Repo activity wakes up again.

By Wolf Richter for WOLF STREET.

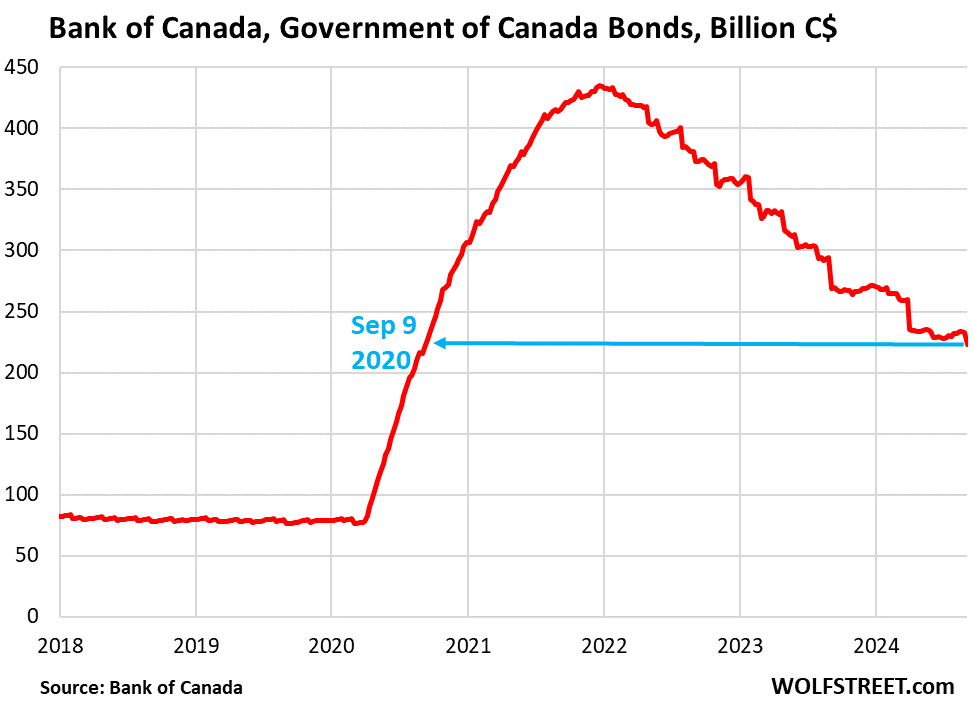

The Bank of Canada shed another $10 billion (all amounts in Canadian dollars) of Government of Canada bonds, bringing its GoC bond holdings down to $223 billion, the lowest since September 9, 2020 – a four-year anniversary and roundtrip – according to its latest weekly balance sheet, released Friday.

GoC bonds are by far the largest component of the BoC’s assets. Under its Quantitative Tightening program, the BoC has reduced its GoC bond holdings by 49% from the peak. The balance sheet has other components that we’ll look at in a moment, including repos, for which there has been some demand recently. Overall, the BoC has reduced its total assets by 52% from the peak.

The $10 billion GoC Bond roll-off occurred while the BoC cut its policy rates for the third time, sticking to the BoC’s announcement in April that QT would continue even as rates get cut.

In April, the BoC outlined a plan for how long QT will continue – possibly into September 2025 – and what might happen after QT ends – let more GoC bonds roll off and replace them with short-term GoC Treasury bills and repos during a “multi-year transition period.”

So after QT ends, possibly a year from now, the composition of the assets will change, with fewer longer-term GoC bonds and more short-term T-bills and short-term repos.

Under its QT program, whenever GoC bonds in its portfolio mature, the BoC gets paid face value for them, and they roll off without replacement. There is no cap (unlike at the Fed). Whatever matures, rolls off.

GoC bonds mature at the first of the month. There are months when nothing in the BoC’s portfolio matures (most recently, July and August), and there are months when a big bond issue matures and rolls off (for example, $23 billion in April).

