“Current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades.”

By Wolf Richter for WOLF STREET.

“It’s important for mortgage investors, the housing market, and consumers to understand that it is unlikely we will again see the low mortgage rates we had during the COVID-19 pandemic, when a unique combination of monetary and fiscal policy sent rates to near all-time lows,” wrote Priscilla Almodovar, the CEO of Fannie Mae, the largest of the Government Sponsored Enterprises that have been in conservatorship of the federal government since the mortgage crisis. They buy mortgages from lenders, guarantee them, package them into MBS, and sell the MBS to investors around the globe.

“In fact, current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades. Since 1990, the 30-year fixed-rate mortgage has averaged 6%,” she said in the post published by MarketWatch today.

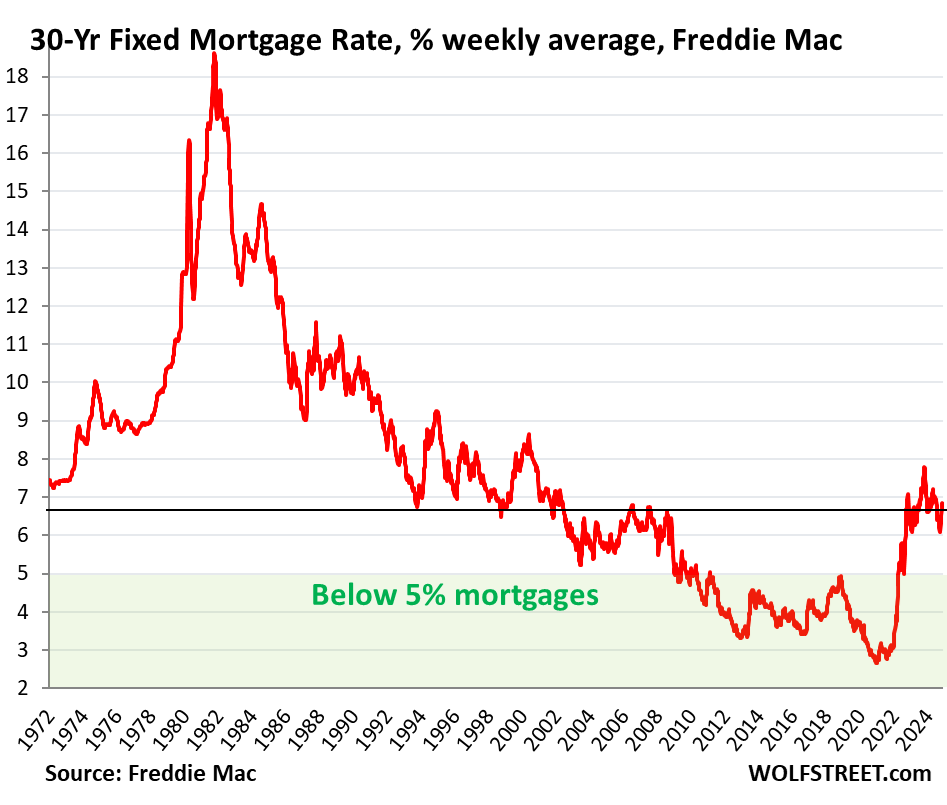

In fact, the average 30-year fixed mortgage rates were never below 5% in the data from Freddie Mac, which goes back to 1971, until the Fed started buying MBS in January 2009, which pushed mortgage rates below 5% for the first time ever.

In fact, in fact, in fact… mortgage rates were above 6% the entire time in the data until October 2002, after the Fed had embarked on slashing rates to create Housing Bubble 1 to make up for the imploded stock market. And three years later, by October 2005, after the Fed had embarked on blowing up its Housing Bubble 1, mortgage rates were back above 6% and stayed there until January 2008, when the Fed kicked off QE by buying Treasury securities to deal with the financial system that was on the brink of imploding due to the imploding mortgages. And mortgage rates began to descend, and in January 2009, with Housing Bubble 1 having collapsed and morphed into the mortgage crisis and the broader Financial Crisis, the Fed started buying MBS which pushed down mortgage rates further.

