Inventories are piling up because prices are too high. But they’re coming down.

By Wolf Richter for WOLF STREET.

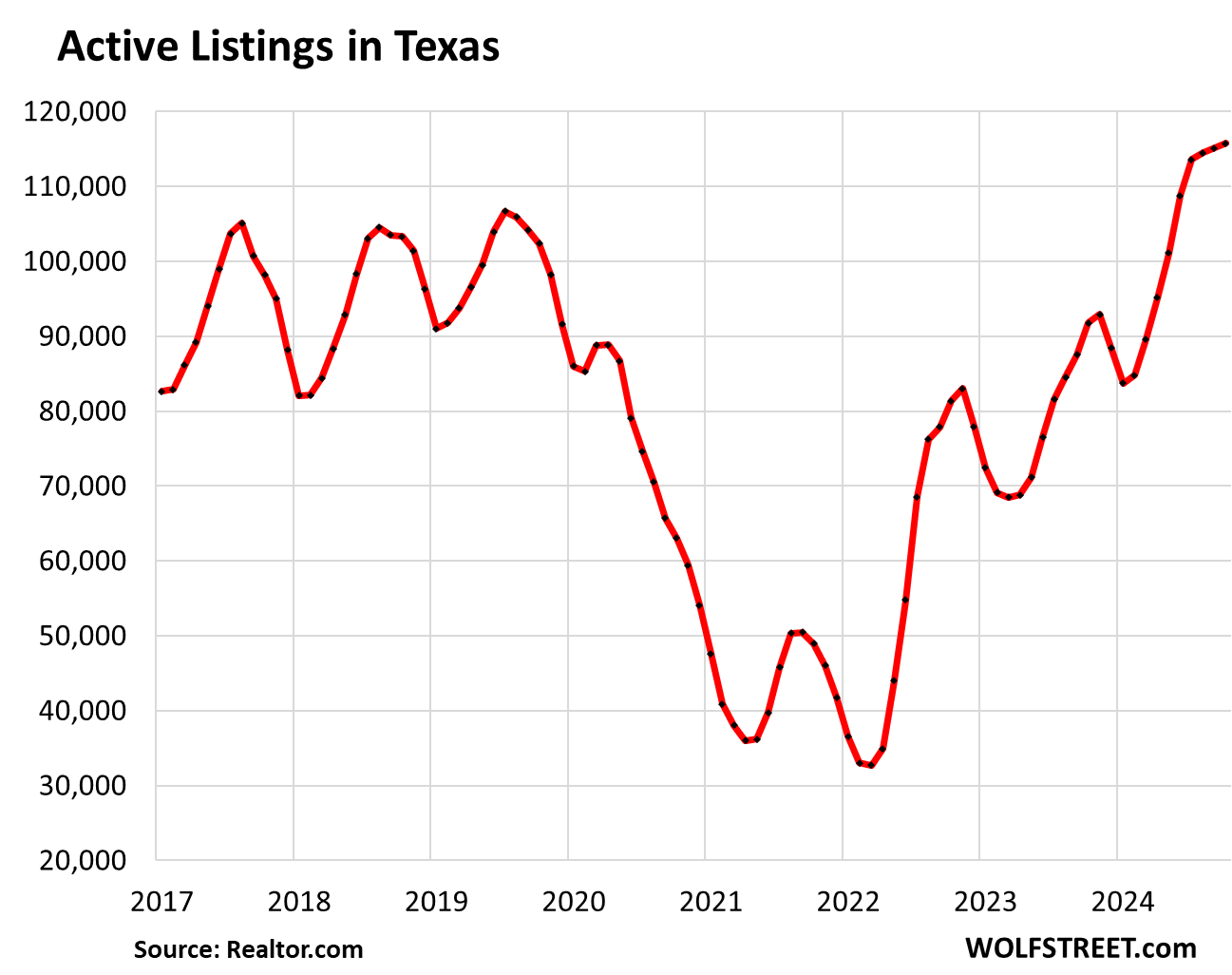

The housing market in Texas just hit another multi-year record of sorts: Active listings reached a new high in October in the data of Realtor.com going back to 2016. New listings are showing up at about the normal rate for this time of the year, but sales are lethargic despite dropping asking prices – prices clearly haven’t dropped enough – and so the inventory keeps piling up and going stale.

Active listings rose to 115,739 homes, up by 28% year-over-year, up by 42% from two years ago, and up by about 13% from 2018 and 2019 (data via Realtor.com).