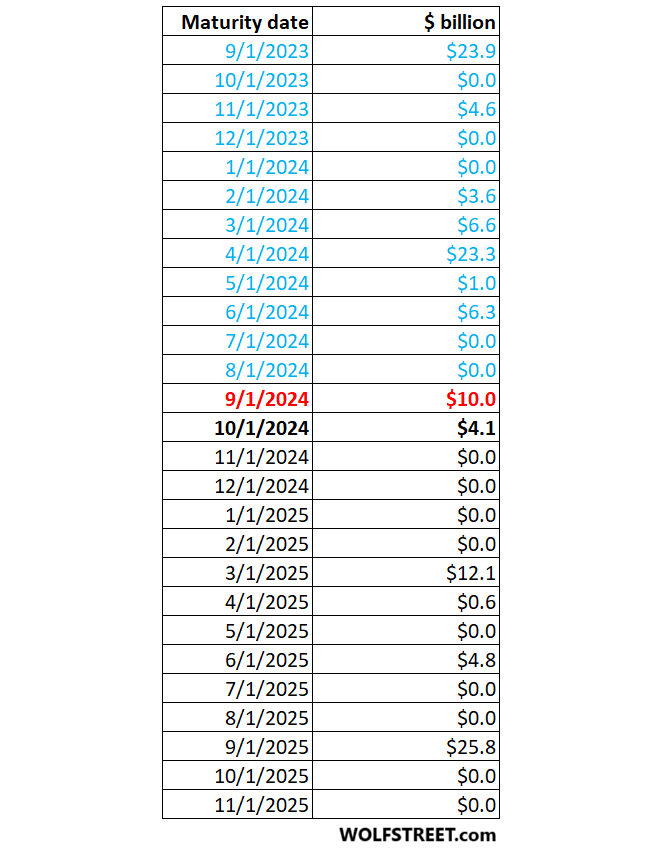

The table below shows the maturity schedule of the BoC’s holdings of GoC bonds. The September maturity of $10 billion just rolled off (red). The blue figures denote the bond issues that recently rolled off. The black figures denote the future maturities. In October, another $4.1 billion bond issue will mature. And then there won’t be any maturities until March 2025.

If QT continues through September 1, 2025, as the BoC suggested in April, another $47 billion in GoC bonds will mature by then.

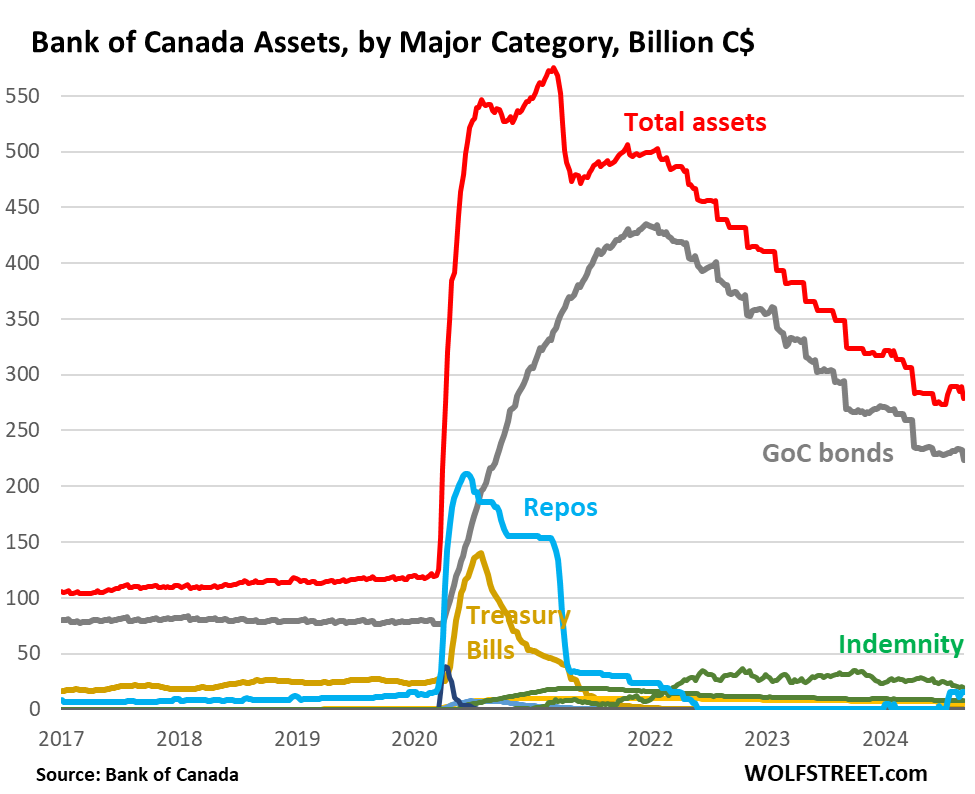

But there are – and were – other assets on the balance sheet.

In March 2020, the BoC started buying from a smorgasbord of assets, some of them in large amounts, and some of them in minuscule amounts. Some of them are now down to zero – they’re gone. Others continue to come off. And repos, which had provided a big part of the liquidity in 2020 then matured and went to zero in June 2022, have seen some activity again recently.

