Households’ money market fund & CD balances rise to a record $7.4 trillion; “savings” are far from depleted, they’re bigger than ever.

By Wolf Richter for WOLF STREET.

Americans hate, hate, hate inflation. But they like the higher yields on their cash that came with it, and they put a lot of cash to work by yanking it out of their bank checking accounts and near-0% savings accounts and putting it into much higher yielding money market funds and “brokered CDs” that they bought through their brokerage accounts, which forced banks to compete by raising their own interest rates they paid on deposits to keep deposits from fleeing, and to attract new deposits to replace those that had fled.

And Americans flocked to those CDs too, and they switched back and forth between CDs, money market funds (MMFs), T-bills (Treasury securities of one year or less), and savings accounts, arbitraging rate differences and convenience, thereby keeping banks on their toes. And they continued.

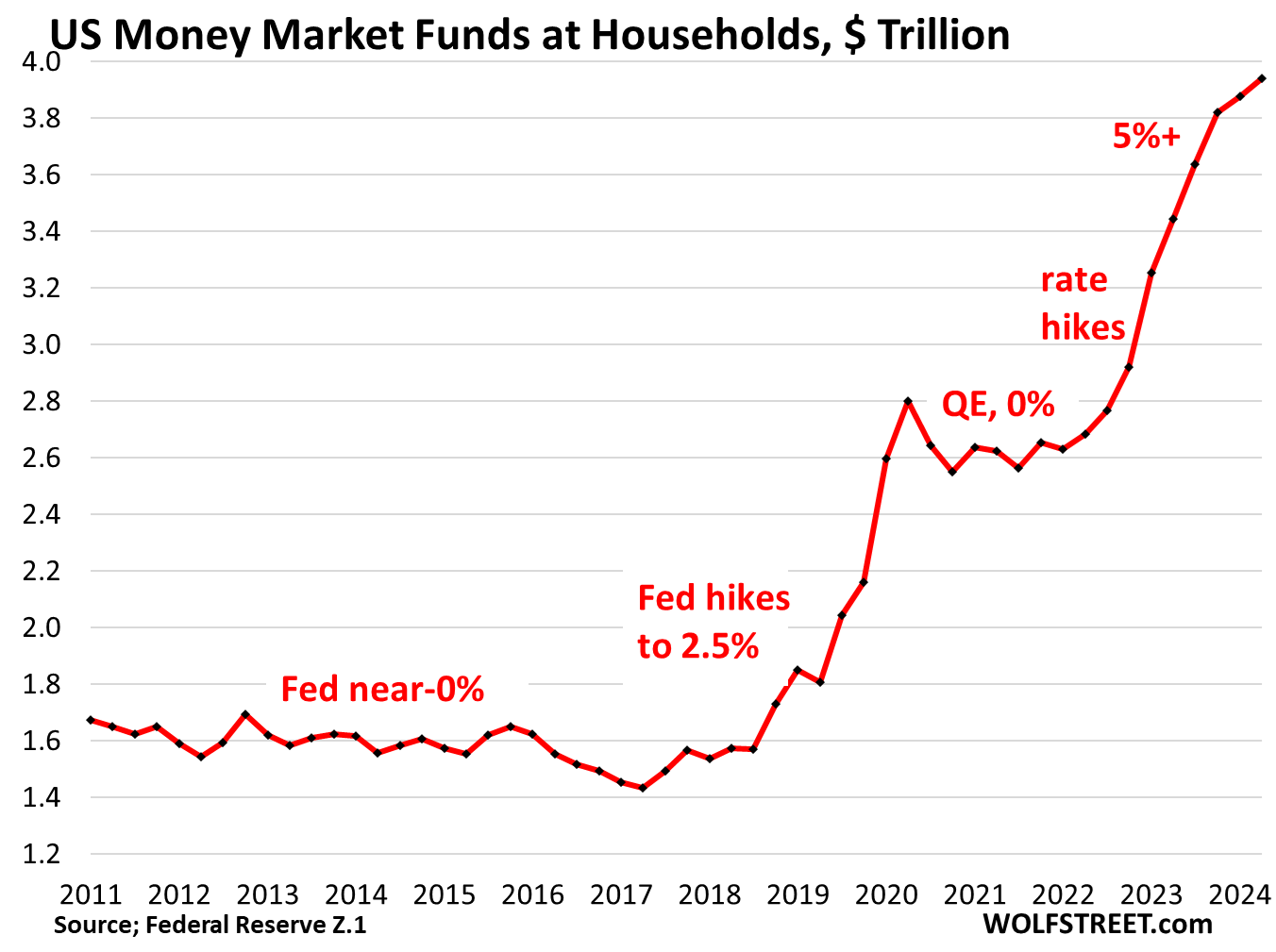

MMF balances held by households jumped to $3.94 trillion at the end of Q2, up from $2.6 trillion during the 0% pandemic era, and up from $1.6 trillion before the rate-hike cycle of 2017-2018, according to data released yesterday afternoon by the Fed as part of its quarterly Z1 Financial Accounts.

These MMF balances include retail MMFs that households buy directly from their broker or bank, and institutional MMFs that households hold indirectly through their employers, trustees, and fiduciaries who buy those funds on behalf of their clients, employees, or owners.

MMFs are mutual funds that invest in relatively safe short-term instruments, such as Treasury bills, repos in the repo market, repos with the Fed – what the Fed calls “Overnight Reverse Repos” (ON RRPs) – high-grade commercial paper, and high-grade asset-backed commercial paper.

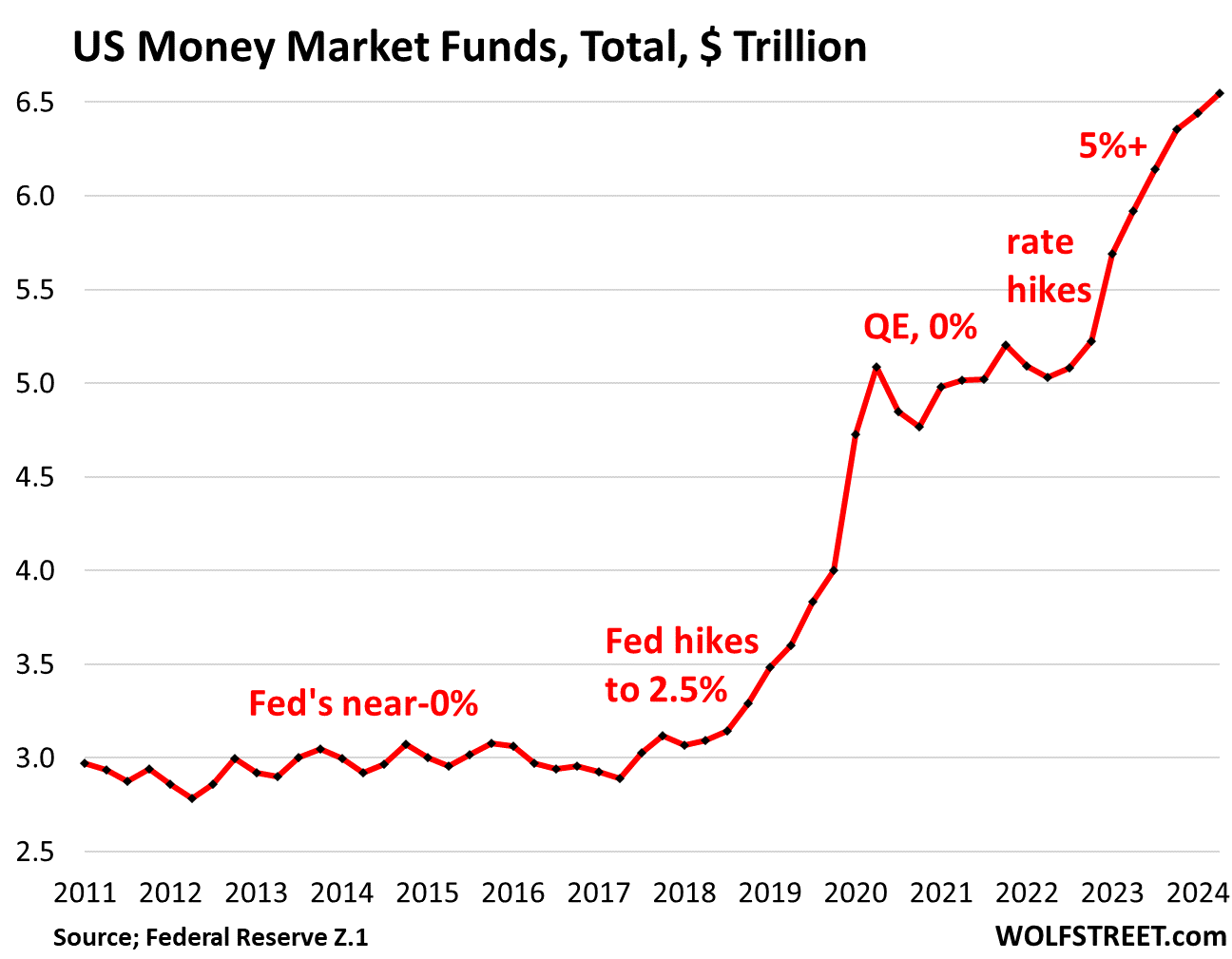

Total MMFs held by households and institutions jumped to $6.55 trillion by the end of Q2, according to the Fed’s data yesterday, having doubled since 2018, and having jumped by over 30% since the rate hikes started in 2022.

