In the West, Midwest, and Northeast, pending sales hobbled along near record-lows. Housing demand got shot in January. Prices are just way too high.

By Wolf Richter for WOLF STREET.

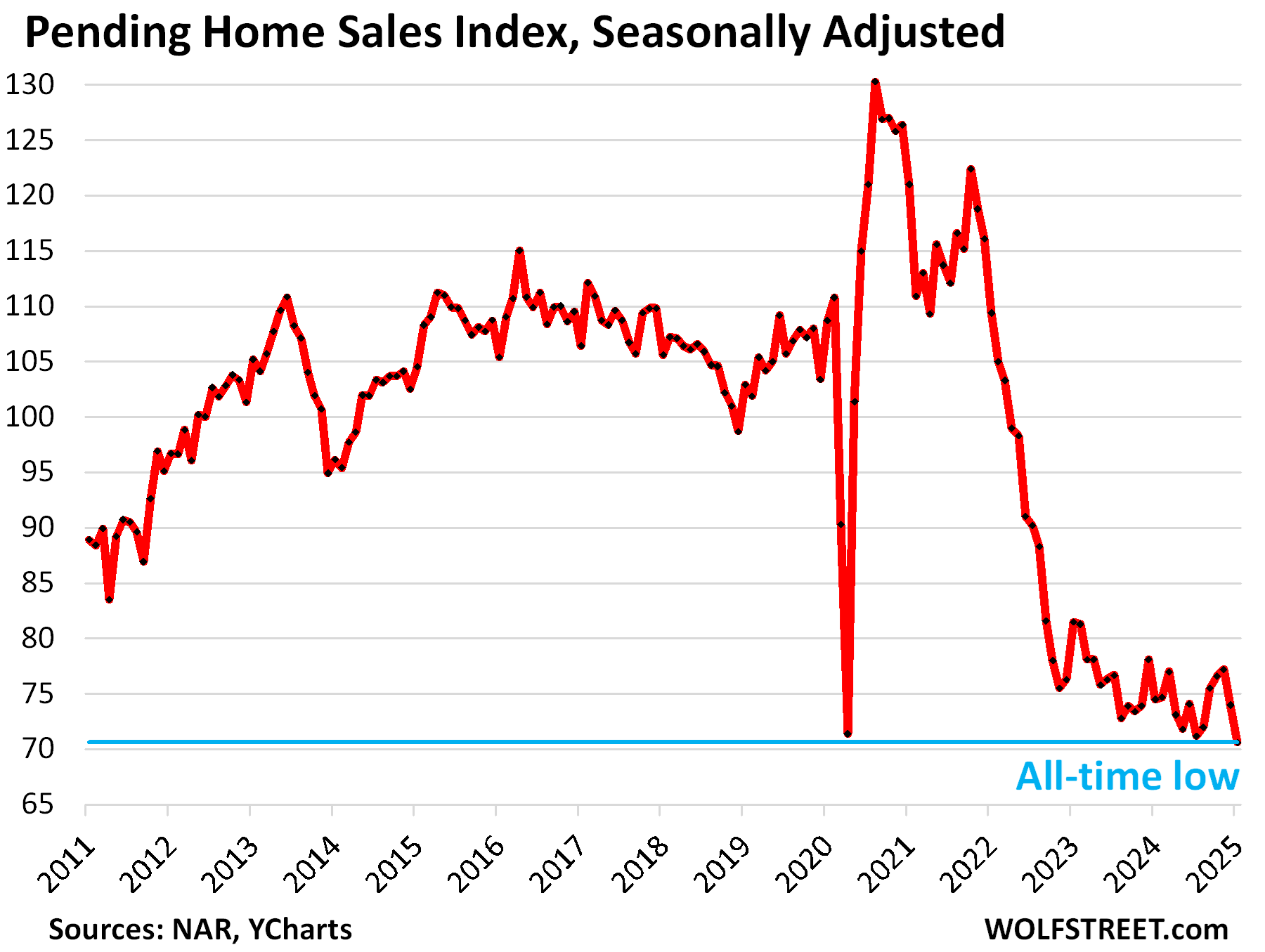

Here we go again, with another record low in demand: Pending home sales – a forward-looking indicator of “closed sales” of existing homes to be reported over the next couple of months – dropped by another 4.6% in January from December, seasonally adjusted, and carved out a new all-time low in the data going back to 2010, according to the National Association of Realtors today. Compared to the January in prior years:

- Jan. 2024: -5.2%

- Jan. 2023: -13.4%

- Jan. 2022: -35.5%%

- Jan. 2021: -41.7%

- Jan. 2020: -35.1%

- Jan. 2019: -31.4%.

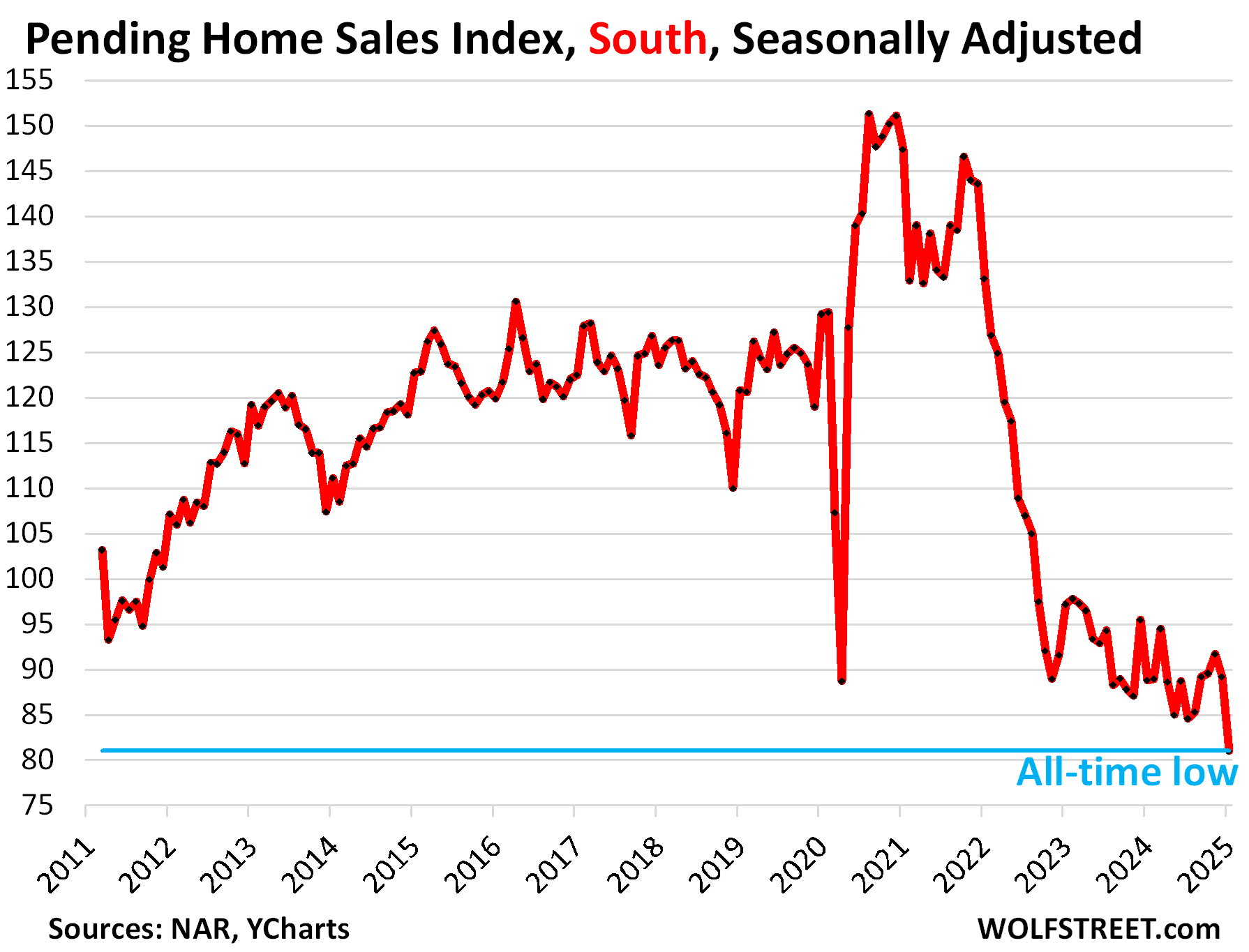

The dive to a new record low was driven by the South, the largest housing market in the US in terms of transactions, where pending sales plunged to a new record low, and where inventories are now ballooning (historic data via YCharts):

The Buyers’ Strike continues because prices are too high – “elevated,” as the NAR called them today, while blaming them and mortgage rates for this situation – after shooting up by 50% or more within a few years.

Pending sales have been hobbling along the bottom for over two years, and each sign of green shoots, that then got hyped endlessly, was trampled by the buyers’ strike. Prices are simply way too high, and they have frozen demand in the resale market.

Pending sales are based on contract signings and track deals that haven’t closed yet and could still fall apart or get canceled, for all kinds of reasons, such as buyers being unable to afford or even get homeowner’s insurance, a big issue in states where homeowner’s insurance premiums have spiked in recent years. Signed contracts that then fall apart are included in the pending sales here, but are not included in the figures of closed sales reported later.

In the South, pending sales plunged 9.2% month-to-month in February, seasonally adjusted, and were down 8.8% from a year ago, the biggest drops of the four regions.

Compared to highflying 2021, sales collapsed by 45%. Compared to 2019, pending sales plunged by 33%.

And it’s precisely in the South where inventories for sale of new houses and existing homes are now piling up the most (a map of the four Census Regions is posted in the comments below).

