One of the attributes of this oil market is its incredible ability to breed selling as it goes lower.

Dan Dicker, Oil & Energy Insider:

One of the incredible attributes of this oil market is its ability to breed selling as it goes lower, precisely because it puts more and more of US and Canadian production at risk. How much at risk? Most of my pessimism on oil as it nears $60 a barrel is contained in the answer to that question and what I see as a major smoke job that’s being done by many of the smaller and mid-cap oil companies and the analysts that follow them. I say “There Will Be Blood” – and their distress is not being correctly measured yet.

Let’s take two interesting updates this week – Conoco Phillips (COP) updated with a capital expenditure slashing for 2015 of almost 40%, yet they are claiming that their production will increase by 7% next year. Oasis Petroleum (OAS), with production far more reliant on short-term capex than Conoco similarly updated by cutting their spending budget in half, yet still claiming to increase production by 10%.

Who’s zooming who? Production increases with cratered budgets? These claims and others inside the distressed oil sector just don’t jibe – capex and production growth is only one of them. You can see the self-deception in several moves of the executives of these companies, from Harold Hamm’s mistimed retirement of his short hedges, to the major share repurchases from RIG and others.

The hope of these re-investments are twofold: Either the oil price – which IS, in fact, unsustainably low – rallies back to a better break even level for many of these players before the balance sheets become irretrievable, OR, the price of oil drives the well-financed majors to swarm around cheapened assets and start buying.

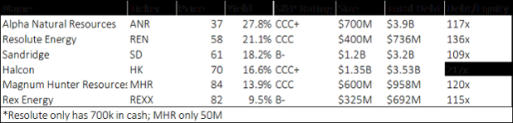

But the real Russian Roulette being played is in the debt positions of these smallcaps and midcaps. Looking at the bond to cash flow positions gives a truer and direr outlook. Here’s one look at some of the worst of them, courtesy of my friend Jim Cramer’s Mad Money research staff:

Truly, we’re looking at a very partial list of the walking dead here, for whom the often bandied about ‘breakeven’ price for crude oil has no meaning: The burden of extreme debt service is far more onerous to survival – in some cases as much as $15 a barrel.

It gets worse. The game for many of these oil companies now is to merely survive and capex reductions won’t get them there alone. They’ll also need to find some refinancing of debt or some other borrowed capital just to keep the drilling going and the doors open. Trouble is, I’ve heard from several sources that revolver credit lines are being retracted by many of the smaller banks on Force Majeure clauses, and being renegotiated based upon $40 oil prices. In other words, the circling of the vultures has already begun.

Let me be clear: The death rattles I hear are distinct only in these marginal, badly capitalized and over-leveraged players. I believe that other E+P’s are providing generational opportunity and will not only survive, but come out the other end of this downturn stronger.

But, am I being overly negative in the ones I view as at terminal risk? No, I don’t think so – I think the bloodletting has only begun. By Dan Dicker, Oil & Energy Insider the Oilprice.com premium publication

Wall Street made a killing on the fracking and offshore booms, but now the tide turns. Read… Oil Bust Contagion Hits Wall Street, Banks Sit on Losses

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()