Something is changing about the perception of the Fed’s free-money policies. While we’ve lambasted them for their nefarious effects on the real economy and the inequality they produce, Wall Street, the prime beneficiary, has been bombastically gung-ho about them. And the mainstream media have praised the Fed’s “bold action,” as it’s called, at every twist and turn.

But now even Wall Street is getting cold feet. The official warning shot came from Fed Chair Janet Yellen, who admitted suddenly that “the extent of and continuing increase in inequality in the United States greatly concern me.”

Then bankers chimed in. FICO, which produces the infamous credit score, found in its latest survey of North American bank risk managers that 62% of them thought “the wealth gap poses a growing risk to the financial system.”

With the economy so dependent on consumer spending, “it makes sense that the concentration of wealth would raise flags among bank risk managers,” explained Andrew Jennings, FICO chief analytics officer. “This concern was echoed on a global scale by Credit Suisse in a recent report that found many indicators of wealth inequality are reaching levels that could result in social or political instability.”

This is a twist: Bankers, beneficiaries of the Fed’s policies that created much of the wealth gap, are fretting that that wealth gap poses a “risk to the financial system,” that it might take the banks through a another death spiral. Turns out, in our consumer-based economy, most consumers no longer have the means to adequately support that economy; and the few who have benefited from the wealth redistribution scheme, are too few to adequately support the economy.

And they fret that this inequality is “reaching levels that could result in social or political instability.” Suddenly the equation no longer works. Wall Street doesn’t want a revolt.

Now even the New York Times, the indefatigable proponent of QE and ZIRP, ran an editorial that explained how QE and ZIRP “contribute to the nation’s inequality problem.” William Cohan, a former M&A banker, quoted at length from Yellen’s inequality speech. Then he slammed into her:

Ms. Yellen’s speech seemed heartfelt. Yet, she has endorsed the Fed’s policies, started by her two immediate predecessors, Alan Greenspan and Ben S. Bernanke, that drove down interest rates to historically low levels – policies that have actually exacerbated the problem that she says she wants to correct.

She is failing to appreciate how Mr. Bernanke’s extraordinary quantitative easing program, started in the wake of the financial crisis, has only widened the gulf between the haves and have-nots. If she does understand, she certainly made no mention of it in her speech in Boston. Indeed, there was no mention whatsoever of the Fed’s easy monetary policies at all, let alone how they have helped to cause income inequality.

That this shows up in the New York Times says something – maybe that QE is becoming politically untenable, that it’s no longer cool to shove free trillions from all over the place into just one small corner of the economy. Not because it isn’t fair somehow, but because it wipes out consumers who are supposed to move the economy forward.

The anecdotal signs of consumers in trouble are everywhere. But they’re partially obscured in our statistics by, among other factors, inflation and population growth.

Retail sales in September, seasonally adjusted, declined 0.3% month-over-month, and while that was somewhat of a cold shower, retail sales have been rising. Doug Short of Advisor Perspectives explains:

The Tech Crash that began in the spring of 2000 had relatively little impact on consumption. The Financial Crisis of 2008 has had a major impact. After the cliff-dive of the Great Recession, the recovery in retail sales has taken us (in nominal terms) 16.3% above the November 2007 pre-recession peak to a record high.

But the retail sales report isn’t adjusted for inflation, and it isn’t adjusted for population growth. When we want to find out real spending per consumer to see how each consumer is contributing to the economy – that’s what we actually see here on the ground – the effects of the wealth transfer become apparent. As Doug writes, “the consumer economy remains at a recessionary level.”

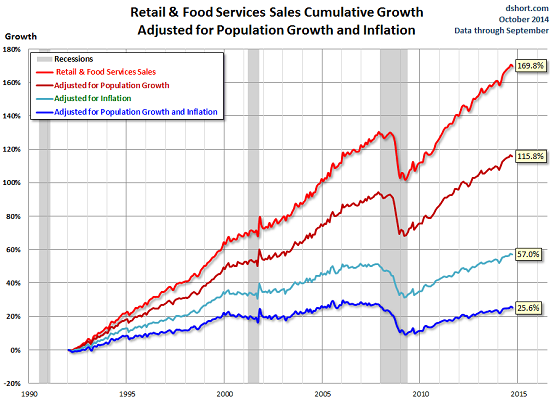

The chart below (his article including methodology is here) shows how much retail sales growth is a function of inflation and population growth.

Reported retails sales (red line, top) are up a whopping 169.8% since 1992. Fluctuations have been relatively minor, except for the collapse during the Financial Crisis. But since 1992, the population has grown 25% and the dollar has lost 42% of its purchasing power thanks to the Fed’s proudest achievement, inflation.

Now look at the stagnating blue line at the bottom: retails sales adjusted for population growth and inflation are up only 25.6% over the past 22 years. They’re now at a level first seen in December 2004!

Based on this method, September retail sales dropped 0.5% from August and are only up 1.9% year-over-year. While they’ve recovered since the horror levels of 2009, they remain 3.3% below the peak of January 2006. That’s what the Fed’s “bold actions” have accomplished.

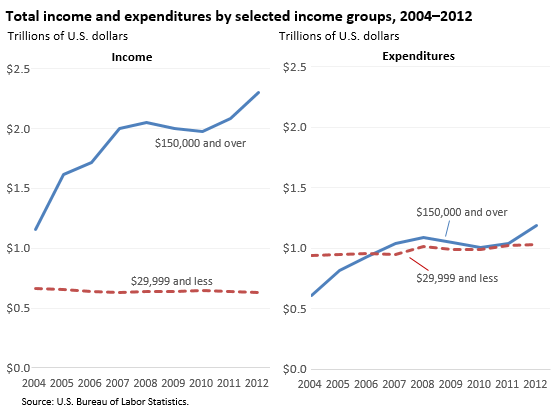

What this chart doesn’t show is the bifurcation in retail sales; but a report by the Bureau of Labor Statistics does: those at the lower-income levels, those who’ve gotten ripped off by inflation, have become terrible consumers in our economy that is so dependent on consumer spending. Note that the chart is not adjusted for inflation. If it were, it would look even more terrible.

