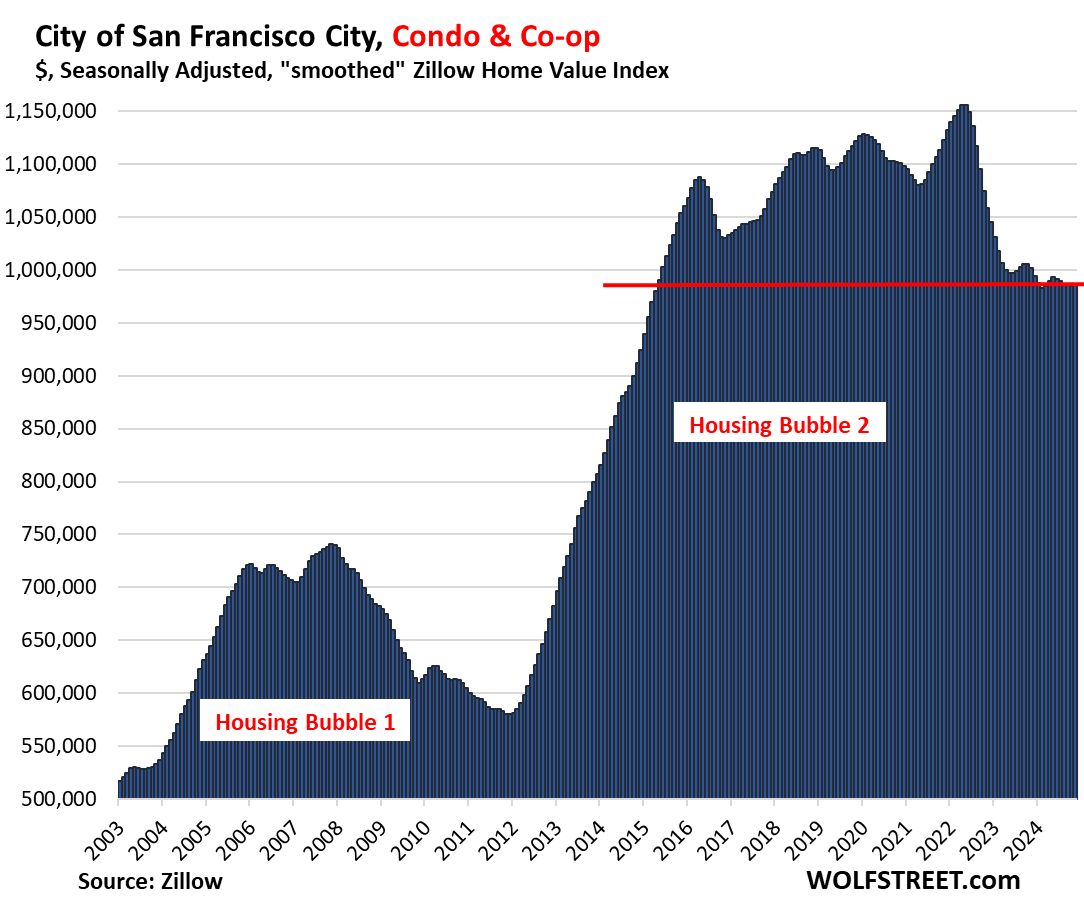

Condo & co-op prices: -14.7% from the peak. Condos and Co-ops account for about half of the home sales in San Francisco. Nearly all new construction over the past two decades has been multifamily (condo and rentals), and there is a lot of new condo supply coming on the market in central locations.

In the city of San Francisco, prices of mid-tier condos, seasonally adjusted and as three-month average, have dropped by 14.7% from the peak in May 2022, to $986,000, and are back where they’d first been in 2015.

From the beginning of 2012 through May 2022, over those 10 years, condo prices doubled. But since May 2022, prices have now reversed about 30% (-$170,000) of the 10-year price spike (+$576,000), thereby beginning to alleviate the Housing Crisis.

Jobs in San Francisco & Northern Part of Silicon Valley.

San Francisco and the northern part of Silicon Valley – the counties of San Francisco and San Mateo which make up the San Francisco-Redwood City-South San Francisco Metropolitan Division – have been among the epicenters of tech jobs in the US, and the epicenter of tech job booms and busts.

We’re going to look at payroll jobs from the Establishment Survey by the Bureau of Labor Statistics. The metro-level data was released on December 20. These jobs are tracked by business location to which the employee is assigned, regardless of where the employee lives. If a worker commutes from the East Bay to an office in San Francisco, it counts as a job in this Metropolitan Division. Same with remote employees.

Jobs in tech and social media are largely in two industries: “Information” and “Professional, Scientific, and Technical Services.”

