With impeccable timing – on Halloween, which is increasingly popular in Japan among adults who are trying to escape their reality – Bank of Japan Governor Haruhiko Kuroda formally announced that he’d cure Japan’s economic and fiscal ills by resorting entirely, and not just partially, to “monetary shamanism.”

That’s what Izuru Kato, an economist and president of Totan Research, calls Kuroda’s dubious strategy. Japan practiced QE before it ever become a term in English. With predictable results: it did nothing for the economy but triggered unbridled government profligacy that generated ever larger budget deficits and an insurmountable mountain of debt.

But the QE that the BOJ has unleashed since April 2013 isn’t just QE anymore. It’s QQE: quantitative and qualitative easing. No-holds-barred QE. So in the true spirit of Halloween, Kuroda promised that the BOJ would:

- Increase the monetary base by ¥80 trillion annually (over 16% of GDP!), up from the previous commitment of ¥60-70 trillion. In a few years, its balance sheet will exceed Japan’s GDP.

- Increase its JGB holdings by ¥80 trillion annually, up 60% from the prior insanity.

- Lengthen the average remaining maturity of its JGB holdings to 7-10 years, up from the current goal of 6-8 years. Before Kuroda arrived at the BOJ, the average maturity was under 3 years.

- Triple the annual purchases of ETFs and J-REITs.

- And keep doing all of this until hell freezes over.

The goal is to demolish the yen, savings, real wages, people’s wealth, and that onerousness mountain of debt, much of which will end up on the BOJ’s balance sheet in a few years. And it seems to be working.

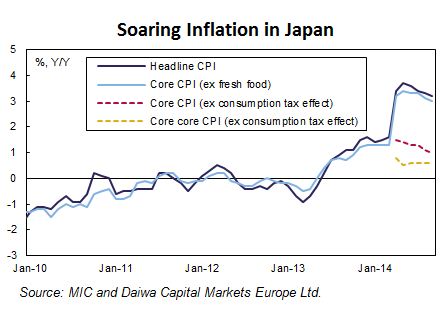

As planned under the economic religion of Abenomics, inflation has roared higher. In September, prices were up 3.2% compared to a year ago, with goods prices up 4.6% and service prices up 1.9% (service providers are so pressured by struggling consumers and businesses that they’re eating the 3-percentage-point consumption tax increase rather than passing it on). Here is what that inflation looks like:

Unperturbed, the BOJ uses its own and more convenient measure of inflation, taking out just about everything that adds to it, such as food, energy, and the impact of the consumption tax increase, to come up with a new and much tamer price index – the yellow dotted line in the chart above – which is still too low and has to be jacked up further.

But wages aren’t rising, so households – which do have to pay for food, energy, and the consumption tax hike – are having a hard time making ends meet. And the increasingly numerous retirees are losing purchasing power and wealth as their savings are being devalued. They’re all coming to grips with the scourge of Abenomics: “inflation without compensation.” It boils down to this, as the Statistics Bureau reported today with equally impeccable timing: In September, inflation-adjusted household incomes plunged 6.0% from a year ago.

And demand? Average monthly inflation-adjusted consumption expenditures by two-or-more-person households plunged 5.6% from a year ago. It’s the sixth month in a row that expenditures and incomes have plunged in this manner.

The Bank of Japandemonium at work in all its glory!

Its announcement was also impeccably coordinated with another hocus-pocus announcement, this one by Japan’s Government Pension Investment Fund (GPIF). It confirmed that the mega-fund would slash its holdings of Japanese Government Bonds (JGB) down to 35% of its ¥127 trillion in assets (from 53% at the end of September). The fund will dump its JGBs at a pace that is slightly below the additional purchases by the BOJ. This way, everything remains under control. The market only gets involved for the sake of appearances. Beyond the charade, the GPIF will hand its JGBs to the BOJ.

But then the GPIF will plow the newly liberated funds into the stock market to buy up domestic and foreign stocks and foreign bonds – by June! This announcement has been made in various forms for months. Each time such verbiage hit the news, stocks jumped on cue, which was the sole purpose of those announcements.

With the total commitment to monetary shamanism artfully pronounced on Halloween during Japan’s trading hours, pandemonium followed. The Nikkei stock index instantly jumped 5%. The yen collapsed by over 3.5%. In one fell swoop, it cut a big chunk out of the still considerable yen-denominated wealth of the Japanese. And JGB yields dropped further.

It is now perfectly clear that the Bank of Japandemonium has imposed a yield peg, which it continues to tighten. There will never again be a market-based yield for JGBs. Whoever bought them originally will get their money back eventually, but that money will be worth a lot less than what it was worth yesterday. In the interim, they will not earn any measurable yield. And shorting them is useless because the BOJ will simply buy every one that isn’t nailed down.

There is no exit. In a few years, the BOJ’s balance sheet will reach the size of Japan’s GDP, but it won’t be able to stop there. It can never allow the market to set the yields. It would instantly bankrupt the country. Politicians and the Japanese economy have already become totally addicted to government deficit spending and can’t shake the habit. But they know they don’t have to; the BOJ will just print the money.

