Consumers are being lackadaisical again with their plastic.

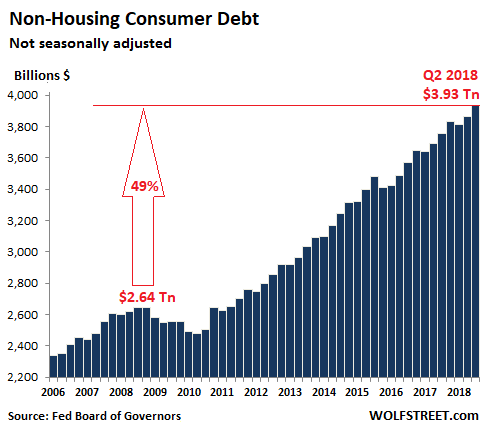

Consumer debt – or euphemistically, consumer “credit” – jumped 4.9% in the third quarter compared to the third quarter last year, or by $182 billion, to almost, but no cigar, $4 trillion, or more precisely $3.93 trillion (not seasonally adjusted), according to the Federal Reserve this afternoon. As befits the stalwart American consumers, it was the highest ever.

Consumer debt includes credit-card debt, auto loans, and student loans, but does not include mortgage-related debt:

The nearly $4 trillion in consumer debt is up 49% from the prior peak at the cusp of the Financial Crisis in Q2 2008 (not adjusted for inflation). Over the same period, nominal GDP (not adjusted for inflation) is up 39% — thus continuing the time-honored trend of debt rising faster than nominal GDP.

But a hot economy is helping out: While over the past 12 months, consumer debt jumped by 4.9%, nominal GDP jumped by 5.5%. A similar phenomenon also occurred in Q2. This is rather rare. The last time nominal GDP outgrew consumer credit, and the only time since the Great Recession, was in the three quarters from Q1 through Q3 2015.

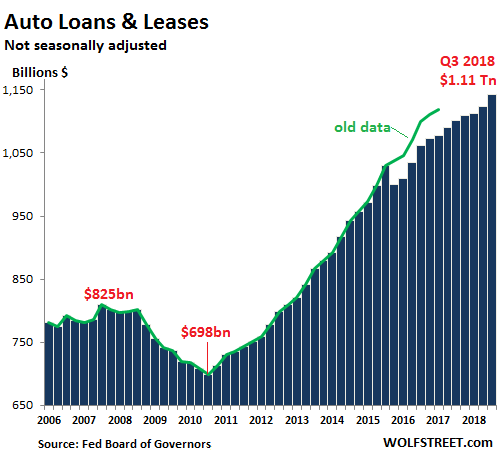

Auto loans and leases

Auto loans and leases for new and used vehicles in Q3 jumped by $41 billion from a year ago, or by 3.7%, to a record of $1.11 trillion. These loan balances are impacted mainly by these factors: prices of vehicles, mix of new and used, number of vehicles financed, the average loan-to-value ratio, and duration of loans originated in prior years.

The green line in the chart represents the old data before the adjustment in September 2017. These adjustments to consumer credit occur every five years, based on new Census survey data. Most of the adjustments affected auto-loan balances, reducing them by $38 billion retroactively to 2015. I included the green line to show that it wasn’t a forgotten collapse of the car business in Q3 2015 that did this.

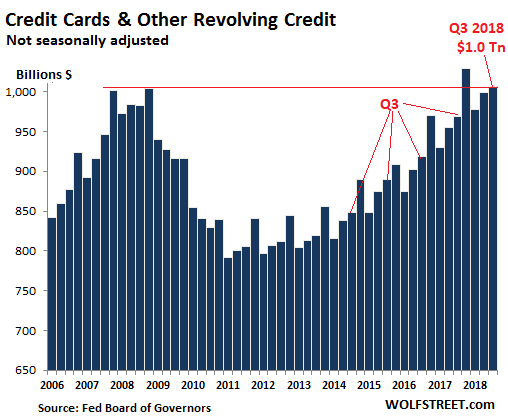

Revolving credit

Revolving credit is composed of credit card balances and other types of unsecured loans, such as a personal loan or an online loan. It has bedeviled economists and bankers for years that consumers aren’t going hog-wild borrowing on their credit cards. This is a problem for two reasons: Credit cards carry enormous interest rates, and bankers feel deprived if consumers don’t use them. And two, spending cranks up the economy, and if otherwise cash-strapped consumers would charge more on their credit cards to spend money they don’t have, Corporate America could show higher earnings.

