Auto sales hit by CDK hack. Gasoline and auto sales in dollars hit by dropping prices, but they boost inflation-adjusted consumer spending.

By Wolf Richter for WOLF STREET.

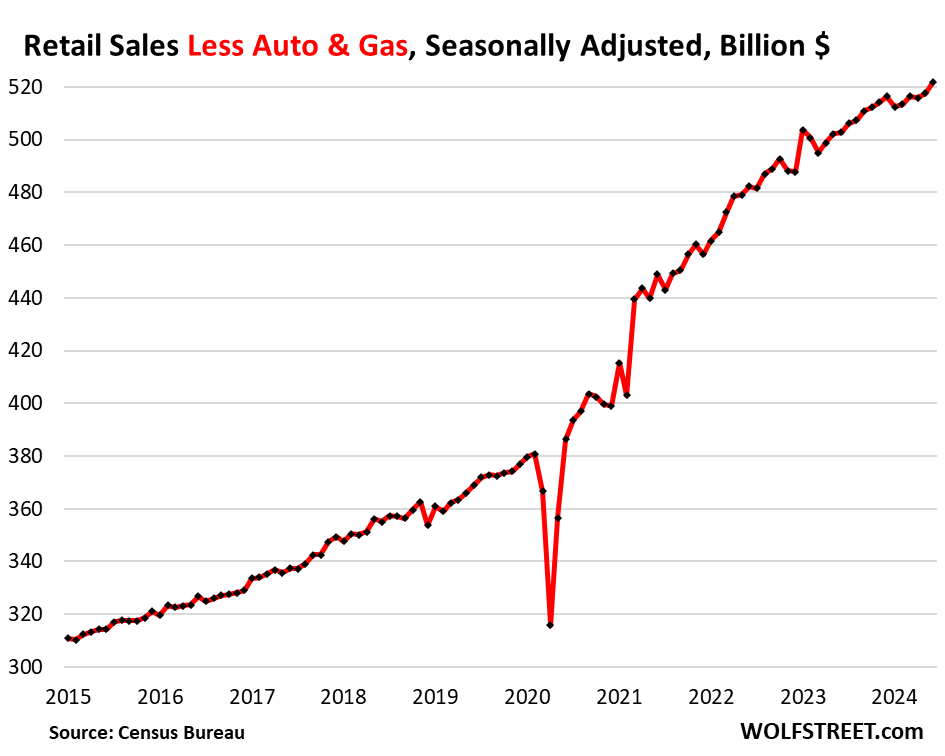

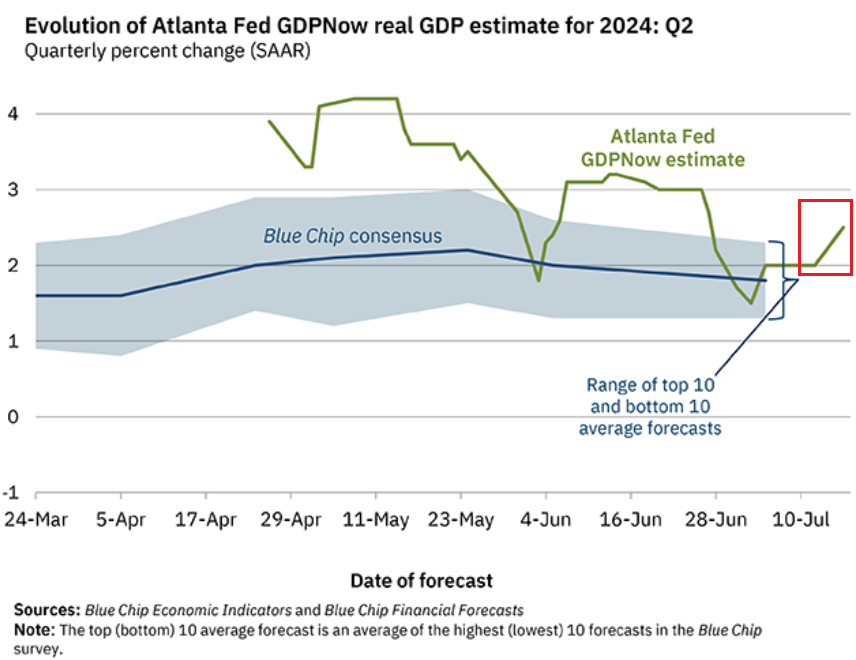

Retail sales without gasoline and auto sales jumped by 0.8% in June from May, seasonally adjusted, the biggest increase since January 2023, spread among many categories of retailers, including a massive increase in ecommerce sales. Year-over-year, they rose 3.8%. This month-to-month jump caused the Atlanta Fed to raise its GDPNow forecast for Q2 GDP growth to 2.5% today, from 2.0% last week.

The Atlanta Fed’s GDPNow forecast for Q2 real GDP was updated today with the data from June retail sales, which caused its real GDP forecast to jump to 2.5% today, from 2.0% last week. For the US, 2.5% real GDP growth is well above the longer-run average of just under 2%. GDPNow’s measure for real consumer spending growth rose to 2.1% from 1.6%.

The CDK hack and lower prices.

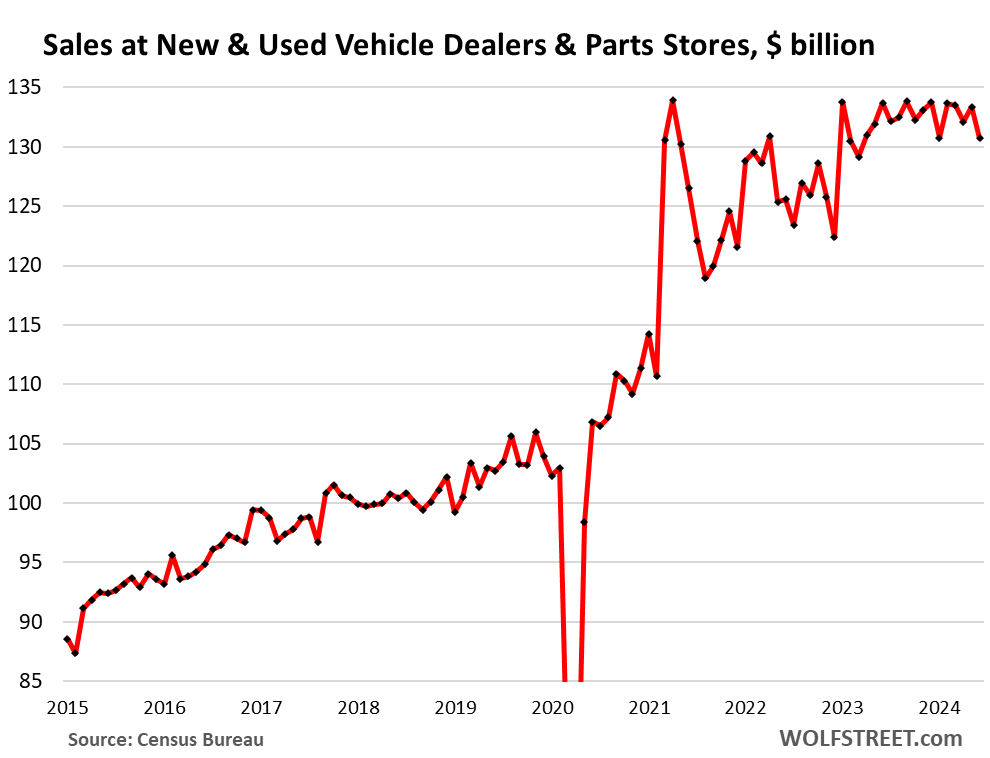

Sales at dealers of new and used motor vehicles and at parts stores are the largest category in retail sales, accounting for 19% of total retail sales. Sales of 15,000 of these auto dealers got hit when the ransomware attack on CDK’s cloud-based dealer management system took down their computers on June 19 for the rest of the month, which reduced their ability to process sales of vehicles and parts in June, which caused the biggest auto dealers to warn about its impact on Q2 revenues and earnings, and dented vehicle unit-sales in June. Those sales that didn’t get processed in June will get processed in July.