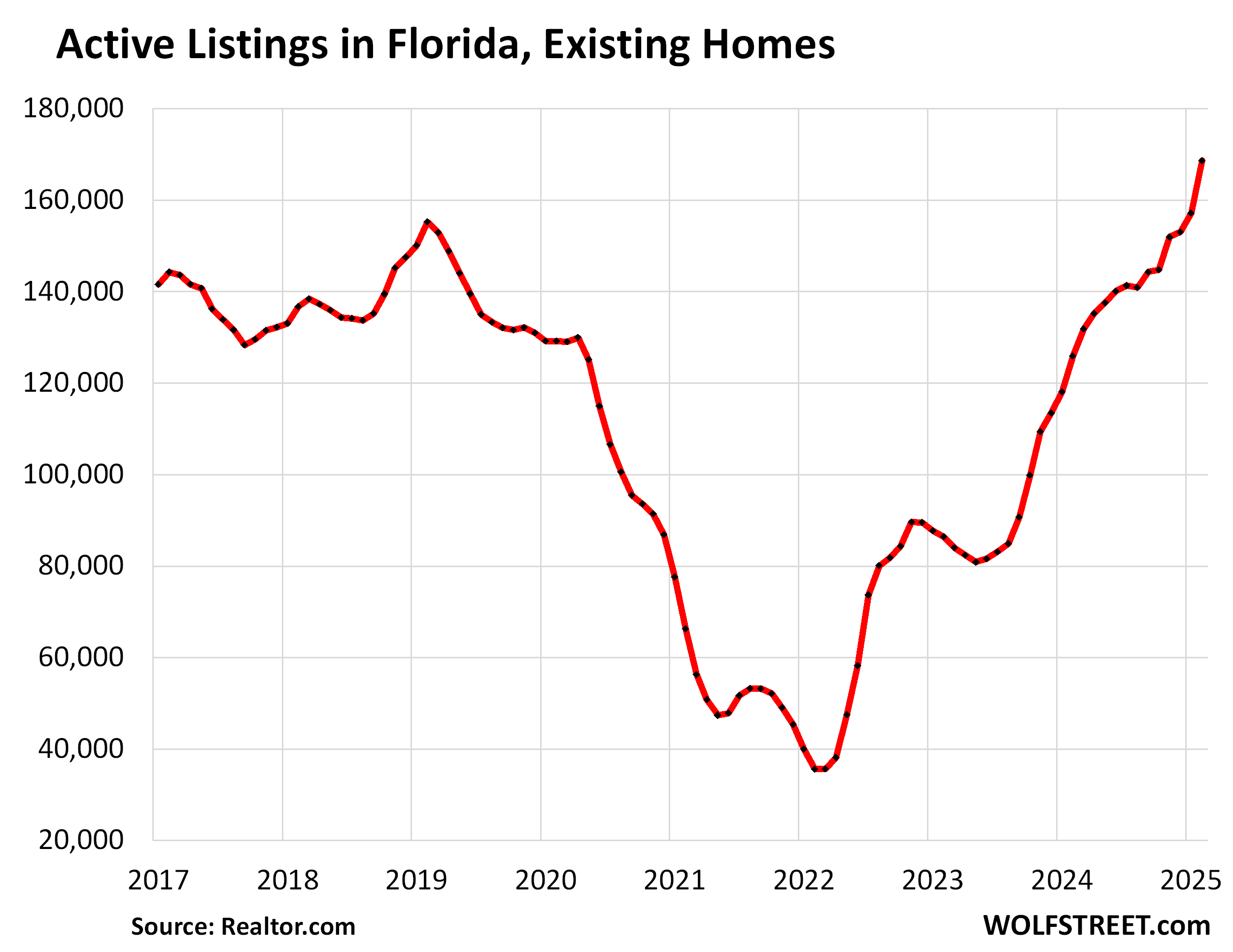

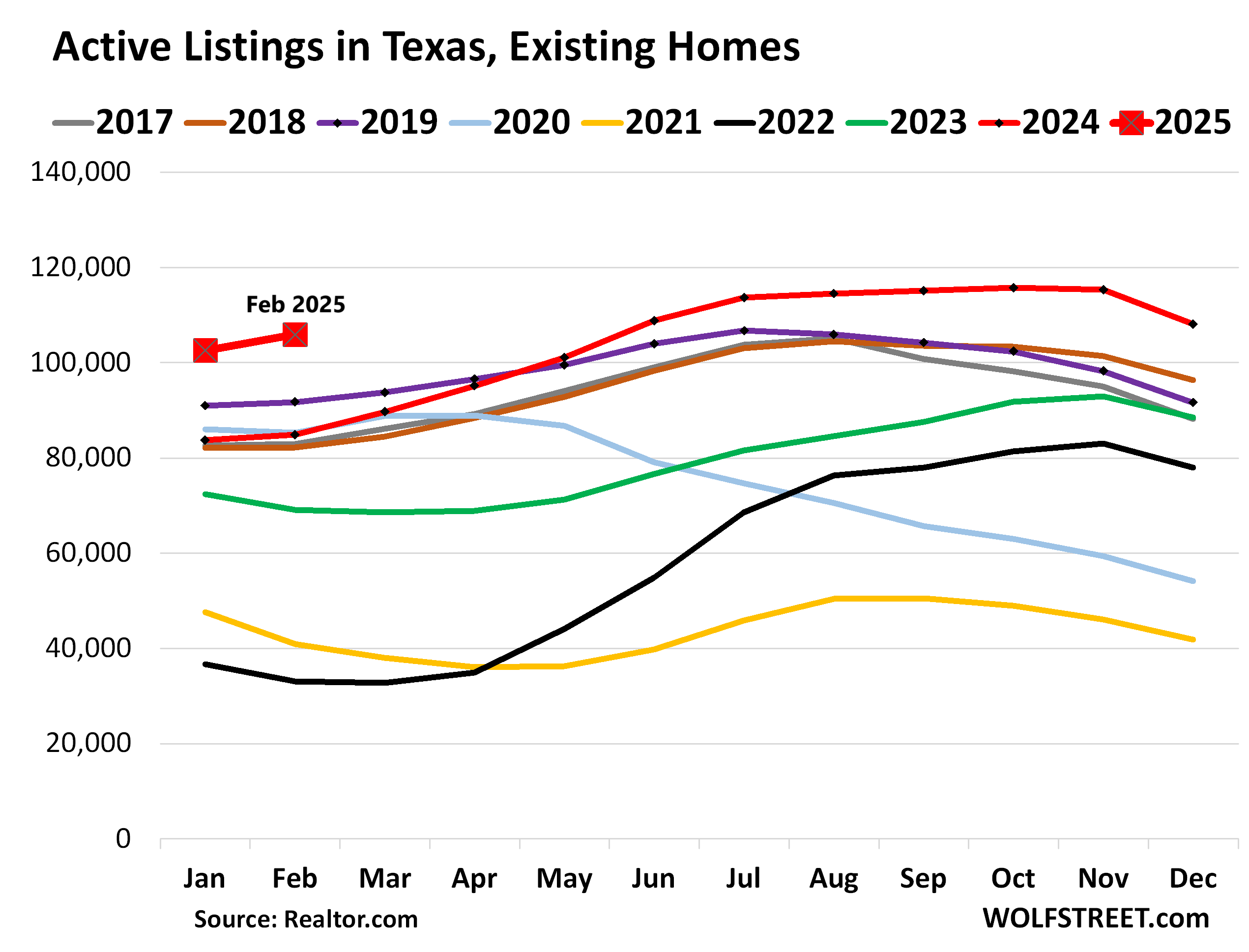

Inventories balloon in Florida and Texas.

In terms of transactions, Florida is the largest housing market in the US. Florida and Texas are by far the largest states in the South. So we’ll look at active listings of existing homes in those two states as an indicator of the South.

In Florida, active listings jumped by 34% year-over-year in February, to 168,717 listings, the highest in the data going back to 2016, released today by Realtor.com.

In Texas, active listings jumped by 25% year-over-year in February, to 105,867 listings, the highest for any February in the data going back to 2016 (data via Realtor.com today).

Because listings in Texas are strongly seasonal – lows in January/February, highs in July/August – we look at the stacked chart. The big red squares are January and February 2025.

