But a drop in energy prices had a soothing effect on overall PPI, which also accelerated, but by less.

By Wolf Richter for WOLF STREET.

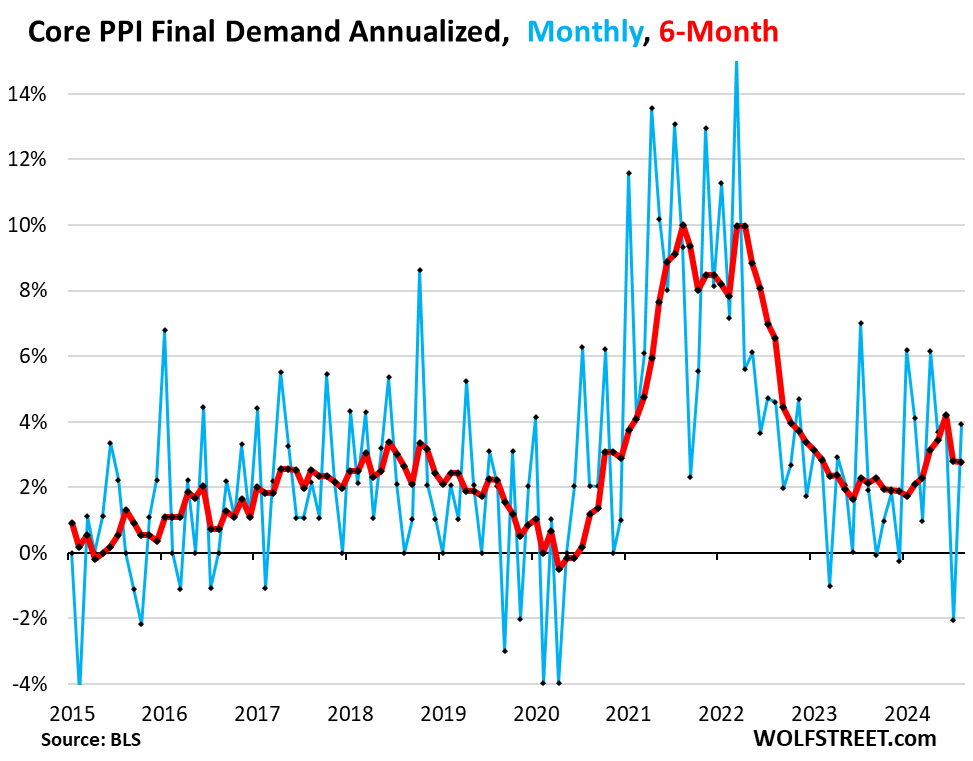

The Core Producer Price Index bounced back sharply in August from the negative reading in July that had been heralded as yet another sign that inflation was dead. So inflation is not dead. The bounce-back was driven by the massive bounce-back of the Services PPI and, very interestingly, a spike in the Finished Goods PPI.