But somewhat counter-intuitively: When the Fed cut rates in 2019, cash continued to pile into money market funds. It wasn’t until Q3 2020, with yields down to near-0%, that some cash left MMFs, but not much, and balances remained high and essentially flat until yields started rising again, at which point more cash came into the funds. In other words, rate cuts to even 0% didn’t drain the MMFs, but balances stopped rising.

Banks have to compete with MMFs and T-bills.

The nonbank entities that offered higher yields on cash – MMFs and T-bills available through brokers and TreasuryDirect – forced bank to do what they loathe to do in 2022 and 2023: raise the interest rates they pay on deposits.

Banks loathe it because it increases their cost of funding. But if they don’t do it, their deposits leave, which can pose big problems for banks: In March and April 2023, Silicon Valley Bank, Signature Bank, First Republic collapsed and Silvergate Capital was forced to shut down by regulators because their depositors yanked their money out essentially overnight. So banks have to try to hang on to their deposits.

Deposits are loans from customers to the banks and form the backbone of bank funding. Customers yank their cash out to put it into MMFs or T-bills when the bank’s interest rates on CDs or savings accounts aren’t high enough. But deposits are generally “sticky,” so this time too, it was a slow process for bank customers to chase higher yields somewhere else.

But eventually banks had to offer more attractive rates, at first to some customers, namely new customers, and eventually more broadly to existing customers to attract new deposits and hang on to their existing deposits.

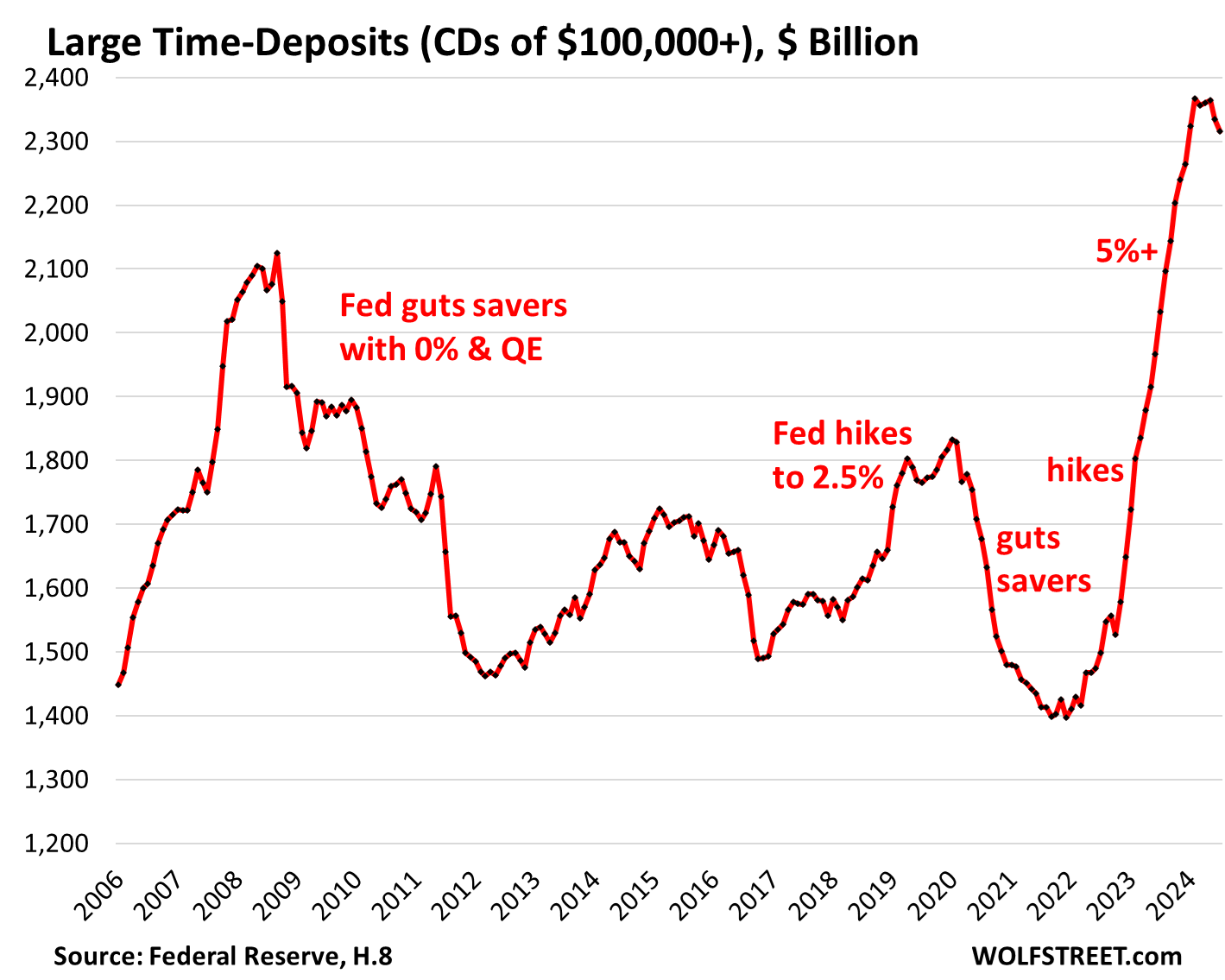

For banks, CDs (“time deposits”) provide funding that is more stable – they mature on a fixed date in the future – than savings or checking accounts whose cash can be yanked out anytime via electronic fund transfers.

But rate hikes stopped in July 2023, and amid endless discussion of rate cuts since then, banks have largely reduced the interest rates they’re offering, and CD balances have stopped rising, and for large deposits, have started to dip.

Large Time-Deposits (CDs of $100,000 or more) dipped in July to $2.32 trillion, the second month in a row of declines from the peak in May, according to the Fed’s monthly H.8 data on Assets and Liabilities of Commercial Banks.

In two years since March 2022, when the rate hikes began, large time-deposits surged by nearly $1 trillion, or by 69%.

The Fed’s interest rate repression during the Financial Crisis caused banks to slash the interest rates on CDs to near-0%. The cashflow of savers was sacrificed at the altar of asset-price inflation. And CD balances plunged, as deposits mostly reverted to other types of bank accounts that paid nothing and whose balances continue to swell.

