OPEC’s Battle and Cheap Money

US natural gas has taught us this: In this era of free money, prices can stay below the cost of production a lot longer than anyone imagined years ago.

When cheaply borrowed money leads to overproduction, which leads to excess inventories despite rising demand, prices plunge to ludicrously low levels. And if borrowed money keeps pouring into the sector to keep existing investors afloat, drillers continue to overproduce because they have to in order to get even more new money to service the pile of existing debt, thus piling up even more debt and causing the price to get hammered down over and over again.

The price of US natural gas collapsed in 2009 and, except for a few brief episodes, has remained below the cost of production ever since. Now that investors are finally turning off the spigot, persistently negative cash flows can no longer be funded with new debt. Two major drillers have gone bankrupt this year. And the second largest natural gas driller in the US, Chesapeake, is headed for deep trouble.

But this is six years after the price collapsed. Tens of billions of dollars from investors have been drilled into the ground to never be seen again. And the price of natural gas is still below the cost of production, as production hit new records.

The oil market is different because it’s global and more geopolitical. But as with US natural gas, it ends up being about money and production. Production will go down only when the new money dries up. That hasn’t happened yet except on the riskiest fringes.

Instead, production continues to exceed demand, and inventories are ballooning globally on a historic scale. The below report is from ISA Intel via Oil & Energy Insider:

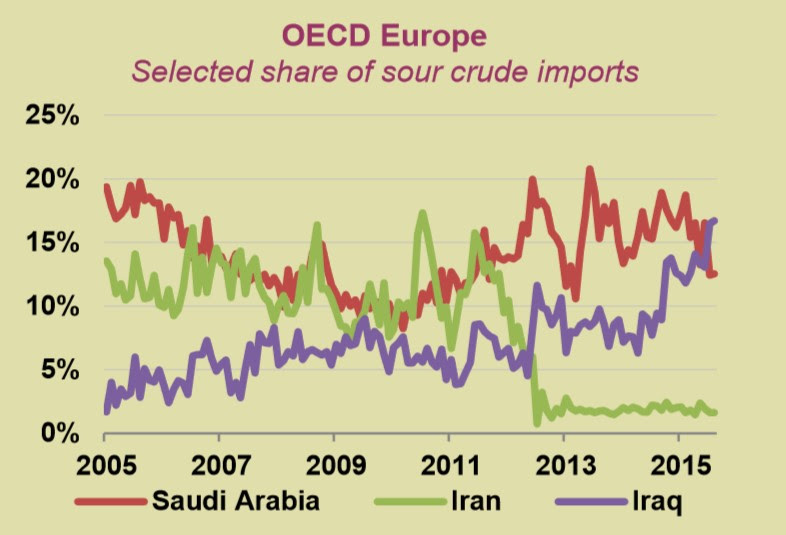

OPEC increased output in 2015. Gains led by Iraq and Saudi Arabia

- OPEC made its now famous decision in November 2014 to leave its production target unchanged at 30 million barrels per day (mb/d). Since then, the group has consistently exceeded that target.

- In October, OPEC produced an average of 31.76 mb/d, well in excess of the stated quota.

- The production gains made since last year have almost entirely come from Saudi Arabia and Iraq, each adding around 500,000 barrels per day.

OPEC fighting for Europe market share

- News reports have documented the battle for market share in Europe between Russia and Saudi Arabia. Saudi Arabia’s increased exports to Europe are pushing down the price of the Urals blend, the benchmark price that Russian oil sells for.

- However, Iraq has also dramatically increased oil exports to Europe.

- Saudi Arabia and Iraq have benefitted from Iranian sanctions. Increased market share came from the 1 mb/d that Iran used to sell to Europe.

- Iranian exports are set to begin again soon. Battle for market share in Europe will intensify, likely pushing down prices.

Record Oil storage levels

- Crude oil inventories are rising around the world (see black line on charts above).

- Swelling storage points to ongoing glut in supply, not enough demand.

