One of my readers sent me an email with questions about Abenomics and how it might end. He’d been reading my Japan articles, including my posts in the right sidebar – Rumblings from the Pit – where I discuss economic data as they bubble up from Japan (but also from the US, China, and Europe), usually in irreverent, one-paragraph bursts, taking neither the numbers nor myself too seriously.

“It looks to me that you don’t think Abenomics is working,” Andrew wrote, followed by a slew of tough questions and a comparison to Kyle Bass, who has been betting on a “full-blown Japan crisis.”

It got me thinking (which is always trouble). I’m attached to Japan in many ways. What started in 1996 has turned into a complex relationship with many ups and downs. I used to live there, my in-laws (yup, it eventually came to that) and many of our friends live there. I love Japan when I’m not there, but when I’m there, I love it too, particularly the people I know, but it can be the most frustrating place on earth. Something to remember when it comes to shorting JGBs.

Part of that experience made it into my book, BIG LIKE: CASCADE INTO AN ODYSSEY, a “funny as hell nonfiction book about wanderlust and traveling abroad,” a reader wrote. Another reader called it “a wonderful reminder of how bubbles get created and evaporate… a must read for everybody trying to understand the enigma inside the riddle of Japan.”

There isn’t a single day when I don’t think about Japan. Because I’m worried. And now that Abenomics has become the religion of salvation, I’m even more worried. So here are some of my thoughts – while they might not answer all of Andrew’s questions, they might answer some, and give him the material to answer the rest.

Japan has three majestic problems of a scale that no other developed country has ever come near: its budget deficit, its debt, and a pandemic unwillingness to pay for it. Japan also has a number of other problems, such as offshoring by manufacturers, an aging workforce, protected markets that make many items still too expensive, an inefficient system – efficiency being culturally pooh-poohed – and the like, but countries can adjust to those or remedy them.

Japan’s Three Majestic problems

The debt. In June, its gross national debt exceeded for the first time ¥1 quadrillion: ¥1,008.63 trillion (about $10.5 trillion), up ¥17 trillion from the prior quarter. With a nominal GDP of ¥475 trillion in fiscal 2012 (ended March 31), Japan’s gross national debt is a phenomenal 212% of GDP. Unlike Japan’s other problems, this problem can no longer be remedied without devastating costs. It’s too big, they waited too long, and they’re still making it worse.

The deficit. For this fiscal year, ending March 31, 2014, parliament passed a budget of ¥92.6 trillion ($962 billion). That was May 15. By July 23, Finance Minister Taro Aso was already bandying about a “supplementary budget” – a stimulus package. Parliament has been voting for them about two to four times a year. By the time the stimulus packages and accounting gimmicks are added into it, the government will likely end up borrowing nearly half of its outlays. Years of near-zero interest rates and quantitative easing before the term had even been invented taught the government that it could borrow forever without limit. And that it would work out somehow, for the generation in power.

A pandemic unwillingness to pay for it. Japan is a corporate and individual welfare state. Just about everyone benefits. Large corporations are coddled to the nth degree. Individuals have benefits such as universal healthcare that costs them almost nothing, by US standards. There are countless such programs. But no one wants to pay for them. The consumption tax increases that were passed last year to take effect in 2014 and 2015 were so unpopular that they contributed to the downfall of the Noda administration. Prime Minister Shinzo Abe has been non-committal, and they may never take effect. The economy has become physically dependent on the stimulus that these huge deficits provide, and Abenomics gurus are worried that paying for some of it would derail economic growth. But even with the consumption tax in effect, the debt will simply get worse and worse, just more slowly.

For the Rest, it’s a mixed bag

Moderate Government spending. The OECD estimated that in 2010, government spending amounted to 27.6% of GDP. Compared to other developed countries, Japan ranked in the lower end of the group. At the top was Denmark at 47.6% [my take with a graph of those 34 countries, including the US … From Tax Hell to Tax Haven].

Using Japan’s own figures, with a GDP of ¥475.6 trillion in 2012, spending by the central government alone accounts for about 19.4% of GDP, which is relatively low. One reason: it spends only a minuscule amount for defense. The US imposed “Peace Constitution” doesn’t allow Japan to maintain a military, and the Self-Defense Forces are a low-budget affair. Instead, the country relies on the US defense umbrella, at the expense of the American taxpayer.