In addition, dollar-sales at auto dealers (19% of total retail) and gas stations (7.7% of total retail) experienced large price drops in June, with used vehicle prices in a historic downward spiral that has now unwound 60% of the crazy price spike in 2021 and 2022. Retail sales are not adjusted for price changes. The lower prices lowered the dollar-sales, not the unit sales. But the lower prices (deflation) of motor vehicles and gasoline boost consumer spending in “real” terms, adjusted for deflation in those items, opposite of what happened back when inflation in those items was hot and reduced “real” consumer spending on those items.

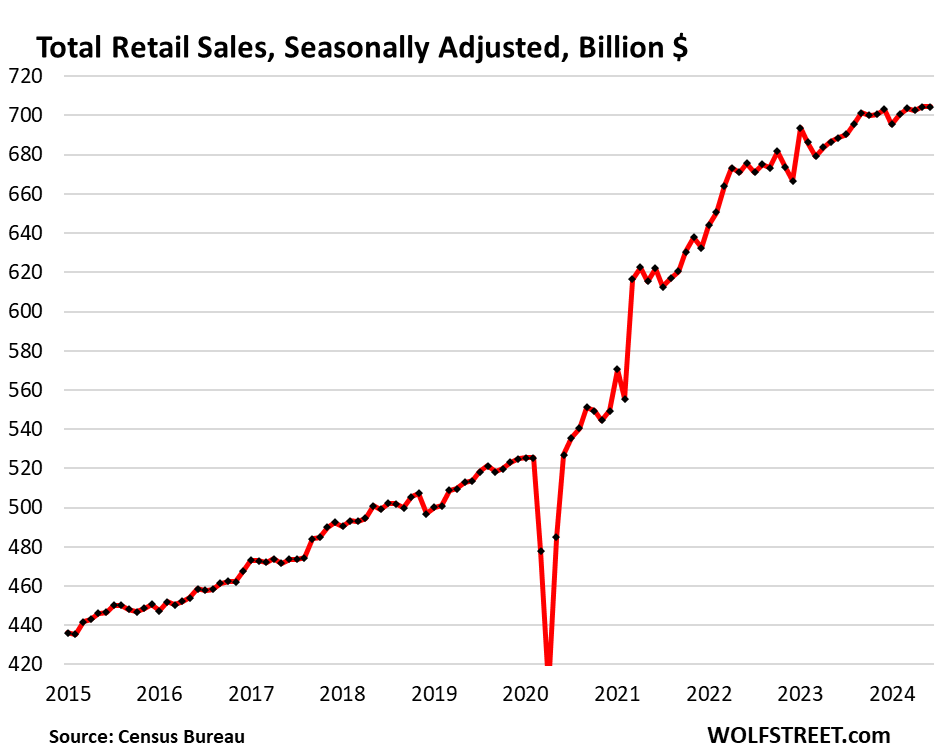

Total retail sales.

Total Retail sales were unchanged in June from May, at $704 billion, seasonally adjusted, and were up 2.3% year-over-year, despite the ransomware hack and the widespread price declines in goods, that included motor vehicles, electronics, furniture, and many other goods.

Sales at the largest categories of retailers.

New and used vehicle dealers and parts stores (19% of total retail). Note the 2% month-to-month drop in June, mostly due to 15,000 dealers not being able to process sales after the CDK hack.

The relatively flat sales for the past 18 months are due to dropping prices. The number of vehicles sold, so unit sales have been up year-over-year all year long, both in new and used vehicles:

- Sales: $131 billion

- From prior month: -2.0%

- Year-over-year: -2.2%

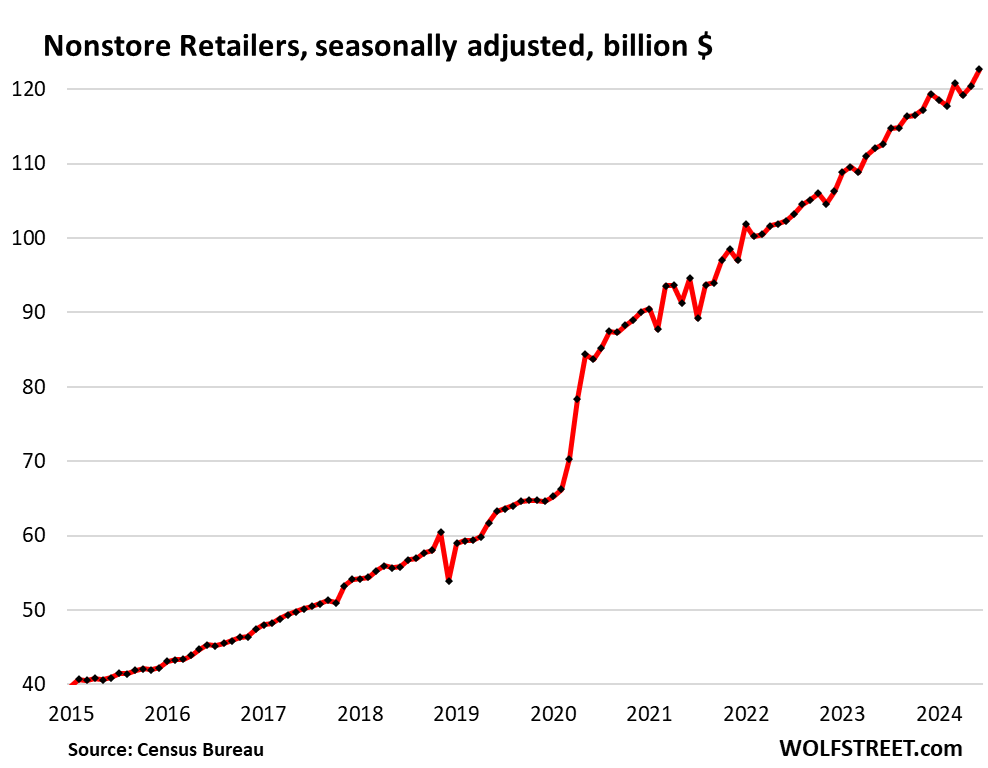

Ecommerce and other “nonstore retailers” (17% of total retail trade), includes ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $123 billion