So credit card debt and other revolving credit in Q3 rose 3.9% year-over-year to $1.0 trillion (not seasonally adjusted). Given that nominal GDP rose 5.5% over the same period, consumers clearly didn’t do their jobs with their credit cards. Compared to the prior peak a decade ago, credit card debt is about flat (Sheesh, makes economist, shakes head):

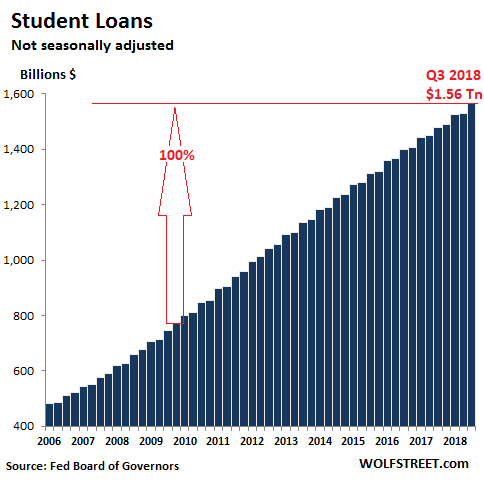

The student-loan GDP scam

Student loans in Q3 jumped by 5.6% year-over-year, or by $83 billion, to $1.56 trillion (not seasonally adjusted), another sad record:

Looking at the sharp and steady surge of student loan balances, you’d think that student enrollment is booming, as millions more Americans must be enrolling in college to lean what it takes to be successful in this economy. But no.

Turns out, the opposite is the case. Higher-education enrollment peaked in 2010 at 18.1 million and then declined 6.6% to 16.9 million by 2016, according to the latest data available from the National Center for Education Statistics. And yet, even while enrollment declined since 2010, student loan balances nearly doubled, from $800 billion to $1.56 trillion.

So the cause of the fiasco isn’t that there are too many Americans getting an education – I wish that were the problem. Instead a mix of factors stick out:

- Colleges are charging too damn much;

- Entire industries, such as consumer electronics and the student housing sector – a thriving subcategory of commercial real estate – are relentlessly sucking on those student loans;

- And occasionally, just a wee bit, the students themselves need to do some navel-gazing; These kids get this borrowed money, and it’s easy money to spend (iPhones, concert tickets, video games, nice housing rather than a dump, clothes…); later, it turns into hard money to pay back, and they’re left wondering how not to buckle under the debt.

And what do these factors of the student loarn fiasco have in common? Ha, this is what makes the American economy tick: They all add to debt-fueled GDP!

“It’s time to wait patiently as the air is slowly let out of this bizarre Ponzi balloon created by the venture capital industry,” says a Silicon Valley investor who has been accused of being outspoken before and, after this, will likely be so accused again. Read… Startup Boom a “Dangerous, High-Stakes Ponzi Scheme”: Silicon Valley Investor

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

GDP grew 5.5%

Consumer debt grew 4.9%

Of course “education” is a ripoff, but it doesn’t seem that growth in consumer debt is our most serious problem.

Federal debt grew 6.3%

Military spending. The biggest wealth transfer from taxpayers to war profiteers.

This is why US taxpayers get so little for how much they pay; they’re supporting a huge military.

Alex,

Consider that Military Spending is the only sector to offer REAL “bang for the buck”….

“Warriors” UGH!!

I noticed that this past weekend viewing NFL games I watched the side line crews (at least most of them) were wearing military “cammies” again….gotta spend that Pentagon public relations money! What a scam!!

Great graphs, Mr. Richter!

Military spending is not the biggest wealth transfer mechanism. The defense budget for 2018 is less than $700B. Meanwhile:

— Rents have tripled since 2007, which is an additional $600B per year extracted from households.

— Healthcare expenditures are up 50% since 2007, an additional $800B per year.

At the same time, since 2003 government policies have resulted in about $1T per year being diverted from earned income to unearned income.

