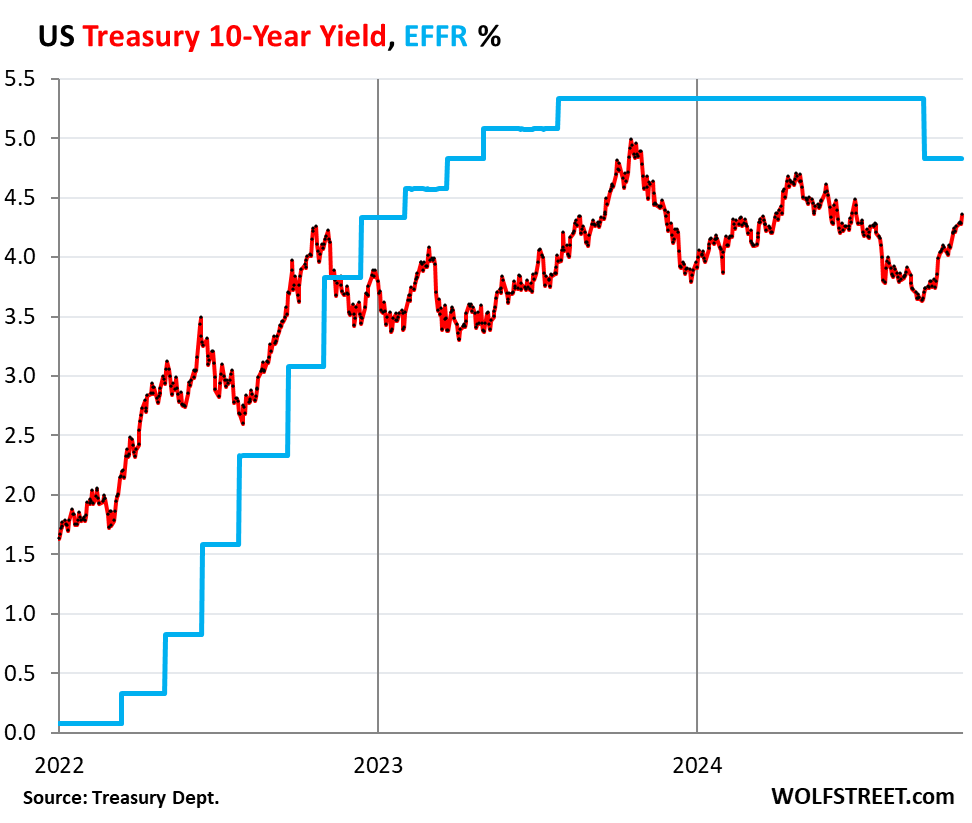

Upon the data’s implications for inflation, the bond market puckered its lips: 10-year Treasury yield jumped to 4.35%, highest since early July.

By Wolf Richter for WOLF STREET.

It always works that way: Major hurricanes with flooding in large multi-state areas and big strikes temporarily knock down the nonfarm payrolls reported by employers. And October payrolls saw both of them come together. But over the next several months, payrolls bounce back sharply, plus some, as flooding-affected employers re-open their businesses and the clean-up and rebuilding start, and as strikers return to work.

Major strikes hit payrolls because workers on strike – and workers temporarily laid off because of the strikes – don’t count in payrolls, and when these workers return to work, nonfarm payrolls bounce back. This happened a year ago with the strikes in the auto industry. And now it happened with the strikes and associated temporary layoffs at Boeing. We expected this hurricane-Boeing impact and said that in terms of the jobs data, “this is going to be a mess,” and that prediction nailed it.

In terms of the hurricanes, the Bureau of Labor Statistics, when it reported the labor market data this morning, said:

“Hurricanes Helene and Milton: October data from the household and establishment surveys are the first collected since Hurricanes Helene and Milton struck the United States. These hurricanes caused severe damage in the southeast portion of the country.”

“It is likely that payroll employment estimates in some industries were affected by the hurricanes; however, it is not possible to quantify the net effect on the over-the-month change in national employment, hours, or earnings estimates because the establishment survey [which produces the nonfarm payrolls and hourly wages] is not designed to isolate effects from extreme weather events. There was no discernible effect on the national unemployment rate from the household survey.”