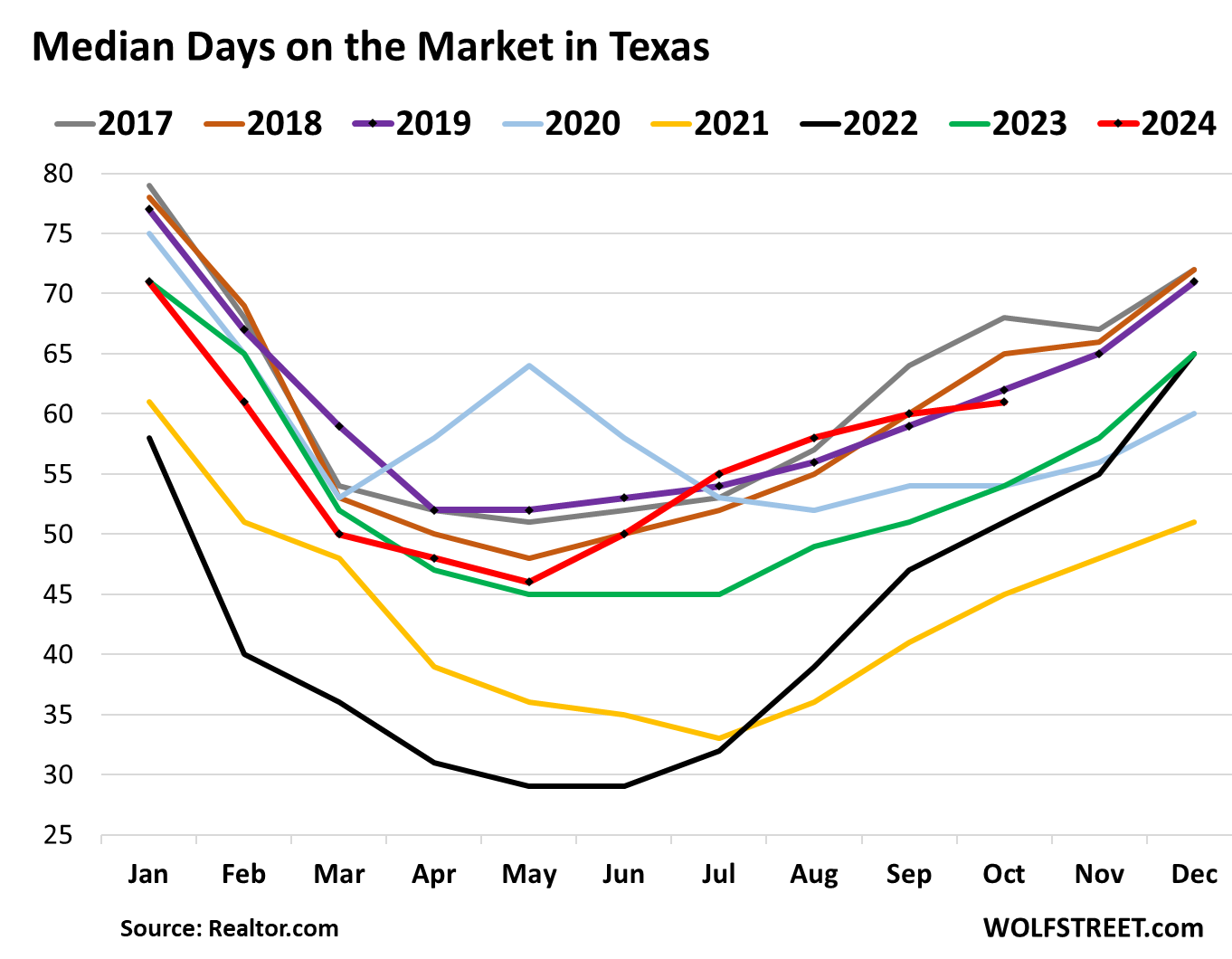

Median Days on the Market drag out.

The median number of days a property sat on the market for sale before it either sold or was pulled off the market in seller-frustration rose to 61 days in October, the most for any October since 2019.

This metric is a result of:

- How aggressively sellers pulled listings off the market without sale;

- And how fast properties sold that did sell.

When sellers get more motivated, they leave the property on the market longer, rather than pulling it off after a few weeks if nothing happens. And they might try reducing the price until it sells. This causes the median number of days on the market to lengthen.

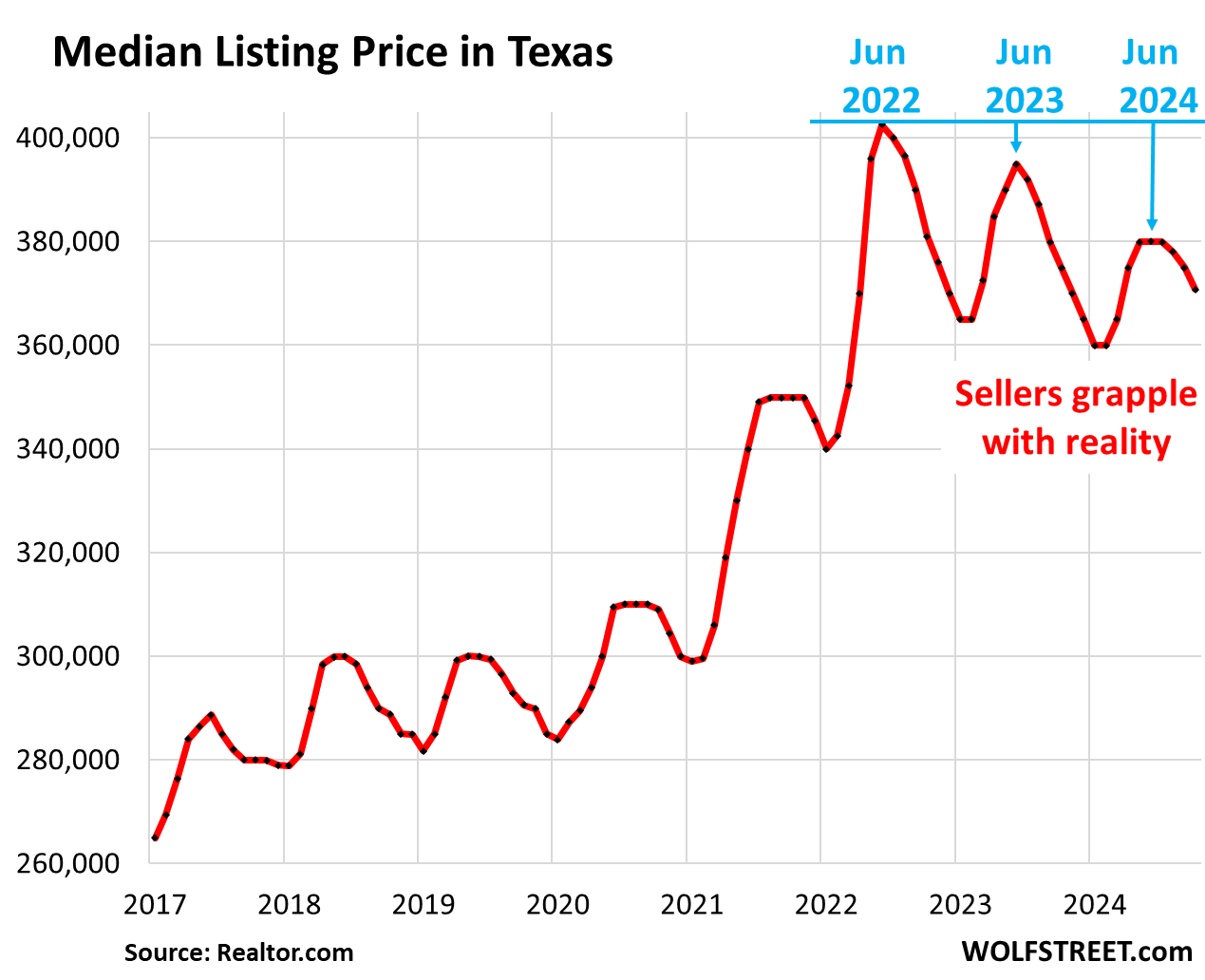

Inventories are piling up because prices are too high. But they’re coming down.

Just about anything can be sold if the price is low enough. But many sellers still want their aspirational prices, and so they pull their vacant home off the market, hoping that this too shall pass, and pay the substantial carrying costs of a vacant home, especially if leveraged, rather than list the home at a price that is low enough to sell.

Listing prices are prices that sellers imagine. They’re not transaction prices. Transaction prices are set by buyers. In the major metros in Texas, transaction prices have fallen to varying degrees. More in a moment.

