Gutted Hopes for a Strong Finish.

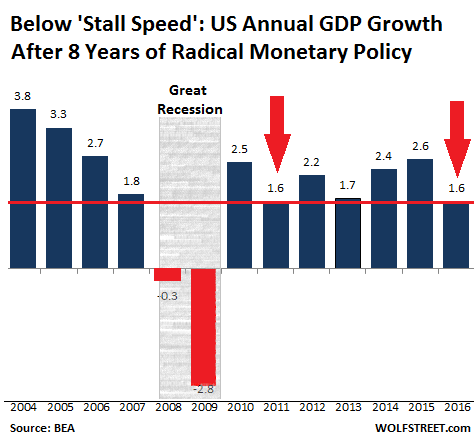

The consensus forecast by economists predicted that the US economy would grow at an rate of 2.2% in the fourth quarter, as measured by inflation-adjusted GDP. The forecasts ranged from 1.5% to 2.8%. The New York Fed’s “Nowcast” pegged it at 2.1%, and the Atlanta Fed’s “GDPNow” at 2.9%. And today, the Bureau of Economic Analysis reported that growth in the fourth quarter was a measly 1.9%.

That was down from 3.5% in the third quarter, a spurt that had once again given rise to the now gutted hopes that the US economy would finally emerge from its stall speed. But instead it has slowed down.

For the year 2016, the growth rate dropped to 1.6%. It was worse even than 2013, when GDP growth tottered along at 1.7%. And it matched the growth rate in 2011. Both 2016 and 2011 were the worst since 2009 when the US was in the middle of the Great Recession:

In fact, over the past 50 years, anytime the economy grew less than 2% in a year, it was either already in a recession for part of the year, or there’d be a recession the following year. Hence “stall speed” – a speed that is too slow to keep the economy from stalling altogether.

What hurt fourth quarter growth particularly, according to the BEA?

- Exports, which add to GDP, dropped -4.3% (exports of goods -6.9%, exports of services + 0.9%)

- Imports, which subtract from GDP, jumped +8.3% (imports of goods +10.9%, imports of services -2.7%)

- Personal Consumption Expenditures by consumers “decelerated” to a meager growth rate of +2.5%, down from 3.0% and 4.3% in the prior two quarters.

- Federal government spending fell -1.2%

On the stronger side:

- Residential fixed investment jumped 10.2%, including the ongoing construction boom in big-city multifamily buildings

- Nonresidential fixed investment rose 2.4%, nudged up in part by a 6.4% gain in intellectual property investment .

- State and local government spending rose 2.6%.

Of note, there was a major and sudden uptick in the inflation measures of the GDP report:

- The price index for “gross domestic purchases” rose 2.0% in Q4, up from 1.5% in Q3.

- The PCE price index rose 2.2% in Q4, up from 1.5% in Q3.

So stall speed for the year. But this time it’s different. This is the third year since the Great Recession when GDP growth dropped below 2%. The Fed’s policies of eight years of cheap credit have entailed soaring debt levels among companies, governments, and consumers – money borrowed from tomorrow that was spent today. Borrowing for productive investment is one thing. Borrowing for consumption is another: it boosts GDP but creates a debt overhang with no productive assets that generate income to service that debt in the future; that debt service for prior consumption then acts as a burden on future consumption.

And the Fed’s policies also created rampant asset price inflation, including house price inflation that supported a construction boom while gutting middle-class budgets. But spending on soaring rents and certain other housing costs also enters into GDP, and so it’s all for the good.

This weird condition – the magic world of QE and ZIRP – has blocked the essential process of economic and financial cleansing back in 2009, but has also kept the economy from taking off afterwards. And so it’s wobbling along, over-indebted and heavily encumbered, with nearly all assets overpriced, kept aloft below stall speed on a monetary wing and a prayer.

But cracks are everywhere. San Francisco’s office leasing activity has worst year since 2009. Read… “Rightsizing Has Once Again Come to the Tech Sector”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Time for another two or three rate increases in 2017.

Oh well….not being a society that learns from mistakes; I d expect to see more money printing, interest rates going back down (once they ve gone up enough to allow it)…maybe a big fat war to cancel all the unpayable debt that s out there.