In terms of Boeing, we see the impact of the strike and the associated temporary layoffs in the industry of manufacturing where employment dropped by 46,000, of which 44,400 job losses occurred in transportation equipment manufacturing, and that’s Boeing. And the unemployment rate in that sector jumped from 2.2% in September to 5.3% in October.

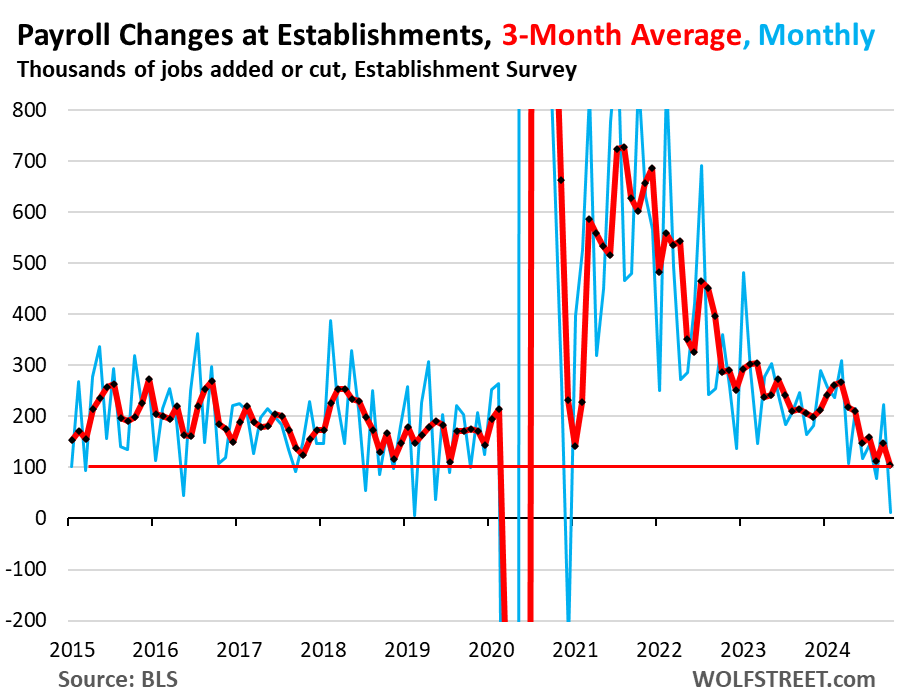

So payrolls at employers, with all this going on, still rose by 12,000 jobs in October, according to the Establishment Survey. September was revised down some (to 223,000 jobs created), and the up-revision a month ago for August was re-revised away (blue line).

The three-month average job creation fell to 104,000 payroll jobs in October (red line).

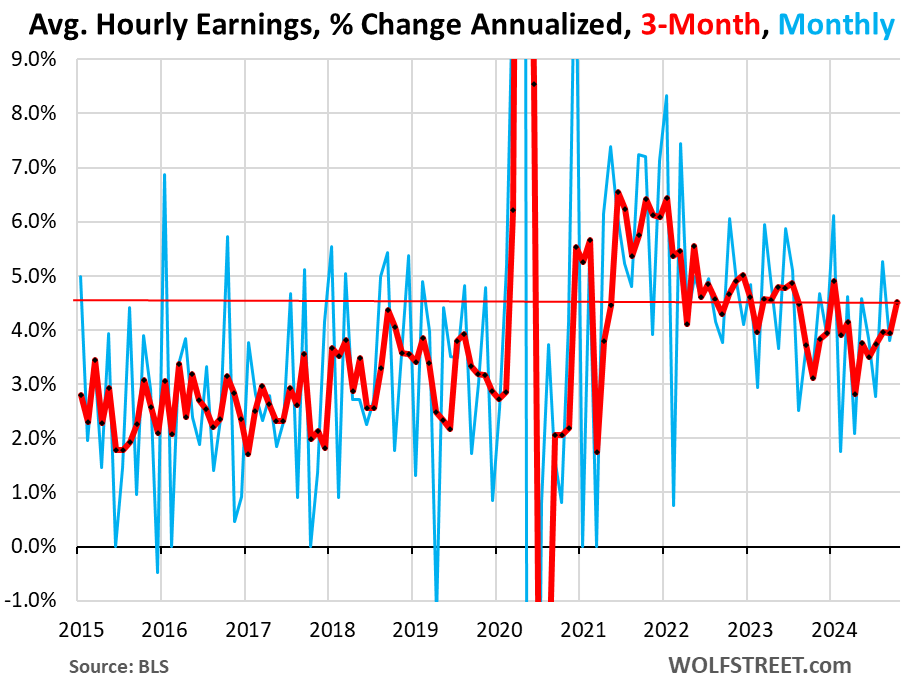

Average hourly earnings, based on what employers reported, jumped by 4.5% annualized in October from September (blue line).

