The supply of rental units on the market is ballooning.

“The trend in rental prices this month was mixed”: so started out the Zumper October Rent Report for the month of September.

“Mixed” is not exactly a bullish term – not when it includes the two most expensive housing markets in the US, San Francisco and New York, where rents have fallen, in some cases sharply, on a year-over-year basis, as the supply of new apartments already on the market and coming on the market is enormous.

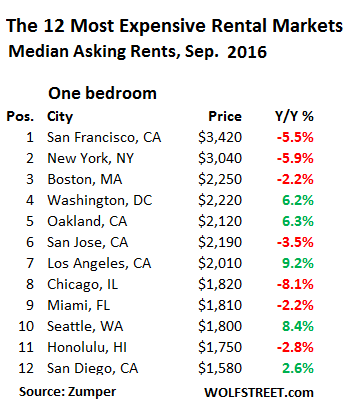

In San Francisco, the median asking rent for a one-bedroom apartment fell 5.5% year-over-year to $3,420, according to Zumper, which analyzes rental data from over 1 million active rental listings in multi-family buildings and does not include single-family houses on the rental market. For a two-bedroom, it fell 4.4% year-over-year to $4,780.

It was the third month in a row of year-over-year declines. The last time the market was negative year-over-year was in April 2010. Since then, rents have soared at astonishing rates. Hence the San Francisco term for it: “Housing Crisis.” It’s when even teachers can’t afford to live in the city – unless they’ve been in a rent-controlled apartment for years and don’t get evicted.

OK, $4,780 a month is still a huge amount for a two-bedroom. Median asking rents means 50% are higher, 50% lower. But not many people, even in San Francisco, can afford those kinds of rents.

To put that in perspective, that median two-bedroom costs the tenant $57,360 a year, which is about the median household income in the US. So there’s a little bit of an affordability problem, even in San Francisco, and hence a demand problem.

Now incentives are piling up, such as one month free rent – previously a rare occurrence in San Francisco. These incentives are not included in asking rents. The rent decline for the median two-bedroom amounts to $2,523 a year. Together with one month free rent, the actual decline in asking rent for the first year is $7,303, or about 12%! A big plunge for both landlord and tenant. But it’s just the beginning.

What a difference! Here is what happened a year ago, according Zumper’s October 2015 rent report:

High priced cities are getting more expensive; in fact, the top four cities on our list all saw rent increases in the near term. San Francisco widened its gap between NYC…. September again marked a new record high for the city, now with a median one bedroom of $3,620 and two bedroom of $5,000. Rents in the city are up 13.1% in the past year.

Note the double-digit year-over-year rent increase. At the time, there were zero incentives.

The supply of rental units on the market is ballooning.

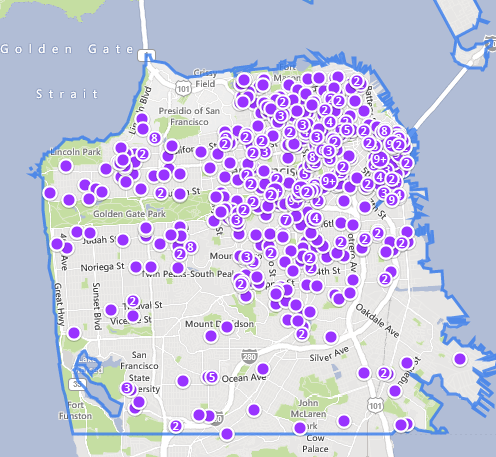

On Zillow, there are 1,237 apartments listed as available for rent in San Francisco, up 7.7% from a month ago (1,149 units) when I last wrote about it. The Zillow image below only shows 500 units. If all available units were shown, over one-third of San Francisco would be solid purple. Note the dots that say “9+.” They represent larger buildings, some of them with dozens of vacant rental units. You can see these towers South of Market and in some other pockets:

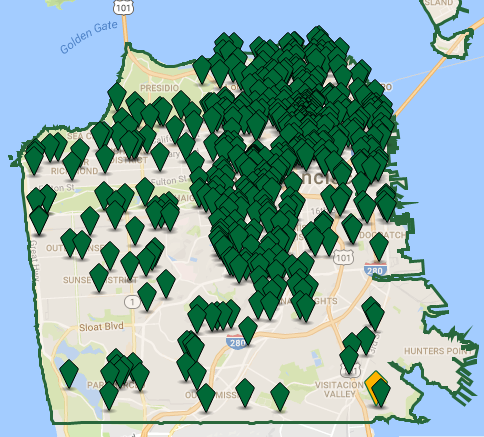

Apartments.com lists 3,534 apartments for rent, up 14% from the 3,094 units a month ago, and up 54% from the 2,302 apartments it listed in June:

The densest clusters of units in both charts are in areas where the high-rise construction boom is most obvious. It’s not just apartments. Condos purchased by investors play a role too. The construction boom created numerous condo towers. Investors who bought the preconstruction units but have no intention of living there are trying to sell them, which is getting difficult, so they’re showing up on the rental market.

Most of these new units are higher end. But as landlords are cutting rents and piling on incentives, they’re pressuring the levels below, and then those levels have to cut rents and offer incentives to compete with then nicer new units, and over times, these pressures cascade all the way down.

New York City is facing similar dynamics: high rents that are crimping demand and a construction boom that is adding an enormous amount of supply.

Median asking rents fell 5.9% year-over-year to $3,040 for a one-bedroom apartment and 7.2% to 3,470 for a two-bedroom apartment, not including incentives.

The median asking rent for a two-bedroom, at $41,640 a year, is now $3,231 lower than it was a year ago. With the additional incentive of one-month free rent, the 12-month cost for the tenant (and revenue for the landlord) plunged by $6,700, or 15%!!

A sea change from a year ago. Zumper’s October 2015 rent report on New York City:

One bedroom asking prices hit $3,230 for a one bedroom and $3,740 for a two bedroom. Prices across the 5 boroughs are up 9.5% in the year.

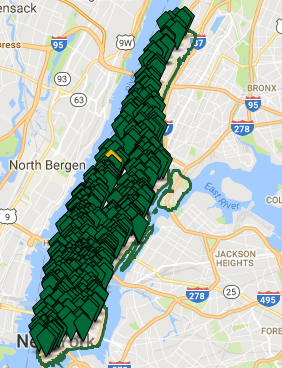

For the five boroughs, Zillow lists 25,432 apartments available for rent. Appartments.com lists 16,717 just in Manhattan:

For landlords that are putting new units on the market in these two cities, the slide in rents is very inconvenient. Capitalization rates have become razor thin in recent years. The process of declining rents and increasing incentives, as new supply surges for years to come, screws up their entire math.

In terms of commercial real estate, this will pressure prices. Given the high leverage, there will be defaults, and creditors will end up with some of those buildings.

But renters, after having their lifeblood squeezed out of them over the past years, will be able to breathe a sigh of relief. Neither of these two markets will ever be cheap, but rents are likely to become less ludicrous. Prospective renters have an opportunity to become tough negotiators, now that they can walk away and shop elsewhere.

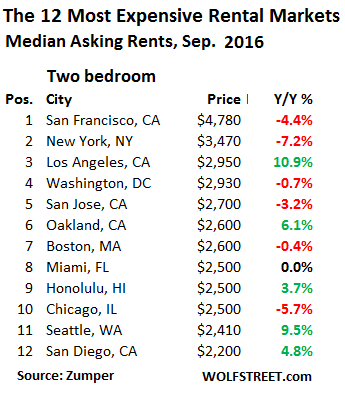

Of the 12 most expensive large rental markets in the US, median rents for one-bedroom apartments fell in 7 cities year-over-year. Suddenly there’s a lot of red on what had been solidly green for the past six years:

In the two-bedroom segment, similar trends are playing out, with rents in six cities of the top 12 in the red and one unchanged:

Note in both charts the declines in Chicago and the surges in Los Angeles and Seattle – hence the infamous “mixed” label.