The chart below shows total assets (red), GoC bonds (gray), repos (blue), Treasury bills (gold), “Indemnity” (green), and a bunch of smaller stuff. More on all of them in a moment.

Total assets are now down by 52% from the peak, to $279 billion.

Note the uptick in total assets in July, when no GoC bonds rolled off, but repo activity increased – with currently $16 billion in repos still outstanding.

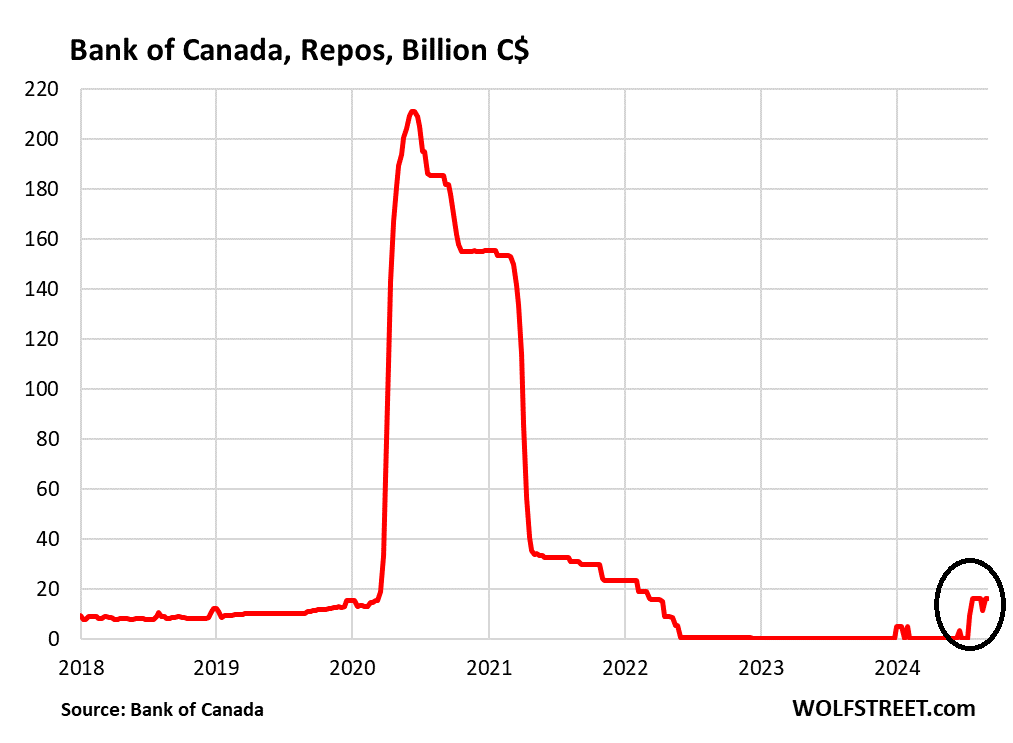

Repo activity restarted in 2024 and rose to $16 billion in July. On Friday’s balance sheet, repos were still at $16 billion.

Repos are demand based. With these repurchase agreements, the BoC lends against collateral, and charges interest. Its primary dealers are the counterparties that act as agent for indirect bidders.

The BoC explained that its rate-cut path kicked off a sudden demand for repos to fund bets on long-term bonds. Repos mature after short periods and then can be renewed at the BoC rate in effect at the time. As the BoC cuts, the carrying costs of those long-term bond bought earlier would decline with each rate cut, but interest income from the longer-term bonds would stay fixed after purchase, and bond prices would rise as market yields decline. So there’s a lot of demand for this trade (not without risks: funding long-term investments with short-term borrowing can backfire when interest rates rise).

Before the pandemic, the BoC carried about $13 billion in repos. During the first few months of the pandemic starting in March 2020, demand for repos exploded and topped out at $211 billion in June 2020. As the BoC flooded the land with money through its GoC bond purchases, demand for repos faded, and by June 2022 they were zero.

In the future, after QT ends, GoC bonds will continue to roll off, and repo balances will rise, along with T-bill balances, as the balance sheet shifts from GoC bonds to those two short-term liquidity instruments, according to the plan.