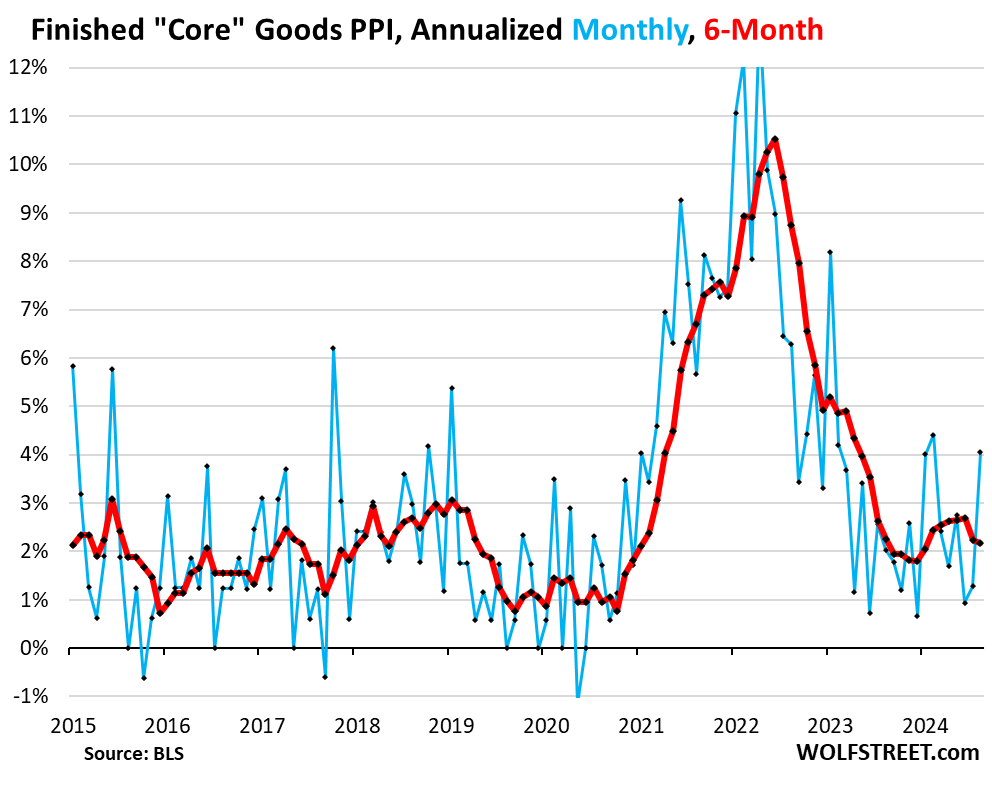

“Core” PPI jumped by 3.9% annualized in August from July, seasonally adjusted (blue in the chart below), driven by services (+4.6%), which dominate core PPI, and also by finished core goods (+4.1%), according to data from the Bureau of Labor Statistics today.

The 6-month rate – which irons out some of the whiplash volatility of the month-to-month readings and includes the often-hefty revisions – remained at 2.8% in August, same as in July. Note how the 6-month rate shifted higher this year, after being well-behaved in much of 2023 near 2% (red).

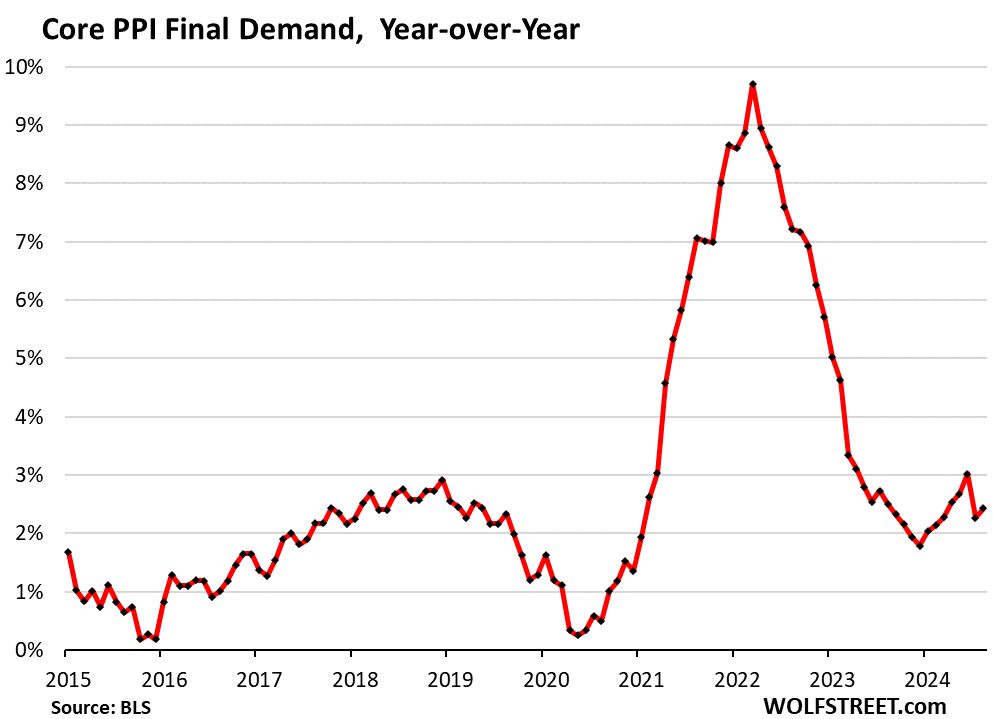

Year-over-year, core PPI rose by 2.4%, after the big deceleration in July that had been driven by the base effect in services that will abate for the remainder of the year.

