A leading indicator of big trouble.

This could not have come at a more perfect time, with the Fed once again flip-flopping about raising rates. After appearing to wipe rate hikes off the table earlier this year, the Fed put them back on the table, perhaps as soon as June, according to the Fed minutes. A coterie of Fed heads was paraded in front of the media today and yesterday to make sure everyone got that point, pending further flip-flopping.

Drowned out by this hullabaloo, the Board of Governors of the Federal Reserve released its delinquency and charge-off data for all commercial banks in the first quarter – very sobering data.

So here a few nuggets.

Consumer loans and credit card loans have been hanging in there so far. Credit card delinquencies rose in the second half of 2015, but in Q1 2016, they ticked down a little. And mortgage delinquencies are low and falling. When home prices are soaring, no one defaults for long; you can sell the home and pay off your mortgage. Mortgage delinquencies rise after home prices have been falling for a while. They’re a lagging indicator.

But on the business side, delinquencies are spiking!

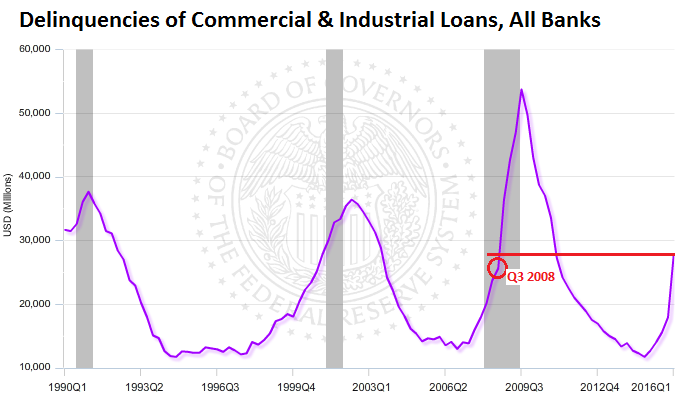

Delinquencies of commercial and industrial loans at all banks, after hitting a low point in Q4 2014 of $11.7 billion, have begun to balloon (they’re delinquent when they’re 30 days or more past due). Initially, this was due to the oil & gas fiasco, but increasingly it’s due to trouble in many other sectors, including retail.

Between Q4 2014 and Q1 2016, delinquencies spiked 137% to $27.8 billion. They’re halfway toward to the all-time peak during the Financial Crisis in Q3 2009 of $53.7 billion. And they’re higher than they’d been in Q3 2008, just as Lehman Brothers had its moment.

Note how, in this chart by the Board of Governors of the Fed, delinquencies of C&I loans start rising before recessions (shaded areas). I added the red marks to point out where we stand in relationship to the Lehman moment:

Business loan delinquencies are a leading indicator of big economic trouble. They begin to rise at the end of the credit cycle, on loans that were made in good times by over-eager loan officers with the encouragement of the Fed. But suddenly, the weight of this debt poses a major problem for borrowers whose sales, instead of soaring as projected during good times, may be shrinking, and whose expenses may be rising, and there’s no money left to service the loan.

The loan officer, feeling the hot breath of regulators on his neck, and seeing the Fed fiddle with the rate button, refuses to “extend and pretend,” as the time-honored banking practice is called of kicking the can down the road in good times.

If delinquencies are not cured within a specified time, they’re removed from the delinquency basket and dropped into the default basket. When defaults are not cured within a specified time, the bank deems a portion or all of the loan balance uncollectible and writes it off, therefore moving it out of the default basket into the write-off basket. That’s why the delinquency basket doesn’t get very large – loans don’t stay in it very long.

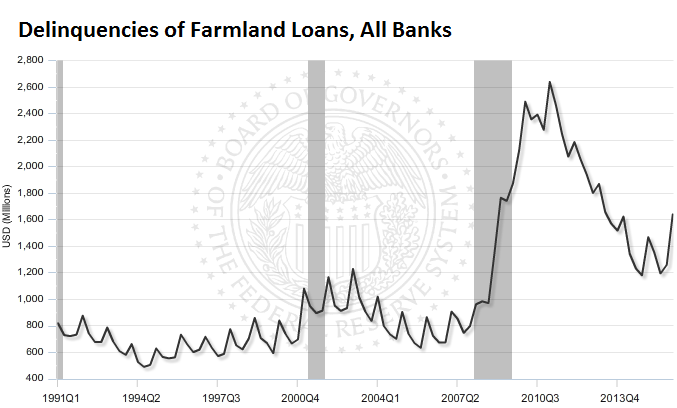

And farmers are having trouble.