The tables don’t include smaller rental markets with super-high rents such as Palo Alto, in Silicon Valley, were the median rent is an utterly insane $5,800.

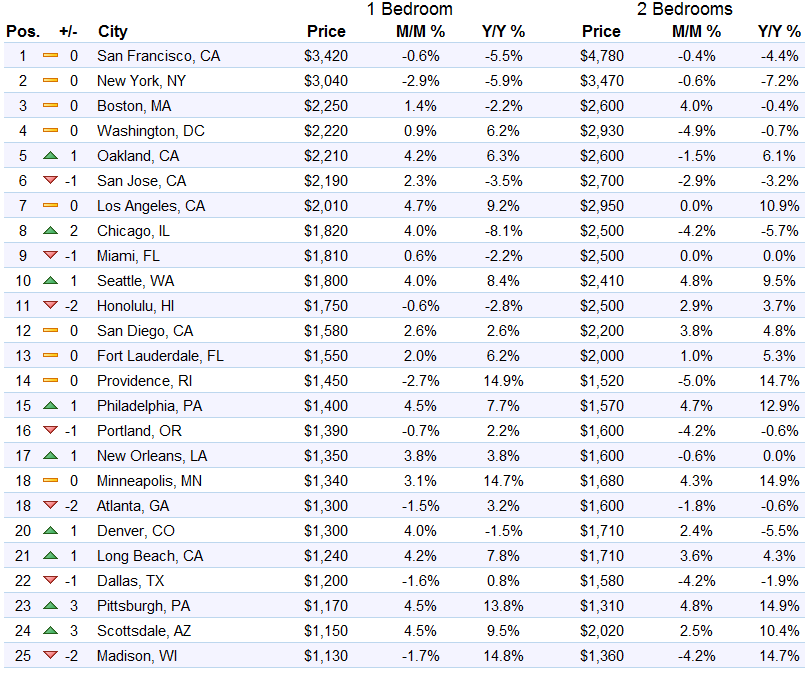

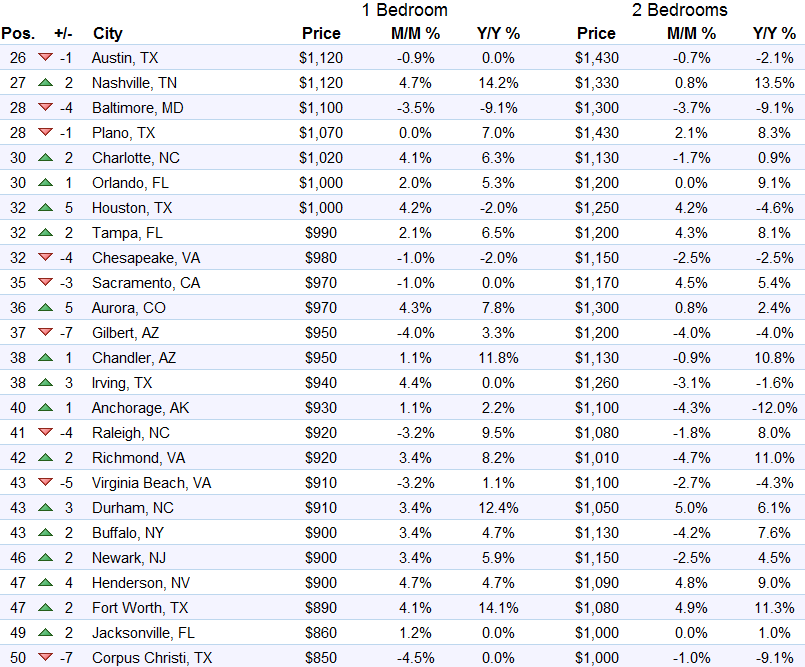

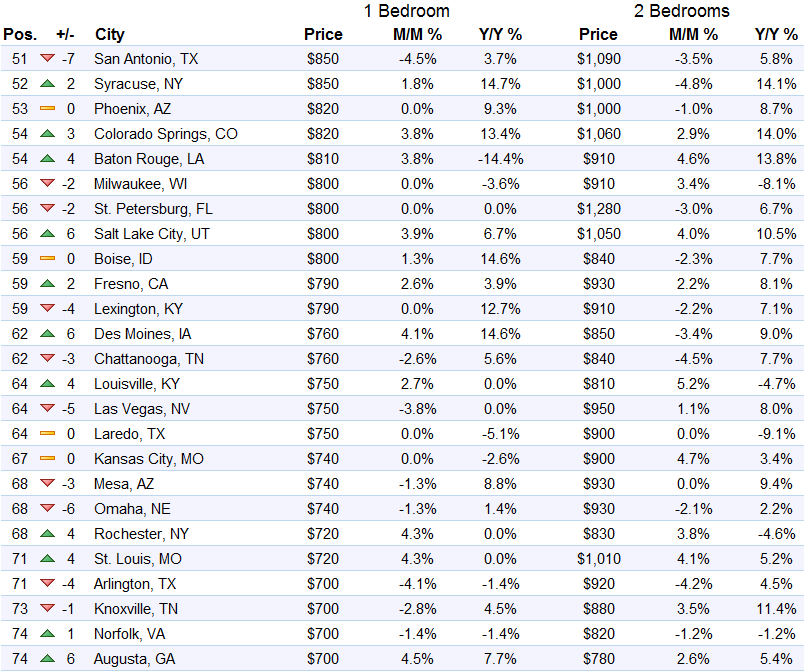

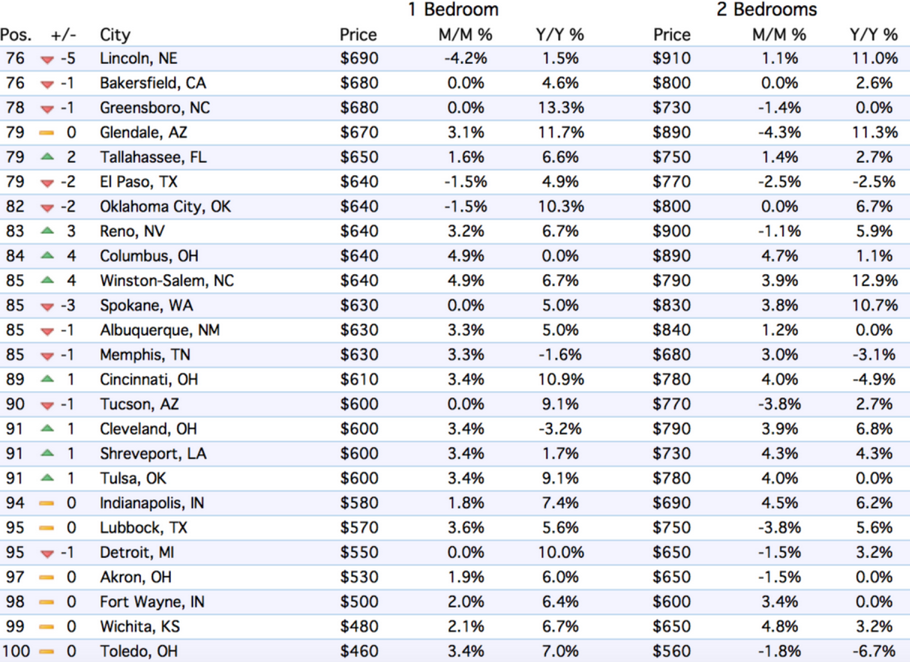

Overall in the top 100 rental markets in the US, median asking rents for one-bedroom apartments rose 2.3% year over year to $1,136. For two-bedrooms it rose 3.0%, to $1,350.

Below are the top 100 markets, in order of the amount of rent for one-bedroom apartments. Check out your city to see what the trends in September were (tables by Zumper, click tables to enlarge):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I live in Walnut Creek CA which is about 35 miles east of San Francisco. I just rented a one bedroom apartment for $2,300 per month (6 month lease). This was at the low end of the many apartments that I shopped. Many were in the upper $2,000s. However, as WOLF has observed there are hundreds of new apartment under construction in Walnut Creek that will undoubtedly weigh on the market in the near future. Builders are assuming there is an unlimited supply of renters at these very high prices.