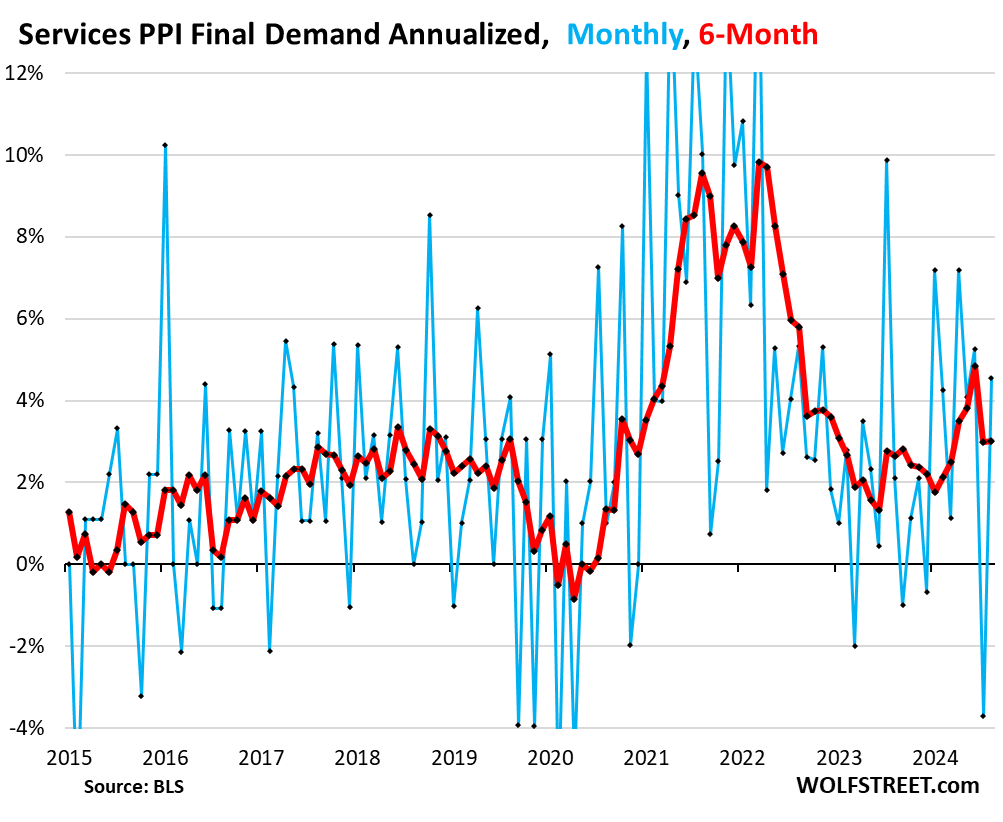

Services PPI jumped by 4.6% annualized in August from July, seasonally adjusted, after the negative reading in July (-3.7%) that had followed to hot readings in the prior months (blue in the chart below).

The 6-month average rose 3.0% annualized, roughly the same increase as in July. Note how it shifted higher this year, after the lower readings last year.