- Until stocks draw down, unlikely oil prices will rebound.

Reported by ISA Intel via Oil & Energy Insider. But beyond these types of crude oil inventories, there is another type of oil storage: fully loaded tankers anchored offshore, waiting for the oil price to rise.

How many of these tankers are there? Bob Miller, author of several books, including Kill Me If You Can, You SOB, sent me his first-hand observations from a 33-day cruise he’d taken from the Eastern then Western Caribbean, through the Panama Canal and on to Canada.

Both St. Lucia and Aruba were loaded with ships. I think we pulled into every deep sea port in Mexico on the way. We actually had to work our way through them to get into some ports. I have taken two world cruises and have never seen this many cargo ships at anchor. They reminded me of WWII pictures of supply ships.

At first it was only the guests who were talking about all the tankers anchored offshore wherever we went. I guess the captain was asked about this so many times that he decided to make a public announcement. He said that most of the tankers were from Saudi Arabia and were having to wait until storage tanks were low enough to unload.

One big tanker had a sign that read, “Arrived 4/12/15. God only know when we’ll depart.”

This speculative inventory of crude oil is lurking everywhere, ready to be dumped on the market without notice as soon as prices rise far enough, or when speculators are forced to sell, practically guaranteeing that prices will get hammered down over and over again. And how low can the price of oil go under these conditions? To ludicrously low levels – just like US natural gas.

So is this the Death of the Petrodollar? Read… Petrodollar Reflux to Hit Treasuries, Other Assets

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s true Wolf that there are tankers being used as storage units around the world at the moment. I suppose that’s better for these shipping companies than having their ships anchored empty because Mr. Greed has finally come face to face with Mr. Reality. Yet, I keep going back to Dan Dicker’s article, “Oil & Energy Insider”. As I understand it, Asia has joined some other countries in limiting coal imports. I might be wrong, but I believe in the long run, as Mr. Dicker implied, “Enjoy this $40 oil while you can.”

Bob Miller – Interesting insights. Regarding the countries limiting coal imports, I would expect the coal to be replaced with natural gas anywhere that it can be. As I have written here before, as a retired petroleum geologist, there are lots of natural gas resources known about and still to be discovered. So, my bet is that much of the coal market goes to natural gas, with regard to fossil fuels. Nuclear and renewables aren’t in my bailiwick, so I can’t speak to their future.

Regards,

NT

All I know about NG is that Ford Motor Company hired us to convert one of their die cast plants from oil to NG. Then they discovered that in the winter, they couldn’t get enough NG to melt the ingots. So, we hooked them back up to oil. I don’t know, maybe the pipe lines are larger and more plentiful now. I for one am afraid of NG. But then I am also afraid of young women (60 and younger).

“But then I am also afraid of young women (60 and younger).”

That’s just good thinking my friend. No point taking unnecessary chances.

Bob, the price of oil will HAVE to go up “eventually” because no one can produce below the cost of production forever. But no one knows when this “eventually” is. As we learned from natural gas, this “eventually” can be a lot further in the distance than expected.

Dan Dicker’s point pretty much agrees – except that perhaps his time frame for a price recovery is shorter. Hence, he may underestimate the damage this bust will do to the companies in the sector. But when the “eventually” arrives, the survivors in this industry will be huge buys. He and I both agree on this.

Hate to disappoint but price of oil will NEVER ever go up again to $100 because we will get fuel from sand, YES SAND. This is already in development stages and almost ready to burn. Now tell me what oil will be worth in such situation? Yes, big oil companies will fight this and they do it as of moment we speak but the future is in the sand not oil. That is why Saudis drive price down and it will stay where it is for foreseeable future. That’s why Saudis want all Arabian peninsula for themselves and finance destruction of all Arab countries around. Sand is worth more then gold these days, believe or not.

Sand is worth exactly what it’s worth these days – namely the price of sand. Sure, if you get enough tons of sand together, it might be worth an ounce of gold.

