An increasingly important question in iffy times. Here are the holders as of Q4, who dumped, who bought.

By Wolf Richter for WOLF STREET.

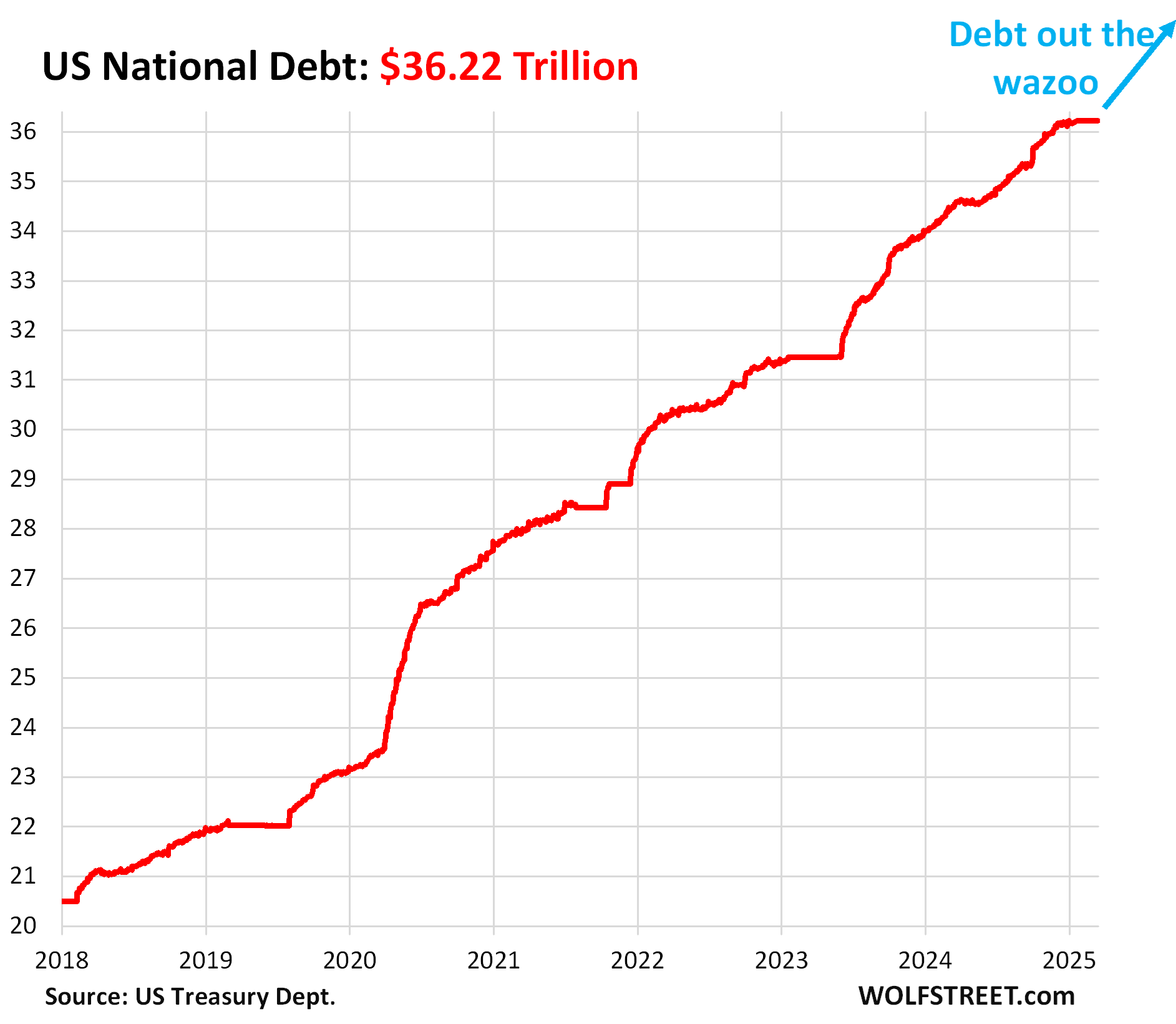

When the incredibly ballooning US national debt reached $36.22 trillion in January, it hit the “Debt Ceiling,” with which Congress prevents the government from borrowing the money needed to spend the money Congress told it to spend.

In the past, just before the government ran out of cash, Congress makes a deal with itself to raise the debt ceiling, upon which the debt spikes by hundreds of billions of dollars in just a few days as the government borrows huge amounts to refill its checking account. The flat parts followed by spikes in the chart reflect that dynamic.

These are Treasury securities that private and public entities in the US and across the world hold as interest-earning assets. The question is: Who holds this debt? And who has been buying it even as the Fed has been shedding its holdings at part of its $2.2 trillion in QT?

Who held this $36.2 trillion in Treasuries at the end of Q4?

