Contributions rose by 5.6%, but benefit payments rose by 8.5%. The Trust Fund paid for the deficit, so its balance declined further, to $2.6 trillion.

By Wolf Richter for WOLF STREET.

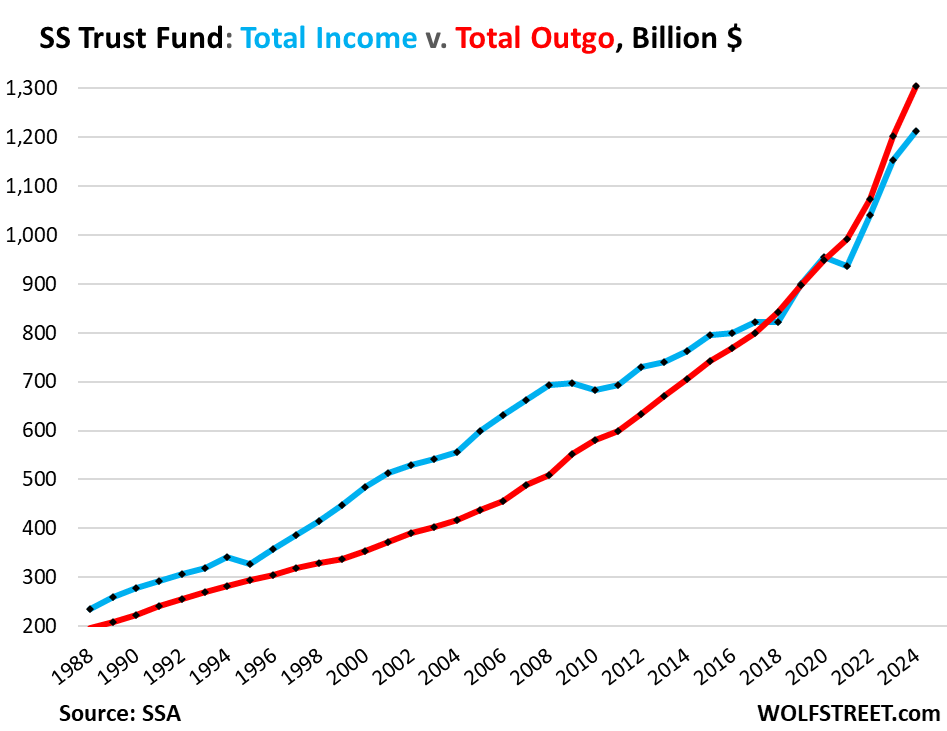

Total income of the Social Security Trust Fund – technically “Old-Age and Survivors Insurance (OASI) Trust Fund” – rose by $61 billion (+5.3%) in the fiscal year ended September 30, to a record $1.21 trillion, according to the Social Security Administration (blue line in the chart below).

By category of income:

- Contributions: +$58 billion (+5.6%), to $1.10 trillion due to employment growth and higher wages.

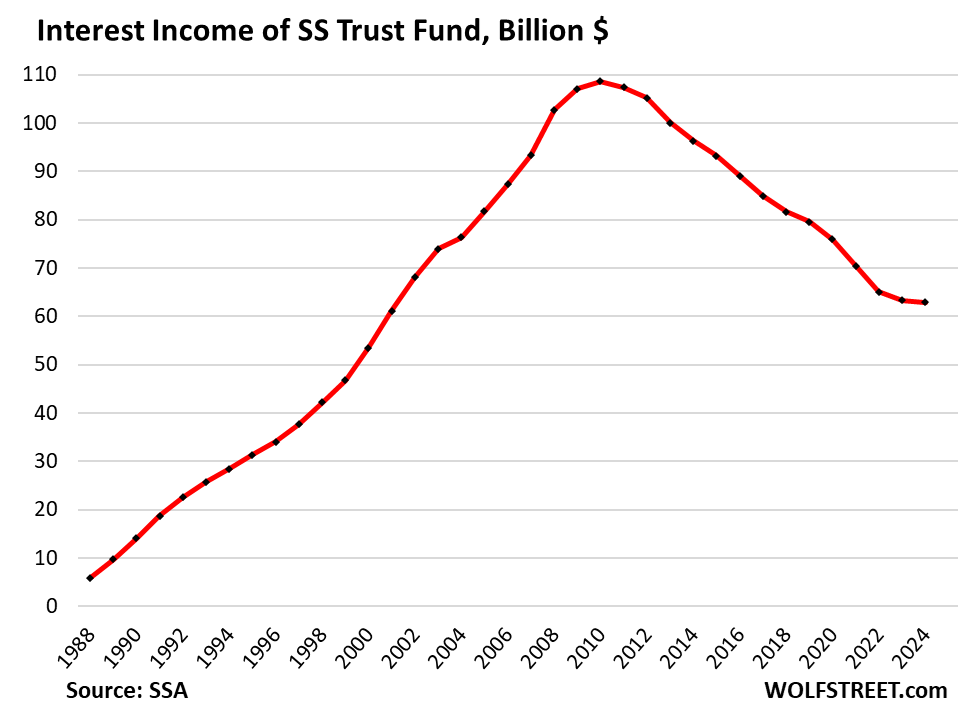

- Interest income from the securities in the Trust Fund: roughly unchanged at $63 billion.

- Taxation of benefits: +$3 billion to $53 billion.

But the outgo rose faster than income. Total outgo rose by $102 billion, or by 8.5%, to a record $1.30 trillion (red line).

By category of outgo:

- Benefit payments: +$102 billion (+8.5%), to $1.29 trillion; more retirees drawing benefits; and COLAs of 8.7% for October, November, and December 2023, and 3.2% this year.

- Administrative expenses: +$500 million to $4.8 billion. They’re relatively small: 0.17% of the Trust Fund balance, and 0.40% of total income.

- Transfer to Railroad Retirement Program: +$300 million to $5.9 billion

When the total income (blue) was above the total outgo (red), the Trust Fund ran a surplus and thereby accumulated assets. When the red line rose above the blue line, the Trust Fund ran a deficit and its assets shrank.

The low 2.5% COLA for the 2025 calendar year will slow the growth of the outgo from that direction, but increasing retirements of boomers will cause the outgo to increase further.

The Social Security Trust Fund.

