Germans are practically euphoric these days—compared to the dour mood that prevailed for nearly two decades following reunification, when real wages declined in a stagnating economy beset with what appeared to be permanently high unemployment. While discontent smolders in other Eurozone countries, 88% of Germans are satisfied with their standard of living (Gallup). And 85%—a record since the beginning of the surveys—believe that they can get ahead if they work hard, up from 71% in 2007. This optimism is joyriding the powerful German export machine, an optimism that appears to be impervious to the nightmarish scenarios playing out at the periphery of the Eurozone. And it still hasn’t reacted to what may be the onset of a recession in Germany as the economic superstar has smacked into a wall.

And now, Germans have something else to be euphoric about (for a while, at least): a housing bubble.

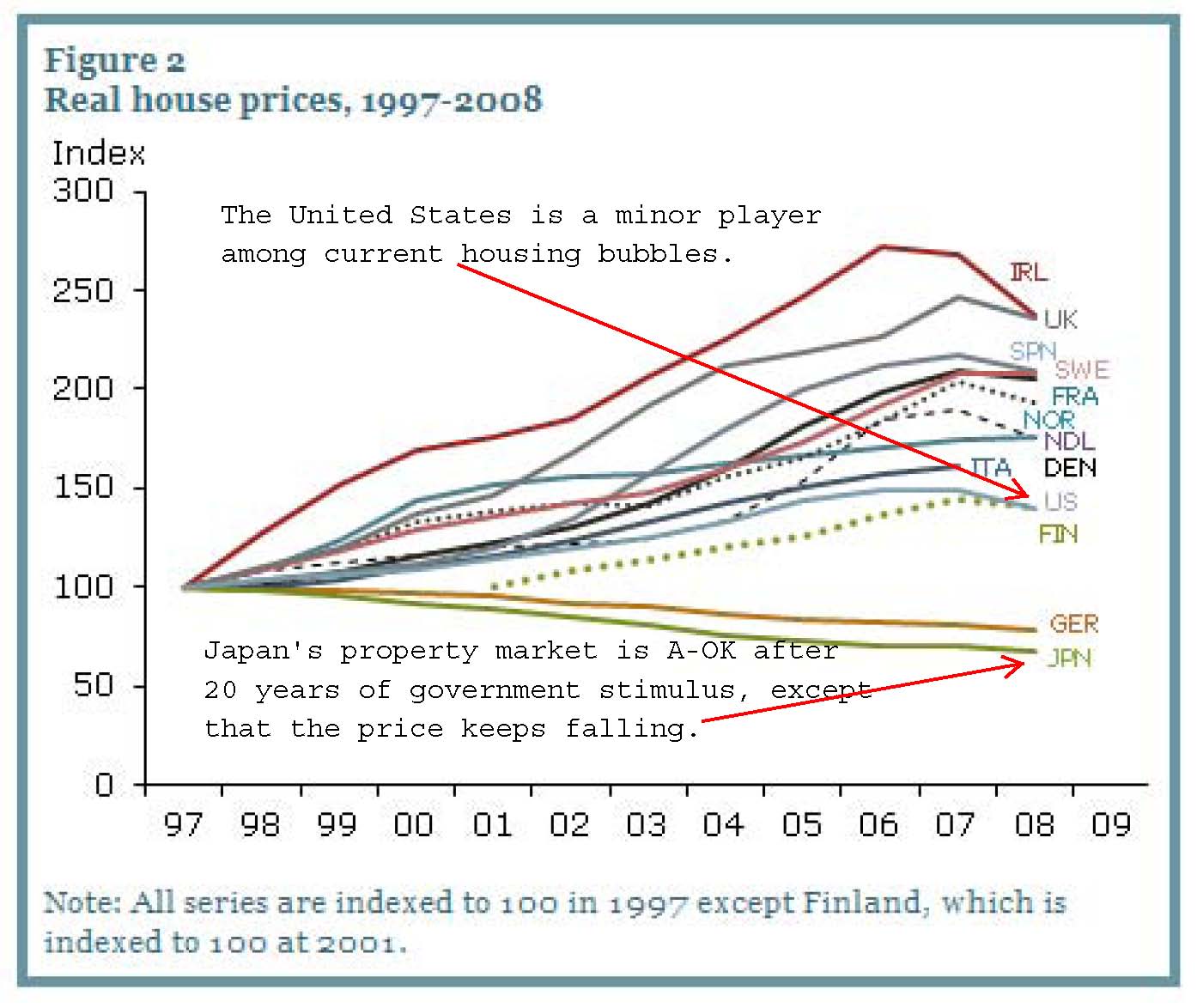

The German housing market stagnated after reunification. And if adjusted for inflation, it declined significantly, while other countries, such as Ireland, the UK, and Spain, experienced huge bubbles. Only Japan’s housing market was more morose over the same period (graph, real housing prices 1997-2008). But by mid-2009, prices began to rise. In 2010, they were up 2.5% nationwide. And in 2011, they climbed 5.5% (Bundesbank, Monatsbericht)—with the hottest locations exhibiting bubble characteristics:

{kind=link}

In Hamburg, prices of existing apartments skyrocketed 14% year over year in January. In Munich, prices of new apartments jumped 12%. In Berlin, prices of existing apartments rose 10%. In Cologne, prices of existing apartments rose 9%. These numbers confirm what I’ve been hearing anecdotally for two years: that Germans were plowing their money into brick and mortar.

It was the first time since reunification that an economic upturn produced significant price increases in housing, the Bundesbank said in its report. Among the top reasons:

– Household optimism—and the fact that the debt crisis hasn’t impacted that optimism.

– Record low financing costs. Average interest for a loan for 60% of the purchase price (Germans are a bit conservative) hovered around 3%, half of what it was ten years ago.

– Inflation fears and a seething frustration with the ECB’s loose monetary policy.