In late 2018, in response to the timid rate-hike cycle and QT, mortgage rates briefly rose to 5%. But with stocks tanking, and with Trump keelhauling Powell on a daily basis over the puny policy rates and QT, the Fed pivoted to rate cuts in 2019 and QT ended in mid-2019.

Then during the pandemic, as part of its immensely reckless QE, the Fed bought huge amounts of MBS which pushed mortgage rates below 3% for much of the time from July 2020 through September 2021, which caused the biggest inflation of home prices in the history of the data, and those inflated home prices are now the biggest problem in the housing market because it’s choking on those too-high prices and sales of existing homes have plunged to the lowest since 1995 because prices are too high.

But since September 2022, the Fed stopped buying MBS and as part of ongoing QT has shed the first $500 billion of them, and has said multiple times in its communications that it plans to get rid of them all. And mortgage rates have shot up.

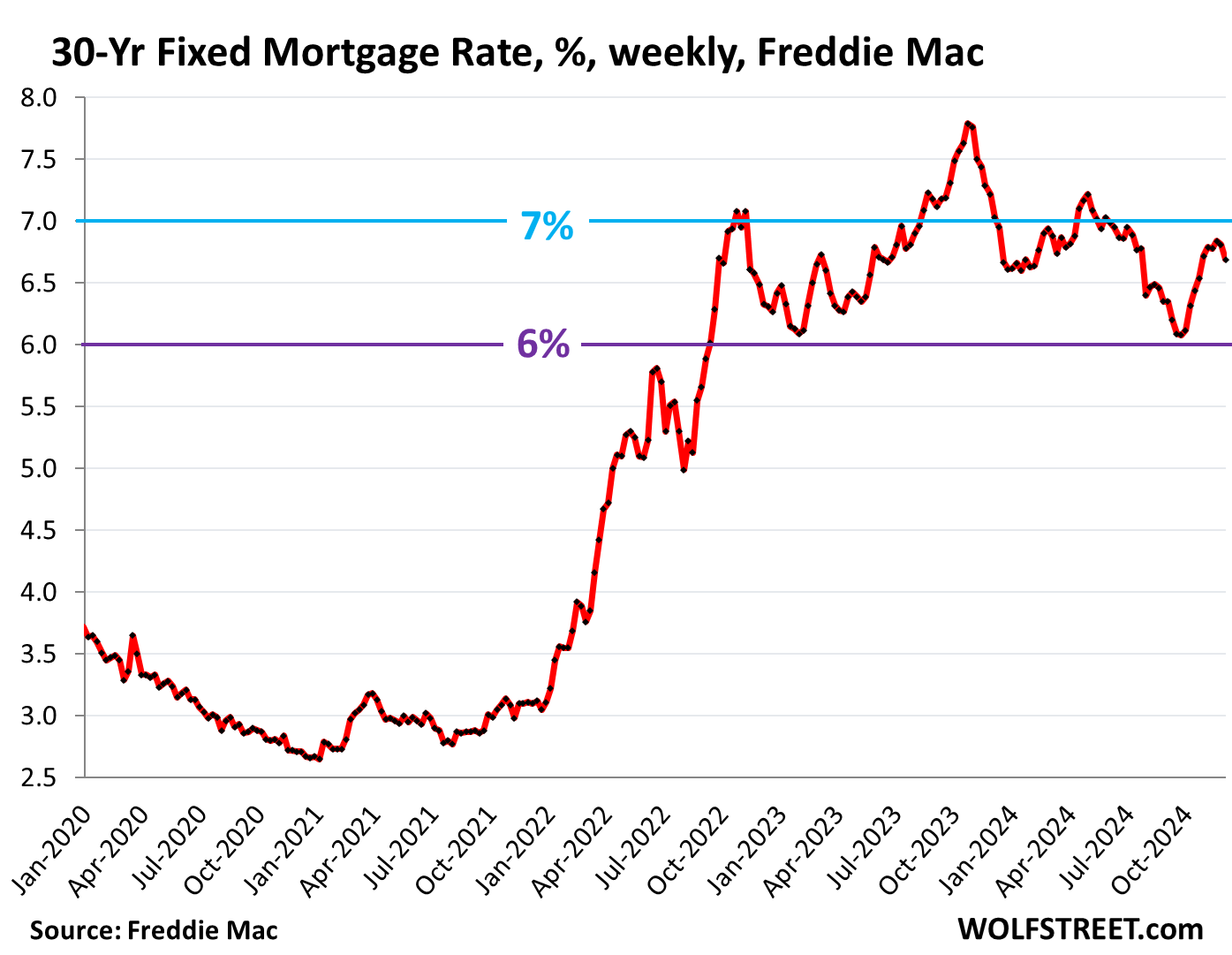

In the latest reporting week, the average 30-year fixed mortgage rate dipped to 6.69%, according to Freddie Mac today. They have been above 6% since September 2022.

“Consequently, recent [mortgage] rate increases might be better viewed as simply a return to historical norms after a relatively brief period of abnormal lows, spurred by a once-in-several-generations pandemic,” the Fannie Mae CEO wrote. And then she said, essentially: everyone needs to get used to those mortgage rates.

Then she went on to explain why mortgage rates are higher, and why they’re likely to stay higher, hitting all the points we’ve been talking about here for the past couple of years.

Mortgage rates are primarily influenced by the 10-year Treasury yield, but are higher than the 10-year Treasury yield because investors in mortgages, even in government-guaranteed mortgages and MBS, face additional risks and costs over Treasuries, including the risk of prepayment. When mortgage rates drop, and borrowers either refinance the mortgage or sell the home, that mortgage with the higher rate gets paid off, and investors are paid prematurely the remaining face value of the mortgage, and that juicy income stream from the higher rates ends, and any replacements will be lower-yielding.