- From prior month: +1.9%

- Year-over-year: +8.9%

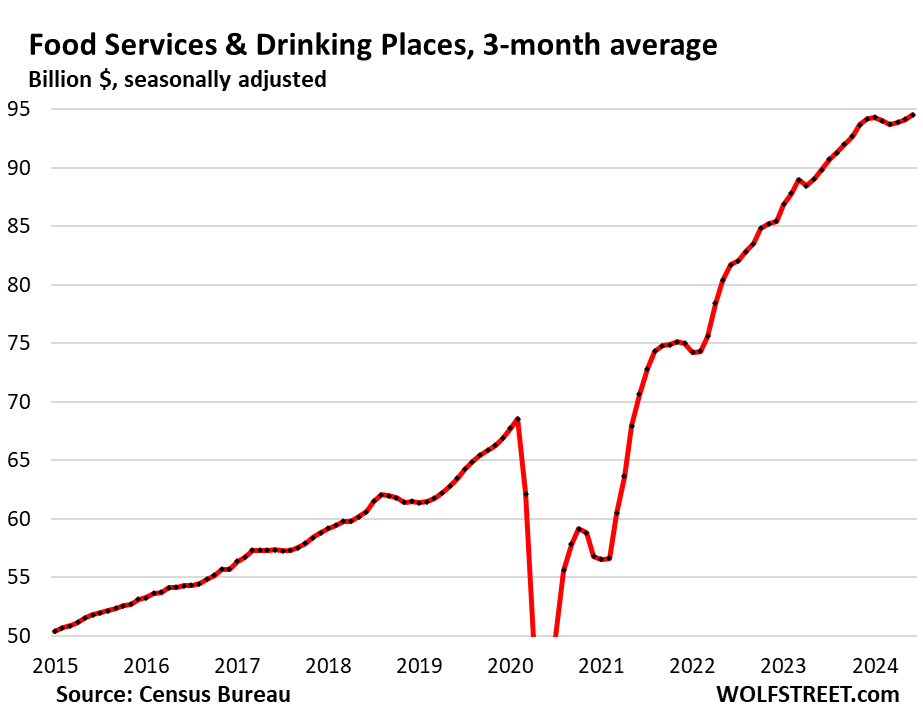

Food services and drinking places (restaurants, cafes, bars, etc., 13% of total retail). The chart shows the three-month moving average (3mma). You can see the slow-down earlier this year, and the re-acceleration over the past three months:

- Sales: $95 billion

- From prior month: +0.3%

- Year-over-year: +4.4%

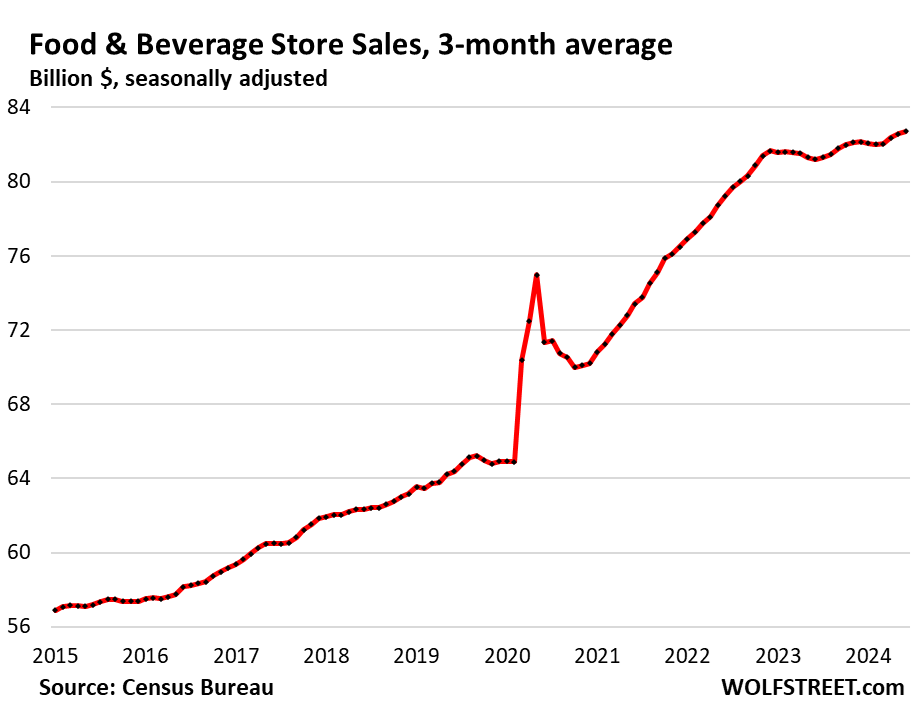

Food and Beverage Stores (12% of total retail):

- Sales: $83 billion

- From prior month: +0.1%

- Year-over-year: +1.9%

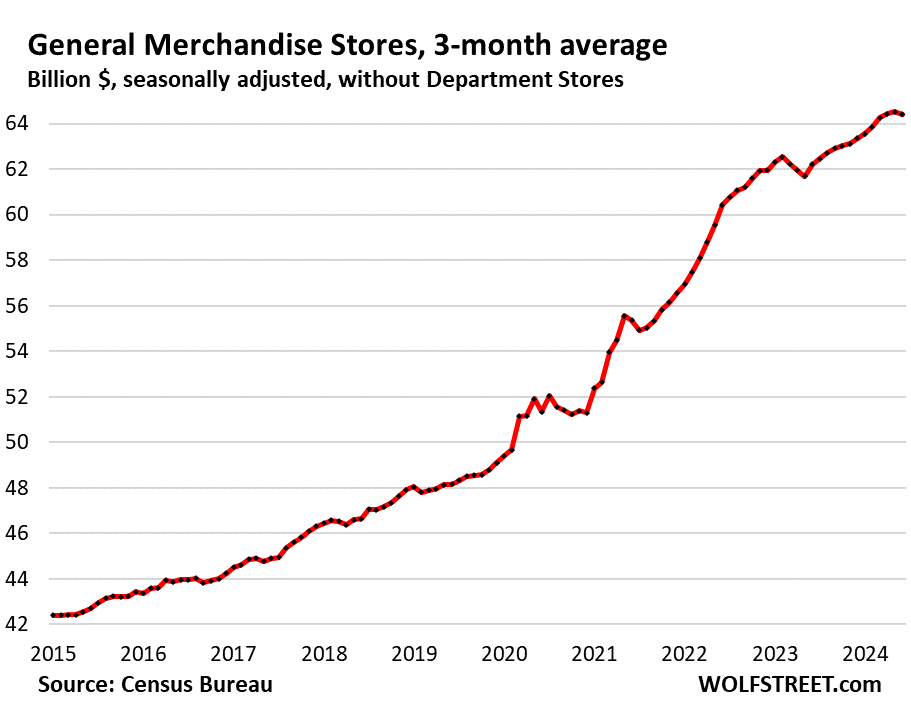

General merchandise stores, without department stores (9% of total retail).