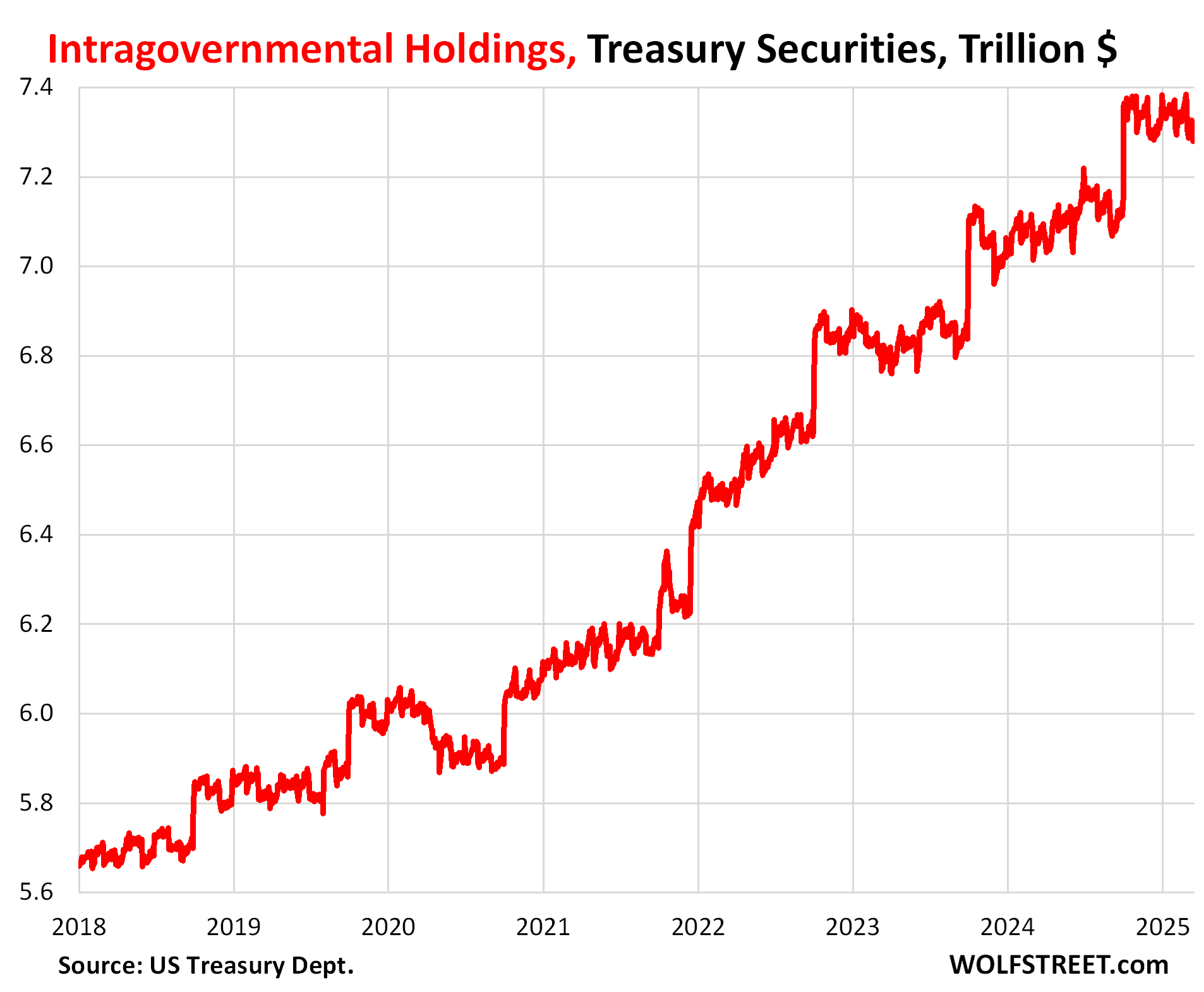

US Government entities: $7.34 trillion. These “intragovernmental holdings” consist of Treasury securities held by various federal civilian pension funds, military pension funds, the Social Security Trust Fund (I discussed the Social Security Trust Fund holdings, income, and outgo here), the Disability Insurance Trust Fund, the Medicare Trust Funds, and other funds. These are securities that are not traded in the market.