At this point, there is no real replacement for oil as a transportation fuel. Sure at the edges, there are some replacements, like CNG, LNG, coal liquefaction, electric vehicles, etc. But oil is still it. Without it, our economy comes to a standstill. So the price of oil will eventually go up far enough to be produced profitably in sufficient quantity. No way around this. It just might not happen very soon, and i don’t know where that price is on a global basis.

This is probably the most amusing post on Wolf Street, so far.

d’Cynic,

You don’t know the discipline it took to avoid posting a youtube of that bit from Sam Kinison

“… its Sand! Ahhh! Ahhhhhhh!”

One just can’t have adult conversations with some people.

Regards,

Cooter

The price will stay low until a major event in the ME or an orchestrated shortage rumor in the US. There is no economic machine to draw down the surplus.

Wall Street investment firms are like drug lords; they will keep the zombie drillers addicted until dead.

I suspected oil would have found a floor at around $45/bbl but I am beginning to suspect that soon it will test the $40/bbl floor.

I started having this suspicion when I learned China is running out of storage capacity… quite an incredible feat considering how much capacity they added in the past five years or so.

If China runs out of her own excess capacity, that’s extremely bad news for oil producers. It means not just that there’s still a glut in supply but demand from China simply isn’t growing.

To make matters worse, the battle for market share between Saudi Arabia and Russia taking place in Europe is nothing compared to what is taking place in China. Right now Russia has a very slight edge over the Saudi, which could become a very definite edge once the new pipelines between the two countries are completed. I very much doubt the Saudi will simply idly sit by.

Which leads me to the next problem: Iran.

Iran’s oil industry is mostly old and degraded and would need massive investments to be competitive with Saudi Arabia’s. But if Iraq is anything to go by, that’s not such a big problem: Shell, Total, BP and ENI have already sent delegations to Teheran to meet with Iranian officials. Rosfnet and Petrochina personnel is already on the ground. The moment sanctions are lifted, investments will start pouring in and the ayatollah will open the tap as much as they can: even oil under $50/bbl is a good deal for Iran, which is starved for sorely needed hard currency.

And this is to say nothing of natural gas, of which Iran has truly enormous reserves.

Iran could easily wreck Saudi Arabia’s and Iraq’s plans for dominance in Europe: as soon as tankers loaded with their crude start leaving ports they could look at gaining a 10% share in less than a couple of years easily. This share would come right out of Iran’s own neighbors.

A while back Shell warned the present “imbalance” on oil markets could last well into 2020. That’s an awful long time during which a lot of things can happen. For example if battery-powered electric engines became more competitive with diesel and otto cycle ones, demand for oil would surely start to wane. And if central banks would just stop playing God, the long-awaited liquidation of malinvestment, with associated reduction in commodity consumption, would finally kick in instead of leaving us gazing nervously into the future to see if a devastating crash is ahead.

$100/bbl oil derivative contract, anyone?

Anyone?

Bueller? Bueller?

Re: the long death spiral of nat gas: it was prolonged by being able to get oil from the gas, depending on the type of gas. But then oil collapsed.

One thing to keep in mind -the crash in nat gas is old news.

The crash in oil is recent- in fact Mexico I see is about to get a huge check from Goldman and frenemies for about 6 billion for production they hedged at 80 or so.

A lot of people hedged but they are all running out now.

So you can’t start your death- watch clock from the time the spot price crashed- you start it when the hedges run out, now-ish.

Second thing that hasn’t happened yet under the new 45-50 price – the banks are just about to start year- end assessment of credit, and valuing reserves. i.e. huge write downs are about to happen.

So to sum up the first part of this comment- I think the appearance that the death spiral can go on for ever was due to factors that are ending.

A big question is how much of the lenders’ patience is self- interest. The officer who ok’d the loan is motivated to ok the extension. Some of these banks may feel their existence threatened if the fracker goes under- so let’s keep him alive.

