Prices Are Still Way too High. Something has to give.

By Wolf Richter for WOLF STREET.

Yesterday, we looked at the surge of new completed “spec” houses for sale, and at the surge of new houses for sale at all stages of construction, for the US overall. Now we’ll look at at new houses for sale in the four regions of the US.

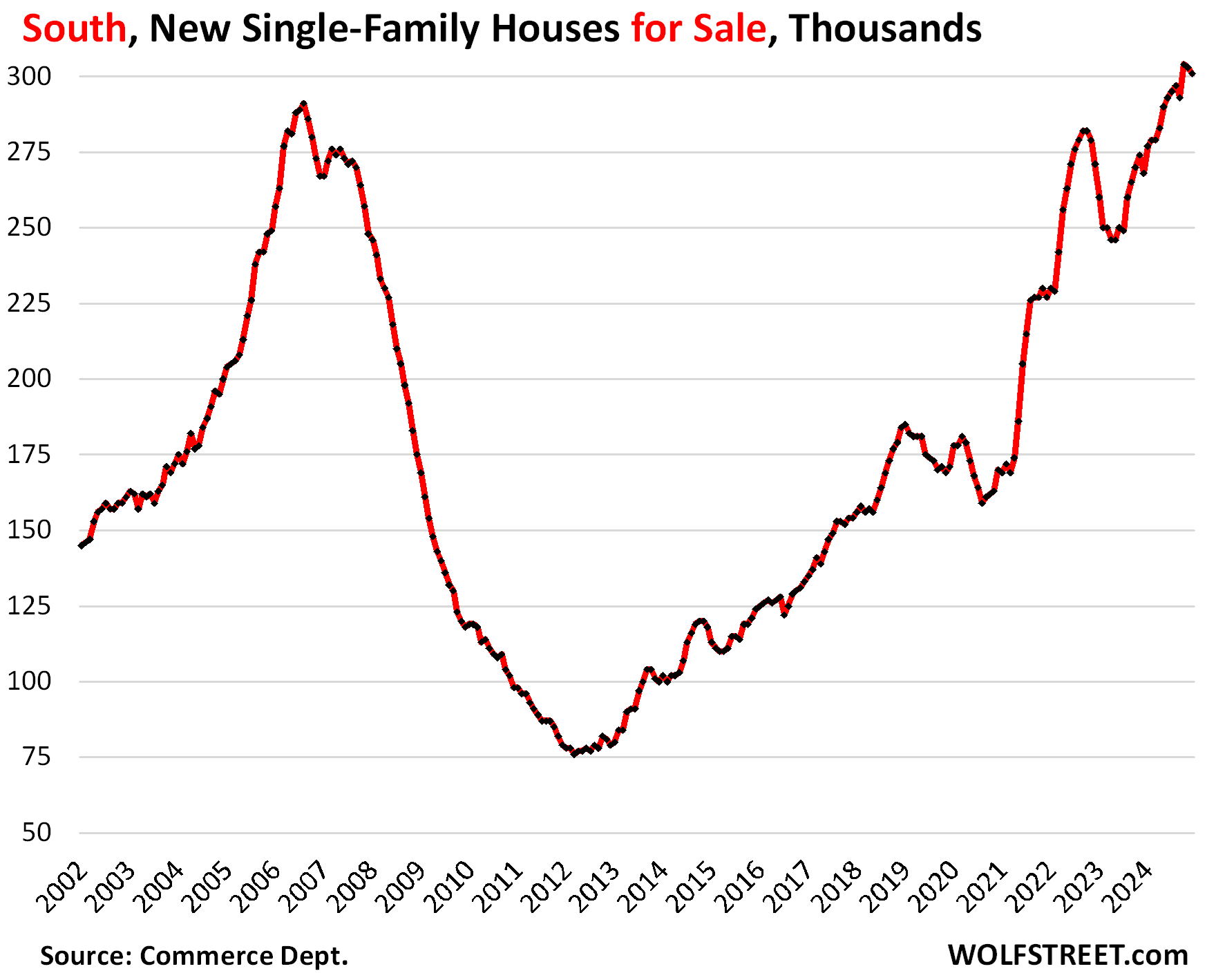

In the South – the largest region, with a population of 133 million, see map below – has the most inventory of new houses ever, surpassing even the astronomical levels on the eve of the Housing Bust, just before it all fell apart.

Since June 2024, new houses for sale in the South have surpassed the high of August 2006. In June, there were 293,000 new houses for sale (compared to 291,000 in August 2006). Since then, the inventory of new houses for sale has further ballooned and in October reached 304,000, and has remained in that range through December (301,000). Since December 2019, inventory has exploded by 76%. This is a massive amount of inventory of new houses for sale.

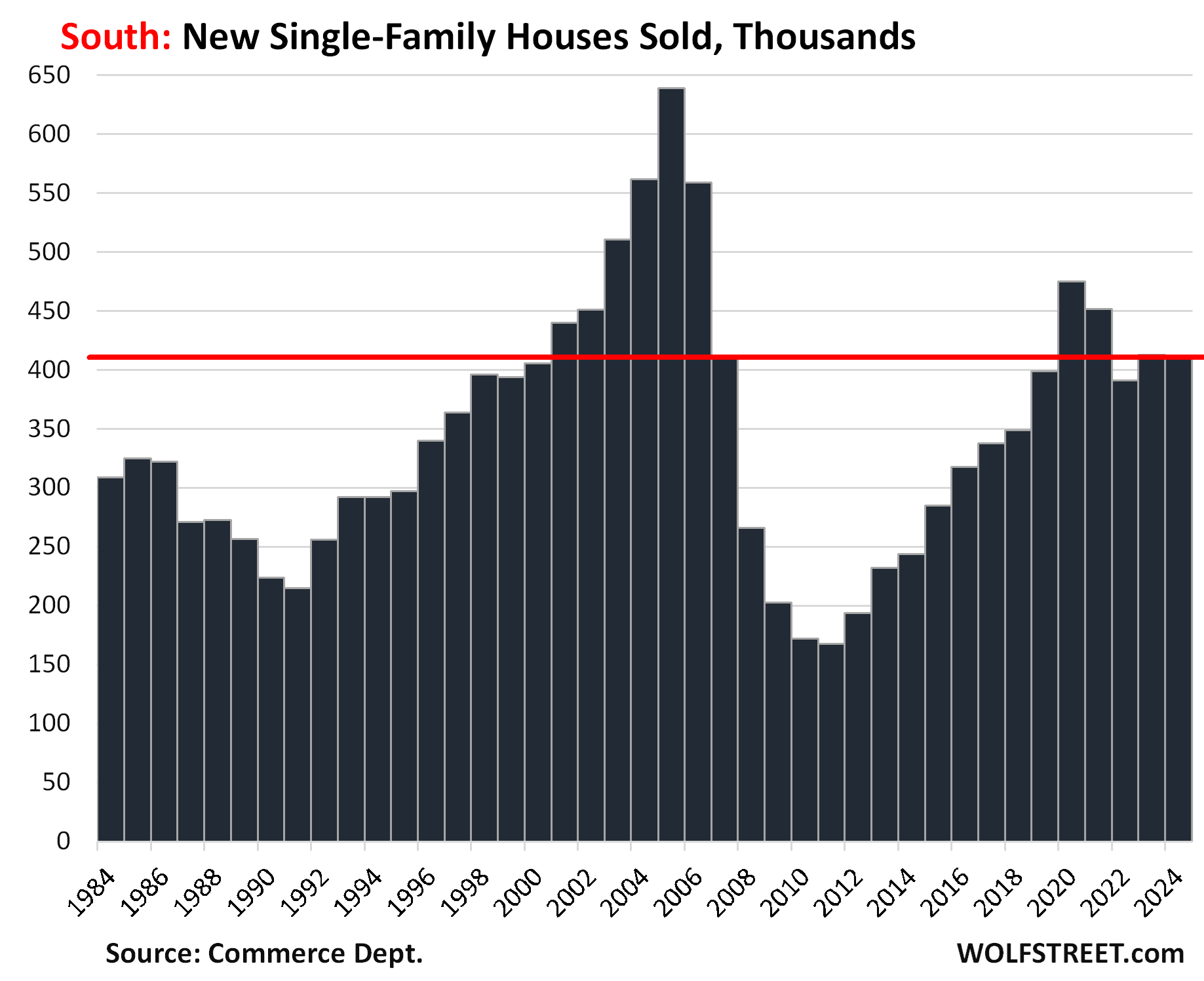

But sales of new houses in the South in 2024 edged down a hair from the prior year, to 411,000 houses sold, and was down by 13% from 2020 and by 9% from 2021, but was up by 3% from 2019.