The median listing price in Texas dropped to $370,700 in October, down by about 2% from a year ago and down by about 3% from two years ago. Compared to the seasonal peak in June 2022, the median listing price is down by 7.9% (data via Realtor.com):

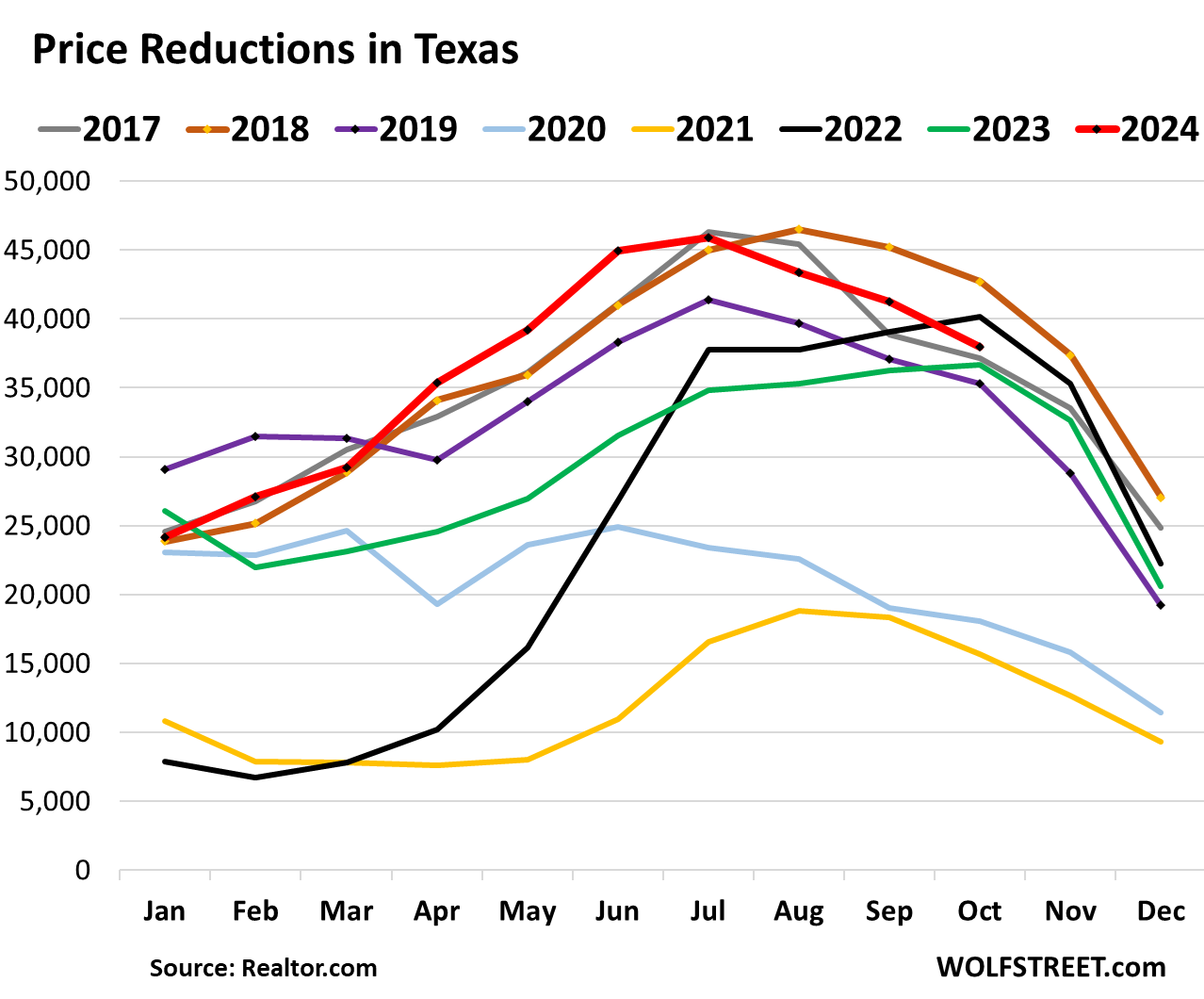

Price reductions trim too-high listing price.

In October, there were 37,984 listings with price reductions in Texas, the third highest for any October in the data by Realtor.com going back to 2016. Only the Octobers in 2022 and 2018 were higher. Obviously, as we can see from the inventory pile-up, these price reductions are not doing the job.

Listing prices need to be attractive in the first place, and when they don’t catch, price reductions need to be bold and stand out in this field of competition, because there is a lot of competition now (data via Realtor.com).