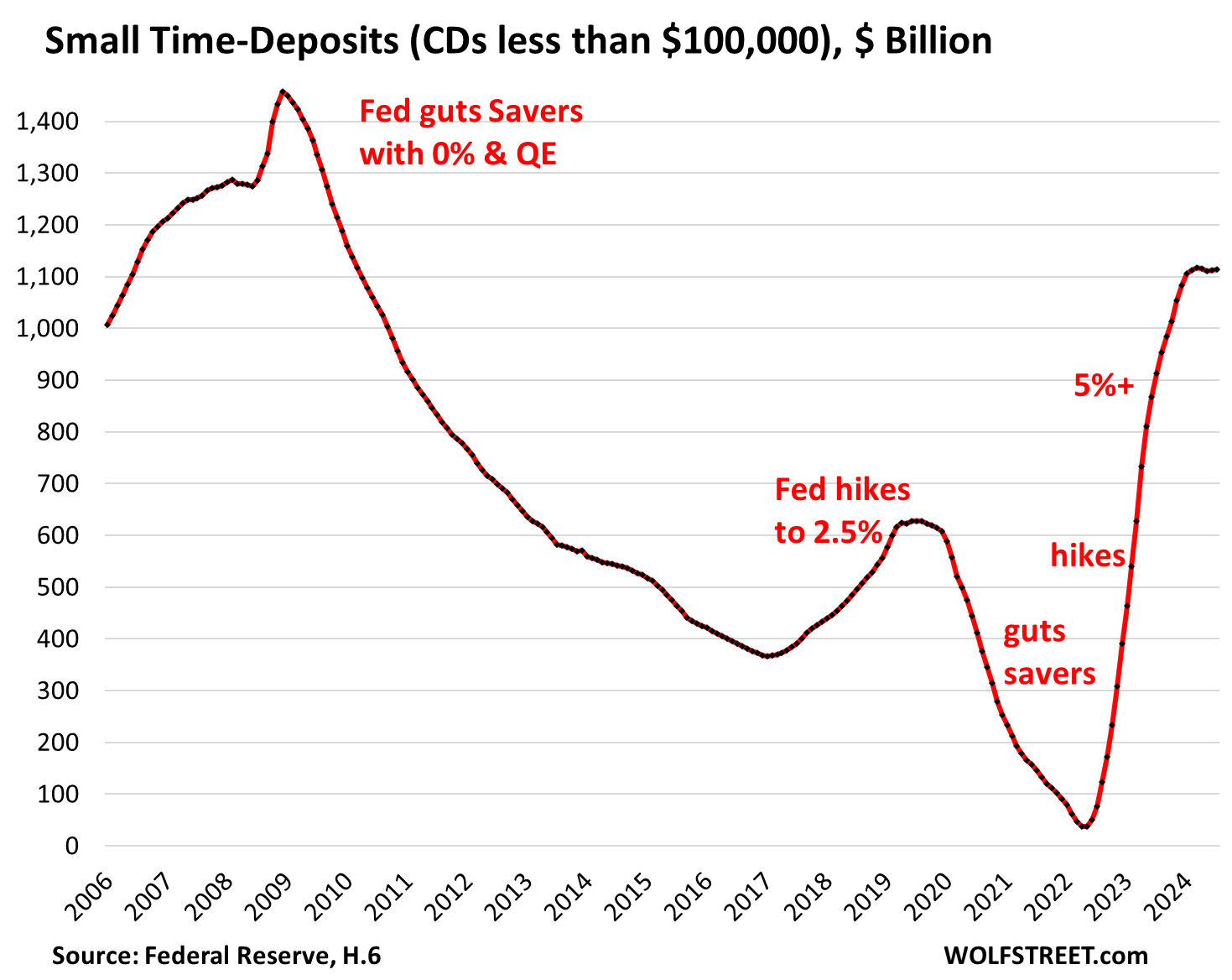

Small Time-Deposits (CDs of less than $100,000) have been roughly unchanged since CD rates stopped rising late last year and in July ticked up a hair to $1.11 trillion, roughly flat with February.

These small CDs reflect what regular folks are doing with their savings. When the Fed gutted their cash flow from savings in 2008, they lost interest in CDs, and the cash reverted to savings and checking accounts, and some wandered off to money market funds and other investments, and CD balances fell by over 70%.

During the rate-hike cycle in the two years through 2018, Americans started buying CDs again. But then the Fed cut rates to near 0% again, starting in 2019, and with their cashflows once again gutted by the Fed, savers lost interest, and by early 2022, just before the new rate hikes, balances of small CDs had collapsed to just $36 billion.

But the move since then has been stunning as banks tried to keep their customers’ cash from fleeing to MMFs and T-bills.

Treasury bills: There are currently $6.11 trillion of T-bills outstanding (they mature in one year or less), and the government is issuing huge amounts of them amid huge demand at T-bill auctions. We don’t know the amounts of cash that households invested in T-bills, either at their broker or directly at TreasuryDirect, but it’s significant.

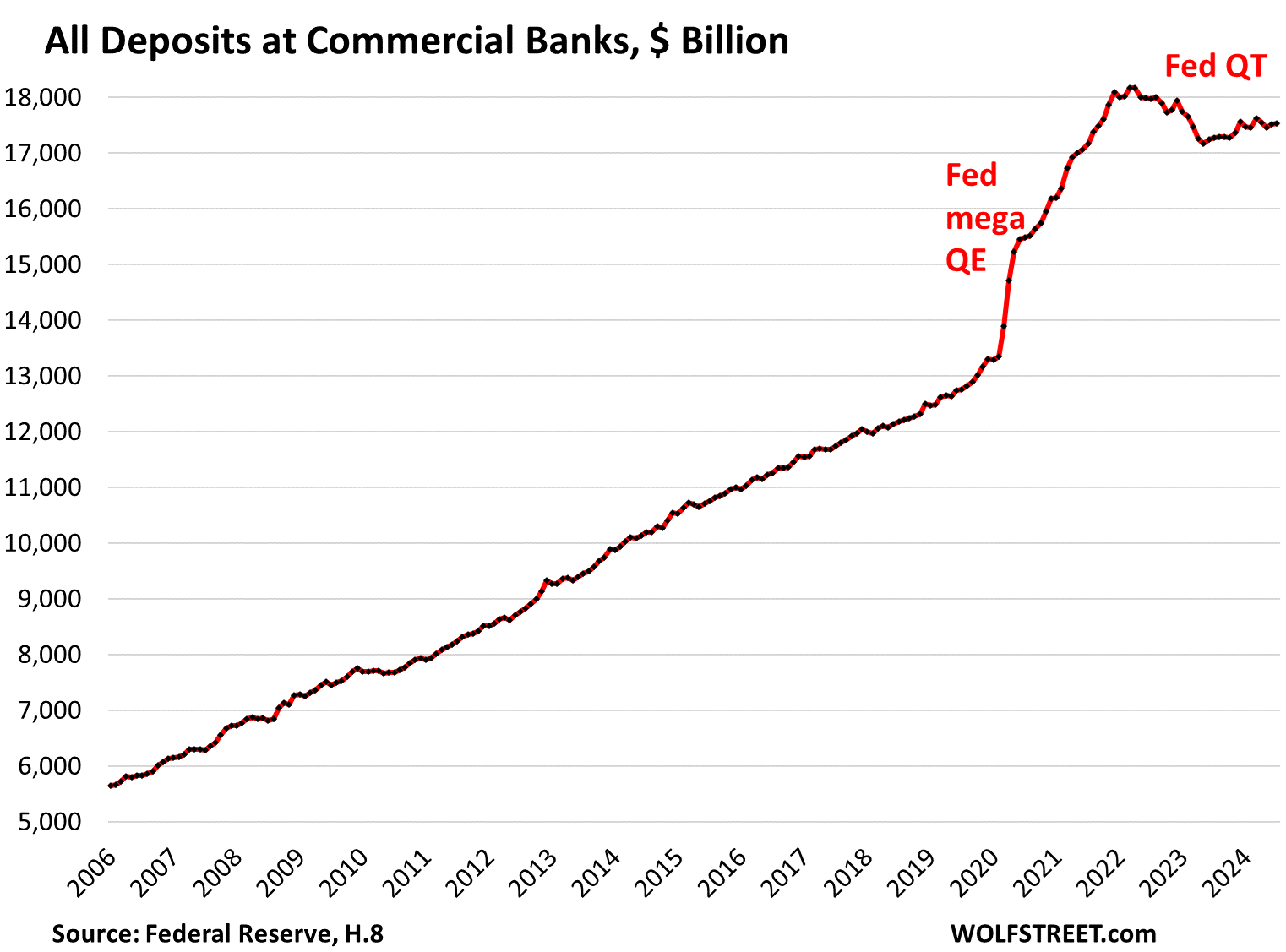

Total deposits at all commercial banks, including CDs and all other bank accounts, edged up to $17.5 trillion in July. These are deposits by all bank customers: households, businesses, and government entities (except the Federal Government, which has its checking account at the New York Fed and is not included here).

Total deposits at all commercial banks spiked during pandemic-era QE. But when interest rates rose, some of the deposits left the banking system and moved to money market funds and T-bills, and total deposits fell by about $1 trillion through mid-2023. Since then, total deposits have slowly grown:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Americans hate, hate, hate inflation. But they like the higher yields on their cash that came with it.”

I guess we’ll see how they like it in the near future when they still have inflation, but the after-tax yields on their cash either just barely keep up with it, or don’t keep up with it at all.

Then the Federal Reserve will say, this is all for the sake of the labor market because we have 2 mandates blah blah blah

I wonder what happens if, after the 0.75~1.25% in rate cuts they’re expected to deliver in the upcoming months, the labor market stabilizes around this level & doesn’t get materially worse?

Would they say, “monetary policy works with a lag, so we’ll wait & see for these cuts to propagate through the economy (and stand ready to act if more cuts are truly needed),” or they’ll just keep cutting & cutting & cutting to 2.6% or whatever laughably low level they consider as “neutral,” because that’s what Wall Street wants. Or a third option, they’ll keep cutting & cutting – even below what they estimate as neutral – until they actually SEE inflation come back with a vengeance?

I think it’ll be one of the latter two. Powell already gave the game away with his Nov 2023 dovish pivot amid a booming economy at the time. Central banks were itching to return to pre-Covid low rates regardless of the labor market, and the recent unemployment mini-spike just gave them a convenient excuse to do it.

Pea Sea,

Everything is taxed, including 1.6% dividends and any gains in the stock market (though only short-term gains are taxed full blast). That’s no different from interest income. I have no idea why that keeps getting brought up. It’s a constant for all income.

Except T-bill interest is not subject to state income taxes, and in California, that makes a difference. But stock market gains are fully taxable.

Actually, people are better off making 4% on their T-bills with inflation at 3%, than making 5.5% on T-bills with inflation at 6%.

And people are better off making 4% on T-bills than losing 50% in the stock market a la 2000-2002 and 2008-2009.

If people sold their Nasdaq Composite holdings in Nov 2021, and bought T-bills with the proceeds, they were better off without all the drama, than people who kept their Nasdaq Composite holdings.