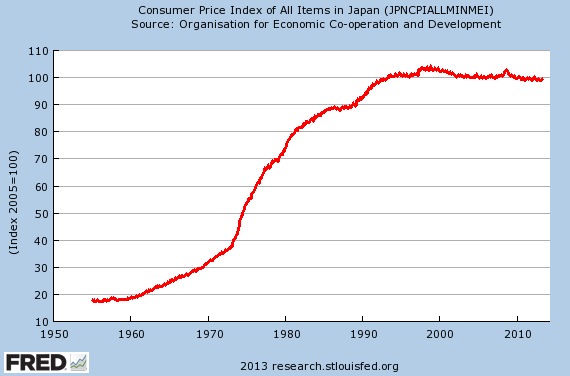

The Infamous “Deflation Spiral.” Without further comment, I present this graph from the St. Louis Fed, tracking Japanese inflation since 1955.

OK, I’ll comment. Since the early 1990s, so for about two decades, Japan has maintained true price stability – not the Fed’s type of “price stability” with nasty bouts of inflation hidden underneath soothing jargon. In Japan, for two decades, periods of slight inflation were followed by periods of slight deflation. That’s not a problem but a strength! The “deflation spiral” that over-indebted Western mainstream media empires and Fed apologists throw around is baloney.

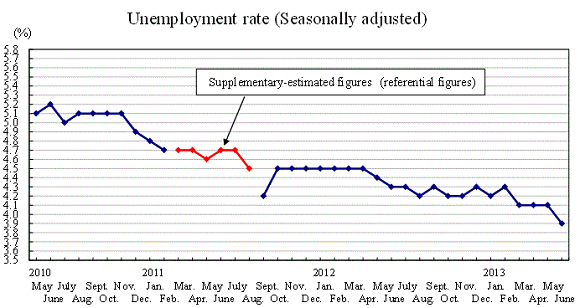

Low Unemployment. There are problems, and once people fall through the cracks, there isn’t much of a safety net for them, and like in the US, Europe, and elsewhere, the raw numbers are beaten with statistics until they make sense. Nevertheless, they’re a measure that is comparable to what is going on elsewhere. In June 2010, the unemployment rate was 5.2%, high for Japanese standards. In June 2013, it was 3.9%.

So, there are a few flies in that delicious soba. The percentage of the nation’s young people not in education, employment or training, the “NEET,” reached a record of 640,000. They’re often thought of as people who are unwilling to work or go to school – Japanese society has little patience with this sort of thing. A bit of youth bashing by the older generation that obscures some real issues, including hiring practices, an infernally rigid system, and a disdain for individuality.

At the other end of the spectrum are people who are going to work but with nothing to do, be it older workers who get shuffled off to window jobs, or younger workers, now dubbed “corporate NEET,” who go to work and play video games. Labor rules allow companies to fire people only under strict conditions (unless they’re temporary workers). It’s sort of a social contract: companies pay for labor problems, instead of the taxpayer. Not a perfect solution, not for the employees whose careers decompose before their very eyes, and not for companies that are trying to be competitive and flexible. Abenomics is trying to address this. Since there is no broad unemployment safety net, diddling with one side without fixing the other side may have catastrophic consequences. But overall, compared to Western countries, unemployment is not a problem in Japan.

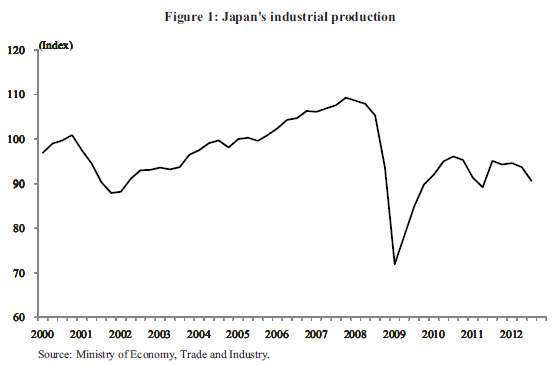

Rampant Offshoring. The Bank of Japan published a study to find out what was going on with Japan’s dreary industrial output trends. Offshoring turned out to be one of the big culprits. Companies, faced with “a deterioration in global competitiveness,” shifted manufacturing to plants in other countries. Part of the problem was the strict labor law. But the push to offshore accelerated due to the supply chain disruptions caused by the earthquake in March 2011. In addition to the reasons in the BOJ study, there is another powerful strategic reason: companies want to be closer to their customers. This graph from the study shows the results:

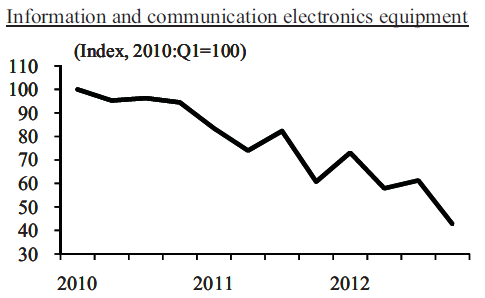

Since 2010, production of information and communication electronics equipment, formerly one of Japan’s glory industries, plunged by more than half in three years!