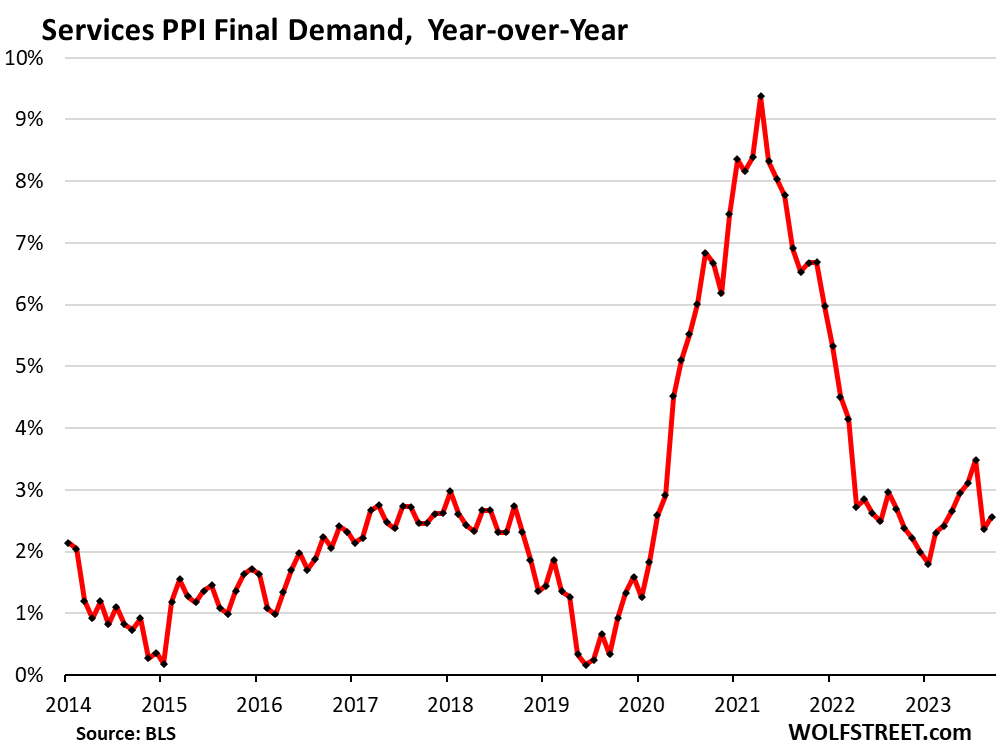

Year-over-year, the services PPI accelerated to 2.6% in August after the sharp deceleration in July that had been the result of the base effect, when the freak month-to-month spike of +9.9% annualized in July 2023 (highest in over two years) fell out of the 12-month range of the year-over-year readings and was replaced by the plunge of -3.7% annualized in July 2024 (the lowest since March 2020). Going forward, the low-to-negative month-to-month readings last year in August through December will come out of the 12-month range and be replaced by the readings going forward, and the base effect that rattled the index in July will fade out.

“Finished core goods” PPI started to act up again in 2024, after being well-behaved in 2023. The 4.1% annualized jump in August from July was the biggest since February and the same as January 2024, and all three had been the highest since January/February 2023.

As we have seen all around, there have been no major inflation pressures building up in core goods in over a year. Inflation has been largely wrung out of core goods. And core goods have been a big factor in bringing inflation down. So this spike in August is not welcome.

But compared to the fiasco in 2021 and 2022, the current situation with core goods is benign:

The PPI for “finished core goods” includes finished goods that companies buy but excludes food and energy products.

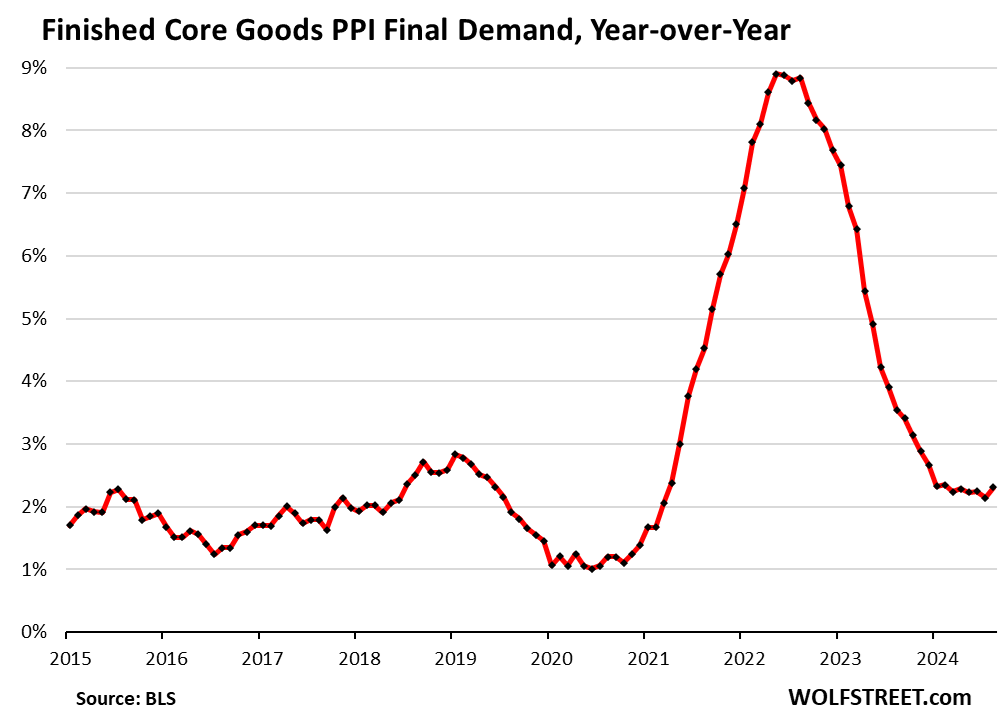

Year-over-year, the finished core goods PPI accelerated to 2.3% in August from 2.1% in July, and the highest since February. Just a bump in the road, or a change in direction? A change in direction would be very unwelcome.