I have been looking into the Seattle market for the last month or so because I’m considering a move there. (I grew up in the area but have been living in the Bay Area for 11 years.)

To your point about builders assuming there is an unlimited supply of renters: in Seattle, there are a ton of “micro studios” on the market. These places live up to their name: they are about 300 square feet total, so barely enough room for a full bed, desk, desk chair, etc. They don’t have full kitchens, just microwaves, tiny counters, and in some cases dishwashers. No ovens, but a few have a burner or two, further reducing the already minuscule counter space. They’re listed for between $950 and $1050 or so. Yet, in adjacent neighborhoods, normal-size studios, with ovens (imagine that!) and room for not just a bed but also a sofa, media center, etc., are listed for $1100 to $1200.

To me, it seems the only people who would actually rent a micro-studio are 1) determined to live in very specific neighborhoods, 2) determined to live on their own rather than find a roommate, and 3) extremely price sensitive. I can understand that in the University district, there are probably a fair number of people in this situation. After all, I could see the micro studio having more appeal than a dorm room. But outside of that area, everyone who doesn’t fit all three of these criteria is just going to look elsewhere.

I’m curious to see what happens with these places. For now, Seattle’s rents are still on the rise, but people have their limits, both in terms of what they can pay and in terms of where they’re willing to live. Certainly, the easiest thing for the building owners to do will be to reduce the price. But there seem to be so many of these micro studios that I think, eventually, something else is going to have to happen. Maybe combining two of them into a one-bedroom with an actual kitchen or something. Who knows.

Lisa, there are affordable apartments, even houses, all over the place. You can get a large place for under $800. You don’t have to live in a closet and you have far more choices than you think. Apartments are all over the place. I don’t see any problem.

Event Horizon — I’m not worried for myself re: finding a place. I just thought the odd (IMO) decision to build these places speaks to a lack of understanding on the part of builders regarding both the supply of housing AND the demand for it. I thought, “What are these developers thinking?” And that got me curious about what they’ll end up doing with these places, which I doubt will ever be at full capacity. It will be interesting to see what happens.

I just read a report on Seattle: there are “over 72,000 units” in the pipeline. Not all of these housing units may get built, but that’s a lot. More than in SF (65K).

That speaks of the huge construction boom going on there. This will eventually impact home prices and rents. But obviously not yet.

Yep, having visited in early July, I saw it, and it’s not just in the city, either. The suburb I grew up in, which was really more of an exurb when I was a kid, is full of new houses/houses under construction. Yes, the area is gaining people, but developers are also miscalculating, IMO.

Will this be enough capacity for proposed communities of low wage refugees who don’t respect law and refuse to speak english?

I live in one of these recent-exurb-now-suburb neighborhoods that Lisa talks about. There are for sale signs everywhere near me for existing single family houses, even now at the end of September. This reminds me alot of 2010 or so when people were desperate to unload houses, and houses just sat on the market. People I know who have been trying to sell say they only get low-bid offers.

On the other hand, every vacant lot has been bought up and is being built on. There are the new housing developments also going up as farmland gets developed. Single family homes that go up for rent get picked up really quickly… this is all quite different from the post GFC period. Bidding war for homes near Microsoft.

But, where are the jobs coming from? Microsoft and Boeing have been doing a lot of layoffs. Among my neighbors, they are mostly getting laid off or going from FTE to contractor, and generally going down the corporate ladder rather than climbing it. The economics just don’t seem to add up.

I think these tiny units are part of the austerity/agenda 21 plan for our future. Max Keiser had a show on these micro unit buildings on the outskirts of London with shared bathrooms.

Here’s what’s going to happen. Those units will flop within a few short years. A new set of investors will pick up the buildings on the cheap and lobby the local gubmint for housing Chicago felons at taxpayer expense. Bye bye neighborhood.

Don’t forget all those new Syrian arrivals ……

I live in Everett, Lisa, but go downtown Seattle 4 days a week.. Construction cranes are everywhere and holes where buildings used to be are everywhere. A book seller friend (2nd level at Pike Place) told me there are 31 cranes operating in the city core. Chain-link fencing surrounds lots of old downtown blocks waiting for a wrecking ball.. The ride into the city via South Lake Union is a combination moon scape and Jetsons.. All of the commutable suburbs are having their own building boom and anyplace where the Light Rail has gone has seen expensive condo/apt. which bumps up the old rental stock.. Welcome home but you won’t recognize it..

There must be a whole lot of cheap money being lent for these projects.

Seems like that might be the future of rentals to ordinary people.

Hi Mr. Wolf,

Some advice, please. I’m 26 years old and looking to buy my first property to finally have a place of my own. My parents and I have substantial savings and are looking to invest in either a condo or house. We live in the SF Bay Area, but I’d like to move somewhere more affordable like Sacramento.

Should I wait a year or two to see if prices go down? Are you confident we’re in another housing bubble? (I’m single w/ no kids)

Thanks

Walter,

I don’t give that sort of financial advice ever. I encourage you to read my site (and other sites) and draw your own conclusions.

Also note that housing markets are local. So what happens in SF may not be happening in Sacramento.

But some other readers – particularly those in the Bay Area – might be willing to chime in and make some recommendations.

Good luck with your decision.

As an old man who has seen America from the 1950’s to Today: Don’t buy. Rent. That is my “simplest” answer.

IF you buy you need to have excellent wisdom and understanding of Demographics. If you buy, buy the most expensive home you can in the most expensive neighborhood, which lessens your chance of financial loss 20 or 30 years from now. A “middle class” home today will be worthless in 20 years.

The advice I give my own children? Only buy a home in a small town at least 50 miles from a major urban center. Better to drive 1 hour each way than lose every dime you put into a home close to a major urban center.

interesting, my advice would be different but of course it really depends on the (local) situation.

In my country I don’t think buying in expensive neighborhoods is safe if you are in it for the long run. History shows that over 20-30 years even elite neighborhoods can get out of style or really go down the drain, while the opposite also happens (but is often difficult to predict for outsiders). With a very expensive neighborhood you are betting it will always stay very expensive which in my country (Netherlands) certainly isn’t true. Over here the most solid ‘home investment’ is usually in ‘mixed’ neighborhoods, that have both lower and higher class properties plus some business activity. Maybe the US is very different ;-)

As to small towns: again in my country many of those have lost almost all facilities like shops etc. over the last 25 years, so living there means you have to spend more time for shopping, entertainment etc. For those who have a job (especially two-income households with children) this doesn’t look very attractive to me.

As to buying and renting: IMHO the best time to buy is when rates are very high, because then the price will be low and the rates can only go down (and value of the property go up, instead of down). But you need to have some own money to buy, because otherwise the initially high rent may be prohibitive.

For those who don’t have money and never plan to have any (spend it all) there probably never was a better time to buy then now ;-(

The Netherlands is virtually on another planet re: real estate Since an axiom RE is that it is local, I’m a little surprised you would advise on North America let alone the US.

In the first place once you leave the NA urban centers

the supply of raw land is by comparison, virtually infinite.

Yes Vancouver is crowded, (why do people on limited income choose to live in one of the worlds most expensive cities?) but the province of BC has roughly the land mass of Western Europe, with only about double the population of greater Vancouver.

By our standards, there are NO bad areas in the Netherlands.

One American writer visiting Amsterdam’s red light area compared it to visiting Disneyland re: clean streets,order, safety.

Chicago alone can have several gun murders per day- more annually than the UK.

Even in Canada a playground by comparison, we have Hastings in Vancouver that shocks Europeans.

As in many parts of the US rust belt. the police don’t go there unless they have to, and then with a partner.

And we haven’t even got to the rather bizarre financial safety- net the Netherlands govt offers home owners, which as you explain does not exist in the US or Canada. The US had a RE crash, the Netherlands didn’t.