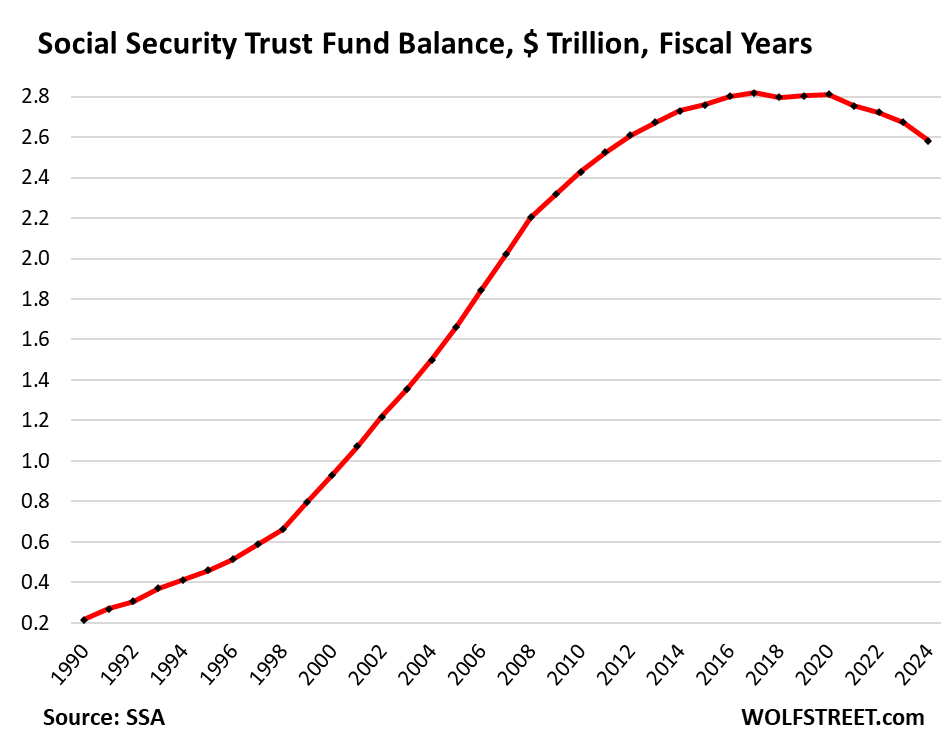

The deficit in the fiscal year was $91.5 billion, the biggest deficit yet, and the fourth year in a row of deficits.

Over the past 35 years, 30 years had surpluses, totaling $2.6 trillion, which accumulated in the Trust Fund. Five years had deficits (2018, 2021, 2022, 2023, 2024), totaling $225 billion.

The shortage between income and outgo is paid out of the Trust Fund, and in the fiscal year, the Trust Fund balance declined by the amount of the deficit, by $91.5 billion, or by 3.4%, to $2.58 trillion.

These figures to not include the Disability Insurance Trust Fund, which by law is a separate entity from the OASI Trust Fund, and is not part of this discussion here.

How the Trust Fund invested the $2.58 trillion.

At the end of the fiscal year, the Trust Fund held $2.39 trillion in interest-bearing special-issue Treasury securities and $197 billion in short-term cash-management securities (“certificates of indebtedness”).

These securities are not traded in the secondary market, and are not subject to the whims of the secondary market, similar to the Treasury I bonds and EE savings bonds that retail investors hold in their accounts at TreasuryDirect.

So the value of these holdings – like the value of investors’ accounts at TreasuryDirect – doesn’t fluctuate with the trading prices in the secondary market. The Trust Fund holds Treasury securities until they mature and then gets paid face value for them. Day-to-day price fluctuations are irrelevant for the Trust Fund.

Investing in Treasury securities when they’re issued and holding them until they mature is a low-risk conservative strategy.

This strategy allows the SSA to operate the system with ultra-low administrative expenses, amounting to just 0.17% of the assets under management.

Fed’s interest rate repression contributed to the deficit.

The Trust Fund earned $63 billion in interest on its Treasury securities in the fiscal year, down by 42% from the peak in 2010, though the Trust Fund balance was a little lower than today.

When the higher-interest-rate securities from before the Financial Crisis matured in 2008 and later, they were replaced with much lower-interest-rate securities as a result of the Fed’s interest rate repression, including QE, which pushed down longer-term interest rates until the 10-year yield finally dropped below 1% in mid-2020.

And the interest income of the Trust Fund – along with the interest income of all yield investors, including savers – took a massive hit.

For example, this fiscal year: If the Trust Fund had earned an average 4.5% on its balance of $2.39 trillion of Treasury securities, it would have earned $107 billion in interest income, instead of $63 billion, and the Fund’s deficit would have been $47 billion, instead of $91.5 billion. Last year, it would have had a surplus!

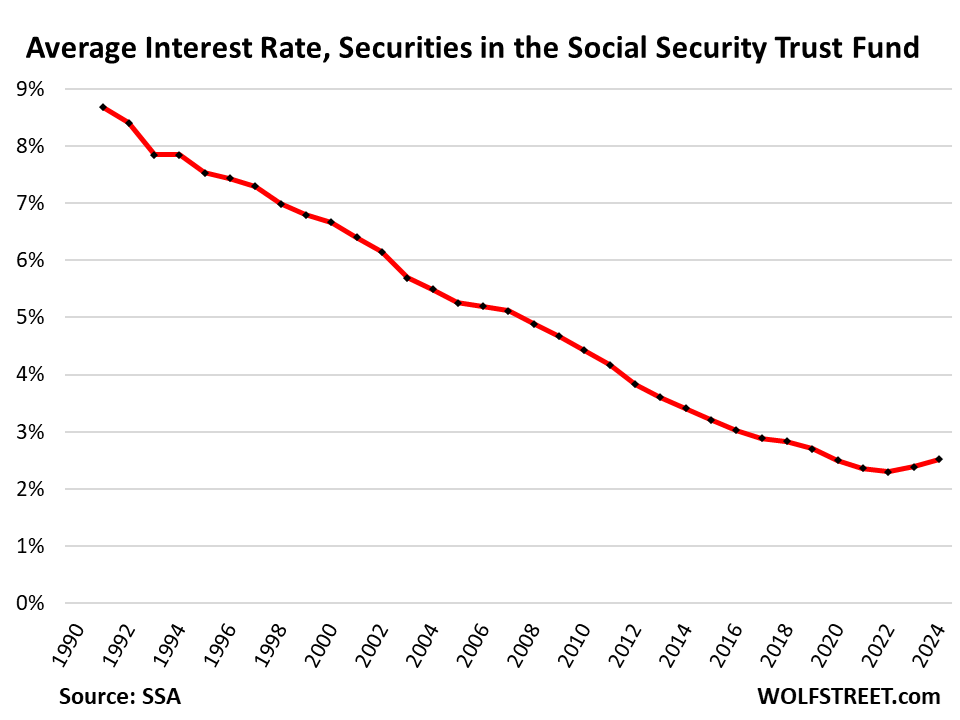

Now, the maturing low-interest rate securities are replaced with higher-interest rate securities, which is slowly pushing up the average interest rate earned by the Trust Fund.

The average interest rate the Trust Fund earned rose to 2.52% in the fiscal year, from 2.39% a year earlier, and from the low of 2.30% in 2022.

Going forward, the average interest rate will continue to rise as those very-low interest-rate securities, including those issued in 2020, are replaced with higher interest-rate securities. For example, the 10-year yield has risen to 4.3%, from below 1% in mid-2020.