The three-month average also jumped by 4.5% annualized, the biggest jump since January. It has been increasing steadily since April (red line).

Year-over-year, average hourly earnings rose to 4.0% in October from September, the biggest year-over-year increase since May, the third month in a row of year-over-year increases, and well above the peaks of the 2017-2019 period.

So in terms of the reborn inflation worries, this accelerating wage growth is not going in the right direction.

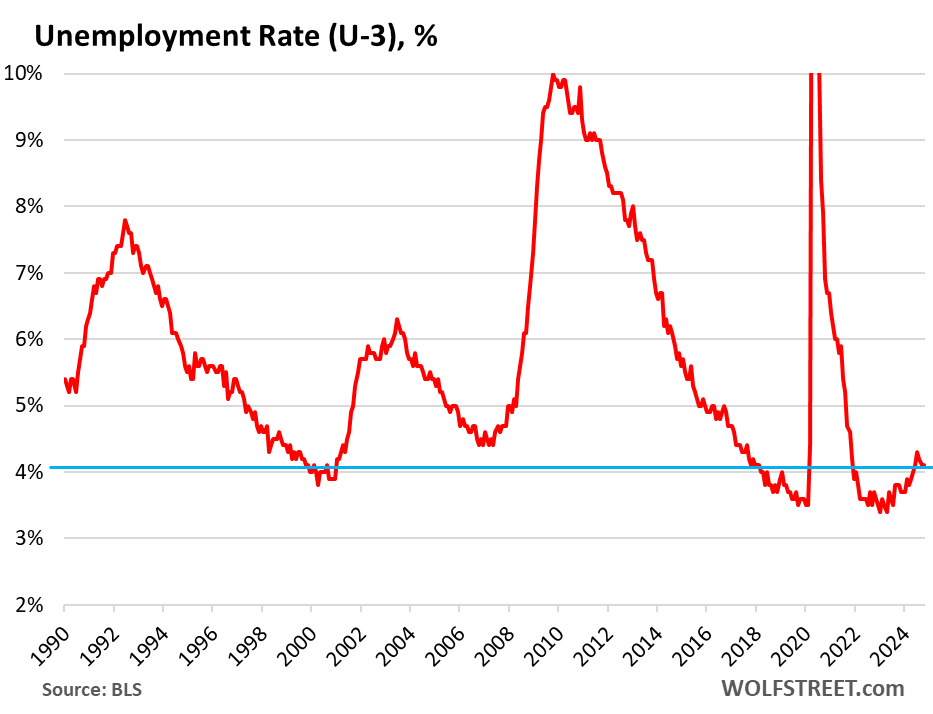

The headline unemployment rate (U-3), based on the household survey, remained at 4.1% in October. In July it had risen to 4.3% but has come down since then. This is a historically low rate, though it is up from the period of the labor shortages in 2022.

The unemployment rate is below the Fed’s 4.4% median projection for the end of 2024 and for the end of 2025, according to the Fed’s Summary of Economic Projections released at the rate-cut meeting.