Adding all of these up, households have suffered a $2.4T per year hit to income net of healthcare and rent. That is why the middle class is angry. It is up to our politicians to ensure they continue to fight amongst themselves over meaningless issues rather than the real issues.

So the defense dept budget costs more than rent? Wow… Should be the other way around, seems like.

FWIW, my property taxes are my single largest monthly expense.

Where have rents tripled since 2007?

“Where have rents tripled since 2007?”

My neighbor in Boise rents out her house. She got $750 in 2007. Now it’s about $2200.

Please clarify your remark- Rents have tripled since 2007, which is an additional $600B per year extracted from households.

Have total rents paid increased by $600 billion?

Have same/similar property rents increased by 300% ?

Citations would be helpful and make your point believable. Anecdotes do not count.

Military spending is nearly $900B for 2019.

https://www.thebalance.com/u-s-military-budget-components-challenges-growth-3306320

My own list would include (off the top of my head):

Pentagon, CIA, FBI, even militarized police departments

Black-box spending

Recruitment

Veteran benefits

Homeland inSecurity

TSA

Academic R&D for military applications

Cleaning up after the military’s MASSIVE pollution driving global warming & chronic diseases. All of the man-hours lost to bureaucracy like the TSA. The effects of destabilizing the world (like harboring refugees, and the bureaucracy entailed). Political buyoffs and negotiations necessitated by our worldwide dislike? The cost of delayed action on infrastructure? Lost opportunity cost of investing $900B into empire-building instead of the ENDLESS list of technologies, human welfare projects, education, etc that we would be investing in if we weren’t led by myopic troglodytes?

Do you REALLY trust an accountant hired by someone else, explaining how your money is spent?

@Dale-

>Military spending is not the biggest wealth

>transfer mechanism.

True.

A cursory glance at the federal budget pie chart (Wikipedia) indicates that entitlement spending consumes roughly 2/3 of the budget.

With all due respect IdahoPotato, you cannot make the general claim that “rents have tripled in three years” just because your neighbor is charging 3x for rent.

In a general sense, while rents have increased since ‘07, they have certainly not gone up 300%.

Economist Steve Keen believes that consumer debt is the real bad boy of debts. Worse than corporate and much worse than government.

The federal government can just keep increasing its debt as long as there are buyers or the Federal Reserve agrees to absorb it. States, counties and cities are in a different category. As far as I understand their problem, they only have two choices. Cut services or raise taxes. Teachers are already unhappy about the lack of funding.

As for the consumer, they pay until they can’t and then they default. Pretty much the same with corporate debt.

All of this would look more reasonable if the incomes had been more even. What we have with consumer debts, used to fund the corporations by buying their production with borrowed money. With income inequity IMO this is going to cause major issues, especially with rising interest rates. Consumer’s problems will become the problems of the corporations and then things will get pretty interesting.

You just can’t have this kind of debt growth with out income growth to support it.

As Wolf’s figures show though, consumer debt actually isn’t rising very much in relation to the economy, at least in the US.

The private debt bubble this time around is in corporates much more than in the consumer segment.

GDP = private consumption + gross investment + government spending + (exports − imports).

Does all that consumer debt fall into the private consumption category of the US GDP calculations?

The debt doesn’t show up in GDP. But the spending funded by that debt shows up in “private consumption.”

Right; and why the Fed Govt deficit is so scary. Neither party does anything about this.

Biggest expense changes in past ~10+ years:

1. medical care

2. college cost increases

3. rent/mortgage cost increases

4. smartphones+monthly service have used up a lot of discretionary income (really)

These are the causes of 1. credit overloads and 2. retail problems

Just in time for a projected trillion dollar holiday spendfest, the banksters strike again…..A major retailer credit card my wife uses infrequently, just raised their monthly revolving interest from 26% to 29% because, “We are charging our new customers 29% so we will set your rate at this same level.”

Taleb says the world is more fragile today than in 2007:

When you start borrowing to pay interest on existing debt, you have entered the Ponzi phase.

The Fed has turned the USA into Idiocracy. Uhhh, it’s got electrolytes. That’s what plants crave.

Over the same period, nominal GDP is up 39%

How the heck can GDP rise by 39% and my income at 0%?