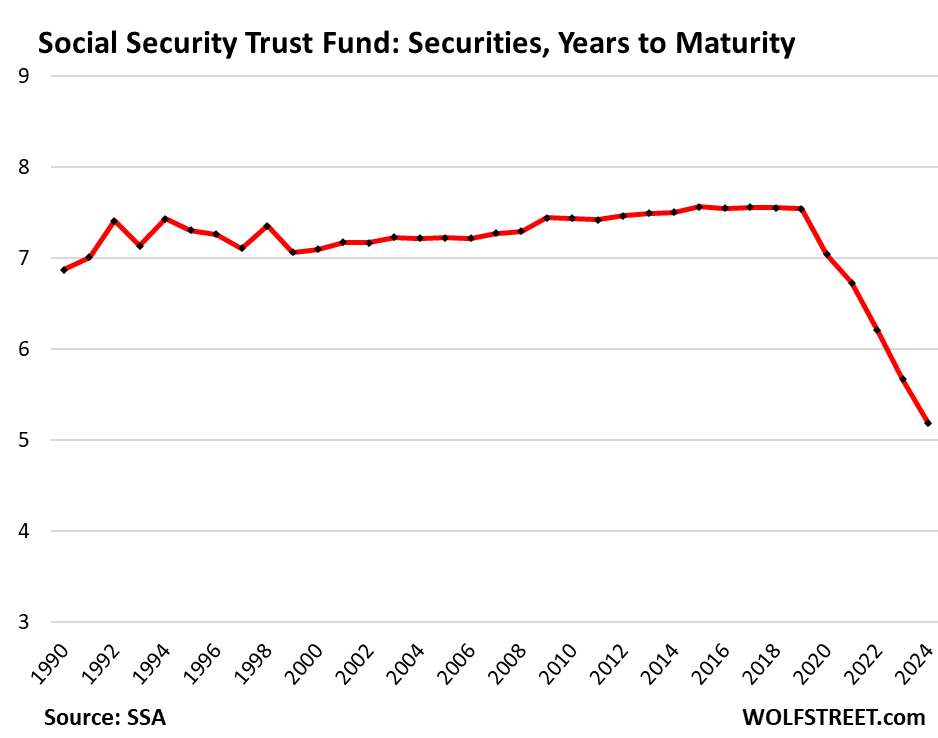

Shifting to shorter-term securities.

The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, likely a strategic decision by the SSA to not load up on the near-0% longer-term securities issued at the time.

In the fiscal year, the average years to maturity declined to 5.19 years, the shortest on record. And the current crop of higher-yielding securities is going to make its way into the Fund a little more quickly.

Tweaking the plan is necessary.

The deficit of $91 billion this year is not large for a $29 trillion economy. If no changes are made to the plan, the Trust Fund will be depleted in about 10 years, and at that out-of-money point, without adjustments till then, either the benefits would need to be trimmed by some percentage to match income on an annual basis, or the general budget would be used to make up the difference. That’s the worst-case scenario, if Congress doesn’t get its act together.

Various proposals have been floated in Congress over the years to tweak the system, but they have gone nowhere. Generally, each proposal tweaks the system in several ways, and each tweak could be relatively small, but combined and over time, it’ll get there. It was done before, and somehow it ended up not being the end of the world. And it can be done again.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So around 2016 is when it leveled off for ~ 4 years and is into decline. I believe the GR moved the depletion date forward by ~ 4 years. I would expect the same to happen over the next five years, and I wouldn’t be surprised to see the terminal date move forward to 2032.

Time will tell, but something certainly needs to be done fairly soon, even if it’s a few modest tweaks. The same can be said for the annual deficits.

But in their last report, the Trustees didn’t move the date further. Demographics have a huge impact. The sudden huge influx of young immigrants in 2022-2024 will further move out the date. These kinds of things are exactly why the date keeps getting moved.

not to worry

FED and CONgress/potus all making sure we

DEVALUE fiat $dollar to make SSI income worth less and less

right now I have dozens of retirees living on less than $1k month

should raise rents but then they will be out on street

won’t even speak about HIGH FOOD INFLATION of 50%

wife spent $400 yesterday at costco and it’s only 2 + 1 daughter in college

TRUE, far damn shore jd:

Two offspring and theirs, total 8 people, in two different HCOL states spending $800 every two weeks for food at Costco, and both thankful for that store…

Degradation of US Dollar continues and continues to penalize folx on fixed incomes and savers of all varieties…

Only recent help is increase in yields of Treasuries and CDs, and WE, in this case the prudent savers We can only hope those yields stay higher than inflation, as SS ”certainly” has NOT, and with good reason as explained by another great Wolf report.

You do understand that the devaluation of USD is happening due to the huge deficit of the Trade Balance, don’t you?!!

Why do you think the yields keep rising, even though the FED cut the rate, because the amount of capital that’s needed to be attracted to finance the huge deficit of the Trade Balance is in direct proportion with that deficit. Just have a look to the data related to exports and imports that were released today. The biggest problem of the US is not the fiscal deficit is the trade deficit, and how to keep financing it in world which is becoming more and more divided. That trade deficit directly impacts the standard of living. So keep your eyes on the real problem and try to understand.

Joe and VNV, I don’t know where you think Costco is such a great grocery chain as I see high prices on pretty much everything in ours. If you want less expensive groceries, go find an Aldi’s .

Although the $5 cooked rotisserie chicken is a good deal.

What is this reference to a “sudden, huge increase in ‘migrants’?” Are they all paying into social security?

This is insane to normalize our open border policy. As if we benefit from these young workers entering our country freely seeking “asylum”? Such baloney!

The effect on our society if much more complex than simply having FICA withheld from “migrants” paychecks (even if they use someone else’s SS# or have a temporary work card.)

Yes, it’s “insane” but it happened. Many are illegal, but many are legal now with work permits or came with visas. If they’re on an actual payroll (not getting paid cash under the table), they’re paying into the system, legal or not (work permits, someone else’s SS#, etc.).

Congressional Budget Office population growth data based on ICE data and Census Data:

We hire “Migrants” and pay under the table, saving thousands each and every week. They are happy and we are extremely happy to have profitable bus…

Wolf, do you believe that we’ll skirt another major recession during the next 10 years? I don’t think we will. It’s reasonable to expect something major to happen within about five years. If so, then the date will jump forward. Until then, yes, it may continue to creep back some.

Cheers!

I think when the AI spending bubble implodes, we might finally get our recession.

But but but I have been told Social Security will not be there for me!

/s

System is perpetually taking in money, you’ll be fine!

Good point Wolf, the immigrants working FICA jobs will bolster fund.

A large portion of those immigrants are working off books and not contributing to FICA

No doubt about that! Most I see in AZ and CA want cash for their pay, especially nannies and landscapers/laborers.

…….and a “large” percentage of Americans are gaining income off the tax books. What’s your point?

Some are paid under the table but the latest estimate by the Institute on Taxation and Economic Policy estimates that undocumented immigrants paid about $26 billion into Social Security and $6 billion into Medicare in 2022.

Another casualty of saving the too big

to fail banks. They screwed up the housing markets, the commercial real estate market, Social Security, pension plans, etc…

But hey, the bankers got to keep their

bonuses.

Considering it’s easier to forecast outgoing $ from the SS trust fund rather than estimate annual taxes Uncle Sam receives, methinks it’s prudent to start trimming from the pot-o-money rather than raise taxes (specifically income taxes) to balance the fund. Another alternative is levying sin taxes on things folks collecting SS spend heavily on. Or tariffs on classes of goods. Perhaps golf clubs, carts, and balls? Jokes aside, there’s at least 10 years to come up with creative solutions. Write to your congressmen and congresswomen.

For non-Americans, please buy our goods. Many thanks.

Tax the living heck out of the rich and wealthy. Done.