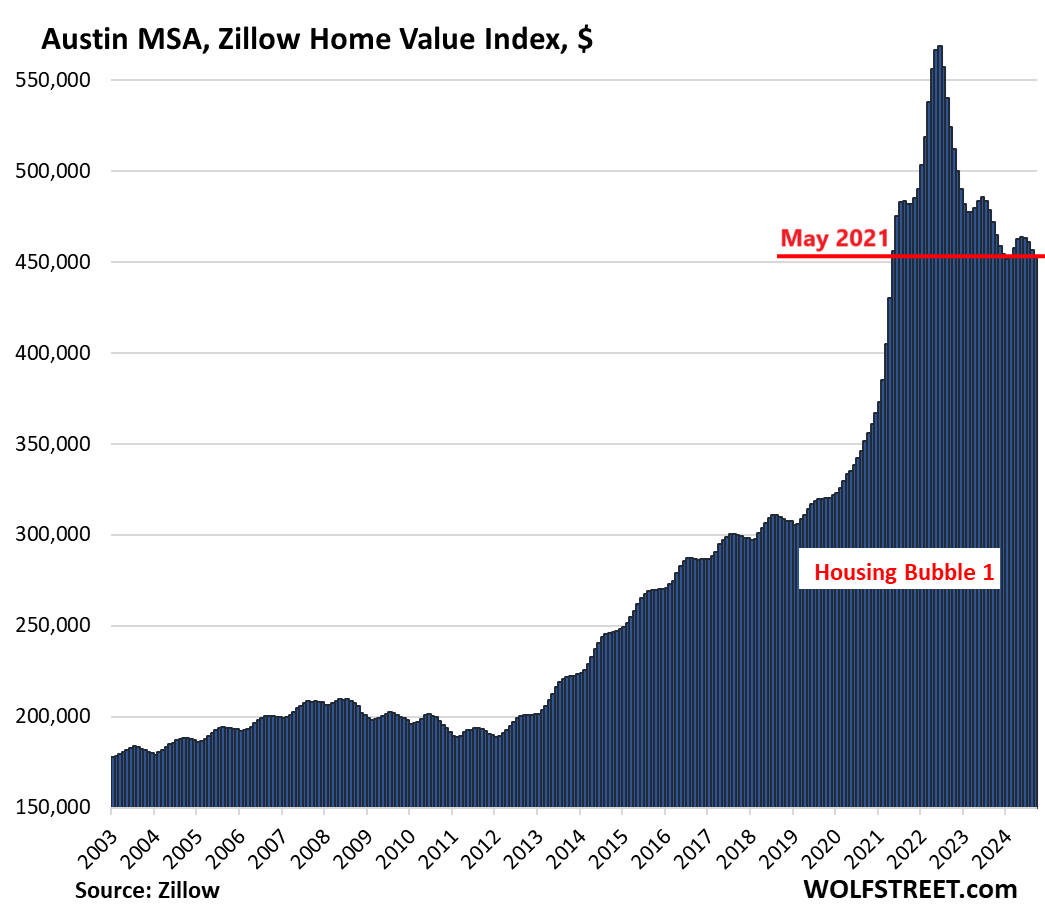

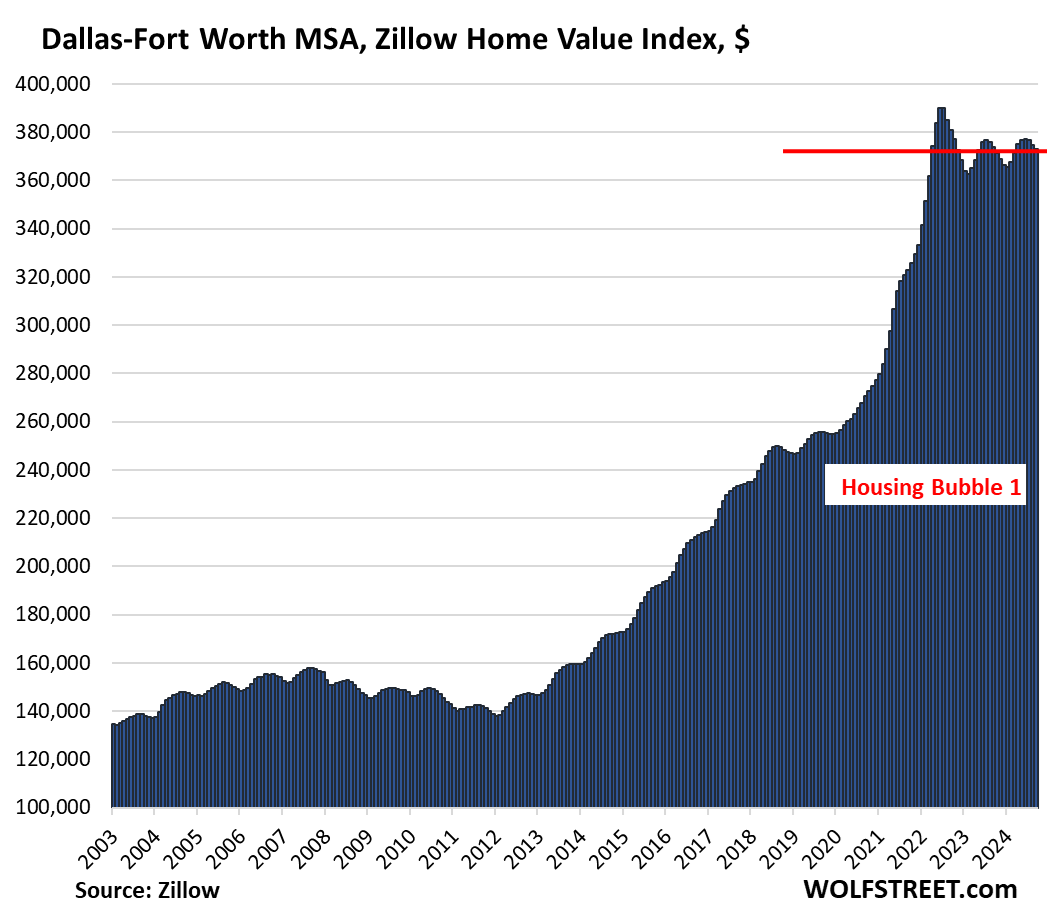

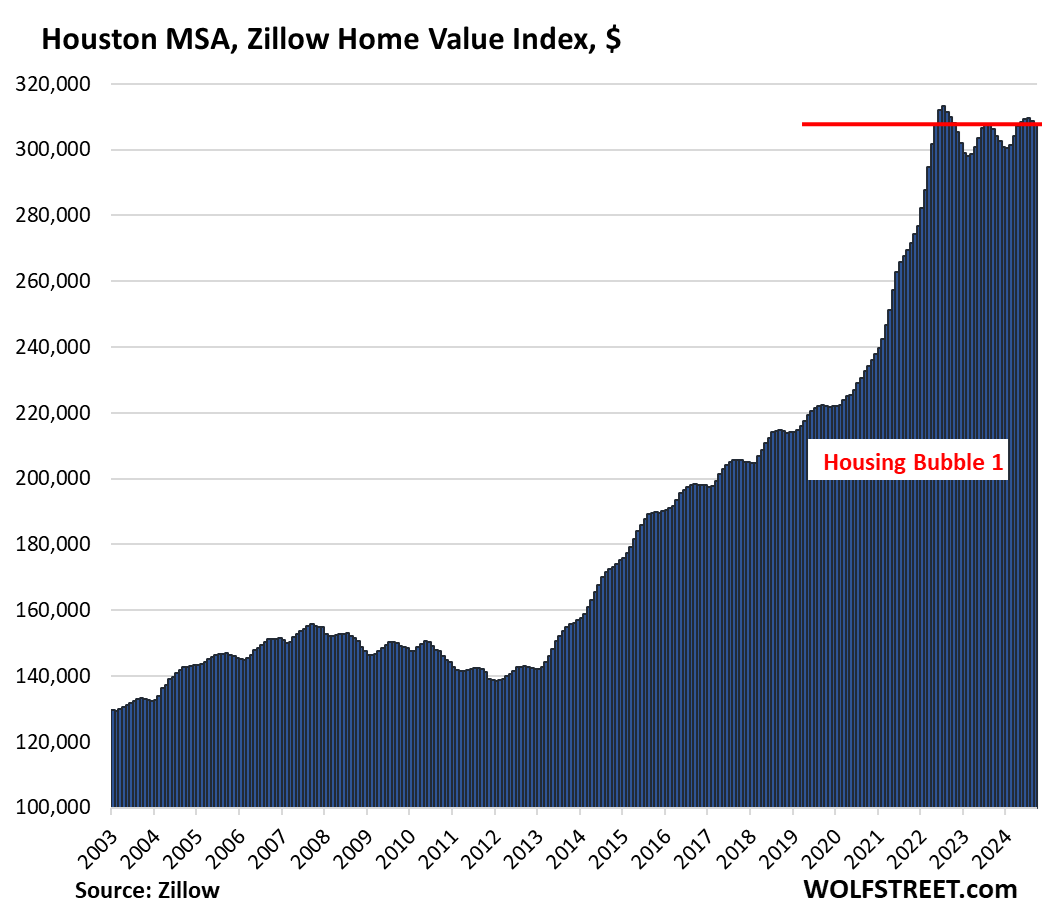

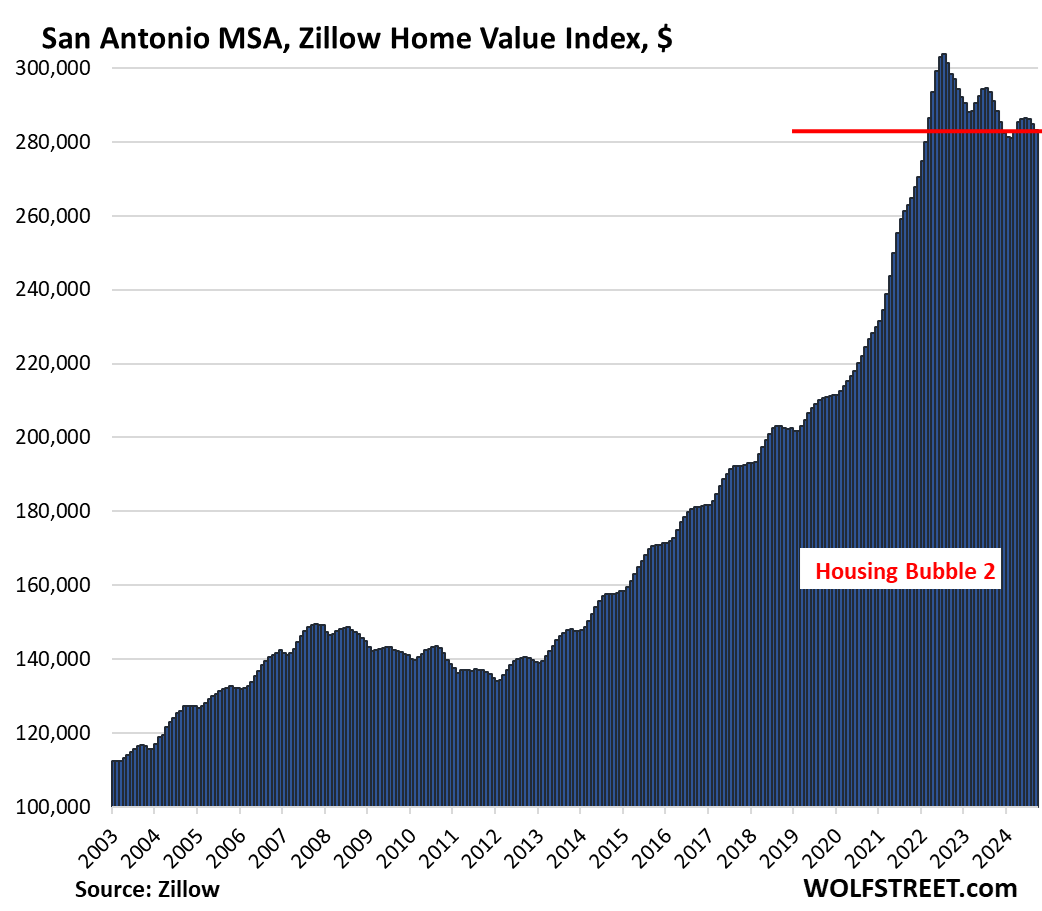

Transaction prices (closed sales) for the major markets in Texas have declined, in some markets more than in others. The October prices will be released in a week. Here are the transaction prices through September, according to data from the “raw” Zillow Home Value Index (ZHVI), which we feature in our Most Splendid Housing Bubbles in America series.

Austin metro: -4.0 year-over-year, -20% from the June 2022 peak, and back to where it had been in May 2021.

Dallas-Fort Worth metro: -0.3% year-over-year, -4.4% from the peak in June 2022:

Houston metro: +0.4% year-over-year, -1.9% from the July 2022 peak

San Antonio metro: -2.7% year-over-year; -6.8% from the July 2022 peak:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Excellent. It’s lovely to see that Texas and Florida are moving the needle in the right direction. Hopefully, by next year, this will accelerate, and the same thing will happen in SoCal. This is wishful thinking, but I’m crossing my fingers for now. I’m really hoping there’s not any recovery of demand when people all of a sudden hop on the rate cut is coming train like we experienced earlier this year.

Just a question, because I’m always confused by your comments. Are you hoping prices come down because you want to buy a house?

Sure, when the price comes back down to earth and you pay the steak price and get a steak. Where I am at, using analogy, right now at best you pay Wagyu price and get a frozen ground beef patty and that to me is unacceptable, I am ok waiting it out and enjoying the show with some level of indifference and disdain..if it doesn’t go down ever then so be it and deal with “missing out”

Boy, you must be fun at parties. Your post is full of opposing views.

If the economics of the housing market where you are are “unacceptable” to you, then move. Find a place you deem the math “acceptable”.

Living life with “indeference” and “disdain” sounds miserable. Hopefully things get better for you.

Moving isn’t always an option or a solution. Being frustrated because homes are less affordable than ever before isn’t inherently wrong, it’s just acknowledging that the system is failing us. Everyone moving to cheaper areas isn’t exactly the solution here. The solution is avoiding reckless policies so the mistakes of the past don’t get repeated. Sometimes the people that are the most fun at parties are the most dumb and reckless. That you, Nunya??

Nunya is just going through difficult times so he’s taking it out on you. But I’m with you. I am indifferent to this property bubble caused the 1) Fed and 2) Administration and 3) worse having no sympathy for all the FOMO lemmings inflating homes at the peak. I was about to buy couple years ago but just looked at the stampede of home buyers and prices and said “call can have it all”. Now they know what I mean but this time I’m waiting for 50% off after unemployment snowballs.

I love parties, they’re fun.

Not reckless at all, not going through any difficulties either. I’m not in the housing market for my primary home, so I’ve got a different lens. I sold two homes in 2021 (primary and rental property), moved to a different state (job relo) and bought an off market home. The home I bought was much cheaper than the primary home I sold.