Those sales were reasonably decent, thanks to the large-scale incentives, including mortgage-rate buydowns that homebuilders have been using to stimulate demand.

So it’s not that sales have collapsed like sales of existing homes – they haven’t – but that sales lagged far behind the speed with which homebuilders put inventory on the market over the past several years, and now there’s this glut of houses for sale.

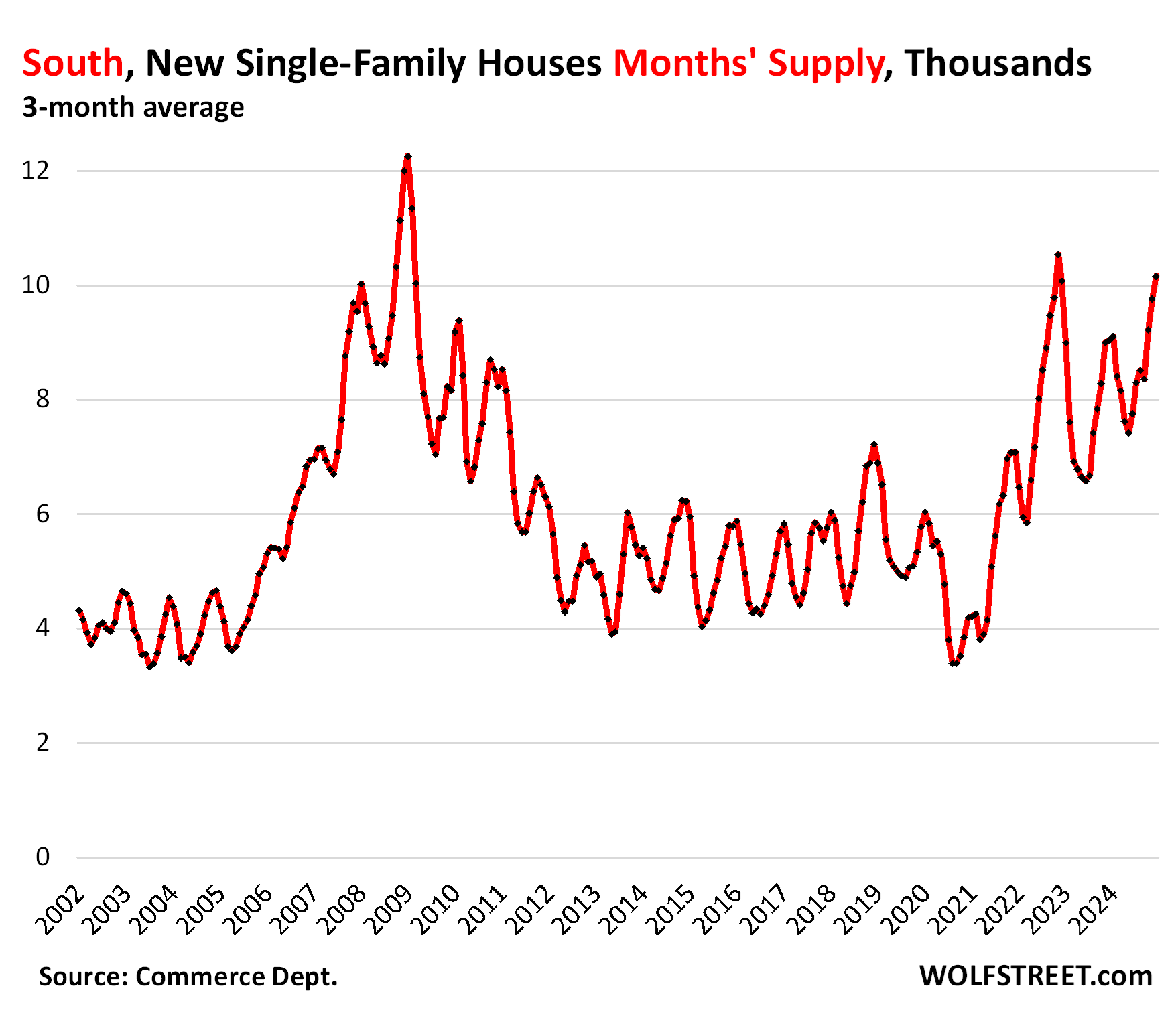

So supply of new houses for sale, at the current rate of sales, has pierced the 10-month range. To iron out some of the big monthly squiggles, we look at the three-month average. Seasonally, the peak supply period is in November through January in this three-month average. Beyond seasonality, the trend is clear, with supply having about doubled from the pre-pandemic range:

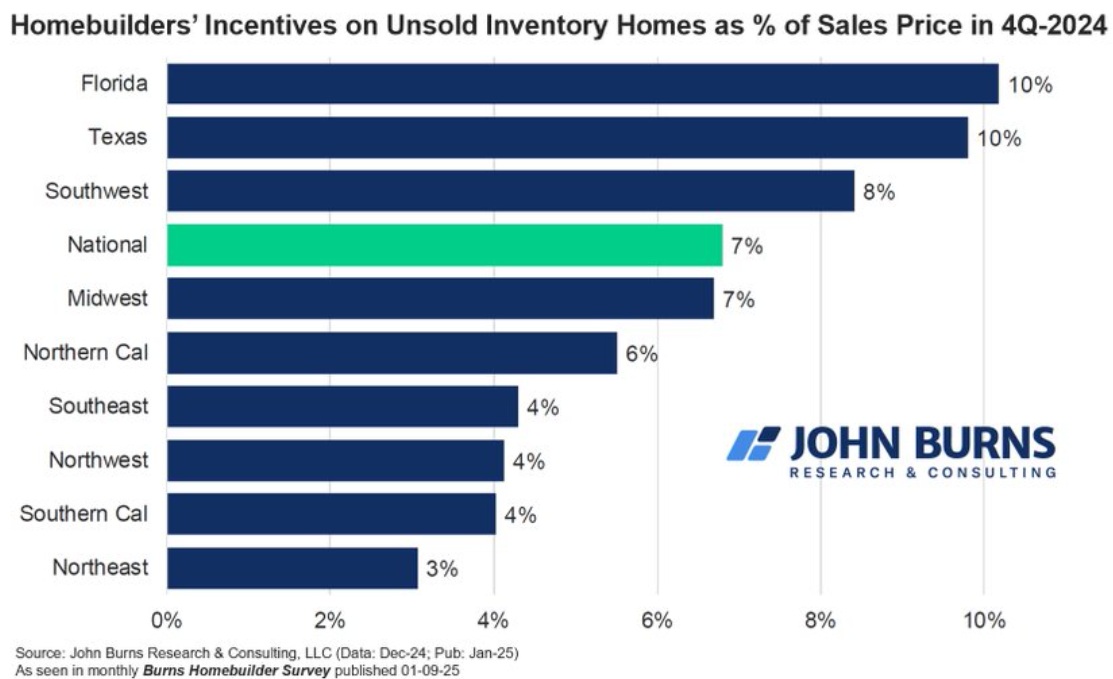

Homebuilders offered incentives amounting to 10% of the sales price on average in Texas and Florida to get the inventory moving, according to the most recent Burns Homebuilder Survey. And that’s clearly not enough to get the inventory moving.

Here is a map of the four Census regions:

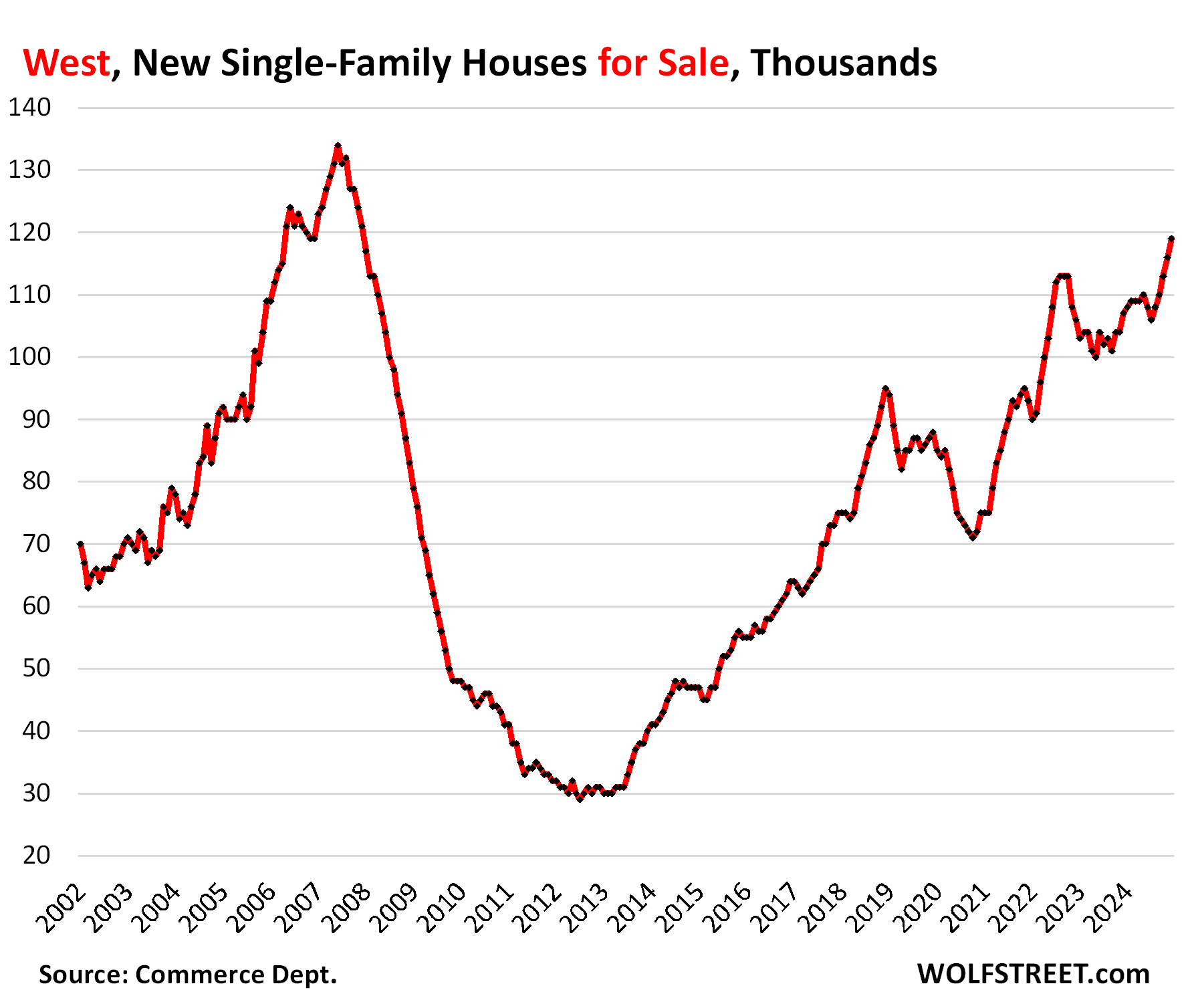

The West.

In the West – the second largest Census region, with a population of 80 million – a similar problem is piling up. Inventory of new houses for sale surged to 119,000, the highest inventory since December 2007, not far below the peak in June 2007 early on in the Housing Bust, and up by 35% from 2019:

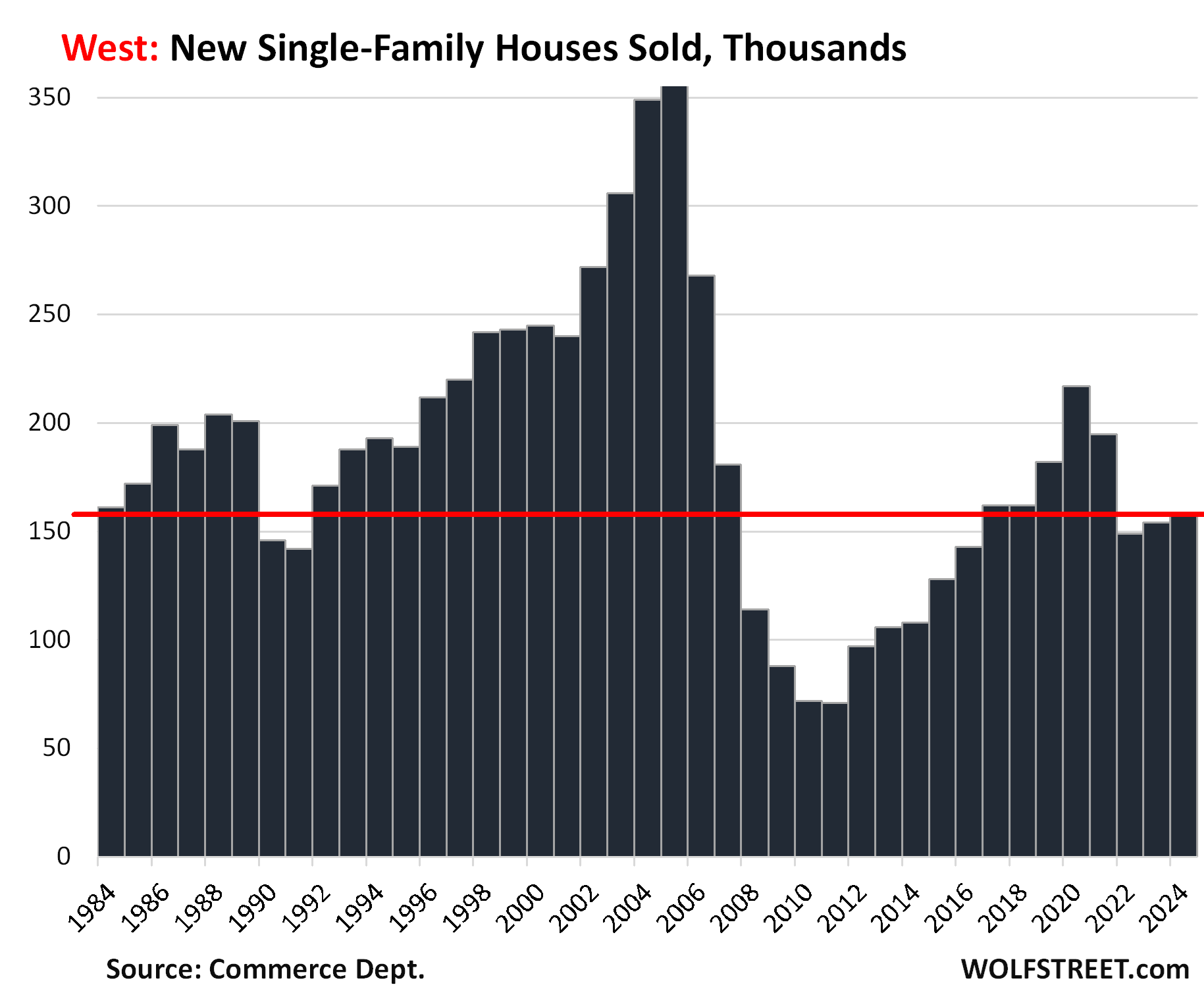

But sales have been anemic in the West because prices are way too high. In 2024, a total of 157,000 new houses were sold, down by 28% from 2020, and down by 14% from 2019. While annual sales were up from the prior two years, all three years were at the lower end of the scale, with only 2008-2016 and 1990 and 1991 having been even lower.

So lots of inventory piling up and sluggish sales:

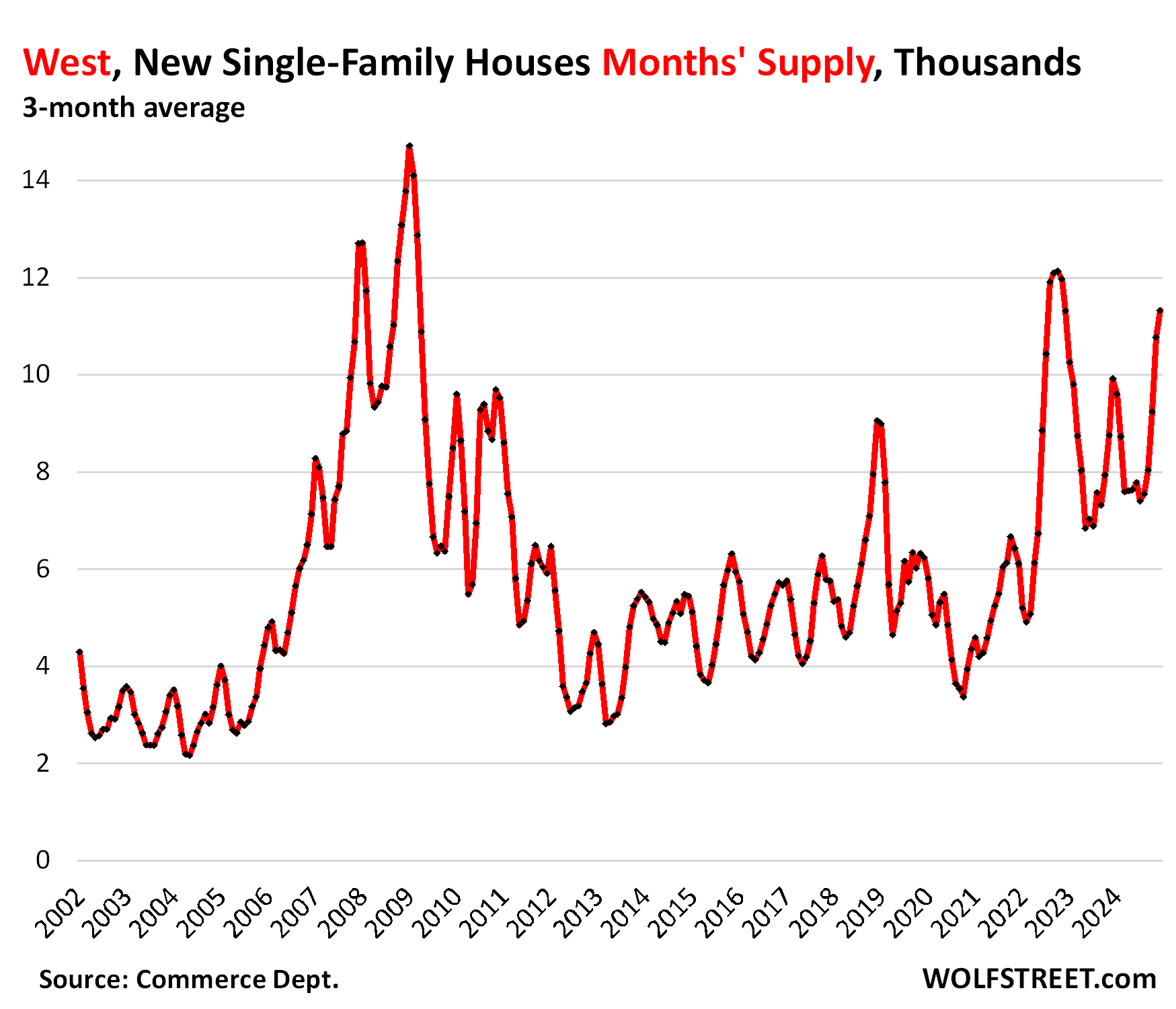

Supply has therefore spiked to 11.3 months on a three-month-average basis. There were only three brief periods with higher supply:

- In late 2022 as the market for new houses was waylaid by the surge in mortgage rates, triggering a tsunami of cancellations of new-house purchases, as buyers who’s sighed the contract when rates were 3% or 4% couldn’t take delivery when rates were 6%.

- Four months of November 2008 to February 2009.

- Two months of December 2007 and January 2008.

The other two regions are not big players in the single-family market

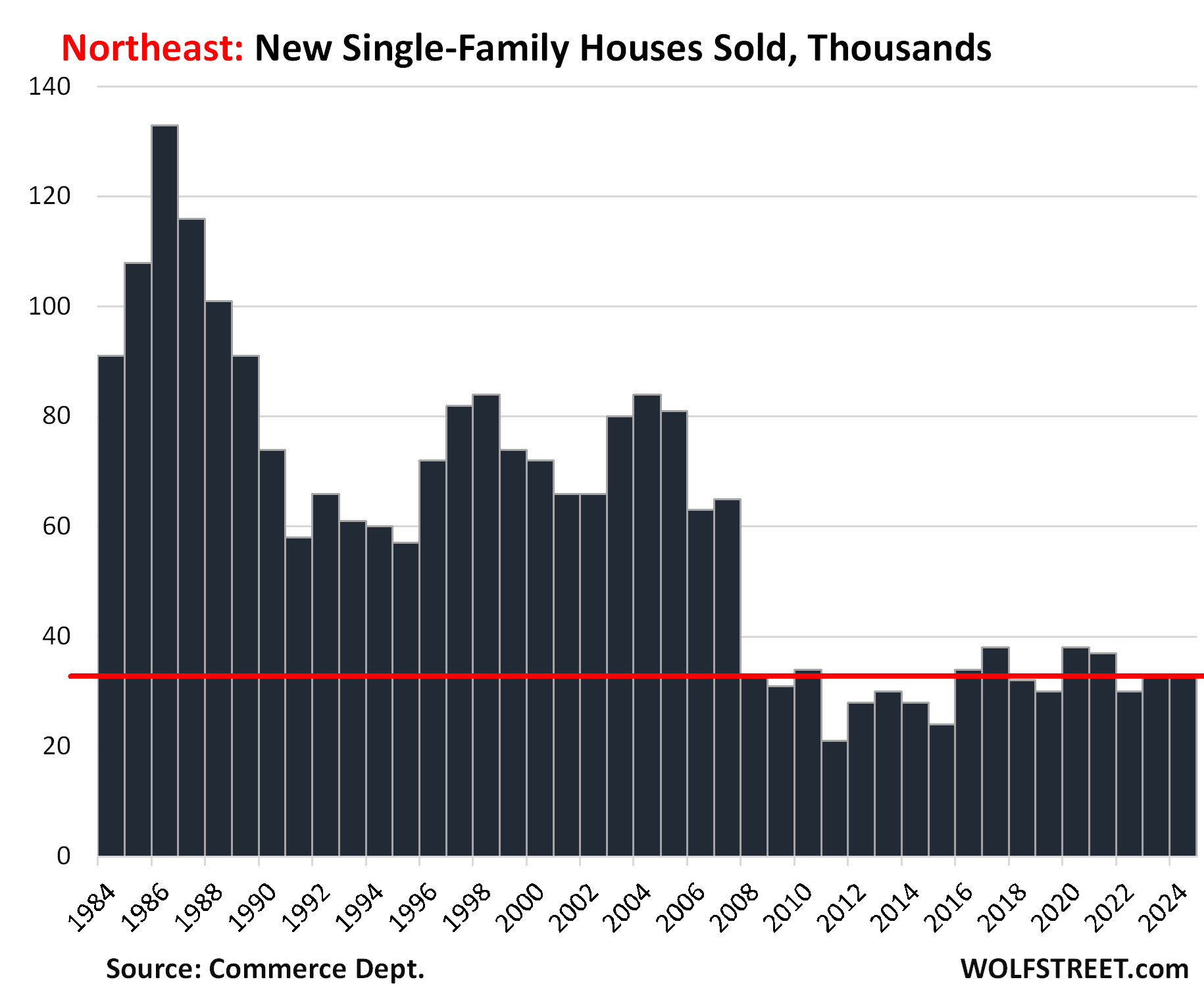

The Northeast and Midwest are smaller in terms of the population, and much much smaller in terms of the market for new single-family houses. The regions are dominated by huge old cities, particularly the Northeast with New York City, Boston, Philadelphia, and the cities and urban areas around them. New construction is focused on multifamily to increase density and shorten commutes from the already unwieldy urban sprawl.

So there are only a few sales of new houses in those two regions, amid rising inventory and supply. But all of it is too small to really weigh on the national scale.

In the Northeast, only 33,000 new houses were sold in all of 2024, down by about two-thirds since the 1980s, but roughly in the range of the past 10 years.

The Census Bureau rounds sales on a monthly basis to the nearest 1,000 houses. In the Northeast, these rounded sales have been either 2,000 a month or 3,000 a month rounded. And on a few occasions 4,000 a month. We use annual sales here which would largely average out the big rounding errors of the monthly data.