This goes on until a bank examiner takes over.

Was it Penn Central sunk by nat gas loans?

One puzzle re nat gas. Alberta, is under intense pressure to produce less green house gas from oil ( not tar!) sands etc.

It still produces about half its electricity from coal.

It is and always has been awash in nat gas. ( Once had 4000 wells capped)

So just switch the coal plants to nat gas.

Then net net you can say you’ve cleaned up your act.

I see Obama has had more to say about dirty oil sands oil than about Kentucky coal.

Guess there aren’t many votes to be had (or lost) in Alberta.

Just read the piece again and was reminded that this whole oil crisis is literally only a year old- Nov. 2014 was the Saudi announcement.

I just posted saying it hasn’t been that long but didn’t realize it was that recent. There may still be a few hedges in place.

So as I’ve been saying to optimists ( bulls) who say crash? what crash?

If the locomotive of a long train goes of a bridge, it takes time before it affects the caboose.

This “increasing production as prices fall” phenomenon seems to be playing out here in British Columbia too, in the forest industry.

Perhaps I’m wrong and lumber prices are in fact soaring due to the US “housing recovery”…but from all the charts I’ve seen lumber prices are beginning to decline rather precipitiously…

I’ve noticed the number of raw log-loading ships bound for the Orient has slowed. I’ve also noticed ‘high-grading’ of timber resources by companies. They’re desperate…extracting mere fence-post size logs from marginal areas very rapidly. Scores of logging trucks on weekends too…a bit unusual…and more of them.

This dynamic is probably playing out in the mining industry and other areas too…thanks to central bank and government counterfeiting.

IMF says Saudi Arabia had enough cash reserves to keep flooding the market with $40 oil until 2020, and other OPEC countries even longer. Meanwhile, US energy companies are already spending 85% of operating income on debt service.

Kreditalstan,

Where do you hail from? Up on the north Island Western Forest products is absolutely laying rape and pillage in the woods. They have also regressed employment standards back 20 years in their bid to cut costs. Brutal.

regards

Paulo, mid-island.

I’ve no objection to cutting employment standards (standards of living HAVE to fall) but remember that these forest-mining companies are subsidized by the government (the public) with virtually free monopoly access to land and timber.

They either have massive debt loads, massive cash-flow problems or massive fixed costs so they are running a lawnmower through the woods in a desperate effort to keep new money coming in.

Because of that, the companies are actually zombie entities, albeit out in the open even in daylight…and they’re becoming even more insolvent as lumber prices fall.

“They either have massive debt loads, massive cash-flow problems or massive fixed costs so they are running a lawnmower through the woods in a desperate effort to keep new money coming in.

Because of that, the companies are actually zombie entities, albeit out in the open even in daylight…and they’re becoming even more insolvent”

And that right there succinctly describes our economic future in “western” markets. First consumers maxxed out, then businesses, and finally government. Once maxed out, every entity is so loaded up on debt there will be mana for anything but debt service – and without growth in debt (i.e. contracting credit), there is no hope to pay anything back.

Defaults and deflation.

Regards,

Cooter

The price of oil is “doomed”

What is the matter with you? There are countless billions upon Planet Earth who are thankful that the price of oil is coming down. And yet you say the price (descending) of oil is “doomed”.

I just think you don’t even understand the words coming out of your mouth (or off the end of your fingers) sometimes. You just simply don’t know what you’re saying.

I feel sorry for you.

Wolf, I dont understand your “the price of gas is below the cost of production” If you own a producing well, the cost of production is zero. I think you mean the cost of NEW production. As is implied in the article, the cost of new production is a function of interest rates. But, if demand for the product is declining below the depletion rate the need for new production is zero. So, in a period of declining demand, the cost of production will stay low for ever. It is just a matter of demographics. Fundamentally, the birth rate drives!