Before anyone gets sore. Capitalism, money, and economic systems are not religions (….neither are religions). Get over it.

It would be swell if you provided specifics of what tax rates you think are appropriate. The rich already pay a higher percentage of income taxes than the percentage of wealth they own. What is their fair share?

CHS

The RICH already HAVE way more than their fair share .

That is why they are said to be RICH.

Having way more than your fair share is the very definition of RICH.

The last time I looked, the top 1% owned about 31% of household wealth and paid about 45% of income taxes.

I don’t know if that is fair or not, but whenever I look at the numbers I have a tough time being too angry about it.

The Beatles song Taxman specifies the appropriate income tax rate: “1 for you 19 for me [the taxman].” That is a top bracket of 95%.

ChS, instead of adjusting tax rates for the rich, another alternative is eliminating tax breaks. I remember aimlessly reading through the New York State tax code three or four years ago. I found a tax exemption for watercraft (e.g., boats, yachts) something along the lines of “Sales tax is only applied on the first $1.5M for watercraft.”

I don’t recall what the specific value was. I do remember it being unattainable to most. Likely in the $1.5 to $15M range. That was such a clear example to me of a tax break for the rich.

Gary,

The Beatles may have understated the situation.

According to Wikipedia: through the 60s and 70s the UK’s top rate of income tax was 97.5%.

ie ‘0.5 for you, 19.5 for me’

‘

Ah, the politics of envy. Remember the original income tax only applied to people earning the modern equivalent of about 30 million a year. Look how that turned out.

Don’t worry about it “Happy”. Anyone who envies you will burn forever in the lake of fire, while you will be in bliss forever.

It is so written.

So, all the bookkeeping is fair in long run, thus sayeth the universe.

Yes by all means tax the rich if you want. Would you also be willing to grant the rich greater voting shares in proportion to the degree to which they support our “Democracy” with their money ?

No, I thought not.

Capitalism is a pejorative term invented by Marx – one of the more unsavory characters in history. The penultimate freeloader on everyone who had the misfortune of coming in contact with him. Read a couple of biographies on him.

I myself am not a “Capitalist”, what I subscribe to is Free Enterprise. It true that most economic “systems” don’t work thats why after the collapse it’s free enterprise which slowly rebuilds things. Wise governments promote this process, but there are very few of those as they almost inevitably fall into the hands of plunderers and looters.

As to religion. What we identify as free enterprise flows out of ideas of Natural Rights which go back many centuries but took familiar form in the enlightenment. At bottom Natural Rights boils down to property rights. In the American version, those rights come to human beings from their Creator…so to an extent it is about religion.

You can deny religion but you already use language that implies ideology which, when you look closely at it turns out to be belief based on story telling.

JC Actually I would suspect your beef should be directed to those politicians (of either major party) who are busy running up the debt instead of balancing budgets….Lets give credit where credit is due.

Just expanding on JC’s excellent outline for the…the……whatever they are,

Look up the 1960 Tax Schedule and then adjust for inflation…..it is perfect.

However, Net wealth Adjustment Taxes will have to be made for SURE as we have gone WAY too far. Like the old Jubilee year.

Making the IRS a full fledged part of the MILITARY is necessary as it would solve even bothering with inventing many complicated little financial tricks.

(And of course, a Constitutional Max net Wealth…..$10-20M sounds right….plenty incentive.)

Like Referees (with power) and rules and OF COURSE BOUNDARIES……like any good “sport has.

Then enjoy playing the game with whatever intensity seems best.

BTW, if a player has some misfortune they don’t just throw him out of the stadium and forget him,

I would think it is easily knowable exactly how many social security withholding taxes they take in.

It’s right there on your check and on your W-2.

Heck now if your receive 25 cents from selling on eBay, they are outside at 7am asking for a nickel!

lol just kidding about that last part.

Btw the nickel is the large half dime.

SufferinS, part of the reason I read comments after reading the GDFA are seeing zingers like your last line. Made me laugh out loud yesterday and again today. Cheers.

You’re absolutely right about social security withholding being on paychecks. I overlooked that. Thank you.

Off topic but related as Medicare is a sister program to SS. Medicare is hobbled by provider abuse and even fraud. Recommended for Wolf’s busted IPO list is PAC Health. It is a highflying, fast growing skilled nursing facility. Went public in April 2024. Currently has 284 facilities in 16 states with 27,000 patients, and plans for more acquisitions. Yearly high $42.94 on Nov. 1. Today fell to $21 after Hindenburg Research alleges systematically scamming the taxpayers. Provides detailed report and of interest is that the described alleged schemes are not unique to PAC Health. Also, Mike Leavitt the former Secretary of Health and Human Services under Bush and son of a former Utah governor is one of five corporate directors.

I am reporting fraud today. My mother-in-law had a pressure sore treated by a wound care nurse last January. I (an internist) recommended an enzymatic debridement cream (expensive -$150- and that we purchased) be used to clean up the wound,. The nurse came weekly, I changed the bandages,etc. , on the third day each week in her absence.

Yesterday I received Medicare statements showing “skin grafting” each week in January 2024 and a bill for $8500 each week for three weeks and $10,500 for the last week. Medicare paid their 80%!!!!!!!! This was for one visit each week for 30-45 minutes and for simple irrigation and cleansing of the wound with a subsequent dressing of the wound.

“Skin grafting” is not performed at the bedside at a senior group home. It was simple wound care. I know, I performed half of the wound care. I practice home-care medicine for 12 years.

Thanks for this report Chris; please continue to LUK on here how this finally ends up.

Sister went to ER with no pulse, spend night in horsepistol, and bill was $88,000.00.

Absurd far damn shore!

IMO, if nothing done soon, WE the peasants WILL ”revolt”.

VNV, my 4+ days in the hospital in July for testing, imaging, etc, for a stent to be put in my neck artery ended up costing Medicare $234,000. My part was $240.00 (Plan G deductible)

Also, who are we going to revolt against?

2 months ago I was forced to call an ambulance after my joints weakened, swelled up, and I lost all strength. I had to be wheeled into the ambulance….moi, a hard working healthy guy. It took just three days from feeling great….to feeling off and flu like, to almost croaking (so I’ve been told). Cause?, specialists finally concluded a rampant kidney infection was caused by excessive dehydration, go figure. Too busy on my tractor to take breaks, probably. They even investigated whether I had been ‘bitten’ by some critter but ruled it out.

They were going to ship me out for dialysis and a stay with more specialists and my brother even offered a kidney if it matched, but then after three more days of decline, with huge amounts of intravenous antibiotics and fluids 24/7….the decline in function stopped and today I’m back to 2/3 of normal levels. Prognosis is good. For those in the know filtration dropped to 8 and bad compound levels skyrocketed. Not so good.

So,12 days in hospital, scads of blood work, ultra sounds, EKGs, chest X rays, and after hospital discharge I have now completed 5 weekly lab visits to monitor blood status and improved kidney function, and am now on a monthly recurring lab visit for the next year or until told to stop. I book the lab visits online so there is no waiting for the procedure, and the lab is brand new.

