Inflation has the upper hand. The market (Goldman Sachs and me included) vastly underestimated the Fed. Someday the market might get it right.

By Wolf Richter for WOLF STREET.

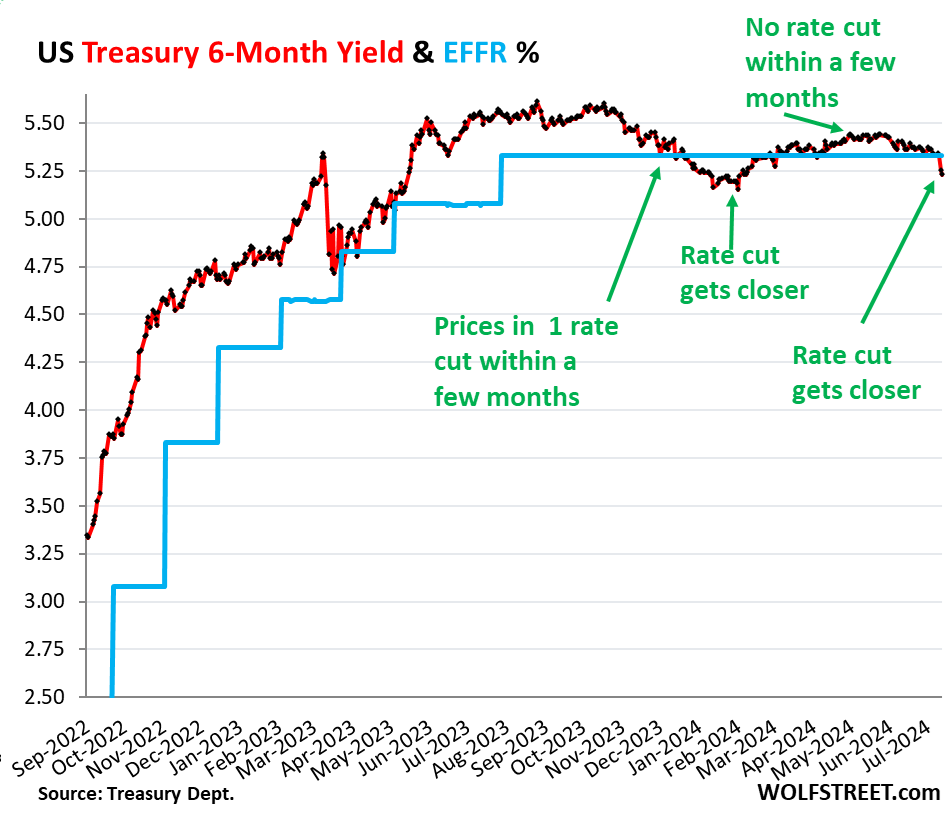

On Thursday, when the CPI report was released with a month-to-month reading of -0.056% (rounded to -0.1%), the six-month Treasury yield dropped by 8 basis points, and on Friday by another 2 basis points, to 5.23%. That combined 10-basis-point drop was a significant and visible 2-day move.

It brought the 6-month yield just a tad below the lower end of the Fed’s target range for the federal funds rate (5.25-5.50%), and below the effective federal funds rate (EFFR), currently 5.33% (blue in the chart below):

So the 6-month yield is now pricing in one rate cut within its 6-month window, more heavily weighted toward the first two-thirds or so of that window, after having already wrongly done so at the beginning of this year.

Back in late November through January, the 6-month yield had also priced in a rate cut within its 6-month window. By February 1, the yield had dropped to 5.15%, a sign the market was certain that there would be a rate cut at the March FOMC meeting.

But the market was wrong. Instead, we got a series of ugly inflation readings for January, February, March, and April, and there still hasn’t been a rate cut.

By March and April, with ugly inflation readings accumulating, rate cuts within the 6-month window of the 6-month yield were taken off the table.

May had provided a much softer inflation reading. And with Thursday’s CPI report of June, a rate cut within the 6-month window of the 6-month yield, weighted toward the first two-thirds of the window, was back on the table.

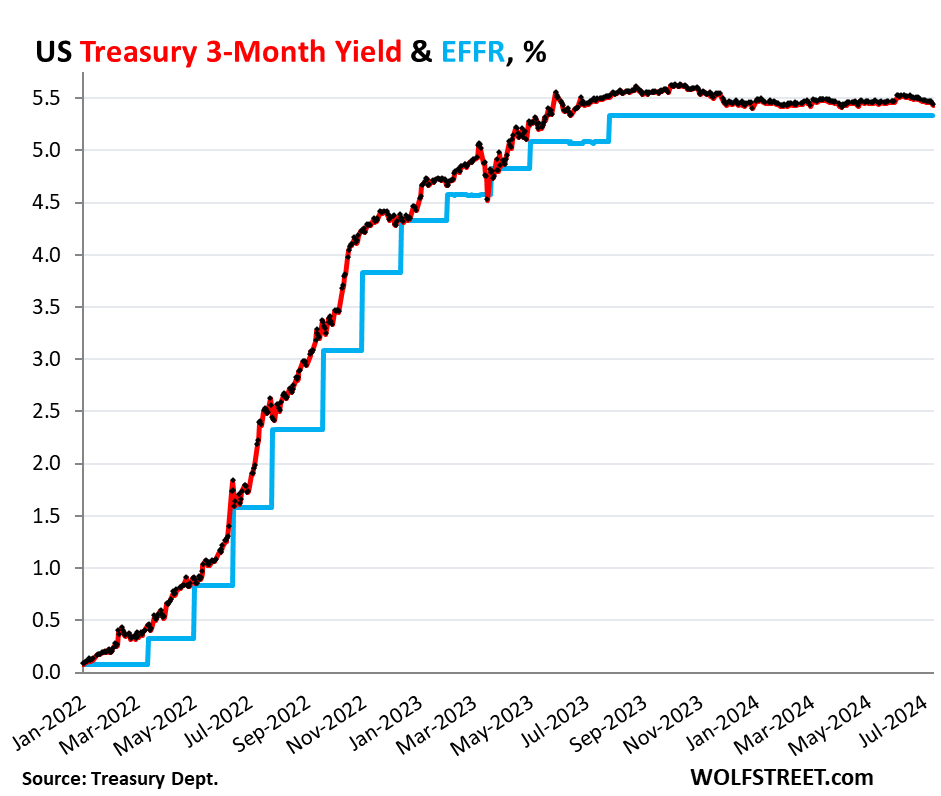

But the shorter-term Treasury yields are not pricing in a rate cut within their shorter windows. The shorter yields didn’t move much since the CPI report, and all were near the upper end of the Fed’s policy rates (5.5%), and all were above the EFFR (5.33%):

- 1-month yield: +1 basis point to 5.47%

- 2-month yield: +2 basis points 5.52%

- 3-month yield: -3 basis points to 5.43%

- 4-month yield: -5 basis points to 5.41%

In other words, the Treasury market is not expecting a rate cut in July at all, but sees a good chance of a rate cut in September, not as strong a chance as they saw in late January, when they saw a rate cut with near certainty by March that never came.