This increase from zero to $16 billion is why total assets ticked up in July:

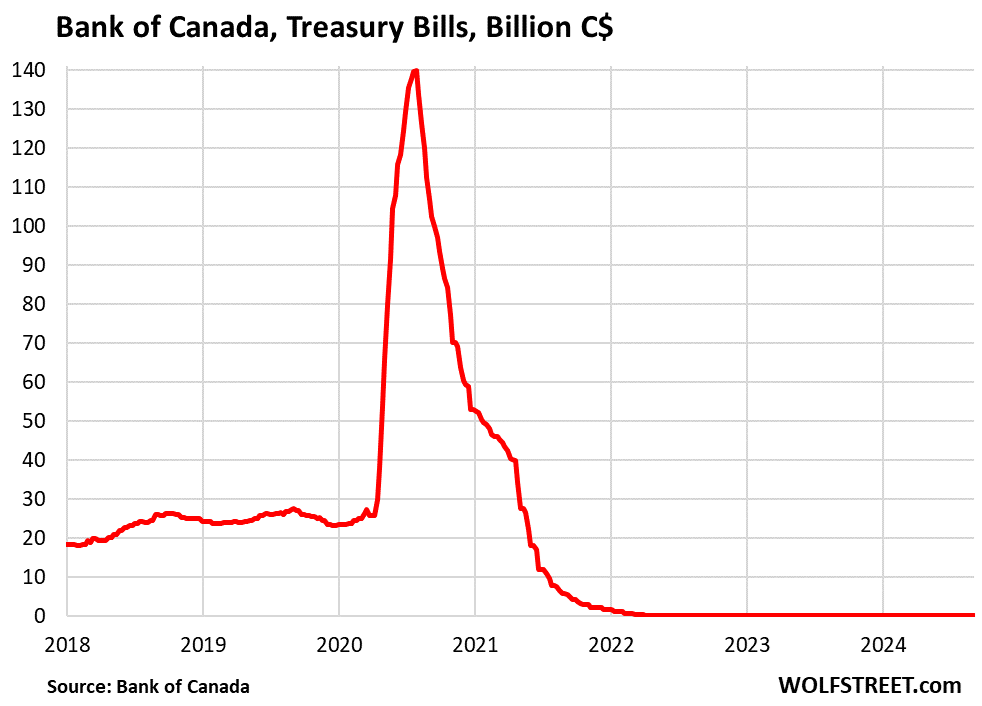

Treasury bills are currently $0. Before the pandemic, the BoC held about $15 billion in short-term Canadian Treasury bills. In the early weeks of the pandemic QE ramp-up, it purchased large amounts of T-bills and brought the total balance to $140 billion by June 2020. It then let them mature and roll off and by March 2022 they went to zero. T-bills will start increasing as the BoC shifts its assets from GoC bonds to T-bills and repos.

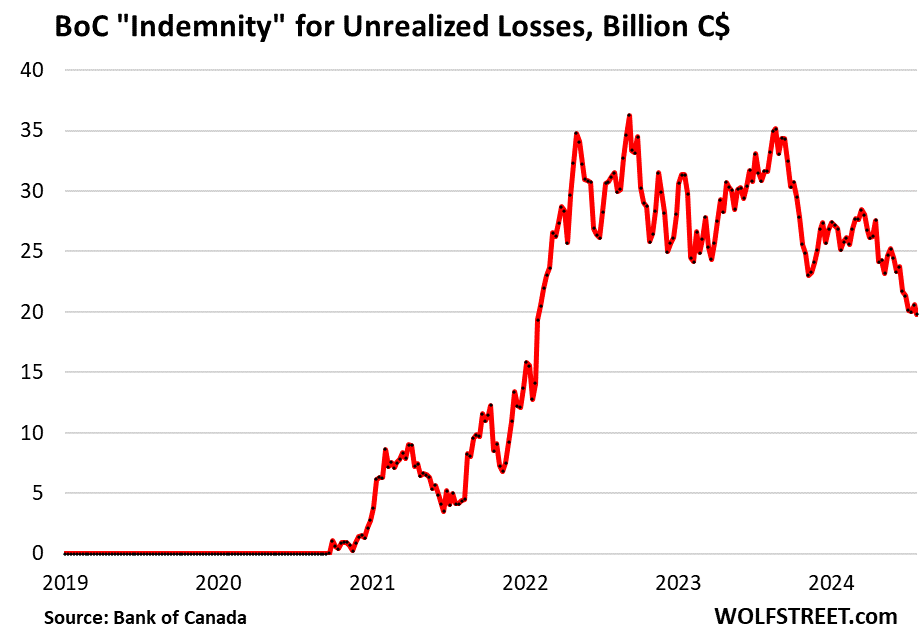

“Indemnity” of $19.8 billion is the value of the indemnity agreements between the federal government and the BoC that represents the unrealized losses on the GoC bond holdings if the BoC sells them outright at today’s market prices, which it has no intention of doing. The amount will eventually go to zero, at the latest when all the bonds that are covered by it mature and roll off.