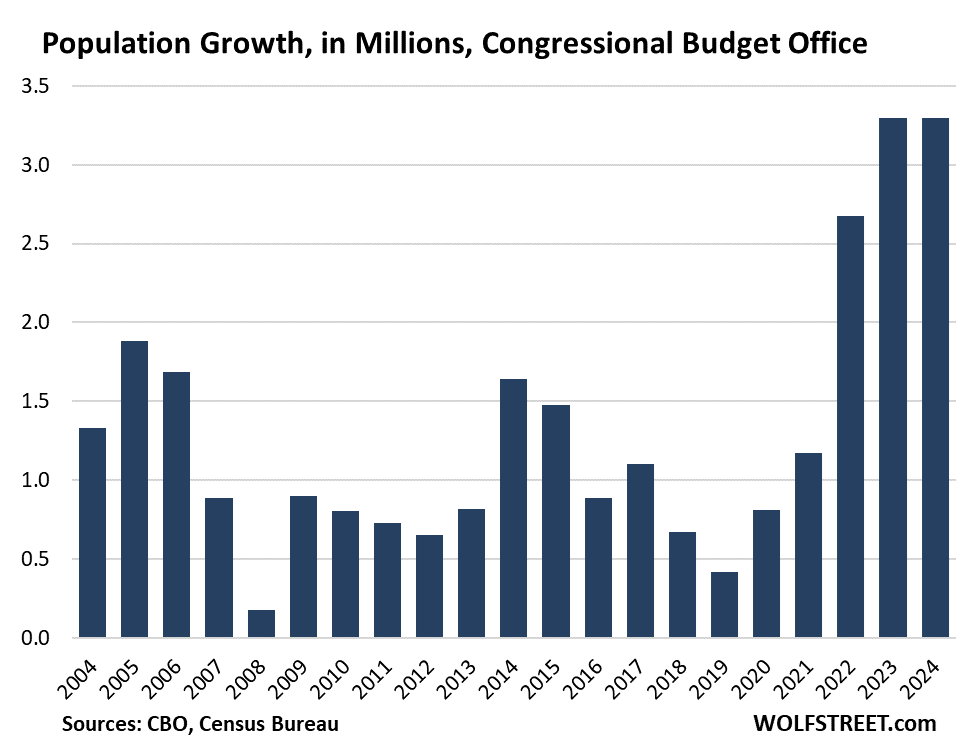

The influx of new immigrants – estimated by the Congressional Budget Office at 6 million in 2022 and 2023 and ongoing in 2024, see chart below – is hard to track in the household employment data because proportionately fewer of them respond to the household surveys.

The newly arrived immigrants who either already have a job or are looking for a job would count in the labor force, regardless of their legal status. If they’re working, they would count as such, regardless of legal status. Those that have not found a job yet would show up in the unemployment rate.

A rise of the unemployment rate due to this new supply of labor is a different dynamic than a rise of the unemployment rate due to job cuts and a reduction in demand for labor, as is typical in a recession.

This chart shows the sudden population growth driven by the huge waves of immigration in 2022 through 2024, according to the Congressional Budget Office, which used ICE data in addition to Census Bureau data:

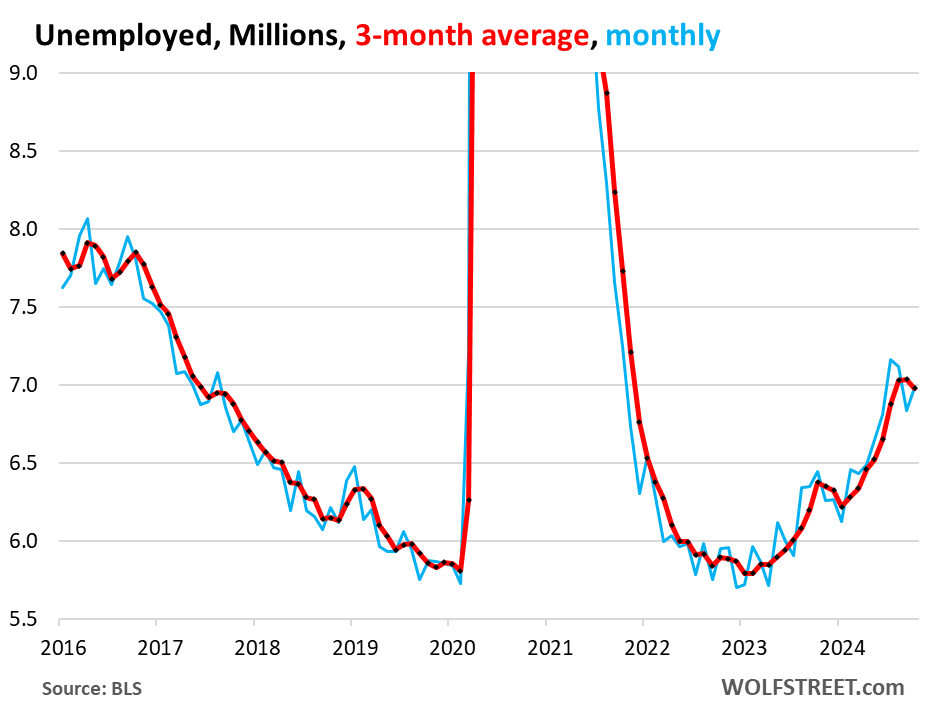

The number of unemployed people looking for a job rose to 6.98 million, after falling for two months in a row. The three-month average dipped to 6.98 million.