The three-month yield is not seeing any rate cuts within the first two-thirds of its window. No rate cut in July, and the September 18 FOMC meeting statement is beyond the first two-thirds of the window and has less impact on the current three-month yield:

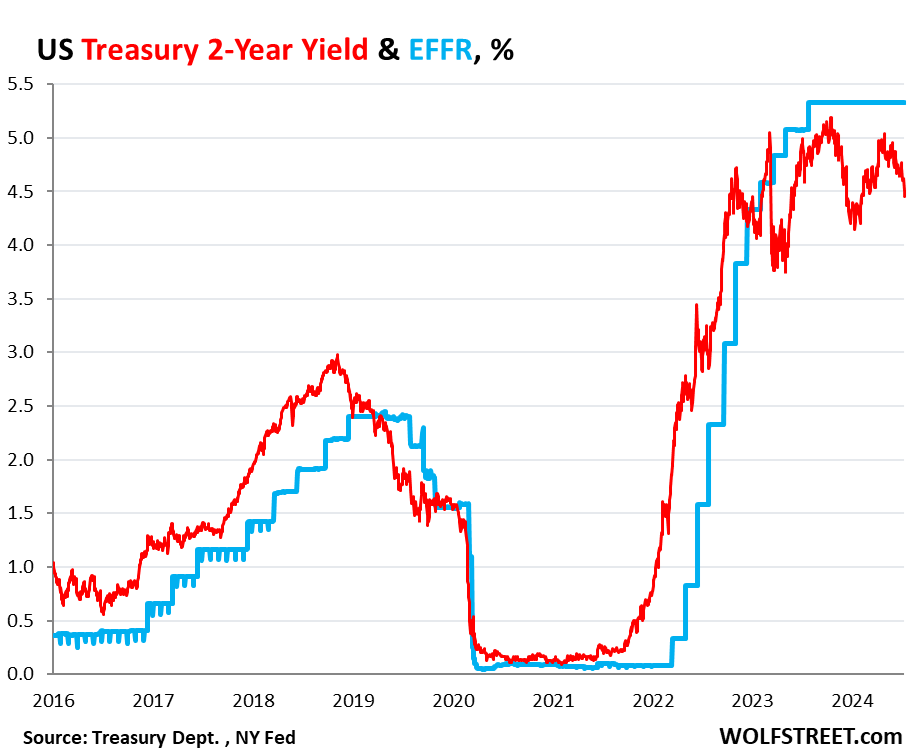

The market for the 2-year yield has been wrong all along.

The 2-year Treasury yield demonstrates how wrong the Treasury market has been all along about the Fed’s rate hikes and rate cuts: it expected far fewer and smaller rate hikes than what the Fed eventually did. And then without ever rising to the level that would price in the actual rates that the Fed has held for nearly a year, it started pricing in rate cuts before the Fed even stopped hiking rates.

So back in April 2022, the two-year yield was about 2.5%. Now, today, 2.5% sounds like a lousy yield, but back then – after 15 years of near-0% interrupted by a few years of higher yields that maxed out at around 2.4% in 2019 – 2.5% sounded pretty good, and the market thought that was getting pretty close to the Fed’s terminal rate.

In February 2022, before the Fed’s rate hikes started, Goldman Sachs predicted that the Fed would hike seven times in 2022, each by 25 basis points, and then in 2023 three times by 25 basis points each, one hike per quarter, to reach a terminal target range for the federal funds rate of 2.5-2.75% by Q3 2023.

The Fed ended up doing more double that, and by July 2023.

So the 2-year Treasury note that sold at auction in April 2022 with a coupon of 2.5% and with a yield close to that sounded like a good deal, and we, being part of the Treasury market, nibbled on some too. Two years was as long as we went. The rest of our Treasuries are T-bills.

Those 2-year notes matured in April 2024, and we got paid face value, and we earned about 2.5% in interest each year over those two years. The entire market was wrong – and so were we. The Fed would raise to 5.25-5.5% by July 2023, more than double the yield we received, and its rate is still there, and the yields of our two- three- and four-month T-bills have by far outrun our 2-year note.

The 2-year yield closed at 4.45% on Friday. The market never once came even close to betting that the Fed would hold rates above 5% for long, and they’ve been above 5% for over 14 months. And the 2-year yield has been below the EFFR for almost the entire time since January 2023, having turned into the Doubting Thomas.

The market was wrong about the Fed’s rates, and all 2-year notes that were bought at auction and that matured in 2024 or will mature in 2024 were a lousy deal. Buyers would have been better off with a series of short-term T-bills that stick closely to Fed’s actual policy rate — rather than follow market projections.

Someday, the market is going to get the rate-cut bets right. But it will only take a few more lousy inflation readings for the rate cuts to get moved further into the future. On Friday, the PPI showed up with red-hot services inflation, now delineating a clear U-Turn in December. Producers that pay those higher prices for services will try to pass them on, and so they may ultimately filter into consumer prices and higher inflation readings over the next few months. Or if producers cannot pass on the higher costs of services, their margins will get squeezed.

Inflation is unpredictable. Once inflation has broken out in a big way, as history shows us, it tends to come in waves and tends to dish up nasty surprises. And it already has dished up nasty surprises multiple times so far, including each of the first four months of this year.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hopefully Powell by now has fully internalized the lessons of the 1970’s (“nasty surprises,” as Wolf wrote). Also I hope Powell is now immune to a forceful president’s pressure (as in 2018 or so). Then there was the “transitory” delusion of a couple years ago, to reinforce the lesson. Any possible next president seems poised to stoke even more inflation. Only a big outburst of actual new productivity would seem to fix it, right? Or else a recession, hopefully transitory? Or else, I’ll just sit tight and collect my yield.

Any and all interest rate policy decisions at the Federal Reserve are based on unanimous consensus among the 12 member Federal Open Market Committee (FOMC) with none being made unilaterally by the Chairman of the Federal Reserve.

No unanimous consensus required, though they aspire to consensus most of the time.

Votes are taken among the relevant FOMC members.

Inflation is unpredictable.

July 2008 = 5.6%

December 2008 = 0.1%

February 2008 = -0.1%

I’m going to miss the 5.00%+ high yield savings accounts. They’re bringing in more than our Social Security. We can get by on our SS but will definitely be cutting back without the interest income.

The Treasury might miss us as well 2 years ago we paid no income tax. Last year we paid $2600 due to the interest income.

Spend the 5 million net worth and enjoy life.