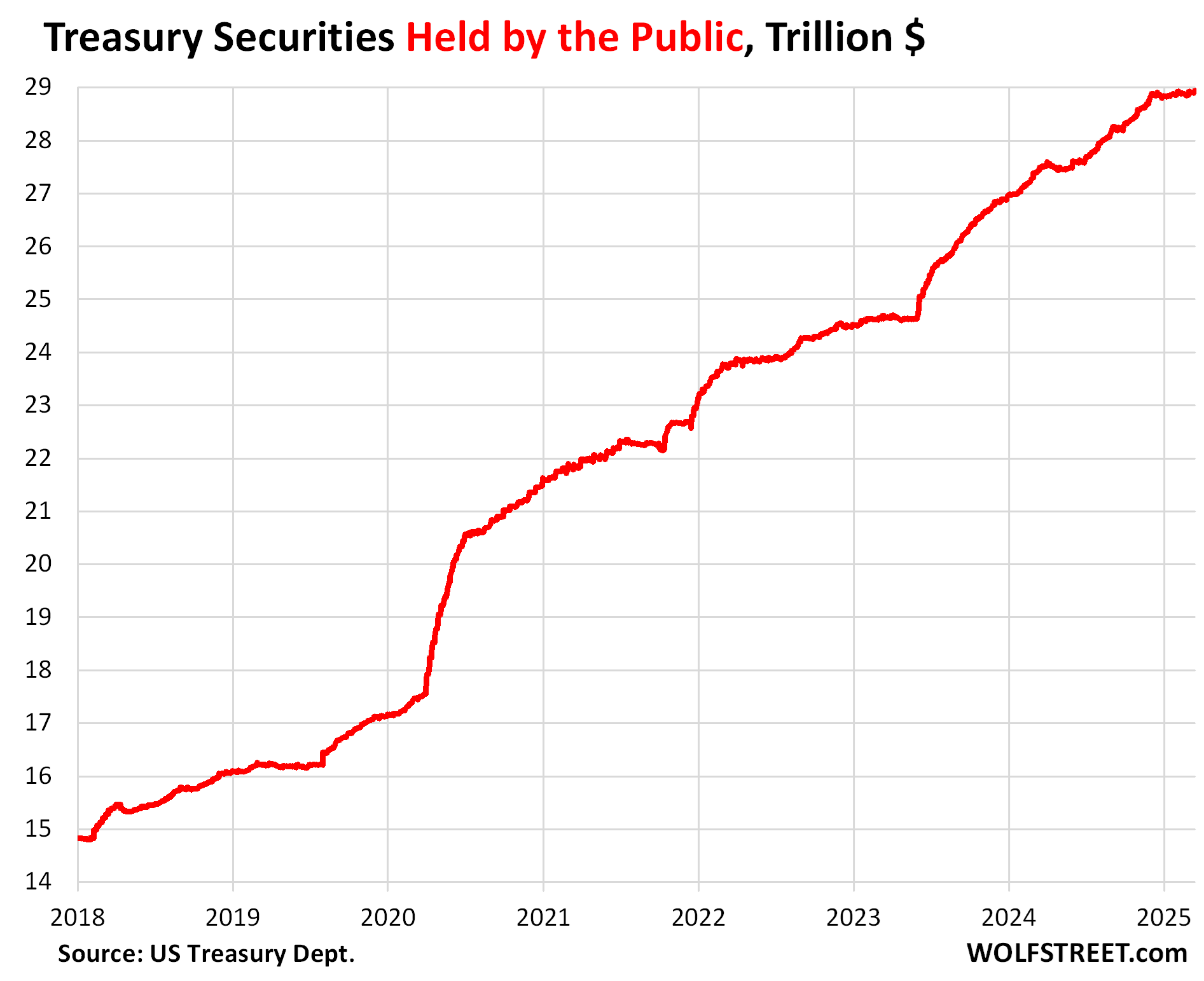

The “public” held the remaining $28.83 trillion in Treasury securities at the end of Q4. Most of these securities are publicly traded and their holders are spread around the US and the rest of the world.

It’s these securities “held by the public” that we’re going to look at here.

The “public” held these Treasuries, by type of security (as of the end of February, published by the Treasury Department).

Publicly traded:

- $6.4 trillion in Treasury bills (short-term securities of 1 year or less)

- $14.7 trillion in Treasury notes (2-10-year securities)

- $4.9 trillion in Treasury bonds (20-year and 30-year securities):

- $2.0 trillion in TIPS (Treasury Inflation Protected Securities):

- $0.63 trillion in Floating Rate Notes (FRN)

Not publicly traded:

- $575 billion in Treasury securities, such as the Series I Savings Bonds, Series EE Savings Bonds, etc.

Who is this “public” that holds these bonds: 30.2% are foreign holders.

Foreign entities held $8.5 trillion, or 30.2% of the publicly traded debt at the end of Q4. These holders included (Treasury Department data):

- Foreign private-sector entities: $4.73 trillion

- Foreign official entities, such as by central banks: $3.78 trillion.

They held in total:

- $7.31 trillion in long-term securities

- $1.2 trillion (14.1%) in T-bills.

That ratio of T-bills to total foreign holdings has been between 12.1% and 14.6% since mid-2020. Before the pandemic, it was in the 10% range.

But they shed securities: Foreign entities shed $166 billion of Treasury securities in Q4, or 1.9% from the record in Q3 ($8.69 trillion), led by:

- Top six financial centers (London, Belgium, Luxembourg, Switzerland, Cayman Islands, and Ireland): -$60 billion

- Japan: -$36 billion

- Brazil: -$33 billion

- India: -$28 billion

- Euro Area: -$12 billion.

But other countries added to their holdings over those three months, including Canada (+$11 billion).