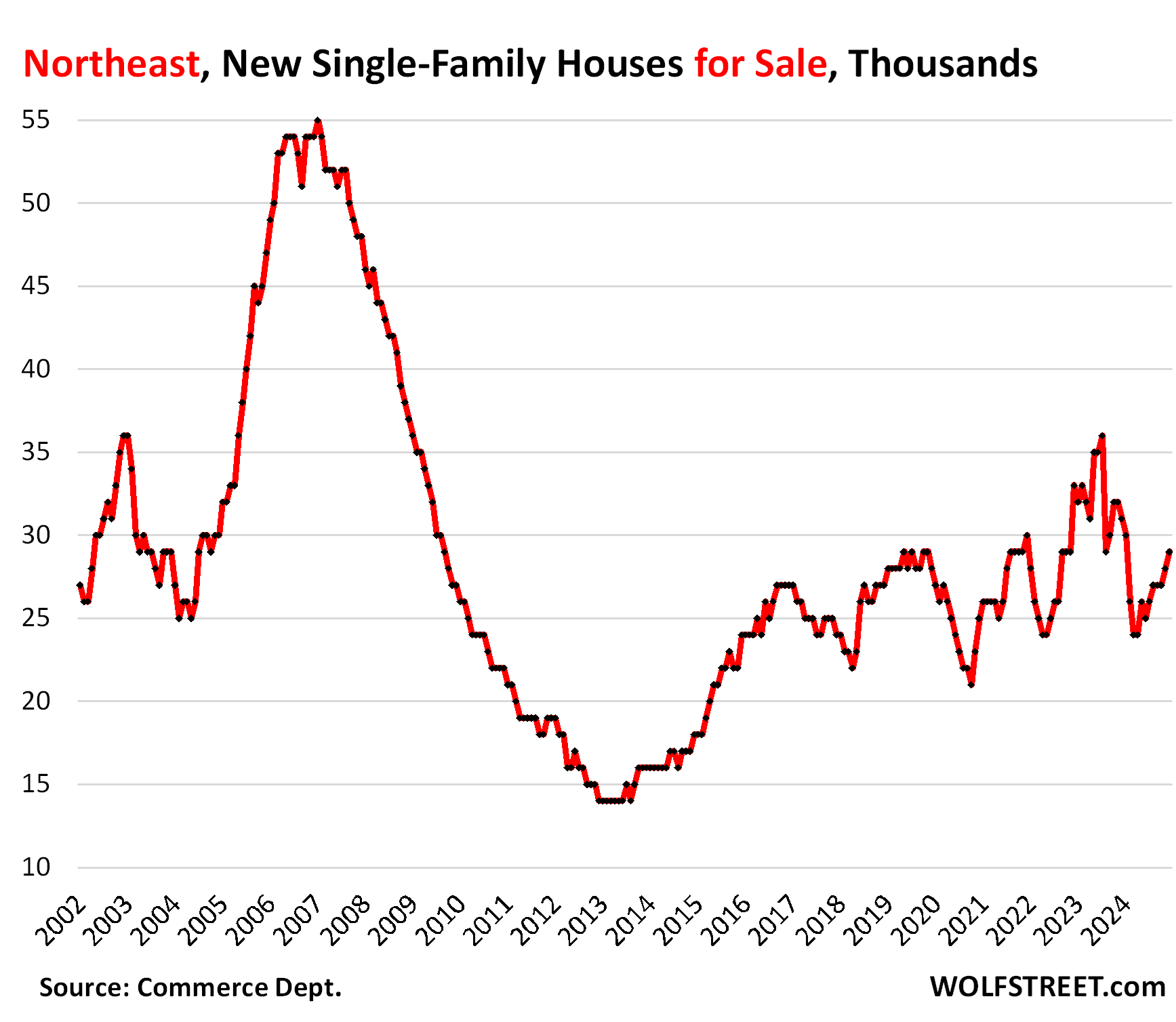

Inventory in the Northeast has been zigzagging higher over the past few years. Supply reached 17 months, by far the highest of any region. During the worst moments during the Housing Bust, supply reached 18 months. This is just not a big market for new single-family houses that would expand the urban sprawl further.

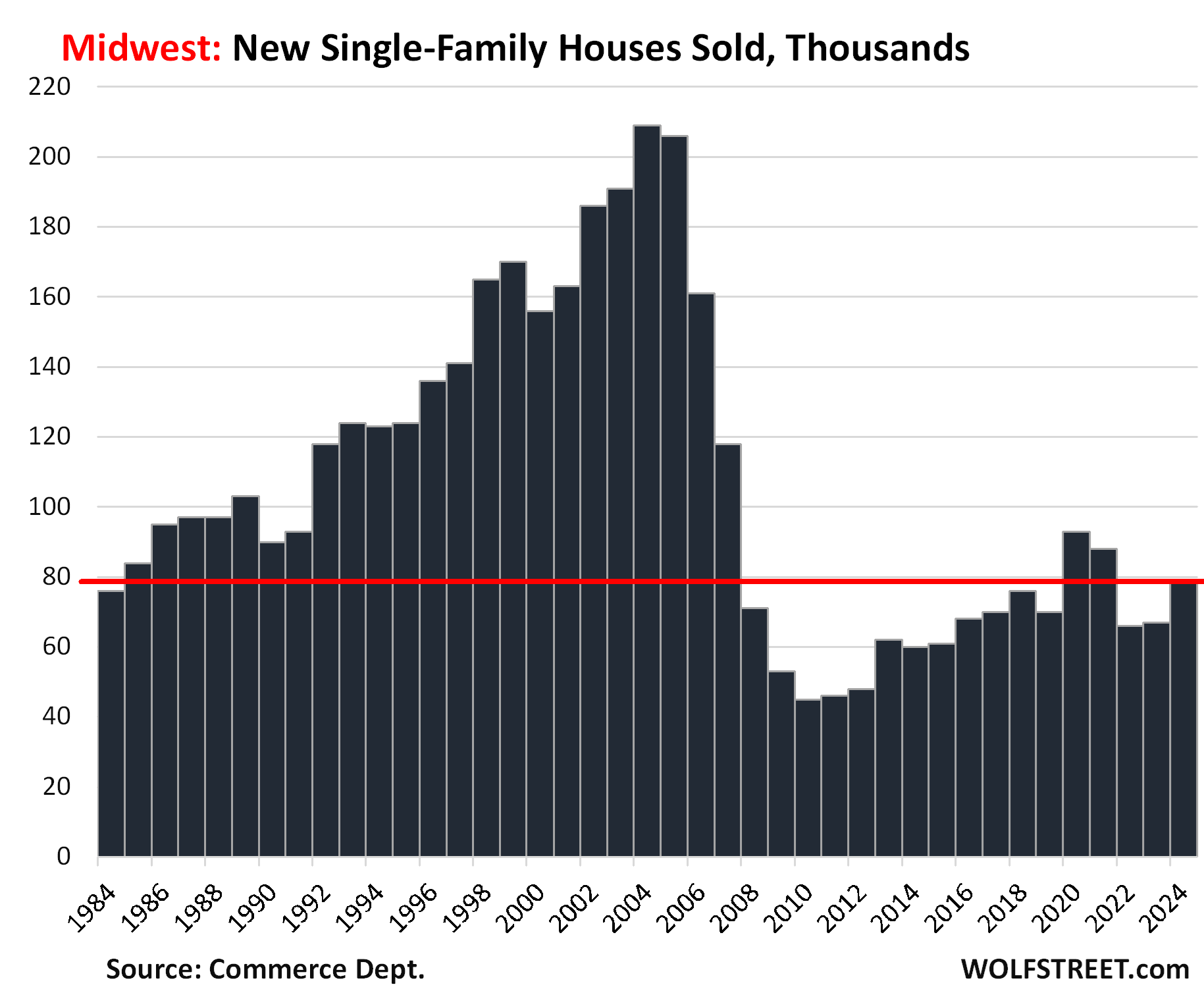

In the Midwest, sales of single-family houses in 2024 rose to 79,000:

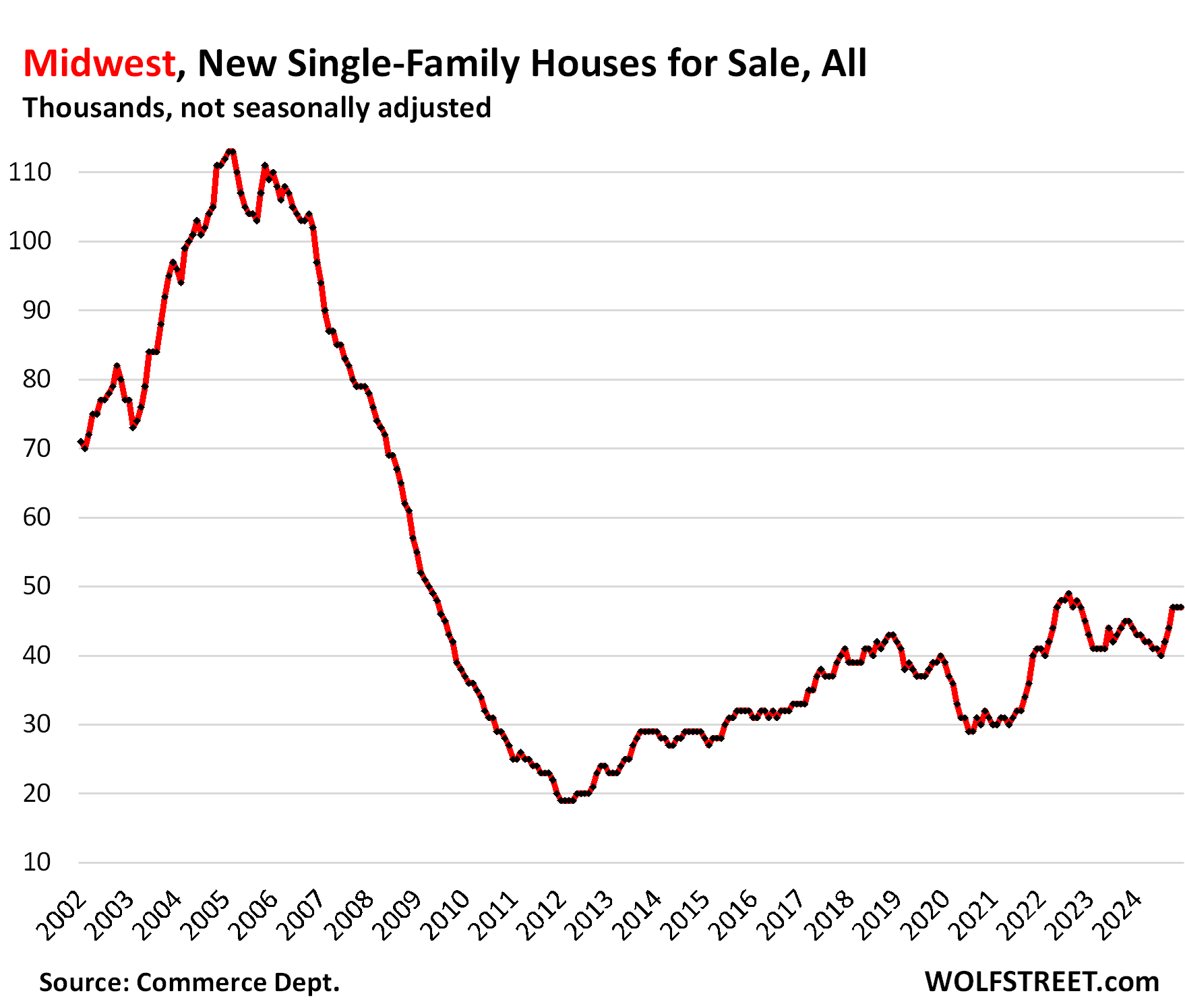

Inventory in the Midwest, at 47,000 houses over the past three months, is at the highest level since late 2022, and beyond that at the highest level since 2009. Supply exceeds 9 months on a three-month average basis.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Too bad when it comes to the West it kind of doesn’t apply to places like Irvine or Ladera Ranch. Price is still insanely bonkers and people are still buying left and right (although less than 2022 mania). Holding out for hopes in any of the desirable SoCal markets for a decent correction feels like a fool’s errand and maybe just a pipe dream.

On the flipside, at least I don’t have to worry about the rise of homeowner insurance that will likely come soon, and it will probably be more substantial than anyone budget for, especially those that bought at a high price, betting on refinance soon or living cost will stay relatively flat…

IN so cal, what would break the market is cost to insure homes!!

I saw a scene in a Netflix show recently. The protagonist (who’s kinda an antagonist… anyway) knocks on a door in LA.. they are doing an above shot of basically Altadena or the Palllisades and that whole neighborhood he’s in, is freaking burnt to the ground now!

Pretty crazy!

I mean we all complain about flooding, earthquakes, hurricanes, snow, rain… but it’s like “go! Or you’ll be burnt to death, extra crispy! Oh yeah and no one may ever even find your body.”

Like that’s pretty much the worst thing right?

Even if you’re burnt a bit, you might die of the infections while you try to heal.

Drowning is pretty bad too or having a building fall on you…

Well anyway, happy evening everyone. 😃 🌙

Well, the eye of hurricane Milton went right over us, so we got the front and back of the eye wall. Ground readings showed 100 mph wind in our neighborhood. The notion that those kind of winds in LA were pushing fire instead of rain is mind boggling.

Phoenix, there are a lot of people like you waiting for those same conditions to buy in those places. I’m guessing that’s installing a solid floor on prices….for now. During the big one (no, not WWII, the GFC!), I had been waiting for the same in Southern Marin. The crash came and went, and Marin barely budged. Immensely frustrating to be right and yet it didn’t matter.

Sold my loft in San Francisco’s WSOMA in Sept 2021 and relocated out of state. That loft has lost $200k since then. My SW Oregon property has appreciated only abit, but importantly held its own. But a house is not an investment, its a home and thats how I rationalize it…but sure glad I got out of SF when I did. South of Market is a war zone and I lived at ground zero

Oh but when you rent you are still paying for the insurance– although maybe if you rent MF the insurnace rates are lower?

Renter insurance vs Homeowner insurance rates are night and day even before this type of event. You can argue that maybe the landlord will try to pass on the increase homeowner premium to the renter, which is a valid to a certain extend but if you homeowner insurance jumps from $3k a year to $12k a year, it will be pretty tough to past all that to the renter, not that they won’t try…

“if you homeowner insurance jumps from $3k a year to $12k a year, it will be pretty tough to past all that to the renter”

But if every landlord’s insurance is going up by the same amount…

In the South – the largest region, with a population of 133 million, see map below – has the most inventory of new houses ever, surpassing even the astronomical levels on the eve of the Housing Bust, just before it all fell apart.

There is a change underway. People seem to be migrating from the older fantasy land which used to be Florida or LA. Since the physical injuries inflicted by the hurricanes and the fires on the people that experienced them, it makes sense.

Move in-land, where they don’t experience the catastrophic weather that occurs where it’s happening.

“Move in-land, where they don’t experience the catastrophic weather..” like the mountains of North Carolina?

Prices will come down. Rates will not drop much over the next few years. The economy will slightly worsen. Like you said, insurance rates will go up significantly soon, they have to

I would imagine that recent increased listings of existing/used homes in the south helps add on to the glut of new stuff for sale thus requiring even more enticements for new build sales. Article today in several Cdn news feeds on snowbirds bailing from Florida and Arizona. Weak cdn dollar and skyrocketing insurance and HOA fees prompting the moves. One owner quoted that between insurance increases, taxes, and maintenance it costs her $20K per year to keep a home in Florida. Agents quoted as saying they are very busy with new listings on properties owned by snowbirds. The gist of the article was the rush to list and sell is just beginning, but that so far it is not political. People are trying to sell while there are still buyers.

The Arizona realtor says this:

“Lavine said he’ll be handling eight listings — all Canadian-owned — in the next few weeks, twice his typical load.

Nor is the departure strictly from stationary homes.

“The RV park that we’re in is normally full of Canadians and Americans from cold weather places,” he said from the Phoenix area. “This year it’s down 30 per cent.”

Thanks for that! I hadn’t heard about it. I know the specific communities in AZ that would be affected. Canadians and older retired sellers (or estates) keep prices from moving too high in the places away from employment hubs.

I wonder what the average hold time is on the properties, a few years or decades.

I live in a Condo here in AZ and keep a close eye on my neighborhood. I have noticed an uptick in listings. But it’s a pretty desirable area, so units that are listed reasonably still sell in a couple weeks. Of course there are still dreamers looking for a bag holder, but those listings just keep aging on the market.

I think that the current housing market is irrational, a feat I may add is impossible for AI. So we can be confident that this cluster____ is not the result of an insane AI.

The new home inventory is important to median prices…but the existing SFH “for sale” inventory may be more important and I’m pretty sure that Wolf’s charts are still showing that those numbers are well below 2018/2019 levels.

Nope. We’re talking the South here, not the US overall. So for example in Florida, active listings of existing homes have been at record highs for the past months compared to the same month in prior years, in the data from Realtor.com which goes back to 2016 (fat red line in the chart below):

Do you have similar inventory charts for CA, NY, TX, and IL?

Sure. i already posted TX some time ago in an article (but not that many people read it). Also highest in the data, first chart:

https://wolfstreet.com/2024/11/05/inventory-of-existing-homes-in-texas-balloons-to-highest-in-many-years-prices-drift-lower-but-are-still-way-too-high/

Wolf, do these stats include “Legacy Condos?” Owners have waived reserves and kicked the can down the road for 30, 40, 50, and 60 years. They all now need rebar replacement/remediation, new stucco, and new roofs for insurance if you can get it. Massive revaluations are coming. Buying one is opaque. You can learn more about the stability of a $10 stock buy on HOOD, or a $9k car on CarFax than you can on an $850k condo!

The metrics that include condos include ALL condos.

Something is going to have to break the stalemate between buyers and sellers who are both on strike.

Only sellers can break the stalemate. Assuming rates don’t return to sub 3%, which they wont.

Right? Buyers can just put their wallets away. They don’t HAVE to buy, they buy when the numbers work for them.

If you have to sell, though, the buyer has the upper hand now.

Well, new build inventory (at lower prices) can *slowly* break the jam.

Anything that adds supply weakens seller strength – that is why so many people are pissed about needlessly restrictive zoning – it artificially lowers supply, greatly favoring incumbent owners.