As for the comment above yours about buying ‘the most expensive house’ the bible here is clear- you buy the cheapest house in the most expensive area: the three things to remember are location, location, location.

There was recently a write up about a guy selling his tear down in Vancouver’s Point Grey. It was a tear down when he bought in 1985 or so. The realtor said ‘oh you won’t like this one’ but the guy insisted and bought it for about 180K.

Just sold instantly for 2.2 million.

Of course only the lot sold, because now it will be torn down

It would be worth about 40K more with no house.

You’re buying for appreciation- only the land appreciates.

at nick kelly:

I’m not trying to advise about buying in the US, I’m just assuming that some readers are from outside the US and may appreciate some perspective on what goes on elsewhere.

If you think the Netherlands is ‘land-locked’ think again: just 11% is built area (including industrial zones, roads, gardens, parks etc.). The rest is mostly agricultural land so there is plenty of room for building homes for the indefinite future. If it weren’t for the migrants, the population would be shrinking by now like in much of Europe. Oh yes, and unlike most other countries we ARE making more land ;-) The only problem is that the government fully controls where building is allowed, and this is used to jack up (land) prices and profit for a very select elite.

Agricultural land is valued at 2-3.5 €/sqm over here; when government changes the destination to building it suddenly is worth 300-3000 €/sqm. Nice profits if you can get your hands on it and they want to protect that privilege at all cost. Many Dutch cities have been living the good life by buying up huge amounts of agricultural land all around (at way too high prices) and booking the increased values every year as profits although all this land just sits on the books doing nothing. When the bubble bursts many cities will go bankrupt.

We certainly do have bad areas in the Netherlands, just not the type where you are likely to get killed like in many US cities. Guns are illegal here, homicide is mostly between criminal gangs. But there are many other problems. I agree that the Amsterdam red light district nowadays is more like a Disneyland for tourists; the big problems were pushed to the outskirts and other cities many years ago.

I have pointed out before that the great homeowner safety net that the Netherlands has is a Ponzi. People keep repeating how great this is but really, you cannot protect the bubble value of almost the complete housing stock in the Netherlands with an insurance premium of just 0.4% that is paid by new buyers who take out a mortgage (effectively the homeowner pays nothing, because they get a similar discount on the mortgage rate as a result of this guarantee). At best this delays the inevitable and make the final crash even more epic.

The Dutch guarantee fund could go bankrupt as soon as there is a serious decline in prices. In 2008 nothing happened because of the ZIRP/NIRP policies of ECB that strongly lowered costs for homeowners, plus the government pressed the banks (most of them were temporarily state-owned) to forgive problematic mortgages or at least give the people a few years extra time to start paying again. Just ignore the problem and hope it disappears, and let the taxpayer bleed for all costs without really telling them, great policy …

I think next time they will change the rules for payout from the guarantee fund, so that it no longer is the blank guarantee that homeowners think it is. Abuse was way too easy and there are signs that they are now clamping down on some bad practices (e.g. people “divorce” on paper so they can have the fund pay for their own losses, often after racking up mortgage debt to the max, and are then “miraculously together again” the next year). There are other abuses e.g. piggyback mortgages so that the government fund insures e.g. the first 275K of a fully mortgaged million euro property; great for the banks and the homeowner, not so much for the fund. Officially it’s illegal but up to now they still pay out if in case of default.

Economists have calculated that the real cost of the Dutch homeowner guarantee in the free market, even assuming there is NO abuse and that valuations are realistic, would require a 4-8% insurance premium of the home value, instead of the current 0.4% of the mortgage amount. With 4-8% extra cost the appetite for this guarantee would quickly disappear as home buyers would have to pay out of their own pocket and most of them probably understand that much of the risk can be avoided by living within your means and avoiding really stupid decisions.

If something looks too good to be true, it usually is.

Good advice. The cities are becoming unlivable in quick fashion. I’ve had way to many close encounters with thugs and insane people this last year and it is only getting worse. I had bet on the city and that bet was wrong. I will leave as soon as circumstances allow.

Event-

I totally agree. There’s no gain in owning today, unless you have a below 4% mortgage. Housing gains are almost over. The Boomer homes will continue to flood the market, along with all the cheap construction, noted in other posts here, built on the 0% money which is laundered in the banks. There are almost no real values around, except in small communities. My small city is being destroyed by a boom on our south end, for which there are no jobs at all. Go figure! But we all know the US economy, like most others, is all smoke & mirrors. What used to work, doesn’t. Like bank savings accounts—-why bother? Taxes will be unrelenting; renters who are high quality will be in demand by quality landlords.

I can’t tell you what and when to buy, but I can give you one piece of advice that has served me well. If you buy – make sure you pay off your mortgage! The faster, the better. Do not use your house/apartment as an ATM. I became debt-free at 34 and vowed never to take another loan.

CA real estate is over priced. By renting, you are having your landlord subsidize your housing expense. You might research renting and using the cash to buy a rental in a stable real estate market where you will have income every month and the tax breaks. Indy, Atlanta, Birmingham, Memphis, Little Rock, Grand Rapids, some Ohio cities and even some Chicago suburbs, believe it or not.

Here’s an example. We live in a CA town in a house that’s supposedly worth $550k. We pay less than $1700 in rent, for a rent to value ratio of 3.71%–common in CA. We just put money down on a rental in Little Rock for $102k that will rent for $1000, or a rent to value ratio of almost 11.76%. Don’t expect the roller coaster on valuation, of course, but who cares? It’s not easy for the CA dreamers to time the market, even though it’s pretty obvious when to sell (hint: now) because they get wrapped up in keeping up with the Jones and convincing themselves that the weather premium is worth it (hint: it’s not). And we’ll be earning tax advantaged income for years.

No matter who wins the election there will be a shift in the money policy. Rates will go up and this could have a major affect on mortgage rates and price of housing. With that said, you can get a 30 year fixed rate now at under 4%. Buy something affordable that would have the same payment you would have if you were renting, yes that’s possible in the Sacramento market. As a Realtor I have seen many ups and downs in the housing market all caused by different factors.

Sacramento is an awesome town. I lived there for 15 years. Even though I grew up in San Jose, and have spent the last 3 years there, I far prefer Sacramento for its Old Town, downtown, mid-town, tons of restaurants and night-life, fewer people, less hurried people, and its proximity to nature. And of, somewhat affordable housing.

We bought a the peak last time with perfect timing; I will not make that mistake again.

As for timing, go on Trulia and set your filter to “reduced prices.” The core regions are still holding strong, but outlying suburban areas like Concord or Roseville, for example, or smaller towns, are already showing 100 plus days on the market, and two, sometimes three price declines.

“To put that in perspective, that median two-bedroom costs the tenant $57,360 a year,…….”

==========

Today than number of USD will buy $75,280 CAD, so I’m guessing that the average Canadian Snowbird will not be maintaining a 2-bedroom apt. in San Fran to fly away to this winter.

But just think, with a little more experimental financial engineering and expanding NIRP just a bit, Janet’s finger could solve all the landlord’s and tenant’s problems.

For the first month all the new tenant would have to do is borrow the money to pay the rent. Next month the tenant borrows enough to pay off the first month (“plus” negative interest) and also borrows even more to pay the second month’s rent. Etc., ad infinitum.

The tenant keeps borrowing to pay off old debt and each month increases the new loan by the amount of the next month’s rent.

When the tenant inevitably decides to move, the month before doing that he/she declares bankruptcy and the TBTF bank that made the bad loan is bailed out by Janet’s finger.

Everybody’s happy! What could go wrong?!

But why does my brilliant new scheme sound so familiar?

if Janet has her way with NIRP the landlord would not have to rent out the property at all, because it would automatically appreciate and they would collect money every month simply for taking out a mortgage. Why bother with renters who only cause nuisance and extra cost?

Even more money!

About your name, any relation to Merwyn Bogue?

Hi Wolf,

I have two questions.