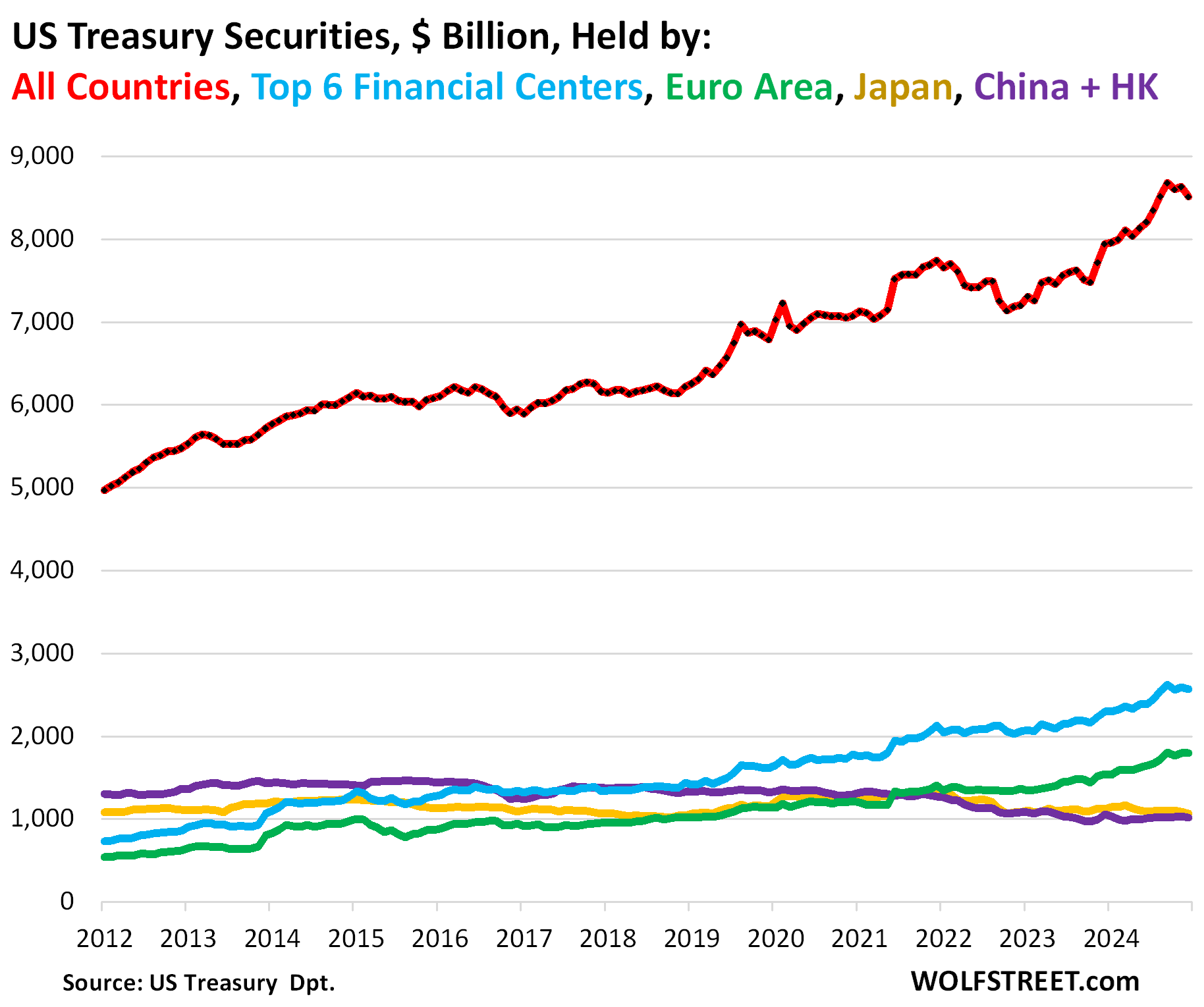

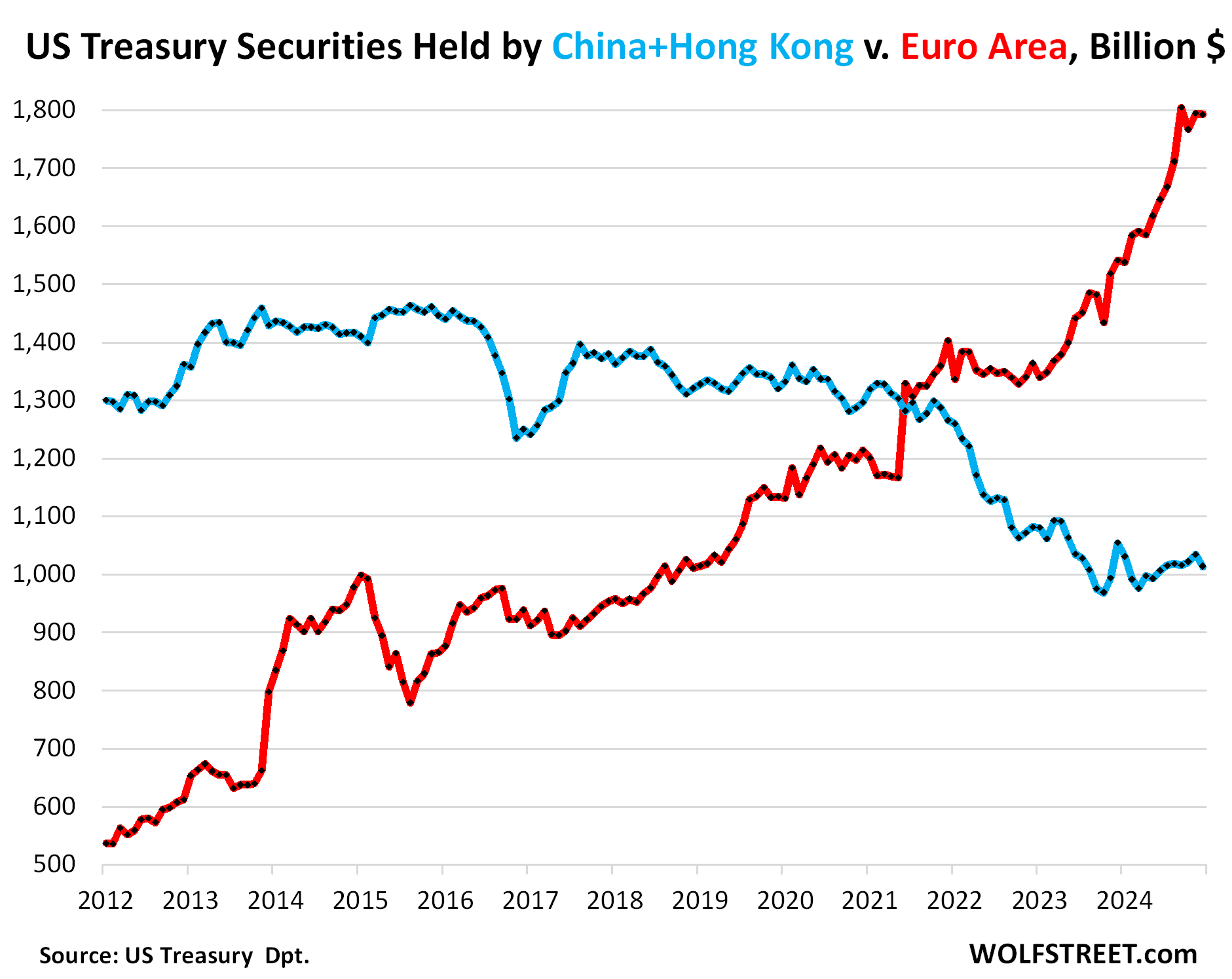

The biggest foreign holders:

- The top six financial centers: $2.56 trillion (blue)

- Euro Area: $1.79 trillion, which includes three of the financial centers (green)

- Japan: $1.06 trillion (gold)

- China and Hong Kong combined: $1.01 trillion (purple).

Top 6 financial centers include US corporate holdings: $2.56 trillion, down by $60 billion from September.

US corporations hold a portion of these Treasury securities to park their overseas profits overseas, as to not have them taxed in the US. Ireland and Apple were a big example of that, as a Senate investigation in 2013 revealed.