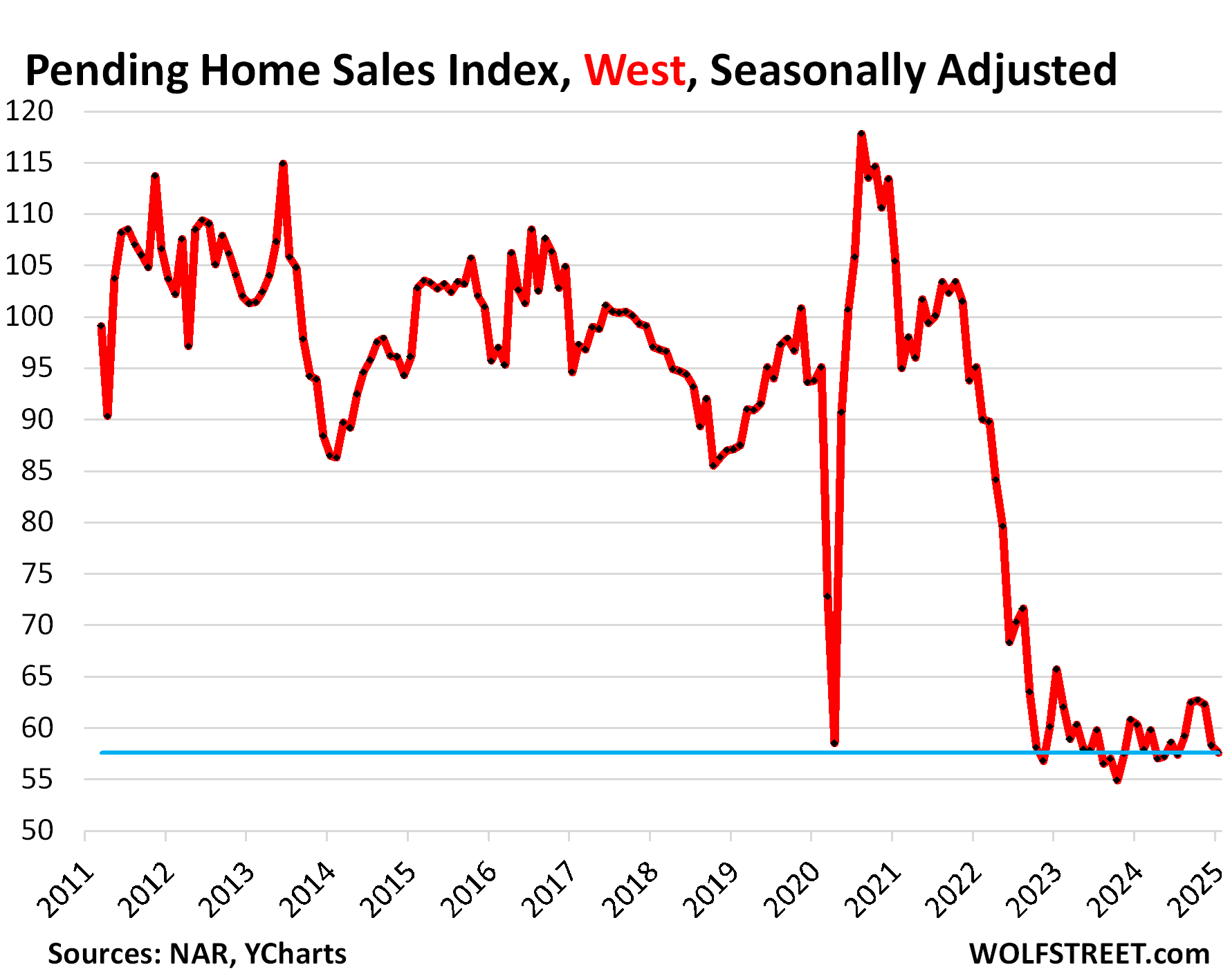

Pending sales in the West fell by 1.2% month-to-month in February, and by 4.5% year-over-year, continuing to hobble along near the record low of October 2023. Compared to February 2021, pending sales collapsed by 45%. Compared to 2019, they plunged by 34% (historic data via YCharts).

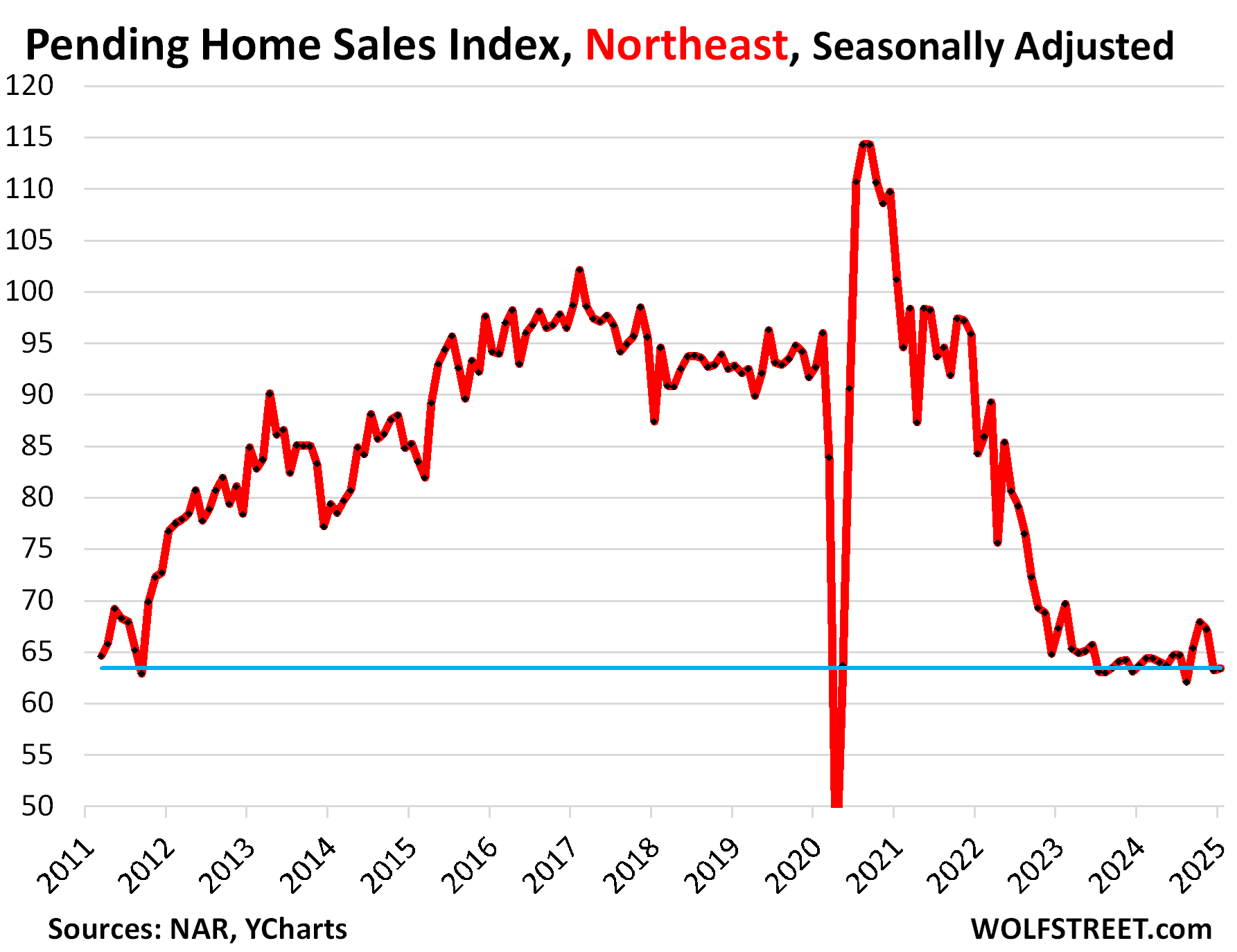

Pending sales in the Northeast ticked up 0.3% month-to-month in February, seasonally adjusted, the only region of the four regions to have experienced this tiny gain. Year-over-year, pending sales were down 0.5%. Compared to February 2021, sales plunged by 37%, and compared to 2019 by 32%. Wobbling along record low levels.

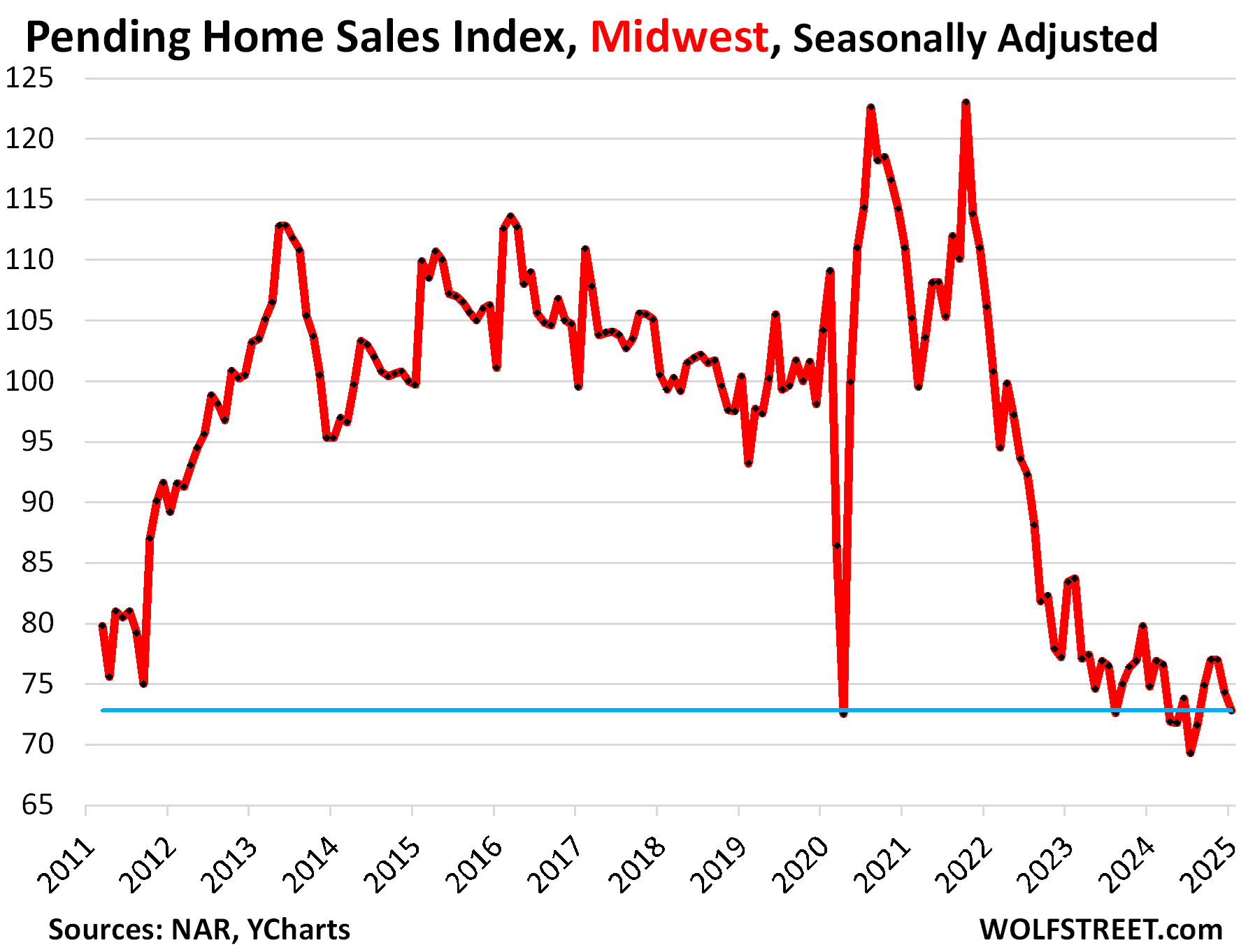

Pending sales in the Midwest fell by 2.0% month-to-month in February, seasonally adjusted, and by 2.7% year-over-year. Compared to February 2021, sales plunged by 34%, and compared to 2019 by 28%. Not a record low, but wobbling along record low levels for over two years.