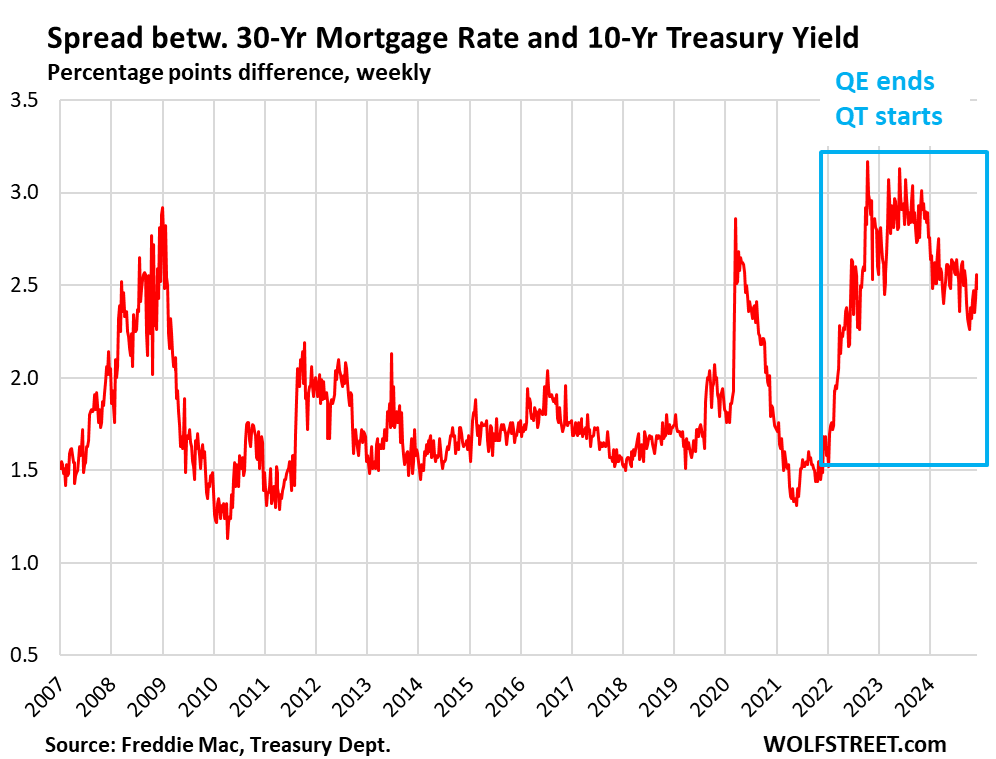

That difference between the 10-year Treasury yield and mortgage rates – the “spread” – varies based on a variety of factors.

And that’s also where the Fed’s QE and QT comes in. When the Fed engaged in QE by buying Treasury securities and MBS, it pushed down the Treasury yields and the yield of MBS, and therefore mortgage rates. In addition, the spread narrowed, and mortgage rates dropped further.

Since the second half of 2022, the Fed has been engaged in QT, shedding Treasury securities and MBS. Its balance sheet has dropped