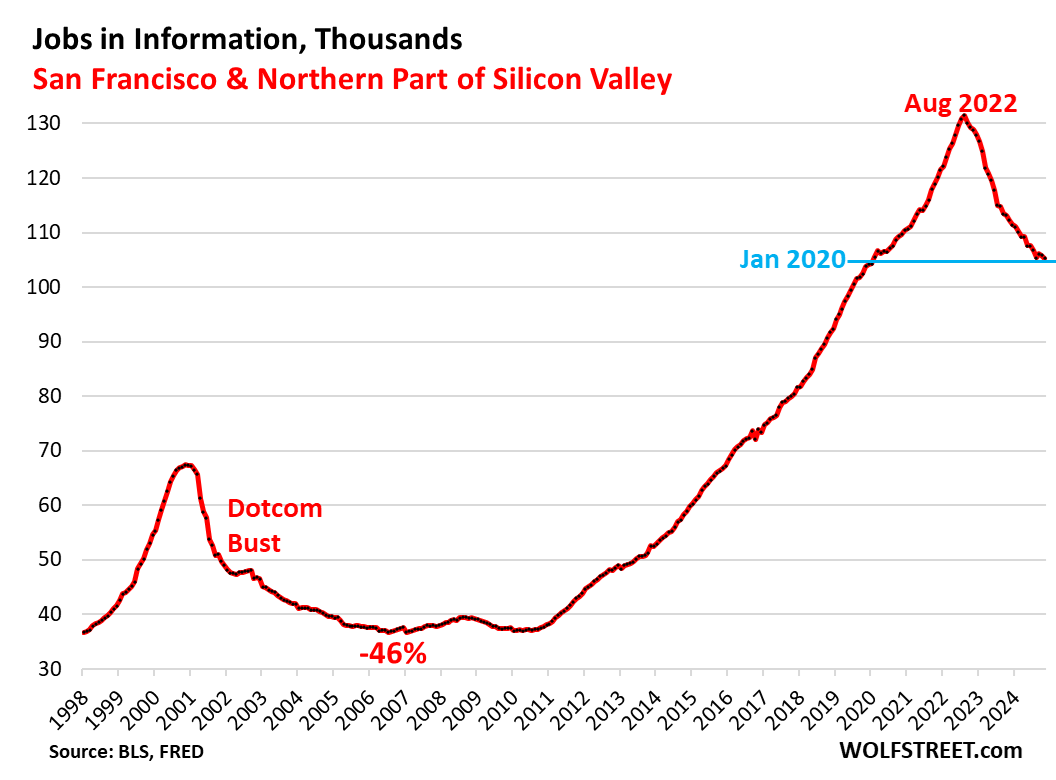

Information: Over the past four months through November, payrolls in this industry roughly remained unchanged at 105,300, the lowest level since January 2020, down by 20%, or by 26,200 employees, from the peak in August 2022.

The drop has now undone the entire hiring boom that occurred during the pandemic – a hiring boom that occurred even as other industries (Leisure & Hospitality, Retail, Healthcare, etc.) were gutted by massive layoffs.

During the Dotcom Bust, the Information industry in the metropolitan division lost 46% of its jobs, beginning in late 2000 and hitting a low in mid-2006, and then it remained low for another four years, before taking off again.

The industry accounted for 9.1% of total payrolls in this metropolitan division in November. In overall US payrolls, jobs in Information account for only about 2% of overall employment.

Jobs in Information are at facilities where people primarily work on web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

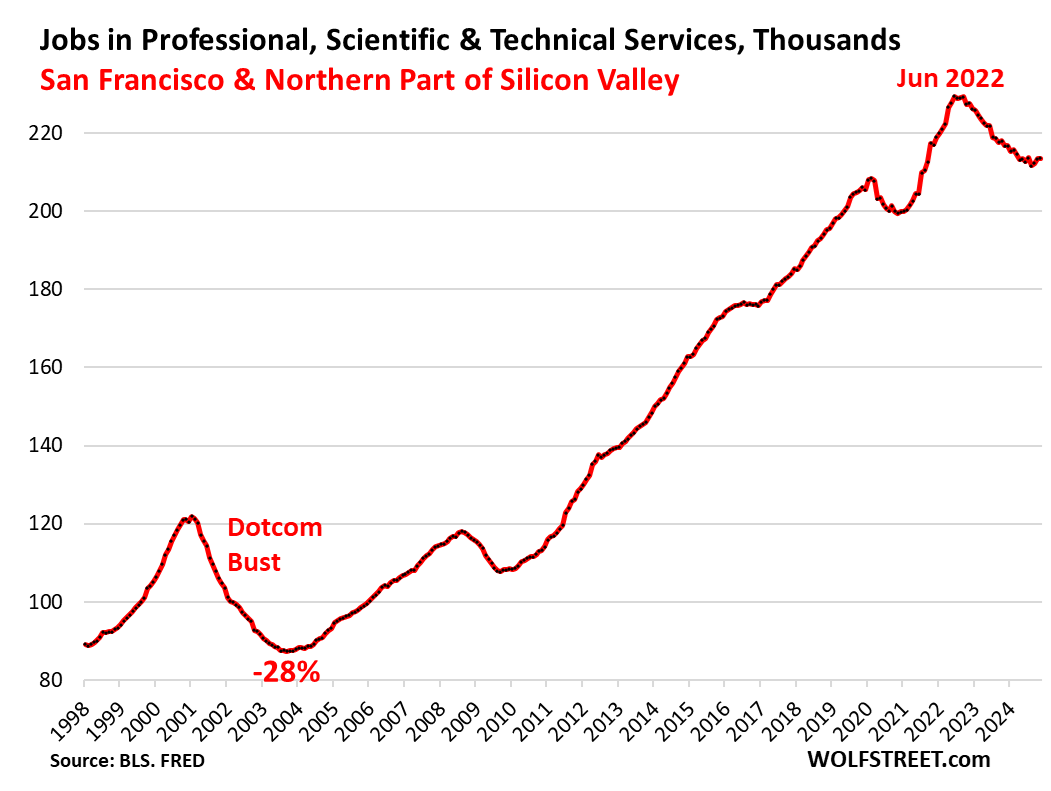

Professional, Scientific, and Technical Services: Employment has remained roughly unchanged since April, maybe a sign it bottomed out. At about 213,500 employees in November, payrolls have dropped by 7% from the peak in June 2022.

