It was a historic day. Google’s market capitalization jumped by over $60 billion, enough to bail out Greece for a couple of years, and handily beating the prior single-day record of $46 billion held by Apple.

The thrilling event occurred on the news that Google’s second-quarter revenues rose 11% year-over-year – which seems like a lot in a quarter when S&P 500 revenues are expected to shrink – and “net profit” rose 17%, while net earnings per share of its class A common stock inched up a measly 1%, which sent these shares up 16%.

Or maybe it was on the news that Google finally hadn’t disappointed analysts’ expectations. Or rather, that they’d finally lowered their expectations enough to where Google could exceed them.

The action gave the NASDAQ a big push to rise almost 1% to another all-time record. It’s now 4% above the prior crazy record of March 2000. And this time, everyone agrees, it’s different.

But at least, Google had a profit. A big one, $3.9 billion, so “earnings” with a plus-sign in front of it, rather than a minus-sign. A feat that seems impossible to reach for a number of other companies in the tech space where profits are optional. Or perhaps even a handicap.

Morgan Stanley’s “New Tech” index is trading at 149.5 times forward earnings, Barbara Kollmeyer at MarketWatch pointed out. And that’s high. But it’s based on pro-forma, ex-bad items estimates of what earnings might possibly look like in the next twelve months under the most optimistic or simply fabricated circumstances. So rose-colored fiction.

As those quarters get closer, analysts whittle their earnings estimates down. By the beginning of the reporting period, they’re then close to something that these companies can actually beat. Even better, those “earnings” to beat might actually be with a minus-sign in front. Just lose less money than expected. That formula works all the time.

So “New Tech” is very expensive. And compared to the peak of the last tech bubble which blew up in March 2000?

“This is probably bubblier than it was then given the lack of market memory,” Keith McCullough, CEO of Hedgeye Risk Management, told Kollmeyer.

Looking at past performance, the “New Tech” index sports an average trailing twelve-month P/E ratio of 69. And it’s high. But it obscures reality.

The P/E ratio of a company that has a loss is undefined. It’s usually expressed as “N/A” or just a dash. It’s thus excluded from the average P/E ratio of the index (table). Hence, only profitable companies are included in the calculation of the P/E multiples of the overall index. Which gives the “earnings” part of the P/E ratio a strong upward bias.

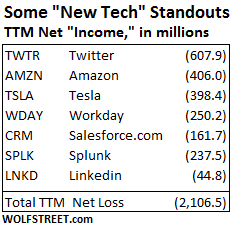

Yet, there are some big losers in the “New Tech” index, including the well-known sinners in the table to the left. These seven companies combined had a total of $2.2 billion in net losses over the past four quarters. Note the three worst offenders – Twitter, Amazon, and Tesla.

Splunk, which had $125.7 million in revenues last quarter, down sharply from the prior quarter, lost $71.2 million in the quarter and $237 million for the year. Yet the company has a market capitalization of over $9 billion. No growth, no profit, no problem. Go figure.

Not to speak of the valuations of Tesla, Amazon, and Twitter. That takes a lot of market enthusiasm to just totally give up on the idea of net profits and focus on the hope that management comes up with some new and more palatable metrics.

Mark Hulbert, who keeps his fingers on the pulse of contrarian indicators, put this sort of enthusiastic disregard of reality into a harsh light:

I draw this worrisome conclusion from this week’s San Francisco Money Show, where hundreds of investment gurus are giving workshops and seminars to thousands of investors. I count on the fingers of one hand the presentations dedicated to managing risk and how to avoid losses.

In contrast, there were numerous workshops catering to greed, with advisers enticing investors with the prospect of triple- and even quadruple-digit returns.

This is a worrisome situation, according to contrarians because at market tops, greed completely replaces fear as investors’ primary concern.

At market bottoms, by the way, fear dominates greed – just the opposite of what prevails today. Consider the Money Show held in May 2009, in the wake of the 2007-2009 bear market: As I wrote at the time, its workshop titles were dominated by the themes of “safety,” “managing risk,” and “survival during market crashes.”