Also in regards to colleges. I watched a video by Heather MacDonald where she claims that much of the increases in tuition costs are mainly due to administrative positions that have very little to do with educating students but ensuring that all students have the “same outcome”

According to that video UCLA has a “Office of Equity, Diversity and Inclusion” and one of the staff members is making over $300K a year……..let that sink in. Check out the website, sure seems like a lot of make work positions with enormous pay packages.

https://equity.ucla.edu/

GDP went up 39% and your income rose 0%. Where did all that money go? It went to the top 5%.

It’s a party, and you weren’t invited.

Education has become a thoroughly unethical scam, whereby a great many drones feed off the debt incurred by unwitting kids.

Massive -and utterly unjustified – building projects, too.

The Education Industrial Complex. You also have the Medical Industrial Complex, the Agricultural Industrial Complex, as well as the traditional Military Industrial Complex. Make your own list and leave room at the bottom.

Finance has proven itself able to corrupt just about anything for the piratically minded. Financial innovation is the world’s top growth industry and has evolved its own arts and sciences and well-established techniques.

Assuming mad money gets tight, I’m sure there’s room for cuts on infrastructure spending to provide additional upside or at least sustain the private money pumps.

It’s an Animal House world.

@interesting-

>How the heck can GDP rise by 39% and my income at 0%?

Now that’s the right question!

Typo Here: “Compared to the prior peak a decade ago, credit card debt is about flat (Sheesh, makes economist, shakes head):”

Feel free to delete this after fixing…

I’m not seeing the typo at the moment. Help me out…

Apparently, you have made an economist and shaken it’s head. Excellent work, Dr. Frankenstein.

Not the most serious typo in the world.

Oh I see what you mean. But…

“made” is also used for “said.” According to my trusty digital Random House Webster’s Unabridged Dictionary, definition #25: “to deliver, utter, or put forth”

LOL

It would be very valuable to know what the weighted-average interest rate is on the various types of consumer debt. Rising rates will impact credit card loans first but will also hit the other types as loans are rolled over.

If the debt serfs are making larger monthly tithes to their creditors, that makes it harder to afford further borrowing.

If rates rise enough, the debtors will be paying so much more to the creditors that they will have to reduce non-interest borrowing/spending altogether. That probably implies a recession?

Auto loans, new, average: 5% for a 60-month loan. Loans can go up to 84 months, and they have higher rates.

Credit cards, average 14.5%.

(Fed Board of Governors, via St. Louis Fed)

Mortgage rates, average: 5.15% for 30-year fixed, 20% down, conforming (MBA)

Yes, higher rates limit what consumers can spend on other things. But as long as they can borrow more, they’re OK, and we’re OK :-]

Credit cards that are being assessed interest went from 14.99% in Q3/17 to 16.46% in Q3/18. That is basically 1.5% in one year. My guess is some of the wealthier card holders are starting to choke on those rates and are paying down some of the principal. Hence the lower rate of increase in revolving debt. I think once that phenomena is over we will see the rate of revolving debt rise increase as those unable to pay down get stuck in the higher rate/more debt viscous cycle.

I don’t think wealthy card holders carry a balance. If they do, they are not wealthy.

Right. I suspect he meant “high-income” card-holders, people with the cash flow to make monthly payments on debt, but not the wealth (or common sense?) to avoid taking on the debt in the first place.

There’s a common misperception, fed by the media and politicians, that “high income” equals “wealthy”. The reality is quite different and is very well described in the excellent book “The Millionaire Next Door”.

I did not say wealthy, I said “wealthier”. Meaning they can if they have to. Some are probably to lazy to take care of it, but given the added cost they may be more attentive.

And how muxh is this if you asjust by inflation?

Hi Wolf, has there ever been a calculation of the detrimental GDP effect of the huge student loan debt. IE if somebody is paying off 600 dollars each month on their loan debt rather than spending that in the economy?

It nets out: The 0.001% will be spending those 600 bucks from the poor student on a nice cigar, which then goes into to BNP /snark.

Where is the cigar made, by those students?

To be fair, much of the student loan debt is probably being paid out to pension beneficiaries and 401K/IRA retirees. Some of them are the ultra-rich but many are just grandmas and grandpas trying not to be a burden directly on their own children. Someone’s student loan interest could be paying for a retiree’s groceries and dialysis.

