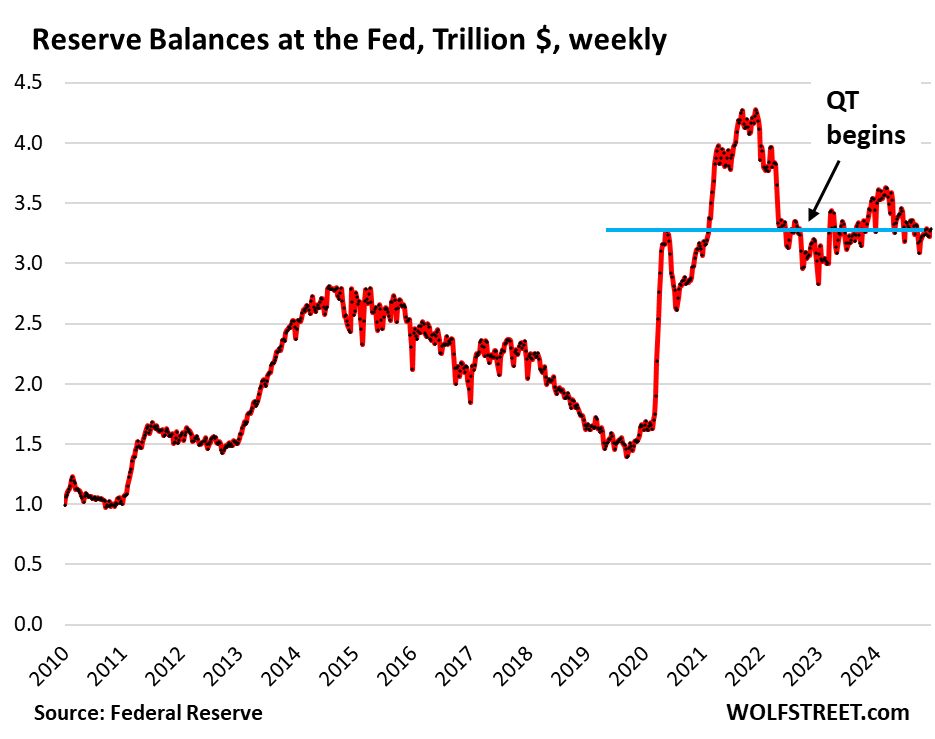

QT has only drained ON RRPs so far, but not Reserves, which are still where they’d been when QT started in July 2022. QT has a long way to go.

By Wolf Richter for WOLF STREET.