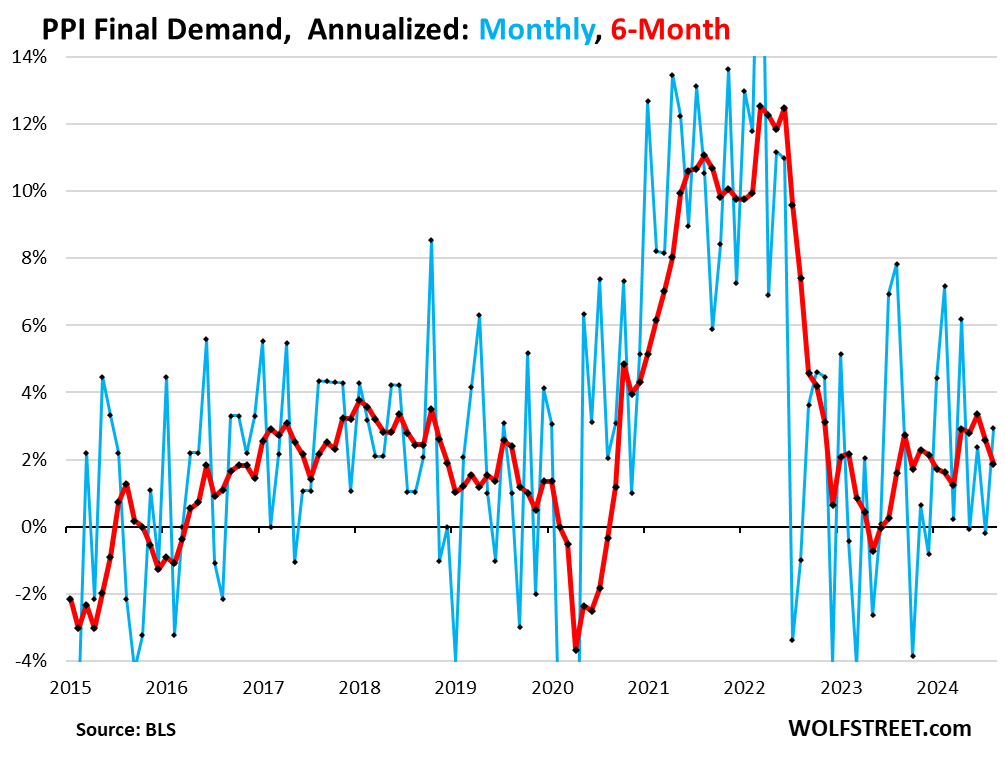

The overall PPI for final demand jumped by 2.9% annualized in August from July, after a negative reading in July, as drops in energy prices softened the impact of jumping prices for services and core goods.

The 6-month rate decelerated to an increase of 1.9% annualized. So, driven by the drop in energy prices, overall PPI looks normal. But energy prices cannot drop forever.

The overall PPI tracks inflation in the goods and services that companies buy and ultimately try to pass on to their customers.

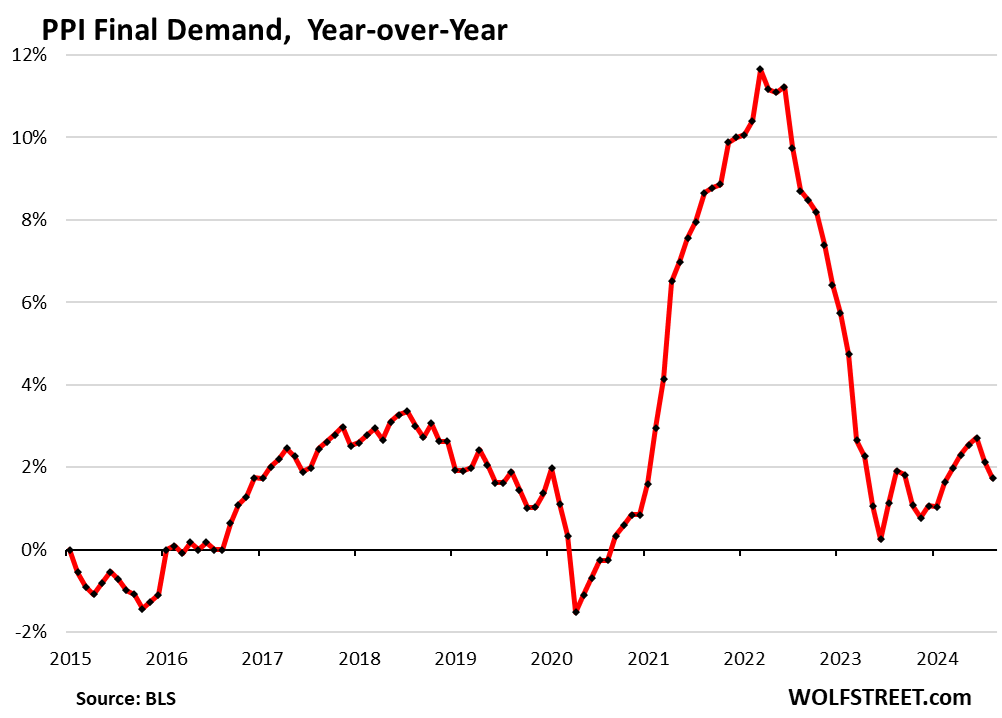

Year-over-year, overall PPI rose by 1.7%, a deceleration from July and June. June had been the highest since February 2023:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