And the BOJ socked it to foreigners who thought they could make a lot of money in Japanese stocks and then convert their gains into dollars. The destruction of the yen will see to it that those gains will be minimal. Worldwide, markets rallied after the announcement, in anticipation of what? True financial pandemonium? Because that’s what this sort of monetary shamanism will lead to.

By comparison, and only by comparison, the Fed has been practically tame. But the impact of its policies since the financial crisis are now clear: for individual Americans, economic “growth” has meant the opposite. Read… That Shrinking Slice of a Barely Growing Pie: Why the Glorious Economy of Ours Feels so Crummy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Paul Craig Roberts might say (he hasn’t said so, I’m just guessing he might say) that the Japanese monetary policy has been cooked up by Washington. And I’d tend to agree with him.

Nearly everything PM Abe is doing looks like assistance for Washington’s “big plan” (as Paul Craig Roberts has spoken about): 1) Changing the constitution to make the military an offensive force 2) Buying military hardware and defense systems from American companies 3) Japan’s “new” East Asia policy 4) Keeping the nuclear reactors going and 5) Pushing TPP.

I hope that Japanese are reading WolfStreet dot com. They really need to!

Maybe I should ask my wife to translate this stuff into Japanese :-) But then, there’s nothing that I’m saying that the folks at the BOJ don’t already know. These are very smart people. That’s the scary part.

Hard to believe that in the 1980’s the Japanese Yen was as low as 240Y / USD. Japan appears to be done with its’ consumer and it’s about to focus on exporting deflation again. The last time this happened was in the late 1990’s and that fall (in the yen) led to the Asian crisis. Anyone wonder what China is feeling like right now?

China should just print Yuan and buy Yens. Easy as pie.

Shocking indeed…

Abenomics and its QEs did not work so the Japanese CB chose to dig deeper into outright flawed fiscal and economic policies. Japan the sick man of Asia is out to get sicker and perhaps code blue.

Yep it ain’t working so heck let’s just double down!

Put yourself in the shoes of the multinationals operating in Japan. They’re being paid in a worthless currency, which is becoming more worthless every day. So many people/companies are willingly taking big hits in order to maintain the status quo.

Japan just robbed every bondholder, every foreign owned business operating in Japan, and its own people.

In the end though, it takes two hands to clap. People get the government they deserve. And rather than moaning about it, may as well go with the flow. I haven’t done very well on my stock portfolio given my distrust of this “recovery”, but I have done extremely well on my Yen short.

What is even worse is that many Japanese that don’t own shares. Their main asset is real estate.

Most real estate in Japan has been falling in price and will continue to do so as a result of many factors.

Demographic factors such as the ageing and falling population will ensure that there is an ample supply of real estate in many areas.

Real estate in big cities and big buildings in those cities may increase in price as a result of the monetary policy in Japan, but those in smaller cities, semi-rural ares, and rural areas will see the value of their property eroded.

With cheap yen Japan will become a real estate paradise for foreigners that have Japanese connections and a good place to live for those with foreign income or assets.

melbourne_yankee

“With cheap yen Japan will become a real estate paradise for foreigners that have Japanese connections and a good place to live for those with foreign income or assets.”

with the undeniable nuclear fallout from Fukushima that the MSM has conveniently swept under the rug for fear of pulling the populace away from the NFL, I don’t think anyone in their right state of mind would want to get anywhere near Japan, being that said fallout has contaminated the soil, air, drinking water and sea life….

just a thought

Paul Krugman’s last note was an “apology to Japan,” printed the day before this announcement, in which he stated “Japan used to be a cautionary tale, but the rest of us have messed up so badly that it almost looks like a role model instead.” God help us if this is our role model. But surely this is the endgame for the new Keynesianism. Don’t expect Krugman to admit it though – the Japanese will have done “something” wrong, one of the deck chairs on the Titanic was out of place – and this is the “right” move. It’s too bad we can’t go back and do the fall of 2008 over again. By the way, the reaction in the currency markets was indistinguishable from calamitous news out of Japan. But it’s all about the headlines!

Jackson, if you can expand this comment (double or triple in length) and post it here again, I will put it on the front page. This is excellent, and I want these thoughts to get more exposure.

I don’t think it’s much of a coincidence that gold has been hammered much lower in the last several weeks and especially this past one. This is the single biggest threat to fiat because the average person can access it, hold it and eventually use it. The Central Banks will do everything within their power and the power of their governments to suppress the true price. A run out of fiat could only occur to gold.

Unlike the decisions in the US of the FOMC, this was an acrimonious 5-4 decision of the BOJ. The dissenters know that Japan is stirring up a lot of sleeping giants around the world.

Already Panasonic has announced plans to bring its manufacturing activities back to Japan. With this move, other electronics, machinery, and car producers are very likely to follow, since a much cheaper yen will make Japanese manufacturing much more competitive than it is now. Until now these producers needed factories in the US, Europe, and China to enhance their sales. Now they can expect that the very cheap yen will be sufficient.