Euro Area and China: The Euro Area – which includes the three financial centers Luxembourg, Belgium, and Ireland – has been a massive purchaser of Treasury securities over the years, even as China and Hong Kong combined have been backing away for nearly a decade. The Euro Area now holds far more than China has ever held. But over the past three months, the Euro Area shed $12 billion:

Canada has emerged as a large buyer since the pandemic, more than tripling its holdings over the past three years to $379 billion.

Other big foreign holders include Taiwan ($282 billion), India ($219 billion), Brazil ($202 billion).

Holders in the US are 69.8% of this “public”:

US mutual funds: 19.3% or about $5.5 trillion of the debt held by the public. This includes bond mutual funds and money market mutual funds, according to the Quarterly Fixed Income Report for Q4 from SIFMA (Securities Industry and Financial Markets Association).

Money market funds alone held $3.0 trillion in Treasury securities, including $2.4 trillion in T-bills.

Money market funds added $335 billion in Treasuries in Q4, amid an overall surge in money market fund balances.

Federal Reserve: 15.2% or $4.29 trillion of the debt held by the public as of the end of Q4.

Under its QT program, the Fed shed $93 billion in Treasuries in Q4. Since mid-2022, it has shed $1.53 trillion in Treasuries and $2.2 trillion in total, as of the Fed’s early March balance sheet.

US Households and nonprofit organizations: 9.5% or $2.68 trillion of the debt held by the public at the end of Q4 (Federal Reserve data). These are investors who hold Treasuries in their accounts in the US. But they shed $229 billion in Q4.

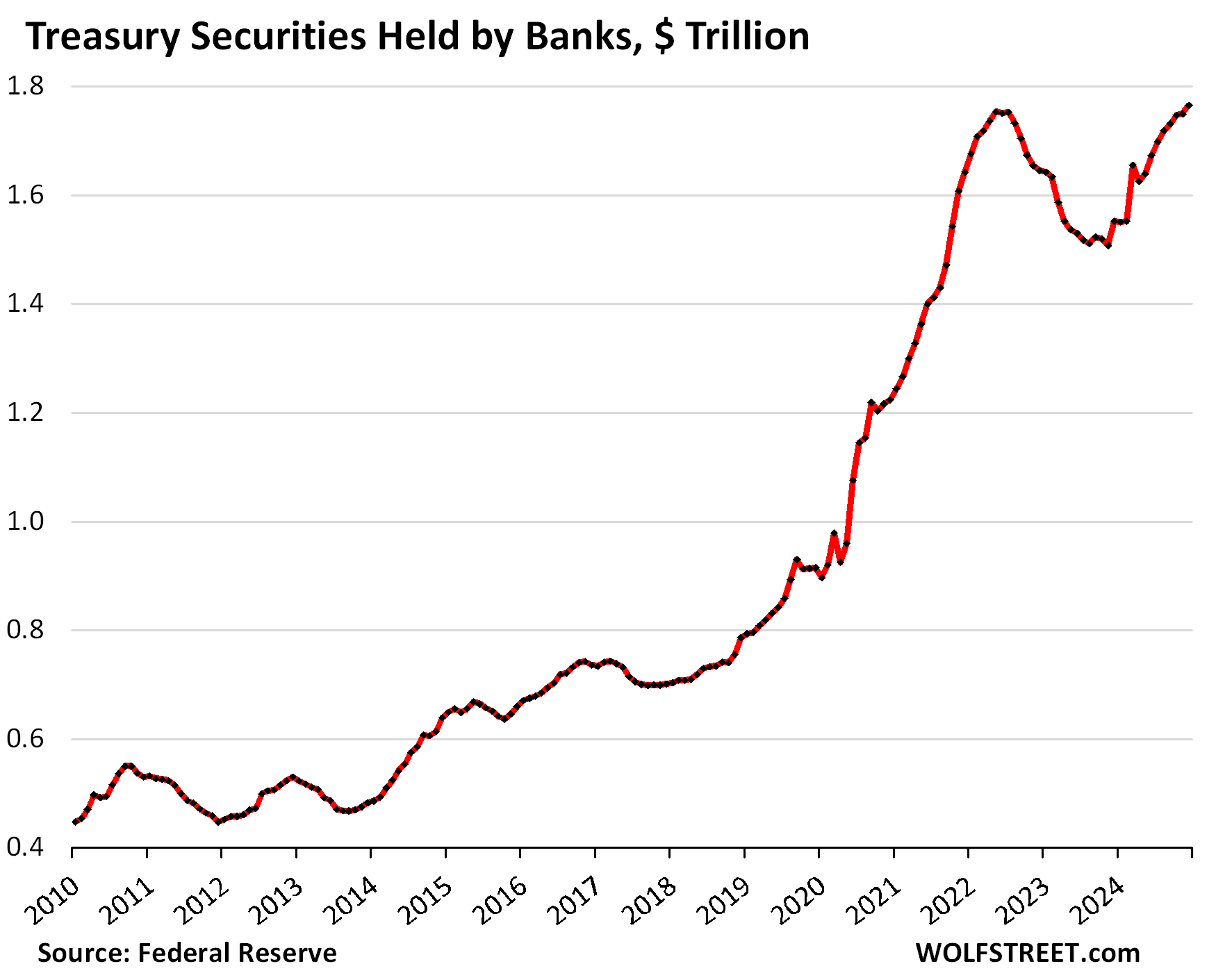

US Commercial Banks: 6.2% or $1.77 trillion of the debt held by the public at the end of Q4, (Federal Reserve data). And added $33 billion in Q4.

These banks include:

- US-chartered commercial banks: $1.54 trillion

- Foreign Banking Offices in the US: $100 billion

- Credit Unions: $63 billion

- Banks in U.S.-affiliated areas: $23 billion

US State and local governments, including pension funds: 7.3% or $2.07 trillion of the debt held by the public. They reduced their holdings by $28 billion in Q4.