I am in the market for investment properties, so that just requires patience.

If that wasn’t sarcasm, Nunya, yes. He’s hoping for the best for himself and the not-so-good for many many others who he feels have screwed him. There are many in that camp, and I’m of pretty much the same feeling, and about equities, too. I just don’t talk my book quite as much. ;-)

Not sarcasm at all. Just genuinely wondering what Phoenix’s end game is regarding the housing market. The answer given still doesn’t answer my question, but I was just curious.

End game? Why would one not want a bubble to deflate except the foolish who jumped on the bubble hype. The giant run up in home prices is only paper money for most. If you sell your $1M home to buy a new $1M home it’s the same as selling your $400k home to buy another $400k home. You still have no new cash. In fact you’re poorer because that’s a lot more debt to finance at higher interest rates (unless you’re paying cash). However, you are paying significantly more at $1M valuation for home owners insurance and property taxes, which is problematic for many of fixed incomes. The only people who benefit from the run up in housing prices are investors, which no one feels bad for.

People do sure love to look at their Zillow valuations and feel good though.

MM1,

Wow. I’ll channel some inner Wolf. WTF are you smoking?

Your scenarios make sense only when you keep your absurd assumptions. I can flip your same scenarios on their heads with a different set of assumptions (equity/interest rates/down payment/tax rate based on different locales/insurance based on different locales/etc.)

At least Phoenix can have a dance partner at the misery dance with you.

You miss the point. When the whole market goes up, you’re not richer. Everything is just more expensive. That is the inherent concept of inflation. So your house goes up in value, but so did all the other houses. Shelter is generally a basic need, so you can sell one overpriced house and make a big equity gain, but you’re now just buying another overpriced house with that equity because the other houses are equally overpriced.

I specifically said this does not apply to investors who own multiple properties. But for the average American who doesn’t want to relocate to a totally different market and needs a place to live. Having a home run up in value when every other house in the market went up the same % doesn’t actually do anything for them – they’re just paying a ton more in property taxes and home owners insurance.

Maybe a more simplistic way of putting it is, you only made money if you can sell and realize those gains, obtain comparable shelter in that same market, and have money left.

Yes I do realize you could switch to a different cheaper market to make a large profit, but most people aren’t wanting to switch jobs, uproot their family, and move so I’m using a single market example because I’m talking about the average american.

So yes, I standby the most people are only paper rich argument. Also no need to be rude just because you don’t understand a concept.

Been following Mitch Vexler’s advocating regarding the massive issues with property taxes and CADs. He started with TX but appears to be a nation wide issue.