The Russel 2000 is even worse off.

The difference is risk.

Wolf,

Thanks for assembling the charts – they are very useful because they (partially) illustrate how trillions in capital sloshes between the giant bathtubs of asset classes as macro factors change (especially interest rates…risk on/risk off, etc.)

But…that raises the question of *where the trillions sloshing into MMFs and large CDs…originated *from*.

Some of it came from the trillions in printed Pandemic money and some came from the collapsing Russell 2000 (maybe).

But trillions haven’t flowed out of the SP 500 or…housing.

It would be difficult, but very valuable, to try and match up the asset classes the *money came *from* as well as those it went *to*.

Only the printed Pandemic money was true *new* money…all the rest of the MMFs/CDs had to *come from somewhere else*

Where?

Wolf — what’s going on in this department in the EU? Are households also flush with savings? Would be interesting if you did a piece on this because you’ve covered ex-US housing markets and central bank balance sheets so this would be a logical next step, perhaps?

Thank you for pointing that out – we are better off with 4% Money Market yields with 3% inflation than 5% and 6% inflation – that is why there will be no mad rush to the exits when the Fed starts to lower rates. Few reporters have pointed out the massive income on 6 trillion in MMarkets getting 5%. Even with 100K in a money market that is $5000 extra income a year.

The short term Federally insured money is still paying 5+ for at least, the next three months. If one were to choose that strategy, too be successful they have to be diligent about reinvesting the dividend and maturing securities to realize the advantage.

Or they can bet that the longer term securities, currently being priced at an interest rate profile which seems hopeful, rather than rational. If the interest rate were too increase on the 10 year to the level of six months ago, holders of those bonds would lose 25 + pct of the principle value which only makes a difference for someone looking to sell.

the fed will always ‘hide’ behind one mandate (excuse) or another to justify what it is, or is not, doing. that much is obvious by now.

but the real issue is.. nothing is going to happen to them for being wrong one way or the other. it does not matter in the least what jerome powell’s ‘scorecard’ ends up being at the end of his tenure. you can be absolutely sure he will have a cushy private sector job lined up if he wants, regardless. and plenty of well-paid speaking engagements.

this is the crux of the issue, not only with the fed.. but with most (if not all) governing entities. FAILURE IS an option. so dont sweat it.. no big deal! the same is true for most of the bigger/integral corporate entities, regardless of industry.. the major banks (JPM, BAC, C) are the most prominent example of this, but you can be sure ALL the major defense companies are also.

this country suffers from an appalling lack of general accountability, on every level of not only government.. but in the private sector as well. in fact, society in general is largely one giant ‘ain’t my problem..’. kennedy’s maxim has been completely inverted. there is so much irrationality and permissiveness ‘out there’, that it has largely become normalized.

but as they say.. ‘every dog has its day’. in this particular case, the day aint quite over yet.. but it will be.

reading this article would lead one to believe that the vast majority of americans have huge piles of interest bearing cash just lying around for their enjoyment.. and while the piles may be large in gross aggregation, they are NOT evenly distributed among the people of this country.

when the likes of dollar tree (DLTR) and dollar general (DG) take gigantic single day losses on their recent earnings: (DG -32% on aug 29th & DLTR -22% on sep 4th) one can surmise that something is very wrong ‘out there’..

when the CEO of NVDA spouts off about chip demand like he did this past wednesday, and it moves the ENTIRE stock market from bloody red to greener than a leprechaun’s a** on st. pattys day… you can BET something is VERY VERY wrong ‘out there’: ‘huge piles of cash’ notwithstanding.

*Rolls eyes*

Yeah the perfect week in the market. A clean 5 day sweep was caused by a tech CEO and not the Ultimate event of the last 4 years.

The fed… wait for it…

Is loosening the purse strings!

Basically a financial slingshot of cash is going to rain down.

So yeah perfect week. Blame whoever you want. But Powell is singing the ol’ Zep tune. Nobody’s Fault But Mine.

n0b0dy

“when the likes of dollar tree (DLTR) and dollar general (DG) take gigantic single day losses on their recent earnings: (DG -32% on aug 29th & DLTR -22% on sep 4th) one can surmise that something is very wrong ‘out there’..”

Nonsense. Walmart and Amazon had blowout quarter in their retail businesses, as did some other retailers, because lower-income people have upgraded and no longer need to buy this junk. You’re using two cherrypicked company-specific problems to come to the wrong conclusion. This stupid BS is now everywhere, which is where you picked it up.

Like Wolf said, people will pull their money out if that happens. Something the banks are not going to want to happen.

1:04 PM 9/13/2024

Dow 41,393.78 297.01 0.72%

S&P 500 5,626.02 30.26 0.54%

Nasdaq 17,683.98 114.30 0.65%

VIX 16.56 -0.51 -2.99%

Gold 2,609.00 28.40 1.10%

Oil 69.27 0.30 0.43%

If anyone had popped into the S&P exactly one year ago they would have:

26% more $

🤷🏻♂️

#indexfund

If they popped into the S&P 500 exactly on January 3, 2022 — so that was 31 months ago — they would have 17% more. And that’s just a little ahead of what T-bills would have earned without all the drama in between. So choose the day wisely?

if, if, if…

‘if’ i had invested all my free $$$ into tesla back in 2010, and held on till now, i would be a borderline centimillionaire…

‘if’ the axis had won WWII, we’d probably be living a real-life version of ‘the man in the high castle’…

‘if’ wolf were a greedy bastard, he would make this website’s content available to subscribers only…

etc etc etc..

see how silly that is?

*EYEROLLS*

Which is exactly the paradox I was trying to get a handle on was how would I handle the distribution of excess wealth. Thanks for highlighting the worthy goal of becoming a borderline centimillionaire…

But I warn you. It’s not paradise.

Far from it. It’s ware romance goes to die.

If I had loaded up on Bitcoin shortly after Satoshi released the Genesis block, I would be a multi-billionaire today.

Some mornings you get up and just make nothing but bad decisions all day long.

DM: America’s most powerful banker issues stark warning about fate of US economy: ‘Worse than recession’

JPMorgan Chase CEO Jamie Dimon has said he would not rule out an outcome for the US economy which is widely considered to be worse than a recession.

He’s been saying this stuff for years. He has a wide range of scenarios that he thinks have a chance of playing out, from a hot economy for years to a bad long downturn, and he is trying to prepare his bank for all of it. That’s what this is all about. I actually wrote about it once or twice in the past. Same-old same-old.

100% agree 👍🏻

A different POV would suggest that everyone should pay attention what Jamie Dimon, the most savvy player since at least his apprenticeship under Sandi Weil.

A winner sharing his potential plans is educational. Not as a comment about his stock as much as a warning of the banking Dr. Frankenstein.

JP Morgan Chase with Jamie Dimon as CEO has 5 felony fraud charges and over the years paid billions in fines . They were Bernie Madoff’s banker and claimed to know nothing.

So I take pretty much anything billionaire confidence man Dimon says with a tablespoon of salt.

JPM always has some regulatory scuffle in some corner of its vastness. I try to look at the vastness and its overall performance and value, rather than a data point or two. It is far from perfect, as is true of most banks. They all have agency problems: bad actors in some department or other, from time to time, poorly monitored (in hindsight). If I would judge on a single data point, I might look at its performance as the holder of my (recently paid off) home mortgage. It provided me in around 2010 with a simple, clear 1-page mortgage modification contract that was the best consumer contract of any kind I have ever seen, bar none. Its interface with me was good, for whatever that’s worth. Dimon spins out those scenarios all over the map for years. There’s nothing I can imagine is fraudulent about that (so far).

“a data point or two” ???

JPM

COMPLETELY ignored bernie madoff’s scheme for over a decade, and facilitated the entire thing. in other words, he couldnt have pulled it off without JPM.

COMPLETELY turned a blind eye to jeffrey epstein’s horrific activities for a decade plus, and facilitated the entire thing. in other words, they were his accomplice the whole time.

gambled with its own depositors money and lost over 6 billion dollars in the london whale scandel..

admittedly rigged countless different markets for its own benefit over decades…

and lets not forget: was neck deep in the GFC shenanigans back in 2008/2009.

and yet.. you have the gall to suggest ‘a data point or two’ ??? like some kind of frivolous type-o? that is.. WOW..

it really does not matter what its ‘interface’ with you personally has been. the sheer magnitude of the grief, damage, and abject criminality this single entity has perpetrated on people/society is nearly incalculable.

but they did your mortgage mod OK, so that absolves them of any wrongdoing in your eyes, huh? what a joke.

Well the first hurdle that you, frankly, fearfully exclaimed, is Dimon is something he clearly is not. If we are being frank he is a man that has earned respect.

Which we all hope, somehow, even the winners will take pity on their victims and be honest.

The everyday man is always the unsung hero.

It’s his job to lay out different scenarios. Many times I see his interviews and he speaks with probabilities and asks his team to prepare for it. All Media and Journalists make a news of every his statement. They just take one part and say it out of context.