US Insurance companies: 2.3% or $650 billion of the debt held by the public, including:

- Property and casualty insurance companies: $459 billion, they’ve been big buyers since the return of higher yields, nearly doubling their holdings since Q4 2022. They added another $40 billion in Q4.

- Life insurance companies: $191 billion.

Exchange traded funds: 2.0% or $554 billion of the debt held by the public.

US Private Pension funds: 1.6% or $452 billion of the debt held by the public. Shed $13 billion in Q4

US securities brokers and dealers: 1.4% or $408 billion of the debt held by the public. They added $72 billion in Q4.

Government Sponsored Enterprises: 0.8% or $227 billion of the debt held by the public. The big GSEs are Fannie Mae and Freddie Mac. They added $36 billion in Q4.

Others: $417 billion

- US nonfinancial corporate businesses: $114 billion. Does not include the Treasuries they hold in foreign financial centers (see above).

- Nonfinancial noncorporate business: $87 billion

- Holding companies: $130 billion

- Central clearing counterparties: $86 billion

Nonmarketable securities held by the public: 2.1% or $575 billion of the debt held by the public (Treasury Department data). These securities are held by the public but cannot be traded in the market and are not purchased at auctions but directly from the government. They include products for retail investors – the Series I Savings Bonds and the Series EE Savings Bonds – plus State and Local Government Series” bonds (held by state and local governments), the Government Account series bonds, and other bonds.

But there’s a new sheriff in town: “We’re focused on the real economy,” Bessent said. “Ouch,” stocks said. Where did the Trump put go? Read… Will Economic Detox Lead to a Recession? Maybe Not. But a Long Deep Stock Market Rout Will (See Dotcom Bust)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I pay attention to you more than anyone else in economics. You really get into the minutia of finance. I have been worried about federal debt since the 1980s. I had a government job and used my telephone at work to call David Stockman who at the time was heading up the Office of Management and Budget. I called him because I was a federal whistleblower about billions in fraudulent compensation awards that I discovered in my federal agency. That’s when my saga began. I paid the price for those disclosures and it ended up in Federal Court. There really is a deep state and I got a chance to talk to other federal whistleblowers and what happened to them is what happened to me. There’s a protocol and it’s pretty much the same in all agencies. Anway, back then in the Reagan years, the federal debt load was appalling but small potatoes compared to $36.6 trillion. I didn’t get to Stockman but I got to his deputy, who told me he used to work for the NY Times. He asked me how much I could save the government. I told him a billion a year. Do you know what he said? Here it is: “I appreciate the call but that’s not even a decimal point on the national debt”. I do have some thoughts about all this debt and I think it’s going to end in a 2nd Great Depression. The Depression of the 1930s was largely a liquidation of debt after it got to 270% of GDP. That liquidation went on for 20 years. Now total debt to GDP is around $450% of GDP, and now government spending is a big part of our phony GDP…and government spending isn’t exactly “product”.

Where did you get your numbers? St Louis Fed shows US debt to GDP ratio of about 120%.

Maybe it was his lucky number?

I guess he meant something like that:

”As of 2024, the United States’ total debt—including federal, state, and local government debt, as well as household and corporate debt—was approximately 722% of its Gross Domestic Product (GDP). “

toby

You’re likely double-counting debt if you include the debts of banks, because banks borrow to lend, and so if you count their debts, and you count the loans they issue funded by their debts, you’re double-counting that debt. That’s why “financial debts” are excluded from total debt figures. So you have total nonfinancial debt as a metric.

Even with financial debt excluded, I think your figure is high, and the 450% would be more on target.

$36 trillion federal

$4 trillion state and local government

$14 trillion nonfinancial corporate

$18 trillion household debt (total)

—-

$72 trillion

$30 trillion GDP, current dollar

= 420%

With japans stated debt to gdp standing at 3 times debt to gdp perhaps debt doesn’t really matter anymore. Regardless, I’d hate to be around if it does, cause that dog has been running wild for some time now Jeff.

Correct…What it really matter is the revenues percentage to service the debt..

Maybe. You are correct: some percentage of tax revenues pays down debt. What the gov’t has been doing is paying off old debt with new debt – while the absolute amount of debt increases every year.

Can kicking.

Interesting post. I don’t doubt your story in the least. I did some engineering contracting with the Dept. of Energy back in the 1990’s and at fairly high levels in that org. DC is filled with power hungry sociopaths, plain and simple. I couldn’t believe some of the behaviors I observed.

Regarding the debt, I share your view on outcome. The new Treasury Secretary and likely Trump know how dire our situation really is. Biden was and his ilk were of the past mindset that USA will always prevail and not to worry. Biden lived in the past; you could see it with his support of unions and Detroit automakers.

Anyway, back to the debt. The price of gold is telling us something about all of this. Based on recent price action, it seems to me likely that something big is going to happen in the near future.

Nice…..union members and autoworkers are people, not some relic of the past.

Debt doesnt matter if you’re willing to retire the debt instead of rolling it over and shrinking the money supply. Nobody wants to do that.

Nope..As long as FED has the power to conjure money out of thin air…no depression.

OK, David Stockman, the budget director for the dauphin president, GW Bush. Author of the idiot princes tax cuts for the wealthy, blowing a hole in the budget, passed only with sunset clause which expired during O’Bama’s occupation. He made them permanent, all the while American manufacturing was being transferred to the low cost producer, the Communist Chinese Party. At a zero rate of interest.

In some ways, O’bama was the worst. For sale.

IIRC , President Obama extended the Bush tax cuts for two years. Then, taxes on income over $400,000 were raised during the “fiscal cliff.”