it will be interesting to see where the new “Normal” ends up being after so many years in our crazy covid economy and prior to that, our crazy zero interest rate economy. It seems like we’re approaching a new baseline.

Well put

Although FED has not stated but new normal is 3% inflation.

How would we know this: if FED cuts in Sep, then new normal is 3% if they don’t cut they they stayed true to explicit 2% inflation.

I generally agree with your comment and the point you are making and how you come to the specific conclusion.

I want to say though, that even if the FED hypothetically doesn’t make a rate cut soon, it doesn’t mean that they stayed true to reaching a 2% inflation target. To me, it still means that they are in support of something like what you are referring to, such as a 3% rate of inflation. I personally think they are have been and still are comfortable with inflation higher than 3% but I won’t try to dispute your point on that. I am taking a more negative view while in agreement with the point you are making. I would say that if they hiked interest rates by even a quarter of a percent, they maybe they could pretend to want inflation to return to 2% in some type of reasonable time frame (such as in our lifetime). They’re all talk, just like the politicians. How do you know when those types are like, as they say? When their lips are moving.

People seem to be giving the central banks a lot kudos for a job not well done.

Don’t quite agree. Even if the FED cuts the rates (most likely 25bp), it will be still above all the inflation measures (CPI, PCE, headlines, cores) and be restrictive.

But I think the real problem is the very slow pace of QT. The slowness emboldens the bulls, consequently putting an upward pressure on asset prices, which translates into consumer inflation with delay. Hence, I hardly think the inflation will go down to 2% in next 2-3 years. In fact, it can go the opposite way and climb up due to irreversible housing inflation due to the exploded RE prices (because of past wreckless QE and govt spending).

That’s a completely incorrect statement. Waiting until inflation is at 2% to start cutting rates would guarantee a recession. The Fed would be WAY behind the curve. Interest rates take 6 to 12 months (maybe even up to 18 months) before we start to see the effects.

Oh I am sure this is transitory…rate cuts already left the station from WS perspective even though it hasn’t happened yet but perhaps the probability of not happening even with this reading is soooo low, they already march on to the next shiny object

I’m equally sure oil/energy prices will never go up again. China’s demand will not go up again. Everything will be sweet perfume and roses now and forever.

DM: GameStop plots mass store closures after shutting 300 locations in past year

GameStop has announced that it plans to shut down more stores amid dwindling sales.

The retailer said it is struggling to sell new and used video game discs in-store as Americans shift toward digital downloads, streaming and online shopping.

Following the announcement of its second-quarter earnings this week, bosses said they are identifying stores for closure.

Worryingly, they said they would shut down more outlets than it has done in the past few years.

In March, GameStop announced it had closed 287 stores worldwide over the previous 12 months, leaving it with just over 4,000 physical locations.

GameStop was at the center of the ‘meme stock’ trading frenzy during the Covid-19 pandemic which sent its stock to dizzying levels – but it has been struggling with sales and profitability.

Shares in GameStop tumbled 15 percent after its earnings report on Wednesday, and are down over 7 percent in the past month.

The video game retailer reported a 31 percent drop in quarterly revenue, sparking fears from investors that the company will not be able to turn things around despite store closures.

GameStop has already closed all its brick-and-mortar locations in Ireland, Switzerland and Austria.

Revenue for the quarter ended August 3 was $798.3 million, compared to $1.16 billion a year prior.

Quick we need Roaring PU$$Y..kitty to pump this back up to the moon again..

My grandkids only buy games they can download. I guess that’s what they all are doing anymore. Goodby Game Stop!

Even Intuit said no more TurboTax program on CD. It will only be sold going forward via download.

I used to ride my bike up to blockbuster and similar places to rent games.

Grabbed a Burger King $2.22 meal while up there, 2 burgers, 2 fries for that.

Fast forward a bit, used to go to the mall to look at PC games. Never really had enough money to buy them outright.