– Low yields for savers and holders of German government bonds. With these yields remaining below the rate of inflation, the average 5% yield on rental property suddenly is appealing.

– Capital preservation in times of increased risks and volatility in the financial markets.

– Capital flight from Eurozone periphery states where Germany is considered a safe heaven, particularly since it didn’t have a housing bubble.

– And now that prices have been rising, optimism is propelling prices even further.

Unlike in the US, most of the homes in Germany are rental properties. Only 43% of German households own their home, according to the Association of German Pfandbrief Banks. Homeownership is not subsidized by the taxpayer, as interest on a home mortgage is not deductible. And the government has stayed out of the mortgage securitization business. Instead, banks issue covered bonds against 60% of mortgage lending value. These bonds fund about 25% of all mortgages. Loans from savings banks and credit cooperatives fund most of the remainder.

As always during a bubble, individual investors are piling in. “And among them are more and more who are trying for the first time to invest directly in rental properties,” said Felix von Saucken, from the brokerage firm Engel & Völkers Commercial.

And so are institutional investors. Last week, in the largest real-estate transaction since the financial crisis, a consortium of German and foreign institutions bought 21,500 apartments from the Landesbank Baden-Württemberg for €1.4 billion.

The irony inherent in a monetary union: even if bubbles become clearly visible in certain countries, such as Germany or Denmark, their central banks are condemned to sit on the sidelines because they cannot set interest rates. Meanwhile, the ECB is flooding the market with cheap money to keep parts of the Eurozone and some large banks from imploding. In doing so, it is inflating bubbles in other parts of the Eurozone. Which comes with a steep cost: when housing bubbles blow up, the damage they leave behind is immense.

It may hit just when Germany can least afford it. Chancellor Angela Merkel warned that the country might be overwhelmed by its efforts to bail out the Eurozone and must not make promises it can’t keep. That reluctance has made Germany a punching bag. But the numbers are already staggering.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()