Also, President Obama led a 12-nation coalition to craft a new type of trade agreement in the Asia-Pacific Rim — the world’s fastest-growing region — that would condition favorable trade terms upon verifiable, enforceable standards for human rights, labor rights and environmental protections, rather than institutionalize cheap exploitable labor in developing countries with lax or nonexistent protections, as prior trade agreements had done.

The idea was to create a large common market outside of China, made up of partners that support fair trade, worker rights and environmental standards, to counteract China’s unfair competition and aggressive market-distorting practices.

But the Republican led Congress refused to take it up, and President Trump withdrew from TPP immediately upon taking office.

“and President Trump withdrew from TPP immediately upon taking office.”

One of the better things he did.

This post is for Mr. Wolf Richter, since I cannot respond directly to his reply to my initial post (no comment button under his reply to me).

When you said, “One of the better things he did,” are you referring to Obama’s allowing the Bush tax cuts on upper bracket income to expire, or do you mean Trump’s withdrawal from TPP was one of the best things that Trump had done?

Thank you.

As I said in my comment, Trump’s withdrawal from TPP

What is your exact worry about the so-called federal debt? Why do you think it’s a problem no matter what its size? I see who holds their extra dollars in treasury securities and am happy they have a safe place to park their dollars while keeping them out of circulation. I am fairly certain that the US government could spend with or without the existence of treasury securities.

Jim Gaddis

There is a basic principle you don’t seem to understand: Every debt is someone else’s asset. That asset can become worthless if the borrower files for bankruptcy to lighten the debt load. But the government cannot file for bankruptcy. The only way out of too much debt is hotter inflation and economic growth. It’s easy to get inflation, it’s much harder for a mature economy to get lots of economic growth. And with enough inflation, everything goes out of whack, including ultimately the currency. So if this debt isn’t delt with in an adult manner, much higher inflation will be result. We now only have a taste of it.

TPTB playing the Monoply & see who can outsmart who as public is waking up to their game. WOHOO

On the weekly Tbill auctions all the auctions are similar in size. Recently $60-90 billion offered at each denomination. 4, 6, 8, 13, 17 and 26 weeks.

But then does the Debt-to-GDP ratio matter? Is it not just something someone imagined would give the public an idea of how big the debt is when the actual debt number becomes too big to relate to? There must be better ratios. Most people don’t know what GDP is anyway. In practical terms, it’s the cost of repaying the debt that matters.

The ratio I like is tax receipts to interest expense… how much of the government’s tax receipts are spent on interest:

Too bad you weren’t called on at todays presser. You could have asked Jay about the above chart. That would have been popcorn worthy.

What’s interesting is that no one seemed to notice that the Fed’s prediction for inflation was revised up from 2.5 to 2.8.

The market rallied because the Fed also threw a bone to the dog, a deceleration in QT. Which instigated a risk on rally in the asset prices that the abundant reserve policy supports.

At what percentage service debt ratio will break up the camel’s back…you think? I’m hearing 70 – 80% will do it…

Numbers don’t lie

I wonder what would happen if Euro Area and Canada decide to focus on domestic pursuits and stopped buying US Debt…wonder if that’s a negotiation option with all this tarriff stuff.

What are they going to do with their USD they get from their trade surplus with the US? The Euro Area has a HUGE trade surplus with the US. Sure, they can buy other stuff with these dollars, such as oil, LNG, or minerals, but they’re already doing that.

Is there a reason they can’t invest the money to build factories in the Euro Area and rebuild their industrial base as the US is also doing right now?

Or does the fact that the trade surplus is denominated in USD block such a move?

Sure, and they do. But they have to sell those dollars for euros because they’d be investing euros not dollars.

Canada also has debt. Note that. Ever increasing. Don’t paint a picture of Canada as a debt free nation

Great information. Confirming that U.S. treasuries are held everywhere by everyone, BUT predominantly be the U.S. public and U.S. institutions. Personally, I think that it would be interesting to see a comparison between government debt and equity. I believe that the stock market is indeed a derivative of the debt market. So long as debt continues to be issued around the globe, equity markets will be fine. It’s when the debt markets start blowing up that you need to worry.

>plus State and Local Government Series”

Missing an open quotation mark somewhere?

“But there’s a new sheriff in town”

My best case: Trump shakes the system just enough to be a wake-up call to heedless public finances, and other clearing of bloat, but without ruining critical institutions. My worst case: the world finds a way to see the USA as financially indispensable in the rear view mirror, and we go down like the UK in the 20th century.

The UK is sowing what they reaped. A pipsqueak imagining that they are somehow relevant because of their culture or their history.

Would like to hear someone with knowledge on that whole “dollar milkshake” theory comment on this in relationship to the global debt markets. Looks like Turkey’s is about to blow up (again).

With the Treasury’s interest and principal expense, and its constant roll-over of its short & long-term debt (and ultimate looming rise in interest rates, as the Gov’ts voracious appetite becomes the paramount driver), it becomes obvious that the burden of higher interest rates will be compounded.

The burden thus becomes a function of the major portion of the debt, not just the current deficits. The burden then becomes exponential. In other words, if the trend is not stopped, the debt inevitably has to be repudiated.

“Treasury Secretary Scott Bessent is concerned about America’s large and growing national deficit. “We have never seen this before when it is not a recession or not a war,”

A crisis of confidence will denigrate the twin deficit hypothesis.

The administration is talking about “no income taxes under $150k”. This is easily achieved with the current tax code by just raising the standard deduction higher over time.

I can see this being coupled with a significant increase in social security payroll taxes such that the average $100k earner takes home about the same amount. SS in “permanent” surplus means a reliable buyer of Treasures as far as the eye can see..

Does anyone here really think the current crowd running things in DC is going to let some silly law about a “debt ceiling” slow them down ?

If they ever get serious about balancing a budget, they will have to start taxing the people who have most of the money. And tax them like they did back in the 1940s and 50’s.