- Sales: $65 billion

- From prior month: +0.5%

- From prior month, 3mma: -0.2%

- Year-over-year: +3.5%

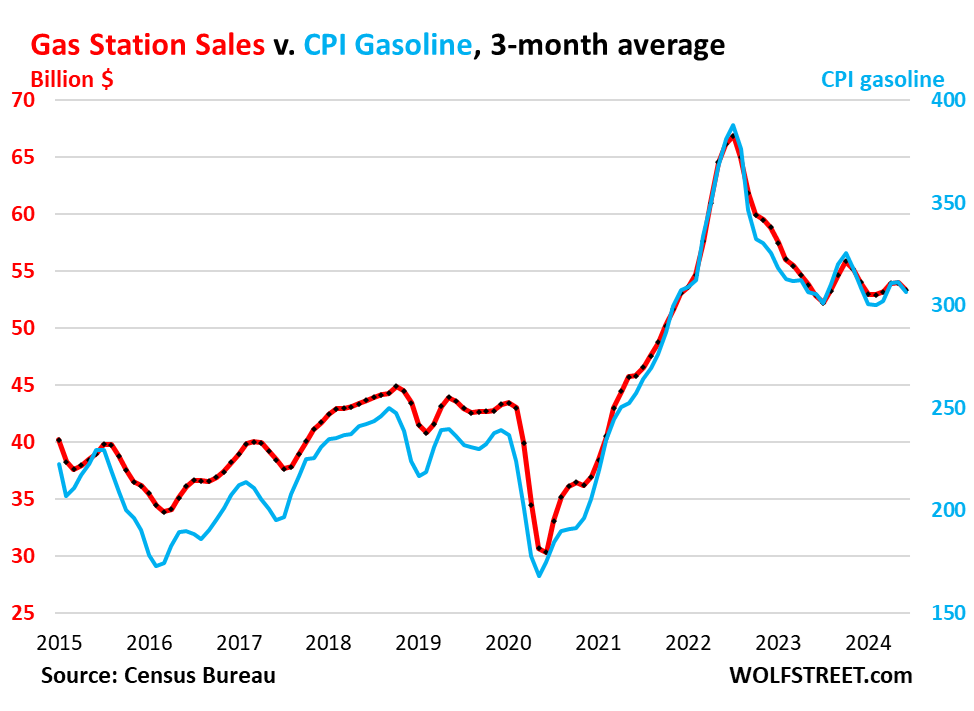

Gas stations (8% of total retail sales). Sales at gas stations move in near-lockstep with the price of gasoline, and the price of gasoline dropped over the past months, and so sales in dollars dropped:

- Sales: $52 billion

- From prior month: -3.0%

- From prior month, 3mma: -1.2%

- Year-over-year: -0.4%

Sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis); and the CPI for gasoline (blue, right axis):

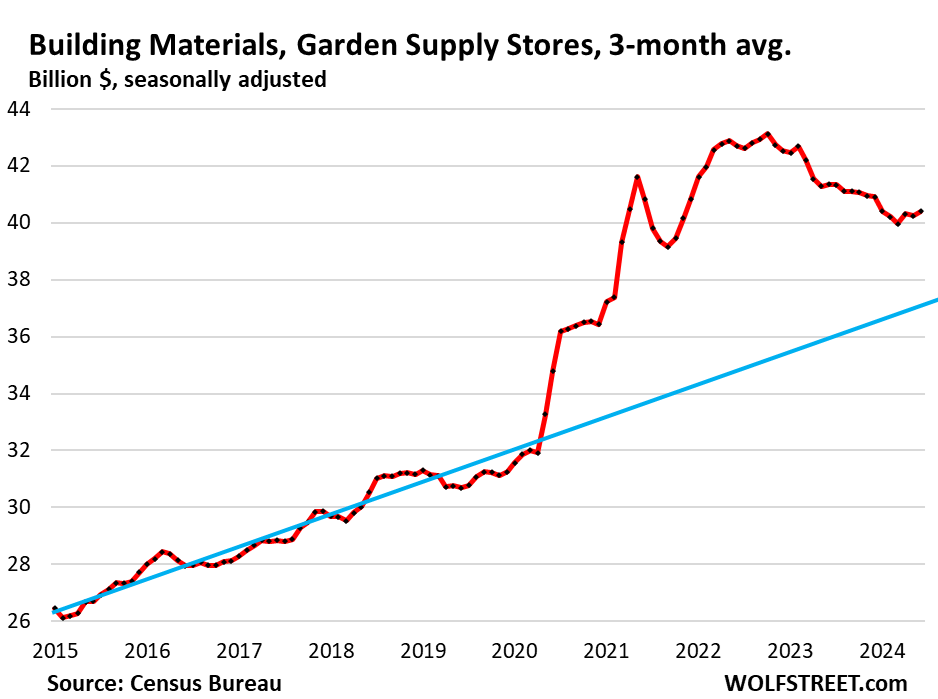

Building materials, garden supply and equipment stores (6% of total retail). The prepandemic trendline in blue:

- Sales: $41 billion

- From prior month: +1.4%%

- From prior month, 3mma: +0.4%

- Year-over-year, 3mma: 5.7%

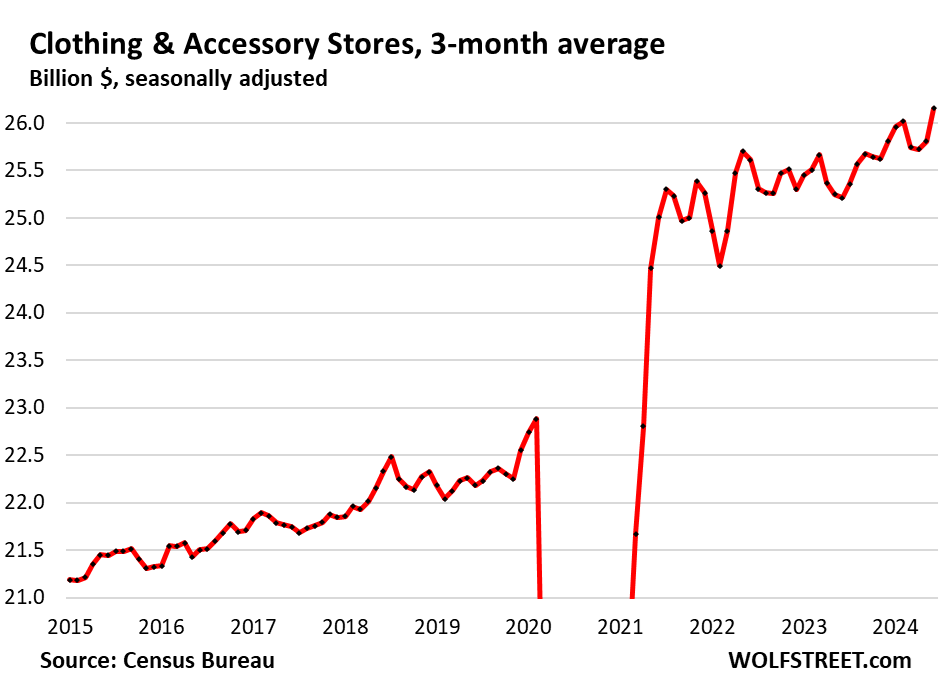

Clothing and accessory stores (3.7% of retail):