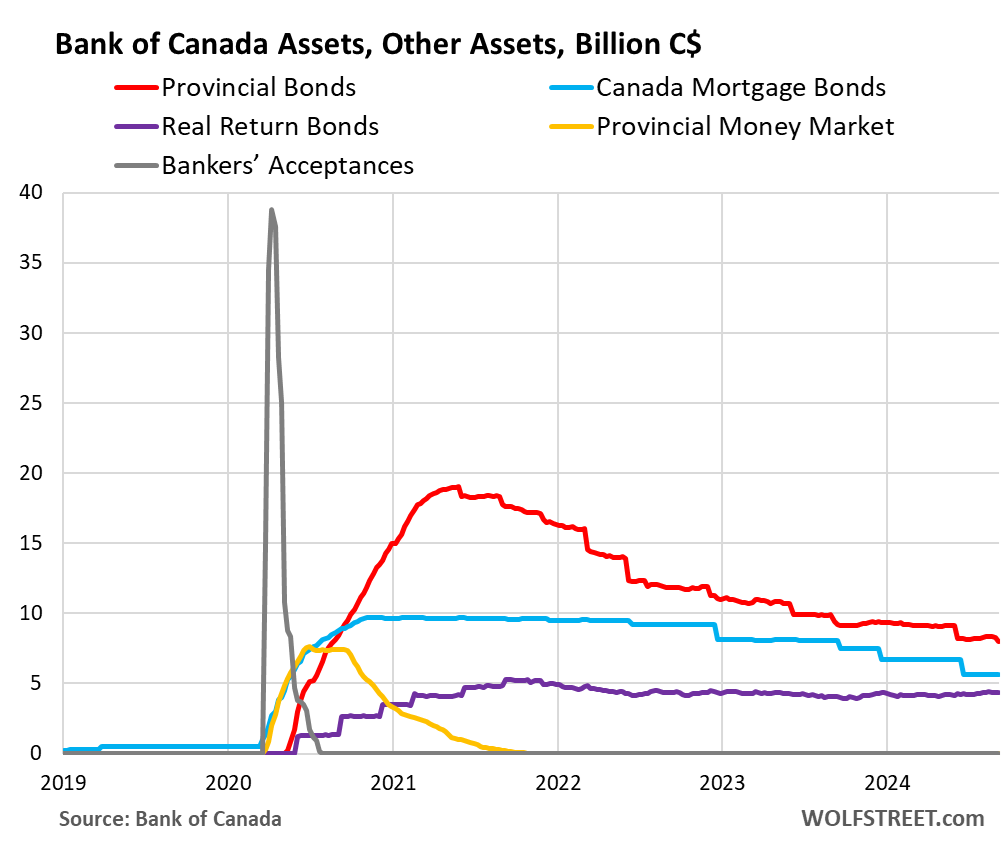

Other assets purchased during the pandemic.

- Provincial Money Market: $0 since September 2021 (gold in the chart below).

- Bankers’ Acceptances: $0 since August 2020. This money market instrument had spiked to $38 billion by April 2020 (gray).

- Provincial bonds: $8.0 billion, down from $19 billion at the peak. They come off when the bond issues mature (red).

- Canada Mortgage Bonds: $5.4 billion, down from $10 billion in November 2020. They come off when the bond issues mature (blue).

- GoC Real return bonds (inflation protected securities): $4.3 billion down from $5.3 billion.

- Corporate bonds: $0. It only purchased about $200 million to begin with, too little to show on this chart.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hey Wolf, awesome article and as a Canadian this is key information to see how things are progressing. Not sure where else to get this info besides WolfStreet. I also noticed in the GoC Real return bonds section there few trillion extra haha. Cheers!

Yeah, those trillions whizz by so fast these days, it’s hard to even see them.

Thanks!

Is there a reason why the reductions are so much slower than the increases? Same in US.

Yes, adding liquidity doesn’t blow up the financial system (though it causes other problems). Withdrawing liquidity too fast will.

Woah – did the BoC balance sheet really quadruple in 2020?

Yes, because it was small to begin with. The BoC hadn’t done QE before. So this was the first time, and there was no huge pile left over from last time.

Clearly it went way overboard, but it’s making good progress undoing the damage.