I know many here think this is a frozen market, a statement. It’s not. Sales are still 70% of whatever of normal. That’s still a lot of homes trading hands.

Think of it like a levee in New Orleans during a 500 year torrential downpour. The pressure of the increased volume (homes for sale) piling up against the levee builds and builds all the while everything seems unchanged on the other side of the levee….. until the pressure causes a catastrophic failure and the dam bursts. Thats our housing market right now.

Jason, I appreciate the imagery of the analogy, but I’m not convinced that the physical phenomena of fluid & soil mechanics also apply to the economics of the housing market. For all we know, there could be a crew (e.g., the Fed, NAR) sourcing and applying fill to increase the capacity of the levee, and strengthen it.

There might be no burst. Doesn’t mean it’s not a failure though…someone, somehow, is paying for all that fill being sourced and applied. And someone’s making a pretty penny off of it.

I like your analogy. Cheers.

NAR coming to the rescue by fixing the housing levee?? That’s hilarious – it was difficult for me to stop laughing. The NAR is probably shi**ing their pants right now realizing that they and all their real-tores are going to be homeless bums in the soup lines before long. Yeah, they’re putting silly putty in the massive hole in Hoover Dam.

Well, as some would suggest that there has never been so many asset value bubbles inflated at the same time, when the sudden or slow leak deflation of asset prices could cause an economic deflation. I think that may be America’s future for the next decade.

Someone has too pay for the party. Obviously, the kids who have been saddled with the cost of the grand giveaways, the legacy of the Trump tax cuts, are pissed, Not enough to divert them from whatever their doing, however.

While I know inventory levels for new homes are higher in the SE, keep in mind the Natinal HBs have almost zero net debt. This compares to 50 to 60% debt levels in 2008. Plus they are trying to maintain 20%+ profit margins. They will be okay.

North of Houston where I am, builders are going bonkers building small, inexpensive homes. All new builds are discounted about 10% from last summer’s prices with a two year mortgage rate buy-down. Sold signs are popping up all over the place.

Welcome to Texas…tie your horse and check your gun!

“builders are going bonkers building small, inexpensive homes”

Thank God for LGI – one of maybe 5% of large SFH builders who didn’t use ZIRP as rocket fuel to rape and pillage via doubled pricing.

Somehow they managed the “Impossible” task of cost-effective construction.

Who is LGI?

Lgihomes – google it

Along these lines, I think it is a fair question to ask why the hell “build” “non-profits” like Habitat for Humanity have been (as far as I have been able to discover) completely MIA in terms of using internet technology to at least *aid* in restraining housing costs.

It is wonderful that they build and add supply (as much as their surprisingly large financial resources and industry connections might permit is another question…) but a long, long, *lonnnnngggg* time ago they could have put online model take-off sheets (for their own builds!!) that would help educate/empower Americans to haggle with SFH sellers/contractors on material costs and at least contemplate owner-construction in the face of Builder price doubling/tripling (Powered by ZIRP).

They had all the necessary info (to build the houses they did, they had to have plans, take-offs, etc.) but for whatever reason H4H never saw fit to share that info online (very rarely, I’ve seen local H4H organizations sort of inadvertently disclose pretty limited info along these lines – but the H4H mothership – which is a very well funded non-profit – has never remotely done anything like this).

One would would think that the Texans are kicking ass and taking names. Small is not the claim that was promoted, big old Texas.

Hey bud, not sure how, but would you mind factoring the population raise from 2006ish.

Hey bud, not sure how, but would you mind reading the article? “Months Supply” is a ratio that factors in sales and inventory. Population doesn’t matter, they could be renters for all we know; sales do because sales are a reflection of demand.

That’s some chutzpah calling Wolf “bud.” I shuddered.

bud lite?

Here in 11570 it’s “To Da Moon”.

Yes I’m seeing new buildings going in all around me in Florida, no one is slowing down at all. I think if people want a house they can pay the asking price, keep paying overpriced apartment rent, or live with mom. That’s what happens when the currency tanks, everyone gets poorer.

Hehe wait til 2030!

Your 2019 salary will look like a million 💵

Collectively, millennials are now worth about $15.95 trillion, up from $3.94 trillion five years earlier, according to Federal Reserve data.

Largely driven by real estate gains, the “median wealth of these younger people more than quadrupled” during this three-year period, the report said.

However, homeownership does not offer the same sort of safety cushion other investments do, noted Michael Liersch, head of advice and planning at Wells Fargo.

“Unless you are willing to downsize, you are really not going to monetize the increase in that asset,

isn’t that a good thing? more building means more supply, which means lower prices, eventually.

It can be a good thing, but speaking anecdotally, even if I could get a newer house with more square feet cheaper, I don’t want to be 45+ minutes outside of Tampa metro. I’m not looking for the white picket fence lifestyle, and my friends (albeit without kids of their own too) feel the same. I suspect existing home prices will be stickier and higher for longer. Can’t remodel one’s home location.

Cities attitudes will change. Smaller lots, duplexes, and manufactured would help. It took two years to get a small local town to allow a nearly 2 acre lot to be split up after I dozed a 1900s mega dump that nobody wanted.

Current owners are the root of the problem in many areas. Another mega dump sits beside my dozed lot. It has been for sale for years with no budge in price. R told me ther are just too damn old and rich to care. Kids will sell in a flash and eight nice small homes would easily fit an fifteen minutes from downtown. Don’t hold your breath as it will take years for people to wake up.

This is the biggest issue I see. My town has average 172 days on market. These old owners would rather watch a property deteriorate than give a young man a chance.

StrongTowns.org talks about the long term economic impacts of suburban development that are bankrupting cities and the benefits of traditional, incremental development.

Property taxes based on inflated valuation is inflation which is increasing at the reported rate of inflation increasing the cost of ownership.

A common tactic for assuming the value of poor peoples property is too raise the property taxes

Old houses – at least any that are halfway decent – should not be torn down.

One can buy a soulless stick-and-plywood craphole anywhere in the States, but old houses are finite, as are many of their locations.

Your town must be dying if no one wants a big old house. People would die for them in a thriving town.

Canadians fleeing Florida due to the costs. Insurance up by a factor of 3. Canadian dollar is tanking. Condo fees doubled in the past year.

There is a good article here quoting US real estate agents with double or triple the listings due to Canadians leaving. Same thing happening in Arizona. Snowbirds are abandoning the US

https://www.ctvnews.ca/business/article/people-are-panicking-snowbirds-rush-to-sell-florida-homes-as-loonie-tanks/

They need to aim lower!

Like any country below Mexico.

Sure safety isn’t great, but sure is more affordable.

Or, hell, in a lot of instances, just go to the next metro (or, god forbid…town) 50 to 100 miles north. The US is *huge* and mostly empty – these re prices frenzies occur because everybody insists on absolutely optimal siting.

Tampa is cheaper than Miami and Jacksonville is cheaper than Tampa.

Augusta is cheaper than all of them. (Ie save a fortune by going inland a bit…the Beach is like Broadway, you ain’t going to visiting it every day in real life, so why pay double the price for unutilized privilege?)

10 minutes on Google maps should gut sunbird monomania.

And you know when the township hits double digit in population…a dollar general will be built.

Tom,

That is a feature not a bug – the most common slam against smaller towns is the hassle of shopping (ie required driving). Every new Dollar General undercuts that objection.

The larger point is that moving even just 10 to 30 miles away from the “hottest” retiree metros can save large amounts of money (because the blind “gotta have it/gotta have it now” frenzy is what spikes prices).

If buyers would just take a compass and draw a circle around the “gotta have it” mkt, they would find out there are a *lot* of almost as good options for a lot less cost.

(See also, Austin where a 70% cost savings advantage got piddled away to a 30%-40% cost savings because incoming tech companies insisted on all moving into 1 or 2 tiny 1 sq mi “hot areas” while surrounded by dozens/hundreds of miles of much cheaper options. If you built a 50 story skyscraper in Austin (now 65% empty), you were a coastal fixated idiot)

It’s not just an attraction to metro areas in general, people of a certain age need reasonable drive times to doctors and hospitals. They don’t put those out where there’s no one to serve, they put them near population centers.

That’s a question we ask as we’re looking, what’s the ambulance response and drive time look like?

Sandy,

That’s a fair point – but brand new medical centers tend to get put on the *perimeter* of existing metros rather than the mostly built out, more expensive urban cores (where traffic would hamper response times anyway).

Still, medical access has to be taken into account for retirees – that is a reasonable enough consideration.

So maybe 10-15 miles out from a metro perimeter rather than 60+. And moderately in-land (vs. coastal) metros have medical centers as well.

Bottom line, there are a lot of options that aren’t Miami/WPB expensive.