Cost? Nothing….not one blessed cent. The hospital and lab is just 5 years old and the facilities are current. I have never received a bill for any medical procedure in my 69 years….. for broken bones, a cancer surgery(caught at stage 1), and yearly preventative physicals including colonoscopies every five years. I also have no premiums to pay. It is accepted by our society to be more cost effective to keep people healthy than have them missing work or adding a care burden to the ‘system’.

It is called ‘single payer’ and I cannot begin to tell you how thankful all of us are (my friends and family) …..how thankful we are to have it. This year a dental program was made available for low earners and seniors for regular care.

Are there problems with single payer? You bet but they are being addressed to increase doctor numbers and nursing shortages caused by the recent Covid burnout and an aging population. My niece lives in Bellingham. This year she split a finger open with a large rock….gardening. Her co-pay bill was over $6,000. Her family had preventative rabies shots because a bat was flitting around the house. Cost? $7,000 per injection? If they don’t pay it goes to collection and ruins their credit.

The hospital food was pretty bad, for sure. The eggs were inedible. Sure it is all arranged and directed by dieticians etc etc but the logistics of feeding hundreds at the same mealtime could be improved. If the navy can feed an entire carrier a hospital should be able to feed 10% of that number. I just had my wife bring me a sandwich every day.

File a fraud complaint with Medicare. They get reviewed.

Several years ago, in Germany, I sustained an injury that went septic and ended up in a hospital, uninsured. Two surgeries and three weeks later, I was happy to have kept my right leg, while dreading a 6-figure bill. The total was just over $5,000 all-in. What is happening in the US is downright criminal.

My mom was visiting Germany last year. During her visit her legs started to swell and were covered with red dots. She didn’t want to go to the hospital but after a week she finally decided she had to.

They did some blood work and some other tests. The cause was over exertion and her blood thinner medication. At the end my mom was handed the bill. She saw it and asked, “When will they send the rest of the bill?” Confused, the doctor was like, “No. That’s it right there.” The bill was $16.

My mom couldn’t believe it. $16 wouldn’t get you a Tylenol at a hospital here in the US.

What a story and scam not for Medicare but for the drs that abuse the system. I pray that your mom gets the best care possible

What you describe is an example of upcoding. It goes on all the time. Hopefully Medicare will look into your complaint. It might help if patients and caregivers reviewed their Medicare statements and correlated them with what actually was provided and reported questionable bills. Sadly, since they often do not pay, patients and caregivers do not read the statements.

Providers who file improper claims are in violation of the False Claims Act and are subject to penalties and even criminal prosecution. Large dollar violations sometimes in the millions are too often resolved with DOJ consent decrees where violators simply pay back, incur suspension from participation in Medicare or Medicaid, but escape prosecution.

Most of the biggest violators are only caught by employees such as office staff filing a qui tam suit whereby they can receive a part of any money recovered.

In Michigan a section of the public health code provides for health professional license sanctions for “bad moral character” as defined by a propensity for unfair dealing with the public in the practice of a licensed profession. Obtaining or attempting to obtain unwarranted compensation, inter alia, insurance fraud is specifically mentioned in the code. Unfortunately, I have never seen a large dollar consent decree prompt an action by the Michigan Board of Medicine. A problem is that medical boards are passive and generally will only respond to specific complaints filed. I believe that the feds should notify the relevant state’s professional boards of consent decrees and insurance program suspensions. I have seen rare examples where an insurance company complaint has resulted in a professional being sanctioned.

Restitution is included among the code’s sanctions. I have reviewed hundreds of our state’s discipline decrees, but I have never seen restitution imposed. A potential example would be where counterfeit Botox and collagen fillers have been used. I believe that the provider should be required to reimburse individual patients.

This is a long response, but if documented financial abuse has occurred, a complaint to your state’s professional board might be indicated.

I read Medicare part D is supposed to go up 100% next year due to the usual election year shenanigans of trying to delay the increase.

You can buy Part D from many firms and there is a government tool online to search for the best drug plan to fit your prescription needs.

My plan (Wellcare) premium went down 100% for 2025. Lots of options in the Part D game.

How does a premium go down 100%? They just don’t charge one At all? If so, maybe that was temporary and gets reversed in 25 and that’s what the writer was referring to.

Under current law, a Social Security trust fund cannot incur negative balances.

Why isn’t this a template for the the presidents budget? Huh?

Because then the aircraft carrier keeping our enemies at bay would run out of fuel.

How much of that goes to disability and how much has it increased? I volunteer with CASA Court Appointed special advocates and every case I have the parents who lost their kids to CPS are on disability. I didn’t know until this it was so widespread and easy to get. One 27 year old mother who had 4 kids in CPS care was on disability for ADHD. Broken system.

BS. From the Trustees report:

“As in last year’s report, the DI Trust Fund reserves do not become depleted within the 75-year long-range projection period.”

“The DI program continued to have low levels of disability applications and benefit awards through 2023. Disability applications have declined substantially since 2010, and the total number of disabled-worker beneficiaries in current payment status has been falling since 2014.”

I cover this periodically just to crush this kind of BS. This is from last year:

Cue up the anti-boomer comments….

I delete most them, same as with anti-millennial comments. I’m sick of this BS.

You mean it’s worse than what we see?? Yikes.

You’re going to need some AI to delete that stuff, because it’s only going to get worse as the misinformation highway only gets more crowded.

Is there a possible and reasonable scenario where higher interest rates could balance the budget? Or would the high rates probably be driven by inflation expectations that would just drive payments up if the expectations are realized?

I would try to math it out myself but I need to get put the next generation of social security payers to bed.

Short-term interest rates above the COLAs (above inflation) and long-term interest rates 200 basis points above inflation would help a lot. But it would have to stay that way for years because it takes years for higher-interest-rate securities to replace low-interest-rate securities and have an impact.

I am still years away from collecting Social Security but I do receive an annual statement. Here’s a quote from this year’s statement:

“The Social Security Board of Trustees estimates that, based on current law, the Trust Funds will be able to pay benefits in full and on time until 2034. In 2034, Social Security would still be able to pay about $800 for every $1000 in benefits scheduled.”

1. LOL, Reddit said that. My SS statement doesn’t say anything like that. It provides a link to a separate page that says:

“The OASI and DI Trust Funds have reached the brink of depletion of asset reserves in the past. However, in 1977 and 1983, Congress made substantial changes to the program that resulted in the $2.788 trillion in the trust funds today. The combined OASI and DI Trust Funds will be able to pay all benefits in full and on time until 2035. Even if legislative changes are not made before 2035, we’ll still be able to pay 83% of scheduled benefits.”

As I said in the article, there are three options:

1. Congress will tweak the system as they tweaked it before (1977 and 1983) and it will be fine for decades

2. Congress doesn’t tweak the system, and when the money runs out, the system will pay reduced benefits

3. Congress doesn’t tweak the system, and when the money runs out, the shortage will be funded from the general budget. The shortage is really pretty small compared to the $6 trillion budget and $2 trillion deficit.

Most likely they will go with option 3 in the short term as it will be a small portion to cover for a while as they work on option 1.

Option 2, while sensible-is politically devastating.

I’m not a time traveler or anything, so we shall see.