- Sales: $26 billion

- From prior month: +0.6%

- From prior month, 3mma: +1.3%

- Year-over-year: +4.3%

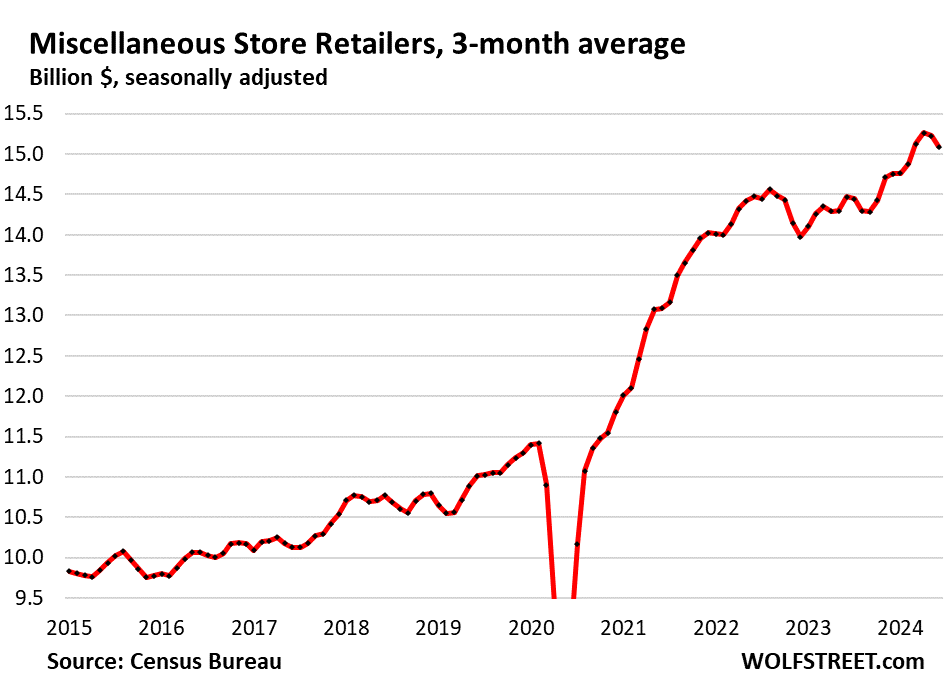

Miscellaneous store retailers (2.2% of total retail): Specialty stores, including cannabis stores.

- Sales: $15 billion

- Month over month: +0.3%

- Month over month 3mma: -0.9%

- Year-over-year, 3mma: +4.3%

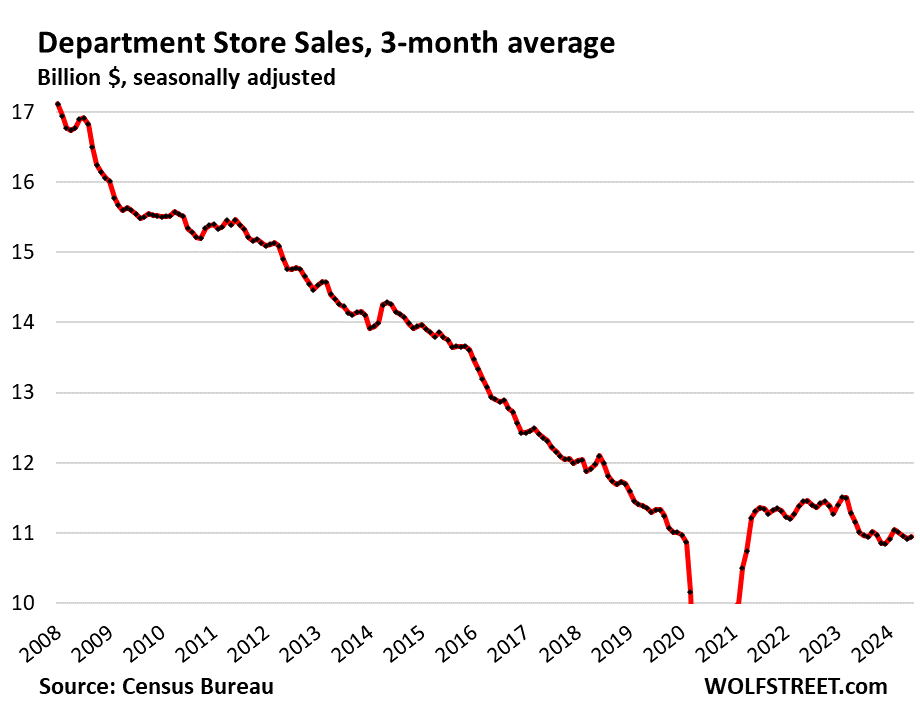

Department stores (now down to just 1.5% of total retail sales, from around 10% in the 1990s). Ecommerce sales by department store chains are not included here, but are included in ecommerce retail sales above. This chart is the epitome of what we started to document in 2016 in our column, Brick and Mortar Meltdown:

- Sales: $11 billion

- From prior month: +0.4%

- From prior month, 3mma: +0.3%

- Year-over-year, 3mma: -0.6%

- From peak in 2001: -43%.

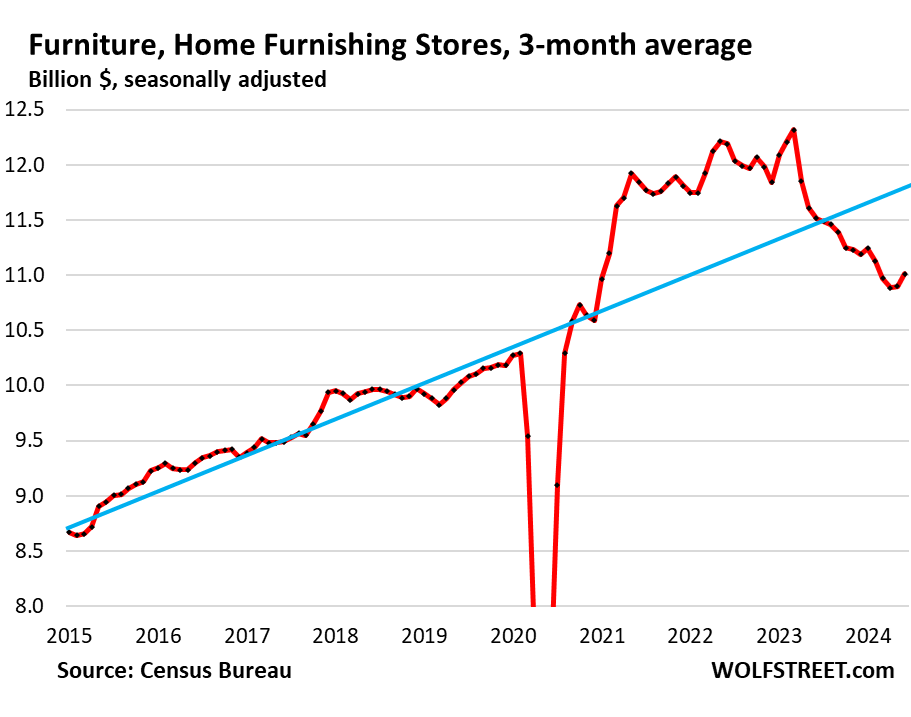

Furniture and home furnishing stores (1.6% of total retail). Much of furniture and furnishing sales have moved to ecommerce. This is what’s left over at brick-and-mortar retailers that specialize in furniture and furnishings.

- Sales: $11 billion

- From prior month: +0.6%

- From prior month, 3mma: +1.0%

- Year-over-year, 3mma: -4.4%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Carvana stock has soared from a mere $9 per share to $145 per share on the enormous excitement over the Fed pivoting and interest rates headed to zero in the near future despite new car prices over $48,000.

Carvana is a meme stock. They do what they do because they do it. Don’t try to squeeze logic into it.

True, but seems like meme stock is making a comeback, same as Crypto, which goes to show we are nowhere near a tighten financial market, still plenty of money/liquidity chasing insanity as this is the new normal..