Then the used game places popped up, those were great. $5 or something and grab a 8 year old Super Nintendo game.

This was all before having a job, cuz after that it was mainly computer games and not many at that.

Anywho, just saying I do not really get stopping at GameStop and spending $50-$100 even today. Go on steam and shop the sales. You can even set a reminder to tell you when it is on sale. Even the particular title you want.

And GameStop straight robs you buying your games back, which they resell for way more.

I’d never buy their stock

“ energy prices cannot drop forever.”

US policy may affect this. One guy wants cheap energy, the other party wants to save the world with metals (Copper, lithium etc).

We do seem to have a regime change. OPEC doesn’t want oil prices lower and will curb production. Even IS shale has a floor (barring government intervention and subsidy).

QT will be more of the elephant moving forward as Pow and Co search for the elusive “r*” neutral rate.

The inflation floor may be 2%, and we may be near the floor for the US oil price. Of course markets are behaving badly (high volatility, yield curve normalization) and the chorus of “economic cliff” folks is again at fever pitch.

I look to geopolitical issues and fiscal policy more than monetary policy for the next “big shock” to the system. Without that, we’re hanging at the punch bowl, refilling until the last drop!

DM: California burger chain founded by Kevin Hart abruptly closes ALL locations

The fast-food chain co-founded by comedian Kevin Hart has closed all of its locations just two years after its debut. It is the latest in a long line of restaurant chains to struggle this year. On Instagram, Hart House posted a farewell message: ‘Thank You. A Hartfelt goodbye for now as we start a new chapter.’

Something like 60% of all restaurants in the US fail within the first year of opening, and 80% fail within 5 years due to the incompetence of their owners. There is nothing special about this.

What’s “special” about this is that the hamburgers weren’t meat but fake meat vegan. I had one bite of this stuff once. Why not just eat actual peas not dressed up as hamburgers? Peas by themselves are delicious. There was a fake-meat craze for a while after the Beyond Meat IPO, which is another Imploded Stock.

Restaurants are a tough business. You have to figure out how to get people to come to your restaurants and spend money there, enjoy everything about it, and then come back forever – and fake meat doesn’t do the trick, I swear. And you have to manage your people, and there are a lot of employees in a bigger restaurant, and you have to fund your operation, and you have to be able to do all this profitably. So maybe not the right job for a comedian whose apparently only qualification was that he was on a largely vegan diet.

Morningstar chorizo crumbles in tacos are quite good. IMO

1:04 PM 9/12/2024

Dow 41,096.77 235.06 0.58%

S&P 500 5,595.76 41.63 0.75%

Nasdaq 17,569.68 174.15 1.00%

VIX 17.06 -0.63 -3.56%

Gold 2,585.50 43.10 1.70%

Oil 69.26 1.95 2.90%

Inflation has come down, but I still don’t see a strong case for rate cuts.

Inflation rates are well below policy rates, so policy rates are very restrictive.

And we’re seeing the signs of it in the labor market, with job creation slowing down quite a bit. Companies are not laying off people, but hiring has slowed a lot. So if it stays that way, OK. But if the labor market loses more momentum, that’s not good.

The Fed’s job is to tamp down on inflation, and it did that, and it’s still doing that. And inflation has come down a LOT. The Fed can cut by 100 basis points, and its policy rates will STILL be restrictive.

It’s NOT the Fed’s job to crush the labor market for nothing.

If inflation rises again, the Fed can hike rates again. That’s how it used to do it, yoyoing rates up and down.

I guess I just like positive real yields. I have always been more of a saver than an investor. We are right near average Fed rate since 1971. I fear lowering of rates too much will just cause more asset inflation, which will feed back into inflation in general. But you are right, the Fed can raise them back up if necessary.

don’t you understand? you should be grateful to get even a 1% real yield, assuming you believe the government’s inflation numbers.

but stonk and real estate holders, they’re entitled to have 10-30% gains every year. if nvda drops by 50%, dragging the nasdaq with it, jerome better get printing. in fact, the market thinks that’s just what he’ll do.

The Fed *can* hike rates again if necessary. And that is, indeed, how they *used to* do it. But will they do it this time if needed, and if they do, will they do it in time? Their long institutional bias toward accommodation, along with the idiotic policy of telegraphing their moves well in advance lest anybody on Wall Street actually experience any uncertainty make me a tad bit skeptical.

They hiked by 525 basis points, the most in decades. So yes, they can and will.