In true contrarian fashion, that came just as the great bull market was taking off.

But, as contrarians constantly remind us, it pays to focus on risk when everyone else is overcome with greed.

Chilling words in this steamy market.

So this time,the asset bubbles are far broader than they used to be, after years of central-bank money-printing and zero-interest-rate policy in major economies around the world, whose sole purpose it was to inflate asset prices. This was supposed to create a “wealth effect,” which was supposed to stimulate the economy. It certainly worked in inflating asset prices.

Now nearly all assets are overpriced. And enthusiasm for even more asset-price inflation is palpable. The insane asset-price stimulus is still rampant, though the Fed has terminated its money-printing binge and is contemplating the idea of raising interest rates from zero to nearly zero. We’ve never had this sort of global environment. Not in 2000, not in 2007. So yes, this time it’s different. But in the wrong direction.

It all boils down to finding the perfect wealth transfer method. JP Morgan did. Read… “Leveraged Loan” Time Bomb Goes Off

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Splunk, which had $125.7 million in revenues last quarter, down sharply from the prior quarter, lost $71.2 million in the quarter and $237 million for the year. Yet the company has a market capitalization of over $9 billion. No growth, no profit, no problem. Go figure.”

What did you expect? There are very few genuine stocks anymore. There are only the horses, the casino counters.

In a time of MASSIVE inflation of money and credit and prodigious oversupply there can be no real economic growth, and rates everywhere are showing this.

All that is left is BETTING.

I tried shorting Amazon and it blew up in my face. As one reader Petunia pointed out, do not try this at home, kids. These things can go up even higher. Amazon can declare a massive loss and declare a stock split the same day and the stock price can hit the stratosphere.

As I never, never tire of telling people unless you plan to do these things seriously, never, ever buy stocks from zombies such as Tesla and Amazon.

These companies are completely disconnected from reality and you’ll never know how they’ll behave. Right now they are doing no wrong despite no profits but, who knows?, perhaps they’ll drop once they start turning profits.

These stocks are better left to those who know how to play a rigged game.

Instead focus on stocks of companies still somehow connected with reality: Royal Dutch Shell, Total (both good buys at the moment in my opinion), Michelin etc. Yes, they may be overvalued, but at least valuations somehow still follow underlying fundamentals.

At the moment it’s nigh on impossible to divine how and when the “No profit, no problem” bubble will deflate: it could go on for another couple years or explode in two weeks. Better be extra careful: nobody ever went broke being cautious.

A special word of advice here regarding car companies: this is the next bubble waiting to brust, and it will probably do so before Twitter, Amazon and Splunk and well before housing.

These companies have to big problems: first they are completely dependent on the latest round of credit manipulation to sustain sales which have no relation with fundamentals. When leveraged to the hilt households buy SUV’s on credit like there’s no tomorrow in basket case Italy, you know you have a big, big problem.

Second, China is their main profit turner. The world seems to have finally woken up to the fact China has been massaging if not downright falsifying macro’s for years now. “Suddenly” analysts realized how Beijing crammed underperforming and non-performing loans in every nook and cranny of her financial system. This is not going to end well for GM and VAG.

Stocks will probably shrug away any bit of bad news from China… for a little while. But when BMW Group AG gets 40% of its profits from the Chinese market… well, it will become impossible to ignore. And when sales in Europe will hit a snag (and they will: we are well past the point of insanity), watch GM, VAG and company start tumbling down.

Well, someone knows something. Housing Starts Jump 26.6%, Building Permits 30% Year-Over-Year In June, yet, both MHK and WHR dropped over a $1 and they were already well off of their yearly highs. Being a short seller, I lit a candle and thanked Joe Pesci.

“Housing starts jump 26% building permits 30%”.

Chinas did to years ago, now they got 20 ghost cities.

Besides you’re looking at multifamily (condo) developments and permits by eager and half broke builders to get a loan and make a little profit so they can exist.