This big broad industry accounted for 18.4% of total employment in the two-county area. It includes many sectors outside tech and social media: Legal advice and representation; accounting, bookkeeping, and payroll services; architectural, engineering, and specialized design services; computer services; consulting services; research services; advertising services; photographic services; translation and interpretation services; veterinary services; and other professional, scientific, and technical services.

During the Dotcom Bust, the industry lost 28% of its jobs in the metropolitan division until it bottomed out in late-2003. But given how much broader the sector is, it didn’t drop nearly as much as Information, and recovered much faster.

Combined, Information and Professional, Scientific, and Technical Services shed 42,100 payroll jobs since the peak in mid-2022.

The AI-related hiring boom – though the number of AI jobs is relatively small – has had a strange and mixed effect, with many companies announcing layoffs out of one side of their mouth, and AI-related hiring plans out of the other side of their mouth. And maybe it has now caused tech jobs in the area to stabilize.

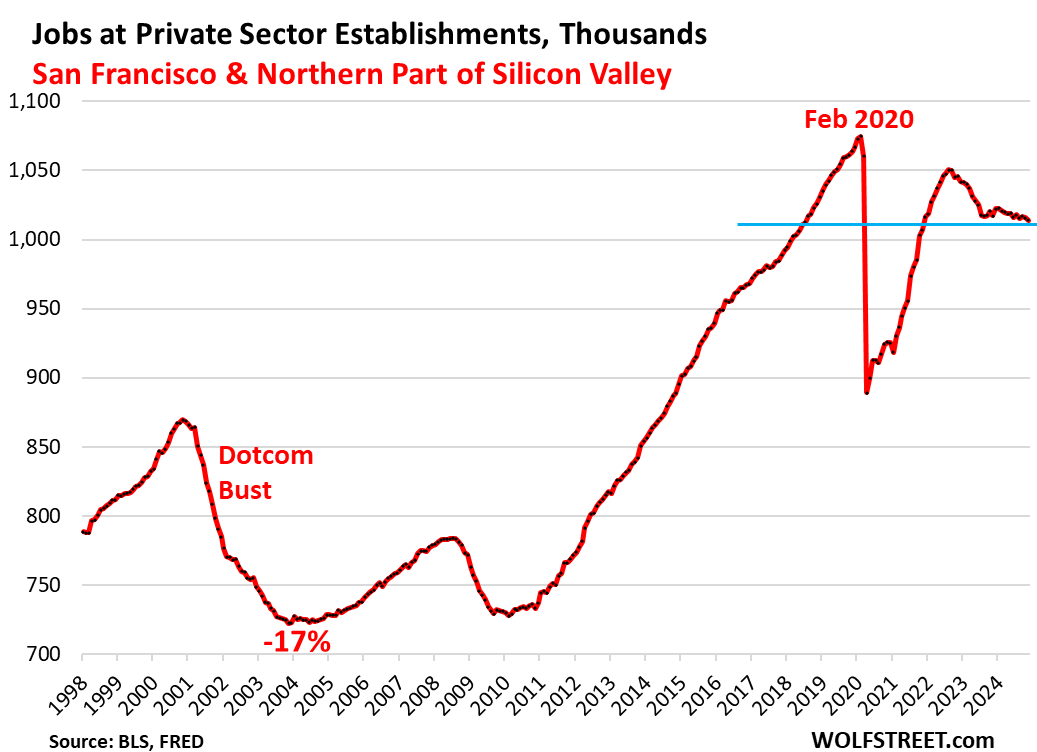

Total private-sector payrolls have dropped to 1.014 million jobs, first seen in mid-2018. Since mid-2022, they’ve dropped by 3.5%, or by 36,500 jobs. Since the peak in February 2020, they’ve dropped by 5.7%, or by 60,900 jobs.

The plunge in payrolls during the pandemic was driven by Leisure & Hospitality, Retail, Healthcare, and some other industries that have now largely recovered.

During the Dotcom Bust, the two-county area lost 17% of its private-sector payroll jobs, a depression-type decline, compared to which the current decline is relatively moderate:

Employment at nonbank mortgage lenders nationwide collapsed by 37% this time around, to the lowest level since 1997. Read… Housing Bubble & Bust #1 and #2 as Seen through Employment in Mortgage Lending

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Leverage works both ways…

We haven’t seen anything yet!

Is there any way to see if the falling price is resulting in foreclosure and default rates climbing?

Interest rates are the cause.

Cousin Richard,

LOL, what we have is a massive drop in private sector employment centered around tech. Look at the last three charts. That’s why I put them there.

If interest rates were the sole cause, we would have to see the same kind of price declines in all cities in the US, since rates are the same everywhere. But we’re not seeing it. We’re seeing big price declines only in some cities (Austin, I mean you!).

Cody,

In multifamily CRE in San Francisco, we have seen some massive defaults, including the $2 billion default by Veritas. Those defaulted loans were sold with big haircuts, and the buyers have taken possession of the rental buildings. But that’s CRE, and it’s in trouble everywhere.

In terms of homeowners, there hasn’t been a big wave of defaults and foreclosures. There are some, like always. We would have to see far bigger price drops before large numbers of mortgages get in trouble.

The chart looks like

Left shoulder ARMS,

Present ARMS,

Right shoulder ARMS

OK this is a stupid question but I’m kinda stupid: WHY are rates the same everywhere?

If prices, incomes, and lenders vary across markets in the US, why don’t the rates?