by nearly $2 trillion so far to $6.9 trillion, including the $500 billion of MBS QT. And the spread has widened over the period.

Today, the spread is at 2.48 percentage points, which is relatively wide. It went over 2% during the prior episode of QT. It then exploded in March 2020 as the market froze, but then was squashed by mega-QE. In 2022, with the announcement of QT coming, it began to widen again (blue box):

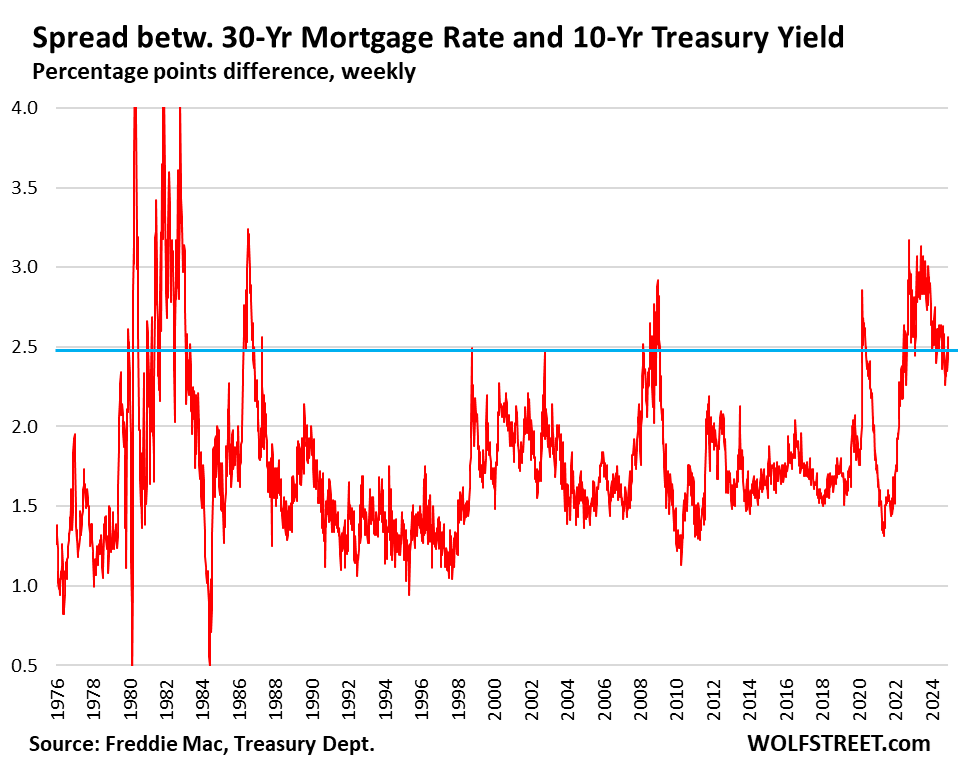

Here is the long view of the spread, which can gyrate widely when mortgage rates and Treasury yields diverge.