2 SS incomes at 60k is only about 1.2 million at 5 percent don’t know where 5 million came to be and please celebrate wealth and prosperity because I don’t like the alternatives having lived in Russia to see the consequences

Right now there are people in America living (and dying, per Angus Deaton’s “Deaths of Despair”) lives just as dreadful as those of the Yeltsin years in Russia. Even that horrible lick-spittle for Empire, Niall Ferguson, can see the awful parallels as outlined in his recent piece in The New Press, “We’re All Soviets Now.”

They’re not bringing in anything. The interest only allows your money to keep up with inflation. Money devalues 5% from “inflation” and gets 5% interest, you break even.

break even before income taxes, that is.

Inflation isn’t 5%. At least not as measured by any sane, reputable information source.

Jerome Powell was in his twenties during the 1970s inflation. There is no way that someone lived that and “not internalized the lessons…” If Powell is doing something else than stopping the 1970s style inflation, then they (FOMC) have some other agenda(s).

Well, he lived through the 1970s inflation and then went on to stoke the 2020s inflation, so…

Other agenda(s).

He did not purposefully stoke 2020 inflation. He prevented having the GFC turn into Great Depression 2.0 and he prevented the pandemic becoming a huge economic crash.

Those were the “other agendas”.

The Fed could have done better but they did do well.

They did horribly, and you know it. That whole “they saved us from another GFC” line of BS gets really old. It may justify what they did during the first three or four months of the pandemic, but it does nothing even close to excusing their unforgivable pouring of gasoline on the raging inferno that was the US economy–and especially the housing market–from late 2020 all the way to mid-2022. They never should have done QE, period. They especially never should have bought MBS.

And having made those gross policy errors, they should have been much quicker to at least taper them. There was very clearly no reason to keep pouring hundreds of billion dollars a month into the markets in February 2021, when meme stocks and crypto and batshit insane housing appreciation and soaring prices for automobiles and other goods made it abundantly evident to everyone everywhere, even to the most model-driven, blind-to-actual-reality FOMC members, that the economy was massively overheated.

And even to the extent that any of this was the result of such fiscal absurdities as PPP “loans” to people who didn’t need the money and CARES Act implementation that wad an open invitation to fraud, the Fed should have been aware of how directly the money they were printing was being pumped directly into the consumer economy, and of what that could leaf to. They ignored all the warning signs, declared the inevitable inflation “transitory” in June 2021, and kept spewing gasoline on to the fire into 2022.

Pea Sea,

It might be easy to live life through the 20/20 hindsight of knowing what happens after the fact and not having to personally act when facing unknown crisis.

That is better known as Monday morning Quarterbacking.

20/20 hindsight, my ass. Monday morning quarterbacking, my ass.

I could see how reckless they were at the time, and I said so, and Wolf could see it at the time, and he said so, and quite a few other people could see how badly they were screwing it up at the time, and they said so. This “hoocoodanode?” BS is just ridiculous, and transparently so.

I agree: When I heard about the general stimulus check that was directly deposited into my account I shuddered.

I am not an economist but to quote one Mr. (Steve) Hanke: “inflation is always and everywhere a function of the money supply.”

He has helped many countries recover from hyperinflation (which is 100%+ per annum).

The authorities have the “other agendas” in mind. I had a neighbor (carpenter, not economist) at the time remark that the pandemic was “a form of financial warfare.”

In the face of the Chinese economy outpacing the US economy (up until…?), this all makes perfect policy sense.

re: “inflation is unpredictable”

No, that’s wrong. Remember that in 1978 (when Vi rose, but Vt fell) all economist’s forecasts for inflation were drastically wrong.

Put into perspective: There were 27 price forecasts by individuals and 9 by econometric models for the year 1978 (Business Week). The lowest (Gary Schilling, White Weld), the highest, (Freund, NY, Stock Exch) and (Sprinkel, Harris Trust and Sav.).

The range CPI, 4.9 – 6.5 percent. For the Econometric models, low (Wharton, U. of Penn) 5.7%; high, 6.6% U. of Ga.). For 1978 inflation based upon the CPI figure was 9.018% [and Leland Prichard, in his Money and Banking class, predicted 9%].

In 2021 as rates started back up I was thrilled to grab a 10 year CD paying 1.8%. I’m holding to maturity as a constant reminder that I know nothing about the future.

Sounds like you went to the “Harvey Mushman School of Investing”!

Great comment. I feel the same when I get a stock pick right.

Wolf

Those shorter term yields 1 month – 4 months have all increased a bit recently, because when the market start to believe that a cut is coming, there is a certain amount of capital (depending on how strong that believe is and how many cuts are expected, and how soon those cuts are expected) is relocated from those shorter terms instruments toward higher duration so it can gain from the appreciation caused by the cuts. That’s how the overnight market and longer term fixed income market are connected, and that’s how a rate movements in overnight market impact the longer term fixed income instruments, through the movement of the capital which impacts directly the real yields. And that’s the problem with cutting rates, because it creates this capital relocation, which results in a scarcity of liquidity in the overnight market, which requires FED to stabilize it initially by injecting liquidity, and that’s why the FED had to decrease the pace of the QT in advance of the rate cut, and the treasure to slowdown it’s borrowing through TB. Here you have the whole picture of what is going on. However, at this point it doesn’t even mater if the FED actually does or not the cut at the end of July or September, because the market movements have already occurred and it will keep occurring during this period.

1. “Those shorter term yields 1 month – 4 months have all increased a bit recently,”

Not really.

1-month yield (5.47%) rose 2 basis points over the past four days, but it’s down 1 basis points from five days ago (5.48%) and it’s the same as a month ago. It really hasn’t changed.

2-month yield (5.52%) is down a little from a week ago, but up from a month ago. But small changes.

3-month yield (5.43%) fell 3 basis points over the past two days and fell about 10 basis points from a month ago.

4-month yield (5.41%) has dropped to the lowest since April 9.

2. “… certain amount of capital … is relocated from those shorter terms instruments toward higher duration …)

No, that’s impossible. The market cannot reallocate capital. Every single T-bill is held by someone, and every single 10-year note is held by someone. If one investor wants to sell T-bills, someone else HAS to buy them, thereby putting into T-bills the same amount of capital that the selling investor pulled out of T-bills, and the net effect is zero. The market cannot draw capital out of T-bills, not possible. The only thing that can change in the market is buying pressure and selling pressure.

In fact, the opposite of what you say is true. Treasury is issuing a huge amount in additional T-bills every week that the market has to absorb. So on net, more money is going into T-bills due to new issuance. Longer term debt is also increasing and new money MUST go into it to absorb it. So your theory doesn’t hold up.

The supply issue is a key point. The Fed is issuing tons of short-term bills to suppress the interest rates on longer notes and bonds. This strategy creates a lot of interesting possibilities.