The plunge in demand in February, as depicted by pending sales, is similar across all four regions, as the above charts show, but it’s worst in the South at the moment, and that’s where also the inventory pileup has started in a serious way.

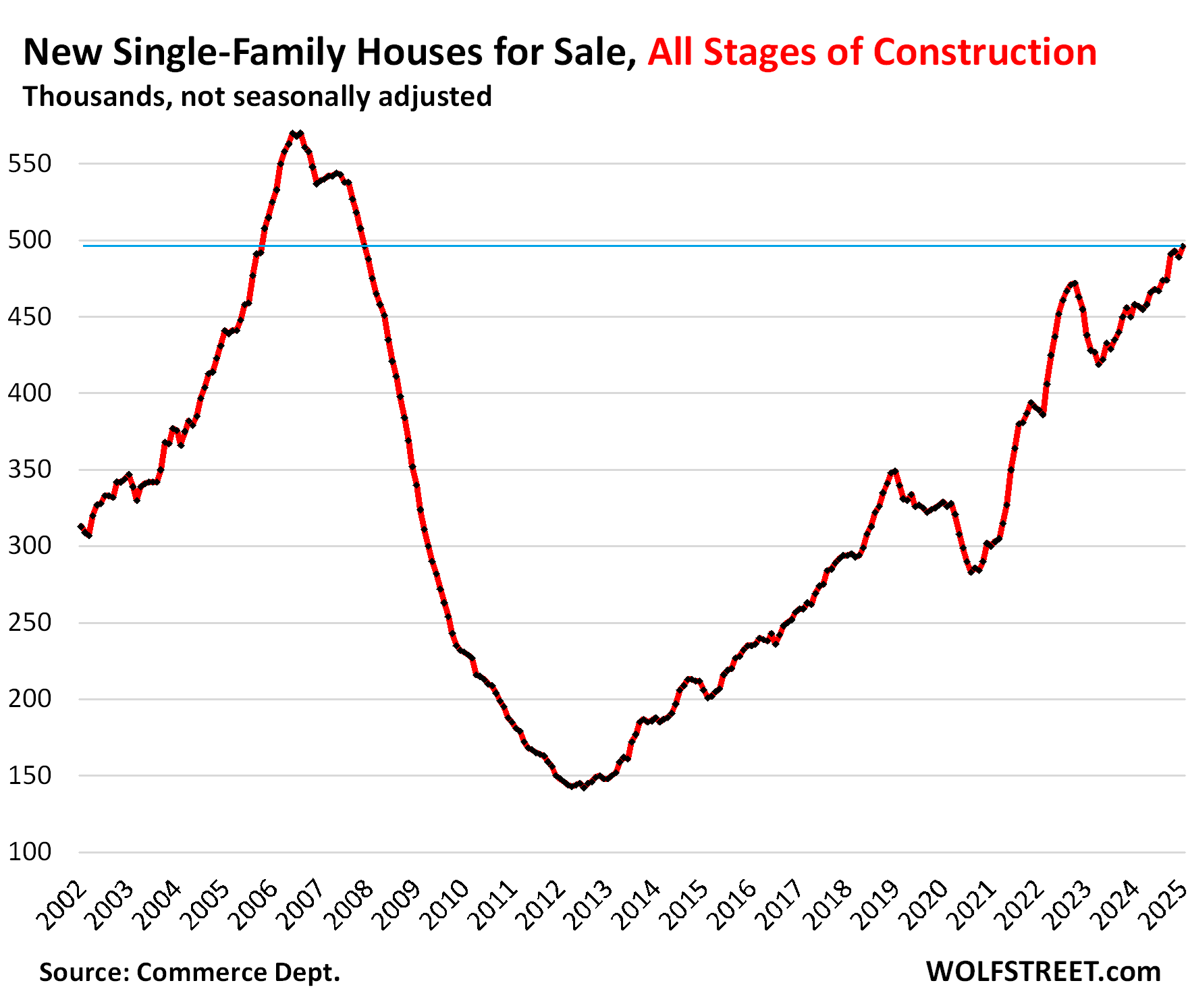

And inventories of new single-family houses across the nation have ballooned to the highest level since 2007, driven by the South, according to Census Bureau data. Those new houses are now adding to the housing supply, to the surging inventories of existing homes, while homebuilders are piling on mortgage-rate buydowns, price cuts, and incentives to move this inventory:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The four Census Regions of the US:

Time to sell.

Time to sell was 2022. Everybody selling now but low demand in buyers

Buy high sell low baby!

Harry,

It was a bloodbath in Nvidia today. Covered part of my shorts (via NVD, and SOXS). Then I looked, and Nvidia is still valued at $3 Trillion imaginary dollars.

Shorting out of the money call options with two days until expiration to earn the premium was free money. There are option strikes up to $300 (!) because of the run it had last year. $240 would be a $6 Trillion market cap(!!) It has yet to have a close above $150. It will never see $200 in my opinion. I am hoping it bounces though. I am in full-out sell the rallies mode now, this looks like a down year for stocks, if it’s another up year it won’t be too much, but it could fall 10-15% easily. All those stocks that have ridiculous valuations that went vertical and plunged, they are finished, they are not going back up.

Some people beleive Nvidia is going to $10 Trillion. I kid you not.

Agree, Palantir and AppLoving and similar are done. Both got to couple hundred $Billions for a day or two. I traded Palantir on short side.

Likely market top is behind us. Either Dec 17th or Feb 19th depending on one’s favorite index.

Bloodbath? -8%??? Dude, that’s nothing unless you were a sucker late to the buying party.

Well, for one day, 8% is a BIG drop, I think that’s what he meant.

Calls on thriple-short etf(s). 60+% in couple of days. Rolled them into September SQQQ calls. Not that you would understand.

There has been a MAJOR bloodbath in Shi*Coin, I mean Bitcoin. Down $24,448 in the last 30 days. Currently, it’s falling like a rock. It fell $1000 in the last few hours.

Let’s talk about the elephant in the room you can have all the grass in church you want but the bottom line is you’re not goingna sell houses what’s 7% interest rates forget about it end of story

Mortgage rates should be higher. The Republicans and Democrats subsidizing mortgages with money printing has caused a lot of unnecessary wrongs. Plenty of houses can sell with lower prices.

How old are you, Mr. Baker? I’m curious – it’s not a put down, but you’ve got the interest rate thing wrong.

Artificially low interest rates and very loose lending practices got us here today. Normally, when interest rates increase by any substantial amount, home prices should come down. In this housing bubble, that hasn’t happened YET, but it will. Give it time, Mr Baker.

Yes. Exactly. As a 38-year-old who’s never owned a home, I certainly won’t be a first-time home buyer if interest rates stay where they are. I personally think we should have laws that prohibit home interest rates ever exceeding 3%. Because housing is a necessity. And on top of that, home prices are just too steep. It compounds together to be outrageously unaffordable. Why would I leave my crappy two bedroom one bath home that I pay $650 a month for for a brand new home or even a used one for upwards of 2,000 to $3,000(modest) a month. It’s just not within the budget at all.

“Because housing is a necessity.”

Yes, but you HAVE housing (a 2-bedroom one-bath apartment … I grew up in one of those, us 3 kids and 2 parents, 5 of us. It was ok.

“we should have laws that prohibit home interest rates ever exceeding 3%.”

LOL, no, we should instead maybe have laws that prohibit mortgage rates ever falling below 6% maybe?

I live in FL and what I’m seeing agrees with this completely. Houses that aren’t dropping price aren’t moving. Ones that drop price a decent amount from the peak still can move. But more and more inventory is appearing.

On a side note, I like how the “South” in the map starts at the New Jersey border.

In Michigan we say it starts at Toledo

In some parts of the flower state, old timers say the south starts at a line from Tampa to Daytona Beach and goes NORTH, (below that line is Florida),,, of course some of those same folx also say anyone born north of the Manatee River are Yankees. LOL

lucky that we all get to call it as we like it, eh

VintageVNvet – Similar in Texas. North is anything above Interstate 10!

The interest rate is the biggest reason why houses aren’t moving everyone knows that If you’re lucky enough to have the cash then you have a lot of bargaining power but outside of that until the interest rate comes down houses will sit Please convey that to the Federal Reserve

nonsense. prices have to come down, not interest rates. it’s not the fed’s job to prop up the housing market.

WRONG. This is the same bullshit line repeated by every realtor on the planet. It’s the prices, stupid. People still believe their house went up 100% in 3 years and can afford to sit on it because they refinanced at 2.5% even though they’ve already moved and it’s vacant. And builders refuse to take an actual loss because it would devalue other new homes. We have vacant new construction homes that have been on the market for 2 years. They are universally shit quality and are asking a 50% premium above equivalent resale as footage.

This is a house of cards and will break rapidly as soon as there is a stock market crash and job losses.

i was looking at some florida zillow pages, and it looks like new builds and in fancy country clubs are still selling for 2022 peak prices. must be stupid money that doesn’t care about cost.

the rest though aren’t selling.

Mason-“Dioxin” Line.

“I like how the “South” in the map starts at the New Jersey border”

This is accurate. In MD they don’t even have gas furnaces or fireplaces because it doesn’t get cold enough – heat pumps are the thing down there.

The Mason-Dixon line marker is actually at a small town named Delta MD. I was raised about 10 miles from it.