I remember he said 5% Fed Funds rate possible and that time Market folks said hell no. It happened. He said he has asked his Bankers to prepare for 6-8% too. He said 10 yr to go above 5%. It did go for very brief time.

One thing is when all other Too Big To Fail were buying 10 yrs at record low yields, Chase stayed away from them. This has helped Chase on their balance sheet and paper losses. So I guess Credit is due to him.

He is no saint or something. Pure Businessman and CEO. But damn good at his job.

JPM suckles at the tit of the Fed. Jamie has his mouth wide open.

And he needs a change.

By him I assume you are referring to Jamie Dimon, the banker that dismantled the New Deal America.

The leader of the Capitalist’s calling the shots, too hire the labor monopsony, the Communist Chinese Party, to compete with American labor.

What he said should be considered drivel unless said drivel was needed to counter another jet of drivel directed at me by a relative.

He literally says this over and over.

I like the guy, but why does he always say the same thing?

Since you never revealed what you think he says, then it is impossible too guess what exactly a man you are apparently attracted too would say, without knowing who he might be.

Are you talking about the stud, Jamie Dimon. A man that is paid, millions, to promote a certain business model. So, yes he may say the same thing unless he said something different.

Life is not predictable, thank goodness.

On day congress will ban zero interest rates

Will never happen. They couldn’t come to a consensus to ban or even limit QE. Both parties are drunk on government spending, whether it’s welfare spending or tax cuts.

Politicians’ only motivation is looting the Treasury to buy themselves to their next reelection.

Agreed.

If Congress were capable of changing, it would have changed long before 100%+ Debt-to-GDP.

The depressing truth is that it is very likely that the Congress will have destroyed itself and the national economy before the pathologies stop.

Regardless of the political side you are on.

Congress could have restrained spending (or, inconceivably, cut spending in pathological areas) – but it hasn’t…for decades.

Congress could have raised taxes (inconceivably, upon the most otherwise exempted) but it hasn’t….for decades.

That leaves money printing, currency debasement, and more likely ruin.

And *that* is what Congress chose.

Certainly the tax cuts transferred the public money being spent on public projects into the pocket of the already rich. A distasteful lot.

Matched only by my dismay at the greed that is the primary motivator of our legislators not public service.

The budget buster is the blank check for defense spending since the destruction of the twin towers. IMO, wasted.

If the Fed is supposed to be neutral, shouldn’t Congress do the same?

Congress is a political branch of government: if 51% of its voters want something, at least at the individual Congress member level, it is usually expected to head that way. It is a people-pleaser, not a stand-alone beacon of conscience. Respect for rights, wisdom, conscience and national balance are imaginary (and sometimes actual) constraints on that. The Fed by design is supposedly to be different, with some wall of separation from the immediate tug of the political branches (Congress and Presidency).

Good thing 49.9% of voters cannot agree with the other 49.9%

lol!

One watches Yellowstone hoping Costner will return and the other is watching HGTV on what shade of gloss grey to use. Hehe. ‘Murica baby

Humans just crawled out of the ocean as microscopic sea creatures a few million years ago.

I looked at my finger under a microscope, I found microscopic worm creatures crawling around on my skin. I was thinking that I once was one of these little creatures squirming around in the sea….you probably think I’m tripping.

I watched the “incredible shrinking man” last night, he was hiding in a match box as a spider was trying to find him. I reminded me of the incredible shrinking dollar.

Yes of course, in a perfect world, the referee is neutral. In the real world the characters may tilt the short term outcome.

I’m rooting for the beautiful naivete that comes with honesty.

Congress can’t reach consensus on much at all. The Supreme Court, in a June 2024 released decision, shifted an enormous amount of the federal regulatory-rulemaking burden from agencies to that very dysfunctional Congress, which can’t get the most rudimentary budgets done. It can’t tie its shoes and make a cup of coffee (which I believe is ultimately constituencies’ fault: I mean ours), and now its job just got orders of magnitude more big and complex. Likewise in that moment, SCOTUS shifted much burden to scattered courts which can’t comprehend a light bulb, much less modern tech, but they know which local oligarchs to please. SCOTUS is already flooded with “emergency” petitions from companies seeking to exploit this chasm which has opened up. This includes financial regulation and enforcement (SEC, etc.) which is pertinent to this site. Just in time for crypto and “DEFI” lobbying money to arrive in Washington at scale.

Phleep-

Great summary of SCOTUS Chevron Deference ruling. Are you suggesting that the reigning in of agency regulatory power that Chevron Deference decision represents, and that re-placing the onus of federal regulation back with congress, is undesirable?

The nub of your comment gets to much of the discussion in Wolfstreet comment section: what is the proper size/scope of the regulatory state, including especially the Federal Reserve System?

For sure the Chevron Deference ruling increases dramatically the work-load of the court system years into the future

(Aside: Are there ETF’s that invest in publicly traded corporate litigation firms; or the lobbyist industry? – /s.)

Respectfully.

The sad part is that it took the Supreme Court to remind congress of its responsibilities.

The Federal regulatory agencies are arms of the Executive branch, and they have been weaponized by both parties to produce guidance that achieves partisan goals. This is not what the founders intended and it circumvents Congress and it’s duty to make the law.

Congress has been happy to offload the very hard work of lawmaking so it can spend time naming post offices, grandstanding on votes of only symbolic importance, holding hearings that get them media attention, and raising money for their campaigns.

If Congress can’t get it done, which it likely can’t, it’s probably time to return to what the founders intended.

Let the Federal government take care of national defense and border control, kill the regulatory agencies or drastically curtail their scope, and allow the 50 states to do the heavy lifting, and let people choose which kind of regulation they want by voting with their feet. The Federal registry adds tens of thousands of pages of regulations per year. People always cite clean air and water, which were massive successes in the 70s, but they don’t talk about the absolute avalanche of other regs that bury our economy and are far beyond the scale of what is helpful or useful.

‘Shifted much burden to scattered courts which can’t comprehend a light bulb, much less modern tech’

Tech is not a judge’s forte, the law should be. After Ailene Cannon was twice reversed by a superior court, in pretty blunt language ” exceeded her competence” you would think she wouldn’t be allowed to adjudicate vital issues. Is the saying ‘justice delayed is justice denied’ well known in the US?

If Nixon had this court, he might have survived.

and Hell will freeze over too.

It’s done it before. The ICE Age froze hell, for sure.

Well if it’s for a few mo till after election when more is known it won’t hurt anyone. I’m set to allocate but tell me what the conditions will be … I can wait. Still have plenty of coupons rolling in….hope others do too. It does all feel uncertain in a different way than just dealing w rates and market contortions.

Wolf

It is great to see all these charts and the numbers going up exponentially. But I cannot get my hands or mind on where this $7.4T came from? The stock market went up by $20T during that time. But it is either a paper gain (unrealized) or if one has sold, another buyer must have yanked out money from somewhere else to pay for it (zero sum game). Is it from the 7 year GDP of approximately $140T — 5% saved = $7T. That GDP was supported by lot of federal deficits and money printing (helicopter money).

Can this money also evaporate like stock market gains or RE gains (when they tank)? But there is an inverse relationship — this money would buy more stocks or houses but the earnings would go down (like in Tucson, home owners willing to rent their homes for $2500 pm but expect $800K as today’s selling price — so much disconnect). If markets are efficient, how all these distortions happened?

“if markets are efficient”–warren buffett once said if markets were efficient, he would have been doomed to selling pencils on the streetcorner.

One reason the stock market has gone up is stock buybacks. You do not need more people selling one thing and buying stock for the market to go up. The biggest buyers of stock have been companies doing stock buy backs. Better yet, many borrowed money to buy stock. So there is some leverage in these stock buybacks too.

Example: Go look at the stock ticker DDS. It is Dillards. They have had flat sales since 2016/2017. 7 years. In 2021, the stock has risen from $51 to up to $450 on zero sales growth. It has dropped down to $350ish now. So the stock has risen 900% at one time and still up 700% over 4 years. Guess what, the PE is only 8. So flat sales but reduced common stock each quarter means the EPS rises. EPS growth for DDS has averaged a 48% annual increase over the past 5 years on essentially zero sales growth.

If you only looked at a chart of the EPS growth you would go…. wow….this company must be a great growth company that is growing 48% YOY. But then look at the revenue chart for the past 7 years and it is flat. So it is not at all a growth company.

PE has always stayed around 8 to 10 during this time frame. Thus, the whole rise in the stock price of 700% is from stock buybacks. Nothing else.

Stock market “value” is a nonsense figure featuring the dumbest Grade 3 math imaginable.

Just reinvested my 26 week Bill…..Waiting to see what the Fed does on Wednesday.

Wait for rates to drop; then watch the spending.

My guess is more inflation “disappointment” ahead.

Excellent. This is how banks are supposed to work. This is the job description. I never thought banks would return to normal after 2009. Thanks, Powell!