Money market funds hold a lot of these short-term T-bills, but the “cash” in money market funds is part of M2. So it’s cash, but not really cash – if the money market fund investors wanted to use their money to buy stocks or goods, the money market funds would have to sell T-bills, flooding the market. This would presumably cause short-term rates to rise even further.

yes, but…

“The Fed is issuing tons of short-term …” should be: “The Treasury Department is issuing tons….”

This Doubting Thomas has been heavy into T-Bills (and no T-Bonds) since 2022. Good in one sense because since April 2023 I have been earning over 5%, free of state income tax, and “risk free” (in terms of credit risk, but not in terms of purchasing power). But I have been absolutely spanked by the opportunity cost of having the money in T-Bills instead of the S&P 500. So, you win some, you lose some. As one of the contributors here often says, may we all live to see a better day.

T-bills and S&P 500 are not the same. The difference is RISK. A lot of risk – the probability of losing money. T-bills have essentially zero chance of capital loss. S&P 500 has a decent risk of a 50% loss.

Thanks, Wolf, (and BenR and ShortTLT below) for reminding me that a 10% return over two years, free of credit risk and state taxes, ain’t too bad. I feel like less of a goof. I’ll stop beating myself up.

Since 1/2022, spx is up 20%. 4 week T Bills earned roughly 10% in that period, no state tax. It’s a big difference, but were you ‘absolutely spanked?’. In SPX, you could’ve earned even more, or you could’ve lost 70% of your principle. It’s called a risk premium. Without a crystal ball, in this financial environment, you made the smart choice imo even if your balance is a bit lower than it could’ve been gambling with extreme stock valuations in a potential bubble. There’s also something to say about risk free investments being less stressful and time consuming through all the variance.

It’s all about perspective. If you’re not a fund manager, no need to worry about outperforming any of the indices imo.

I’m up 20% since this time last year yet still underperforming SPX. I don’t care, it’s still a great return. If it were two years ago SPX would be -20%.

You can always buy SQQQ.

I too went thru a big de-risking (moved 75% into T-bills) at the end of 2022 after being UP 2% for the year, but also missed the 2023 SPX rally.

Don’t worry, there are still lots of great investment opportunities. Income-focused mutual funds are paying 8-14% distributions if you’re looking for a more ‘drama-free’ way of getting a better yield.

NB: for entertainment only, not investment advice.

That’s the longest comment in Wolfstreet history

FYI: read this at treasury:

Remarks by Assistant Secretary for Financial Markets Joshua Frost on Principles of U.S. Debt Management Policy

July 11, 2024

I tried to keep it short.

I will read that, thank you for the suggestion.

IMHO, producers are more likely to eat the price increases this time around and not, in general, pass them along to consumers. At most over the next few months, it may lead to a plateauing of inflation, but I don’t think we’re on the cusp of a reversal of the overall trend down of headline CPI. The Fed is now watching the unemployment rate as much or more than the CPI readings. JPowell just came out this week, without giving us an estimate, that the neutral rate has moved higher. Everyone has been waiting at least six months for him to finally make this proclamation. In the meantime, the 4W unemployment moving average has moved higher six out of the last 7 weeks.

The Fed will lower rates in Sept.

The Federal Reserve will not change its rates at all during this year which is an election year.

With red-hot services inflation, I wouldn’t count on a rate cut. As for raising the natural rate, I doubt it, but if they do, don’t be surprised when the entire yield curve goes up 100 basis points. You think there’s no cost to permanently raising the target rate, you’re going to be disappointed.

Of 2025?

Inflation is still running at 3.3-3.5%. the Fed will keep pretending to be planning to lower rates soon so that the market doesn’t freak out.

I think after the election they’ll let reality dawn a bit more on everyone – that inflation is still too high and they need to remain in wait and see mode. Rates cuts… someday.

Honestly, given what is already happening in this country right now a 25-30% market dip into the new year would be the least of our problems.

Howdy Folks. Bubba said this before to the squirrels that were reading??? So here it is again, purchase 28 day T Bills and wait and watch. Bubba bets you it will take a few years or more and then, lock into bonds. Maybe. We could see history repeat like the Carter Reagan years. Check out what the inflation rate and interest rates were then. Gonna be a great show. You know the new president and new congress is gonna spend more……

Hang in there Youngins

Completely agree. All cycles repeat and this one is the 70’s. You might want to portion some T bill cash into miners. 5% doesn’t even keep up with real inflation.

I’m looking for one rate cut as soon as possible. The sooner they cut, the faster inflation will return with a vengence. If they wait until the beginning of 2025 for the first cut, they may actually dodge the inflation bullet, which would be a bummer. I’d like to see those long treasury yields move higher for the *long term health of the economy*, and a return of inflation through a cut as soon as possible is the best way to make that happen.

Some see it so that once they start cutting, the market will go down (Di Martino Booth, for example). Historical data confirms this as well.

Both correlate to a souring economy.

How fast the data can change.

Work: Excavators…regardless of manufacturer all offering 0%

loans 48 – 60 months

Personal: Mrs is looking at new car…1st since 2015.

Expecting to trade & pay balance with cash.

Surprise: Her 2 choices: Mazda CX-5 ..0% 36 months

Hyundai Tucson: 1.9% @ 48 months

I think I’ll keep my cash working.

Those low/no interest rates are being subsidized by the mfgr if I had to guess.

Same principle as rate buydowns by the homebuilders.

Isn’t it that they typically cut rates in response to an economic slowdown in order to stimulate and that is why it correlates like that? I never checked for myself I just heard it somewhere and always assumed it to be so

Apparently, yes.

I was just reacting to JeffD’s statement: “The sooner they cut, the faster inflation will return with a vengence.”

I think if the cut triggers (or correlates with) the bull market reversal, this will hardly result in the return of inflation.

BTW, Di Martino just the other day suggested the FED are already behind the curve and will urgently cut 0.5 in September.

Interesting.

The kind of inflation we saw over the last four years is hard to suppress, and surges in waves. You have got to remember that $10 trillion was dumped into the economy essentially overnight during the pandemic, and is still out there circulating and recirculating. On top of that, there is huge fiscal stimulus coursing through the economy, with much of it just now arriving from legislation passed many many months ago. The bifurcated distribution of wealth during the pandemic has resulted in entrenched inflationary mindset as about 1/3 of the population is wealthier than they have ever been, and are still spending with a “pay whatever” mindset. For this third of the population, many of them refinanced at sub 3% mortgages dumping more money into their pockets than they have ever had, and now that their home prices have appreciated 50% or more, they are feeling flush as they can “cash out” more of their home value than they could have ever imagined. Another portion of that wealthy 1/3 has seen their stock market assets almost double. If you think this situation does not mean more inflation down the road, you are fooling yourself. As rates drop further, all these asset holders can (and will) take out loans on their increased equity to stimulates the economy even more.