“It can’t be good, Mama, it can’t be good!”

The American dream of owning a house is becoming the American nightmare for many homeowners, with skyrocketing insurance, property taxes, maintenance, and HOA (for some). I think I will just rent for a while.

Just back to the old days when you and a couple of relatives or friends simply built the home yourself after you bought a piece of land. Depending on DR horton, Lennar, Pulte homes etc and needing a mortgage is NOT the way going forward. The ‘Mortgage’ was a banking invention for homeownership, previously people just built things and owned ’em free & clear. No friends or relatives? You can always pay the non-English speaking amigo builders around your area in T-bills for their labor. They love those LOL

Around here we just pay them in cash!

Oh the good days..we did just that with a solar room addition, was fun, created flow to the house and got back 5x in use plus market value when sold yrs later…

Mortgages are the reason nobody can afford a home. If everyone had to pay cash, people would save and be responsible and houses would be affordable through an efficient market. Nobody could ever save 1 million to buy a home in cash. When mortgages first came out post world war 2 you needed a 50% down payment and had to pay them off in 5-10 years. They want to make 40 year mortgages now so people can “afford” houses. LOL it’s just going to make it worse.

Same thing with student loans and tuition. Tuition is 50k/year because the banks and govt let you borrow that much. When they increased the borrowing limits, prices went up. Coincidence I’m sure. Without the lender the universities would have to cut their glut of wasteful admin positions and price efficiently to have customers. Yet again, the solution hurled to the ignorant masses by the govt is the fake free money give away. It will just make the problem worse.

The solutions are painful and nobody wants even an ounce of pain.

Same thing with consumer goods and credit cards and payday lending.

This is what happens when you let money lenders run amok in society. Usury is an ancient recognized sin for a reason. We’ve known about this problem for literally forever.

Excellent take and the truth.

Rent until they start giving houses away, like in Japan (or villas in Spain or Italy for a Euro). I’ve seen it on TV.

I did recently see a town on the Italian island of Sandinia, offering homes for €1 (one Euro) which is currently $1.04! The economy there has cratered and the population is dwindling. They were catering to Americans who want to ‘flee due to T being elected.’ $1.04! Don’t move there expecting paradise though. Just a personal suggestion.

“Sardinia”

There are many small towns scattered across Italy with those offers. They are not deals for lots of reasons I won’t bother explaining. And they have been around for years, nothing to do with T.

As Gattopardo has said, those 1 dollar homes are not a good deal. The maintenance that most will need to be livable is usually a very large figure. And you need to put large deposits in escrow as you guarantee you will make the house livable.

thurd2,

HOA issues are on the agenda in Minnesota’s House and Senate. With broad bipartisan support, their aim is to reign in the power that HOAs wield. As I follow the events, this number surprised me: 82% of all new homes in Minnesota require HOA membership; with the monthly fees and the relinquishing of sovereignty when one owns a home under a HOA.

This is the opening part of a long proposal made Monday, 24 February (House File 1268):

“A bill for an act relating to common interest communities; prohibiting certain practices relating to property management companies; modifying rights and duties of common interest communities; modifying rights of a unit owner; modifying termination threshold; establishing a meet and confer process; modifying notice of meetings; prohibiting certain governing bodies from requiring or incentivizing creation of homeowners associations; amending Minnesota Statutes 2024, sections 394.25.”

There’s a detailed list of changes that the Legislature has for the bill, and it will probably pass in two months, before the Legislature adjourns, and get signed into law by the governor.

I reckon that the pendulum of power has swung too far in favor of homeowner associations. Power and control needs to move back towards, “A man’s home is his castle.”

YMMV

Come to Florida. The governor is talk about abolishing property tax. It’s getting crazy ok.

I’d rather pay no prop tax than no income tax.

Sounds good.

Correction. The time frame for valid signatures might be two years.

But you’ll need at least 20 million just to try:

According to Claude AI:

Citizen Initiatives in Florida

In Florida, a citizen initiative is a process that allows voters to propose constitutional amendments directly.

Here’s an overview of the requirements, process, and associated costs:

Basic Requirements

1. Initiative Sponsor: Form a political committee to sponsor the initiative.

2. Registration: Register the committee with the Florida Division of Elections.

3. Petition Format: Submit your proposed amendment text and petition format to the Division of Elections for approval.

4. Signatures: Collect valid signatures equal to 8% of the votes cast in the last presidential election, distributed across at least 14 of Florida’s 28 congressional districts.

5. Supreme Court Review: The Florida Supreme Court will review the amendment’s compliance with single-subject rule and clarity requirements.

6. Ballot Placement: If approved, the amendment appears on the next general election ballot and requires 60% voter approval to pass.

Timeline Considerations

The entire process typically takes 2-4 years from start to finish. Signature petitions are valid for only two years, so timing is crucial.

Estimated Costs

Launching a successful citizen initiative in Florida is expensive:

– Signature Collection: $3-10 per signature (professional collectors)

– Total Signature Requirement: Approximately 900,000 valid signatures (as of 2025)

– Legal Services: $50,000-$250,000+ for legal guidance and Supreme Court review

– Campaign Costs: $1-5+ million for public education and voter outreach.

– Administrative Fees: Various filing fees and verification costs

Expert Assistance

While I don’t have information about specific individuals who can assist, these types of organizations typically provide guidance:

– Ballot initiative law firms specializing in Florida constitutional law

– Political consulting firms with Florida ballot measure experience

– The Florida Division of Elections (for procedural guidance)

– University law schools with constitutional law departments

– Advocacy organizations aligned with your initiative’s subject matter

Tina Willis Law

Wolf – you put out some good information. My interpretation of your data is that a potential Level 5 hurricane is soon to come in the housing market. What other conclusion can one come to?

As far as a ‘plunge in demand’ in the housing market, I always smirk a bit at that concept. There is an absolute demand for housing. Everyone needs housing. It’s just that people are not WILLING to buy are current insane prices.

So yeah, more like a buyer’s strike. Deferred demand.

We’re not talking about homeless people buying homes. We’re talking about people who already live in a home buying another home. If they don’t want to buy another home, demand collapses. That’s what “demand” means.

It also includes people like me who currently rents and would love to buy a home but refuse to pay these insane prices. I guess I will never own a home again.

There’s another issue that nobody wants to talk about. The sudden influx of 20 million illegal immigrants. These people live somewhere and we are told with a straight face that had nothing to do with the supply and demand shock that occurred in 2021-2022. Yeah, right. Sure, they didn’t buy houses but they occupied something and that has a ripple effect upwards.

Removing millions from the demand pool is going to have an effect, obviously.

Yes, the influx of immigrants was huge. But what you have to look at is not border crossers that then get deported right away only to recross multiple times. If you add up all the border crossers you double-count and triple-count, and you’re not deducting the people that got deported right away.

The measure to look at, what you really want to know in terms of the housing market, is population growth. The US population surged by 8 million people in the three years from July 2021 through July 2024, to 340.1 million. That was a huge and sudden increase in the population (mostly through immigration illegal and legal).

More details here:

https://wolfstreet.com/2024/12/19/census-bureau-revises-up-population-growth-8-million-in-3-years-due-to-immigration-total-us-population-340-million/

Most of the people who buy homes are not that smart generally to see if the prices are high or not

It’s not that people are not willing at these prices and rates but people are not able to afford monthly payment of owning a home

Home prices need to fall a lot I think

It’s a slow moving truck.

I think it’s a fast moving truck that most people cannot catch. However – I think that truck is gonna hit the brick wall straight ahead.

Jon,

Most people look at monthly payment just like you mentioned in your second paragraph, period. They are living somewhere at the moment, example: at home with parents with very little expenses, renting a room, renting a cheap apartment, renting a cheap house, renting an expensive apartment, renting an expensive house, having their job pay for their housing because they relocated, etc.

They then think “I would like to buy a house” and then either crunch numbers themselves, go online and fill out the “how much home can you afford calculator” or reach out to a professional (Realtor, Bank, Financial Planner, Mom and Dad) to get advice. Then they ask themselves “Can I swing those closing costs and monthly payments?” That’s it.

MOST people do not go “Let me look at a chart of housing prices and see if this is a good time to buy a house when compared to the last 15 years.” SOME people do that. Those people are more likely to be on a website like Wolf’s.

MOST people don’t care about the price of something, they just care about whether or not they can afford it. MOST people don’t need a $1,600 phone, but the carriers have subsidized it for $20 a month, so now they can afford it. There are countless ways to better spend that $1,600 and everyone will have an OPINION on what’s best.

You’d have to believe that the FOMC will continue with a tight money policy. Otherwise, I don’t see the downswing.

The economy is still strong. January was just cold.

The odds are great that the Real Estate market will become even more stagnant with fewer homes getting listed and fewer buyers. The vast majority of sellers don’t need to sell. 40% own their own outright and 60% have a rate less than 5%.

You forget the large number of vacant homes that people moved out of a few years ago but didn’t sell in order to ride up the price spike. Quite a few people have multiple homes. When prices fall, the carrying costs make a vacant home a very costly deal. That’s where the inventory is now coming from.

Exactly this. Tons of vacant homes sitting on the market at crackpipe prices. They either have price reductions or are converted into rentals. The increased supply of rentals is widening the gap between owning vs. renting costs dramatically in renting’s favor further worsening the problem.

We’re talking double. Cost to own of $6k/month vs $3k/month to rent average house around here. Who are the idiots that are financing house purchases right now?

I wish I knew how this is going to end but I could see this continuing for decades. We had 10 years of real estate price appreciation in 2 years with liar real estate middlemen saying it would continue forever. What’s more likely than mean reversion through a sudden crash is a flat stagnant market until mean reversion finally occurs through inflation.

The real question regarding stagnant vs. dropping home prices, is whether Vanguard and Blackrock will let the market drop or if they’ll decide to put a bottom on the market and soak up all the excess supply.