If the Fed cuts rates bond holders will have unrealized gains first, before the yield curve will normalized due to higher a CPI. A good econ lift all workers. Bank’s spread might shrink, but demand for bank’s loans will rise. Bank’s deposits and savings will rise. The gov will cut debt and SPY will fly, after a correction under 2022 high. Perhaps two corrections spread apart.

All that $1Trillion interest the Federal Government paid T-bill holders is taxable income..

The IRS will be busy next tax season…

Good point on the 1 trillion of interest. It looks like the MMF funds increased from 5.5 to 6.5 trillion lately. I wonder if lot of that 1 trillion increase is just the 1 trillion in interest going right back into the money market funds buying more treasuries.

That is my story. I have not increased my MMF buying in over a year but I am not selling and just watching the MMF account grow from interest.

But, my MMF is in a 401k. So I will not be paying taxes on it for many years yet.

I have something similar, a gov’t bond fund in an IRA. I’ve been almost shocked at the monthly (not taxed yet) interest piling up in this account. Of course Uncle Sam and his RMD are coming soon for their take.

The only good thing about paying lots of taxes is that it means you made lots of money?

Absolutely. That is exactly what it means.

Most retail investors with money market funds will not be quick to move them. I am looking for alternative investments for yield on our cash.

but but but….most Americans only have $400 in their savings account, that’s what been preach across doom gloom media…lol

Distribution is not a bell curve, and mean and median are different.

Median household wealth (assets minus debts) at the end of 2022, after financial markets plunged in 2022, was still $192,000. Meaning, even after the plunge in the markets, over 50% of US households had a wealth exceeding $192,000. This median wealth has soared since then as stock prices rocketed higher in 2023 and through the first half of 2024.

Also CDs and household money market funds are not really the products that cater to the rich. They cater to run-of-the-mill Americans, like you and me.

Less than 1% of the population is homeless (living in vehicles, shelters, couch-surfing and on the street). About 13%, including the homeless and retirees, live below the poverty line (Census data). About the bottom 25% on the income scale — including the homeless and those living below the poverty line — don’t have enough income to invest. Those 25% are the people that never really have any money unless they’re able to climb out of the hole, which many of them do (while others fall into that hole or are born into that hole). It’s not static.

But 65% of households are homeowners, and 39% of them own their homes free and clear, a new record. And about half of the renters are “renters of choice,” who could buy but don’t want to and rent in the new glitzy buildings and houses built for them over the past 15 years; lots of workers and small business owners have 401ks, IRAs, SEP IRAs, plus brokerage accounts and wealth management accounts. How do you think all these huge mega brokers and wealth managers such as Schwab, and the gazillion financial advisors are making their money? Catering to the top 10%? LOL, they’d all starve to death. There aren’t enough top 10% to go around, and there a brokers and wealth managers that specialize catering to the top 10%.

The run of the mill American has quite a bit of money – though the high end has huge amounts of money, and so there is huge wealth disparity, but that doesn’t mean that the rest of the Americans aren’t poor. People who think that most Americans don’t have anything will NEVER understand the US economy and will always be surprised by it.

Wolf,

Great presentation as usual! Thanks for explaining things so clearly that even I can, kind of, understand it.

When people ask where we live I usually answer in a box by the railroad tracks. So we don’t appear to be in the upper 50% of American Households. We’re lucky … not smart.

Of course the box is a nice, to us, condo in the downtown of a western Chicago suburb, across the street from the commuter rail station. Ha Ha Ha Ha Ha Ha

I definitely bounced around banks but mostly stayed in treasuries. The only real challenge I had with some was the amount of effort to get accounts into name of trust. Some were same day and some took months. Still have 5% APY with a saving account for my liquid needs but will see how long that holds up with rate cuts.

Looking back to the beginning edges of the GFC, 3 month treasury rate — a massive constituency of money market funds, went from about 5% around July 2007 to almost zero within 1 year.

This time, is no doubt different, but in a year, we won’t be anywhere near 5% — it was nice while it lasted — I enjoyed the compound interest.

Apparently we now return to TINA, with indexes 30% overvalued and pandemic bubbles still floating higher.

“IMPLODED STOCKS

Brick & Mortar Meltdown

Bloodletting in Semiconductor Stocks Kicks Off September: Nvidia -11.7% Regular & Late Trading, Market Cap Drops by Half a Tesla”

10 days ago “Nasdaq” was presented as not much better than t-bills. I could see a potential article that if at that moment you don’t do t-bills (but sell them) and get/keep “nasdaq-like” then you will get 5-7% return in these 10 days.

Writing that just to keep opinions balanced. Personally, “get VTI/VOO/VT and chill” is the way to go.

No-one can tell the future. Including Buffet. I still see articles in places saying that do like Buffet and get CRE… Really….

“10 days ago “Nasdaq” was presented as not much better than t-bills. ”

That’s still the case today. If you had sold the Nasdaq Composite in Nov 2021 and bought T-bills with the proceeds — that was the precise context 10 days ago and not the generic statement you made — you would have been better off today than keeping it, risk free without all the drama of the plunge and then the 70% recovery rally in 2023 through July 2024.

But if you had put your entire nest egg into Nvidia in November 2021, you would have been far better off. And now you could pull a Buffett, sell all your NVDA and buy T-bills with it and chill.

Or you could have put your entire nest egg into B. Riley Financial in November 2021, and you would have lost 90% of it by now. There are over 1,000 stocks in that category, so much to choose from.

I’m not giving investment advice; I’m cracking down on all this silly maligning of T-bills and CDs that some commenters wallow in. I’ve just had enough of it. People have no concept of risk anymore. But risk is THE most fundamental principle in finance, and it has a price. But people now think that it doesn’t have a price.

Wolf, well said. I guess a lot of investors have not been through the long down times

Very true Wolf, I have been on this planet for a good while and “risk has a price”, in everything. Thanks for all the excellent work.

The risk concept always goes out the window at market highs. Peruse bogleheads right now and you see new threads arguing for 100% equity allocations.

You always see “what about inflation and what about taxes” applied to CD and Treasury returns (especially individual ones)….last time I looked taxes are applied to stocks, bond funds, etc etc. And inflation effects all equally.

You know stocks like Raymond James Financial, I just don’t get?

Raymond James is like an insurance brokerage. You pop by thinking you will get into the market and it’s just a bunch of insurance agents pretending their fiduciaries thru sleight of hand. I mean I get insurance people love to sell products, and they are very good at it.

But why on earth is RJF a stock?

The increase in MMMFs is an increase in the supply of loanable funds activating monetary savings, but not the supply of money. I.e., it is a velocity relationship. Consequently, the demand for money is falling / velocity rising.

That’s suppressing rates.

I’ve got everything in Money Market Funds and CDs. I sleep well at night and get a guaranteed 5% return. I also have a short term tax free muni bond fund which is starting to perform well. I’m 3 for 3.

Let’s hope that lasts…

Prob gonna drop to 3% at some point. Maybe within the year.

But hey better than the Bernanke days! Wooo

Another great article! I had moved 250, 000 from t bills to high-yield savings account, it was just easier to deal with, it was amazing I was getting almost 0% interest from Chase Bank and then I went from that to getting a little over $1,000 a month interest. I don’t know what Chase bank is thinking it seems like they would give you a little more there must be something to that.

Here I don’t know if you can include this link to a video I had made about the high yield savings account or the one that I thought was the best I did a lot of research and a lot of trial and error and it’s what I thought was the best and works the best for me.

Dang $1,000 a month, that’s sick.

It’s like you have a little invisible man (perhaps a grumpy one? Who knows) who goes to work 40 hours a week and brings home $6.25 an hour.

Luckily he’s not taxed or Fica’d, well cuz he’s invisible.

💼 😆

That’s a good way of thinking about it.

I hope my little man doesn’t run off with half my money like he did in 2008.

Thanks to J Powell, he was forced to return it all by now.

I’m very happy earning 5.28% risk-free with Schwab’s Value Advantage MMF.

FYI

From the Schwab Value Advantage Money Fund prospectus:

“The fund is subject to risks, any of which could cause an investor

to lose money.”

https://connect.rightprospectus.com/Schwab/TVT/808515605/SP?site=FundDocs

An excellent portrayal and explanation of “savings” in the US over time, Wolf.

A chart that shows Annual Interest Received on all of those forms of savings over the same timeframe would be informative, if such a thing can be gleaned. (Perhaps as a percent of total consumer spending or total household income – sort of like charting US treasury interest as a % of GDP or federal receipts).

Apologies for being tedious! Thanks for your work.

Wolf,

Any data on funds like SGOV, which invests in 0-3 month bills? It’s an ETF, not a MMF, but I’ve been using it as a “cash equivalent” since you can buy increments of $100 (vs $1000 for T-bills). It generally has a stable NAV due to the ultra-short duration and spits out a monthly dividend.

I don’t directly own those T-bills, however – the fund manager presumably does.