Slumping prices of agricultural commodities have done a job on farmers, many of whom are good-sized enterprises. Farmland is also owned by investors, including hedge funds, who’ve piled into it during the boom, powered by the meme that land prices would soar for all times because humans will always need food. Then they leased the land to growers.

Now there are reports that farmland, in Illinois for example, goes through auctions at prices that are 20% or even 30% below where they’d been a year ago. Land prices are adjusting to lower farm incomes, which are lower because commodity prices have plunged. (However, top farmland still fetches a good price.)

Now delinquencies of farmland loans and agricultural loans are sending serious warning signals. These delinquencies don’t hit the megabanks. They hit smaller specialized farm lenders.

Delinquencies of farmland loans jumped 37% from $1.19 billion in Q3 2015 to $1.64 billion in Q1 this year, the vast majority of it in the last quarter (chart by the Board of Governors of the Fed):

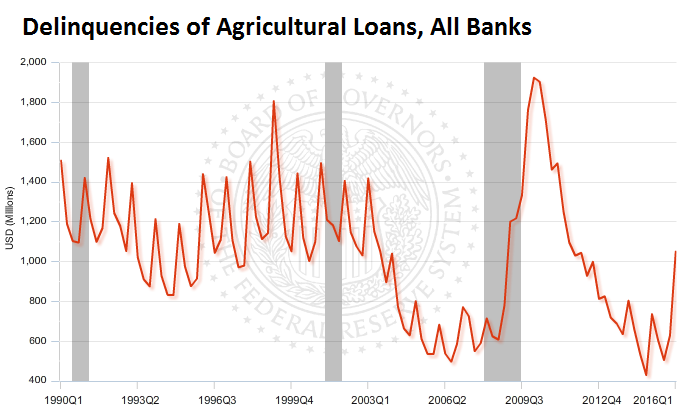

Delinquencies of agricultural loans spiked 108% in just two quarters to $1.05 billion in Q1. On the way up during the financial crisis, they’d shot past that level during Q1 2009:

Bad loans are made in good times — the oldest banking rule. “Good times” may not be a good economy, but one when rates are low and commercial loan officers are desperate to bring in some interest income. With a wink and a nod, they extend loans to businesses that look good for the moment. That has been the case ever since the Fed repressed interest rates during the Financial Crisis. A lot of bad loans were made during those “good times,” precisely as the Fed had encouraged them to do. And these loans are now coming home to roost.

One of the big indicators of the end of the “credit cycle” is the number of bankruptcies. During good times, so earlier in the credit cycle, companies borrow money. Lured by low interest rates and rosy-scenario rhetoric, they borrow even more. Then reality sets in. Read… US Commercial Bankruptcies Skyrocket

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’ve heard that many no interest mortgages with a ten year readjustments that were made in 2006 are now about to get changed.

This was from a guy who subcontracts eviction work from the Alameda Sheriffs office. Says he’s never been busier. I see him at Starbucks when he’s getting ready to go to work. I call him the grim reaper.

That guy at the Starbucks – he’s working on evictions of tenants, I assume, not foreclosed homeowners. Did I read this correctly?

Says he does both. Tenants from rentals and people in foreclosed properties. Hear say, but interesting.

The “other” pink elephant in the room are derivatives.

There must be tremendous pressure building in the OTC , CDS, and CLO’s that have been written up using these loans as the collateral base. I don’t foresee a fed rate hike, as this would add more weight to an already fragile sector.

When a derivative defaults, then the “notional” amount becomes active and is immediately called. These weapons of mass financial destruction amount to tens of trillions of dollars.

The Fed has painted themselves into a corner.

They have to raise rates because if they don’t they will destroy many pension funds. Pension funds when they were setup years ago were modelled on an interest rate of between 6&8% which they have not been able to get for about ten years now. Here in the UK it has been estimated that a £650 billion hole has opened up.

You can bet that some of these funds have had to take riskier position to chase yield so I am expecting a full blown pension crisis in the years to come.

The Fed can’t raise rates enough to bail out pensions funds. If the Fed is raising rates, it’s just to give itself some room to lower them again, to once again goose the stock market.