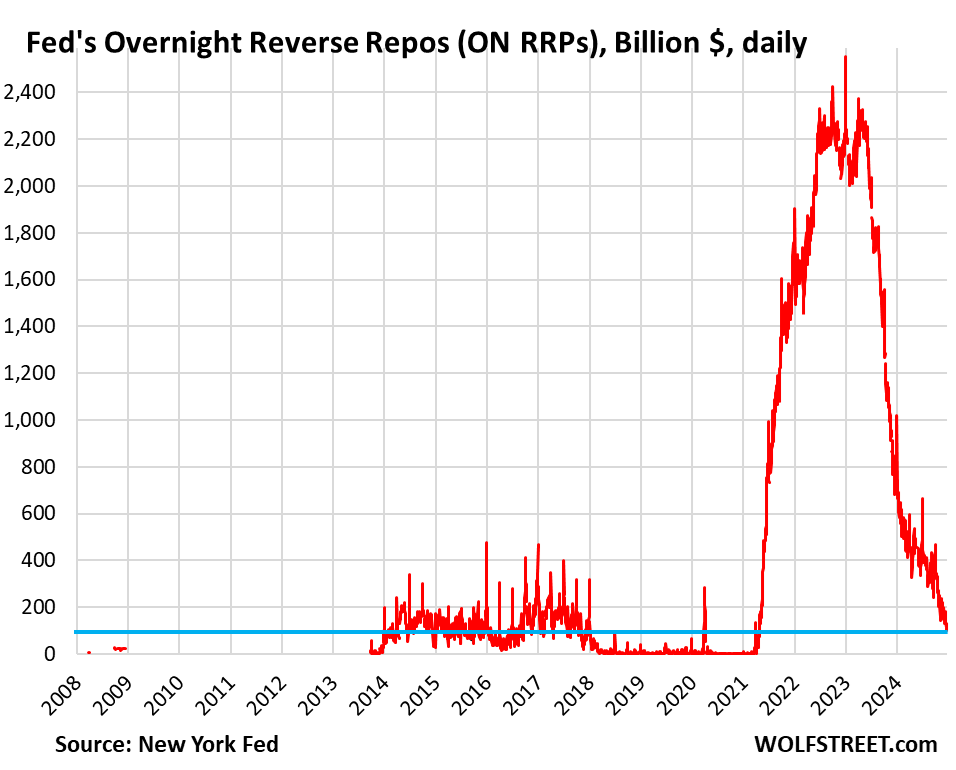

Balances at the Fed’s facility for Overnight Reverse Repurchase agreements (ON RRPs) fell to $98 billion on Friday, the lowest since April 2021, down from $2.4 trillion from the peak at the end of December 2022, and well on their way to zero or near-zero, where they were in normal times, and where the Fed wants them to be again.

To help them get to zero more quickly, the Fed lowered its ON RRP offering rate – one of its five policy rates – on Wednesday by 5 basis points, in addition to the 25-basis-point cut that all its five policy rates got. At 4.25%, the offering rate is now even with the bottom of the Fed’s target range for the federal funds rate. The minutes of the November meeting already revealed a discussion to that effect, and so this was not a surprise.

The purpose of this reduction in the ON RRP offering rate was to encourage money market funds (MMFs) to pull their cash out of this facility that the Fed provides and find other places for their cash where they can earn a little more interest, such as regular repos or T-bills (4.30%-plus), which currently yield more than the reduced ON RRP offering rate (4.25%).

MMFs are the primary users of the ON RRP facility at the Fed. The ON RRP balances represent excess liquidity that the Fed created during QE that financial markets don’t know what else to do with, so they stash it at the Fed.

As part of its QT, the Fed has now drained $2.1 trillion in liquidity from the markets, and essentially all of the drainage has come out of ON RRPs, instead of the reserves.

Reserves represent cash that banks deposit at the Fed to settle transactions and to collect interest on the balances. Interest on reserves (IOR) is one of the Fed’s five policy rates, currently 4.40%.

QT is supposed to whittle reserves down from “abundant” to merely “ample,” but the Fed doesn’t know where “ample” is, except it’s quite a bit lower, and the Fed is trying to get reserve balances there carefully.

But QT has so far only drained ON RRPs, while reserves, currently at $3.28 trillion, are still where they had been when the Fed started QT in the summer of 2022. As far as reserves are concerned, QT hasn’t even started yet, and there is still quite a ways to go before they get to “ample.”

The ON RRP offering rate is usually at the bottom of the target range for the federal funds rate, and at this rate, and under normal conditions, ON RRP balances are generally zero or close to zero, as we can see in the first chart above.

The Fed had raised the ON RRP rate by 5 basis points off the bottom of its target range on June 17, 2021. At the time, its target range for the federal funds rate was 0.0% to 0.25%, and it raised the offering rate from 0% to 0.05%. And until Wednesday, it remained 5 basis points above the bottom of the target range.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The question is will the draining of bank reserve from QT take away the excess liquidity that has created the everything bubble? It seems to be a complex issue. Maybe Wolf can answer that.

Draining reserves at the Fed will drain some liquidity, not all, obviously.

The posts that try to explain all the convoluted ways (5 policy rates…) the Fed attempts to operationalize its fundamental power (to print unbacked money to buy various financial assets to alter various interest rates) normally give me a migraine but this post is one of the clearest and most helpful.

I think that is because the post discusses what a policy change (extra 5 BP reduction in ON RRP) is trying to accomplish (incentivize shift of bank idle cash from Fed to…Treasuries/other).

Which also helps to explain what all the various Fed policy levers/flywheels/whirligigs/perpetual motion machines are theoretically trying to accomplish…to *differentially* shift interest rate incentives across *different* financial asset classes (Mmfs, Fed storage, Treasuries, etc).