Dummy 4ever Renter

In the US market, mortgages are a national financial product, whose rates parallel roughly 10-year Treasury yields, and the spread between them — the percentage points that mortgage rates are higher — is a function of various things, including credit risks, costs and fees of all the middlemen, etc.

So not every individual borrower can get the same mortgage rate. A subprime borrower is going to have a higher rate than a super-prime borrower. That’s individual risk premium. But that’s the same everywhere, whether in California or Florida.

You can find out more here:

https://wolfstreet.com/2024/12/05/everybody-should-get-used-to-these-mortgage-rates-says-fannie-mae-ceo-mortgage-rates-10-year-treasury-yields-qt-and-spreads/

Dummy 4ever Renter: Not a stupid question and the reason rates are the same everywhere is because the Federalists ‘won’ in the 19th Century, and their centralist objectives have progressed and permeated the guiding culture ever since, defeating the original idea of a republic.

The original Federal government really didn’t have that much to do, and certainly not originally envisioned was micromanaging by laws and regulations every region of the nation.

Even when the Fed was created in 1913, and still today, there were 13 regional branches, but the interest rates today are decreed by central fiat; one size fits all, soviet style.

Money printing and inflation,are big reasons also foreigners buying

What is your evidence of that or are you just guessing?

Flea,

They’re the reasons for the price declines that brought house prices back to 2019 and condo prices back to 2015 levels? Interesting theory.

With property taxes on a 1.5 million $ home @.0125%. prop taxes alone causes $1,562 per month bill in addition to the mortgage and other normal expenses. The housing pyramid is falling in on itself.

Home prices surged in the past, due to foriegn investor money. They and the monopoly money kids over bidding are far and few.

Its time for some reality. I luckily own properties purchased in the 70’s thru 90’s. With very low prop taxes (thank you prop 13).

We need the younger generations to be able to afford housing/living life.

I welcome the price drop. Let it be a soft landing and not a crash.

Price adjustments are healthy and in this house market, desperatly required.

Re: “ strange and mixed effect, with many companies announcing layoffs out of one side of their mouth, and AI-related hiring plans out of the other side of their mouth”

That keen insight is probably a good model for the post-pandemic Schrödinger Cat, Simultaneity Model.

The delayed recession that didn’t fully unfold in late 2022, almost happened in October, but then AI suddenly appeared with ChatGPT — and there was an instantaneous shift in sentiment — that resulted in a spontaneous arms race, that ignited tech growth. The economy found stability,

Another example of super hyper sentiment shifting is the SVB banking collapse, with the instantaneous rollout of the Fed BTFP. More synthetic stability, created on the fly.

The point here is, massive economic swings with sudden sentiment shifts may become an embedded feature of economics, as technology acceleration intensifies — amplifying volatility, with both downward, then upward shocks.

The slow motion housing train wreck occurring now, was obviously preceded by a huge upward price shock, but that bubble dynamic had been offset by the nimble handiwork of new home builders, who took advantage of a mkt anomaly. Once again, a weak situation, flipped to prevent the housing mkt to collapse.

So — maybe problems find solutions faster now — but maybe, the solutions end up causing new problems, and we end up with a weird equilibrium between volatile faster cycles.

Nowadays I only look at Zillow to feed my self fulfilling prophecy of misery. All these homes here that are for sale for $700k-$800k sold for $300k-$400k 5-10 years ago. From reasonable to not. The slow passing of time waiting for a reversal that may never come has eroded my mental wellbeing, and excitement for life.

I hope San Fran is leading the way to something larger. I’m tired of working to pay someone else’s mortgage.

I guess your patience would be rewarded

If not then its not good for anyone and society in general

Also don’t forget to live your life

This present moment is the only thing you have as the next moment is not guaranteed

A house is a place to provide shelter .. whether you rent or you own .. nothing less nothing more

As a senior citizen I have listened to this patience my whole life and life is short. When Jerome Powell was buying up MBS to boost housing assets for the rich, they got their money right away. A little less patience and more political grassroots pressure in contacting elected officials might be helpful. Specifically, removing tariffs on building products and moving zoning from the local level to the state.

@Gary: I agree with you in the case of housing which is absolutely essential that people cannot defer this buying for any length of time.

I have watched the housing market since the early 90’s and almost all of the time there is a concerted effort to keep blowing the housing (and stock market) bubbles. Greenspan literally played around with the wealth effect to keep up the illusion of a prosperous economy till the whole thing blew up in 2000-2001. Bernanke and his successors have done the same thing since.

However, I don’t think that your solution of contacting elected officials and participating in grassroots pressure will work. It is not that the elected officials don’t know, they do know. However, Citizens United ensured that they will not do anything about it.

The common man is at the mercy of strong business constituencies that will not let the free market operate and/or the federal/state governments to go ahead with mega projects which will improve the life of the average citizen.

Here is a possible solution: Planning and building mass transit systems in bigger cities which will open up phenomenal housing opportunities. People can live in nice communities further away, yet still be able to commute quickly and efficiently.

Can this happen? Not very easily. Vested interests will spend tons of money to influence government officials and confuse the citizens that these projects would be a boondoggle. They will point to the high costs, but they will however not discuss any of the benefits.

The average citizen would be fooled by business propaganda into thinking that their tax dollars would be wasted instead of considering all the benefits of such a system.

There are several major issues with our current housing and transit – the time spent by commuters on the highways that take a huge toll on their health and well-being. Mass transit systems will save enormous commuting time, bring physical and mental health benefits, and result in lower housing costs. This will bring about enormous improvement in the quality of life of a huge percentage of American citizens.