The spread could remain around the 2.5-percentage-point range because the Fed no longer supports the mortgage market, as it had done during QE, but instead is doing the opposite, letting its holdings of MBS run off at the pace of the passthrough principal payments. And the Fed said repeatedly that it would let the MBS run entirely off its balance sheet even after QT ends, and replace them with Treasury securities, likely with T-bills, which would take years and help keep the spread wider, all of which would put upward pressure on mortgage rates.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wonder if realtors will finally stop spending the “interest rates will be coming down soon” mantra.

Probably but they’ll just move on to the next sale’s pitch.

The last two years after rate hikes we’ve had the following from the NAR:

Date the rate, marry the house

There’s a housing shortage

There’s pent up demand so get in now before rates drop

Good houses are still selling. There’s inventory but not good inventory

The fed rate doesn’t influence mortgage rates so buy now

Can’t wait to hear the next one

Lol, the new Realtor mantra in Miami is “Just go find yourself a cheap rental, bud. You cant afford a house, nor will you be able to anytime soon.

Besides we dont have time to work with people who have to finance their purchases now that everyone want to cut our commissions. We have plenty of uber wealthy cash buyers.”

Exactly why wage increases need to occur as inflation rises. The interest rates will come down eventually but the constant increase in property value will keep homes out of reach for the proletariat, among other factors.

Here in San Diego, we just keep moving further from city centers, many people commute over 2 hours each way to work. Rentals are still crazy expensive too!

Good thing that the 7.0 magnitude earthquake in Eureka, California off the coast didn’t do any real damage to the San Francisco Bay area or other parts of California today and that the forecast tsunami didn’t happen at all at 12:10 today. That wouldn’t have been good for house sales.

you ever hear of the livermore fire station light bulb? i remember visiting it many years ago. it’s been burning for like 125 years or something crazy like that.

i always think of it when an earthquake strikes northern california.

The opposite of what you think is true. A natural disaster that destroys homes, raises rent and the value on the houses not affected in the immediate area. Supply and demand.

True. But on the other hand, when all the insurers stop offering coverage, it’s not so great for local real estate prices. See Florida and CA wildfire risk areas.

1:04 PM 12/5/2024

Dow 44,765.71 -248.33 -0.55%

S&P 500 6,075.11 -11.38 -0.19%

Nasdaq 19,700.26 -34.86 -0.18%

VIX 13.44 -0.01 -0.07%

Gold 2,655.10 -21.10 -0.79%

Oil 68.45 -0.09 -0.13%

I’d suggest that buyers have gotten used to them. Sellers OTOH…

In Canada over one million of the five year term mortgages come due in 2025. They were taken out when BoC rate was 1% and the 5 yr term less than 3%. So the new rates won’t be lower for those folks. One couple written up in Globe a few months ago were coming off a five year at 2.2 !

The best they could do now would at least double.

Just clicked on a pop ad, a rare event, for a mortgage offer of 3.49! from True North. That’s just for 3 months. I thought teaser rates were a US phenom from just before GFC.

Correction: 6 month term for 3.49

Looks like the Bank of Canada is constantly buying up 5 year treasury bonds in an attempt to drive down the rate so the 5 year fixed mortgage rate will fall.

Nonsense. These are repos, most of them are overnight repos, some have longer terms, and the collateral is Government of Canada bonds. The BOC has always offered repos to the banks. But when the system was flooded with money, there was no demand for repos. Now liquidity is much tighter, and banks are using repos for their daily liquidity needs, same as before the pandemic.

30Y Fix mortgage rate % : H&S ????

Homes are so last year I buy Bitcoin and GPUs now

Drawback of living in a GPU instead of a house: I hear GPUs are very hot and that people who live in them melt.

Should be fun to watch home sales remain frozen for another 3-5 years while rates sit around 6% as sellers refuse to budge. Guessing that won’t be positive for the birth rate issue. 😌🫡

Sellers wont sell unless they are forced to sale for multitude of reasons: job loss, relocation, divorce, death etc.