But my guess is that a big honking flow chart (looking like the toilet piping blueprints for the Pentagon) would be necessary to track all the Fed flywheels/whirligigs.

And that raises the question of ultimate effectiveness/reliability of all the flywheels/whirligigs…after all money is fungible and therefore flows…in response to *real asset* realities and not necessarily according to paper-created differentials.

The “complicatedness” of it all brings to mind Venezuela-like attempts to create multiple different exchange-rates in order to obscure the fundamental dysfunction of the Venezuelan real asset economy.

Channeling Rube Goldberg?!

Wolf, my inference is that we should understand that you think draining reserves has somewhat greater potency in reducing liquidity to markets than draining ONRRPs.

Is that correct?

TrBond,

That’s my impression. The effects of QT will get more serious and riskier as bank reserves begin to decline.

In terms of the “risky” part, the Fed revived its Standing Repo Facility in July 2021 to deal with the risks of withdrawing liquidity (QT), after Bernanke shut it down during QE. The SRF offers repos (collateralized loans essentially) at the Fed’s repo rate (4.50% currently) to approved counterparties (banks), so they can use it to manage their daily liquidity requirements.

The Fed announced this week that it will test the SRF with two auctions a day (one at around 8 am, the other around 2 pm) during year-end days, when liquidity strains are usually the largest. It normally just operates the afternoon auction, and there has been essentially no activity because there is still so much liquidity in the banking system.

The lack of the SRF was a problem in the fall of 2019 that contributed to the repo market blow-out which turned into a panic, that then caused the Fed to step in with emergency repo measures. With the SRF in place, that kind of panic would have never happened: As repo market rates started spiking, banks would have borrowed at the SRF at the Fed’s rate and lent to the repo market to profit from the rate differential, which would have quickly calmed the repo market at the very early stages.

So it looks like to me that the Fed is setting up to run the banking system with substantially lower reserves, kind of like it used to.

Will be nice when it reaches zero. One thing less to worry about. ;)

Stand aside weaklings, I can get the number to minus zero.

But to what purpose, just to watch it flounder about once again….

The Russians have the sleeping bear to awaken when needed, the Americans have a fat pig to awaken…. gobbling up everything.

Haha, hopefully it will not come back in a while with Standing Repo Facility in place, as Wolf so nicely explained.

Everyone has a plan, until they get punched in the face.

MT

Wonder why Bernanke got rid of this?

Seems like a nice safety feature.

sufferinsucatash

Bernanke thought and has said so at the time that the Fed’s balance sheet would never shrink, that reserves would always be huge. There was no discussion of QT under him, only QE. And the SRF really isn’t needed if the banking system is totally awash in reserves.

QT-1 was designed and started under Janet Yellen in the fall of 2017, years after Bernanke departed, and it was continued by Powell.

DawnsEarlyLight has it right…

“Everybody has a plan until they get hit in the face”

Decades of Fed/DC “planning” by “the very best minds” has yielded up a Debt-to-GDP well in excess of 100%, an inevitable entitlements crisis, and actual “plans to fix it all” that show little more genius than that of the Weimar Republic.

But for decades fiscal Conservatives were told “nothing to see here, nothing to worry about, your worldview is obsolete”.

Some “plan”.

Some “planners”.

I think we can conclude the Fed himself want a RRP facility at zero, and this is absolutley the right way, because the RRP is no “investment facility.” Additionally these step (cut the RRP rate) shows, that the empty RRP facility panic mainly posted by bank analysts is ridicolous.

Banking reserves and which is ample and which not, is a complete different topic and must be tested out. For problems the SRF is there to solve.

Next steps for the Fed are in my view, maintain QT at the present maybe higher level, and shift the balance sheet to treasuries and bills only, which means offloading MBS and CMBS.

What is the purpose of ample reserves? Ample reserves increase liquidity, they do not guarantee solvency. No bank can survive a run, even if its reserves are “ample.” That is why central banks are the lenders of last resort to the commercial banks. Ample reserves may encourage banks to lend; is there any evidence that this is the case?

How can the Fed make (incentivize?) banks reduce their reserves? I assume those reserves belong to people as deposits or the banks as bank capital.

the banks are not losing money or cash in this shift, LOL. Your CDs and checking account deposits will be just fine. This is part of the internal financial plumbing and the flows through that plumbing. Don’t worry about it.