PS As of September 2023, the annual spending of the top 20% of the population is essentially equal to the annual spending of the lowest 60% of the population. Here is the average annual expenditures by income quintile:

1st: $32,612

2nd: $47,657

3rd: $61,950

4th: $81,957

5th: $140,654

Yes, you read that right, *twenty percent* of income earners (not households, but individuals), spends an average of $140,654 year, each. Guess which group businesses focus on when setting prices? That’s right, the “pay whatever” group in the top 30% of income.

Correction: a BLS “consumer unit” is sometimes an individual, and sometimes a household. The BLS won’t come right out and say it, but a “consumer unit” likely equates to a tax return filing.

@JeffD

The vast majority of the CPI & PCE indices consist of everyday necessities (food, electricity etc.) that everyone buys.

The so-called K-shaped economy might inflate the prices of yachts & private jets, but they hold very little weight in the CPI if any at all. Because a very very small fraction of Americans buy them.

The 2009-2020 bull market made the rich fabulously richer, yet none of that added wealth made its way into the inflation indices.

@Jackson Y,

There was no “pay whatever” spending by the upper 30% between 2009-2020. Now you can’t get away from it, and it affects *everybody*. It’s akin to winning the lottery — an immediate infusion of a ridiculous amount of money. Most lottery winners go broke because of the mindset that ensues with such winnings. Now, the upper 30% of the country have the lottery winner mindset, and they are breaking the economy. It is a “trickle down” lifestyle model that aspirational spenders now look to as the standard. Consumer credit has not dried up, one lick. In fact it has loosened. This won’t end well.

@Jackson Y,

PS Services is where all the inflation is coming from, not goods, which buttresses my argument in spades. If there is anyone in the country that consistently overspends on services, it is definitely the top 20%. Contractors come over to a house, throw out a ridiculously high number, and eight times out of 10 these people just say, “ok”. That’s it, with no mention or ask of *specifically* what they are getting for the quoted price.

Base effects going into the fall will likely show inflation hot or at least warm enough to keep things higher for longer.

I thought base effect was expected to impact inflation numbers by June/July…

Why would there be any rate cuts whatsoever in the Federal Funds interbank lending rate set by the Federal Reserve?

Bad decision making?

There’s another perspective to the 2-year rates under-performing the actual: the holders are making bearish bets.

They might be betting that buying a 2-year at 4.5% now will gain them hefty appreciation if the economy tanks and the FED drops rates into the dirt overnight like it did in March of 2020.

Depending on the timeframe, their 4.5% notes could appreciate substantially if EFFR hits much less than that earlier enough in the life of the note.

Rate cut hopium is the only reason duration is yielding less than the 13-week bill.

The shooting of Trump is likely to cause another wave in the bond market.

But Trump has actually been calling for a rate cut so far, and I don’t think it’s right to shake rates just by speculation.

Because long-term high interest rates, corporate bankruptcy, unemployment, etc., are more serious problems, and Trump is a clever person who is not stupid enough to overlook that

Trump just cares about inflating away his own debt and pumping his own assets.

He is not clever.

@MussSyke It’s all relative: To his supporters, he’s a genius! =]

What I’ve noticed with my 3 & 6 month T-Bills “ladder,” is that it is very difficult to buy through my brokerage account longer term than 6 months.

This is a bit of a problem, because I want to hedge my bets and buy 1 yr, 18 months or even 2 year (the beginning of the “belly of the curve”) BUT THE MINIMUM necessary is 300K or even 500k which is a nit more than I can handle!

Seems like the Janet is forcing the small time M&P (non institutional) investor (not gambler) into the less than one year maturities !

WHY? & so what does that mean for the future?

Thanks Wolf for your charts & words that clearly illustrate what the heck happened. It’s so important to pause & think and look back to put things into perspective!

Consider getting a treasury direct account, and bypass that broker.

Exactly. Treasury Direct has a somewhat dated online interface, but it works fine *and* you can buy the maturity you want in the amount that you want, with no middleman.

By the way… does anyone here know what would happen if the broker who took your money, and was holding a T-Bill or T-Bond on your account, went bust before your Treasury matured? I assume you would get your money back eventually (right?), but how long would it take, and by what process?

In any case, another reason to cut out the broker and buy your Treasuries on TreasuryDirect.gov.

(Correct me if I’m wrong. I’m here to learn.)

And in smaller quantities. My construction of a sinking car fund is constructed of 4 wk, 26 wk (previously, now just 4wks), 2 yr and a few 3 yr notes bought each month. Coupons and reinvestment proceeds go directly to Ibonds at the end of the month. 18 months into this strategy. I guess I’m part of the demand problem.

Howdy dougzero. Ditto

I’ve found some cusips have absurdly high minimums thru both my brokers (Merril & Schwab). I just use their fixed income search tools to browse the offerings, and then open a bunch of them in new tabs till I find one with a $1000 minimum.

There are almost always 13-39 week offerings with that $1k minimum, just keep looking. There should be 1-2 year offerings with that minimum too, but personally I’m not buying that kind of duration yet.

FWIW, I don’t think this is a deliberate choice on the part of Yellen or some other tsy official, but I too have wondered where these high minimums on some CUSIPs comes from. I bet Wolf can explain.

Wolf — can you elaborate on what you mean by “The three-month yield is not seeing any rate cuts within the first two-thirds of its window” specifically the part that on “first two-thirds of its window” ?

I understand that you’re comparing the Fed rates to the yield on the 3 mo bill. What I don’t fully understand is if you’re implying that the last third [of the 3 mo T bill] implies a rate cut in Sept?

Today’s T bill matures ~Oct 13 or whatever so it would need to trade somewhat below EFFR to imply a rate cut in Sept, no ?

The closer you get to the maturity date, the closer the price will be to face value. At the maturity date, you will get face value, and then whatever the Fed does has zero impact on you because you got the proceeds from face value. If you’re one month away from maturity date, you know you get face value in 30 days. If the Fed cuts 30 days before maturity date, and you then sell, there is little price difference.