Indeed. It’s hilarious that this administration is hellbent on saving money by firing the common man instead collecting the due bill from the upper class. And the previous admins are just as guilty for their complacency.

@old-ghost: In case we forget, no one is going to tax themselves. In fact, it appears that it is going to go the other way!

FYI: the Fed is going to reduce the pace of Treasury QT to $5B a month – basically a trickle that just keeps the plumbing intact. The ~$4.3 trillion in Treasuries the Fed is holding appears to be the bottom. They’ll let MBS run off up to $35B a month which it never comes close to anyway.

The Fed has effectively cut QT in half today, at the current natural runoff pace of MBS of $15 billion a month via passthrough principal payments plus $5 billion in Treasuries.

At the press conference, Powell said that after discussing these issues, participants “liked” the idea of going “slower for longer” with QT, to avoid risks associated with withdrawing this much liquidity, and this “slower for longer” was the reason they effectively cut QT in half.

No one in 2022 thought that QT could go for $2.2 trillion without blowing up something big. Everyone thought QT would have to end much sooner. And “slower for longer” is now the official ticket to get as far as possible.

https://wolfstreet.com/2025/03/19/fed-sticks-to-wait-and-see-sees-only-2-cuts-in-2025-dot-plot-shifts-hawkish-amid-rising-inflation-uncertainties-slows-treasury-qt-maintains-mbs-qt/#comment-629992

You have said previously that buying treasuries was very safe because they are guaranteed by the government which can print money. Do you still feel that way? If not, what is a safe?

The credit risk (risk of default) of Treasury securities is essentially zero. If you buy long-term securities (any, not just Treasuries), there are other risks. Inflation might take off and run hotter than your interest income, and then you don’t get compensated enough for this inflation. This also entails higher yields, so it translates into lower market prices during the years before they mature, so you would lose money if you sell them before maturity. If you hold till maturity, you’ll get your money back, but it will be in deflated dollars, so if you didn’t get enough interest to compensate you for inflation over those years and for the other risks, you got a bad deal.

The bond market really hates inflation.

Thank you once again Wolf; in this case, for providing in writing what I have been communicating to my dearest.

In spite of the VAST ”mis” and ”dis” information now SO prevalent on the web, YOU continue to provide clear reporting,,,, EXACTLY why I send more $$ to you than any other currently supported website.

Thanks again,,,

Please allow me to add my voice to VintageVNvet. As a private investor who manages a large portfolio, I read extensively. There is no better source of key financial data than Wolf Richter. Yet, ironically, he is free. I have argued with Wolf numerous times about this. His presentation of data is better than many very expensive financial services. So, dear Reader, please consider sending Wolf a generous and regular donation. He provides a very valuable service, so please consider showing your gratitude with a financial contribution. Thanks.

The Longer View, thank you!

The risk to treasuries is more than zero if you are treasury bonds held in Chinas foreign reserves, or if you are an American public pension fund, ie liberal. (I am just the messenger) This says nothing about risk premia, or the likelihood of another credit downgrade -Moodys says Greece – the cradle of DEMOCRACY- is now investment grade. About the maturity issue, if the bond market hates inflation, how does it feel about deflation? (and they are really the same thing) If you buy a 10 year bond and in 10 years a house is worth half of what it is now, you have doubled your money, if you hold a mortgage, even at zirp rates you lose. and the US is huge bond fund, do you like your manager?

Ongoing QT is roughly $400 billion per year.

The new holders of the debt when the Fed rolls it off are paid interest by the treasury after it issues a new bond to pay the matured treasury. This interest, which the Fed previously remitted to the Treasury, is now adding to the national debt.

At 4 percent interest that’s an additional $16 billion per year added to the debt.

Am I completely off base? I’ve tried,am still trying, to understand the accounting side but find it complex.

It just seems odd that reducing the Fed debt does not reduce our national debt. Any correctiion from this talented forum would be appreciated.

So, the press secretary was asked by a reporter about tariffs and responded that “tariffs are a tax cut for the American people” He than asked her if she had ever paid a tariff and said ‘because, I have.” She then got upset and said “I think it’s insulting that you’re trying to test my knowledge of economics.”

What a upside down world we live in.

I’ve read 2 different articles recently. One says StableCoins are now backed by 200 Billion in US Treasury securities. A second article says that number is 1.2 Trillion. Some discussion boards talking about the Trump Admins Crypto strategy is looking to grow Stable Coins to hold 18% of Federal Debt. Perhaps it’s too aspirational, but it seems to me to be part of the general scheme to use StableCoins as the basis for a new cohort of US debt buyers

I think there may be two different figures here. One is “backed by Treasury securities,” and the other may be “backed by securities of any kind, including equity stakes in startup companies” (which is what Tether is doing).

Please correct me if I am wrong, but to my knowledge none of these stablecoins issue audited financial statements by a reputable U.S. based CPA firm.

With our system of rotating parties leading the government it is unlikely to know whether current policies will indeed shrink trade and fiscal deficit. Sure, they might trend in a certain direction but really might need even be able to undo what was done with outsourcing and other policies. Reshoring doesn’t happen quickly and tariffs, while revenue, are not that significant in big picture by themselves and done incorrectly, can be negatives. We might end up pouring the money we make from tariffs into subsidizing the industries we hurt with them through counter tariffs.

Since covid, it looks like 14 trillion was added to the debt. What did all that money buy? Probably a lot of stocks, cars, homes and ?? I guess the tax cuts are a part of it. But where oh where did the bulk of it go?

The federal government desperately needs to get to a fiscal surplus. The debt needs to be reduced, and there need to be deep cuts everywhere, especially social programs. In the event the budget is balanced, and a small surplus is generated, the USA can pay the debt off in time as GDP growth occurs.