Sure, just lower the interest rates on those reserves Money will flow elsewhere?

How to bank reserves relate to the capital requirements we see banks and the Fed fighting over in the news? I assume they must be far below where we are at since the Fed (and I think most here) want reserves to continue to drop. However, I am trying to reconcile all these large bank reserves with my understanding that banks are usually trying to keep as little capital as possible.

“Reserves” have nothing to with “capital.”

Reserves and capital each had their own separate regulatory requirements, until Powell did away with the “minimum reserve requirement” in 2020 (because QE put a huge amount of reserves into the system). Now there are only minimum capital requirements.

At the most basic theoretical level:

1. Reserves = bank cash on deposit at the Fed.

2. Capital = bank assets (loans, mortgages, investments, cash, etc.) minus bank liabilities (deposits owed their customers, bonds outstanding, etc.)

What the fight is about is how “regulatory capital” is figured, what is included and what isn’t, how the capital ratios are figured, and what the minimum ratios should be. This is hugely complex, and the banks are complaining that it’s too complex and needs to be simplified, and they fought against raising those requirements further.

Wolf: You needed to mention that small & medium size banks have a much higher capital requirement than the giant banks. When small banks capital gets below about 10% the bank examiners start raising their eyebrows and complaining. The Giant banks are allowed to have their capital half the size of the smaller banks which is not justified as the giant banks are the risky banks that have trillions of dollars at risk speculating in derivatives. All derivatives are is an unsecured bet on an underlying asset and that is why the whole economic system is at risk.

You got this backwards.

Very respectfully Wolf:

According to recent data, the average Tier 1 capital percentage for Global Systemically Important Banks (G-SIBs) is around 7% based on the leverage ratio, with some sources reporting slightly higher figures like 7.24% as of the end of 2023,

The average tier 1 capital percentage for community banks is 10.52%. This is higher than the average for large (9.22%) and regional (9.76%) banking organizations.

Jeeeesus, you’re comparing “leverage ratio” of 7% for GSIBs to “tier 1 capital ratio” of community banks of 10.5%. Can you not even read? “Leverage ratio” is a completely different thing than “capital ratio.” And the minimum leverage ratio is LOT LOWER than the minimum capital ratio.

So let me crush your knuckles one at a time.

1. In your prior comment, you said that G-SIBs have smaller capital requirements than smaller banks. I replied that you had this backwards.

This is public information. You can just look it up. The Federal Reserve as US bank regulator imposes a “G-SIB surcharge” of 1.0% to 4.5% on G-SIBs in additional capital requirements.

Federal Reserve’s Minimum CET1 Capital requirements – which includes base requirement (4.5%), plus stress buffer requirement (which varies from bank to bank), plus G-SIB surcharge:

#1 JP Morgan: 12.3%, including a G-SIB surcharge of 4.5%

#2 Citigroup: 12.1% including a G-SIB surcharge of 3.5%

#3 BofA: 10.7% including a G-SIB surcharge of 3.0%

#4 Wells Fargo: 9.8% including a G-SIB surcharge of 1.5%

All US G-SIBs have actual Tier 1 capital ratios (= your “capital requirements”) in the double digits. For example, JP Morgan’s, in Q3 2024:

— Common Equity Tier 1 (CET1) capital ratio: 15.3%

— Tier 1 Capital ratio: 16.4%

— Total capital ratio: 18.2%

This is public information. It’s disclosed on every bank’s 10-Q. Here is JPM’s 10-Q:

https://www.sec.gov/ix?doc=/Archives/edgar/data/19617/000001961724000611/jpm-20240930.htm

2. same thing in terms “leverage ratio” ( which is a completely different thing than “capital ratio.”)

Under Basel III, the minimum Tier 1 Leverage ratio = 3%, which is also the case in the US. But US regulators have imposed on bank holding companies with over $700 billion in total assets or more than $10 trillion in assets under management an ADDITIONAL 2%, for total minimum requirement of 5%.