But, as I said above, the vested interests will not allow this to happen. They have to drive up housing prices to stratospheric heights so that the banks can get enormous loan closing costs (and if they hold on to the loans, mortgage interest revenues), the real estate brokers can continue to rake in huge commissions, and cities can keep pushing up property taxes. Everyone except the common man benefits.

I am paraphrasing George Carlin who said: They want all your money and they will get it.

sean, you are right in many ways, but this is way too simplistic. citizens united or not, the wealthy will always have more influence. it’s the way it is. the common man can still rise above it, but he has to educate himself. i’m not seeing any evidence he’s interested in doing that.

about mass transit, i agree that in the united states it sucks. but building it is not enough. you need to make sure the public unions don’t see it as a multi year boondoggle with cost overruns that’ll end up making it cost 10x what is projected.

you also need to get crime under control. it doesn’t matter how good public transportation is in terms of speed if people don’t feel safe.

@Franz: You said:

“citizens united or not, the wealthy will always have more influence. it’s the way it is. the common man can still rise above it, but he has to educate himself. i’m not seeing any evidence he’s interested in doing that.”

I absolutely agree with your statement that the wealthy have more influence. Citizens United was a final nail in the coffin.

Your point on putting the onus cannot be put on the common man is difficult to achieve – because he/she is being asked to parse through enormous self-serving propaganda from business interests. The common man is “common” because he has limited time, knowledge, and the ability to sift through data.

The only way out is for the wealthy to develop a broader identity of what good citizenship means. And see what is good for the community and their fellow citizens. But where the prevailing mantra is “Greed is Good”, it would take enormous introspection, awareness, and good sense to develop this broader identity. I can only hope that this will happen over time.

On the point of mass transit and cost overruns – as population increases, my view is that we have no choice but to build mass transit. All major cities worldwide have recognized and built mass transit systems. We are only deferring it to the future when it will cost even more.

Btw, there are major cities in Europe which have made public transit free. Even in the US, several cities have made public transit free of cost. This is what innovative governments do – and we need more of this to happen.

In terms of safety, we have transit systems in New York, Boston, DC, and San Francisco among others. New York is shabby, Boston, DC, and San Francisco seem to function better.

As I said in my original post, the issues of cost and safety are often raised mainly by self-serving business interests to postpone the inevitable.

“Boston, DC, and San Francisco seem to function better.”

In Boston, our transit agency is called the MBTA (aka “the T”). It stands for Money Being Thrown Away.

But lots of people use it. Think of what would happen to traffic congestion if all those people drove everywhere and then tried to park their cars. It’s easy to complain about mass-transit, but it makes life easier for the drivers. It also makes life easier for its users, or they wouldn’t used it.

“A house is a place to provide shelter .. whether you rent or you own .. nothing less nothing more”

Oh? With all due respect for the sentiment, a nice thing to say, cold comfort maybe. But I thought a house was an asset that has been the foundation of wealth building (hence a sense of personal security) for the middle class. And a chance to get off a ladder of inflation and price hikes (fairly steadily since the early 1970s). That’s absolutely what it has been for my life, since the 90’s (now paid off, zero mortgage payout). Similarly, I own movies on DVD so I don’t have to re-rent them or be ousted from them by someone else at indeterminate future times, with needs of forever payments and being subject to price hikes.

Also my house is a principal hedge for me (store of wealth) against being obsoleted by the AI revolution, and whatever other crazy things happen in intangible assets.

For the last few decades owning a home has been a vehicle for amassing wealth. But what if that goes into reverse and housing becomes a vehicle for slow motion wealth destruction?

kramartini – BTC and the SP500 have been vehicles to amass wealth and not housing. The home I live in has risen 120% since I bought it in 1999. The average appreciation has been 2.8% YOY. That is not amassing wealth.

I also own a rental house I bought in 2002 for $60k. It is now worth $140k or 133% gain.

If I put that $60k into the SP500, my gains would 400% ($300k) and not 120% ($80k).

These houses have barely kept up with inflation.

LOL

A house is a ticket to not paying rent for the rest of your life. After the morttage is paid off, your cost of living goes down.

Agree with Jon. A house is a liability not an asset. It’s a place to live and nothing more. Even if the price goes up due to inflation, so does your property taxes, insurance, and home maintenance, which go up even after your house is paid off. The appraised value is just a number on a piece of paper, as it does you no good other than make you feel good, that is if you are dumb enough to believe all the BS from the RE industry Shills. What about your kids and the next guy who has to pay for these outrageous prices just to have shelter, which has gone up 70% in the last 4 years alone.

I suppose all assets could be viewed as liabilities if you look hard enough. Maybe for housing the “asset” part of it is the location, or if you own the house and put it out to rent, the net, after tax income or better yet the tax free cash flow.

It’s true that even if you own the house debt free, you still effectively rent it from the State in the form of property taxes. Dont kid yourself into thinking that if you rent you are not paying the landlords property tax bill AND insurance AND repair expenses.

As the property tax grab gets outrageous enough the voters eventually rebel – thats what has happened in my state this year with much of the old cadre of state office holders forced out in the last cycle and suddenly property tax reform emerging from the legislature and overriding the gov’s veto to effectively cut my property tax bill by 50%.

So I’d argue that housing is a somewhat unique kind of asset being both potentially a financial asset and a necessary utility for survival.