RH,

There are numerous costs incurred in producing natural gas wells and they are referred to as operating costs. Royalty payments, well work-overs, possible recompilation, gathering system costs, produced fluids disposal, just to name a few. A well site is like a small manufacturing plant. Depending on the type of gas being produced, there are several pieces of expensive equipment required onsite. The equipment has to be maintained, repaired and sometimes replaced. Personnel costs as well.

Invest as a working interest in a well and take a look at your accounting statements. The well operator even charges you for the toilet tissue in their bathrooms. First thing I learned in the oil business: Never take a working interest. Always take an over-riding royalty.

One well-placed anonymous “terrorist attack” near Ghawar could change the whole situation overnight. And trust me, there are people crazy enough from every faction, from the Pentagon, from ISIS, from the Kremlin, from Ankara, even from Caracus, to do such a thing …

Like I’ve said before one of the few reasons why it isn’t already at $25/bbl is because so much of it sits underneath people who are nuttier than a squirrel turd.

The oil price decline is just the early stage of a cold war between Saudi Arabia and Russia/Iran. Do you really believe that Putin will allow the his power to be destroyed by $20/barrel oil, or will the war turn hot before that point?

There is no sustainable hope for natural gas above $2/MMBTU, and this will continue to be a drain on oil demand as oil and gas compete in chemical feedstock, heating and other markets.

In a combustion turbine, natural gas at $2/MMBTU is a fuel cost of about $23.5/MWh. This means that as wind and solar approach all-in PPA rates of $23.5/MWh, they beat natural gas on fuel price alone and leave no additional revenue to cover NG generator capex or other marginal costs. This is a price point at which even fully depreciated plants can no longer compete with brand new wind and solar capacity. Thus, we will see massive destruction of demand for natural gas as PPAs descend to this level and go even lower.

How long will this take? Recent solar PPAs have been in range of $40 to $50 per MWh within the US. The cost of solar should continue to decline 10% to 15% per year. So solar could reach $23/MWh by 2020. Wind PPAs are already in ranger of $25 to $40 per MWh in the US and can continue to fall 5% or more per year. Thus, wind at $23/MWh is imminent. The cintinuing decline in the cost of solar and wind is based on advancing technology and manufacturing and supply chain efficiencies that come with doubling production ever couple of years.

Moreover, Tesla now prices their Powerpack 100kWh battery at $250/kWh. This is sufficient for SolarCity to price a utility scale dispatchable solar facitity capable of storing all its energy to be dispatched after dark at $145/MWh. This beats a new gas peaking plant with $160/MWh LCOE with natural gas at $2/MMBTU. Battery costs should fall just as fast as solar. So fully dispatchable solar should fall below $70/MWh. Thus, dispatachable solar and other applications of battery will out compete gas peakers very soon. This deprives natural gas pretty much any longterm market in stabilizing the grid except perhaps to address seasonal demand. The presence of sufficient batteries in the grid will impose an arbitrage bound on the daily spread between high and low electricity prices. That arbitrage bound shrinks with the price of batteries and other storage technology. So longrun any grid stabilization demand for natural gas shrinks with each passing year. It will be cheaper to stabilize the grid with batteries.

The problem with natural gas prices above $2/MMBTU is that it simply hasten the rate at which wind, solar and batteries are brought into the grid. Once installed, these assets will permanently destroy demand for natural gas. For example, this year the US will install about 5 GW of solar, and that is enough to displace demand for 82 trillion BTU per year for the next 30 years. And in 2016, the US will another 7 to 9 GW of solar. If gas prices were to recover to $3/MMBTU or higher next year, that would only boost solar and wind installations even higher in 2017.

Any investor who is looking for a floor for natural gas, coal or oil will need to give serious attention to where floors might exist for wind, solar and batteries. As far as I can see there are none, and these new technologies will continue to exert deflationary pressure on all energy markets for decades to come. Wind, solar and batteries are the black hole of the energy markets permanently sucking demand away from coal, gas and oil. The only thing in question is the pace at which demand is destroyed, and this is why the Saudis had to allow prices to fall.