They may not be able to raise rates at all. The pension funds are at risk, but the flip side is that American corporations are awash in short term debt that they used to fund share buy backs. That debt has to be rolled over periodically. If rates rise enough to save the pension funds, they could sink a number of major companies. If that wasn’t bad enough, Europe and the Chinese are increasingly looking fragile, so even if the Fed engineers a miracle, it may not be enough.

Warren Buffet said only CNBC {i.e. Cyber, Nuclear, Biological and Chemical}weapons can hurt Berkshire. I guess in his old age he forget mortgage derivatives. He original coined the phrase mortgage derivatives are financial weapons of mass destruction.

All buffets derivatives pay him, and he holds the cash bond in then, that’s the only way the handle Derivatives.

Research it.

They declared a while ago what they had, and how they were structured.

Rumors around our area (Hickman) is almonds are at or heading toward 25% of what they got last harvest. That seemed a little bit exaggerated, but hey, I’m not a farmer and wouldn’t know.

This is from a couple small farmer friends/neighbors of mine… And I would assume anything under 100 acres would be considered small these days…..Unfortunately.

I just looked it up: Nonpareil Inshell Almonds peaked last July at around $5.00 per pound. Now at $2.36 … so that’s down over 50% from the peak. This is based on a published rate. So your neighbors – who are almond growers and who know the price of almonds based on actual money changing hands – may not be far off target with their expectations.

And I would think that the “small farmers” will be the ones struggling without “big money” backing like some of the large co-op style mega ranches that have popped up just about everywhere. Sadly

rates increase, so does rent. costs for landlords goes up.

question wolf. why r mortgage rates between Canada and usa so different?

Are the vast majority of mortgages in Canada government originated or guaranteed like the in US?

The entirety of the mortgage market in Canada is guaranteed by the government insurance fund. Banks have the option to hand over defaulted mortgages for full cash value.

I was checking out our local Tax Collector’s published list of properties for an upcoming tax sale. I noticed a number of real estate developers with multiple properties on the list. The ones I checked out were undeveloped lots in subdivisions, commercial lots, and a fair amount of raw acreage close to previous developments. I am wondering if this is the standard operating procedure for developers, or, are these businesses in distress?

If you are a developer, you dont sell you land bank (you build on it) or let somebody else do so.

Logic. Distressed Developer.

d: This isn’t my area of expertise. And I know that banks give developer types a lot more rope than we mortals. But it seems to me, that when you stop paying taxes on a piece of property; you are walking away from something you no longer see as an asset. I don’t know if this is a valid business model, or if it signals that the company is in financial trouble.

Land bank’s, undeveloped lots/land/farms brought to buy and sell as undeveloped lots, are very long term. 30 + years, or there is no Huge Profit.

shorter term Lots brought to develop, as urban areas sprawl, are 5 -15 + depending on purchase price and knowledge (generally Crony Sourced), of exact intended municipal urban expansion plans.

The money is in develop and build on your land-bank. How many small urban 400K plus units do they cram on to an Acre at 50% plus net profit on retail sale?

Remembering the land owner/s developer/s will sell “his/their land” to “his/their Sacrificial, indebted, Phoenix development Company” to distance him/themselves from any liability’s or development risk, at a huge profit, before they put in the services and build. So that they have the Majority of their profit banked, before the first machine arrives to work.

So if the Muni/state is selling the land to recover taxes, somebody has a financial, or the land itself has, a problem.

As you need the land to make the Huge profits that are in the housing game, for develop/build operations.

Crony group’s buy up the land in this game 20, 30, 50, Years in advance

1 block I missed, 800 K at the time, huge money. The crony brought it, 30 years before for 50 K. Absentee owner brought it.

26 years later, 120 M asking, will consider cash offer over 85 M. average annually Muni taxes taxes, 6K, in that 26 Year time frame.

Absentee, overseas, owner. SOLD. Due to the laws in that country, that profit, 84 + M (Sale price was confidential). Is ALL TAX FREE. Money for jam. Now being built on

There were over 200 blocks in that area that went through that 55 year development time frame. The crony’s tied it all up for themselves in the late 50’s. Then they dribbled it out over time.

The easy flat ones for industrial (Cheap SQ Ft to build (Frequently design build, to long term, committed, lease tenant instructions)) they developed themselves.

The more difficult Residential ones. Like the 800 K 1 I missed (that was Residential) they sold, all the blocks are now just about developed.