There doesn’t seem to be a lack of commitment in the words of the law,

High strung capitalists seem to have convulsions when someone says something like tax the rich. How about modifying that to say, apply the SS tax to the rich as it’s applied to the poor tax all income (top line) and stop giving an unnecessary and unneeded tax break to those earning over 165K (this year) and stop the corporate giveaway when its employees make over 165K. It’s ludicrous and while everyone knows it’s ludicrous and grossly unfair it’s ridiculously easy to fix. As one Fortune 500 company says: Just do it.

The reason the tax tops out is the benefit tops out as well. SS taxes are already highly progressive.

How about the retirement age get adjusted more in line with life expectancy?

The dirty little secret of SS is most retirees are still working because they have to, and they are still paying into the system, while paying taxes on their “entitlement” benefit.

Me, I’m just enjoying mooching off my massive payment that doesn’t cover my monthly groceries after Medicare premiums and taxes.

I’m still working (and contributing) not because I “have to” but because I “want to.” A good (wealthy) friend of mine is still working not because she has to, but because she wants to because she loves what she is doing (she has her own company). Her husband might like to work, but he was in Big Tech and got aged out of the industry years ago, and is no longer working. Trump and Biden and all the others are still working, not because they have to, but because they want to, unfortunately.

It depends on what you do. If you work in construction, your body will not allow you to work into old age. Other physically tough jobs are like that too. And many jobs are just boring or uselessly stressful, and they’re not fun, and people want to retire from those jobs. But there are lots of money-making activities that are not physically difficult, and that people enjoy doing, and so why quit? Sure, some day. But not when you’re young whippersnapper in your 60s or70s.

SS was designed to not tax the rich. FDR understood that as long as the rich weren’t overly impacted, they wouldn’t put forth the effort to shut it down completely. Tax the rich at your own peril.

Some tweaks that I’ve heard that may have value:

1. Increase immigration (more people paying in)

2. Increase the minimum wage (more getting paid in)

3. By law, increase interest rates on securities (higher earnings)

4. Increase the max income subject to SS by $100k

5. A small corporate revenue (not income) tax.

6. A small increase to individual and corporate contribution rates.

When I was in the early parts of my working life, my full retirement age got moved out by a little over a year. That’s a long-term tweak that didn’t help the fund at the time, but it’s helping now. They could move the full retirement age out a few more months for people who are now in their early careers, and it would help in 30-40 years.

Jack Bogle taxed them. Wall Street hated him.

He put money in the pockets of those whom know how to save and invest.

What a saint he was.

yes yes yes you do not become rich in a vacuum you benefit from all of societies improvements the ss payment should apply to everyone. When I started making enough to not take ss out on my September paychecks the only thing I could think is they stopped taking the money when I can actually afford to pay it in. the spoiled rich will whine about it but they will not go hungry and for a fact they will not miss it. everyone should pay the 8.7% or what ever it is.

15.4% SS/MC for self employed. Not insignificant. My 2022 taxes show a deficit for me being “retired”. I was taxed more than I collected.

This may sound controversial, and it wouldn’t really make a huge dent or anything. But why do people that have millions of dollars in assets qualify for SSI? Maybe instead of taxing benefits, start also phasing out benefits. Someone with $5 million in assets aside (from primary residence) doesn’t really need it.

Talk about a lack of the all important “fairness”. You pay for something your entire working life and when it’s time to collect what you paid for you’re told you can’t have it because “you don’t need it”.

Instead of collecting social security, they should die. It’s not like society has anything good for them to do. What use are these people if they can’t work and be factored in as a technical analysis indicator?

/s

Change the law so SS invests like state pension funds. They make way more than SS 2.5%. Stop funding government deficit by buying low yield federal bonds. But that’s precisely why this change will not be made.

1. In 2000-2002, the S&P 500 lost 50% of its value. In 2007-2009 it happened again, -50%. Money printing finally bailed it out. At the time, pension funds were on the verge of collapse, hugely underfunded. So cut benefits by 50% if market values tank like that?

2. The good thing about SS is that Wall Street gets exactly $0 from it. That’s how it should be.

3. You can privately invest in stocks, cryptos, commodities, CRE, and election bets if you want, but do not plow MY money into it. Plow YOUR money into it.

Great answer Wolf!!

I’m disagree. Treat it like a sovereign wealth fund, like Norway, we would have several times the current balance. Yes, there are stupid sovereign wealth funds, like those in the middle east, and yes, the value can fluctuate, but even a 60/40 fund would demolish the returns of the current system. Chile is another positive example.

Happy1

The sovereign wealth fund of Norway is funded from the profits of national (state owned) oil and natural gas production. It’s NOT a result of taxpayers or future beneficiaries contributing to it. That’s an entirely different beast. Norway is a tiny country with a huge mostly state-owned oil and gas industry. And they nationalize a part of the profits from that industry into their Government Pension Fund of Norway.

So let’s nationalize the US oil and gas industry, and channel the profits to the Social Security Trust Fund, instead of to dividends and share buybacks. That would be the equivalent of what Norway, Saudi Arabia, and others with national oil companies have done. But that’s not the American way, we don’t nationalize oil companies in this joint here. Our pensions are paid for by the future beneficiaries (the current contributors), not by nationalized oil companies.

Nope, if you want to invest in stocks, invest in stocks. But keep taxpayer money out of the stock market.

If I hear stocks, CRE and cryptos in the same sentence then I just shrug and move on. You don’t really see the difference stock vs crypto?

Not anymore, LOL

Current SS tax rate of 6.2% (for employee & employer) has been in effect since 1990. Simplest solution would be for Congress to increase rate by .1% or .2%/yr. EITC could be increased to offset extra SS taxes for working class families. Same would happen for Medicare tax of 1.45%.

This cannot be the only solution. There must be benefit cuts or increases in the full retirement age. This must be achieved with bipartisan compromise. It happened with Reagan and a Democratic house in 83, we way overdue. Both sides have to give a little.

H

Nope.

It is bleed the rich time.

The top 10% have been bleeding the other 90% for the past four decades.

It is now time for the top 10% to be bled.

OTB, I think you need to look at who pays the taxes in this country.

G

I have looked at who pays the taxes in the good ol USA.

The top 10% have been getting a free ride.

Wolf,

The social security site also provides the COLA increases by year. If you add these to the Average Interest Rate plot, you can see the impact of QE.

As a thought experiment, I asked how much more would be in the trust fund if it had been paid a historically reasonable interest rate from 2013 until 2023. My numbers (not compounding interest) is about $380 Billion was stolen from the trust fund by QE. In that same time period the Fed paid the treasury over $800 Billion, so our government (effectively) took it out of the Social Security Trust Fund and put it into the general fund.

Now this doesn’t fix the long term problem completely, but it certainly makes things look much better. That says to me the FIRST thing the government should do is agree to pay the shortage out of the general budget, or at least agree to put half the Fed remittances during QE into the Social Security Trust Fund.

I am old enough to remember the 80s discussion on fixing social security. At the time the actuarial projections believed the fund would peak in 2018 at 5.8 trillion. This assumed normal interest rates. Based on the info in this and other articles it looks like 2.8 trillion is what happened so we lost 3 trillion from interest rate suppression.

In retrospect the concern that 5.8 trillion would greatly exceed the national debt now seems silly. At the time people said they might have to buy state debt or even invest surplus in the stock market.