1) approximately 11/2 years ago I was evicted from my studio in Alameda ca

Because the major landlords forced out their long term tenants for techies & the coming eviction restrictions now in place.

As a result of these evictions the city is seeing more retailers fail as well as restaurants….

My friend owns a restaurant on the main drag and his revenues have gone down…

Once rents plummet far enough, do you think the the techies will simply go back to SF?

2) How much are these price increases as a result of the AIRBNB effect and when this all come crashing down will it be as bad as 2008, worse or?

Thanks, Gustave

These are great questions! I don’t have an answer. So a few thoughts….

Sorry to hear about your eviction!

I have also seen the problem with small retailers and some restaurants and service suppliers, like hair salons: their rents get jacked up, and they have to shut down. They have another problem: many people who live here don’t have enough money to spend after housing costs, and so they spend less. Lots of small shop spaces are shuttered around here.

My gut feeling is that the tech employment boom will eventually taper off or deflate. This would come on top of the surging supply of housing, which would put further downward pressure on rents and home prices. We’ve seen this movie before.

But I have no idea how people will react – if they will move back to SF, or if they like it in Oakland or Alameda or Emeryville or wherever and grow roots and stay. So keep your ears to the ground.

>>>> Your question: 2) How much are these price increases as a result of the AIRBNB effect and when this all come crashing down will it be as bad as 2008, worse or?

I’m seeing rents falling and condo prices starting to skid. So this may answer your question about Airbnb. No telling how bad it will get.

Yellen just said that the Fed ought to be able to buy corporate stocks and bonds (not legal right now). Soon she may ask Congress for the authority to rent apartments too if rents begin falling across the country. The biggest landlords are probably already having dinner with her.

A perfect example of high rents destroying small businesses. In my neighborhood (San francisco, FIDI), a man’s haircut will cost you at least $40 plus tip. I only get haircuts when I am on an errand in suburbia.

Gold Rush pricing …….

I find it deeply ironic this goes on mere miles from where almost fifty years ago the Diggers attempted building their moneyless society…

i hear ya; i stopped cutting my hair and have turned even THAT into part of my new wild style.

(smile)

I wouldn’t want to be an investor in any of the big landlords. As the rents slide down the value of the properties go right along with them. Zell got out just in time.

Sam Zell’s sales are NOT equivalent to his complete exit in 2007.

He is not “GETTING OUT”. He is “dumping the dogs”, “concentrating on central business districts”, “selling suburban properties”, and “stockpiling cash”.

As near as I can calculate, he has sold or is selling about 2/3rds of his office portfolio:

http://www.barrons.com/articles/sam-zells-real-estate-assets-selling-at-20-off-1461753690

And he sold about 20% of his apartments to Starwood Capital:

http://therealdeal.com/2016/01/27/equity-residential-starwood-close-5-4b-resi-deal/

As far as the “BIG INVESTORS” go, they still own less than 1% of rental homes. Compare that to the consolidation / roll-ups that we have seen in other industries. I do not know which companies will succeed, but I have NO DOUBT that this will continue and grow. Wall Street is just getting started in milking this new cash cow.

Chris,

No doubt the trend will continue until it blows up, which is why I wouldn’t want to be an investor or renter in any of these companies.

regarding AIRBNB:

I don’t know about SF, but I just read a report about Amsterdam that says the recent introduction of AIRBNB there has jacked up the already very high rents there by at least 20% (extra), in just a few years. The main reason is that it is far more profitable to rent out properties for short times (at very high daily rate) to tourists than it is to rent out for longer time and relatively lower rate to normal renters. I guess a city like SF that also attracts many tourists will not be any different.

Of course the rent could go down by the same percentage when e.g. tourism dwindles or when AIRBNB or its landlords finally start getting taxed for their income. At least in my country their business model seems to fully depend on tax evasion and circumventing all the rules of the Dutch housing market.

I saw a report on Iceland saying basically the same thing. A big surge in tourism caused many landlord to evict tenants and rent as air bnb. Causing a strong rise in rental rates for locals.

Tourism will soon become a political hot potato like it’s becoming in Barcelona.

Yes, it generates cash but like most other markets these days it’s also rapidly becoming commoditized, leading to so many problems many are asking themselves if that fistful of dollars is worth all the troubles commonly associated with a tourism boom.

Tourism commodization is not like smartphone commodization. It affects infrastructures and life quality. Anybody who has seen one of those new cruise ships disgorge its human cargo knows what I am talking about.

The road of excesses may lead to the palace of wisdom, but it’s taking an awful lot of time.

True, same story in Amsterdam. For normal citizens it becomes a kind of dark Disneyland (with drug tourists, drunks, street violence, filth and nightly noise everywhere) while only those who rent out through AIRBNB etc. and disregard the rules have the benefits (again: privatise the gains, socialize the losses). And not just that, as others have mentioned small ‘non–tourist’ business starts to disappear which in a few years works out really bad because unlike AIRBNB and its landlords these small companies do pay taxes and often try to keep the area in good shape. But it seems that once a place gets really popular there is no way stopping this :-(

My relatively small city recently also started attracting small cruise ships. It’s currently mostly funny to see a huge chunk of foreign tourists unload for a few hours in the city, they dominate the scene everywhere they go. But this could easily get out of hand…

I do an airbnb—-locals wouldn’t rent my house because it is in a commercial mix area. “Too noisy,” they all said.

Tourists love it, they can walk all over town & still have a driveway to park in. I pay 3 taxes: Lodgers tax, gross receipts & small business, which add up to almost 18%. Oh, and there are yearly fees & two inspections by city. I do all the work myself to keep the margin worth it.

Are you all noticing that the airbnb phenomenon is about many of us saving our property? I would never do this if I didn’t have to……!!!!!! Re Barcelona, I’ll boycott that city. Those residents are just trying to hang on. No one in their right mind changes beds & cleans for free if they don’t have to.

The real point: the government regulations have destroyed ways of making income. People are desperate now. That’s the real issue…..we pick at each other when the culprit is the high government costs.

Many of the tech companies provide meals for their employees. I recently read that Facebook provides 3 free meals and snacks. Who needs to go out to eat.

Someone caters those meals. But it does seem rather like standing in a bread line instead of riding your skateboard.

Pretty soon these employees will be accused of being freeloaders at their exit interviews as their jobs are ended in favor of cheaper labor or al-gore-ithms.

I went to lunch at Google HQ last year. You have to see to see it to believe it. At least 4 eateries of very high quality and a great coffe shop. No one has to pay. All provided by Goog for free. Also personal trainers and a state of the art gym facility. Brightly painted bicycles parked at the doors for easy cross-campus transportation.

Great article Wolf. I’m usually a lurker, but I read practically everything you and your readers have to offer as insights. But seriously…”even teachers”? When have teachers ever (recently) been paid enough to make ends meet…or even what they are worth in societal terms? Much less in a housing/rent bubble.

It’s more like “even doctors.” My husband is a specialist on the peninsula, and we can’t afford to buy. 15 years of training (no debt), and we’re looking to leave. Apparently the collective pool of “talent” excludes people who save lives for a living.

I can’t wait to get out of here. Tax attorney + tax CPA couple, both working full time but it is just a dead end. I am so sick of it.

So I quote the late great Daniel Boone: “to hell with yall, I’m going to Texas” or somewhere without Prop. 13 and sickening growth restrictions that only benefit the rentiers.

Also a lurker here! These comments caught my eye – we live in SoCal (LA) and have also been wanting to buy for a while but haven’t because at every price point, I think we should be getting 2-3x the house (size, property, condition) for the money! We used to joke, but are now seriously considering moving to Nevada!

I have a house near Tucson. Bought it last year for $38k. It’s a fixer in the desert near saguaro national park on 1.2 acres. AZ is like CA 50 years ago. 10 minute wait at the DMV, people are nice to each other, traffic almost nonexistent and everything you pay to the gov is almost comical for how cheap it is. Gas is $1.90/gallon. I could go on. Downside…105F is common in the summer.

Agree.