The people in charge believe debt creates prosperity (for the bankers perhaps, who wind up being owed massive interest even at low rates) but it kills everyone who doesn t own ‘assets’ and endangers those who do because what goes up artificially, will eventually go down,,no one knows when…

They ve gutted the American Class and it s small business culture, once the envy of the rest of the world; our middle class hired the most people, did the most work, paid the lion s share of the taxes, and then went shopping.

Did they stop teaching how the system works along with ethics, at our supposedly fab ivy league schools?…it appears so.

An economy is bottom- up, not top-down; what we ve seen (in spite of Hilary s fervent condemnation of it), hasn t been ‘trickle down’ but TRICKLE UP!

I guess Wall St and DC are having fun in a luxury bubble on their private jets and private golf courses…too bad ….how can it end in anything but tears for all concerned.

Bank of international settlement’s still functions, what you think makes debt disappear except remittances from GDP?

After so many years, are there still people who believe that the Fed has the power to improve the economy in any way? How much failure does it take to convince Yellen and her fellowship of irrelevant and incompetent “economists” to just stop making things worse?

I heard them say they are not supporting wealth concentration, which implies they view their intervention as temporary. Well, if they never let the economy repair itself through a recession, and they constantly prop markets when they fall, they really are supporting permanent wealth concentration.

This is just one of the many contradictions they spout. They are a worthless organization with no clear mandate, no conviction, and no clear thinking. They should be dismantled.

Remember the most important FACT The Fed is the “Great Whore” as the Bible tells us. The greatest criminal act in History was committed to this country with the creation of these Blood Sucking Vultures of America”. Their plan is destruction and no other. You think these 10 banks have a plan. You don’t that’s for sure. and nothing will change. Woodrow Wilson took a hike on a vacation and these vultures came in and control ever since. It’s all a plan my friend not a coincidence. Facts of the Money and control over world economics and financing whatever they have in mind. World Wars, crisis and sucking this country dry of its

GOLD.

Choices!

The fed gains a mountain of income from its print much to buy dear strategy? And it doesn’t want to seem greedy so it makes remittances to the treasury (85b) each year. (Which it plans to slowly pull back from naturally by retiring the balance sheet?)

The battle over this remittance will be furious between social security (people) and treasury (administration)!

The frd thinks and acts like a hedge fund and not a bank?

The decline/contraction continues, the 3Q uptick was simply the uptick from a recession or dead cat bounce as they call it on Wall Street.

US GDP, and indeed, world GDP has been “recalculated” and with a positive boost by now categorizing R&D expenses as capital investments.

An increase in stocks of “unsold” output and a bit more business investment after three quarters of decline helped the Q4.

That growth figure doesn’t sound too impressive to me, Wolf. I guess those who are in their right minds must be pleased by the figure.

Growth overstated. 1% was inventory stuffing, actual growth .9%.

And falling as year ended. Future production down to work off inventory, which costs more to carry as interest rates rise.

I wonder how much real growth we’ve actually had since the late ’90’s. If you factored out growth from the ‘net bubble and the housing bubble, I’m betting we’ve been running at less than 2% for close to 20 years.

And that would help explain the lack of growth in wages and productivity.

“I wonder how much real growth we’ve actually had since the late ’90’s.”

Glad you asked.

The blue line on the graph clearly shows there has been plenty of growth, almost entirely negative.

http://www.shadowstats.com/alternate_data/gross-domestic-product-charts

The red line is to fool gullible people into thinking the U.S. economy isn’t being liquidated.

Thanks……the lines look parallel more or less but Williams has it negative. Do you know what the big modifications are?

You do understand that when most every thing is leveraged, meaning that there are payments on every level. This acts like a VATax. This takes a piece of every transaction and transfers money to the banksters. It doesn’t really matter about interest rates on the way down, the amount taken from the system remains pretty much the same or even grows as the value of all assets go up.

This does become rather distorted as the time frame expands but what is happening during this financialization is that debt acts like a tax on the system diverting productive energy away from wages and productivity growth into the hands of the banksters who end up owning and controlling more and more.

The math no longer works. I don’t really care what the FED thinks about deflation. We have been and are deflating on a real basis since the turn of the century.Our dollars aren’t worth what they were… This is deflation.