The question I have is what happens if eventually the US “my way or the highway” policy of managing USD blows up. What happens if those who make the goods we consume overseas say they no longer want USD in payment. Impossible we all say, but countries have this funny desire to survive.

If that “impossible” event were to happen. What will the impact be on our dollar denominated existence ? Inflation or radical deflation ? Perhaps inflation in consumables and deflation in “assets”

ru82, inflation is a huge problem, and mcdonalds prices have gone up way faster than they should have, which is why their ceo announced on earnings calls that they had to reduce prices to get customers back. see the $5 meal deal.

but your prices are incredibly cherry picked.

I’m so glad my house is paid off. It is my biggest asset, and it is not even close. The amount of money I save every year after paying taxes, insurance and maintenance puts bitcoin to shame. And these savings can be invested in anything I choose! Pay off a house in flyover country and you will live like a king.

“A house (or condominium) is a place to provide shelter …

whether you rent or you own … nothing less nothing more”

Like pretty much everything that has to do with money … it depends.

For me, personally, I look at my residence only as shelter.

We make upgrades to it to make it more “livable” for me and our family. We do look at the cost, but not the “added value”.

Others, including many of those here on wolfstreet, may hold different opinions.

In my mind there is neither a right nor wrong way to look at it.

It always comes down to personal preference.

“We make upgrades to it to make it more “livable” for me and our family. We do look at the cost, but not the “added value”.”

The added value is the actual benefit you get from those upgrades.

I spent $3k on a high-end whole-home water filtration system. The added value is the clean water I now enjoy (and the added longevity of appliances etc.).

I try to avoid doing anything that would require pulling permits and trigger a re-assessment. I don’t want the property value going up.

From a coyotes point of view a rabbits only purpose is a meal, To me the rabbits only purpose is to lay colorful Easter eggs.

As for your views on a home/house the rabbit and coyote might agree with you but not me, a house is a place to put the wife and kids while I explore.

Wait until the giant squirrels attack then your home will become a fort against the large rodents.

As an owner of a few properties, I can tell you that housing isn’t all that its hyped up to be. Had I invested in the sp500 or BTC instead, I could have been a millionaire many times over and lived anywherein the world. I am tired of paying ever-increasing property taxes, repairs, fire and other property insurances.

As a landlord…..I agree. There have been much better ways to make money the past 20 years. Just put money into the SP500 or NASDAQ and sit back and watch them hit new highs and new highs.

No late night tenant calls when the A/C breaks or the bathroom faucet leaks…etc. Cleaning up when a tenant moves. If I had to do it over I would have put the money into the stock market.

the u.s. stock market, and only the u.s., is the last global bubble where people buy irrespective of valuations.

all bubbles eventually pop.

Haha exactly Franz. The mentality of ‘i should have bought stocks, I missed out’ would also be fixed if stocks fell back to historical normal valuations. It may not be long before people are saying ‘I wish I wouldn’t have put all my savings into the stock market and instead’. Thats when history will have finally repeated itself and human nature finally caught up to us, once again. Boom to bust

Also, it takes a lot of extra work to squeeze out an 8% YOY profit. It is a 2nd job that does not pay that well.

“pay someone else’s mortgage.”

Worse than that – pay some newbie flipper’s dipshit mortgage.

Basically, since 2000, moron ZIRP grossly empowered a ton of fairly ignorant home flippers (who could barely fog a mirror, mortgage loan qualification wise) to use way too much leverage to speculate on homes…speculation that was going to inevitably end in foreclosure explosions…because the newbie flippers were largely ignorant of the macro stats concerning “ability to pay” doubled/tripled housing costs (in brief…US incomes came nowhere close to doubling/tripling, end of story).

But enroute to foreclosure, these ignorant flippers were going to create a shit ton of externalities, while desperately trying to squeeze home-cost blood from stagnant-economy rocks.

So home costs explode…for 3 to 5 years, driven by ZIRP engorged SFH speculators (who desperately try to impose their foolish costs on their renters) only to later crash as the imposed-upon either move away or collapse under the housing cost pressure they simply cannot sustain – again, idiot housing prices can double/triple (for a while, due to the fraud of ZIRP rate gutting) – but household *incomes* have not come within 1000 miles of doubling/tripling.

This isn’t the Fed “pushing on a string” – it is the Fed literally leveraging idiots…to sow harmful chaos.

Twice.

So far.

And SFO landlords may be getting tired of watching their equity evaporate just so tenants have a place to live…

@SOL – My exact feelings and thoughts.

As a young renter who doesn’t own a home, I don’t think most people understand the lifelong impacts between buying your first home for $450k compared to buying it for $900k.

My life expectancy has not been doubled. Average salary has not been doubled.

Although it is still financeable, The price difference is compensated by paying tens of years of longer mortgages, living in smaller spaces, inability to buy a second property, inability to save money for other investments and generally living a life much more limited and unfulfilling.

Additionally discouraging part is that majority of people who can vote, either own a home or going to inherit one from their families, so I don’t expect this problem to be anddressed anytime soon.

In other words, people from all over the world want to live in the bay area, and pay a little less…

Yet the population is declining

Wanting and having,….

The ohlone indians lived in the San Francisco area for 10 Thousand years before they were discovered and killed.

They wanted to live in the Bay area also.

After consulting with the “great spirit” I have now found my happy hunting ground and am at peace…I’m not going to tell you where it is but there’s lots of fun.

It seems like a lot of Silicon Valley types have relocated south to San Diego over the last 4 years or so potentially easing some of the demand pressure in SF. Remote work during the pandemic let people tap into relatively low prices to the south, while companies like Apple that were non existent in San Diego previously now have a significant presence.