JPM’s leverage ratio = 7.1%

I don’t know why I have to waste my Saturday night on your bullshit.

re: “essentially all of the drainage has come out of ON RRPs, instead of the reserves”

In contrast, Bernanke drained legal reserves for 29 contiguous months.

Funny, when I see numbers like 98 billion I think ‘pocket change.’. I am course can’t fathom that amount of money personally but in the larger content seems miniscule. I get this will get near zero but what is the overall significance if that money just flows into something else other than Fed balance sheet? If this money just flows into money markets they invest in treasuries that could drive yields down although not significantly since a drop in the bucket.

I can recall the late 1980’s when the richest man in the US, Sam Walton, had $2.5 billion…and how amazing I thought that was.

Now $98 billion is just pocket change.

Is the correct way to think of Reserve Balances at Fed as a nominal figure? Or as a % of assets/liabilties?

For instance – is $3 trillion in reserves in 2024-25 the same as $3 trillion in reserve in 2020. Or is it less relative to expansion in deposits, loans, and money supply.

“Is the correct way to think of Reserve Balances at Fed as a nominal figure?”

Yes, it’s correct.

“Or as a % of assets/liabilties?”

No that’s doesn’t make sense. ALWAYS on EVERY balance sheet:

Assets = liabilities + capital.

Capital at the Fed is set by Congress and is only $40 billion. So when liabilities (including reserves) go down, the assets go down by exactly the same amount. That’s the relationship. Expressing one as percent of the other doesn’t make any sense at all since they move in parallel and equal amounts.

The big three liabilities are: reserves, currency in circulation (paper dollars), and the government’s checking account (TGA). Currency in circulation moves very slowly and is demand based. The TGA’s level is decided by the government, and it can move a lot. But when the TGA drops, the cash shifts to reserves, and vice versa, it’s a shift within liabilities, from one liability to another, and it doesn’t change the overall level of assets and liabilities. But when QT draws down reserves, that reduces assets in equal amounts.

Wolf-

You said: “Interest on reserves (IOR) is one of the Fed’s five policy rates, currently 4.40%.”

Does a return to a “scarce reserve” regime imply the abolition of IOR, and a return to mandated and audited commercial bank reserves?

Would that be an improvement, in your opinion?

The old way — scarce reserves, minimum required reserves, no IOR, and the Standing Repo Facility to provide daily liquidity to banks — was far better than the regime started by Bernanke in 2008. Everything that the Fed has been doing since July 2021 (revival of the SRF that Bernanke had shut down) indicates that the Fed is trying to go back to the future, but painstakingly slowly, over many years.

Thank you, Wolf. Always appreciative of the unique service you provide, I will be sending my annual donation with the new year.

Hope you enjoy the Holidays and enjoy a prosperous and healthy 2025!

The intractable monetary problem is the Federal government is unable to fully fund government operations other than the Defense budget. Congress and the White House must instead pass deficit budgets that require Treasury to issue more notes and bonds. The long term bond market suffers slack demand due to over supply as these deficit budgets require.

The Fed cannot shed its bond holdings due to slack demand. The glutted bond market is coupled with “excess liquidity” a nice way of saying glut of cash. M2 was inundated with new money the Fed pushed into the economy when it had to pull Treasury bonds out of the market to prevent a bond crash. The Treasury bond glut was created when Congress funded COVID relief with Treasury-financed money.

The domestic crisis is further threatened by BRICS.

You’ll never get a job at CNBC.

That’s meant to be a complement.

I think they wanted the slow motion QT plan to gradually deflate the asset bubble. It isn’t happening for stocks. Tells me things will adjust at once.

Researchers at the Federal Reserve of St.Louis concluded with an analysis that the reason Reserves have Not decreased since Quantitative Tightening started in June 2022 is because the US Treasury Yield Curve has been mostly inverted since, and which incentivize Banks to deposit at the FED account at the IORB Rate ( Interest on Reserves Balance ) , because the IORB Rate is greater than the US 10 Year Treasury Yield Rate.