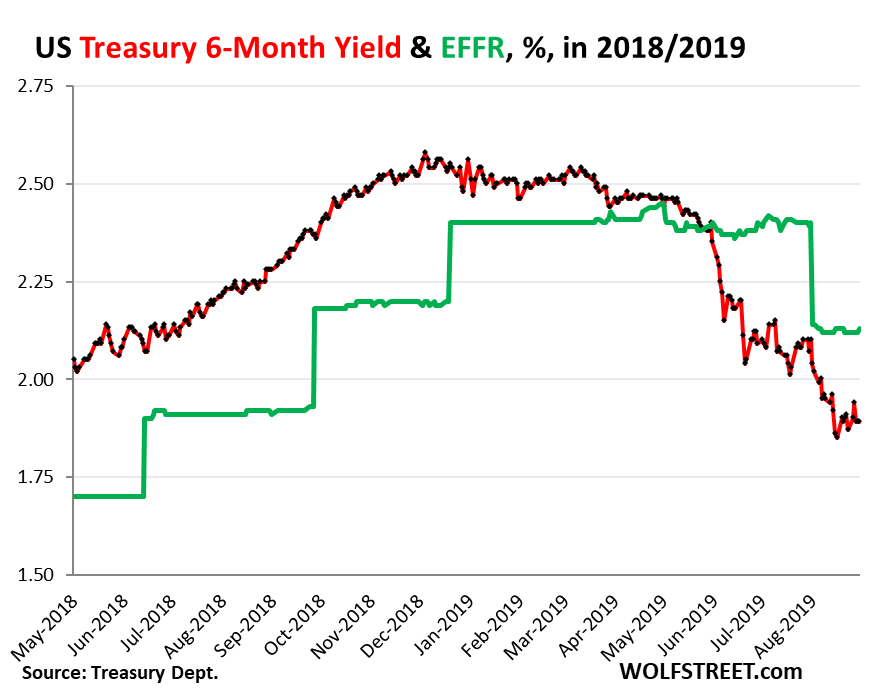

Here is the six-month yield anticipating the Aug 1, 2019, rate cut. Five months ahead of time (with a maturity date in early September), it started moving down, but stayed above the EFFR. About 70 days before the rate cut, the six-month yield fell below the EFFR. And 60 days before the rate cut, the six-month yield (matures four months after the rate cut) had dropped to the rate-cut level, fully pricing in the rate cut.

The $1000 minimum likely is there because the interest earned at that level barely covers the administrative cost of tracking/managing the bill/note/bond over the term of the security. Imagine what it was like when the bill were just paying 0.15% interest. That said, I’m just guessing though.

When I go to roll over my T-bills, the CUSIPs I’m looking at occasionally have very high (i.e. $20k, $100k) minimums vs the typical $1k minimum.

It’s common for corporate bonds to have very high minimums, but I’m a little surprised to see some T-bills like that.

The best rates come usually with high minimums. However, most bills have deeper order books with much lower minimums at least on Fidelity. You might give up a pip or two but that is not an issue if you do not invest multiple 100ks or more.

Not sure what Janet has to do anything with Brokers putting minimum 1K and in multiples of 1K limit to trade Treasury Securities. They are your Broker’s rules and nothing to do with US Treasury. US Treasury sell them in multiples of 100 and NOT 1000.

TBH I dont even know why someone should go with Broker for T-Bills and Treasury Securities if you are going to hold them till Maturity. Just use TreasuryDirect. It has numerous benefits.

e.g. We dont lose any Interest too (not even a day) e.g. 4 Week gets picked from your Bank Acct on Tuesday and gets Deposited on Monday. If Monday is Holiday then your Bank may credit them on Friday itself.

4 Week Bill Auction happens on Thursday.

Brokers block your money as soon as Auction is over and they take 2 days after Maturity to Credit the Money to your Account.

I have rarely had to wait a single day past maturity to receive bond proceeds. And those rare cases where funds were deposited a day late were corporate issuers.

Same. On the day of maturity, Merril credits my account (shows up as ‘anticipated funds’) and then it formally settles the next day. But the anticipated funds are part of the ‘cash available to invest’ pool, so I can imediately roll over the T-bill.

My broker is smart about this. The Thursday T-bill auction settles on the same Tuesday on which I get proceeds from the maturing T-Bill that I bought 28 days prior.

Schwab knows this, so they let me participate in the the auction that occurs four days before my old T-Bill matures. The two transactions settle on the same day, so I don’t pay margin interest, and I have no gap between last month’s T-bill and this month’s T-bill.

Ahh so it’s the broker doing that – but why?

Fwiw: I have a TD acct for my I-bonds, but prefer to keep my T-bill ladder in my brokerage acct. This ladder is basically my long term “cash” that I want to maximze the risk-free yield on. I can sell the entire ladder at any time with no haircut, and it would just take a day to settle and become actual cash.

I’ve found that Schwab has very high minimums after hours. But during market open hours, the minimums are reasonable, and I can almost always find a $5k minimum.

“Someday, the market is going to get the rate-cut bets right.”

Hah Wolf, you’re more optimistic about this than I am. I feel like the stupid bond & fed fund futs markets have been “pricing in” the wrong rates since the Fed started hiking.

Rate cut bets are greatly influenced by Fed officials blabbing to the press. The fact that Powell starting talking about rate cuts in 12/23 is almost criminally negligent, and softened much of the impact they were hoping to achieve by raising rates. So we end up with higher, for longer, and asset bubbles becoming more entrenched and harder to pop.

For me I don’t see it that way, I think if FED officials were barred from speaking the analysts, media, fund managers etc. would still speculate in the exact same manner as they do now. Even if FED officials were strictly “hawkish” when speaking it wouldn’t matter IMO, people would still find a way to justify rate cut projections somehow and the FED would be blamed for doing or not doing something.

1) JP first attempt to eradicate negative rates failed in Dec 2018. His second attempt was more successful. All CB rates, including Japan’s, are positive. Gravity between the US yield curve and the rest of the world pull them together. Gravity pulled the US10Y is under EFFR.

2) The Inflation M/M % downtrend cont. Its down from 9.1% to 3%. If the

Fed will not take defensive actions it might breach the 2%, the Fed target, on the way to zero.

3) Lower rates will help the regional banks that buy O/N. They will reduce gov interest payments, unless we enter a recession.

4) QQQ needs a decent correction. When our new national industrial factories will be completed or almost completed demand for highly skilled and semi highly skilled workers will be high. Transfer money will deflate. Needy elderly might get some help from the gov.

5) The gov will collect more taxes and fill up its coffer. The budget deficit might flip to surplus. Debt will be cut and the stock markets will roar and popup. At a certain point the Fed will have to send a few negative pulses to the feedback loop, to stop the madness, before it collapse like in 1929.

“The budget deficit might flip to a surplus”

That is an extremely bold prediction that ought to be backed up with evidence. Or at least a reasonable theory.

We have not run an annual budget surplus since the days of Bill Clinton, or maybe the 1st year of GW Bush’s term. That’s over 20 years ago.

Somebody has to buy the $34,000+ billions of bills & bonds every week..

Boils down to the Fed and/or the public. My guess is that the Fed will cave Ito political pressure and reduce rates. How will the public react?

My guess is inflation will be the big factor in the equation.

B

The Federal Reserve does not control the yields (interest rates) on US Treasuries and they will not be reducing their Federal Funds rate at all in this election year of 2024.

“The Federal Reserve does not control the yields (interest rates) on US Treasuries”

This is technically true but misleading. The whole point of the Fed’s various policy rates is to set a floor & ceiling on rates in the broader market.

Re: “ Buyers would have been better off with a series of short-term T-bills that stick closely to Fed’s actual policy rate — rather than follow market projections.”