Also doesn’t help everyone is buying into rate cuts by Sept and the market is going to blow another load higher, will it actually happen is a different story

“Meme stocks” should have never existed in the first place. They are the result of the most reckless money-printing endeavor in history, which is still going. The FED completely failed to take away the punch bowl.

This all has turned into a sick joke. A rate cut would be economic terrorism at this point. The FED is a diabolical regime hell-bent on destroying the country, it would seem.

powell, lagarde, abe, all of these people are bad people who relish in pain and destruction on others.

once you understand that, their behavior makes a lot more sense.

Nah man. Meme stocks have a pretty straightforward history and it has more to do with gambling addicts on Reddit than anything the Fed is doing. I don’t know how interest rates convinced thousands of people that GameStop and AMC will work a mega company that will take down Amazon but only if you keep your physical stock certificates in a lockbox under your bed.

You might as well blame Iraq currency speculators on the Fed.

There were “meme” stocks long before there were memes, or even before the creation of the Fed.

The author of Reminiscences of a Stock Operator described one brokerage firm more than a century ago, “their specialty was trimming suckers who wanted to get rich quick.”

Such people have always existed, and always will. We can only try not to be one of them.

Home Builder stocks are up 15% to 20% in just a one week over the FED Pivoting. Crazy.

I am getting multiple calls a day from investors wanting to buy my rental houses.

Just my two cents. What this mean. I don’t know.

You are expecting a pivot? Don’t hold your breath.

Trump says Powell will maintain his job IF Powell does the right thing. In Trump’s view, that means not doing anything that helps Democrats, such as an interest rate drop before the election.

As we are witnessing, the political pressure on Powell is immense. It will only worsen if/when Trump takes office. The job of Fed chair will be continually in jeopardy.

On the other side of the political aisle, it appears Democrats forced Powell into a dovish verbal flip-flop back in Dec 2023, so Powell gets some pressure from both sides.

But this latest threat from Trump’s side is very blatant.

Strangely, despite the “better than expected” number along with upward revisions, treasury yields tanked along with the daily stock market melt-up.

Q2 GDP looks likely to be a healthy number, but Powell has conveniently said “the Federal Reserve doesn’t have a growth mandate” and keeps talking about the “weakening” labor market that’s still adding 200K+ jobs/month.

Federal funds futures have now priced in a 100% chance of lower rates at the September meeting, and Powell, unlike in previous months, has not pushed back against market expectations. Barring anything unexpected, looks like this is it this time: September will be the start of the easing cycle.

The Fed is losing its political cover for 5.5% rates, with inflation where it is now. If there is a big rebound in inflation, such as there was in Jan-Mar, it’ll have political cover for more wait-and-see.

so if they lose their political cover for 5.5 and drop it to 5.25 or 5, so what? worldwide assets are not priced for 5 or even 4.5, they’re priced for 0.

that means either the market is wrong or the central banks are lying about not returning to zirp

That’s a good question Franz. Many stock market valuation metrics are now higher in 2024 despite rates at 5.5%, than they were in 2021 with ZIRP & QE running at full blast.

I guess from the Federal Reserve’s perspective, they have a clear easing bias, so they’re going to “cautiously” lower rates until inflation shoots up again. That’s how they know they’ll have hit the neutral rate, as cutting rates below that theoretical level acts as economic stimulus, pushing inflation & growth higher. The committee’s current median estimate for neutral is 2.8%, slightly higher than the pre-COVID estimates of 2.5%.

Home prices corrected in 2022 and then went up again in many areas. Town-homes and Condos are in balanced market but SFH are still selling fast (may not be crazy in 2021 times) but still. Unlike Stocks, Real Estate is Local market. National trends do not reveal everything.

Stock Markets boom doesn’t need any proof. Just look at all indices and Tech sector evaluations. Apple from 165- 235 in matter of weeks. NVIDIA to moon.

Fools (including myself) are those who thought we will have Asset Price corrections when Rates went so high. But I guess FED expanded its balance sheet so much in last 15 years, I think its foolish to think we will have any major Asset Price correction.

srk, the fed balance sheet is roughly where it was at the end of 2020, and stock prices are nearly 80% up. that’s not the cause here.

Franz G,

I said Balanced Sheet expansion in last 15 years and not from 2020.

Also if you compare to beginning of 2020, we are still way to high.

The rebound in inflation, if it happens, isn’t going to come until after September or no sooner than there’s a significant rise in the cost of oil. The real problem for Powell is the real possibility that the economy is taking a temporary slowdown. Companies have increased job cuts, but this doesn’t mean it’s going to be a long-term trend.

As usual, time will tell, but I know this much. The 30YFRM has dropped 45 basis points over the last 12 weeks just from the expectation of a Sept rate cut. It very well may drop to 6.5% by the Sept FMOC meeting. Then a 25 BP cut will push it towards or below 6%. My concern is that housing stabilizes by next Spring and creates a big turnaround in durable goods without any REAL deterioration of the economy towards a recession.

With $2T in deficit spending this year, Powell had better take a very long pause / look at hastily cutting the FFR. This is massive levels of stimulus that I do not think he’s correctly taking into account at how buoyant it’s making the job market. Now, if we all of a sudden start seeing job losses in construction, then I’d be more open to Powell cutting. Until then, he’s potentially making a grave mistake for letting inflation surge again by early next year. I believe you call this the classic head fake.

Cheers!

“or no sooner than there’s a significant rise in the cost of oil.”

It’s core inflation measures that everyone will be looking at, and the cost of oil just doesn’t contribute much to core inflation measures.

“the real possibility that the economy is taking a temporary slowdown.”

It looks like the temporary slowdown is already over. This data here shows that, plus data we got today on industrial production, and earlier data. The slowdown may have been centered on Q1 and the early part of Q2.

I like how you assume the markets are right. There’s still two more inflation and employment reports before the September meeting so nothing is 100%.

Of course stranger things have happened, but inflation tends to be seasonal, peaking around mid-year as gas prices peak and declining towards year-end as gas demand falls & holiday discounts arrive. Monthly inflation percentages are seasonally-adjusted, but somehow, these seasonal adjustment factors have not been enough to break the trend. In the latest 3 years (2021-23), inflation was substantially hotter in each year’s first half than the corresponding year’s second half, seasonal adjustments or not.

An inflation rebound in July/August is certainly possible, but the big picture is pretty clear that a disinflationary trend has been in place since Summer 2022. The Federal Reserve & markets aren’t going to panic unless there were a multi-month rise to break this trend.

Talk of price reductions on anything is not very amusing. It’s a flood, a few dry spots here and there. Back things up 4 years like wolfs charts show for a ‘toad size’ price reduction.

NO thing IS Ever 100% folx,,,

You and everyone You Know can speculate however much You want,,, including especially those who speculate that ”Science Says”,,, but science is actually only a method of inquiry,,, and to speculate otherwise usually leads to very bad and frequently very very wrong conclusions.

Generalizing on the basis of insufficient information, while certifiably frequently regarded as science, has nothing to do with science, but only to do with opinionating.

The aim of science is not to open the door to infinite wisdom, but to set a limit to infinite error.

Glad you decided to quit following those “theory of everything chasers”……they are as bad as preachers.