This issue is amazing. When I moved to Texas and saw what my CAD was doing, I hired a protest company to protest my taxes, provided photos of the house, etc. This dropped my valuation way down compared to neighbors. Next year will be 4th year in a row of protesting and every year it goes down.

Their “market analysis” approach may hold up in court though as the burden of proof is extremely high.

Good luck! TX and other states like it have crazy prop tax rules. Why should a home’s value have anything to do with the tax you pay?

Good luck to others hoping for XYZ to change or happen or go “in their favor’. This is poker. Play the cards you were dealt which means bet on yourself, bluff others, or fold. The greatest part of it all is this is America, so you get dealt a new hand the more you play.

Because, as Mitch uncovered, they are not using the official appraisal guidelines to appraise home values, instead they are basically being told by the school boards what the schools need to meet budget/cover the bonds interest, then going in and fudging the #’s based on that.

Rough explanation but the truly insane aspect is, no one seems to know how much is owed in these municipal bonds, they just keep taking more bonds out. The districts are essentially bankrupt and hiking property taxes to kick the can down the road and cover their arses.

Awesome! Keep fighting. Apparently, if you don’t protest a tax increase and just pay it, they will use that as evidence the following year that you accepted their valuation of your property.

Pardon the emode, but I have never been more grateful to have passed on numerous accepted offers in ’21-22 on gut instinct before getting priced out and stuck renting. Whined and omplained non stop at first, but now I’m learning more about economics and RE then most homeowners I know (thanks to sites like Wolf’s and others I’ve been following). When I’m finally ready to jump in, I’ll be on much more solid footing than the FOMO crowd was.

You are over the target on the CADs. I was an appraiser at the Dallas Central Appraisal District in the late 1990s. I was told we did “mass appraisal.” If I couldn’t get values high enough (for an entire neighborhood) for my supervisors’ approvals, I was told to “up my number” by tweaking one critical “number” (multiplier). It was crooked. I was the one who signed off on the neighborhoods….I quit. Any honest would. Most appraisers had been there for years and decades, complying, knowingly, with the tweaking of the Tax Base value. Of course, it ALWAYS increased.

I’ve mentioned this before….the new home builders near me (Lennar and others) have dropped the prices of their new builds 10% across the board. And they are STILL offering loan buydowns for two years @3.99%.

Doesn’t make me feel too good as I bought a new small home 16 months ago, but, then again, where I was living before I moved here is dropping in price too. I did sell that house at the top of the market at that time so I’m just giving a little of it back! LOL!!!

A house is a place to live as that’s been my game plan for the last 5 decades plus!

For the record, I am north of Houston, Texas about 50 miles or so (Conroe).

Only in Texas and Florida, one can only wish anywhere in Cali this is happening at all…

Btw, IMHO I still think there are wayyyy too many people who still think the return of low mortgage rates to 3% is a thing and that’s the only opportunity they will have ever to afford to buy, people need to wake the F up and disregard mortgage rates as the equalizer and continue, if not ramp up effort in boycotting these ridiculous prices and let price alone be the incentives to bring buyer’s demand back. I know as a whole, this sagging buyer’s demand is showing that but perhaps not all markets, I can’t tell you how many in my neck of the wood still glaze to the star hoping for the return of 3% rate so they can finally afford that tiny crappy condo for $1M, meanwhile not questioning even at 0%, that condo should never be worth $1M to begin with…

There are plenty of affordable areas in California or at least in comparison to the Bay Area and Southern California. They aren’t terrible places to live and you get all the seasons. 600K will get you a 2000 sqft house in a decent school district. A friend just moved from SoCal to Roseville for just that reason.

I view a house as an inverse annuity: instead of providing a fixed monthly income, it sets a fixed monthly housing cost.

“Compared to the seasonal peak in June 2022, the median listing price is down by 7.9%”.

Just another 30-35% to go. With the 200 year average correction being 4.6 years, the bottom should arrive at the end of 2027.

Then again, the past two corrections (89-96, 06-12) took 7 and 6 years, respectively.

So 2028 or even 2029 are still in play.

Just a wild food for thoughts….last time, home prices also didn’t rocket up 30-40% in matter of 2 years so perhaps the trajectory downward might be just as violent….wishful thinking again but this cycle is abnormal in many aspects..

This is what gets me. See the Austin chart it’s down 20% from the June 2022 peak but still almost 50% up from 2020. Inflation doesn’t justify that.

I’m moving and I’ve decided to rent. The rental market is almost equally weak; I was offered a 2bd2ba rental for $1600 with 6 weeks free for a 12-month contract. That’s not bad but I’d prefer to set the rent at $1500 instead of the silly incentive games. I’ll hold off another month if I can and there should be more weakness as long as the Fed holds steadfast on QT, methinks.

Depending on the outcome of tonight’s election we may see JPow cave in to loudmouths on TV yet again like in 2019 and screw this further.

@DownWithRE: Someone connected closely to the Austin real estate told me that there are about 60,000 new apartments coming to market in the near-term.

You might want to check this out, will give you more negotiating leverage of this information is accurate.

I would be ready for A 90% drop ,history repeats .but most people prefer to play video games instead of . Paying attention to what’s really happening

Just 15% would stop the hedge funds from buying up normal houses. Bring it on.

Almost step for step, housing prices and stocks spiked upwards to bubble peaks — houses are falling a little, as stocks remain resilient, but I seriously don’t see that as sustainable — except in the minds of delusional, speculative minds.

Only an idiot would dare speak of recession for next year, so instead — I’d suggest that along with a buyers strike in housing, we see an increase in equity earnings declines — across virtually every mkt sector.

IMHO, the Buffett Indicator and Warren’s recent portfolio adjustments are a very simple wake-up call for what’s soon to be ahead.

It took four years to get to this bubble level and it’ll take years to unwind for houses and stocks.

If Trump gets elected, if we’re getting a recession in the next 4 years it will happen in year 1. If it doesn’t come in 2025 I don’t think it’s coming at all. That way he can blame the predecessors and come out as the hero.

It seems both parties don’t want a recession going into an election and will prop the economy with whatever spending it takes, so I feel like 2027 and 2028 are off the table for recession regardless of who wins.

The “if” is settled.

The Buffett Indicator is currently in the danger zone, which seemingly is at odds with the no recession / soft landing narratives — that have been goosed by excessive fiscal stimulus.

That conundrum sets up a very awkward series of events, with more (unnecessary) rate cuts, a juicy end of year Santa Claus rally— then tax cuts, tariffs and massive deficit growth — and apparently, a yuge explosion is stock prices, as earnings growth expectations are falling.

It’s an incredibly unstable six months ahead — and, meanwhile with all that coalescing — we have a nice spike in home inventories with a buyers strike — as mortgage rates head far higher!

It’s an explosive disconnect that’s underway — the Buffett Indicator is pretty decent at smelling out mkt tops and inflection points, and I think it’s indirectly going to start calling attention to inflation picking up pace.