The loss of better compound interest makes a pretty big difference over 40 years.

Another way to look at the impact of interest rate repression is to look at the real (using 2010 dollars) trust fund balance per capita. If I am doing the math right that figure has dropped by 30% since 2010. For a true retirement trust fund that figure should be stable. The gap to restore the real per capita balance to its 2010 level ties to the $800B figure of FED remittances to Treasury you note.

Wolf who manages the investments of the SS Trust?

The US Treasury Department.

I’ve never really been an anti Fed person, but now that I’ve reached retirement age (2025) how can I keep from being anti Fed when you begin to realize the REAL devastation that the zero to near zero interest rate policies have produced. I find myself camping more and more in the “reign in the Fed” Camp these days. I truly hope a movement along these lines builds because the results of the Feds actions are nothing shy of criminal.

While the charter of the Fed hasn’t changed significantly, the economic thinking has changed a lot.

From being a lender of last resort, the central bankers in the West are fine tuners of the economy. Intervention has become more frequent and there has been total disregard for asset bubbles. The Fed publicly states that they do not believe in asset bubbles. Yet the two of last three recessions were caused by asset bubbles breaking.

They are singlemindedly focused on inflation and unemployment and pay no attention to everything else (wealth disparity, debt build up, unsustainable deficits etc.).

The Fed is a giant ship and barring any legislative action, this is likely to continue. The proxy war is against the currency. Debasement is the future till there is bond market revolt.

The fundamental shift of the Fed has been to take more and more risk out of the banking system.

This is praiseworthy move.

“Shifting to shorter-term securities.

The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, likely a strategic decision by the SSA to not load up on the near-0% longer-term securities issued at the time.

In the fiscal year, the average years to maturity declined to 5.19 years, the shortest on record. And the current crop of higher-yielding securities is going to make its way into the Fund a little more quickly.”

And if those funds had been invested in the S&P500 20 years ago, we would be sitting on a significantly higher balance. Paying into Social Security should be considered as investing in the American economy and Social Security should be able to do the same. Of course this means a large captive buyer of government debt has shifted to equities, putting upward pressure on rates. The wage amount subject to Social Security should also be increased. Talk of reductions in benefits irritates the heck out of me when you consider the “limitations” being placed on the fund from an earnings perspective.

You invest YOUR personal money in stocks, cryptos, or whatever. That’s what you have personal funds for.

SS is “old age and survivors insurance” it’s insurance. It needs to be there when needed.

The S&P 500 plunged 50% in 2000-2002 and plunged again 50% in 2007-2009. It took the S&P 500 13 years to get back to where it had been in 2000. The Nasdaq plunged 78% in 2000-2002 and didn’t get back to its 2000 high until 15 year later. Stocks only recovered due to huge amounts of money printing.

When stocks crashed in 2000, it shut down the budding efforts in Congress to invest some of the Trust Funds in stocks. Wall Street was salivating over it.

But after stocks crashed in the 2000-2014 period, most pension funds were on the verge of collapse, totally underfunded. Only the Fed’s 14 years of money printing bailed everyone out. But now we have inflation back, so forget money printing.

Are people so unaware of how stock markets behave?

Underlying the earlier comment is an assumption of efficient market. Therefore every price is always correct and stocks only go up.

People no longer see investments as a liability and asset matching process. The idea is to increase asset values supported with more and more debt.

Who needs income when wealth is going up so fast :)

Social Security is essential for millions of people and important for millions more. The fact is we eventually get to a point where we cannot work to support ourselves. Thats part of why we SAVE and invest.

As Mr. Wolf so concisely points out, there are relatively easy paths to fixing things (assuming the currency is not completely destroyed).

On the other hand, most everyone Daylight Savings and twice a year time changes to end. Legislation was even passed in the Senate in 2022 I think. Yet here we are in 2024 and the change is moldering in the process somewhere.

If our current “Democracy” cannot bring something relatively uncontroversial to a conclusion, what hope is there for fixing Social Security ?

Re: (assuming the currency is not completely destroyed)

I think we’re actually pretty close to Banana Republic destruction levels — but thank God for reserve currency status and the post GFC economy that relies exclusively on asset bubble management. Essentially there’s very little real growth not linked to financial speculation or manipulation — but, for now, the empire is moving forward. I don’t think very many people realize that we’re at a fork in road inflection point!!!!

Social Security will be interesting to watch as baby boomer dynamics really begin to unfold.

Simple solution:

Each person has his/her SS account. SS taxes collected go directly to that person’s account. The account buys a selection of Bills, Notes and Bonds which are reinvested via a DRIP until retirement or disability.

The account proceeds can be inherited by the spouse or Children under the age of 21. Automatic cutoffs can be implemented(death of spouse, completion of 4 year degree or age limit 25, etc.

This is the foundation. I’m sure many tweaks can be added for fairness.

That’s not how insurance works. Insurance spreads the risk. Part of why people who live till 100 collect so much in SS over the 35 years compared to what they paid in (it’s a really good deal for them) is because many people die during their working years or soon after retirement and don’t have spouses and kids who get survivor benefits, and the funds they paid in go into the kitty to pay for the retirement of people who live till 100.

Health insurance, auto insurance, private pensions, etc. they all work on the same principle. People who never had an accident pay for the damages caused by drivers who did have the accidents. It’s just how insurance works.

Otherwise, you’re just self-insured, which is what you propose, and which is what you should do with retirement anyway, you should save for retirement and have assets, that’s your self-insurance for retirement. SS is just the bottom layer of your retirement safety net. SS is officially called “insurance” for that reason — “Old-Age and Survivors Insurance” (OASI).

My CPA reviewed my SS records and did a little compound interest calc based on the average 30 year bond rate over my lifetime. I could have retired at 65 with 2.5M in my account under a 30 year bond DRIP.. Even 2.5m at 3.5% interest I’d be doing far, far better than currently. After I’m gone and my wife is gone then the proceeds could revert back to a general SS fund.

Banks are allowed to compound interest….why not the working stiff? As it is, I do love my work but there is no way I can retire and I just hit 75. SS doesn’t cover squat.

I just did the math in your CPA example, but since I don’t know how much you made, I assume you earned more than the taxable maximum each year from 1975 through 2024, meaning that this is the maximum you and your employer would have contributed to SS, to get the maximum benefits.

You and your employer, or you alone if self-employed, would have paid $486,000 into the system. That’s the maximum possible since the contributions are capped. If you earned 3.5% interest (the figure your CPA used) every year on all your funds, so the $486,000 plus interest and interest on interest in prior years, you would now have $963,000, not $2.5 million.

These contributions would pay for maximum benefits. If you retired at 70 this year, the maximum benefit is $4,873 per month, or $58,476 per year.

Assuming an average COLA of 3% every year (last 6 COLAs are: 1.6%, 1.3%, 5.9%, 8.7%, 3.2%, 2.5%), your SS benefits would grow every year, $60.2K in 2025, $62.0K in 2026, etc. until in your final year, when you’re 100, you would make $137.8k. In total, all added up, your total SS benefits for 30 years would amount to $2.78 million.

So that was the math. I have no idea what your CPA was doing. Smoking dope?