Although the fed is supposed to be independent, it’s members haven’t always done a good job at that. It’s looking likely Trump wins the election, if they cut before the election Trump will view it as helping Biden so those that want to stay on his good side might actually be looking for reasons not to cut. Just a theory, but why I can’t get behind a 100% chance of a rate cut in September. Also remember January? The market was pricing in 6 cuts – it’s been wrong with most of it’s predictions.

Also if my theory is correct, the safest time to cut rates is December if they can find reasons to hold out that long.

The November meeting will be after the election.

I agree. A 100% chance is just crazy. It’s almost as if the market is taking Powell’s decision making away from him. In addition, Powell appears to be signaling that a Sept rate cut is likely, almost no matter what the data says IMHO. I for one do not expect a notable deterioration in economy over the next 2 months.

Best thing for Trump is to take the big hit of getting fiscal spending in check in the first two years of his administration so by the end of it things look good and VP becomes president.

Only problem is that he seems wedded to big tax cuts, where did Republican deficit prudence disappear to? Oh that right, when deficits benefit the rich.

If Trump lets it rip in 2025 and the Fed cuts rates we are in the late 1970s territory, and quite the possibility that the FX markets will play the role of Paul Volcker quite near the end of Trump’s term. A poisoned chalice to his VP. In the interim buy precious metals and physicals!

Oh boy, can’t wait until Sept rate cuts, you think we’re going to the moon now with the numbers like this and market action in the last couple of day…forget moon, we’re aiming straight for Mars..

Not only did Pow Pow managed to do the impossible and avoid any landing, better than a soft landing, he happens to pull a trick landing instead..kudos to him. High growth, strong employment numbers and lowering inflation…and now teasing potential rate cuts, give this man a nobel prize asap.

Yes amazing, my car insurance went up almost 40% despite my car being older and no traffic violations or accidents, my gym membership went up over 40%, and my rent just got raised $200 but there’s nowhere cheaper to go and it’s still about $1500 cheaper than a mortgage for a small house, and food I don’t know how it’s so much more each month because individually the price changes are small. Not to mention he screwed a whole generation of non-home owners by inflating the value of housing at an insane rate. I hope you’re being sarcastic. He could have raised rates to 1% in 2021 and then slowly as needed thereafter but everyone’s so afraid of a recession they err on the side of letting inflation run.

yup but yet nothing is breaking and apparently drunken sailors still have plenty of ammo to spend, so everything must be great right? Oh and we do need that rate cut cause home and car prices or anything that rely on interest rates is not quite high enough yet for the liking of the elites..

How would we know if anything is broken with 2 trillion in deficit spending and maybe another 500 billion in interest income flowing into our pockets.

Everything is wonderful. The markets cannot lie. But perhaps, neither can they tell the truth.

Stop blaming others for not investing properly. If you were paying attention for the last 16 years you would have started putting Capital toward equities and real estate a long time ago. We’re in a new era of managed economies where equity and hard asset holders will be rewarded while everyone else is punished that’s just the sad reality.

you better hope that’s not right or the currency will collapse along with society.

if no one wants to hold money, and would rather hold stocks at silly valuations, and in perpetuity, that means the end of the currency.

16 years? Try 40. That’s when the US dumped all the desire to be an industrial country with mass industrial employment and become a finance based society. Greenspan set the wheels in motion.

A new era where nothing has a logical valuation? Historically that’s been a bubble. Ask people who got hit hard 2001 what that was like.

This time is interesting because will it be the generative ai bubble, the crypto bubble, or the real estate bubble?

I guess some people have a harder time than others accepting that 2+2 now equals 5. Of course for those who can’t do math, this transition is not a problem.

Franz G – Stock at silly valuations is the new normal. You have trillions of dollars being dumped into 401ks as that is the only option employers give employees to invest in. The government really only gives investment tax breaks if you invest in 401ks or IRAs. Meanwhile, the number of stocks to invest in has dropped from 7000ish in the 1990s to 3500 now.

So over the past 30 years there has been a huge influx of 401k dollars chasing fewer and fewer stocks. It is a supply and demand thing. More demand and less supply and prices go up. People have few investment choices besides their 401k. The other options are real estate or cryptos. Well those are also going up in price.

BTC, is supply constrained. No more new coins. At least with real estate, we can add supply to try to keep prices in check.

Just like the new normal of the SPY at 20+ PE, housing at 4x the median salary is probably reality too.

Only a good deep recession will knock these silly valuations down.

But then again, the Government will give out money to combat any big recession.

“People have few investment choices besides their 401k. The other options are real estate or cryptos.”

There’s this new thing all the kids are into called “bonds”

“yup but yet nothing is breaking and apparently drunken sailors still have plenty of ammo to spend, so everything must be great right?”

I’ve had a sneaking suspicion for some time that the nouveau economic ministrations (balance sheet expansion, zirp) have the effect of spreading the pain away from businesses and asset holders and onto lower deciles of society (sub 70-80 percent). I think economic pain been going on since the mid-2000s. I think Obama was a protest vote, ditto with Trump (recall “Deez Nutz” from 2016). I don’t know that there’s a protest candidate this time so voter behavior will be interesting to watch (see recent events).

From his Q&A yesterday, Powell is concerned about “undershooting” the 2% inflation target and the “weakening labor market” if rates are not lowered soon…

Oh, heavens, please, ANYTHING but a >2% annual decrease in the already decimated purchasing power of my savings! I demand that the value of my money continue to erode in a robust manner!

I agree. The Fed is going to do everything they can to keep housing from seeing a spike in foreclosures like the GR. Congress will jump in as well and trot out rent & mortgage relief and expanded unemployment benefits. Any chance of a real decrease in housing prices doesn’t arrive until the Armagedón of the BIG ONE. Thay’s when bond investors lose confidence in the US dollar and treasury yields spike to unprecedented levels. This big event will be directly tied to BRICS reducing the dollar as the global reserve currency. I think things will get dicey when it dips below 50% from its current ~58%.

In Canada the government at last seems to be failing in its desperate attempts to support property speculators and the real estate industry generally. Even mass uncontrolled immigration isn’t hacking it anymore.

Toronto and the Greater Toronto Area seems to be rolling over for the second shoe to drop, I would not be surprised at a 1990s style dump of 40% to 50% plus from peak. Toronto Condos are already a complete disaster.

The “macro guys” have been joining the Wall St. chorus.

I hear of the rates globally; creating “rate gravity” to bring the US (down) into line.

What I don’t hear is the same recessionary forces in play.

The hot air is coming from the upper quintile (per yesterday’s Wolf Street comments), keeping the numbers up, plus the overall resiliency of the ‘Merican consumer (which I was very concerned about early on in the “fight”): I just buy and pay, regardless of prices going up or down. I have hungry mouths and a lifestyle to maintain.

The job market is soft under the surface, with multiple job holders spiking. While anecdotally my friend got the only job he applied to, at a high negotiated pay rate. I live in a scarce market where HCOL housing prevents most companies from EVER getting fully staffed.

Return to paying whatever for anything: people drive 1.5-2 hours each way to work here. They get a premium compared to working “down the hill.” They take their “good money” down the hill and grow their family and lifestyle (conversely I also get my groceries from 1.5 hours away and save 30-50% per item).

The spiral continues. We haven’t hit the “stagflation” wall officially; see the rate differential above (of growth and CB interest) and Phx-Ikki is nailing the “trick landing” concept.