Oh, it gets lots hotter than that! Not to mention all the critters you have to deal with if you live on the desert. especially the many-leggeds and no-legs. The tarantulas are actually kind of amusing and sweet, but the centipedes are big and mean. Expect to have to vacate a gila (heela) monster off the premises once a year. This is best done by sliding a shovel under the hissing huffing and puffing beastie and escorting him out to the desert. The worst are those evil red and black “kissing bugs” which will lurk around your bed room waiting for you to fall asleep….

Maybe San Francisco isn’t so bad after all.

:-]

Didn’t you know, an educated population is a problem for the government? They chipped away at teacher salaries starting in the 60’s when the dumbing down policy went into effect.

My family is full of teachers & medical people….they’re all pressed now. It’s about the corporate takeover of medicine & education.

Seems that at least in this part of the economy the market is still doing its job for adjusting prices to reality (not what the FED wants …).

I don’t see any of that in the rental market in my own country but at least our rents are not so impossibly high as in the SF area (the average Dutch renter spends 30-50% of income on rent; the average Dutch homeowner effectively spends about 10% of income on mortgage, property taxes etc.). Rents have been climbing steeply ever since the 2008 crisis, while homeowner expenses (especially for those with more recent contracts) declined strongly.

But I wonder how reliable the numbers about asking rent are. In my country those numbers from rental websites are extremely unreliable, because they are ‘asking’ rents and don’t tell you what the tenant really is paying. Often many properties with sky-high rents that list forever skew the average numbers, even though they are never rented and so are not really part of ‘the market’. Properties with attractive prices will be few because they will be listed only for a short time. And the websites often have a financial incentive to boost the average rental price because most of them work for the owners, not the renters.

In my country there are other issues e.g. most rental agencies asked ‘key money’ equivalent to 1-2 months rent for their services (which in practice often means people pay 1-2 months rent without getting anything). This is officially not allowed here and last year the government finally started to clamp down on this. The result: rents on the rental websites are now an average of 10-15% higher (also per square meter of space) than last year, because the rental agencies simply added the ‘key money’ to the official rent.

As someone who lives in the SF Bay Area, along the mid-peninsula, I can tell you that these prices are absolutely reliable and common, and not any high-priced one-offs on the rental websites. We sold our home in early 2015 because the market seemed to be heading into bubble territory, and I did not want to get trapped again.

We got a rental for $4500, which was actually a good price for a 3b/2bth 1900 sf (larger than avg size condo at the time). When our lease came up, the landlord increased our rent $500. We could not find anything equivalent/ cheaper, and were stuck paying the asking. However, in the past two months or so, I’ve been seeing more single family rentals on the market in the high $4000s to low $5000s range again (last yr., it was pretty much all $5500-$6500 for a 3bd), and the rentals have been staying on the market more than a month- some, even 2 months! This is certainly a sea change, since I have not seen lower rents for the past 5 yrs I’ve been watching.

When we first rented in 2015, the rental agency also took the first month’s rent as their fee, but the landlord paid it, as he had requisitioned the agency. We replied to an ad placed by the rental agency on behalf of the landlord, and paid a $45 application fee.

interesting, and I hope rents over here don’t go that high here…

I have been renting for the last eight years and have had one rent decrease and one increase, while asking rents in the free market have been rising by 5-10% every year since 2008. I have seen many rental properties with high asking prices staying empty on the market for years … No sign of lower rents over here.

But I’m probably lucky, I’m renting a luxury apartment in the inner city from a family that got too big for living there and could no longer afford the mortgage. It’s really not suitable for a family and most singles cannot afford the rent for these apartments. My landlord is quite happy to have someone help with the mortgage payments (he’s under water like many and tries to avoid default, because he is not covered by the state guarantee and would lose a lot of money).

For families it is really difficult, those with lowest income get strongly subsidized homes from the government, but as soon as income rises you have to rent in the free market which is completely distorted and there are very few rental family homes. The only option is usually renting in one of the newer suburbs where there is still some unsold housing stock form the 2008 crisis; but those aren’t really attractive areas due to almost total lack of facilities.

But most people give up and buy, why not when no money down is needed and the mortgage cost is far below renting. People still complain though that in some cases the maximum mortgage is now only 102-103%, while the cost can be 104% of closing price; so you may need a 1% down payment, it’s a shame ;-)

Geez………….

Glad I don’t live in the USA!

Even with our so called property ‘bubble’ here in Australia you can still rent a nice house for a lot less than a 2 bedroom apartment in most of those top 20 places in the USA.

One thing I have noticed about condos in the USA is that fees have gone way up over the years.

Some of the places I look at in Honolulu have monthly fees in the US$600 or more per month range.

Add in monthly RE taxes of $100 to $150 a bucks a month to that as well. That’s almost half of the rental income gone even before you add in other running costs or a mortgage.

How much are those month maintenance fees in other cities in the USA?

It depends on the building. In a luxury building with all kinds of goodies in the common area that cost money and need maintenance, such as an indoor pool, plus 24/7 staff at the door, plus, plus, plus, association fees can be a big chunk. They’re figured on the percentage of building ownership that you have. So if you own a larger place, you pay more. $600 a month sounds very cheap to me.

Some condos in Florida, really nice ones in golf communities, go for as little as 10K. The reason is that there is a membership fee for the golf course of maybe 70K and the monthly maintenance is over 2K. I have seen many listings of this type. The higher the maintenance, the lower the price.

In Hawaii there are two types of ‘ownership’ for many condos: fee simple and lease.

With the fee simple you own the land. For the ones still under a lease arrangement you pay a lease on land every month.

The lease is usually renegotiated at some fixed points in time and is based on the market value of the land. Some of these lease units have the option to buy the land. Others don’t.

I remember one condo in Kahala (Kahala Beach) where the units were valued in the million dollar area (1990 some where around the $1.5 million area), but when the lease ran out the new lease rent was repriced to something around US$2000 or more a month.

The price of the condos fell to around $150,000 or so with some changing hands around $100,000.

Huge monthly costs: lease rent A$2000 or so, monthly fees around $1000, and that continual obligation to fork out the lease rent for the next 12 years or so when the lease expires…………again…………..another increase.

Here is one example:

http://www.honoluluhi5.com/kahala-beach-249-waialae-g-c-condo-for-sale-201620108/

Job losses are the only thing that will bring rental and housing prices down in the bay area, in the long term. It would be nice to correlate the info you have in this article with immigration and employment data.

Nope, it only takes rent prices to make it untenable for anyone to afford after taxes and other living expenses. And that is already happening in the bay area and many other places.

My best friend has a waterfront condo in Uclulet (west coast Vancouver island) that he paid $300,000 for. His strata fees are $250 month. 2 bedrooms, the best appliances and furnishings, quiet….overlooking the marina while we barbecue on his deck. They could use another doctor, intrigue.

You folks are getting hosed, imho. There are many options out there.

I like Uclulet -compared to the places discussed it is in the middle of nowhere.

Your friend wouldn’t like it if a realtor used comparables on the Queen Charlottes to appraise his place.

Re: options. Most people need to locate much closer to jobs.

supply meets demand and exceeds it. open eyes see what can’t be missed.

arithmetic. imagine that.

These few bucks in the $200 to $300 bucks lower rents are a just a baby drop and really meaningless in the pocket of the consumer.

Rents and housing costs of real estate need to go down some 25-40% and you won’t see that until a MAJOR RECESSION hits the tech companies… nothing like major layoffs to bring housing down.

All these layoffs that have been happening in the Bay Area and Silicon Valley since the beginning of the year are just a drop in a big bucket. Too many useless App and social media companies hiring and getting money from who knows who… at some point will implode these stoopid apps market.

Yahoo, Cisco, IBM, NetApp, twitter, Intel, HP, plus many other have had layoffs and some will take effect soon. But The 101 traffic from Palo Alto to 85 South San jose… has never been worse… except maybe in 99-01 before the .com bubble Popped.

maybe that traffic congestion is thanks to the ‘free’ car loans?