At the time when the issued the analysis

the IORB Rate = 5.40 % , US 10 Year Yield Rate = 4.45 %,

right now with the last Fed Funds Cut that just happened, the IORB Rate has decreased, and 10 Year Treasury Yield has increased recently, where the US 10 Year Yield is higher currently,

IORB Rate = 4.40 % , US 10 Year Yield Rate = 4.51 %

https://www.stlouisfed.org/on-the-economy/2024/apr/bank-reserves-start-quantitative-tightening

Yield curve still not steep enough to incentivize more market participants to lend for 5-30 years vs the short-term rates. (Unless one thinks the end of the inversion signals an imminent recession and lower yields ahead, which many do.)

“Unless one thinks the end of the inversion signals an imminent recession and lower yields ahead, which many do.”

For the last two years we were told a recession was imminent because the yield curve was inverted. Now a recession is imminent because the yield curve un-inverted?

Ugh.

Often repeated: a broken clock is right two times a day.

Black swan events are always right around the corner.

WWSJ: America’s Farm Recession Is Here. One Early Response Is Sending Billions to Farmers.

Reeling from falling crop prices, farmers and agricultural companies have grappled with diminished income and pulled back spending

That’s not good news, the farmers have many controls on their operation, they can’t just raise their prices….so sad.

But they can sell the tractor and the 2000 acres with barn to an eager Chinese buyer…not so sad.

Or they can dip into the working capital they built from record farm income from the past couple of years instead of lobbying for a bailout when margins go negative.

Wolf,

Did you publish any article on chronology of FED’s rules changes GFC?

I know in many articles and comments, you share various points.

e.g. Ben stopping SRF in 2008. Powell moving away from Minimum Reserve. ON RRP rate going up by 5 BP in 2021. I felt that was in order to make Buck doesnt break for MMF. Now FED reverting back to 5 BP below for ON RRP.

Just checking if any article where we can read all of them together?

Thank you.

I have not written a chronology of the Fed’s rule changes. I probably have never written a chronology of anything that’s longer than two paragraphs. I feel like chronology-writing is someone else’s job.

Sandeep, the St Louis Fed published a chronology going back to 1913. It is accessible at this URL:

https://fraser.stlouisfed.org/timeline/monetary-policy-history#66

No need to write your own chronology now.

Thanks. It’s kind of funny: The last entry is the July 2021 revival of the SRF. That’s how important that was. Nothing else that the Fed changed since then qualified to be included on the list.

Thank you MC Bear. Appreciate it.

Wow. Treasure trove of interesting evolutionary developments that lead up to 21st century “elastic currency” (and Debt out the Wazou).

Thank you for this link!

Meanwhile, on a different but similar planet:

Assets and Liabilities of Commercial Banks in the United States – H.8 (just released):

Just curious, but how does this slow paced QT play out in relation to bank liabilities and reserves?

We know QE was to prevent a depression, but then along came the SVB era — so is this new level of QT an indication that banks are stable?

A few years ago the Fed was showing a relationship for:

Bank Assets and Reserves Relative to Bank Assets

Just asking for a friend — lol

Wolf-

It’s good that ON repos are going to zero. My question is, why can’t reserves go to zero now too? Once Powell removed minimum reserve requirements, what exactly is the purpose of reserves anyway? And why pay interest to banks to keep them?

As you mentioned above, bank capitalization is now determined by other assets. Reserves used to restrict lending, but no longer. They are basically an anachronism, unless the goal is to re-introduce minimum reserves at a later date.

The Fed should just do away with IOR, but the problem with that isn’t that it will lead to bank failures, but the opposite: it will lead to asset inflation. If a bank is no longer earning interest on reserves parked at the Fed, they’ll yank them out and put them in treasuries. This won’t make the bank fail; as you mention, bank liquidity regulations are based on how much tier 1 assets they have, and Treasuries qualify. Rather, it will inflate the bond market (driving down yields and leading to spillage of money flows into other asset classes) working against the Fed’s goals of QT.

But what this means is that the Fed should be able to go faster with QT. Essentially, to keep asset markets where they are (which is still quite inflated), they would have to remove the same amount of treasuries from the market, as banks would buy if they shift their money out of reserves. IOW, what they should be doing is decreasing the IOR rate (incentivizing banks to take money out), and increasing QT to absorb the additional flows into treasuries. Would you agree?