“The first and biggest to print, Wins!” Is the new age Fiat- warfare?!? (SMH)

Powell does not look he is in good health.

The US needs to worry about the decision making of aging boomers.

^^^ This. Why do we not have mandatory retirement ages for political offices? Something like cannot be over at the start of their term

Even 67 is concerning though tbh, what do they know about the modern would?

Pretty sure a lot of law firms and hospitals have a mandatory retirement age because of cognitive decline and probably just an inability to fully adapt to the modern world/practices

I have said many times that there needs to be a mandatory retirement age of 70 for all Federal and State jobs; President, Supreme Court Judges, and down. Not only would this force turnover in positions and help to minimize the inability of the current crop to invest in developing future leaders, but it would also help to insure that those making laws were, at least, more capable of understanding current technologies and sociological changes.

OK people, slow down here. You’re stewing in and spreading ageism bullshit. Age brings knowledge and wisdom and wise decision-making. Wisdom is something you accumulate in the school of hard knocks. It’s not something you get automatically by swiping your smartphone. Most people are stupid in their younger years. Some stay stupid, and others get wise over time as the get older. Some people’s mental abilities deteriorate sooner, but lots of people never develop good mental abilities in the first place. Some people are mentally super-crisp into their 90s, and they fully benefit from the wisdom they’ve accumulated, and if others paid attention to them (rather than brushing them off as over 67 and in cognitive decline or whatever bullshit), they would also benefit. Other people start to deteriorate mentally at an early age and keep going downhill. So if you judge someone’s mental ability by the number of years they’ve been around, you haven’t been around long enough and haven’t figured things out yet. But wisdom may still come to you over time if you try hard.

Good one Wolf:

One of, perhaps my fave of the old folx who were kind enough to be mentors and femtors from 1940s to this now old one, said many decades ago, ”How soon we grow old and how late we grow wise.” ,,, and, clearly, some folx never do grow wise, eh?

Typing this, another proverb came to mind, ” Those who are not liberals in their youth have no heart; Those who are not conservative in their old age have not gained wisdom.” BUT, that does NOT absolve anyone of NOT thinking, eh?

Thanks again for your clear reporting!!!

Exactly. 67 is way too young to put out to pasture. And most 70 somethings, even those in their 80s, use a smartphone. It takes no talent to use the monkey see, monkey do technology of the modern era. Technology is made so easy nowadays even a caveman can do it. When computers first came out for the average consumer, you had to educate yourself on computers. DOS required some tech skill. Technology today has been dumbed down so anyone can use it. The young people who disparage older people think they are tech gurus. It’s laughable.

iM nint93 anddd…

Well said, Wolf! Absolutely correct.

What’s odd is that most of those trends go up and to the right. I’m old enough to rember when Japanese cars hit the market and nearly wiped out US auto producers.

Everyone with a brain said that the US was toast. Finished, but not so.

Beware of those who underestimate the power of the larget economy of the world. They are typically wrong.

We are a sick patient, don’t kid yourself.

But as you say we are also hungry hippos. The biggest and hungriest hippo of all.

The Ottoman Empire was a sick patient for roughly 200 years before it ended.

The Roman Empire was pretty sick for the last 1,000 years of its existence.

What the hell. The Roman Empire did not even last 1000 years from start to finish but during that time, it had some pretty good years considering the disarray most of the world was in. Is it that hard to use Wikipedia or Google?

Only 11% of our economy is in manufacturing,we need 10 years of onshoring .then we can’t compete because of wages and benefits.A SadsStory

The US is the second largest manufacturing country in the world, behind China. It’s larger than the next three manufacturing countries combined. But yes, agreed, the US needs to increase manufacturing high-value products such as semis and cars, not T-shirts.

The problem is the “Wall.”

In the NAFTA days we moved auto assembly to Mexico.

We could easily have a similar situation regarding semis (regarding infrastructural development and labor pool) but, the “wall.”

It’s already been built into the psyche of the World, due to the pandemic. It’s getting higher with each new conflict and geopolitical snark.

Interesting. We ordered a Subaru just ahead of COVID. Last year the dealer offered to buy the car back for just 4K under the purchase price after us driving the car for 40K miles. Crazy. Not sure how they are making any money, unless it is simply because they know the car has been cared for and can make money on the financing, whereas we just pay cash. So we took them up on the offer and are driving the new model.

Interesting times.

So, presuming all those auto sales that didn’t happen in June just got pushed ’til July, July should be a banner month.

And boost retail sales overall for July, given that autos are such a big-ticket item. Just in time to ruin the rate-cut party!

In terms of the number of vehicles sold, July should be pretty good. In terms of prices, I expect new and used vehicle prices to continue to drop in July. So those two combined would boost inflation-adjusted consumer spending measures. In terms of retail sales, the increase in vehicle unit sales would be balanced against the price declines, and we’ll have to see how that comes out.

I have a sneaking suspicion the hack or whatever is overblown. Autos are showing signs of a cooldown. A lot of demand was pulled forward and prices ran up a truly insane amount. Look at the retail sales data less gas and autos at your own risk. I’ve always felt the end game of this whole pandemic fiasco was that consumers find themselves overconsumed and underpaid. I’ve noticed it in my personal budget, where once it felt comfortable putting a set amount in savings monthly, a little bit of cost increase here and there has added up to make things a tighter than expected. I would be shocked if many people weren’t finding themselves in a similar or worse situation. The easiest remedy is to limit spending, which will show up one way or another in revenues the next couple quarters. I expect earnings to underperform as well.

Anecdotally I heard from my co-worker’s nephew who works at a large (chain of?) subaru dealer.

He said “they” paid $15 Million and got half their data back. The hackers want another $15 million.

Also that there’s a person of interest in custody. IDK/ I haven’t followed this closely.

If everyone reported real numbers, China is already number one. There is an advantage in being seen number 2.

Just look at our GDP. Wrinkle cream, adult diapers, and huge trucks for guys with size insecurity, is not the same as machine parts and exposts.

The Fed is just another government agency and expect rate cuts no matter who wins.

That will bring much larger deficits to support the lower half+ that do not benefit from any of the markets.

Ecommerce with the highest yoy gains once again.

Wolf – any idea what the lag is between spot freight rates jumping and when retailers pass this cost onto consumers?

Second, do you think this cost will cause a visible jump in the price of imported goods or just slow (pull in the opposite direction of where goods prices are currently trending) the drop as prices normalize ?

What is costly per product is shipping from the fulfillment center to the retail customer. That’s ecommerce. Amazon has its own shipping and delivery system, owned and through contractors. But others rely on freight companies. So if those rates go up, shipping costs in ecommerce will go up. Those shipping costs are either added to the bill as a separate line item when you check out, or eaten by the retailer (when you qualify for “free shipping”). So they might not change the posted retail price of the product.

But the freight costs of a container of merchandise spread over each item of merchandise in that container is relatively small compared to the ultimate retail price of the product (after huge markups), so increases in container shipping costs are not a significant part of the retail price.

A lot of stuff is shipped by air now, including the crap from Temu directly from China. Temu is losing a ton of money on each shipment, so higher shipping costs don’t really matter. But smartphones are shipped by air, so a plane full of smartphones costs a lot, but there are a gazillion smartphones on that plane, so per $500-smartphone retail price, the airfreight component is not significant.