America is on the verge of becoming a natural gas net exporter in a year or two. It can relieve energy-starved Japan from extortionary prices and free Europe from the clutches of Gazprom. A number of liquefied natural gas (LNG) export facilities on the Gulf Coast and on the West Coast have been approved, are under construction, or are in the pipeline, so to speak. Untold riches await daring investors.

Or so it would seem, according to the hype, often as thick as San Francisco fog in the summer, that has shrouded the segment of the industry. Some stocks of companies hoping to ride that LNG export boom are soaring. Billions, mostly borrowed from unsuspecting or blind lenders of one type or another, have already been spent, and many more are going to be spent, on highly capital-intensive LNG export terminals.

For example, Cheniere Energy which by now is famous for producing ever increasing losses on declining revenues: in 2013, it generated $507 million in losses on $267 million in revenues – which is quite a feat! The losses are up 156% from 2011, while revenues are down 8%. It now has $9.5 billion in debt, up from $3.3 billion in 2011. Its stock price soared from penny stock in 2003 to over $40 a share in 2006 and 2007, before it revisited the penny stock purgatory in 2008. Then in 2012, the LNG export hype began wafting around its operations, and the stock soared again, and it recently spiked, and closed today at $72. It’s been one heck of a ride.

How can this insanity occur? Consensual hallucination. Analysts, hype mongers, company pronouncements, free money from the Fed, and willing traders or investors – all are part of it. For them, the outfit is a highly leveraged arbitrage wager on the difference in natural gas prices in the US, Japan, and Europe.

In the US, natural gas prices in electronic trading are currently below $4 per million Btu. In Europe they’re more than twice as much, in Japan more than four times as much. But processing natural gas into LNG in the US and transporting the LNG from the US to Europe or Japan is going to eat up a chunk of that price differential.

So the stock is a nose-bleed bet that the price in the US will remain this low, and that prices in Japan and Europe will remain high, and that contracts are signed to reflect these price differentials for years to come.

This assumes that there will be natural gas to export.

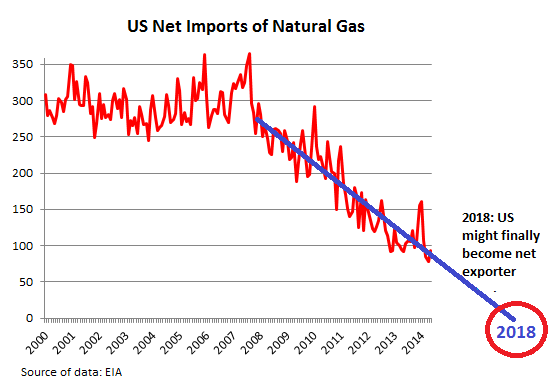

But there has been a hiccup: the US is a natural gas net importer, still, despite years over “over-drilling” and a presumed natural gas “glut” that whacked the price below the cost of production, where it still languishes today.

The US currently exports natural gas via pipelines to Mexico and Canada, but it imports even more natural gas via pipelines from Canada (in addition to a small amount of LNG from overseas). The chart, based on the EIA’s latest data through May 2014, shows the net results from the drilling boom: the US remains a net importer of natural gas.

So what natural gas exactly are these LNG exporters going to export?

Currently, US production doesn’t meet domestic demand. Period. The hole is filled with imports from Canada. Large-scale LNG exports remain a pipedream for the moment. Unless a miracle happens, and they’re unlikely in the oil and gas business, US production might meet domestic demand without reliance on imports by 2018. And if production continues to grow beyond that, the US might eventually produce enough to become a net exporter of significant quantities of LNG.

But there has been another hiccup: Drilling for dry gas has been grinding to a halt. By last week, only 313 rigs were drilling for natural gas across the country, down from 1,606 in September 2008.

Production is up, but these production increases come mostly from the Marcellus shale where an enormous drilling boom over the last few years left thousands of gas wells without pipeline connections. Now that the pipeline infrastructure is catching up, take-away capacity is rising. Gas that is taken to market is counted as “production.” But many of those wells that are now responsible for the increase in production were drilled years ago.

Yet drilling activity – that is, future production – in the Marcellus shale is a shadow of its former self: In January 2012, 143 rigs were drilling for gas; in the most recent week 77 rigs. Fracked wells have steep decline rates. And after 18 months, production has petered out to only a small fraction of initial production. Once the steep decline rates catch up, production in the Marcellus is going to taper off.

Only a new drilling boom could re-launch production.

And there we have a third hiccup. The current price is simply too low to justify fracking for dry gas, though if the well primarily produces oil and natural gas liquids, which sell for higher prices, and dry gas is merely a byproduct, the equation is less dreary. So for that new drilling boom to take off, the price would have to be significantly higher.

Hence the fourth hiccup: these significantly higher prices of natural gas in the US that would be needed to restart the drilling boom also destroy the highly leveraged arbitrage bets that LNG export investors are counting on in the first place. But consensual hallucination allows for no doubts and no paradoxes. Reality no longer matters. What matters instead is the Fed’s limitless, nearly free money and the plentiful availability of corporate and Wall-Street hype.

Drillers that have joined the fracking boom in the US have stepped into a toxic mix. Read…. Where Money Goes to Die: How Fracking Blows Up Balance Sheets of Oil and Gas Companies

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I confess that I bought into the hype in late 2012 after reading news like “Cheniere Energy Partners LP (CQP -2.27%) reached an 20-year deal under which Total SA (TOT, FP.FR), the France-based energy major, has agreed to purchase nearly half the volume of a fifth train planned for Cheniere’s liquefied natural-gas export facility that is being developed in Louisiana”.

As recently as this June Credit Suisse had it rated “outperform”.

This is held in a taxable account to generate income so selling would be problematic for me. I’m just toddling along with a trailing stop and collecting my checks, but this is one tiger whose tail I wish I’d never grabbed.

Hype makes participants a lot of money for an astonishing amount of time. That’s why it exists. And if we buy at the right time, congrats. But what happens afterwards? There is a good chance LNG will return for a third time to penny-stock purgatory.

So the question is: when do you get out? When everyone else is getting out?

If Europe keeps messing with Putin, he can shut off the gas pipelines. America has assured that it can come to the rescue if that happens, but it looks like an empty promise, doesn’t it?

What the overoptimistic prognosis likely will do is open up the US market, even if the US will remain a nett importer. But in a negative way for the US consumer.

Canadian etc producers that are now fully relying on the US, have to hedge the possibility that fracking actually does work and asap. Meaning create export possibilities.

And from the moment they can export to 8 USDplus markets nobody will be really interested in selling to the 4 USD US market.

Which means imho that unless fracking really starts to work prices in the US will go up. Same demand less supply.