In terms of GDP, the question is whether the recipients of the student loan interest have a higher propensity to spend than those paying the interest? Ditto for credit card interest, mortgage interest etc.?

I’m fairly certain the answer is “no” – the debtors almost by definition spend everything (and then some), and that’s how they became debtors. Whereas the creditors have demonstrated a tendency to save, because that’s how they became creditors.

But it’s mathematically impossible to have a modern economy with a large fraction of elderly retired people, without having a large amount of income transfer going on. When the retirees demand more income than is available from income-generating equity assets, generational-transfer taxes and subsidies, they come up with debt traps as well.

@Wisdom Seeker-

>Someone’s student loan interest could be paying

>for a retiree’s groceries and dialysis.

FWIW, dialysis is incredibly expensive, and most of these patients haven’t worked long enough to reach retirement age.

BAD Retirees,After They built this Country without Entitlements from the Government and parents,lets get rid of them.

Then give all the funds to the entitled parasites.

Household formation has been dropping like a rock, although it has turned recently. This debt prevents people from getting a mortgage, which partially explains why mortgage debt is slightly lower than 2008. If you aren’t buying houses, you doing all the other things that are associated with home owership.

Meanwhile, some very inefficient colleges are being propped up and many have built mini-kingdoms. Visit your alma mater lately?

Just to clarify household formation comment – younger people impacted most.

Yes, this has been pointed out as a problem for big-ticket items, like auto sales and the housing market (the housing market is constantly whining about it). But I have not seen any solid estimates to what extent in the overall economy the need to service student loans crimps spending on other things. But this effect is there. All consumer debt just moves future spending into the presence. Student loans fall into that category too.

Grandchildren; live in Silicon V.; one works in computer sales approx income $80,000; wife passed Vet boards and is lucky to have landed (after 8 years of college) a decent position at approx $120,000 year. Medical College debt is a $350,000 nut. So how can they “spend” to stimulate the economy (home, children, car(s) etc) except to survive?? Medium to long term they want to flee SV as soon as possible and move to more rural area. This couple are very responsible and very hard working. With $200,000 income and $2-3 thousand dollars monthly payments just for tuition they are just barely getting by. And, yes many “institutions of higher learning” have become fiefdoms in themselves no longer really dedicated to free/open education. But that’s another story.

What are the monthly payments on $1.56 Trillion. My guess is, that is pretty close to the spending lost elsewhere.

Here’s a question: do loan payments figure into GDP?

No, they don’t. But indirectly they do to some extent: when loan payments force consumers to spend less on other items.

No.

Payments to credit accounts are neither Durable Goods, nor Non-Durable Goods, nor Services, the three elements comprising the Personal Consumption Expenditures component of GDP.

The omission of several important categories of economic activity severely compromises the value of economics as a ‘science’. Properly, a science is recognized as a science because it has a high level of both explanatory and predictive value.

Take the simple example of chemistry, which tells you what stuff is, often in detail sufficient to allow you to predict what will happen when you mix this stuff with that stuff. Or celestial mechanics, which explains the motion of planets and stars and can tell you where they’ll be in the future with great accuracy.

Economics does a very poor job of explaining the nature of economic activity and of predicting the outcomes of economic activity or of changes to economic systems. This is why the characterization of economics as a ‘science’ is so often rejected, even by economists, if they are honest. The people who run nakedcapitalism dot com strongly reject economics as a science.

Because they are not ‘sciences’, economics and finance lend themselves to extremely profitable abuse. And that is why mainstream economics and finance may never be reformed and advanced to where they would have adequate explanatory and predictive value. Where’s the profit in that?

The honest economist is necessarily a cynic, although cynics are not always economists, much less honest economists.

Where are you unamused? Read this excellent summary of consumer credit and remind me how my comment a week ago “has been debunked”. Although admittedly, when I said that consumers were being more prudent relative to past periods, was not thinking about student loans. 90%+ of $ being federal student loans.

Guessing that student loans will feature big in 2020. $1.5 trillion is a very big and shiny object to dangle …and nobody can allow the correct image to form in anyone’s mind – a very big ball and chain.

So while student debt provides some juice to gdp, a lot goes to building college kingdoms while dragging many other sectors of the economy.