Do you mean that 60% of sellers with a mortgage have a rate under 5%? That would mean 76% of sellers own their home outright (40%) or have a mortgage under 5% (36%). As written your comment suggests every seller has a rate less than 5% or owns their home outright.

In Tampa we’re getting thumped by flood insurance which in my area is running ~8k a year same as home owners which is another 8k, with Usaa, plus taxes which is ~3 k on a 400k house that we homestead for lowest rate. Good thing we own it, but for potential buyers; something’s gotta give with mortgage rates as they are. Oh, and we flooded recently.

$16k on $400k just for insurance? OK, now you have my attention.

Not sure what’s worse – that, or paying $7k in annual taxes on a $400k assessment.

At least you can buy less insurance – you can’t buy fewer city services to lower your bill.

Agreed! I hate prop tax more than income tax, because I can avoid income if I really want to (sometimes, it avoids me!). Prop tax is unavoidable, and in perpetuity.

A definite area the federal government should get out of, flood insurance and protecting the tinderbox cabins in the woods of the wealthy.

So if home prices get cut in half here, how do the mbs that got off loaded to wallstreet by the banks get paid off, a dollar on a dollar. To me it’s a very big systemic problem in the very near future. As we all know, the banks sold those mortgages to wallstreet in order to turn into bonds called mortgage backed securities. No green shoots here. Mostly brown shoots.

Did you miss the biggest change since the Financial Crisis??

Most MBS are guaranteed by the government, and the taxpayer will take care of them, thank you, us all. MBS holders, including banks, will be fine though.

Oh, like in privatizing the gains and socializing the losses? Ten four.

No, not in the current setup. These mortgage companies (Fannie Mae, Freddie Mac, etc.) are under government conservatorship after having been “socialized” during the bailouts of 2008/2009. Over the past 10 years or so, they have been highly profitable. They collect fees for every mortgage they securitize. That’s how they make their money, is from these fees. Ultimately the homeowners pay those fees. And the government gets every dime of their profit. If they make losses, the government will eat those losses.

So for now, “socializing the gains, and socializing the losses.” Fair enough.

However, the Trump administration will try to privatize them, and then we’re back to “privatizing the gains and socializing the losses.”

Can anyone comment on how the foreclosure or short sale process may have changed? In 2010 someone at the bank made the final decision on a short sale or (in the case of a foreclosure) the sale price after the bank repossessed the property and put it up for sale, at least in the dozen or so I was involved in. If that is still the case, what incentive would they have to get top dollar if the difference is being covered by Fannie Mae (so we the taxpayer)? Or does that decision transfer at some point if/when the homeowner to gets behind?

Have to put in my obligatory remark…”Not in SoCal!” ‘Definitely not in OC” SoCal exceptiionalism is a thing and everyone and their mom is convinced we are exempt from any gravitational down pull…

I live in SOCAL and noticed homes aren’t selling.

Also, the prices may still seem the same when compared to 2022 but the homes are completely different. My neighborhood in San Diego had homes that needed to be gutted and remodeled sell for $1.6M in 2022. Homes on the same street are posted for $1.6M but are completely flipped and redone. They’re not selling and it is important to keep in mind that the home in 2022 solid for $300K over asking and had 20 plus bids. Not homes can’t even get an offer after 6 weeks on the marker.

I am in SD and market is very tough here

Realtors are suffering

Buyers are sweating

Sellers are salivating

Homes are not selling

Prices need to come big time

The cost of owning home in socal has increased drastically

Same in most of the NE & MW

@Jon,

Can’t believe the homes aren’t selling when a mortgage on a house in Rancho Bernardo or Poway that is 45 minutes from downtown would cost $12K+ per month. I can rent the same home for $4500. I rent and will continue to rent until sellers face reality. My neighbor just rented out her fully redone home in Poway for $4400 and it took her awhile to find someone willing to pay that who could meet all of her qualification requirements.

Back in bubble 1.0, the SD RE market was considered raging hot in 2004 and I put my house on the market in the spring after noticing inventory piling up in Rancho Santa Fe. Turned out it peaked in my area exactly when the Fed started raising rates that spring. Didnt get an offer for a couple months and took the first one and ran. Took over a decade+ for the buyer to recover.

Interesting, waiting for counterpoint from someone to post SD is still red hot, it really wasn’t that long ago so many on here saying SD is infallible and bidding wars forever and what not, who knows maybe that’s still happening at certain area in SD…now it’s the time to give your testimony.

Or maybe SD is starting to fizzle, as far as I can tell the insanity is still in OC unfortunately…maybe OC is the new SD and next to claim that infallible crown.

I don’t recall anyone, other than maybe some troll, pimping SD RE as infallible, bidding wars forever. I do recall you, perhaps sarcastically, saying your preferred areas might be.

SD is clearly weaker. Anecdotally, my areas of observation are too small (and my attention too sparse) to really see same home sales to give hard proof of price changes. There are, however, still some eye poppingly high sale prices on the high end. Those are the easiest to spot (filter to sold, sort high to low, and they pop right up). It’s much harder to see what’s happening in the middle.

CNBC: Pending home sales drop to the lowest level on record in January

High mortgage rates and elevated home prices combined to crush home sales in January.

Pending sales, which are based on signed contracts for existing homes, dropped 4.6% from December to the lowest level since the National Association of Realtors began tracking this metric in 2001. Sales were down 5.2% from January 2024. These sales are an indicator of future closings.

“It is unclear if the coldest January in 25 years contributed to fewer buyers in the market, and if so, expect greater sales activity in upcoming months,” said Lawrence Yun, NAR’s chief economist. “However, it’s evident that elevated home prices and higher mortgage rates strained affordability.”

While weather may have been a factor, sales rose month to month in the Northeast and fell in the West, which would have seen the smallest impact of cold temperatures. Sales fell hardest in the South, which has been the most active region for home sales in recent years.

Mortgage rates were also higher in January. The average rate on the popular 30-year fixed loan spent the first half of December below 7% but then began rising. It was solidly above 7% for all of January, according to Mortgage News Daily.

Home prices have been easing over the last few months in certain areas, with more sellers cutting prices, but nationally they are still higher than they were a year ago.

You gotta love Good old Lawrence, spin doctor to the rescue everytime..

“It is unclear if the coldest January in 25 years contributed to fewer buyers in the market, and if so, expect greater sales activity in upcoming months,” said Lawrence Yun, NAR’s chief economist

I thought that was funny too – blaming the weather for poor home sales.

Next they’ll be blaming lunar cycles for low sales vol.

We just finished an appraisal of a new townhouse in a very good section of NW Washington D.C. It’s on the site of the old Walter Reed medical Center, which was moved a few years ago. The builder gave a $30,000 concession on the 1 million sales price. It’s a well built property, and brand new with all the latest amenities. So, if they had to give $30,000 back to unload it, then I’d hate to imagine what the used homes in that price range will have to do to unload them.

So you’re saying there’s a chance I can get that 1900s Georgetown townhouse I’ve always wanted for….less? Nice!

Manchester NH Zillow Home Price Index still up between 6.4-7% increase. Real estate ALWAYS goes up, right? Right?

Right. Until it goes down.

here is one of many examples of “Real estate ALWAYS goes up, right? Right?,” even in major and expensive cities:

I bet they are assessing well above actual comps. Nashua does this to get more money out of homeowners.

Greedy city assessors benefit from higher home prices just like the NAR et al.

can’t wait for the housing market to crash. The assessed value of my properties is insanely high. can’t afford the property tax anymore.

Many will have you believe it will not crash ever, remember this time is different as they say… Just like Bitcoin now, maybe this is the perfect buy the dip moment before price and demand back to the moon again…

Bitcoin descending thru 79k

A real estate agent looked at me with a straight face when I told her the market was stagnant right now and said, “I don’t know where you heard that! The market is HOT right now we are closing sales left and right”

If I had been drinking coffee I would have spit it in her face. Just Wild. These are the same people that were telling you 20% year over year gains were the “new normal” and to buy NOW in 2022.

Just absolute snakes and leaches. Their profession needs to die, rapidly. I only have about a 50% success rate of even viewing a house without an agent since their corrupt “settlement” last August. YOU DO NOT NEED A BUYERS AGENT TO SEE A HOUSE. THEY ARE LYING TO YOU. I even showed one listing agent the language in the settlement proving that and she just shrugged and said, well I require it so if you don’t have your own agent you have to sign with me to buy the house (and pay me). You can’t just expect to offer 3% less because you don’t have an agent. They can all fuck off. That’s exactly what I expect. They’re starving because they are greedy and corrupt and did this to themselves by engaging in a worthless profession.

As a seller I decide who I let in my house. I’m not letting some rando walk around without an agent.

Overall the Real Estate market won’t be crashing. It may drop in certain areas of the country and there will be certain areas of the country like the NE and MW that will be flat with slight increases. The NE and the MW still have low inventory levels and unless a seller has a life event they aren’t selling their home. Overall it will be a stagnant market

Typecheck-

Reduced “assessed value” on your properties does not ensure a lower of your “property tax.” Reduced property tax requires a decline in local government spending, additional support from other tax jurisdictions, or a broadening of the tax base.

“Reduced “assessed value” on your properties does not ensure a lower of your “property tax.””

Right – you have to fight for it with an abatement.

My County decided back circa 2009 to ditch the “comparable sales” valuation method of assessment and go with “replacement value”. That trickery kept assessments from heading into the basement even though many homes dropped 80% in value by 2010-2013.

Now the County uses a combo of the two to keep assessments on a ever higher march.