This metric of the number of unemployed does not take into account the growth of the labor force over the decades. But the unemployment rate (above) accounts for it.

The bond market figured it out too.

The return to work of the Boeing employees with big pay increases in their new contracts will cause manufacturing employment to bounce back. And the after-effects of the hurricanes will include a jump in payrolls.

So over the next few months, there should be a sharp increase in nonfarm payrolls. And this comes on top of the already accelerating average hourly wages that are among the factors stirring up inflation worries.

So upon seeing all this unfold, the bond market puckered its lips. After initially dropping, the 10-year yield jumped and is now up by 6 basis points, to 4.35%, the highest yield since early July. Since the Fed’s rate cut, the 10-year Treasury yield has risen by 70 basis points.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The bond market certainly saw thru all the BS headlines about “spiking unemployment” or whatever.

Thanks Wolf for helping us see the forest thru the trees. I’ll be mailing in my annual donation soon.

The real problem in the September and October reports was the seasonal adjustment factors. The September numbers were higher than expected due to the seasonal adjustment factors. The pandemic has made these adjustments less or unreliable. As a result, it was expected that the October numbers would be negatively impacted by the seasonal adjustment factors even if there were no strike or hurricanes.

You got that wrong maybe?

Not seasonally adjusted:

October payrolls: +826,000

September payrolls: +450,000

Both of the increases were smaller increases than a year ago, September a little smaller, October a lot smaller reflecting Boeing and the hurricanes.

Wolf, where did you get those non-seasonal job changes?

Does the BLS include such monthly adjs explicitly in its NFP reports or by displaying nsa vs sa added job totals?

I presume that published sa net job changes were arrived at by adjusting downward due to typical seasonal hiring trends.

Surprised somewhat by levels of sa’s.

Thanks.

Jobs are HUGELY seasonal, as are hiring and weekly unemployment claims, if you look at the NSA figures.

You can get all the BLS detailed data, SA and NSA, at the BLS data finder:

https://data.bls.gov/dataQuery/search

The Data Finder is a huge resource. It has everything. And you can download everything. Which makes it hard to use if you just want to look up one thing. You might also try to find it on FRED, it probably has that too.

Does this mean mortgage rates will continue rising?

That’s a possibility. But this stuff, as they say, fluctuates.

Anecdotal from a Guaranteed Rate loan officer with 40+ years in the business….

Top loan officers are cutting their commissions to keep buyers in their loans till closing. Volume is way down and half a loaf is better than no bread at all.

“Top loan officers are cutting their commissions to keep buyers in their loans till closing.”

Does that mean the rates are going up after the customer gets their rate-lock?

Rates have been rising steadily, so yes, rates could be higher after the loan lock but it wouldn’t affect your locked loan.

But when a customer shops for a loan, Company A quotes 6.95 apr and Company Loan officer can go 6.75 by shaving his cut.

Thanks for clarifying. I had misunderstood your comment initially.

I assume this lack of volume is affecting both purchase mortgages and refi/HELOC?

Yeah, thanks for input. (especially if generally true)

Boeing workers will get close to the 10% per year raise they want. Longshoremen wil probably get their 10%/year in January. Won’t this set the tone for wage increases across the economy adding pressure to the next wave of inflation ?

Seems like given most of the companies profitability is doing well they will simply accept making less profit and not drive prices higher:)

HAHAHAHA

0H MY GOD YOURE SUCH A JOKESTER

But Boeing is a vanishingly small percentage of overall employment. And the damage done by hurricanes is usually overprojected for the dramatic effect of the stories themselves. It seems to me that the reasons for the unadjusted job seeking numbers have more to do with improper reporting, i.e. from new immigrants, than anything else.

Nonsense. Boeing and the hurricanes are part of the INCREASE in employment (+12,000), and they weighed hugely on that 12,000.

And RTGDFA. I gave you Boeing’s numbers.