Actually other than few companies like Apple not a lot of jobs relocated to SD

Apple created jobs in San Diego to poach local modem engineers from local wireless company so that Apple can create its own modem

A lot of companies moved out of SFO to other states well documented in media

Btw.. sd hime prices are also going down albeit slowly

It’s great to see SF and Austin leading the trend. My theory is that tech workers have not only tended to relocate to more affordable locations or become nomadic, but that they can see that investing their money in more inflation protected assets is a better financial move than keeping it tied up in a declining asset like real estate at bubble peak. In terms of inflation adjusted dollars, national “home” (a marketing term used to convert financial decisions into emotional ones) prices have clearly fallen since the peak in mid 2022 and selling at that point to minimize capital gains and put the money into some other less taxed vehicle while renting and or traveling makes a lot of sense financially. I believe the smart money got out of real estate as the speculators moved in and this also leads to population declines when single buyers gobble up multiple properties and jack up rents to some stupid level they were told by YouTube or HGTV would make them rich.

My company is calling people back to office 4-5 days a week with a stern warning: Come back or bid good bye. I guess, this would be happening everywhere over time .

Might that company be Qualcom? They’ve been at battle over modems for years.

Yes

Interesting!

Biotech in San Diego is imploding. Lots of jobs losses all over the country so places where it’s concentrated like SD feel it the most. Also adds to the CRE crash. But they’ve got great weather!

The comps just wont fall in some tech cities because builders offer incentives like rate buydowns for 2-3 years. That prevents price discovery. My question is that is a buydown or not ? I feel that it might seem fair, but its probably not. Has a buydown got anything to do with legal issues around concessions ?

A smaller/milder version of the same thing is going on in many cities. Tech hiring is definitely in an adjustment period after the insane hiring binge of the Covid era. Not quite as extreme as in SF, but certainly noticeable many places.

What about south Bay area

Wonder how the housing and employment look there

We just need one good earthquake

Interesting word choice. Unfortunately, folks don’t tend to have a big enough imagination of what can go wrong. Thankfully, it’s often the case that there is no need to, since day-to-day there are less than 5 earthquakes at a 5.0 magnitude or more on the Richter Scale. The United States Geological Survey (USGS) has issued fantastic graphics showing the statistics of earthquakes at various magnitudes, and maps of where the high-magnitude (i.e., 7+) quakes are most likely to occur. I won’t provide any hyperlinks, but I encourage folks to search for quake-related info from the USGS.

People and communities are resilient.

But, but … fake, greased, marketing dreck, fraudulent, bezzling AI gonna create zee jobz! Where are muh AI jobz?

Dude, AI is so yesterday. Haven’t you heard, it’s Quantum computing that’s going to save the economy from collapse. Companies with a couple employees that were in the energy drink biz are now rebranding themselves and their stock prices are going up 30% in a day.

And fartcoin, can’t forget that. Soon to replace the dollar. Yellen and JPow loading up on taco bell as we speak.

I see Musk cutting the Federal Workforce by 30% here in the Swamp soon after the new administration takes office. Contractors who are sucking off the Federal contracts will be the first to take the hit. Musk will do what he did at Twitter, where he fired 80% of their employees. Many working from home now, doing squat, will get e-mails telling them they are no longer needed. The govees will be the next to go, but they will get the message and leave on their own. This could decimate property values here just like they did in SFO.

Let’s see, we had the “Roaring 20’s” before and perhaps, this decade is roaring as well…we know how the previous one ended.

While I know you are jesting it is important to know the roaring twenties was really only good for the wealthy and really considered that as a result of media. Average Americans have it much better off now, obviously especially blacks and other minorities, but farmers and working class as well. Wealth inequality still significant obviously so that consistent.

Yeah, my dad grew up on a farm in the 20s and 30s. South Dakota wasn’t roaring much back then.

Just wait until investors realize that there is really no such thing as “Artificial Intelligence,” machines can’t think, they have no feelings, they can’t laugh or cry, they can’t understand anything. Machines have no blood. They are not alive. They are machines. It is all a big Silly Con Valley/Wall Street fairy tale. I never had any desire to have a “conversation” with a machine, and never will. I can’t even stand the annoying chat bots that occasionally pop up on my screen. The computers are more powerful now, but intelligence? That is absurd. The hype has gotten out of control.

I still think AI is going to hit a wall at some point. It will either be model collapse, or it will be when these companies can no longer just burn cash and have to deal with the reality of the cost/benefit ratio here.

It is suspicious that Wall Street is having to use FOMO to get everyone on the AI train. Invest in AI or be left out! Your competition is going to be using it, so you’d better!

This all sounds like the F.U.D. (Fear, uncertainty, and doubt) strategy that Microsoft used to be famous for.

AI is an accelerant. If you are smart and productive, it can massively increase your output in multiple ways. If you are lazy and stupid, AI will dramatically increase the speed at which you get caught and exposed as being lazy and stupid.

Google AI frequently returns incorrect results. And even more often returns answers to questions other than what I asked….

AI = Atrocious Idiocy

I ignore all the AI stuff and turn it off when I can. Remember those news articles about how many grams of CO2 your Google search creates? Well now thanks to technology, we’ve increased emissions per search by 100x and decreased accuracy and relevance by the same amount! Now that’s progress!

Next up, we’re going to fill the whole page of search results you do get with AI generated spam. And then train the AI search on that spam! What could possibly go wrong??