At least partially explains why total mortgage debt is slightly lower than it was a decade ago.

->Read this excellent summary of consumer credit and remind me how my comment a week ago “has been debunked”.

No need. This article does it for me.

Read what it actually says, starting with “Consumers are being lackadaisical again with their plastic” and note how it flatly contradicts you.

->Re-read the comments in the piece titled “There’s Nothing in this GDP Report to Slow the Fed’s Rate Hikes”

You want to dance, do you? Let’s look at your comment, then.

You: “Consumers and their individual/personal debt management is also quite solid”

WR: “Consumers are being lackadaisical again with their plastic.”

WR backs up his statements. You don’t. Because you can’t.

@unamused, dude, I know you are not this obtuse – give up the dancing, I mean deception. You are exposed big boy.

WR: Consumers are being lackadaisical again with their plastic.

Yep, and he goes on to write

“So credit card debt and other revolving credit in Q3 rose 3.9% year-over-year to $1.0 trillion (not seasonally adjusted). Given that nominal GDP rose 5.5% over the same period, consumers clearly didn’t do their jobs with their credit cards. Compared to the prior peak a decade ago, credit card debt is about flat (Sheesh, makes economist, shakes head):”

Again, re-read the comments from 10/26!

At some point, maybe you will get sick and tired and unamused of being sick and tired and amusing.

This

->Consumers and their individual/personal debt management is also quite solid

Contradicts these

->We just got back to the consumer debt levels of a decade ago and that isn’t even inflation adjusted.

-> In the past decade, we added roughly $1 trillion in student loan debt, approximately triple

Now walk it back for us, would you?

->Although admittedly, when I said that consumers were being more prudent relative to past periods, was not thinking about student loans. 90%+ of $ being federal student loans.

Okay, “was not thinking”. No argument there.

Thanks for clearing that up for us.

I acquiesce to what David Walker, former U.S. Comptroller General, and Stephen Roach, former chairman of Morgan Stanley Asia, have often said (paraphrased). ‘None of this S**T is sustainable long-term’.

Many nights I wake up in a cold sweat after this same nightmare. That a debt jubilee is announced and all those $70k pickup trucks people are financing are suddenly free and clear. While I am stuck with my 10 year old paid for beater.

HAHA! I started thinking that in 2010, with all of the “help for upside-down” homeowners” (ie, cash-transfer to bad lenders). But we have to bail out the idiots. They’re the only ones oblivious enough and shameless enough to drive $70k trucks. Plus, otherwise I’ll be dead before my student loans are gone. Guilty idiot :(

Also, wasn’t the recent “credit bump” everyone got basically a tiny jubilee? “Here you go! Keep spending, assholes!”

“While I am stuck with my 10 year old paid for beater.”

You still win. They’re still losing more in annual depreciation on their $70k pick-em-ups than your truck is worth. That depreciation money is still in your pocket.

Last comment – another way to look at this data. In the past decade, we added roughly $1 trillion in student loan debt, approximately triple, 3x, on all other credit categories combined. Student debt will soon be 1/2 of all consumer debt.

Typo: …must be enrolling in college to lean* what it takes to be successful in this economy.

learn*?

Thanks! Fixed :-]

That giant pile of debt is why the country’s largest homebuilder just posted tepid numbers even with LOWER average prices. You can inflate asset prices by suppressing interest rates with a massive liquidity injection, but flipping the switch and raising rates way too late in the cycle has consequences…

The reason for the tardiness is because the FED’s employers call the shots and that’s what they wanted, to create a bubble, for no crisis should be wasted and the larger the crisis (amplitude of pendulum, or what have you) the more opportunity.

No need to be so naive.

And now comes Xmas season, so the plastic will be worn thin. January’s credit card bill may be a big shock, with another year of interest rate hikes behind it. China, Europe, the USA and everyone else-everyone and every thing is maxed out. And yet up and up the stock market goes. The Fed is trying to deflate the bubble with glacial interest rate hikes, but Mr Market wants to get bigger and bigger, everywhere and in everything. I just don’t know what will finally bring this to an end-an old style crash or a Japan style mummification, but one would think it must be close.

->WR: “The debt doesn’t show up in GDP.”

The macroeconomic equivalent of listing Gross Revenue, but not Cost of Goods and Services Sold, or assets, but not liabilities.