Will they do it in time? Probably not, they were super-slow last time and they admit it and they suggest having learned a lesson. But preemptive rate hikes may not be in the cards. Just less far behind maybe.

If they’re late again, and inflation starts taking off, they will eventually hike faster and further than anyone expected — see 2022-2023.

Price rises coming down is not enough. How are people supposed to make up for prices being higher that they were? How can folks afford the “stuff” that is more costly than last year,and the year before and so on? Unless prices fall back to previous levels, buyers are worse off. Inflation is a cruel evil, (unless you are selling something).

A new golden era of prosperity coming, no matter which charlatan wins in November?

We’ve had the biggest wage gains in 40 years. In 2021 through mid-2022, even these wage gains were less than inflation and people fell behind; but since mid-2022, the wage gains have outrun inflation, for a good part of it by a wide margin, and so people started catching back up. These “real” wage gains (outrunning inflation) need to continue for people to catch up further. But that’s how you catch up: wage gains.

But yes, inflation is an evil.

telegraphing moves is idiotic, as it lets people front run them.

Wolf, thanks for the excellent report. Two questions: 1) I see energy prices are seasonally adjusted, but I can’t find a report with non-seasonally adjusted numbers. Any idea where one can be found. 2) Trade Services, as I understand it, are mostly importers profits. So, if correct, importers profits went up at a 4.6% annual rate due to raising prices. I don’t get how they can raise prices when there is a general price deflation in goods. Can you comment?

In terms of PPI, I have all data seasonally adjusted and not seasonally adjusted. Year-over-year percentages are always from not seasonally adjusted data. You can download all this stuff from the BLS data finder page.

1) In Mar 2022, when Putin invaded Ukraine, Crude oil futures, CL, reached $130. Since then CL is down. In recession CL might drop to $42. If re-accumulation it might rise $90/$100 first, before testing 2008 high. The PPI will fly above the 2022 cliff.

2) The cost of land/house in the suburbs prohibiting construction. Home builders who bought Land/house in 2011, at bargain prices, when rates were zero, are paying over 8%, bc Land/house isn’t a good collateral. Banks will not lend over 40% of the est project cost unless the builders can prove that they sold a few houses. No contracts the banks will takeover.

3) With new regulations home builders can erect 20/30 floors houses in the suburbs and 4/6 floors in the flyover areas, lowering the cost of Land/Apt by 1/50 to 1/200. Lower construction cost, negative construction rates and longer terms will reboot constructions. It will kickstart transactions even without $50,000 gov jubilee . Wages will rise. The econ will thrive ==> gov debt will be drop.

Certainly will be an interesting couple of years. We could see inflation come roaring back and short term rates rising to 6-7%. We could see a hard landing and short term rates around 1-2%. We could see the soft landing and short term rates leveling off around 3-4%. All we can do is try to stay as informed as possible, and react accordingly.

Well, I have to tell you what a clever presentation of the facts this article suggested by the opening paragraph:

” The Core Producer Price Index bounced back sharply in August from the negative reading in July that had been heralded as yet another sign that inflation was dead. So inflation is not dead. The bounce-back was driven by the massive bounce-back of the Services PPI and, very interestingly, a spike in the Finished Goods PPI.”

I thought, as I processed the suggestion that inflation is alive and well and the Fed probably should cut in September 25 bpt and see what happens.

I agree. Unemployment, which follows the downturn in business activity as the expected outcome, duh.

Unemployment is worse than inflation, perhaps.

I’ve been considering shelter rental costs. When I initially heard inflation in groceries was being blamed on some sort of corporate malfeasance, that struck me as simple economic illiteracy. Inflation is reasonably supposed to be when demand is greater than supply, and in this case, driven by monetary policy stimulus.

However with rents… with the rise of rental supermajor companies (e.g. Greystar, Berskshire, Blackrock); the collusion enabled by rent information aggregators, like RealPage (DOJ just sued them for this – top 6 rental companies use it); and the advent of cost-plus style rental leases, where landlords add additional rents per month, on top of base rent, calling them pass-through expenses – I think corporate behavior in the case of rents – collusion, company size and new billing styles – may be a factor in its significant increase.

The first wave of inflation is now well documented. Thanks Wolfs, now let’s see how the eCONomy handles the second wave…

Interesting times.

Let’s see if the FED and their economists take this data into carefully next week. 25 vs 50 rate cuts? If they do the latter my opinion is that they are really worried about the labor markets, of the first option, they are not, and will likely telegraph staying more patient to watch the incoming data.

No-one has used the term “base effect” to sow some gloom. LOL