Some of my acquaintances are going one of the above.

Just the few reasons you just listed will cause a lot of sales. Many moves are initiated/caused by “life events”, not mortgage rates.

Is someone who won’t sell really a seller?

“Life Events” cause/force a lot of buyers as well. Marriages and child births cause a lot of forced buyers.

My college classmate just bought a house because kid was growing up and he had to move out of a rental in NJ. Paid through the nose because they were waiting for a few years and homes on market were very few. After losing bidding wars a few times, they paid over asking price and bit the bullet.

There are a lot of families that have been waiting to buy and move out of a rental.

Plenty of real estate is selling. We sold and bought homes with double digit interest rates and life went on. It might require more drinking and smoking for the working class, but if that’s you believe, load up on MO, their dividend has been outstanding for 40+ years, but then again drinking/smoking is the curse of the working class…

Ya got that backward WB, stop believing the propaganda nonsense:

” Work is the curse of the drinking class.”

Is the correct way to phrase that, and I can testify to that being correct after having worked for enough years to be rid of that curse.

Please read WR’s other real estate posts. Plenty of real estate is selling, but prices are coming down in most locals, and that’s what we want!

“those inflated home prices are now the biggest problem in the housing market because it’s choking on those too-high prices and sales of existing homes have plunged to 1995 levels because prices are too high.”

Mortgage rates won’t go below 5% again in your lifetime (I think I said that before at least a year ago).

Everyone on the internet thinks that trend changes occur immediately and catastrophically. Rates will remain elevated, and over time, sellers will adjust. It won’t happen everywhere, all at once – it will, however, happen.

According to Fannie Mae, it won’t happen in 2025. They adjusted their mortgage rate forecast to higher rates, but reiterated that home prices will continue to rise (by 3.6%) in 2025. Same as all the other “expert” forecasts.

No one in government or real estate is every allowed to forecast a decline in home prices.

I would love to see mortgage rates at 10 or 12 per cent. Once we get going with super sized inflation in the next four years, I expect that sky high mortgage rates will be the trigger for the complete collapse of the housing market. Sellers will rue the day they held out for their dream price. Think it can’t happen? It has happened before and it will happen again.

Agree totally E:

Been there and done that twice!

First house purchased, as opposed to built, was $40K with 1st mortgage at 18%. (Last sold for $800K.)

Penultimate RE, land, purchased was $2K/acre, now $12K.

Last house purchased was $80K, now allegedly $360K.

Location Location Location

I think we need 10-12% again just to reset expectations and make everyone grateful and happy again.

Let me explain.

When I bought my first house in the late 80’s in S. CA, with an 11% mortgage, I did it partly because house prices were still exploding up due to high inflation. I had a bad case of FOMO.

When rates fell to 7% during the mid 90’s, I was so happy and exuberant that I went out and had 3 kids with all that extra money from the refi. My expectations were reset into happiness.

We need that to happen again. Everyone will be happier.

I remember people saying in the late 70s and early 80’s, money would never drop below 12%. In 87 I bought a nice little rancher on 1/2 acre with monthly payments below local rents, and the asking price was just 2X my yearly salary. It was a for sale by owner with a price drop after the listing ran out. I drove by and saw the hand printed sign on my way to look at another place.

And now, after 2 decades of low low rates, look where we are.

Housing prices will eventually drop and sellers will just have to adjust their expectations. Of course how long this might take also depends on when owners bought and for how much, but the market will set the rules going forward, and not the sellers or agents. It is criminal how hard it is for young people to afford housing. Hopefully this situation will adjust over time, but I have little to no faith that it will considering the interference on just about everything these days.

… and no disaster shall ever strike, no wars, no recessions, can’t imagine a reason why rates would ever drop again… 🤦

There was 15 years between the last two recessions.

“can’t imagine a reason why rates would ever drop again… ”

Neither can I, and none of the things you listed justify cutting rates. Natural disasters? Really?