Those crony familys in that late 50’s group, own over a 1/4 of the industrial land in one of the largest per capita population city’s in the world. Just from their crony Land deals. Their true nett worth can not be ascertained. As it is all buried in trusts. Not one of them is on a rich list, they all would feature on one, if you could get the Data.

Stupid people let themselves get put on rich list’s, or appear as known high nett worth individuals, to the Taxer’s? IRS.

Wonder how this all gets swept onto taxpayers and prudent savers again this time, perhaps by pulling forward demand for moar warships??

northwest territorial mint declared chapter 11 and i had 3000 oz of silver bullion stolen by those crooks This country is toast with the criminality and fraud

Why was you Bullion not in your possession???????

If it was on order, why did you release funds from escrow, before Delivery/Handover.

İ was overseas and had a storage contract with them but the owner was a criminal Lucky me right and i thought İ was playing it safe

SAFE? Was your silver IN a SAFE in your home, behind a wall?

Sorry to jump all over you, but I am going to use you as a perfect example of somebody who “trust” and learns an easy lesson the hard way:

Never, ever trust anybody. Not your wife, your parents or your kids. Love, them. Yes. Support them, yes. Trust? NEVER.

Trust nobody and no organization. Ever.

That is unfortunate.

This is teh Issue with “Storage Facilitys, Finding a good one not woned ?controlled by a bank or the state.

Like forex brokers, finding an online one, you can get your money back from quickly and easily, that is stable and sound.

I keep my metal underground in an unusual place. Unless you have an idea where to look you are wasting your time.

Sorry to hear!

On the other hand, you could have invested it in a conservative-sounding bond fund, and one day it implodes.

For us, the world is a minefield when it comes to hanging on to our hard-earned money. You’re not the only one! Sooner or later, we all get screwed, no matter how hard we try to avoid it.

I hope you have more luck next time.

NEVER EVER BUY GOLD/SILVER WITHOUT TAKING IT HOME WITH YOU.

A while ago the Canadian and Australian mints were offering allocated accounts. What do you think of this?

Then you are effectively banking with the state again.

Your bars, With your serial numbers, are not in. Your deposit box.

If the state wants to take, or freeze it. It will.

A lot of US owned Bullion moved from Switzerland to vaults in Singapore. During the Swiss bank account data leaks to the IRS.

The problem with Singapore, is that if Malaya, Indonesia, or china, decide to Occupy Singapore, and strip the vaults. Nobody will be able to stop them before it is too late. Apart from that, the US wouldn’t really care, as it is not US state gold.

Due to their bad behaviors banks and the state have effectively returned us to the 1700’s, hidden wall and floor safes, or other types of safe places for our Liquidity, Jewelry and bullion. Is now becoming the norm as the state is a bigger thief than than burglars .

As in greece, bank controlled safe depository’s can be sealed by the state, and not opened without a state inspector present. Overnight without warning. They can do the same to all the private safe depository’s.

Burglars are really quiet far down the capital risk list .

I still think farmland is a great long-term investment. Or any land for that matter. I’m very happy with the two wooded lots I bought in 2010, the timber pays the taxes and occasionally there is a cheque from the logging company. I can even feel good about it as I’ve set aside a few acres to just stay wild as a wildlife refuge.

So if we are going to have a crash in farm prices I’ll be standing by, ready to buy. I’m ~50% in ultra liquid investments nowadays (cash and solid muni bonds). One needs a loupe to see the yield but I sleep soundly at night ..

I have a wood lot as well.

The only issue with land units, is if the state wants to take them, it can, and will.

d: Thanks for the detailed answer to my question regarding developers, above. I appreciate you taking the time to answer.

Night-Train

Thank you.

I agree. I have really been thinking of businesses that I would like to purchase or start from the ground up. I like your idea and I commend you for the property you set aside. There are federal incentives for rural businesses to increase the value and assist them in pursuing their goals to keep their land for farming. It also promotes them to go the extra mile and be creative with energy efficiency. I think there are some smart people who see the value and the big picture.

Can you tell me where to find this data? I’ve found the delinquency rates, but not the dollar amount. I am doing this research project and would really appreciate it.

Thank you!

Sure. Go to the linked site (Fed), choose which delinquency or charge-off category you want to look at, and on that page (it shows percentages), click on the chart icon at the top right corner, which takes you to the data download center where you can download the dollar data and build the charts.