Without thriving consumers, the American economy that is so dependent on them will continue to languish. Just adding more consumers to the mix may increase overall consumer spending, and stirring up inflation may cover up the issue. But as the majority of individual consumers falls further behind, the risks of financial, social, or political “instability” might be looking ever more plausible to those bankers.

So is the Fed now on the hot seat for its policies? Now that bankers, Yellen, and even the New York Times are showing a modicum of doubt, are these the first signs that there is finally some resistance building up? If this is the case, perhaps, just perhaps, you can kiss QE – and with a little patience, ZIRP – goodbye. And just perhaps, it’s already dawning on skittish market participants what this might do to pandemic asset price inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I bet that many in the retail sector find themselves wishing that more folks would just stop paying their student loans altogether and start throwing that money their way.

Yeah it must be tough graduating as an indentured servant.

It is obvious Yellen & market are itching for QE because Xmas is coming. They need to make sure the poor can buy things that they don’t need.

The poor need many things and can’t afford them. Yellen is right to be concerned about instability in the country. You can see the instability everywhere if you look. The one percenters should enjoy their money while they still can. I don’t think it will be to much longer.

I posted this to BI several days ago, but it is also appropriate here in this context:

We are well past the point of “fixes”, that point was years ago. The political hacks have distorted the entire economy and correcting what is wrong will not be easy or painless.

For a start, we need to stop pretending that the S&P actually matters. Let it find it’s own level, that’s what a market is supposed to do. The money that isn’t going prop up the market should be invested in our country. Our infrastructure is in appalling condition. Our roads, bridges, electrical grids, rail lines, and more are in desperate need of repair. Those repairs could not be off shored, and the jobs they create would be a huge boost to our failing retail sector.

We also need to reconsider our bartering of access to our markets as a quid pro quo for political advantage. That has led to the sour remark that we have the best allies money can buy. Sadly, it’s true too. In particular we should no longer tolerate the predatory trade practices of other countries who could barely be called trading partners let alone friends (insert your favorite name here).

There are other things too, a lot of them. But most of all, we have got to stop sacrificing our own interests in favor of others. Our defense budget is equal to the next twenty-five countries combined, and most of it isn’t even for our own defense. If our defense contractors want business, they are free to sell overseas.

well there next step to fix this will be to give money directly to the people to use to buy things and sense the fed changes the way the gauge inflation almost on a daily basis, the latest one I like . going out side to measure the growth of the moss on the side of the fed building and then multiplying that by a factor of 1000 and then moving the decimal point, and thus there will never be a interest rate hike

Didn’t GW do that when he was in the office as part of tax cut before Ebola took over? As I recall many people paid their debt rather than spend.

As for retail sales – scores of stores closing due to over-expansion also means minions surviving on close to minimum wage service jobs will soon be joining those unemployed…

There is no small amount of irony in bankers being concerned about inequality.

Let’s get real. The only reason bankers are concerned about inequality, is their growing fear of the terminal effect it will have on their necks. Eventually, as has been shown repeatedly throughout history, their necks will either be stretched by hemp or severed by steel. I, personally, look forward to finding out what banker tastes like. My guess would be chicken.

Soylent Green, Kim, Soylent Green LOL…………………….

The Fed is looking at consumer behavior wrong. They think if people since their stock portfolio rising, they’ll feel richer and spend more. Likewise if interest rates are low, they’ll borrow and spend more. Anyone with enough money to invest understands that equities are volatile and just because they’re up today, doesn’t mean they’ll be up tomorrow.

On the other hand, if I can have some of my money in fixed income assets and I see they’re producing a nice income stream, I’ll have more confidence in my financial situation and may actually spend more.

One side of the coin: low interest rates mean I can borrow more but if I’m uncertain about my job & the economy, I may not want to.

Other side of the coin: higher interest rates on my bank account, etc. means I’ll feel more secure about my financial future and may spend more.

The view the that low borrowing costs = higher spending is overly simplistic.

Interesting contrarian view. Think you have a point.

Nevertheless maybe to soon to raise interest rates but i would advise the US to replace QE with direct cash injection in highly needed infrastructure upgrades projects until inflation pick up close to the 2% target.

I suspect the anxiety about income-inequality isn’t coming from the bottom 80% peasant debt-serf class (they’ve never mattered and never will matter and don’t even know what the problem is). It’s the “middle-class” (the top 20 – 10%) noticing that the Elysium Support Class (the top 10 – 2%) are now pulling away.

Pretty soon, the “middle class” (the top 20 – 10%) won’t be able to mix their above-average kids with the (truly) above-average kids of the Elysium support class.

Oh well, looks like we’ll be going back to only the top 10% sending their kids to Yerp for a semester of “study”.

An article like this reinforces my belief that the Fed does not really decide its own policy.

I suspect that the decisions of the Fed are in fact made by insiders on Wall Street and the large banks. Those decisions are then circulated in the media. If they resonate favorably with a majority of the wider Wall Street and banking community they can be discussed and adopted at the next FOMC meeting.

If the Fed started charging modest interest some sectors of the financial community would be harmed if they retain their current positions. However, since they are forewarned, some will change their positions to avoid harm and join the majority favoring the new FOMC “decision”, or, perhaps if a majority does not yet exist their changed positions will establish the majority.

The insiders are a shadow FOMC. The people who sit around a fancy dining table for 2 days are merely fronting for them and pretending to make policy.