Notes on the three worst offenders – Twitter, Amazon, and Tesla.

As I have written before, stock prices have nothing to do with fundamentals. Having said it again, the most vulnerable of the three is Twitter because it is an easy program to replicate. I wrote a similar program when I worked on Wall St. many years before Twitter came on the scene.

Amazon is harder to replicate because they offer good service, a rare commodity, has a good technical platform, and is well liked by customers. They will be around as long as they maintain good cash flow.

Tesla is the real gem. They make real stuff you can sell. Tesla is the only stock in the entire market I would ever use my own money to buy.

Well I lost my shirt and whole lot more shorting AMZN and broke even on TSLA… Now if I had huge cash chest than I’d short these 2 to hilt :(

That said AMZN is just another retailer burgeoning to become Wallymart of internet but geesh how long can they go on losing money albeit in very competitive retail space where they lost the edge of not charging sales tax?

TSLA – sorry another freakin scam with exorbitant cost being low volume niche player and I’m sure German luxury makers who took years to perfect and refine their technology can easily bring electric cars if they wanted to provided it does not eat into their gas/diesel engines. Musk’s polished BS presence aside this guys won’t cut it in more competitive mid end luxury and new SUV market competing against other German and Japanese companies.

I believe Amazon chooses to be slightly in a loss. They invest heavily in new areas, technology and lines of business. If cash were ever a problem,i believe amazon could easily pull back and show a nominal profit whenever they want.

I wouldn’t touch Tesla with a ten foot pole.

The day the government stops subsidizing Tesla’s overpriced electric cars, you’ll see TSLA head for zero in very short order.

It’s not Tesla’s car business I like, although I think it’s ok, it’s the battery business and aerospace.

Petunia,

Psst – You think Tesla the electric car company which literally buys most components including batteries really has the IP and mfg prowess to compete against Panasonic, LG and probably no-name yet large Chinese company? I think NOT and remember these guys are hemorrhaging lot of cash and losses galore but I guess who cares about profit like early 2000?

Vespa,

I think Musk is the smartest guy in the tech business today. I wouldn’t count on a Chinese company to innovate themselves out of a paper bag. All the nifty stuff they make they were given or stole.

So buy stocks in Australia. Plenty of fine firms not already priced for perfection with decent P/E’s. American bourses are waaay overvalued generally.

Apple = Sony

Facebook, Twitter, Linkden, Instagram and all other social media = Myspace

Tesla = GM

Amazon = Sears

Splunk = Gimmick

Salesforce = yet another App gimmick

Workday = more useless graphs

AND

Google = Yahoo

GDP is dead…

growth is an illusion….

welcome to the new marxist economy

welcome to marxist multicullturism

welcome to soclaism and then communism.

NWO where everyone is equally POOR !

I laughed ‘cos I think you will be noted years from now as the one who predicted the demise of today’s darlings as how many of the hot sotck from the 70’s AKA nifty fifty are still around?

If negative earnings, or loss, can be expressed as a negative number, how come we don’t just go ahead and calculate the P/E as usual for companies showing a loss and show the P/E as a negative number?

I think the reason is because a negative p/e indicates a price below zero.

If you have a p/e = 10/1 = 10, it means you are paying 10 for each point of earnings.

If you show a loss, say the p/e = 10/-1 = -10, it indicates a price per point of earnings less than zero. Therefore the indicator becomes “worthless” as an incentive for you to buy the stock.

Tesla is the new Prius. It is the status symbol of the Green Left, plus a few hardcore techies who love the interconnectedness. One sees many Teslas in California, and a few in other leftist cities. I imagine a Tesla museum some day next to the Tucker museum on the Strip.

Yep – I see so many of them in SF bay area and in my neighborhood… It has become indeed some kind of status symbol which I can’t figure out why but the suckers already bought theirs so demand may be slacking and hey more of new SUVs they sell more $$$ they lose – kind a like Government Motors?

In Florida you see them because they get set aside parking and free electricity too. Lots of places they can park and plug in. All free.