It makes for one extremely misleading economic statistic. Other, more derogatory adjectives would also be appropriate.

“Externalities, externalities!!!” “Nothing to see here!!!” (Sarc)

Students older then me knew what credit card debt was, because they used them to get buy. I knew a guy who literally paid for a degree with a credit card… he is probably 40 now…

By my generation (born 1985) no one in college was using a credit card to survive. Why? Student loans were easy to get and you could pay for rent and living with those. And everyone agreed this was more or less normal…

Student loans basically fund early adulthood and everything has been marked up to accommodate everyone having tens of thousands of dollars in loan money :/.

I was fortunate to live at home while going to school and take out most of my loans while they were still in the 2% range. And then pay them off quickly. But many were not so lucky or properly steered away from borrowing too much.

My daughter once took out a student loan, misread the fine print, and used a portion of it to take her future husband to Mexico that Christmas. When she ran out of funds before the end of the school year, (we had a formula…Dad pays for 1/3, she worked and paid for 1/3, and a student loan for 1/3…community college/Uni and low expenses)…this Dad met her at a Starbucks (neutral location) and made her sign a loan agreement to make restitution at the going rate. It was about $125 per month if I remember correctly; for two years. I made her give me post-dated cheques. In hindsight it is funny but I was choked at the time. It was a great lesson for her.

Fast forward to today: She has been married to the (mexican vacation compadre) fellow for 15 years and I could not imagine a finer son-in-law. We often get together and talk hockey and woodworking-shop-man-talk stuff :-) They own a modest home which will be paid off before they are 40. They both have decent jobs with excellent job security. She has never borrowed money since that episode.

My ex (her mother) thought I was a rigid jerk about it because I formalized it in writing but I noticed at the time she didn’t offer to pay any portion of her default and she never helped out with her education costs, either. Thinking about it, she didn’t help with the house down payment, either! hmmmm. It was a good lesson for my daughter and hilarious 15 years later.

Student loans are still easy to get. The problem might actually be that they are TOO EASY to get now.

The difference between then and now is that going to college has become much more expenseive, with tuition and fees inflation exceeding even medical inflation.

In a midlife return to a top public university in California graduating in 1994, my total annual tuition & fees averaged about $4,000. Today, it’s approaching $15,000, 3.75 x my cost in 24 years, a 275% net jump.

In the 1960’s and earlier years, tuition & fees at the same school were zero. No wonder student loans are exploding.

so what you are saying is this is still supply side economics?

Supply side >> demand side. No wonder the boat keeps capsizing.

I worked my way through college, graduating with very little student debt. Indeed, it took longer to complete my degree, but I also gained valuable work experience along the way. For some reason, students today seem to believe that going to college is a vocation and a full-time endeavor, racking up 10’s of thousands of dollars of debt in pursuit of a liberal arts degree. Perhaps this is why colleges do not teach personal finance?

A lot of this data is interesting, but I’m curious about the story here.

What I would be curious about if such data exist would include:

1. What was the student loan debt percentage like as a function of time going back to 1980. Then segregate between the time frames of the Gen Xers and the Millennials.

2. Look at how college tuition on average (and perhaps segregated between for profit, and non-profit schools) has increased over time between 1980 and today. I know for example, my alma mater at CMU had pricing go from $20K to $25K in tuition to over $50K in the last twenty years.

3. What was credit card usage on an annual basis for households as a function of time and how that has fluctuated between 1980 and today?

I know this would be only on the demand side, but my guess is that there is a big issue with financial education for the kids. I would think that in general such education are not well done before, but I wonder if it has gotten much worse with time. Certainly, the rise of the internet, on demand satisfaction, and the ongoing move to disintermediate real cash from the economy has helped to fuel this problem. After all, one click on Amazon, and it’s not real money. It’s more like a video game.

But I am very curious about what it would look like if you break down the supply and demand side of those loans, and get into behaviors

Financial education for the kids as you say could be taught in a single quarter in tenth grade.

My first year at the U of MN was 1980/1981. An in-state resident’s tuition was an affordable $383.50 a trimester for a grand total of $1,150.50.

I feel sympathy for today’s students that rack up debt on their way to earning a degree.