ETFs belong to the category of stocks in that they trade publicly, and if you want to get your money back, you have to sell the shares to someone else, and the cash changes hands between the buyer and you. This is fundamentally different from cashing out a CD (bank has to give you the cash) or a MMF (fund manager has to give you the cash), and if they don’t have the cash, they collapse. This cannot happen with an ETF because liquidity is provided by other buyers. But ETFs can lose value. So they don’t count as cash.

^ This is a characteristically excellent answer, Wolf.

The whole subject of what IS money reminds me of the poem by 20th century economist Kenneth Boulding, which I’ve posted here before:

_________

We must have a good definition of Money,

For if we do not, then what have we got,

But a Quantity Theory of no-one knows what,

And that would be almost to true to be funny.

Now, Banks secrete something, like bees secrete honey;

(It sticks to their fingers some even when hot!),

But what things are liquid and what things are not,

Rests on whether the climate for business is sunny.

For both Stores of Value and Means of Exchange

Include, among Assets, a very wide range,

So your definition’s no better than mine.

Still, with credit-card-clever computers it’s clear,

That money as such will some day disappear,

Then, what isn’t there we won’t have to define.

(By Kenneth Boulding , Michigan Business Review, March 1969, as quoted in Melchior Palyi’s book – Twilight of Gold)

__________

Few economists, past or present, have been versatile enough to pen pertinent and clever Miltonian sonnets about knotty banking subjects in there spare time!

“Money,” especially fiat money based on debt, can evolve, and not always for the better. Boulding seemed to recognize this.

Caveat Emptor.

(Apologies if the verse gets misformatted in the comments column…)

Oops, I got the wrong “their,” there…

Sacrificed at the alter…catchy…well done. So the next EVENT is already planned, just waiting on which clown they choose for the throne, I’m thinking this one will be mother nature event on west coast…people don’t trust Wall Street and their bubbles…how many yachts can you own at once…sports entertainment is imploding…what’s the script Mr. WOLF…TC.

The issue of yields is huge with Fed in the circus spotlight — are we on the cusp of seeing plunging rates in just a few days?

I reluctantly watch Jeff Snider occasionally, continually tired of the same song for a decade plus — but he recently made a decent case about the 2-year treasury being below Fed effective yield — which is rare.

That’s supposed to indicate current yields being too tight, or not.

As we’ve watched for a year with CME projections — along with Wolf constantly reminding everyone that CME is generally stupid, and Wall Street hype for cuts is always insanely stupid.

Nonetheless, the blabbering idiots are now projecting something like nine cuts (again). The astrology forecasts and tarot cards are definitely in hyper space traveling through well worn wormholes.

Even with all that BS, yields have been falling hard, along with oil — but I’m wondering if Wall Street is getting better at manipulating volatility and ramping fear and greed into more efficient, more predictable micro patterns.

Maybe we’re just seeing a new upgraded version of manipulation that super amplifies stressful volatile news cycles — and coordinates narrative into actionable manipulation?

Whatever polarized narrative gets picked up on, this new upgrade expands the envelope exponentially.

I think a cut of 1/4 is too much, but a conservative notch lower is calm, versus panicky — nonetheless, seems like lower yields will just drift lower.

I’m thinking they cut by 0.25. I have heard reasonable cases for a 0.5 cut.

The 3-month appears to be pricing in a 0.50 cut (in the next 3- months?).

I’m wondering if this is a buy the rumor, sell the news event (as usual?)?

“once again gutted by the Fed”

I’m inspired by the mental image of this turn of a phrase.

The latest personal savings rate I could find was July 31, 2024 at 2.9%.

The long term average is 8.44%.

2.9% is unusually low.

This is the EXACT BS that causes me to post these articles. The Savings Rate is the difference every month between what people earn and what they spend, expressed as seasonally adjusted annual rate. But it doesn’t include income from capital gains, stock sales, home equity, etc., but it includes all interest expenses. People have forever used this data point — clueless about what it actually tracks — to show that Americans are poor, don’t have anything, are tapped out, charge everything on their credit card, don’t save anything, etc…. just braindead BS. Which is why I rub the growing trillions of dollars that consumers actually have in cash savings into your face, to disabuse you of this BS, LOL.

I cover the savings rate in my articles about consumer spending. You can see the chart there.

Yes! I’m soooooo tired of that personal savings rate is low BS… I see too many parrot that line without even understanding it. Look at ALL that cash on the sidelines.. it’s at record levels. Look at the equity markets.. near all-time highs. Equity in their homes.. most people are NOT poor, folks.. wake up!

That’s why I always read your stuff…unadultrated data…

Re: the Canadian banks like Canadian Imperial Bank of Commerce, that I was in briefly. Wish I’d stayed in instead of leaping into a tech that while recovering took a big hit. CIBC has risen a lot in last 10 days, to the point where I’ve stopped looking.

The Canadian banks are paying more for deposits but are making more on mortgages. Not everyone here went 5 yr although they must have been nuts to think rates on the 5 would go lower than the 2.2 scored by a couple written up in Globe and Mail. Lots went 1 yr, 2 yr or variable, which can change monthly. Played poker with a realtor and he said a lot of folks are getting big boosts in their mortgage payments. So from viewpoint of the banks’ income, are they ahead or behind?

The Canadian banks are among the world’s most successful oligopolists. I buy them all and sleep like a baby …

I’m collecting about 4.5% from my HYS. When this changes (and it will), I guess I’ll just put back into the market? I don’t like lock up my $ in CD…want access.

I hope someone from the banking community or Wolf responds to Pascal’s comment about CD liquidity versus stock market “liquidity.”

Assuming his comment was not made using sarcasm, it’s a dangerous view (stocks more liquid than CD’s) to pass on to inexperienced investors who might be looking to inform their own investment decisions…

You may have misread what Pascal said. He said “my HYS” = high-yield savings account. And he said: “I don’t like lock up my $ in CD.. want access.”

Savings accounts are same-day or next-day (if after 2 pm) liquid, just transfer your money out. Now try to sell a CD. If it’s a brokered CD, you can eventually, maybe, after some time, sell it with a haircut. If it comes directly from your bank, you may not be able to sell it at all, or you may be able to get the bank to redeemed it with a haircut. That’s what lack of liquidity means.

So if you want to keep your powder dry to pounce on something, don’t put it into a CD. Put it into T-bills at your broker (can sell easily), money market funds, savings accounts, etc. That’s kind of what Pascal is doing.

“Put it into T-bills at your broker (can sell easily)”

Not necessarily – on occasion I’ve been unable to liquidate certain CUSIPs due to broker restrictions.

Pascal,

I agree with you that High Yield savings accounts are good at 4.5%. 1 month and 3 month TBills are almost a point higher. To preserve liquidity, I keep 25% of savings in the savings account and auto-withdraw into TBills for the rest. Money goes in on maturity and out on purchase of the savings account thanks to Treasury Direct. I use my high yield savings accounts as a sweep account. TBills are tax free from state income taxes unlike CDs.

If rates fall far enough, I will look at large cap high dividend stocks (taxed at 15% for some) and index stock funds. I think the TBill rates need to be below 3.5% to make me move.

TBills won’t make me wealthy but they won’t make me poor. My criteria for buying index funds is severe. If they fall 20% like in 2020, then I’ll buy. The volatility now is noise.

I subscribe to the theory that you buy into the stock market when the trend over 3 months is up over 5%. I need to wait. That ain’t happening now.

The information that I would like to know is, where is all the demand for T-bills coming from. Aside from me, who else is buying the short end? What percentage of those buyers are foreign entities?

“where is all the demand for T-bills coming from”

It’s coming from Warren Buffett, and from me, LOL, and from lots of other people here, and from money market funds, and from corporate America and banks, etc. Huge insatiable demand. Look at the auction results.

I wanna know the opposite – where is all the demand for duration coming from? Who in their right mind is buying 10 years <4%??

Just think of Powell’s interest rate inversion.

Link: “The 2006 Financial Services Regulatory Relief Act gives the Fed permission to pay interest on reserves. The IOR rate was always higher than “the general level of short-term interest rates” which is imposed in the Law. “A Legal Barrier to Higher Interest Rates,” The Wall Street Journal, Sept. 28, p. A13.

This creates a monetary policy blunder or non-bank dis-intermediation. It destroys money velocity. It reduces N-gDp (overall incomes).

I’ve been wondering with the way our politicians keep spending if we have no choice but to cut rates because the interest payments on the national debt and we’ll just tolerate 3% inflation and bubbles? The rich will get richer and the poor will get poorer and the middle class will slowly dissolve much like a lot of South America

I’m curious what these numbers look like if we looked at medians. Yes we all know the rich are doing well. Rotating out of risk into cash type assets totally makes sense when you can get 5% risk free and the market looks bubbly. I’m not sure we can extrapolate totals to the avg American consumer though and say they have lots of savings. I’d love to see how middle class households are doing

LOL, this BS never stops?