I think it’s somewhat ironic that trumps landslide victory is apparently a referendum that’s focused on “the economy” and juicing markets and firing up growth — but, the mass hallucination that the economy is in bad shape, isn’t expressed in the Buffett Indicator — so, a real head scratcher, as how we go from this dangerous level of excessive overvaluation to the next higher for longer range.

Stock valuation is insane and not based in reality, and housing remains massively unaffordable — as mortgage rates higher — which shines the flashlight back on income growth again and again ….

And finally, The Buffett Indicator kinda implies, if I’ve read Warren correctly, that if stock valuation stays at this level, GDP would have to double, in order for stock values to appear to be fairly valued — chances are extremely high, that GDP isn’t going to duh moon! I’m betting every penny I have on that!

Disclaimer: it didn’t matter who won, this is just an epic train wreck ahead imho.

Yeah I wasn’t necessarily saying it matters who won. The same fundamental issues exist. I just meant no one wants a bad economy going into an election so they’ll spend to prop up the economy IF they can – so the last 2 years of a 4 year term are unlikely. With a switch in administrations, it’s really easy to let some problems happen/shake out in the first year and blame it on the previous administration. But yes – we’ll rally here for a bit for a lot of reasons and have a Santa Claus rally.

Stock market up and a ‘better’ economy though will be inflationary. I wonder how long before the market realizes that. I don’t think there’s a way to kill inflation while making individuals better off, I think they need to allow a small amount of economic weakness at this point, with a stock market correction (i.e. normal 20% not saying it needs to implode down 50%), and some softening in house prices – people who bought in the last 4 years shouldn’t be immediately selling anyways and people who bought 10+ have enough equity that a 10% drop shouldn’t impact them.

Equities are poised for a downturn based on demographics. The retiring boomers will need to start draining those 401K’s, which means they are net sellers not net buyers. The biggest things moving the markets higher were passive investors and the dwindling pool of stocks to purchase. Going forward the demand will be lower for equities.

Two quick observations in prices:

First, if you assume a home increases in value at roughly 3.5% per year, and start with a value in Texas of approximately $265k in 2017 (eyeball estimate from WS’s chart), the future value after seven years (2017 to 2024) would be approximately $337k. This compares to a current approximate value of roughly $370k (again, eyeball estimate) which indicates a price difference of $33k is still present or roughly 9% too high.

Second, assuming 20% down on a $370k home, a loan of roughly $300k would be required. At a 4% 30-yr interest rate (from 2020/2021), the monthly P&I payment would be $1,432. Let’s assume that after 4 years, our 2020/2021 buyer can afford $1,600 per month P&I (as they received some compensation raises). Using a 7% interest rate (today’s rate), the loan they can afford would be roughly $240k to maintain a P&I payment of $1,600 per month. Now, let’s add a higher down payment (as they invested their $70k wisely) of $80k and the total price of the home would be $320k. This compares to $370k current price which indicates the home is overpriced by $50k or roughly 13.5%.

This is very simple cowboy math/estimates but based on these two quick and dirty calculations, it would appear that the Texas homes are still overpriced by 10% to maybe 15%. At least Texas is heading in the right direction but still has a way to go.

Giddy up 👏

Your analysis makes sense. The issue is that the typical/common homebuyer is looking at monthly payment. What does it cost me to rent to live where I want? What does it cost me to buy to live where I want? Right now, in most of Texas, it is cheaper to rent. So the buyers wait, sales sag, inventories move up.

Another layer regarding Texas is that the major metros have an influx of out-of-state buyers with hugh salaries, relocation incentives covered (sometimes up to 100%) from their employers, and some have cash from their previous home sale due to the move. (I am part of this group). Those people said “Wait, I can get a brand new 3,500 SF in Texas for $550K? Where do I sign?!” And the bidding wars drove it out of control.

So that brings to today. I know people who are willing to “overpay” by 10% in order to get the house they want. I don’t necessarily agree with that, but to each their own. And with higher incomes, remote work, cash from precious sale, employer incentives, etc, it really doesn’t impact people’s finances as much.

Most people have to live somewhere.

The drunken sailors seem to be sobering up a little bit, at least on big-ticket items …

Anecdotal evidence from the real estate market in North Texas: We’re boned.

The 10-year is under significant pressure, yield is rising almost by 10 basis points tonight. Sellers need to adjust their expectations and recognize that waiting for rates to drop and a sudden influx of buyers is increasingly unrealistic.”

This is almost funny. It’s at 4.41% right now. At this pace, it’s going to be over 5% by Christmas. Bond vigilantes rising from the dead?

Wolf, can I ask…

Is there a realistic interest rate that would actually change things in much of any significant way? As things have been, it doesn’t seem like increasing interest rates or even some decrease in interest rates has done anything to readjust the housing market. It does seem to have helped the stock market and the Mike hold on I’m trying to get this finished. Yeah, can you here me? Alexa, tell google that I’m on the phone. Turn off. Turn off. Mike, ya there. Sarah is supposed to be home in a little while. Wanna come by and put it in. Yeah. Not much. I was reading the news, that’s about it. Yeah, I head. I don’t know I don’t vote. I guess. Okay, don’t take too long.

“…has done anything to readjust the housing market.”

Oh, did you miss it? The interest rates we had and have now killed demand in the housing market, and sales have plunged to the lowest levels in decades. Inventories are piling up. Prices have started to come down in many markets, and that will spread and accelerate when people get tired of paying for their vacant home every month even as prices decline. There are millions of year-round vacant homes that are not on the market right now, with potential sellers trying to outwait this market. That works for a little while, but it’s very costly longer-term when prices no longer rise, and especially when they fall. This is where the new inventory is suddenly coming from.

Actually for Wolf:

While it is likely too early to know clearly, it does seem that these most recent storms, Helene and Milton being the last so far this year, but others far damn shore, might be similar to the one(s) in 1926 that caused the beginning of the really great crash in FL RE in that era…

While I was hoping our current location in the Saintly Part of the TPA bay area would be waterfront property for our Grandchildren, LOL, NOW I am thinking it too may be under a foot or meter of salt water…

And, for the record, have advised Saint Skip down the block, a GC trying to help, NOT to suggest any definite amount of raise of houses or AC pads, especially after long long term records of ”surge water” were exceeded recently…

Really and truly folx,,, WHO KNOWs???

Don’t know about “bond vigilantes”, but the bank stock do seem to be rising from the dead this morning.

Agree that interest rates are going up however.

People who are driving up bank stocks today are betting on looser bank regulations that allow banks to take bigger risks, become even more leveraged, and blow up even more spectacularly.

“become even more leveraged, and blow up even more spectacularly.”

I agree, but can you put a date on that? Seems many smart people have been saying the same thing since 2008/2009, and yet, here we are.

I didn’t say that they “will blow up,” I said “allow“:

“…are betting on looser bank regulations that allow banks to take bigger risks, become even more leveraged, and blow up even more spectacularly.”

Stock jockeys are betting on that. But banks may choose not to go that route, because three that chose to go that route during the relaxation of the regulations under Trump1 already blew up (SVB, First Republic, Signature).

The king of unpaid debt returns

why not go up?