The cost of a student loan to qualified US citizens should be tied to the Fed funds rate IMO.

Inflation is a repricing mechanism. Repricing by inflation requires border control (to increase low skilled wages), automation (to increase productivity), tariffs (to capture gains), and a military buildup (to protect against angry mercantile governments). A military buildup also makes inflation easy. Worked 1953-1968.

“GDP is a terrible measure of the economy. It measures what money gets spent on and invested in. It’s a measurement of flow. Among other shortcomings, it doesn’t include the source of money – whether it’s earned money or borrowed money. This leads to the distortion that piling on debt is somehow good for the economy, when in reality it’s only good for GDP but will act as a drag on the economy down the road”.

This from a wise man.

In Canada, house prices are sliding; with estimates that this will continue for two more years!

Wages have stagnated for some 40+ years, and too often gone down over that time. The ‘gig economy’ cannot allow real human beings to be part of “the way it used to be” (whenever that was!). Our corporate masters have abandoned us to serfdom while they reap the benefits of $3.00 per hour labour versus those who did the work for $20+ per hour – those ripoff union types you know!

How long can this piling of debt continue, but too, who will own the world when it blows? Who will the serfs serve then?

I experienced an issue with delivery of an item I purchased through ebay; at first they denied my claim thus I had to call them.

I discovered the human portion of this particular claims department is outside the country.

You talked to a human being ?!? You don’t know how lucky you are. I have found the foreign call center reps are usually willing to repeat what they said, speak slowly, and so on.

I have no luck at all with the recorded voices asking me to punch in account number, Social Security number, nature of problem, etc. etc.. They often seem to be programmed to believe that there is no problem, and they cut me off.

The effort to get “real human beings”, and especially domestic ones, out of the work force, continues.

Aren’t most credit cards variable rate? And other consumer debt, I imagine. This is definitely worth some discussion, is it not?

Also, the Mortgage Delinquency Rate rose in Q3. I hear that’s not counted as consumer debt, though, so we shouldn’t talk about it ;)

Credit cards are variable rate. Auto loans and student loans are fixed rate.

Personally, I believe we should encourage thrift and an old school approach of purchasing items one can afford or learning to do without. Not that it covers the underlying issues the article covers.

That is pinko commie anti-american propaganda. You don’t care about the ponzi – I mean GDP – at all, do you? You’ve got to spend more so that the major corporations you’ve invested in can privatize, monopolize and capitalize all the things, so that your stocks go up so you can afford anti-depression medication and, when your useful consumer years are over, a decent enbalming and burial! Don’t be short-sighted!

Your top chart (non-housing CD) represents an average annual inflation rate of about 3.8% and a corresponding USD half life of 18 years over the 10 year period.

A coworker, age about 74, graduated from Butler Univ. in the mid sixties. I asked him what he paid for tuition back then, and he remembered without hesitating, it was about $365/semester. At the time, he thought that was expensive. My dad went to Butler in the late forties prior to dental school and he paid $50/semester for tuition. I remember him telling me at the time (this would have been probably in the eighties) that he thought that was expensive. Currently the tuition runs about $20,000/semester. It’s a very long term bubble.

TYPO: “student loan balances nearly doubled, from $800 billion to $1.56 billion.” should read $1.56 TRILLION, if my math is correct (which does happen occasionally).

Ha, yes your math is correct. Thanks.

Those dang trillions fly by so fast they’re hard to see sometimes :-]

Perhaps important to note that undergraduate enrollments fell most among learners age 25 and above during the time frames referenced while age 25 and below enrollments have remained relatively stable since 2010. More student debt is being incurred by people at a younger age.

1st time poster. In short I have a 10th grade education & a GED. Took some community college & eventually quit due to working so much. I just retired @ 61, living off savings until 62. I ended my career making 75K a year as a production planner. I was shocked that I was able to make that much money compared to some out there including college kids (& older). To me it’s quite simple. Whether you make 75K or 175K if you die before retiring, you lost out on life. I now get to see the worker bees drive to a job they hate, while I enjoy time home with my wife, debt free. It’s not that hard to live within your means if you actually “think” about it & have a plan.

It is not just kids taking on debt I read a fed report about people over 50 taking out record levels of debt to fund the family welfare system. They have better credit.