I think this is where I (and others) who keep telling the Fed to move faster are coming from. No, I don’t want to destroy the economy. But at this point, we’re still at the stage of moving balances around, without really draining any money from the economy (I leave out interest rates, where the Fed *has* substantially tightened asset markets dependent on credit, such as real estate). The shifts on ledgers at the Fed can be done much quicker with minimal harm. After all, no one (outside of weirdos like me) was predicting that draining $2tril from ON repos could be done with basically no issue. And delaying this part of QT means the actual economic effects of QT (reducing overheated asset prices) are unnecessarily delayed.

Now we’re going to see the same overly cautious, slow approach to draining reserves, while people suffering real harm from overinflated asset prices (like young people who can’t afford houses or paying high rents) have to wait several more years to see any relief.

1. “why can’t reserves go to zero now too?”

Reserves were never ever zero. It’s called the “fractional reserve banking system” for a reason. Reserves are important. But they were called different things, such as “Required Reserves” and “Excess Reserves.” When Powell did away with the required reserves, “excess reserves” were also done away with, and the whole thing was renamed “Reserves.”

2. “Once Powell removed minimum reserve requirements, what exactly is the purpose of reserves anyway? And why pay interest to banks to keep them?

Reserves are cash that banks use to pay each other through the central clearing that there reserve accounts at the Fed provide. Every day, there are several trillion dollars flowing through these reserve accounts to settle securities transactions, home purchases, credit card payments, etc. Every day, in the morning and in the afternoon, banks pay and receive huge amounts of cash through their reserve accounts.

If a bank doesn’t have enough reserves to meet that day’s needs – maybe their income cash arrives after their cash goes out – it can borrow that amount for a few hours until the cash comes in. This borrowing used to be done at the Fed’s Standing Repo Facility before 2008, which Bernanke killed.

In July 2021, the Fed revived the SRF, so banks can once gain borrow through it to meet their daily cash needs. With the SRF back in action, theoretically, the Fed can go back to how it used to do it, with minimum “Required Reserves” and not paying interest on reserves, and banks can borrow the rest they might need at the SRF. So the Fed is now set up to gradually draw down reserves, if it wants to go that route — all of which takes years.

Just how in a any way is the Federal Reserve supposed to drain reserves? These are DEPOSITOR funds earning interest at the Federal Reserve in reserve accounts of banks and are EXCESS reserves due to the fact that there is such low demand for borrowing from bank customers.

“Just how in a any way is the Federal Reserve supposed to drain reserves?”

Watch it happen right here 🤣

BTW, there are no more “Excess Reserves.” It’s now all just “Reserves.”

Will they ever take a crack at removing that large line upwards from 1 trillion to 3.25? Or would that shock all the markets too much?

Just mechanically, it probably cannot happen. Over those 15 years, everything has ballooned, the economy, the population, businesses, the banking system to deal with this economy, businesses, and population, while the purchasing power of dollar-denominated assets and liabilities has withered. It takes a lot more in loans, deposits, assets, etc. to deal with today’s economy. So I doubt reserves can revisit those lower levels from 15 years ago.

Why were my two posts completely removed / censored?

That’s not cool. I said nothing that would break your community guidelines. Specifically, my last post, I was asking questions.

Wow!

You based the question on a copy-and-paste bullshit statement that you put at the beginning. I have shot down that statement here so many times already that it’s not funny anymore, and that I’m not doing it anymore.

By basing your question on a bullshit statement, your question became bullshit. So to address that I would have had to spend an hour shooting down the bullshit statement first that I have already shot down a gazillion times.

I decided some time ago that I’m going to make my job easier because life is too short: If you base a question on a bullshit statement, the whole thing gets deleted. If the question itself is bullshit, the whole thing gets deleted.

You often point out that cash in circulation is demand-based, as is (effectively) the Treasury General Account. But it seems to me that reserves are also demand-based. These are capital owned by banks which they have lent to the Fed.

How then, does QT work? Do these banks try to lend to the Fed and the Fed just says “no”?

To word this question another way — I understand QT as the Fed reducing its assets by e.g. allowing Treasurys to expire. But to balance, it must reduce its liabilities by an equal amount. How can it control its liabilities so precisely?