Less than 1% of the population is homeless (living in vehicles, shelters, couch-surfing and on the street). About 13%, including the homeless and retirees, live below the poverty line (Census data). About the bottom 25% on the income scale — including the homeless and those living below the poverty line — don’t have enough income to invest. Those 25% are the people that never really have any money unless they’re able to climb out of the hole, which many of them do (while others fall into that hole or are born into that hole). It’s not static.

But 65% of households are homeowners, and about half of the renters are “renters of choice,” who could buy but don’t want to and rent in the new buildings and houses built for them over the past 15 years; lots of workers and small business owners have 401ks, IRAs, SEP IRAs, plus brokerage accounts and wealth management accounts. How do you think all these huge mega brokers and wealth managers such as Schwab, and the gazillion financial advisors are making their money? Catering to the top 10%? LOL, they’d all starve to death. There aren’t enough top 10% to go around, and there a brokers and wealth managers that specialize catering to the top 10%. The run of the mill American has lots of money – though the high end has huge amounts of money. Get used to it or you will NEVER understand the US economy.

Also CDs and household money market funds are not really the products that cater to the rich. They cater to run-of—the-mill Americans, like you and me.

Median household wealth (assets minus debts) at the end of 2022, after financial markets plunged in 2022, was still $192,000. Meaning, even after the plunge in the markets, over 50% of US households had a wealth exceeding $192,000. This median wealth has soared since then as stock prices rocketed higher in 2023 and through the first half of 2024.

You people need to get off of this nonsense.

The majority of everything you lay out as a case for exceptionalism is indisputable— but to push back a bit, I suggest that much of this Wealth Effect is linked to the Everything Bubbles — which is further amplified by a lot off people falling into this unique period of a stock index like S&P being totally distorted by nividia, ai and mag5.

If liquidity gets further sucked out of the market or if markets simply trend sideways the next six months — with epic/generational volatility — the genius cohort is just drifting along for the ride up, are susceptible to more risk than they have been seeing.

That gets back to the point of decreasing yields and being in a position to accept the decline as a way to reduce risk short term — or to jump into the volatility game and chase extreme risk and whipsawing swings that go nowhere.

Cem Karsan believes the Feds main mandate is to protect the Wealth Effect — so maybe all this noise is meaningless in the long run?

Redundant,

“…but to push back a bit, I suggest that much of this Wealth Effect is linked to the Everything Bubbles”

RTGDFA. The entire article is all about interest-earning CASH. It’s not invested in bubble assets; it’s invested in CDs. money market funds, and T-bills, whose value doesn’t change much — that’s what the entire article is about.

I actually was asking a question. And I think it was misinterpreted. I’m curious how the median American is doing outside of their home equity and 401k? How much cash that they can actually spend is still sitting on the sidelines? I mean I have a lot of money in my 401K, but if I’m touching that and not retired, it means I’m in trouble. It’s not my piggy bank.

I have a place to live and a few porkers in the pen so I’m ok.

Poverty will find it’s way to our shores if we’re not careful…but now everybody is fat and carefree.

I was walking around Walmart today, guess it’s ok now to just open up the chips….start eating…roam the aisles with your mouth full of food.

If they scan the code and pay for them at the time of checkout, and Walmart doesn’t care, what’s the problem? I’m assuming these chips are being pilfered (we hope).

Seems like a win win. Wal Mart sells an extra bag of chips and the buyer gets some entertainment and calories while roaming the store.

It just bothers you to see this, or what, lol?

I’ll head over to your house and help myself to your fridge…

Guess I was raised differently, guess I could sell my high horse and get burro.

Some positive numbers for consumers I read the past couple of days.

The number of mortgages underwater is 1.7% Lowest number on recorded history.

The number of homes without a mortgage rose from 1.5% to 39%.

1.5%? Is this a mistake? Isn’t the norm 1/3 of homes are paid for, about 33%?

When they remake The Big Short they will have to skip the strip clubs with the “irresponsible subprime borrower” part, and go right to the TBTF Wall Street wh- houses.

A lot of “what is money” posts in this thread.

Meanwhile, I look at CAPE10 for the S&P, yield over inflation, housing prices verses wage gains, and the feds cutting rates and go, yep, makes sense some folks are holding more cash. Not that they’re necessarily right…the future is unknowable. But the play makes sense. Not a ton of bargains out there.

MW: Berkshire’s stock hadn’t seen a losing streak like this in a decade and a half. What’s causing it?

BRK is down 6.4% from the all-time high on Sep 4. So in terms of a percentage decline, there were much bigger ones. But in terms of days in a row of small declines, maybe that was a long “losing streak.”

All this money in savings sounds good. However, I’ll bet that chart of how much savings per household is held in the different income ranges would tell a story that is not so good for 60% of Americans. Disparity in wealth is a main contributor to internal strife and conflict.

LOL, this BS never stops?

Median household wealth (assets minus debts) at the end of 2022, after financial markets plunged in 2022, was still $192,000. Meaning, even after the plunge in the markets, over 50% of US households had a wealth exceeding $192,000. This median wealth has soared since then as stock prices rocketed higher in 2023 and through the first half of 2024.

Also CDs and household money market funds are not really the products that cater to the rich. They cater to run-of-the-mill Americans, like you and me.

Less than 1% of the population is homeless (living in vehicles, shelters, couch-surfing and on the street). About 13%, including the homeless and retirees, live below the poverty line (Census data). About the bottom 25% on the income scale — including the homeless and those living below the poverty line — don’t have enough income to invest. Those 25% are the people that never really have any money unless they’re able to climb out of the hole, which many of them do (while others fall into that hole or are born into that hole). It’s not static.

But 65% of households are homeowners, and 39% of them own their homes free and clear, a new record. And about half of the renters are “renters of choice,” who could buy but don’t want to and rent in the new glitzy buildings and houses built for them over the past 15 years; lots of workers and small business owners have 401ks, IRAs, SEP IRAs, plus brokerage accounts and wealth management accounts. How do you think all these huge mega brokers and wealth managers such as Schwab, and the gazillion financial advisors are making their money? Catering to the top 10%? LOL, they’d all starve to death. There aren’t enough top 10% to go around, and there a brokers and wealth managers that specialize catering to the top 10%.

The run of the mill American has quite a bit of money – though the high end has huge amounts of money, and so there is huge wealth disparity, but that doesn’t mean that the rest of the Americans aren’t poor. People who think that most Americans don’t have anything will NEVER understand the US economy and will always be surprised by it.

You people need to get off of this nonsense about most Americans being poor, it’s just BS.

Perma bull Wolf Richter!!! NVDA to $150!

65% of households are homeowners, but how many of those folks could afford their own home if they had to buy it at today’s price levels and mortgage rates?

We’ll never know how weak or strong our economy is until the unsustainable artificial interventions end, allowing asset prices and interest rates to reach true equilibrium. Until then, the Fed and legislators are simply transferring wealth from those who earn it to those who engage in unsustainable behaviors.

Jerome is almost ready to, once again, stab savers in the back.

He wants you to go out and buy some Goddamned equities,(just in time for those to crash).

Also buy some overpriced houses too. The upper one tenth of one percent need your money, gentle sucker( I mean reader).

Right now, short-term risk-free interest rates are way above inflation rates, which is very unusual. You don’t normally earn this kind of “real” interest rate (interest minus inflation) without taking some credit risk or duration risk, or both.

Off-subject, but Bloomberg article today, headlined:

“Fed Ready to Unshackle US Economy With Soft Landing at Stake”

Opening paragraph:

”The Federal Reserve will begin a crucial pivot this week, lowering interest rates for the first time in more than four years as it pursues a rare soft landing for the US economy…”

Within the article they do use the term “wisely expected,” but sheesh, has there ever been such consensus, or such an insistent and near dictatorial mainstream media?

I see Warren & gang are demanding a 3/4 cut.

I’m sure that way they can stomp their feet when

Powell only gives a 1/2pt.

After Powell said he was ready to lower rates, the media indeed came to expect it.

I’ve been moving out of MMFs and into the market. Lower rates without the possibility of price appreciation, drove me in this direction.

I liked the monthly distributions so I set out to find securities that paid monthly with a long-term track record of increasing NAV. 8% yields are also a big plus. EOS, ETY, CSQ, SCD are a few that working well.

I am buyying NVDA!! It is going to $150 before end of the year!! Hop on train!

Wolf,

You have the patience of a Buddhist monk. But I do like when you go all Shaolin kung fu on the unbelievers.

Folks, there is no place like America. Click your heels and always wish to go home. Good luck.

Expected Three-Month Average SOFR Path From Atlanta Fed showing at least100 Bps downdraft in next 6 months, potentially taking the 3M around mid 3%, with sticky inflation hovering around that range — but with increasing likelihood of recession within this exciting framework.

3 month at 4.86% today — try to get a cd, treasury of money mkt above that — you won’t — enjoy the ride down, with equities to follow.

Fyii

Money markets run to max peaks right before recessions, kinda like GFC and dotcom, and obviously a year from now this peak cycle will crash because of low rates

Amrn