I realize you didn’t specify /natural/ distasters but the thrust of my comment still stands. Vague and undefined disasters have nothing to do with central bank interest rate policy.

Beautiful inverse H&S pattern forming on TLT……..🤔

Here’s a way rates can start to drop. A friend or relative brings up a worry he might be losing his job, followed by that friend or relative losing his job, followed by you start to worry you might lose your job, followed by you losing your job, followed by a friend or relative losing his house through foreclosure followed by etc etc. You then read unemployment in your area is well in to double digits. Rates will start to come down shortly after that. What is not known is what rate they will start down from. That could be a double digit number itself. Read the history of the early 80s for more information.

Yes, all it will take is another pandemic slightly more deadly than Covid. Bird Flu? Ebola?

QE and interest rate slashing will happen again. The question is when.

Powell has repeatedly said we’re not going back to the era of low rates (which preceeded covid).

BobE,

Don’t equate cutting rates (normal) and QE (experimental radical).

This stuff is really funny. The Fed has been shedding assets for two years, and it shed $2 trillion, far more than anyone thought possible, and all you people are doing month after month is fantasizing about QE. We want our QE back. The Fed’s going to do QE again!

I’m getting really sick of this BS, after two years of having to read it here every month.

“QE (experimental & radical)”.

Wolf, Appreciate you pointing this out as so few on Wall Street, Financial News, the Government and certainly not the Fed have.

I think it will be a long time before investors regain an healthy appetite for mortgages. I was surprised the spread vs 10 years is still so small.

“In fact, the average 30-year fixed mortgage rates were never below 5% in the data from Freddie Mac, which goes back to 1971, until the Fed started buying MBS in January 2009, which pushed mortgage rates below 5% for the first time ever.”-Wolf

Nice to see some historical perspective, rather than the usual hysterical perspective from Wall Street. Most Wall Street “experts” are so so so worried about the current “high” fed funds rate. (Yes, I know everyone wants cheap money, but they don’t seem to want to think about a semi-paralyzed housing market and double digit inflation).

The average fed funds rate 1970 to 2022 was 4.90%. 1955 to 2022 it was 4.62%. Before ZIRP started in 2009, from 1970 to 2008 it was 6.45%. Somehow the economy survived these numbers. Certainly lots of ups and downs, but on average the US economy has done pretty well since 1970. Current one-year t-bill yield is 4.47%. We are already seeing resurgent inflation within the context of a strong labor market. So what will the imbeciles at the Fed do? Why they will lower rates again, of course.

Ha, most wall street folks (not media mouthpieces) could care less about high rates. They are all involved in private equity now. Private equity credit and private equity for the dumbass little guy is the latest game.

They are making so much money, there is now a SHORTAGE of $10,000,000+ homes in Florida for them to buy (without mortgages).

Besides, Blackrock just announced we are in a new transformed world economy where boom and bust economic cycles (think recessions) will no longer exist.

“… simply a return to historical norms after a relatively brief period of abnormal lows, spurred by a once-in-several-generations pandemic” —Fannie Mae CEO

This statement seems ambiguous. It says that the “abnormal lows” period was post pandemic, but dismisses the abnormal lows for 11 years (sub-5% from 2009 to 2020), ignoring that rates were equally problematic and abnormal. (And “housing bubble” blowing really began shortly after the tech stock disaster in 2001, so the entire 21st century up until 2022 was arguably a period of “abnormal lows.”)

At least 12 years of mortgage market and treasury rate manipulation have brought us to our current housing bubble situation. If Newton’s 3rd Law has any bearing, the unwinding promises to be hard, lengthy, and disruptively painful.

It’s only ambiguous if you cherrypick it out of context. It’s not ambiguous within the other things she said, including:

“In fact, current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades. Since 1990, the 30-year fixed-rate mortgage has averaged 6%.”

Point taken.

But isn’t her claim, “Since 1990, the 30-year fixed-rate mortgage has averaged 6%” also “cherry picking” by omitting years 1972 to 1989 in your first chart?