I totally agree! I parked my dough in a money market after selling my house and decided to do nothing, which has worked reasonably well, but like everyone, I’m antsy about the likelihood of these rates falling eventually. I’m not entirely sold that I’ll end up in a better position with shorter t-bills — seems like a wash?

I appreciate you sharing your experiences with investing in treasuries!

It’s painful watching the concentrated S&P defy reality — I guess I’m dumb. I’m increasingly wondering about capitulation and pondering my pessimism — full of doubt about my intuition, thinking that I might as well through in the towel and embrace the ai bubble — but I just can’t get the courage to believe in optimism that’s fueled by contrived hype, that has no context.

I don’t think money market yields will drastically crash in the next year, so I’m trying to train myself to ignore more and more media spin and double down on being patient.

Read my lips; “Higher for much, much longer”

All the comparisons to the 70’s, when DEBT/GDP was manageable, are wrong. This is 2001, with the added complication of unhinged corruption in D.C.via K-street, and massive deficit spending on top of an already paralyzing DEBT/GDB.

Hedge accordingly

I tried to donate 25 but I changed my phone number and can’t get a text message.

Thank you.

I assume that’s PayPal?

You can try Zelle through your bank. That works great, and once it’s set up, it’s a breeze to use. And it’s free for both of us. You can use my contact email.

Learned from you today.

I analyze interest rates using the monetary aggregates. Money lags are not long and variable. I use a 24-month moving average of long-term money flows relative to the prior trend’s “arrow of time”.

The reason that the market gets this wrong so often is that their analysis is done by a bunch of Wall Street “quants” who think they can plug a bunch of numbers into a spreadsheet and have it spit out an answer. Meanwhile the actual policymakers have a VARIETY of problems that they are looking at…

1) Short-term economic policy (eg. fighting inflation without triggering too much of a recession)

2) Long-term economic policy (eg. reducing the Fed’s ballooning balance sheet which brought on the inflation in the first place and would certainly feed it going forward)

3) POLITICS!!! The Fed is an INSTITUTION and institutions absolutely excel at ONE thing… protecting themselves!!!

Consider this…the Fed delayed ANY Fed Funds Rate increases this cycle until AFTER Jerome Powell’s nomination had been confirmed by the Senate Banking Committee in March of 2022. Why? It was more than obvious (by then) that interest rates needed to go up because inflation was in fact NOT “transitory” at all. Simple answer… the Fed didn’t want to give ammunition to those in Washington who were trying to derail Powell’s reappointment (such as Sen. Elizabeth Warren).

Another example… Wolf says that the Fed more than doubled the Goldman Sachs estimate of a terminal FFR (2.5-2.75%) and did it faster than GS expected. Why? Because the Fed has INSTITUTIONAL knowledge of how hard it is politically to get a “do-over” on these big policy moves. Whether it is the Obama-era “Recovery Act” that ended up being too small (but not repeatable) or the 1980 yanking of Volcker’s chain by the Carter White House… in a politically divided era you basically only get a single chance to get a policy right before opponents handcuff you. 20-something year old “quants” are not going to remember these lessons but they are definitely remembered by 60-something year old bureaucrats embedded in ANY governmental organization.

So the Fed doubled the pace AND the amount of interest rate increases so they could get out of that game well before the 2024 election year… and then they adopted a wait-and-see approach that continues to this very day. I have been saying ever since the market went crazy reading the December “Dot Plot” to not believe that ANY rate cuts were coming… absent a double-digit inflation reading or a 9/11-style attack, the Fed is NOT going to adjust interest rates (up or down) until after this election is over in November.

PS: I am not saying that everything the Fed does is because of politics. I am simply saying that the political environment that an institution operates in impacts the speed and timing of their decisions. For instance, in the rest of the government a Presidential election year is a time to SPEED UP the policy-making process… they try to get as much done in that last year of a term as possible…that way a change in government doesn’t cause a halt in that policy-making process for X amount of months/years waiting on a review by the new incumbent President’s team.

The Fed works the other way… a Presidential election year is a time to do next to nothing in order to avoid their INSTITUTION being blamed (by one party or the other) for the outcome of the election.

My apologies People… that was way too long of a post. I need an Editor.

Not IMO SG,,, appreciate your thoughts on the political aspect; mostly similar to mine, but you did a good job of integrating the politics with the other fundamental challenges facing FRB.

As to the editor question, it Would clearly be handy to be able to repair spelling especially on Wolf’s Wonder, but he has explained why editing is not available, so we just need to be more carfull, eh?

“absent a double-digit inflation reading or a 9/11-style attack, the Fed is NOT going to adjust interest rates (up or down)”

I agree with this.

The Fed right now is like a big oil tanker – it will take a LOT for them to change course (in any direction).

Treasury Direct seems to work pretty well for short term bond buying but I can’t tell if the reinvestment option gives you a continuous return or not.

Seems like there’s a gap between auctions that may not be covered so the real return on X dollars is less than the annualized one. Hoping I’m wrong about that. Info appreciated.

In my years-long experience, all scheduled reinvestments via Treasury Direct occur on the same day that the original T-Bill or T-Bond matures. There is no gap or delay in earning interest on the newly issued security.

Thanks!

If you click on the “History” tab at the top of the Treasury Direct home page and then click on “Security history” you will be able to see the reinvestment dates for your securities. For example, A 4-week bill might show 4-9-24, 5-7-24, 6-4-24 as the transaction dates for “Reinvested Security Issued.” The reinvestment interval should match the term of the security. Reinvestments should be scheduled more than 4 days before maturity since that is the duration of the “closed book period.”

Thanks! I think that’s what I’m running into with the individual ‘cash flow’ ones I’m doing. Gotta make the call whether to re-up sooner. Basic stuff but been investing in myself for a long time and haven’t paid much attention while rates were zero. Way better returns. ;-)

What happens to the leftover interst when you roll bills over on TD. Does that also get reinvested?

Go to:

History » Security History » Detail

and look for “Refund” and “Refund Payment Destination:”

This makes it convenient for investors that wish to tap into interest income. I could be wrong, but when it comes to interest it does not seem possible to “let it ride” for scheduled reinvestments.

I have tried, but failed, to figure out how to get T-bill interest reinvested automatically along with the T-bills on auto-rollover. There may be a way, but it’s not apparent to me.

You can specify how many times you want to reinvest any particular Security you have bought. You can EDIT it prior to certain days only before its Maturity.

When you can buy itself you can specify how many times you want to reinvest. If 4 week Bill I guess you can change it till Tuesday afternoon. Not sure about exact cut off time. But until Security goes into Pending for Maturity status. Option is under Manage tab. Select the Security. Manage View/Delete a pending purchase/reinvestment or Redemption.

As far as T-Bill, if you choose to reinvest, the Interest goes to your Primary or Default Bank Account. You can verify your Primary account from Bank list. Usually it is first account which you gave to TD.