They can make the GDP look like it is growing but it is only growing because the asset values keep growing due to low interest rates and easy access to more debt. When most of the profits from productive enterprise get eaten up by the cost of leverage it eventually eats up the system that supports it. This is where we are.

All that is to be know is the when and how the collapse of the debt pyramid starts.

Perhaps we’re looking at the wrong metrics, it’s difficult to export goods if you make nothing.

How about social justice exports?

I’ve said this since I first traveled around the USA on business ( I no longer travel on business ) :

“What the USA makes, and exports, is Corn, Porn and Dollars.” No doubt I thought I was being clever by imitating something that Archie Bunker could have said.

Yup, you can’t export what you don’t make.

I would add this — Hollywood, full of looney-left crackpots these days, does a pretty nice job of enhancing USA export figures with foreign distribution of USA based films. Many times when I see the figures for a recent movie, they’ll look something like this :

Production and marketing : $20 million

Domestic ticket sales : $36 million

Foreign ticket sales : $78 million to $118M and often much much more.

And I read these figures long before the inevitable world-wide distribution of the film on DVD and Blu-Ray.

THREE CHEERS FOR THE LOONEY-LEFTIST HOLLYWOOD CROWD ! ! For making a product that exports well and provides a welcome trade boost for America.

And no, as much as I despise these narcissistic nitwits, I am not being sarcastic. I really appreciate what they do for our trade deficit.

SnowieGeorgie

Only fools believe that “social justice” is a substitute for economic opportunity.

s’right. It’s BLT before LBGT.

You mean invasions? Apparently the US is going to get ‘another chance’ to seize Iraq’s oil although it ‘should have kept it’ the first time.

maybe the “great recession of 2008” exposed just how weak are economy really is. After providing the the liquidity to the stressed financial markets post 2008 , the feds kept the pedal to the metal as did the BOJ and EU. Both are also overly financialized economies. This enabled governments to expand by borrowing at non market rates. there wasn’t any corresponding recession at the federal level. Substituting financial and government growth for more enduring private sector goods producing growth is a travesty. Maybe it is an indication of whom the feds really

serve.

What ever happened to the Velocity of Money (M2V) measure? It seems to have been dropped from the lexicon of current economic analysis. While the indicator has a reputation for being variable it has been incredibly accurate in measuring the economic stagnation on Main Street. According to the St Louis Fed (https://fred.stlouisfed.org/series/M2V) the velocity of money has dropped from 2.005 in 1Q 2007 to a 1.436 last December which is the lowest it’s been since the Great Depression. I repeat – the lowest it’s been since the Great Depression. In comparison from 1959 through 2007, the velocity of M2V averaged 1.86x with a maximum of 2.21x in 1997 and a minimum of 1.66x in 1964. In fairness though M2V hasn’t always been a statistical outcast – Harry Dent has brought the M2V indicator in from the cold in a July 2016 article but that’s about it. Q1 2007

Lego,

Inflation can increase velocity strongly https://fred.stlouisfed.org/series/M2V#0.

Until 1992 the correlation between inflation and velocity has been excellent, not so much since 1992.

It could be also the fact that capital is more concentrated as previously. So the key element is here that capital must be distributed to many hands. Capitalism is good until capital is in many hands. Also left state capitalism is a bad thing as then investment decisions are made by a small circle of people, which make often big errors.

The same for power: power is fine and works efficient as long it is distributed in many hands.

Any concentration of capital and power (it does not matter if capitalists or government bureaucrats do it), slows down the economy and velocity of money.

We see this exactly in the US, Japan and Europe. There is too much concentration of power and money (the biggest capitalists are actually the Central Banks). Nature will exert its power and readjust this in its own way. Any wave breaks down at some point.

I do not believe that inflation can increase the velocity of money in today’s environment of excessive debt. All an increase in inflation or rising prices will do in an overly indebted system is cause it to contract.

Inflation transfers wealth upward as those who control/own the assets benefit and everyone else loses.

There will be a breaking point.

After this unprecedented stimulus, these meager numbers indicate an unseen but detectable ‘black hole’ …a huge deflationary gravitational force that can not be warded off much longer.

