The long-term problem in the horrendous jobs report issued by the Department of Labor today—a problem in every jobs report since April 2000—is the strangely inconspicuous Employment-Population Ratio.

It measures the percentage of people age 16 and older who have jobs. It’s not perfect. But it’s the purest, least corruptible employment number out there: It’s not seasonally adjusted, manipulated by the infamous “Birth Death Adjustment,” or mucked up in any other way—unlike the headline numbers that have become a joke.

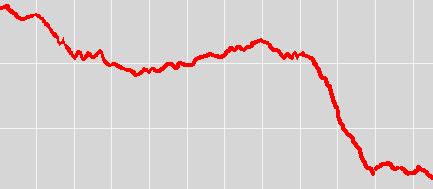

And it hovers at a 30-year low.

After World War II until 1975, it bounced up and down between 55% and 58%. As women entered the workforce in ever greater numbers, the participation rate began to edge up; and after the recession of 1983, it went on a bull run that peaked in April 2000 at 64.7%.

Then it began to decline. Whatever the cited reasons. Outsourcing, innovation, off-shoring, tax laws, technological progress, corporate shortsightedness, cheaper labor elsewhere, whatever. When the housing bubble and related activities unfolded in 2004, it stabilized at around 62.3% and increased a notch to 63.4% in 2006. As the housing bubble deflated, it began to decline again. And then it crashed.

The ugly trajectory of the Employment Participation rate:

Today, it came in at 58.2% (a rounding error up from last month’s 58.1%). These are numbers we haven’t seen since August 1983.

In other words, 41.8% of the working-age people in the U.S. don’t have jobs, as opposed to 35.3% in the year 2000. To convert this percentage into real people: Since the working-age population in the U.S. these days is 238 million people, a decline of 6.5% in participation represents 15.4 million jobs.

There are no green shoots or improvements or recoveries in sight. It’s a structural issue. Every time a U.S. company outsources production or services to entities overseas, or buys from foreign suppliers when it used to buy from domestic suppliers, it removes more jobs.

A superb example—not only because of its majestic physical aspect but also because of its economic impact—is the new San Francisco Bay Bridge, the most expensive single structure in the U.S. Incredibly, its most prominent segment was built in China.

These jobs gone offshore will continue to drag down our economy, and no amount of money-printing by the Fed and no amount of hope-mongering by the White House and no amount of deficit-spending by Congress are going to change that. Only one thing will: A collective corporate decision to reverse the trend of off-shoring production and services. Because, mathematically, you can’t grow an economy by removing jobs.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()