I see the same in Netherlands, economic activity is still sluggish (I don’t think there is any real improvement compared to 2008 or even 2001), government has gone on a spending spree for new roads etc. over the last years but the traffic jams seem to be worse than ever. I don’t think all those extra cars on the road are due to improving economy. Maybe it’s because all those people without a job have decided to enjoy driving their ‘free’ new cars now they have the time to do so ;-(

A friend manages a 20 unit apt near California and van ness in SF. Spring of this year he said the market was clearly slowing. Having lunch with him in 3 weeks. So I’ll get the latest info. Another friend got a year lease on a 3/2 in walnut creek back in June. Cost her $4200/month and she was glad to get it. She said as soon as the lease is up, she’s moving out of CA.

If Hillary is elected, there’s no limit to how high rents and real estate will go. Modern monetary adherents tend to believe that the price of money should be near 0%. Rates as noted might even go negative. Vancouver showed us you don’t need actual renters for real estate to go ballistic.

There will be a near psychotic push into real things as money is devalued. Foreign pension funds will buy, the Chinese will continue to buy and each new surge of the real estate bubble will serve as collateral (a credit line) for the next wave up.

I disagree with anyone who states there are sane limits here.

Also immigration will surge as Hillary welcomes in scores of new immigrants to depress wages and fill the high priced real estate. There is no incentive to help real people any more.

http://www.computerworld.com/article/3089314/it-careers/clinton-wants-to-staple-green-cards-on-stem-grads-diplomas.html

And this will be different how if Mr. Real Estate is elected?

Have you ever heard the aformentioned gentleman speak about monetary policy? Do you think prior to the campaign the words had ever left his lips?

For one thing: Hillary is committed to lots of immigration, including amnesty for everybody already here. I’m going to assume you have some idea of Trump’s position on immigration.

So Nick – don’t you think that this one policy position all by itself will have a yuge impact?

Tim,

It seems like you’re conflating Market Monetarism with Modern Monetary Theory. Their respective positive and normative perspectives are very, very different. You’re describing Market Monetarism. Modern Monetary Theory is an empirical accounting of how money enters the system, not an advocacy for NIRP and ZIRP.

This is some of the most beautiful land around me. Someone bought the other place, the farm with the guesthouse on the ridge across the hollar…

http://www.unitedcountry.com/search06/SearchViewProperty.asp?SID=244505555&Item=911369&Lcnt=&Page=1&Office=03067&No=03067-60116&AU=N&FT=P

Since I am not a tech elite and my view is from the gutter. I am not viewing this from the mountain top, but from the bottom. I clearly see a Federal Reserve Bubble that has engineered this absurd start-up boom which has inflated, illogically, irrationally the cost of housing in the Bay Area.

I see luxury housing being built, every where. I ask myself there are only 600,000 millionaires in California. It is a large number but not all live in Mountain View, or in Palo Alto or San Jose. California millionaires live all over the place. Perhaps they have a place in Beverly Hills, or Orange County. I am certain they are not all going to live in “the Valley”.

The tech IPO market for 2016 has essentially locked up. So that exit is limited. Tech stock analyst Trip Chowdhry says that the start-up boom will crack in March of 2017.

From my view in the gutter, I surmise that he is correct. The beginning of the end was Super Bowl week when Fitbit, LinkedIn, Twitter all crashed by 70%. The noveau riche techies found themselves in a locked up IPO market which has set in motion a chain reaction which ultimately leads to the start-up bubble bursting.

I ask myself how is Tesla going to compete with the zillions of auto makers out there? How is Oculus going to compete with Samsung and Sony when they start putting out VR headsets?

One can make the best product in the world but competition from high-powered consumer electronics firms and auto-makers is going to cut your market share. I guess…Apple wants to get into the auto business. We will see how that goes.

Tesla is, in my opinion, a sociological experiment to see how far people can be pushed before they snap and/or reality comes back to bite them.

But it’s a story for another day.

Speaking of IPO’s, regulars here know I have a pet peeve for jet.com, that startup which promised to beat Amazon into a pulp by losing money on every item they sell.

Up until August 2015 or so the much awaited jet.com IPO was the next big thing. Never mind there were no hard facts about the IPO, just a heap of rumors. Then everything went silent until August 2016.

Early that month it was announced Walmart would buy jet.com for $3 billion: one tenth in stocks and the rest in cash.

Sure, jet.com investors will make a bundle out Walmart’s desperate scramble for any discernible scrap of growth, but the usual people making a killing out of IPO’s are left high and dry.

Much more critically, the extremely dangerous phenomenon of narrowing (financial markets are driven higher by a dwindling number of assets) continues unabated, together with the reduction in the number of publicly traded companies in the US: we are now back to where we were when Ronald Reagan was still president and the USSR still existed.

One thing Wolf I would like to toss in for thought. According to Harvard research 70 to 90% of mergers and acquisitions fail. I would bet a bottle of Riesling that tech mergers and acquisitions are probably closer to that 90% end.

I would also bet that the LinkedIn acquisition for Microsoft may not workout like their acquisition of Skype, Nokia and Yammer, that it is just going to be a big waste of 27 billion dollars. Those mentioned acquired companies were sort of swallowed up by Micorsoft and have not done much relative to the price paid. I own a Windows phone, it is actually a good phone but the competition from Apple and Samsung is just too much.

Sorry for the slightly off topic rant but it does tie into this whole housing disaster in the Bay Area.

M&A is a way by which companies attempt to “buy” growth by taking advantage of a low interest environment.

These benefits are usually shortlived but financial markets have never been known for their foresight.

The big problem with M&A is they invariably mean “synergies” which translates into “layoffs”. These layoffs invariably consist of decently to well paid people, often around 40, an age at which even a great curriculum doesn’t help anymore finding an equally well paid job.

These people, fired through no fault of their own, can often find a job, but it invariably pays less than the previous one.

It doesn’t need to be a big paycut for the consequences to be felt: a few hundreds a month will suffice.

Multiply those few hundred dollars amonth by tens of thousand and you have part of the explanation why for the average person the last eight years have been so crummy and with no end in sight.

A couple earning a few hundreds less a month has to cut on expenses, especially if they have children and local childcare costs are high as they are in California. This means going to the hairdresser twice a month instead every week, a couple days less on vacation in Idaho, consuming less wine etc.

Again multiply by the huge numbers of laid off people due to M&A deals, throw into the mix a low interest rates environment (which tends to favor the highest tax brackets) inflating assets, a fair bit of lobbying and rent seeking driving some fixed costs up year after year and you get why the general feeling is, despite official figures and crazy bubbles, we as a whole are not doing as well as we were doing in the 90’s.

The nature of M&A in tech is different than the general deal on Wall Street. In tech the deals are mostly done to acquire the founders and/or outright kill the competition. In either case, they inject a lot of valuation into the tech community.

All those millionaires are mostly paper millionaires handcuffed to tech companies. While more cash is injected into the local economy, most of it is fantasy accounting, which morphs into reality at a real estate closing or a car dealership. They are borrowing based on their paper wealth. Those “lucky” techies are vesting over time in their “deals”, which could evaporate.

While incomes are definitely higher in tech, financialization has taken a big foothold. The VC funding system is a shadow banking system. They only want to generate profits, they care about innovation to the extent it generates a profit for them. The goal is an IPO. Shift the illusion to the general public.

We moved earlier this year (January) to a somewhat more central neighborhood in San Francisco for quality of life and better commutes. 4 or 5 months later, the house next door to us sold for $225,000 more than we paid for ours and with a more or less identical layout, though with probably $100,000 of improvements over ours. The home prices in our new neighborhood haven’t begun falling yet as far as I’ve seen. We’ve been trying to get a contractor to do about $10,000 in estimated repairs and have contacted 5 to 7 people who were recommended and none have time or will touch such a small job because they can make much more money elsewhere on bigger jobs and major remodels. The market may be cooling, but it still seems quite overheated to me.