All that’s left to try is massive fiscal spending (on something useful please) or helicopter money. The last being accomplished by direct deposit into every personal account under 10K , one per person, of maybe a thousand dollars.

Or if you want to get really radical, a wealth tax.

But that would require a huge shift to the left in pretty much the least left G 20 country.

So that doesn’t seem likely.

Something like this?:

https://www.youtube.com/watch?v=BjdCNRRL-ko

:)

I think the cores are under vacuum, they will implode instead of exploding. Direct deposit might happen, though, except after the implosion.

Hey Wolf, how about an article detailing the Dow stocks with flat and/or declining sales? I count around half a dozen off the top of my head, but there might be more.

Interesting idea. I’ll keep it in mind … the companies with the biggest revenues declines are probably the ones whose shares have recently risen the most :-)

Done!! :-)

Thanks for the suggestion. It’s a lot worse than I thought.

I will gladly pay you on Tuesday..for an ATM style Big Mac…Today,Oh wait they are giving them away for FREE..with your “twitter handle” for three hours,in Boston on Tuesday..? ‘Stall-speed Robotics’ hits the Fast Food Industry…lolol

That worthless Trump, 2016 was all his fault. If it wasn’t for him there would’ve been another fantastic year of growth.

On the contrary, per former President Obama as quoted from a CNN Money article titled “Obama’s gift to Trump: A ‘pretty solid’ economy” just last month:

“Anyone claiming that America’s economy is in decline is peddling fiction,” Obama said earlier this year.

The final component to Dow 50k is finally here. We just need negative rates for companies to buy their own stock and get paid doing it. Not sure how the banks would like it though since companies would be raising capital (neither stock or bonds) while buying stocks.

All this leveraged wealth looking for productivity to support it.

Trump better pop this artificial stock market quickly or he’ll own it. Asset prices have to drop before businesses will invest any serious money in the future. Only fools would be investing anything at these price levels.

Aren’t you subscribed to his twitter? He has already chosen to own it and celebrates every milestone cheerfully

If American companies build their factories in Mexico or overseas and then import their goods back into the US, doesn’t that blur the trade deficit and GDP?

It doesn’t blur GDP. It lowers GDP :-]

Imports lower GDP, Exports raise it. So our trade deficit is a big negative force in the GDP calculation (and in the economy).

Keep up the good work, Wolf, and thanks for using NUMBERS instead of EMOTION (e.g. “Loony Left”) to describe our situation.

To ascribe uniform behavior to large blocks of people doesn’t help anyone except those in power, and the “Loony Left” is NOT in power.

Goebbels perfected the propaganda style of condemning a block of people (Jews) as a push point to promote National Socialism. Rush L. and “hate radio” have pushed the “uniform block of bad guys (“Liberals”, “Democrats”, “Washington insiders”) from which to push off, to promote various unsupported-by-facts ideology.

Thanks for all your research and supported material you write, Wolf!!

OK,so if companies can’t pay back loans,

old banks don’t want to give out loans, and

consumers don’t want to circulate the money (hoarding), you can just let some

companies become banks to prevent them

from defaulting and maybe even issue new

loans to themselves. Zerohedge 6/8/16

One silver lining in the US(S)A might be the mall-death all around small town America. The malls did kill of the mom-&-pop shops and other small buisness in those small towns where the malls were established and downtown centres were quite deserted. And when the small buisnesses did shut down, with them went went the jobs provided by these businesses and jobs in other businesses like transport services etc. Now when malls are going belly up all over the place, there’s again going to be demand for different kind of small businesses in those small towns, reviving stagnated city centers and providing jobs for local people and thus slowly increasing local wealth. And this happens not thanks to TPTB in the Imperial City, in fact this happens despite TPTB in Washington.

Perhaps a little bit here and there – but the migration to online for goods and services to replace malls is where the investment is going (e.g. Amazon). If a local can offer a physical service (e.g. Bike shop, where revenue comes from tune-ups, etc.) – but the model where retail is essentially distributed inventory warehousing is on a precipitous decline. As the move accelerates, fewer institutions are going to finance conventional brick & mortar. This will create space for on demand manufacturing that is close to market. That is where the opportunity lies: 21st century, fully digitized supply chains that are truly demand driven with no human intervention outside of design and support functions.