Just eye-balling it, that would put the average closer to 8%, it appears.

COVID along with the feeling of entitlement killed the desire to work. Our history was built on the premise of work hard, spend and save wisely, and receive a wage that allowed for growth. Like any program that involves the mindless meddling of unequivocal inefficiency the power of the free market controlling the cost of goods and services is skewed to those who control the pursestrings of the program. In my lifetime of 70 years I have yet to see a government controlled anything ran efficiently and benefiting those who have to utilize their services. Pick any government regulated program from housing, healthcare to social security and it always has been and will continue to be in turmoil. Like it or not we live in a feudal society where the powerful kings and queens of government along with their bureaucratic jesters literally control what we say, the platform we say it on, and the percentage of crumbs that is allowed to fall off of their table of control that we are allowed to utilize to live our lives. We are approaching 250 years as a nation established on the idea of freedom to control our own lives and destiny and sadly in the past 50 years those freedoms have been slowly stripped away by a class of individuals sadly put into power by us who truly do believe they and they alone know what is best for us, in reality it’s what benefits “them” the most. They may call themselves D’s, R’s, and I’s but in reality they are all greedy, addicted to power, and mired in the quagmire they have created for their own well being.

@Wolf

Curious on your perspective of the US’s fairly unique ability to prepay mortgages. It’s the only country I know of that allows paying back mortgage principal in advance to dismiss the loan vs prepay including contracted interest revenue.

Is it good for the housing market? Our economy?

No, I think this is a universal feature of mortgages just about anywhere, that borrowers can pay off the mortgage early, or else people wouldn’t ever be able to sell their homes within the term of the mortgage.

But what’s unusual in the US is that the 30-year fixed rate mortgage is standard.

In countries where adjustable-rate mortgages are the norm, any fixed-rate mortgage terms typically impose a hefty fee for pre-payment to offset the bank’s loss due to prepayment. This is the case in all of the EU, UK, and all of Asia that I’m familiar with. It’s part of why fixed rate mortgage rates are lower in the EU than the US–less prepayment risk.

Obviously with adjustable rate mortgages there is no prepayment risk, but it’s odd that in our fixed-rate heavy mortgage market borrowers can collect the upside, but not the downside when rates move in their favor and creates this “lock-in” effect. Seems like a loophole from a time when folks didn’t transact housing as frequently.

What ever happened to the 20 year mortgage ?

Same thing that happened to the 3 year car loan.

I think you can still get a 15, 20, or 30 year mortgage. The last time I refi’d 4 years ago, I was even offered a 13 year loan since I didn’t want to reset my retirement plans. In retrospect, I should have taken the 50 year option at 3% and invested my monthly savings in TBills. Crazy Times.

I noticed at the time, that 15 year and below mortgages were about 0.5% lower than 20 and 30 year mortgages.

The biggest problem is the grossly overpriced housing market.

If history repeats itself then the GOP will cause another recession and you will see lots of foreclosures, and home prices and interest rates will drop drastically.

The rates have gone up and down over the 25+ years that I have been in the mortgage industry and it will continue to do the same thing. Throughout those years, there were many times that the rates hit the lower 3% (Apr 3.255%) range for an 30 year mortgage and we will have it again. Once our energy prices, food prices, and major government spending come down, rates will come down too. Jerome Powell stated recently, due to Covid and the major government spending, it caused the inflation that we have had for the last 3-4 years. The more cuts that are made, the better the economy will be.

LOL. You’re just trolling for the ravenous mortgage industry so you can get rich off homebuyers and home-refinancers. You just want mega-QE to come back so that you can get 3% mortgage rates so everyone will refi, and you get rich, LOL. You people are praying to the god of QE every day, and he just doesn’t listen. does he? Frustrating isn’t it? You people would sacrifice your firstborn on the altar of QE so you can make more money.

Some will imprison themselves for the next x years just to find out that they weren’t able to do better than current mortgage rates.

Eventually current rates will become the new norm and people will find a way to accept and move on…

Asset prices WILL deflate.