Admirable resolve shown by BoC.

Wolf, quick question – do repo balances count as settlement balances, or are they too volatile and short term? If QT ends in September 2025, there would still be 176b(ish) in GoC bonds on the BoC’s books – are these also part of the BoC’s settlement balance target? If so, is ending QT in September 2025 possible? Your other article mentions the deputy governor suggested a target of 20-60b, which seems like a long way away, despite the rapid QT.

Thanks, I really enjoy your BoC articles!

TEMPLE

Just to clarify: Settlement balances are a liability on the BoC’s balance sheet. Repos and GoC bonds are an asset on the balance sheet. They’re completely different.

Settlement balances (a liability) will come down as the BoC drains liquidity via QT. So the target is for settlement balances to drop into $20-60 billion range. They’re currently in the $100-120 billion range (fluctuate a lot from week to week). So they need to drop $60+ billion. That will happen in Sep 2025 if $47 billion in GoC bonds run off and $16 billion in repos are not renewed. If repos stay the same or rise, GoC bonds can drop further into 2026 to get settlement balances below $60 billion. This would conform to the shift from GoC bonds to short-term repos and T-bills.

Thank you! Slowly wrapping my head around all this…

All is redeemed and the past is forgotten when a serial killer does some community service for a little while. Let’s all show some appreciation for the sincere effort. They’re only human and we all have our ups and downs. Life, after all, is transitory, and that is certain. No reason to dwell on, or even try to remember the past, interpret the intentions, assess the results, or try to hold anyone accountable for their past. Let’s let bygones be bygones. Let’s learn to forgive and forget. Just let it go. It only hurts you more than them to dwell on what has happened. It’s like water under the bridge. Just let it go……….let it go.

Brilliant sarcasm!

Apparently, you weren’t married to someone like my ex wife!

Relatively, BoC did better job at reducing balance sheet. Its relative but still.

FED started but slowed down prematurely in June. They could have waited till ON-RRP levels become closer to zero. They opened SRF. Banks have huge Reserves earning 5.4%. Treasury tweaked more Bills than Notes and Bonds. So FED could have taken advantage.

Anyways it was harder to believe FED will do so much QT after years and year of ZIRP and QE. They did. so some credit due.

But then Chris Rock would say dont expect a cookie to do but obvious thing. :)

My thoughts here are that the larger US economy is structurally more important to more people. The US economy is the benchmark for the world.

Also, the fact remains that it is a competitive world economy. No war has been declared by the US since WWII (besides on drugs, terror etc) but the conflict has been non stop.

Tanks bombs and bullets have to be manufactured but currency can be computer generated.

They have told us the “next war” will be fought virtually. They just haven’t pointed out that the pandemic quickly turned into that (financial) war (Putin noticed and got grumpy, Xi knows).

Where do the billions of the TD Bank Group laundering illicit fentanyl profits go in these charts?

😆

Sorry that’s on China’s balance sheet not Canada’s

Laundered money goes into Vancouver Canada real estate and then with the paper profits the same laundered money is funneled into Fentanyl by the Chinese Fentanyl gangs. Soon the homeless will outnumber the ones with a home in Vancouver.

The fundamental problem with “assets” being left on ANY central bank balance sheet (i.e. Wolf has provided ample evidence that the Fed cannot go below ~6 trillion) is that those “assets” represent real fucking currency that was created out of nothing to the great benefit of a relative few BUT that we ALL pay for through inflation. It’s a global market, so this is a global phenomena. The Bank of Canada has probably been the best about managing their QE efforts, but it’s still an outright confirmation of the failure of “representative” governments around the world. Hopefully, Wolf’s work (evidence of this failure and corruption) is backed up on secure severs around the world…

Interesting times.

But – BoC or Canadian government own no physical gold.

I have a question for you Wolf. How is it even possible for the FED to have ~7 trillion on their balance sheet and the central bank of Canada to have ~200 billion USD when the US population is around 8.5 times the size of Canada. Seams like a really enormous difference in size no?

The BOC never did QE before 2020. That’s your answer.

The big question is what will happen first the Canadian dollar hitting 50 cents U.S. or the Bank of Canada rate hitting zero?

Neither?

Debts to dollars, the US has a lot out there. That’s probably what’s keeping the exchange rates somewhat stable… until BRICs does something drastic – which they won’t. They’re all about operating in the shadows until they drain all their US paper.

There’s no obvious reason for the BOC to lower rates to 0%, why do you think it would ever happen?