If I understanding you correctly you’re implying a supply demand balanced economy. If so, the one thing I guarantee is chaos in the production sphere. A supply demand balance is impossible in the current economic system. When capitals invest in machinery, equipment, structures, etc. they have no idea what the exact final demand will be. It’s all guess works. So a total chaos in production as has always been.

You’re starting with distribution and the working your way back to production. But like I said companies do not invest knowing the final demand. So you have to also go from production and work your way forward to distribution to see the entire picture.

When profits are handsome manufacturers cannot build enough capacity and they’d keep adding capacity until there is overproduction.

Many companies are in an environment where there is essentially little or no automatic demand for their products, and they have to CREATE demand for their products via marketing, advertising, discounts, etc. This demand they create will either be new (that’s what Apple did with the iPhone initially) or they’ll have to take share away from some other companies.

There will be new products, and they will certainly pull share from existing supply chains. In my industry, supply chains are primarily China and Southeast Asia with leadtimes from 6-8 months – too long to respond to shifts in consumer tastes, and, as interest rates rise, the cost of those supply chains will rise tremendously as interest rates are amplified through the supply chain. New technologies will allow unprecedented alignment between supply and demand that is more flexible and scaleable than previously possible. Unfortunately, the Asia supply chains have invested capital in technologies that are not significantly more advanced than those found in western factories 40 years ago. The upshot: to compete in the new market opportunity, a much higher value will be placed on market proximity (speed), and brand new investment that is more digitally driven through each step of the supply chain. It will require a complete replacement of existing capacity. The new capacity will mean new, but fewer, higher paying jobs than those lost in the late 90’s/ early 00’s, but the value produced per unit will be much higher due to better alignment, fewer incentives/markdowns, higher efficiency by avoiding the retail middlemen.

I recall the same projections being made when Walmart went to RFID for inventory control. I recall the glory days of B2B technology companies (most of which had no revenue and are now gone) I recall the same pronouncements on just-in-time inventory supply. A publisher can order just as many books as he has an order to fill, (if anyone reads) and the printer in China will drop ship the product.

We now have drop shipping (it took a while but its here) and its creating a problem, as is the small number of defective knock off products which find their way into Amazon fulfillment bins. The problem ( Trump?) is that everyone wants fewer regulations, (China needs more) and the downside of the threat to safety and product integrity is a lack of confidence in the supply chain, and a sullying of product integrity for brand names, since the knock offs look the like real thing. Surprise the corporate office won’t honor those defective products, just check the reviews. Customer service centers are being closed, products are shipped without instructions. Chinese suppliers scramble to maintain some semblance of support from behind their Chinese wall.

I am pretty certain the runaway Toyota problem had to do with defective circuit boards from China, but everyone has to keep their mouth shut, including Trump. As you say in for a dime in for a dollar, we have to make China work, or the entire consumer product business collapses. And its a lot like the last days of the Roman Empire, long supply lines across hostile territory. Then there is the enigma of higher energy costs, which the fed can fight with ZIRP if it so chooses.

This should read:

“2016 Economy Matches Worst Year since THE LAST Great Recession”

because we are in a depression right now.

It has been disguised by the central banks propping up the company bonds and shares – or in other words – becoming owners of stuff that used to belong to other, non central bank people.

The simple mathematics of central banking – renting a currency – means that eventually the central bank owns all the wealth. The maths is basic and inescapable.

We are now in a period where much wealth is being rapidly transferred to those banks via these purchases of bonds and shares, people look at the actions and think they are just propping up prices but rest assured that the exchange of their worthless fiat for ownership of real assets has just started surfacing in this obvious manner.

As there’s technically no way to repay a loan to a central bank (because they issue the capital, not the interest), look forward to this continuing until it’s time for the currency to collapse, as all debt fiat currencies do.

This is why the US constitution mandates a government issued currency and forbids the existence of the FED, itself created under a highly dubious ‘vote’ in an empty chamber. 1913 was the date the US lost the war against the European money changers that they’d sought to escape in Boston.

so how is it the Fed policy created a massive construction boom which did not benefit the middle class?