That is related to your ability to write a good prompt. GIGO.

Someone gets it! I like my homes and they are not asetts, they are liabilities. In the same class as life insurance. Someone may benefit and it is going to be you. Small children is the only reason to have either!

Rent and drop your life insurance! More money in your pocket and they will have a reason to cry when you die!

My current home would rent out at a minimum of $2500 per month. That is $30,000 per year of after tax dollars that I would have to pay to live here. I have a paid for rental that covers all our property taxes and insurance. About once per month I run into one of the tenants (a young 20 something couple) while on a walk. I just ask them if everything is going okay? They keep the place up to snuff so no worries there. They pay by email transfer. I just leave them alone. They asked me if they could get a dog? Absolutely, but no cats!! Nice dog for sure.

I have been retired since age 57….12 years ago. I could only do this because I have no mortgage payment or rent charges. Renters think they don’t pay property taxes or insurance? Nuts. Renters are simply paying the owners taxes and insurance for them.

When I was in my early 20’s I sucked up a down payment and bought an old house. Broke even during the 81 housing bust we had here and then relocated for work. Bought another place and paid that off by age 43. Took the same mortgage payment and used it to buy more property elsewhere, then relocated. Never bought anything beyond the house on time, ever. Drove junk vehicles that I maintained myself.

But more important where you live defines your life. Is there a park nearby that you walk in, or if it is a condo in a city do you have favourite haunts nearby? For us we live rural on a river. The view is spectacular. We kayak whenever we feel like it. It is us, and has been for 20 years.

When you eat supper is it just fuel so you buy and eat whatever? Of course not. Housing is the same kind of thing. If you eat cheap you will have more money in your pocket. Life is short and money unto itself has no value as far as I’m concerned.

.

Why no cats? They are great at keeping mice out of your property.

STATEMENT | DECEMBER 27, 2024

Statement by Director Jonathan McKernan on Monitoring the Passivity of Index Fund Complexes: Vanguard’s New Passivity Agreement

The passivity agreement entered into by Vanguard today should enable the FDIC to address, with respect to Vanguard, the concerns I raised in January and several times since about gaps in the FDIC’s monitoring of the purported passivity of the largest index fund complexes.

Those concerns have some urgency given the rapid growth of these index fund complexes and the growing body of academic work and other evidence raising doubt about whether these index fund complexes are truly passive. Some critics have pointed to evidence that these index fund complexes have pushed ESG agendas at public companies. Others have expressed concerns about the risks to competition posed by concentrated ownership. Still others have focused more generally on the concentration of power in a few institutional investors.

1:04 PM 12/27/2024

Dow 42,992.21 -333.59 -0.77%

S&P 500 5,970.84 -66.75 -1.11%

Nasdaq 19,722.03 -298.33 -1.49%

VIX 15.95 1.22 8.28%

Gold 2,635.80 -18.10 -0.68%

Oil 70.26 0.64 0.92%

Wait until there’s a big WHOOPSIE! in crypto, and all those Shitoshis and their fake valuations evaporate into thin air. Then we’ll start seeing what’s up.

A mid tier condo for just under a million! And I am sure the condo fee is significant. Bubble still has a way to go….

The dumbest thing I heard was that these companies were hiring because the others were hiring and all competing for talent that they didn’t even really have a role for. How are these companies still in business making these dumb decisions? Oh yeah, lack of competition.

@Cole: Yes, lack of competition cos they managed to gobble up the smaller companies or put them out of business through underhanded means. The number of companies Microsoft put out of business by “adding” features to Windows, Office, and the browser is significant. Apple famously advertised about people being in the trance of IBM but became a walled garden itself when it got the opportunity. They acquired key software companies and made them accessible only on Mac OS. Almost very large company has a monopoly in its markets while our antitrust regulators have clearly been pushed into a corner by “anti-regulation activists” most of whom are corporate lobbyists and shills. Our free-market system exists only as a facade for the oligarchy.

Market schmarket. There is a serious dislocation in the capitalist doctrine. As the asset bubble begins the inevitable process of asset price deflation.

Your graphics demonstrate the magnitude of the asset bubble where by a 20 pct reduction in price seems like a seasonal variation.

Ignoring the mountain of risky debt that made it all possible. The ens, perhaps, of the economic summer of milk and honey.

On the other hand someone may be waiting, with pockets full of fiat currency, to purchase, what they perceive as the devalued real estate. China purchasing the Rockefeller Center.

Which is the risk that has been concentrated in these asset price bubbles, purchased by the Fed during QE.

As a renter in the vibrant Bay Area, I’m taking a strategic pause until housing prices find a more reasonable level—I’m optimistic that will happen in about eight years. In the meantime, I’m making the most of my rewarding tech job, which allows me to save and invest in exciting opportunities while also treating my family to wonderful vacations! If my wife joins the workforce, our approach to entering the housing market could shift. Yet, I’m open-minded and ready to explore other investment options if I don’t find the right opportunity here. Embracing this journey with positivity and enthusiasm is key! Live your best life now. Stop doom scrolling Zillow!

Can someone help me understand why I keep seeing conflicting data on home price levels? For instance FastCompany article that dropped today titled “28 housing markets where home prices are actually falling” shows home price levels in the Bay area increasing. Both articles site the same Zillow Home Value index… What am I missing? Thanks (:

This article above is about the CITY of San Francisco.

Here is the San Francisco Metropolitan Statistical Area (MSA), officially called “San Francisco-Oakland-Fremont, CA MSA” This is about half of the Bay Area.