Personally I don’t prefer the reinvestment option. For me, 4-weeks Bill, I get Monday night interest from Bank. Monday I get credit in Bank and Tuesday it gets picked up again. So if you give reinvestment option, Principal never comes into your account.

If your amounts are big, overnight interest makes a big diff. Specially when Monday is Holiday. Bank gives me credit on Friday itself so it gives 4 days of Interest.

likely because you actually receive the ”interest” when they charge your bank account for face value LESS the interest of the T-bill at the settlement???

VVV,

Yes, but then when you go to buy the new T-bill, you’re *also* buying it below par.

So you get your $1000 at maturity, but only $970, $980, $990 etc. of that get’s reinvested since that’s the market price of the new bill, and you can only buy them in $1000 (maturity) increments.

That’s another benefit of holding a T-bill ladder in one’s brokerage: you can toss your ‘leftovers’ into a MMF that probably gets it’s yield from the RRP.

There is an ETF marketed by SPDR that tracks the Bloomberg index of 1-3 month Treasury Bills and yields about 5.2% p.a. Ticker BIL in the US. It has admin. expenses of 0.14% per year, plus broker commissions for purchase or sale, but that might be worth the convenience of not having to repeatedly repurchase the bills yourself at maturity. In Europe the ETF is obtainable under ISIN IE00BJXRT698.

This is slightly riskier than holding the actual T-Bills, and you’re paying for that risk. No TY.

There was a graph in The Economist a little while back which showed how the Fed itself has a TERRIBLE record of forecasting its own rate-setting activity. Why would we expect “the markets” to be better at predicting an institution’s behaviour than those in charge of running it?

Even though this is basically a nonevent, from last week, it’s yet another background issue related to future policies and economic concerns that add risk to yields:

“The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance” relative to peers, said Fitch in a statement.”

Although the downgrade isn’t critical, it amplifies the concern people have with deficit and treasury issuance — a problem that is compounding and growing in sequential steps, that eventually has consequences.

Rating of US Gov debt does not really matter at all because US Govt would never default. They would print to ad infinitum to pay off debts/interest.

Looking at yields, came across a nice piece from November 2000. There was a lot of uncertainty then, as the dotcom bubble continued to mystify investors, some of whom, were chasing yields. It wasn’t a great time to look away and ignore cumulative layers of risk. I had been looking at yield curve inversion dynamics with unemployment rate.

“The report offered few indications that the tight labor market is easing, even as a host of other indicators shows the economy has begun to react to the Fed’s series of rate increases. The Fed raised rates six times between June 1999 and May 2000 but has held rates steady at three meetings since. It is expected to do so again when it next meets Nov. 15.

“It confirms that as we started the fourth quarter the economy continues to slow,” said Hugh Johnson, chief investment strategist with First Albany Corp. in Albany, N.Y. “At the same time that the economy is slowing, there is ongoing tightness in the labor markets and ongoing upward pressure on wages.”

Short-term money flows, proxy for R-gDp, rose going into 2024. Long-term money flows, proxy for inflation have steadily decelerated and could become negative in the 4th qtr.

07/1/2023 ,,,,,, -0.03 ,,,,,. 0.12

08/1/2023 ,,,,,, -0.04 ,,,,,. 0.10

09/1/2023 ,,,,,, -0.05 ,,,,,. 0.09

10/1/2023 ,,,,,, -0.03 ,,,,,. 0.07

11/1/2023 ,,,,,, -0.02 ,,,,,. 0.06

12/1/2023 ,,,,,, -0.01 ,,,,,. 0.05

01/1/2024 ,,,,,, -0.01 ,,,,,. 0.04

02/1/2024 ,,,,,, -0.01 ,,,,,. 0.04

03/1/2024 ,,,,,, 0.02 ,,,,,. 0.04

04/1/2024 ,,,,,, 0.05 ,,,,,. 0.06

05/1/2024 ,,,,,, 0.05 ,,,,,. 0.04

06/1/2024 ,,,,,, 0.06 ,,,,,. 0.04

07/1/2024 ,,,,,, 0.05 ,,,,,. 0.03

08/1/2024 ,,,,,, 0.05 ,,,,,. -0.01

09/1/2024 ,,,,,, 0.03 ,,,,,. 0.00

10/1/2024 ,,,,,, 0.04 ,,,,,. 0.01

11/1/2024 ,,,,,, 0.05 ,,,,,. 0.01

12/1/2024 ,,,,,, 0.02 ,,,,,. 0.01

I.e., no recession, but a decline in N-gDp

Powell is no different than incompetent doctor trying to use extreme measures that were not appropriate.

The Fed is lucky they did not get 50% inflation for a few months.

SOFR (the most important interest rate in the world noone is talking about) still at 5.3 something %.

And noone is talking about it.

Crazy.

Everyone is talking about it any time anyone talks about the Fed’s policy rates — there are five of them, see below — because SOFR is bracketed by the Fed’s policy rates, particularly its repo and reverse repo rates. The Fed’s policy rates go from 5.25% to 5.50%. The effective federal funds rate (EFFR), the target of one of the policy rates, is 5.33%.

Why? Because SOFR (Secured Overnight Financing Rate) is a measure of the cost of borrowing cash overnight collateralized by Treasury securities.

Here are the Fed’s 5 policy rates, right off the top of this article about the Fed’s last FOMC meeting:

https://wolfstreet.com/2024/06/12/fed-sees-only-1-rate-cut-in-2024-holds-rates-at-5-50-top-of-range-qt-continues-at-slower-pace-as-announced-in-may/

I’d argue SOFR is even more important than the FFR, given the death of the interbank market and transition to the secured standard.

Correct. The EFFR is essentially useless in modern finance. SOFR is everywhere, it’s written into all floating-rate loans, etc.

“Markets now pricing in 100% probability of a rate cut in September.” -CNBC headline

Also a 100% chance of Trump II term.

Also 100% chance of being 100% correct.

I just took out a 2nd mortgage to buy NVDA.

My daughters will 100% thank me later.

/s

Serious hyperbubble melt-up in progress. The FED sh!t the bed on their inflation fight. There will be hell to pay for years.

In a new research note on Monday, Goldman Sachs chief economist Jan Hatzius argued there’s “a solid rationale” for the Fed to begin cutting at its next meeting on July 31. “First, if the case for a cut is clear, why wait another seven weeks before delivering it,” Hatzius wrote. “Second, monthly inflation is volatile and there is always a risk of a temporary reacceleration, which could make a September cut awkward to explain. Starting in July would sidestep that risk.”

_________

Uhhh, if I’m reading this right, the logic is that there’s a significant chance of an inflation spike in September, so the Fed should cut in July while they still can? What could go wrong? Someone give this Hatzius fella a raise!

The same guy said in February 2022 that the Fed’s policy rate would reach a terminal rate of 2.75% by Q3 2023. The Fed did twice that and by July 2023.