Most internet commenters do not understand “mill rate” concept for property taxes

Typechek,

They gonna fight it tooth and nail. Invitation homes, American Homes for Rent, Progress Residential etc…. if the market crashes the value of their extensive portfolio goes down. So instead of letting a house sell for 20% less right next door to a house they own, they are coming in with other LLC’s they control and buying those homes or they are leasing them back to the person who was in foreclosure so the house never hits the market. Once these big rental companies have liquidated say 80% of their holdings, then maybe they let the housing market crash. Govt’s get used to those property tax levels so expect a slow crawl for those to get reduced. But if you think the housing market is going down while private equity are holding the bag… its just not possible. How long will it take for those housing rental behemoths to unload their portfolios? At least 2-3yrs so the housing crash wont occur before that & property tax aint going down til 6mo-1yr after the crash. I’m trying to buy a home now that is currently being rented out by Padsplit, its a bigger firm in NYC that actually owns the LLC to the house while padsplit manages it. There has been a price cut on it of about 7%, they are budging a little but I just don’t see them giving it away for 25% below the original listing. Its been for sale or over 100 days

Those States where they deport the most should see a corresponding drop in housing costs. Simple supply and demand.

There are about 2 million illegals in Texas so if you deport them and another 2 million legal family members follow them, we could be seeing 4 million people hit the road. Fear and loathing has already seized the country and it’s only just started.

I always imagined illegals as extremely poor, jobless latinos looking to make a better life for themselves and their families. Who knew they actually have great jobs and 20% down waiting in their bank accounts, with banks eager to lend.

They rent. What happens when landlords have less available tenants?

Been seeing families, quite extended families get together to buy houses and pickup trucks for a long time.

Not only recent immigrants, legal or not, have been doing this for generations.

Sometimes with recent immigrants, many more folx end up in the houses. For instance, next to a friend, a 2&1 ended up with 12 adults living in the house, w several children and always at least one adult home while all the others were working…

Anecdotal for sure, but have read it has always been done like that by some folx in the land of opportunity.

These types of comments drive me absolutely insane. How are people this thick headed? They live somewhere. Even if they don’t own the house, by occupying a physical piece of property this has an upward ripple effect on the market through supply and demand.

It is a remarkably simple concept.

Early on, there was a banner day reported if over 900 ice arrests. If they keep up at that banner day pace every single day, it will take a mere 30 years to reach their 10 mil goal.

Oh ok, then they should just give up then.

Yes, they should give up tricking rubes into believing that 900 ICE arrests a day are either extraordinary, or a realistic pace to expel the illegals they promised to expel.

This assumes that the people that they deport are the same people that are competing for home purchases.

Unless you’re talking about H1B visa holders, and I’m thinking this probably isn’t the case…

Well there is an additional 3 million drop in demand per year due to stopping them in the first place plus those deported. Add in the current homebuilding rate and it begins to make sense shelter cost is going to drop, likely significantly many/most States. Economic Migrants are known to double/triple up families per household so they are indeed a significant factor renting and homebuying plus the Government aid they receive. For example Canada has an insane immigration policy right now, their shelter costs thru the roof and quality of life drastically reduced cost of living, access to medical care and Education. Net result current political party about to be dumped by voters. Perhaps those who advocate for open borders might consider the negative effects?

The fall of the Western Roman Empire (5th century AD) was heavily influenced by mass migrations of Germanic tribes, including the Visigoths and Vandals.

No, it doesn’t. They are occupying rental units that were made rental units because of the increased demand for rentals. What happens to these rental units when there are no more tenants to cash flow the property? Hint: They sell it. Then rental units go on the market. Bigger hint: these are cheap houses, the kind the market is in very short supply of.

No one wants to admit that the sudden shock of low supply of cheap starter homes in 2021-2022 occurred at least in part because of the millions suddenly demanding rentals in this space.

It’s so simple yet then open-borders-are-compassionate-and-not-harmful crowd refuses to admit how stupidly wrong they were because Trump is mean and orange or something.

I disagree. The people being deported represent a substantial portion of our labor force and losing them will increase the shortage and drive up labor costs. That, with the increased lumber costs from proposed tariffs, will make it hard for builders to lower prices at a time when demand is at its lowest. They may have to as inventory piles up but they will take a bath and it will create another sizable gap in building like after the 2008 downturn and perpetuate the overall inventory shortage into the future.

Agreed, Tim. If deportations of this scale were logistically possible (unlikely), it’s estimated that would include “1.5 million construction workers, including more than one in three roofers, ceiling tilers, stucco masons, plasterers and drywall installers.” Not good for the housing market.

Have you seen the quality of construction these people are putting out for the likes of D.R. Horton, etc.? It is ABYSMAL. They are not qualified for what they are doing. Put a marble on the floor and it quickly rolls to the wall. There is no such thing as plumb, level or square. I’d like to see these corporate builder scum in jail for what they’re doing.

For some entertainment (or horror), google “DR Horton Reviews” and read the stories.

Yet Wolf’s articles constantly show that newbuilds are selling.

You are welcome to have your opinion on their quality, but the people putting cash on the counter clearly think the quality is good enough.

If there are several million fewer people in the US, rents will definitely come down. This may somewhat offset what you are talking about.

Wrong. House prices remained very low for 10 years post GFC despite a 5 year nadir of home building 2008-2013.

I bought a 3900 sq ft new construction house for $435k in 2015 that had been on the market for 1 year vacant and got a sub 3% 5/1 ARM on it.

It is simple supply and demand. That’s it. Salaries have not doubled in 10 years, I’m sorry. What’s happened is the cheap end of the real estate market got bought up and converted to rentals in 2021 due to interest rate cuts and the sudden shock of millions of illegals threw fuel on the fire and this effect rippled upwards into all price tiers.

All the new construction that happened since has been in the mid-upper range, not the starter home category that is needed to fix the problem.

It is asinine and rather ethically horrible to say that cheap illegal labor is needed to keep homes affordable. Umm, were you not paying attention in 2021 when illegals were flooding through the border and labor prices were skyrocketing? That blows your theory of correlation there right out of the water. All kinds of horrible things go on at construction sites where there is illegal labor. Sex trafficking is rampant. You can look this up and see what your “compassionate” ideas actually result in.

Matt,

“It is simple supply and demand.” New construction is a major variable in supply and demand. Availability of cheap labor significantly impacts input costs, as do tariffs on lumber and other imports as Tim mentions. Another variable is availability of unoccupied homes, which was very high after the GFC. More than 5 years averaging over 1 million foreclosures a year is why there wasn’t enough demand for homebuilders to churn out homes. Since COVID there has been less than 200k foreclosures a year.

“new construction that happened since has been in the mid-upper range, not the starter home category.” Wolf’s articles repeatedly debunk this. New construction has been smaller homes on smaller lots, especially over the past 3-4 years.

“It is asinine and rather ethically horrible to say that cheap illegal labor is needed to keep homes affordable.” It’s not asinine and unethical to state a fact. Perhaps it’s unethical for companies to hire illegal workers? Perhaps many workers are legal immigrants who would leave with their families if there are deportations? Perhaps it’s hard for you to accept that illegal workers make up a significant portion of the construction labor force, and that US citizens are not interested in those jobs for those wages.

“sub 3% 5/1 ARM” ooof, probably should’ve went with a fixed rate, hope you paid it off quick.

Not sure what can move this. Economy is humming and supposedly 50% of the consumer spending is done by households making over 250K a year. Not sure how tariffs kicking in affect all of this but assuming minimal. More wait and see until something happens that forces mortgage rates down but that generally means other bad stuff happening.

I agree with your comments. Stagnation is the keyword right now. In most markets especially in the NE and MW there are fewer sellers and fewer buyers.

In Florida inventory is up huge BUT prices still haven’t budged. They remain at extremely high levels while inventory keeps building, and building, and building…

Perhaps if this giant pile inventory remains unsold at the end of the upcoming Spring selling season sellers will finally get a clue and we’ll start to see some significant downward price movement. Not sure where the point is when sellers cry uncle but I think there is reasonable chance that 2025 is the year it finally happens.

Condos are budging more than houses, though houses have started to budge too:

What you could see is after the helocers get under water and no longer draw on house like a personal piggy bank is people simply walking and flipping the keys back to the banks. But this time the banks are simply servicers and not bag holders, and they’re just gonna mark properties down and resell and the supply slowly goes away after a while and prices drop significantly We hope. As prices fall that will capture more and more underwater helocers and they’ll walk too until despair sets in and the thing bottoms out.

I’d love to see my taxes drop on my rentals, but somehow that won’t happen as the county will just up the mileage rates to make up shortfalls.

A question for wolf would be just which taxes will pay off the underwater mbs holders, state, federal, or municipalitie?

“which taxes will pay off the underwater mbs holders, state, federal, or municipalitie?”

D. None of the above.

Correct answer: federal borrowing will make them whole.

Then, federal taxpayers pay interest on that new borrowing forever.

The majority of people are financially sound and don’t have to sell. They want to sell buy they are not in a distressed situation and have to unload it.

You forget the large number of vacant homes that people moved out of a few years ago but didn’t sell in order to ride up the price spike. Quite a few people have multiple homes. When prices fall, the carrying costs make a vacant home a very costly deal. That’s where the inventory is now coming from.

Sellers are really stubborn. I live in northeast Florida and follow my neighborhoods sales on Zillow. 2 houses have sold in my neighborhood in the last 90 days. One house was bought in September of 2023 for 183k, and the buyer immediately tried to flip it for 299k.

It finally sold in January 2025 for 255k after MANY MONTHS of very tiny price drops. My anecdote doesn’t mean squat of course, but it seems as though the seller could’ve gotten their 255k a lot more quickly if they were less greedy.

No one got the memo in 11570.

I’m so grateful, for a change, not to be in the crosshairs of the latest gold rush. Several decades of that was enough. I’m glad I didn’t freshly move into a storm corridor with an impending insurance and property tax crisis, and buy in at the top. Sometimes torpor is a blessing? Buy and hold, I know, is so out of style. But over several decades, inflation seems a pretty sure thing, and this shack has been a hedge. But expecting all that ease to come quickly would have been a pipedream. There was a financial crash, and a divorce, a pandemic, and some other things.