Here are the other issues:

1. You put your personal money in bonds and stocks and then fire your CPA because he is an idiot.

2. SS is “insurance” – the I in its official name, OASI

3. Your CPA wants you to be “self-insured” for Old Age. And that’s great, that’s what you do with your personal money.

4. Your CPA is an idiot because he cannot distinguish between insurance and personal investment. Think of how much money you could have saved by not paying for auto insurance, health insurance, and homeowners insurance.

He’s in SF. Maybe you two can grab a beer. LOL!

Why should Joe6Pack not get to compound interest? If the feds can require “insurance” then surely the retiree should be on the same level playing field as Bankers with their Wharton degrees…? I mean, we do call SS a benefit, yes?

FWIW, name the public school that teaches kids how to balance a checking account, formulate a budget, how to invest….

Of course, first the schools need to teach them reading and math.

See my comment above — the revised version with the math — in reply to yours.

The first version which you might have read didn’t have the math in it. It took me a while to do the math.

Excellent explanation of social security insurance! As a retired CPA I agree with your analysis. I took SS early at 62 and invested the difference in stocks and bonds (that is my personal retirement savings that I didn’t have to spend) from age 62 until now, benefiting from compound interest to this day. But you have to make over 8% on the money to make it work in your favor (this year the S&P500 index funds are up over 21%).

This is just so so stupid. The shortfall can be entirely eliminated by simply lifting the cap on how much income can be taxed for SS. There are millions of households who make well over 250K a year who pay zero SS tax above the current legal threshold. Either lifting or eliminating that cap would solve the problem, its just that the wealthy do not like to have taxes going up so there will be lot of groaning and complaining about it. What else is new. And yes, I count myself in that group of people who would be taxed at higher rate. In my opinion, well worth the money. Much better than spending it on nuclear weapons. I want grandma to not have to eat crackers and die of exposure.

Read that in the future, the remaining people will build floating cities couple of miles above the earth to avoid the radiation. It beats going to Mars.

Anton,

It’s not like the govt will stop spending on nukes or anything else. Just more debt.

BTW, you are confusing high income with “wealthy”. Younger people can have boatloads of income and haven’t had enough time to become wealthy.

You’re also forgetting…..37% Fed tax, up to 14% state tax. You want to throw another 6% onto that? You’ll certainly keep a lot of younger workers from becoming wealthy.

The Cap is per person on their earned income and is 176,100 for 2025 and goes up every year. If you eliminate the cap without raising benefits in tandem to those paying the extra money in, which I assume is what you are suggesting or it wouldn’t make any difference, then you are advocating for a forced bailout from that group. That isn’t how insurance works. That’s socialism and targets the upper middle class. A single earner supporting a family of 4 or 5 on 200,000 a year is not “rich” in any part of the country and should be able to decide for themselves how they want to contribute to charity, not the government. The people with the real money are so high up you can’t see them and they don’t pay ANY OASDI tax because all their wealth is generated by capital gains and asset appreciation.

I’m bias, but I wouldn’t consider TLT a safe investment.

The really sad and pathetic issue for social security recipients is that the government has not raised the threshold where social security income starts to be taxed since 1974. It is ridiculous that social security money is supposed to be used to help elderly people, yet they are taxing them using threshold numbers from 1974. That number should go up each year by the CPI, at least, and should be adjusted now. Trump wants to get rid of taxing social security income altogether, which would be a good idea.

As unpleasant/tough as it is for people in the income category where benefits get taxed, those taxes brought $53 billion into the Trust Fund in the fiscal year. Without it, the deficit would have been 50% higher.

I’m awfully sorrry, but the deficit doesn’t matter and neither do taxes:

Trump said. “People on Social Security are being killed, and one of the things I’m doing is no tax for seniors on Social Security, and I’ll get it done quickly

We need to e brace higher deficits maga rocks lol couldn’t resist

Let them eat inflation Maria Antoinette

$53 billion is a drop in the bucket compared to the current $1.7 trillion deficit. Seniors were forced to pay into social security their whole working lives and expect to be rewarded for the government-forced “investment” (you cannot opt out of paying into Social Security). The government taking money out of social security benefits is obscene, the benefits are low enough already. Even states with notoriously high state income tax rates, like California, do not tax social security benefits.

How about this little project for the IRS, Now that the IRS has more IT resources:

To streamline inheritance tax – for more transparency for the treasury department, for the national annual budget, and for more visibility for family financial planning.

(voluntary) Amortizing inheritance tax over work-life expectancy for individuals with over $12 million or more of present net worth.

Voluntary as in behavioral economics – give them a nudge, incentive to do what is good for them, for their wealth and for their families and descendants.

This is a suggestion to get the richest “top 1% or 3%” to pay their inheritance tax, pay as you go at their convenience; to amortize this over about 10-20-40 years, depending on work/life expectancy, just as a reverse RMD, no R-in-required, as it would be V-voluntary, O-optional, depending on individual willingness. Some people might want to start this about 5-years before estimated life expectancy, but then it would be less manageable, it would be better to spread it over longer period of time.

Make it optional, voluntary just like IRA contributions, if one wants to pay one year, and not pay another year, it is Ok.

So that high wealthy older people do not get to scramble at end-of-life, and expend time and treasure on how to not pay so much in taxes, on how to find loopholes

That could be an answer for https://patrioticmillionaires.org/ So if these patriotic millionaires, Warren Buffet and billionaires for example, if they (voluntarily) want to do this, to pay on a monthly or yearly basis, they could, for their benefit really.

Suppose a person is now worth 20 M, and expects to have more at the end-of-life, the person work life expectancy could be 20 to 50 years from now.

We know inheritance tax kicks in after 12 Million net worth. Suppose inheritance tax is 45% for over 12 M. So amortizing this over 50 years; common sense would say the percentage would be about 1% per year, over 50 years.

Suppose the actuarial number is to pay one 1% per year. Of course if work life expectancy is 25 years, then the pay would be about 2% per year, or 0.2% per month.

Now that the IRS has more IT resources, they could make a project to put the money from individual contributors into a TSP-like accounts for the gov. that could buy treasury bills on behalf of the gov. and they can compute how much each contributor account grows over time. This way, at end of life, they could compare that to the actual inheritance tax, then pay back or ask for the difference. Anyway IRS personnel usually get involved in the accounting after end-of-life; but then lawyers get involved; well this time it’s pro-active, before end-of-life, to get more streamlined results, less lawyer fees.

The gov. is borrowing from the SSA fund, etc. also from the real TSP fund, they could just take from this (above) fund, count it in the plus column.

An idea would be that the IRS would have a line item on the 1040 for the yearly payments that would add up, accumulate against their inheritance tax, so that at the end-of-life event they would owe nothing or not much, or even their estate/inheritors could be getting a refund if they overpaid. Just like a reverse mortgage.

The Treasury can make it much easier for these high net worth individuals to have an IRS agent dedicated to a few of similar accounts, that would be worth it, I guess. Have people get their own accounts, like savings accounts; much easier, they could buy treasuries in these accounts that mature and be given as payment for taxes. Or they could pay it when they pay their monthly/quarterly estimates. On the part of the Treasury dept., there would be visibility, transparency to know how much $$ it is getting, every year or even every month, into the near future.