Rapidly deteriorating trade deficits. Japan has entered a new frontier. In terms of trade deficits, June was the worst June ever, May the worst May ever, April the worst April ever, and so on…. Fossil fuel imports jumped since the nuclear powerplants were taken off line, but it’s not the dominant factor. The structural problem is offshoring. Now Japan imports products that used to be manufactured in Japan.

Abenomics attempts to debase the yen to make exports cheaper and discourage imports. But the opposite is happening: imports, now required for structural reasons, are more expensive in yen, and thus a larger drain on the economy. At the same time, the strategic reasons to offshore production don’t just disappear when the yen drops by 25%. And corporate profits rise as profits from products built and sold overseas are converted into a weaker yen. Looks good on paper. But it rewards corporations for producing overseas.

A mountain of foreign exchange assets. After decades of running now fondly remembered trade surpluses, Japan has accumulated a war chest of $2.4 trillion in foreign exchange assets, including $1.3 trillion in US dollars, at the end of 2012. This is a huge resource for Japan, and it will come in handy as Japan’s debt will attempt to get a life of its own. But even that resource pales compared to the challenges ahead.

There is no good solution. Deficits and debt, and the economy’s dependence on deficit spending, remain by far the largest problems Japan is facing. Over 90% of the debt is held by Japanese banks, retirement funds, insurance companies, and other Japanese institutions, including increasingly the Bank of Japan, along with Japanese investors, directly or indirectly. This internal ownership gives Japan a lot of control. Japan is an insular cohesive society, and practically no Japanese wants JGBs to collapse in value. A short faces a powerful and united opposition.

Much of the country’s wealth is invested in these JGBs. So every effort will be made to maintain their “value.” For example, based on a communal decision, Japan could refuse to sell JGBs beyond what the BOJ is buying. When push comes to shove, the BOJ could institute a peg – say, 2% on 10-year JGBs – and buy up everything it can get if the yield threatens to drift past it. It was done in the US during World War II. It can be done in Japan. There are other tools Japan has in maintaining the “value” of the JGBs – not forever, but for long enough to make any gaijin short tear his or her hair out.

The yen could crash – until Japan decides to sell its foreign currency assets and buy yen. So, the yen will likely not fall much below the tolerance level, though that level may be much lower than today’s exchange rate. In 2006, the exchange rate approached ¥130 to the dollar. It made everyone in Japan nervous. That’s a number to keep an eye on.

But if the trade deficit continues to worsen, Japan may not be able to afford a weak yen and may have to prop it up! And if the trade deficit continues for long enough, it will eat up the foreign exchange reserves needed to prop up the yen. A bit of a conundrum.

While Japan will struggle to keep the debt balloon intact for as long as possible, there are in the end no other solutions than default, either sort of slowly through hefty inflation, or fast. Part of the wealth that has been sunk into JGBs no longer exists. But it hasn’t been written off yet. The older generation has benefitted from that system enormously, but the younger generation will end up paying the price. They all know it – hence their pessimism.

Abenomics attempts to whittle away at the problem by inflicting inflation on the people. At the current ¥1,008 trillion in debt, and about ¥45 trillion in new debt issued this year to cover the deficit, it would take 3% inflation and 1.5% economic growth just to keep the debt-to-GDP ratio at the perilous 212%.

But 1.5% economic growth year after year is hard to achieve for Japan – or other economies with aging and shrinking populations. If GDP growth on average is 1%, it would take 3.5% inflation just to keep the debt-to-GDP from getting worse, and it would take something like 6.5% inflation, year after year, to make a serious dent into it. That level of inflation will rob the people blind. That’s what Japan is facing. The 2% inflation target that Abenomics claims publically to be shooting for won’t be enough. The gurus behind Abenomics know that. And they might be pushing Japan down that road.

Due to global competitiveness issues, companies won’t be able to raise wages at the same rate. Hence, lower real wages, a process that has hollowed out the middle class in the US since 2000. Meanwhile, low interest rates and higher inflation will inflict financial repression on everyone with money in the bank or with JGBs in their portfolio, including pension funds. And if the BOJ institutes a yield peg, financial repression will be brutal. It will strangle the economy as strung-out consumers, including the many retirees who live off their savings that are getting demolished by inflation, no longer have the means to consume.

Abenomics attempts to shift the costs away from Japan Inc. and those who run it and can diversify out of harm’s way. And it will be painful for the average Japanese. There are alternatives – but no good solutions. All solutions are going to be tough and brutal. No one wanted to pay for what the government spent this money on. It was, and still is, a free lunch. But in the end, it will be paid for. One way or the other. Only uncertainty: who, when, and how. But I doubt it will be sudden.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()