I wasn’t particularly happy about the timing of our move since I felt like we were buying in near the top of the market and also getting locked into higher taxes which are more per month than the rent on a two bedrooms some of the places on that rent list. But we like the neighborhood and place we got into. It took my husband 5 years to finally get serious about moving and he makes double what I do and he suddenly decided he wanted to move, so I agreed to it despite all my financial reservations with regards to the timing.

It might not be the best financial decision, but sometimes you have to take the options you’re given when you’re dealing with other people. I hope I don’t regret it in the future.

Folks, these big city housing prices shock the system of those of us who live in smaller towns where real estate, though still overpriced, is very much affordable for middle class buyers. I live in a southern state university town of approximately 100,000 population. My wife and I worked here and retired here. It is reasonably affordable living, especially for two income MC households.

But, here too we have seen house, condo and apartment building that can’t be explained by current or even reasonably expected population increases.

The city has pushed retail development hard, even though many of the national outfits have closed here, as they have elsewhere. Good deals have been offered to retail by the city/county and developers over-develop, here as well as other places. There will be a reckoning here too. Granted, I don’t have a Golden Gate Bridge view, but $1000 – 1500 will get a very nice rental.

But, I do understand that those still in their work years have to be where their work is. So for those who find themselves in the high price real estate bubbles, I hope you at least enjoy living where you do.

As to the ‘unexplained building’, are they building for speculators?

I see this in my remote part of the Netherlands, much of the new building is very expensive vacation homes (costing 2-5 times the median home price) and seaside luxury apartments that are clearly used as a ‘store of value’ by the elite from the big cities. These homes are empty all year except for maybe 1-2 weeks, they cause a lot of destruction of nature because the building is often in the most beautiful areas, and they provide very little boost to the economy (even the builders are usually from far away). Plus this drives up prices of other homes in the area, so young people have to move out because everything becomes unaffordable. In my inner city, probably over 10% of the monumental 17-18th century canal houses have been empty for years and are just used for speculation as well, effectively removing housing stock from the market.

It’s all a logical result of many years of ZIRP/NIRP policy and will be very destructive in the long run.

NHZ: There is a degree of speculation, although not as much as we see in my state’s coastal areas.

I absolutely agree with your comment regarding ZIRP/NIRP. I have heard all sorts of excuses and theories put forth to justify these misguided policies. But, misallocated monies rarely yield desirable results.

Agree, and it’s difficult to predict what the result of this mis-allocated money will be.

I bet that most owners of the investment properties in my area are not paying full cash and take out a big mortgage so they can afford the current price level (after all, the monthly payment is next to nothing). In a downturn many will default.

For now the government is clever enough to state that you cannot live in these properties for the whole year, so they cannot be purchased as a primary residence. But that could change if the bubble burst end there are no buyers without changing the rules; that would put much pressure on prices of other homes.

The properties could also be purchased by the government and used for migrant housing, or to provide those on social security even more luxury housing options (they already have far better housing on average then many middle class people).

Politics will decide who gets the bill for all this madness and who profits …

For the moment I prefer to keep my money on a savings account (which means losing about 2% every year due to wealth tax etc. plus significant risk of course) instead of dumping it in some ‘investment’ that is sure to lose when the money printing bonanza ends.

In practical terms, YOU NEED TO CHANGE ZONING to allow smaller, more efficient houses.

While this may not help SF and NYC, most cities could easily increase their housing density by 50% using ADUs.

ADUs are “Accessory Dwelling Units”. Sort of big brothers to the Tiny House movement. ADUs are typically much larger (400-800sqft, 37-74m) than Tiny Houses (120-240sqft, 11-22m) and have fixed foundations and regular plumbing.

ADUs are much more practical and less expensive to build than Tiny Houses (per sqft/m) as they do not have the constraints caused by mobility and highway laws.

Tiny Houses must be lower than 13.5ft (4.1m), with the building height reduced by 21-30in (.5-.7m) for trailer clearance, cannot be wider than 8.5ft (2.6m), cannot weigh more than 10,000lbs (4536kg) without a special towing vehicle, and cannot be larger than 400sqft (37m2) even with a special towing vehicle. The cost for special towing can easily be $2000-$5000.

As the article below states, “most Bay Area communities now allow A.D.U.s. Only Palo Alto has not yet caught up with its northern neighbors in liberalizing A.D.U. construction.” Portland added 250 ADUs last year.

http://www.nytimes.com/2016/10/06/style/portland-affordable-housing-solutions-tiny-homes.html?_r=0

My wife started out HATING the whole Tiny House idea, but is becoming more open to it now that our sons have moved out. Given today’s incredible 3D drafting/walk-through programs and internet-sourced resources we could easily design a 400sqft house that feels as spacious and is as practical as the 600-800sqft that we actually use on a daily basis in our large Dallas home.

I would add one or two 150sqft bunkies (ie. out-buildings) for her crafting and/or for occasional guests. These would only need to be heated/cooled for short periods of time, thus saving tremendously on our electricity costs and environmental impact.

On the other hand, today’s litigious society and Texas’ UNLIMITED homestead exemption in bankruptcy make it wiser to have as much VALUE as possible locked up in our primary residence. Note that Florida, Iowa and Kansas also have the same unlimited exemptions.

New York City had a type of tiny house rentals, they were called single residency apartments. They were basically long term hotel room rentals. There was one such building on a street I lived on for many years. This type of housing attracts a very transient population. While I did know some people that lived in them for decades, that is not the norm. They attract the very poor, welfare actually considered it only temporary housing. They also attract the unstable, prostitution, drug addicts, and constant police attention. This was in spite of being located across the street from a church and next door to a convent. You will see the same thing anywhere you build this type of housing, which is why NYC finally got rid of it.

Zoning is one of the problematic housing issues that the Netherlands has in common with ‘Commiefornia’ (there are quite some political and cultural similarities as well).

But over here zoning primarily acts to jack up land prices and the result is that homes get smaller and smaller. Land for even a small new home is already very expensive (like 100-200K euro) especially near the inner cities due to government policy, and building a bigger home like what is common in the US would make it unaffordable for almost anyone. Unfortunately, small homes usually means low quality as well, the homes are really an ‘afterthought’ because the builders make their real money on selling the land that the home is build on.

The zoning stuff here even applies to houseboats, in my area they can easily cost upwards from 300K or so: that’s about 250K for the government for the right to have your boat on that location, and 50K at most for construction value of the dwelling ;-(

I’m all for small homes, even though I lived in a 8000 sqft monumental building for many years. But the homes need to be well designed (including self-sufficiency where possible) and that is extremely rare over here. Most of the new construction of the last 25 years or so is junk IMHO, which is a direct effect of our housing bubble. When housing is in a bubble, you can sell even the worst crap because people will line up anyway.

I have seen some nice prefab designs from the US that look affordable and nice to live in. Some Chinese companies are also working on this with promising stuff. Unfortunately home building is not a global market because the local regulations, conditions like weather and foundation, customers demands etc. vary strongly :-(

There needs to be a law passed that dictates homes can only purchased by a person who will be strictly the owner-occupier. This means no owning homes as a money laundering vehicle, no owning homes as rental income properties nor owning homes for speculative house flipping purposes. So guess it means there will be no vacation rentals in Santa Cruz but that is a good thing because local folks will be able to buy a home to live in. People are just going to have to say in hotels when they travel.

If housing prices plunge that will put downward pressure on rents because apartment owners will know that if they charge to high of rent, the tenant will just own a home.

In theory, this proposal should make housing prices more in line with median household incomes.

As a life long Bay Area resident, I understand that homes here will never be cheap but the current prices are insane considering the median household income is $70,000 per year. I read a report that one needs to make $150,000 per year to live a decent life.

Well, the tech companies can only afford to pay so much because they will not be profitable otherwise (that is assuming they are in the first place as most tech companies are not, especially the start-ups).

One funny observation made by a venture capitalist was that he never has seen so many people working for unprofitable companies.