Trump win is pumping the 10 yr. Inflation expectations up?

Seems like it… Hot off the press:

https://wolfstreet.com/2024/11/06/longer-term-treasury-yields-mortgage-rates-explode-yield-curve-un-inverts-further-as-bond-market-gets-spooked/

0530 hrs, CT

U$ TSY Paper, especiall the 30yr is collapsing…

U$ Treasury paper, all maturities (2s, 5s, 10s, and 30s), continuing their downward slide (higher rates) begun six weeks ago.

All are painting scary, red candles.

The largest market on the world stage is saying, “We need higher interest rates.”

Allow me to propose something for us all to consider in light of the data; First, since the Nixon administration wealthy people from all over the world (including previously excluded countries like China and Russia) have been allowed to purchase property in America. At the same time the American worker has had to compete with billions of desperate people around the world who have been willing to sell their labor for a mere pittance of what the American worker has been demanding. Is it really any surprise that the prices in the real estate market have been doing what they have been doing for 50+ years? Is it really that surprising that the average American worker is priced out? I don’t think so. I agree with Wolf, with interest rate most certainly heading up, what happens next?

Interesting times.

^^^ This, I believe Canada finally banned (I don’t remember if it was permanent or temporary) purchases by non residents a few years back. I don’t know why we haven’t floated this idea. My understanding (not sure if it’s true because I don’t remember where I heard it) is coming out of the 2008 bubble, people living in China bought up a lot of the East Coat and West Coast properties. This seems like an obvious one that is a-political, why not make make it people need to be living in the US as a citizen, permanent resident, or on a work VISA for at least a year to buy?

Yes, Canadian foreign buyer ban started in 2023 and is in effect through 2027 as it now stands. Will probably be extended. Furthermore, vacant properties in large cities often have additional property tax penalties.

If this has helped increase housing supply? hard to prove a negative or hard to see from the sidelines. RE folks keep saying prices will still rise….but anecdotal evidence indicates sellers dropping asking to close a deal. Case in point, my son in law just sold his Dad’s patio home. He dropped the price several times over one year, fired his agent and replaced, had to pony up a further reduction to cover a proposed new roof assessment by the strata council, and replaced the HW tank as the final condition of sale.

On the west coast foreign ownership ramped up big time a few years before Hong Kong was to revert to China in ’97. It never dropped off as the wealthy continued to relocate their funds out of China to safer locations. This has affected major cities first as the new arrivals are/were urban and moved to larger centres by choice. However, as this pressure elevated city prices locals sold out, reaped the windfalls, and relocated to to smaller cities which eventually pushed up all markets, even rural ones. It was common enough to see a newbie at a nearby city (40 K) purchase a brand new McMansion or something very nice with a view….for cash, put a million in the bank and retire or work part time. In 2004 I sold my home in that same small city and moved rural. I bought the town place in ’87, and in 15 years it increased in value by 500% due to these new arrivals. The new owners had sold their condo in Victoria for what they paid for my rancher on 1/2 acre with a pool and view. It was a win win for both parties.

As an aside, most new people moving to my current location seem to last 3-5 years before they move on. We are just an hour from town, but many can’t take the quiet and lack of amenities. It is provincial law that major hospital hubs must be no more that 1 hour and fifteen minutes away by ambulance, and we do have a small clinic with a nurse practitioner available 5 days per week, but the grocery store is tiny and pretty limited. The school is small and and grades 7 and up bus to town. If your kids are in sports, forget it….they have to stay overnight with friends.

Good comment WB, and I will testify as an analyst/cost estimator in the construction industry after many years in the field as skilled labor and on site supervisor, your idea is correct IMO.

Lost a large project in SF bay area to an owner who brought in his long term workers from Asia in the ’70s, no idea if ”legal” or not ,, and before then lost another bid to ”legal” temporary workers imported to do work in USA National Forests and BLM lands…

Many such challenges continue, and IMO must be stopped so that any USA Citizen who actually Wants to work can work and reap the harvest of their work….

OTOH, most, if not all workers coming here legally or otherwise that I have encountered since mid 1990s have been very good workers and earned their pay…

Foreigners buying is one thing, and debatable whether it should be allowed if Americans cant buy where the foreigners are from, but the Fed/govt *buying* thousands of billions of MBS with money printing for mortgage rate suppression was totally unnecessary and made it a lot worse it seems to me but hopefully the mbs holdings will continue decreasing all the way to zero.

Still a lot of “location, location, location “ in the housing market. The overall Austin area was due for a major correction, but the metro areas for Houston and DFW are huge and within those regions there are areas that still have decent demand and prices are not coming down that much if any. In desirable areas closer in you still see a lot of older homes being bought, torn down and replaced by new giant McMansions. Houston and DFW both have continued development of new homes which I think will help address the demand from hopeful first time buyers.

4.47% now.

Look at the market this morning!!! Uncertainty aside, onward and upward.

For bonds, this is a massive bloodbath today. TLT bond ETF is down 3.4% in premarket trading. Since the rate cut, the price of TLT has dropped by 11%. Bondholders are feeling the pain.

One man’s bloodbath is another man’s profit.

Yes. Also future bond buyers are licking their chops. The 30-year auction today, the bonds sold at 4.608% which wasn’t too bad. Some of those bond buyers licking their chops maybe showed up.

US 30 Year Bond Yield was 4.64 percent on Wednesday November 6.

Was 3.93% from Sept (last rate drop).

Imagine that. Everyone knows the FED will drop the rate and yet people

are betting that this is it for the 30yrs. 30yrs @ ~5% — that is what investors are demanding.

MW: Wall Street’s VIX ‘fear gauge’ collapses as stocks soar

Keep in mind that part of the drop in the VIX is not based on which candidate won, but rather is based on the fact that someone won, with certainty, and thus we won’t have a repeat of Bush-Gore, with violence this time.

DM: The Trump effect – Global stock markets surge while Bitcoin jumps to a record high as The Donald claims election victory

Analysts generally assume Trump’s plans for restricted immigration, tax cuts and sweeping tariffs if enacted would put more upward pressure on inflation and bond yields, than Harris’s policies.

Many had mkt puts Bec of how crazy man would react. Vix was elevated.

U won’t see follow thru

Dry to burst your bubble

Not only have house asking prices gone into the stratosphere and need to come down, I also think the middle (maybe a little above middle) and lower income buyers have lost quite a bit of their former buying power due to actual general inflation not covered by income increases. End result is the price gulf between sellers and potential buyers might be wider than otherwise might have been. Just guessing here.

///

I dont see an incentive for the owners to sell. Holding the property might have some downsides in terms of maintenance, and taxes, but why sell if you can rent? If no-one is buying and everyone is renting it seems like a win-win situation for current home owners. Of course the construction companies and realestate developers will suffer, but the market is stable and will not significantly adjust. Then again, the data might say something different.

///

We were gaslit and abused by a political issue which was created and fueled by politicians.

The end of the political race has come and so with it, the illusion they created.

I think the residential RE, major stock index, crypto, etc. bubbles need to burst for the wealth illusion to end.