It is a given China, Korea and Germany will not be happy with Japan’s move here because it increases Japan’s competitiveness at their expense. The larger question is how will the US and the rest of Europe respond.

The US highly values the jobs that Japanese manufacturers have bestowed on US workers. Individual states and political subdivisions have granted subsidies and tax concessions and have incurred public debt to lure these manufacturers. There will surely be a backlash if Japan closes these factories and returns their activities to Japan. Perhaps not on a national level, but local backlashes are a certainty.

Similarly, in Europe Japan manufacturers provide much needed jobs. Their European factories have also been built with subsidies, tax concessions and public debt. The unemployment rate in most of Europe is so high that the loss of these jobs would be intolerable. Although I expect no adverse reaction from the ECB, the affected localities will react. Their reaction may effect national elections.

I’m not convinced that shorting JGBs is “useless.” The 5-4 vote and increasing unpopularity of Abe tell you that this policy could be curtailed very quickly, and thus the current 45bp yield on the 10-year means that a short position provides great asymmetrical optionality. (You can use the ETN with the ticker JGBD, but need to simultaneously hedge the currency exposure– I combined it with YCS). I think that after Japan destroys the yen (my USD/JPY target is at least 250) it will just outright haircut the national debt by some massive amount, but as I’m unsure of the timing (this whole thing can now unwind at ANY time) I hate to give up the exposure to the bond short, especially as the convexity of a 45bp yield on 10- year paper means you really can’t lose that much. Also, keep in mind that the BOJ currently still owns “just” 20-something percent of the outstanding bonds and the pension fund that will be selling them owns far fewer than that. Thus, the vast majority of the debt is in the hands of organizations that could rush for the exit at any time, thereby overwhelming even the BOJ’s massive buying program Those organizations can see Abe’s unpopularity and the 5-4 vote as clearly as we can, and “loyal Japanese” or not, it only takes a few to decide to “get out while the getting is good” before they ALL rush for the exits.

Mark, it’s certainly possible that someday Kuroda will lose his increasingly shaky majority. And eventually, new people will move into the BOJ. And it is possible that they will try to back off.

But one thing they will never, ever do: let Japan slither into a messy, nay chaotic default. With the current debt load (increasing rapidly without end in sight), even a slight uptick in the cost of funding could have chaotic outcomes. And the Japanese hate chaos above all. They’ll default slowly through inflation and devaluation. It will be orderly. It will be hard, but people will have time to adjust. And the yield peg will remain in place, no matter who runs the joint.

The “free market” has never meant a lot in Japan. They’ve never been big fans of it. It’s something they’ve experimented with only since the bubble blew up. They’ll keep their government debt market under iron-fisted control.

That said, foreign JGB shorts, by definition, are also shorting the yen. And that’s where I would bet money is to be made.

Here is a possible scenario: the yen crashes too fast, too far. What is the BOJ going to do? It could stop printing yen and buying yen-assets, and start selling its foreign exchange holdings to buy yen and prop up it up. But if it causes chaos in the JGB market, or if yields edge up to where Japan can’t afford them anymore, they’ll back off in a second. And they’ll let the yen slide instead. That would be my bet.

So let’s say roughly 75% of the debt outstanding is currently not in the hands of the BOJ and the yen slide continues. At what point do those 75% holders– native Japanese or not– say “Screw this– I’ve got to get out before all those other guys do, because if my bank (or pension fund, or insurance company) blows up over this, I’m the guy who’s going to get the sword”?

Never underestimate the power of central banks.

The BOJ can buy ALL of the outstanding JGBs that anyone wants to sell. They’ll just bid for everything that comes on the market. There is no limit. It’s a guarantee, and because of that guarantee, there won’t be a panic. It WILL be orderly (though painful for the Japanese). There will never be a free market for JGBs.

That’s not to say that there might not be some fluctuations that would allow a nimble short to jump in and make a few bucks.

Smart people have bet against JGBs for years, based on free-market logic. But free-market logic doesn’t apply in this case. And it has been a terrible bet for that simple reason.

Okay, I’ll take one last shot: let’s say there’s a 25% chance that I’m right and a 75% chance that you’re right. (I happen to think– based on history and human nature trumping “the myth of BOJ omnipotence” that those odds are reversed, but for the sake of argument let’s say they’re not.) Considering the convexity inherent in a 10-year bond currently yielding 45bp, where does that bond price go if you’re right vs. where does it go if I’m right (keeping in mind that you can put this trade on with 3x leveraged for a carry cost of less than 3%/year)?

If you’re right, you’ll make lots of money :-)

Every bet has to have two sides. So I’m partially on the other side. I wouldn’t short JGBs, but I would short the yen.

Yes, I’m short both– the yen since the high 70s in early 2012 and the 10-year JGB since 58bp earlier this year. I think the next near-term targets are 120 for the yen and 80bp for the 10-year, but within 18 months we’ll see 150 on both. Thanks for the great dialogue– I think your blog is terrific.

IMO you’ll won’t see 150 bp on the ten year bond for a long, long time.

If you do, then the yen will more likey be at 250, the Nikkei at 4000 and the Dow matching it.