I feel while the prices are too damn high also the south got hit with some serious storms and devastation,almost bought a home on 60 acres in NC(priced within reason),while the town directly was OK that county got hit pretty damn hard along with other counties and states,feel will affect sales there along with other regional states for awhile.

I will just hold out renting,am open to buying just not at insanity levels.

To high? go to Home Depot and price out some windows $24-$28,000 for the windows and then you gotta get them installed. The house is not even worth the sum of its parts due to Biden‘s manufacturing delays.

And as a financial guy, you should know the largest tradable commodity is a collateralized debt obligation, a CDO, which is back by the home if we have inflation, the only thing to counteract that is the home note.

“…the largest tradable commodity is a collateralized debt obligation, a CDO, which is back by the home if we…”

You mean MBS?

CDOs are mostly used in CRE and other commercial lending, mostly with non-housing debts. And the outstanding balance of CDOs is much smaller than the MBS out there. But most MBS are guaranteed by the government, so the taxpayers are on the hook for credit risk, not investors.

Yes, Jessup, you are totally right, Biden should be ashamed of manufacturing those cheap Milgard and Pella windows so slowly. F him!

CDOs, c’mon, man. I’m guessing WR didn’t smack you down because maybe you did RTGDFA. OR he otherwise took mercy upon your soul.

Howdy. YEA HAW. NO more peaking with housing prices????? Lets hope so…. Lets hope the hissing continues without a POP……..Still a long way to go down Youngins. Stay Tuned…….

In the movie “Wall Street,” which takes place in 1985, Charlie Sheen is making big bucks with Gordon Gekko and he needs a new place to live with his new girlfriend Daryl Hannah. The real estate agent tells him she can get him a mortgage for 10%. They had been much higher, so 10% at the time seemed like a bargain. Now, since mortgage rates had been much lower for many, many years, 7 percent seems way too high. So my point is it’s all relative. Coming from a much higher cost makes it seem cheap, coming from a much lower cost makes it seem expensive. I think there are many factors besides mortgage rates which have the housing market in limbo, probably the number one reason is simply that home prices are, as Mr. Richter points out, still way too high.

—Along with just about everything else.

I see that there are many agents and mortgage lenders with egg all over their faces due to the “marry the house and date the rate” tactics!

Remember this, the AVERAGE 30 yr frm over the last 50 YEARS, approaches 8 PERCENT!!

So, are you still holding your breath waiting for lower rates?

What they should have said is: “Marry the purchase price, date the rate.” It’s the purchase price you have to live with. You can never change it.

Hopefully someday there will also be a buyer’s strike in the stock market. “What, 10 times p/sales? No thank you”. Stock prices are hugely inflated. Also they are paying too much for the privilege of holding Bitcoin.

“Something” is starting to happen. I was taking a cursory glance at my local Raleigh metro region this week, and there is suddenly a TON (comparative to the last 3-4 years) of newer existing homes coming to market. Units that either sold for ~$400K new in 2014-2019 or ~$750K new in 2021-2023.

We’re talking about stuff that was bought brand-new in 2022-2023 for $800K at peak mania that are now being listed — they won’t sell — for $1.2M… and, it’s not just a few. I’m not sure how much of this is just aspirational pricing vs. “I need to get this amount to cover my perceived investment.” I guess we’ll see. We’ve recently had new property assessments that have skyrocketed taxes and insurance in the past year.

I think there are potentially some bag-holders starting to come out of the woodwork, or maybe just people waking up to the realities of their plight who are trying to get out before it all goes to shit.

Either way, I really hope there isn’t a single buyer out there gullible enough to fall for a $400,000 increase from 2023. The greed is just astounding. I really hope all these types of sellers just try to game too long and wind-up bankrupt.

“I really hope all these types of sellers just try to game too long and wind-up bankrupt.”

Most will. Same thing happened last time. What they don’t even realize is that they are already underwater.

me too. i’ve looked at zillow listings all over america. it’s fun to see people who bought their homes in 2017-2019 for $400k, listing it for $1 million in 2022, take it down when it doesn’t sell, relist it in 2024 for $1.3 million, and then slowly reduce the price down to $950k. still delusional.

i hope these greedy whores lose everything.

The depth charges have been set. The timer is ticking. I am hoping to (like a few other Wolfstreet readers) jump in right after the big KABOOM while everyone else is dazed and confused.

I just witnessed a home sold for $600k summer of last year hit the market for $1,250,000 after new paint and obvious flipper quality shit kitchen and bathroom remodels.

No, I’m sorry. A trendy paint scheme doesn’t more than double the value of the house in 7 months.

These people can all eat shit. If anyone is gullible enough to fall for this, the entire market is permanently screwed. I fell for this kind of junk flipped house on my first house but it was at the 300k price point. The interior flooring they used on the front porch fell apart in 6 months and that was only the beginning of the nightmare….

I hope anyone who can afford a 1.2 million dollar house isn’t a fool, but all it takes is one.

While it’s not that level, I can say that in Columbus Ohio where I reside, inventory is skyrocketing and back to 2020 levels. My guess is it will be around 2019 levels by eoy. It’s piling up and south Columbus is covered in price cuts. The more affluent areas are holding out but even those are having difficulty moving and often sit for weeks or months.

I’m seeing the same slimy tactics as well. Someone bought in 2023 for 250k and then 3 months later they try sell for 400k. It doesn’t, they remove it and then relist and slowly decrease price 2k every 3 months, then take it off and relist again.

Condos in FL have a long way to fall because of the new law that took affect this year requiring more reserves for repairs. Many condo associations monthly fees are $500, $600 a month. I have seen some pushing $1,000 a month.

Inventory is rising and prices are starting to crack, sellers are starting to lower prices after the place doesnt sell after 6 months.

if you look at the Western towns that were the biggest targets for the pandemic migration boom, you see a lot of luxury homes that were purchased in 2020 or 2021, with tons of money, dumped into “updates” since purchase. And now many are listed for sale for astronomical asking prices, and there they sit! Places like Breckenridge, Colorado, and Park City, Utah just a name a few.

Also a ton of luxury, new construction in these same destination mountain towns in the West, but none have more homes for sale over $5 MM than Park City and its surrounding towns. Over 200 for sale listings over $5 MM rn in Park City area. If you compare this with other mountain town destinations with a similar size, geographic footprint, Park city has – in some comparisons -three times the number of listings over $5 MM.

But as WR always says, real estate is hyper local.

Wolf Man – you should do a column on cryptos.

BitCoin fell over $4300 today and $23.6K in the last 30 days. Personally, I hate cryptos, but it’s interesting what’s happening.

let them burn.

That’s my three-word column on cryptos.

Yup, the new tulips…

LOL – excellent article on crypto

can you give me a tl;dr on that? ;-)

I see it now…a new Netcrap mini-series…”Wolf Richter, Salem Witch Hunter”. Burn Baby Burn! 😡🥳

I wish to see bitcoin go the way of Beanie babies….both have about as much real world use case…except one has long overstayed the hype train…burn it to ground Rome collapse style please

You can still buy or sell a Beanie Baby and hold it in your hand (it may be with $2 though). Try doing that with Bitcoin.

I think that an underlying assumption of the always optimistic real estate market,particularly at the lower end, was that the open border policy off the dems would continue. The excess inventory in Jacksonville Fla. Is staggering. If the present administration is serious about the border,and reducing the 2 1/2 trillion a year stimmy,serious slowdown is on the way.

Bitcoin is heading for a price below zero. Investors in Bitcoin will have to pay money to liquidate their positions in order to take a capitol gains tax loss.

‘Investors’ have nothing to do with BitCON.

Bloomberg is reporting today that BlackRock is adding its record-growth Bitcoin ETF – IBIT – to its model portfolios that allow alternative assets. Whatever you think about Bitcoin, it isn’t going to zero. It’s now a very large and established part of the financial marketplace. The younger generation views it how Boomers, GenX, and older generations viewed gold.

Somebody should make a list of the all the stocks that BlackRock had in its various funds at some point that then went to zero and vanished. Many thousands of them. Happens all the time. But sometime before they’re at zero, BlackRock pulls them out of the fund.

The Wyoming Senator who was hosting the bitcoin conference in NYC said BITCOIN was digital gold. What a pile of bull s%it.

He got the first part right. It’s “digital.”

It was a she. Also, no one mentioned that Bitcoin dropped $20,000 right in the middle of the Bitcoin convention in NYC. While she was speaking it dropped $5,000.

Maybe Bitcoin ETFs will become this generation’s mortgage bond credit default swap. So many unknowns

The “shadow inventory” of existing homes appears to be quite substantial (“now you see the listing, now you don’t”).

Every house sells for exactly the right price at exactly the right time. Never too high or low.

For that buyer and that seller.

LOL, no, if volume and demand collapse, like they have, then prices are too high (includes the price of credit). That’s what high prices do: they collapse demand. Basic economics.

Realtors are really suffering here in the DC area. No listings, no sales, no commissions. Now we have 375,000 federal workers of which 37,000 have already been given their walking papers, with more to come, and 5 times that amount of contractors and spin off jobs to be lost in addition to the 37K. The only saving grace is we’re not too far from New Jersey. It’s the only state that won’t let you pump your own gas,. I hear there are a lot of job openings up there for gas station attendants.

Maybe nobody wants to live in the south anymore

Can you imagine the shi* show the stock market would be if it were to function as the housing market currently is? Insane sky high prices, but nobody wants to lower their prices. Buyers? They are on strike, not buying much. Stagnation on steroids. Can you imagine if the NYSE were like this? it would be depression city: Something is off in the current housing market. It’s not behaving like a normal marketplace.

Imagine the economy if the stock market behaved as such.