Boeing’s striking workers and the associated temporary layoffs caused a drop of 44,400 jobs. Without strike, those 44,400 jobs would be added to the 12,000 jobs created for 56,000 jobs created. If the hurricanes knocked employment down temporarily by 100,000 to 200,000 jobs, the payrolls increase without hurricanes would have been between +166,000 to +266,000. And that would have been right on track.

You can also see this in the “not seasonally adjusted” payrolls, as I said earlier here:

October payrolls: +826,000

September payrolls: +450,000

Both of the increases were smaller increases than a year ago, September a little smaller, October a lot smaller reflecting Boeing and the hurricanes.

The fact that the clear downwards trend in hourly earnings appears to have stalled well above the supposed rate of inflation has to be turning on some red flags at the Fed. Or at least one would hope it does.

“September was revised down some (to 223,000 jobs created”

I believe the downward revision was 88,000.

My definition of ‘some’ is obviously different than yours.

BS. It was revised down by 31,000, from 254,000 to 223,000.

1:04 PM 11/1/2024

Dow 42,052.19 288.73 0.69%

S&P 500 5,728.80 23.35 0.41%

Nasdaq 18,239.92 144.77 0.80%

VIX 21.88 -1.28 -5.53%

Gold 2,744.00 -5.30 -0.19%

Oil 69.48 0.22 0.32%

Things might get rough and require you to go with a blend versus a single malt or pick up some Lyft or Uber revenue.

Spoke with a mortgage banker that did not lock in rates for clients. Oops. Explained to the banker that just because rates go down, it does not mean that yields will follow. Mortgage banker is waiting for yields to drop as they have a portfolio of clients that want to refinance that is worth millions. Yeah, so does every other mortgage banker in the country, thus having billions of dollars worth of refinancing that is like essentially a mini stimulus making yields rise again. Yields may not run out of steam just yet.

🤣

The few people you know, out of the 335 million in the US, are the wrong people?

Whatever you do, don’t commit the idiocy of extrapolating from your minuscule personal experience to the vast US economy, because that’s just BS. If you do that, you’re in the wrong place, dude.

I believe rates are heading higher since the Fed will most likely cause inflation to go higher if they start QE again. There other factors as well, such as the increasing debt service requirements to maintain the current cumulative deficit. This means that the the US is on a path that will cause deteriorating credit quality. There is also the political uncertainty like what happened on Jan 6th. There also are public statements by Trump that he would like to selectively default on our nation’s debt to countries and people he does not like. Higher risk demands higher returns. Best guess – the UST 10-year will be priced to yield 5% within the next six months or so.

rates are headed higher because supply of government bonds is too high. it simply means bond prices are falling (when rates rise). if the Fed does QE (which it will at some point) it will help stabilize rates, but add to long term inflationary pressures. gold prices have sniffed out this inevitable QE, and begun repricing fiat for the next cycle.

“gold prices have sniffed out this inevitable QE, and begun repricing fiat for the next cycle”

But bonds are selling off – especially longer durations – which is the opposite of what you’d expect with imminent QE.

I think I have a better explanation for both of these: the market is pricing in inflation and higher rates after years of excess liquidity. This explains both the bid in gold and lack of in bonds.

respectfully disagree. you are confusing price inflation (consumer goods and services) vs monetary supply inflation (gold has stable supply metric vs fiat uncontrolled supply metric).

it may sound semantic

and argumentative, but I assure you. I’m just trying to be precise because cause and effect matter. price inflation is “downstream” of monetary inflation.

Will the people choose cancer or the train wreck?

Miracles are expected in either case………one is where the savior has actually shown up, and the other is the saving technology or societal change savior may still show up given more time.

Just another crazy thought that occurred to me. But it WILL affect everything financial and therefore everyone’s “investment” plans, so it’s ON topic.

Disclosure: I have no investment plans either way….not enough money saved to make any meaningful investment……

I don’t see any of my people getting decent raises this year, either. They’re screwing us as much as they can all around.

The reason workforce attitudes are so bad is because companies treat people like sh!t. So many companies are just so lame, with their little in-house propaganda videos and bad leadership that jerks people around back and forth every time some C-suite twit wants to make a name for himself, everyone else be damned.

And that prick from Amazon, claiming that 9 out of 10 people he surveyed are happy about RTO. Who is he asking – just the few lonely old guys in the office with nothing else to do?!? So now they just lie to you like the CCP, while standing next to the truth…