In Florida, the further north you go, the further south you get.

And that is for real.

You all are getting too smart. All you need is a Walmart Supercenter and a hospital. Then be within a 100 miles of a big city for entertainment. Ardmore, Ok is a good example, 100 miles between Dallas TX and Oklahoma City both directions. No, I’ve never lived in Oklahoma, but these are the kind of places I scope out. Kingman, Az if you like the heat. Vegas, California, Phoenix right there..

are you thinking Panama, Costa Rica, Nicaragua, Guatemala, Belize, Columbia, Ecuador, Peru, or Uruguay? You wouldn’t necessarily be unsafe – as long as you don’t make a spectacle of yourself.

There are plenty of hotspots for expats (we’ve been exploring those as well) that offer lower cost of living with excellent medical care.

One thing I think doesn’t get discussed enough it the growing world-wide opposition to migration, it’s happening in almost every country as people relocate for a better standard of living. So, if you are considering a off continent move, look at what’s going on politically very closely.

This will get worse as certain resources become more scarce as scarcity brings out the worst in people.

/sarc

There could be a lot of empty house in Mexico and South America from all the people migration the past 4 or 5 years? lol

True. But Guantanamo Bay is filling up quickly, gotta catch a flight soon or be priced out forever.

I see a bearish flag in the data. While prices may move sideways, I will maintain my position until they decline. The focus is on affordability amid the uncertainty in the employment market. I plan to wait out the decline before making any commitments. Assets are dropping. Buy the dip?

as someone else posted yesterday, not until the stock bubble pops. as long as every drop in stocks like nvidia is seen as a buying opportunity, the housing market will largely follow.

Thank you, Franz G. I missed the mention from yesterday, so I will go back and read it. I often post a lot of unrelated content since I’m not a finance expert, but I will keep an eye on the obvious topic: NVIDIA. I appreciate the insights and narratives shared by everyone. Much respect!

Florida is just one hurricane, like hurricane Andrew in 1992, away from a complete Real Estate meltdown. That hurricane hit just south of the major population center of Miami, when it turned south at the last minute, and hit in a relatively poor undeveloped part of South Florida, where there were mostly cheap homes and little commercial infrastructure. Every home in it’s path was destroyed. The next time Florida may not be so lucky. I would not buy a property down there with this risk hanging over your investment.

Why would a major subtraction of housing stock melt the market down? Could be like LA, where prices are rising (and will rise a lot more, likely, from this increased shortage).

The Florida Building Code was enacted after Andrew. Hurricanes will continue to wipe away crap built in the 70s and 80s, but anything built after 2000 has stood up well to hurricanes. Roof decking is all tied to foundations, you are losing shingles but not your roof decking in a hurricane now, Andrew wiped so many houses away because once your roof deck is compromised, the winds rip apart the entire home.

I visit Andrew area maybe 8 weeks after the storm. That was my ‘wow, TV can not do this justice at all.’ moment. It can’t. One has to be there to really understand how vast the damage is.

They setup drive through permitting which I thought was good.

Agree. I’ve been through Irma, Ian and Milton on the west coast. Not to minimize what people went through in the flood zones, but if you’re house is up to modern code, the winds were just not a problem as long as your hurricane shutters were up or you had impact glass. Definitely don’t buy a house in flood zone A unless it’s a second house.

The wind blew a cigarette butt can into the pool. Does that count.,

Insurance companies defrauded homeowners after the hurricanes in Florida and elsewhere. If the damage was cause by wind they said it was caused by the storm surge. If they had flood insurance, they said it didn’t cover storm surge, and said it was caused by the wind. No matter what they had the insurance companies didn’t cover it. If they were covered then the insurance companies didn’t have the money to pay out all the claims or paid some of them and pulled out of the State, or stayed and raised the rates on everyone else left there.

Too bad we can’t get all those razed forests back.

They’ll grow back on their own. Just leave them alone for a while.

In the south, there are >10x more new homes being sold than the northeast. But are there 10x as many people Perhaps that’s why prices are so stubborn here.

Tomorrow we’re getting snow and then a flash freeze in Boston. Wouldn’t you rather live in the south?

Not sure how I missed the question mark at the end of the second line there…

There are not 10x as many people in the South as in the Northeast. There are 133 million people in the South and 58 million people in the Northeast. so that’s about 2.3 times as many, not 10x as many.

And yes, prices are stubborn but they’re coming down in the South, I’ve already shown you the charts of existing-home prices of the Texas cities, with Austin prices having dropped about 20% from mid-2022, and with Tampa down about 10%.

“Tomorrow we’re getting snow and then a flash freeze in Boston. Wouldn’t you rather live in the south?”

Spend an August in Florida. You can always put more clothes on in Boston and get out and have some fun. You can’t keep taking clothes off in Florida.

I lived in new england for 38 years and now 10+ in FL. You can shift your time of day in the summer and still get great temps in FL (until 10 am and after 6 pm). If you shift your time of day in January in Boston, you’re still freezing. Drive around at 7 am or 7 pm and see all the athletic activity – runners, golfers, etc – in the summer. Plus, there are pools and air conditioning. I actually like the summer. If I had to give up January in FL or August in FL, I would give up January (we were freezing last week!).

My comment was somewhat tongue-in-cheek. I wish more folks would consider moving to southern cities that seem to have considerably more available housing inventory per capita. Boston is already too crowded and there’s nowhere to build…

August 1, 2025 headline:

“FLORIDA MAN ARRESTED FOR INDECENT EXPOSURE

Reporting from Jacksonville, man intended to make a politically motivated statement indicating that Florida is better to live in than Massachusetts, saying ‘People up north have their heads stuck in the snow…they say summers down south are too oppressive. You just gotta shed layers like I do. Hang in the shade and spritz some water every once in a while and you’re fine.’ When asked about potentially facing prison time, the man said ‘We also don’t have an oppressive government like they do up north. Watch, my case will show ya.’”

Jokes aside, it is kind of a Wild West feel down here that I like. Summers do suck but I don’t miss the biting cold. Just skiing. To each their own.

Respectfully.

Hah, they have a different kind of oppressive government — not to mention nearly every new build comes with an oppressive HOA.

Choose your poison.

I had a coworker during the last Lesser Housing Bubble. She and her husband bought a brand spanking new home for about $540K. I’m sure it was a nice home, but problem being it was in a crappy, secluded town with almost no jobs. Nearest town with good jobs was 35 to 40 minutes away. Then the bust came!

She walked into work one day, and said, “Larry, I don’t think our house is even worth $200K!” They made their payments for a while longer until her husband who worked in finance got laid off. Then they decided it was game over.

It was called ‘jingle mail’ — placing your keys in the mail box to send them back to the bank.

A lot of people were furious when they lost their homes during the last bust. I heard a few stories of people gutting the homes they lost – taking all light fixtures, cabinets, water faucets – anything they could. In another instance, I was shown a home that was a bi-level home. The people who lost this home turned on an upstairs faucet, closed the drain, and let the lower level flood. Oh, how sweet, the American dream!

Thanks Wolf! Very timely as I am in the south and looking to expand my rentals. Prices are definitely coming down. Just looked at a three bedroom, three bath for $220,000. Needs paint, but that’s it. HOA is less than $200 per month. I can get $700-800 per room in rent easy, so we are getting back into a zone where adding another investment property may make sense. Many other properties are still too high, but we are definitely getting back into reasonable territory.

The surplus of new houses for sale in the South surpassing levels seen during the housing bust is a clear indicator of shifting market dynamics. While it reflects overconstruction or slowed demand in certain areas, it also opens opportunities for buyers seeking better deals. Similarly, the near-glut in the West underscores the need for better market balance, with potential lessons to be learned about sustainable development and aligning housing supply with regional demand.

Wolf, you mention sfh in the north east and expanding the urban sprawl further. My experience here is the sfh construction is tear downs, which has no impact on the sprawl at all. Are those not included in the figures?

The current preference seems to be to tear down an sfh and put a couple of townhouses in its place. Or (less often but still common) to refurb an old sfh into a 2-3 unit mfh. How are those counted?

Good question. Definitely a lot of this happen here. Old sfh homes being replaced with duplexes and quads.

Tearing down a SFH and replacing it with another SFH doesn’t add to the supply. It’s good for GDP but doesn’t add housing. It’s like a big remodeling job.

Tearing down a SFH and replacing it with multifamily, or with a bunch of townhouses on the same property… that adds to supply. So if you tear down 1 house on a big property and build 8 townhouses on the same property, you added 7 homes to the supply.

Understood, I’m just wondering if tear downs are included in the “new single family houses for sale” in the article, assuming a single family house is built, and also whether townhouse units are considered single family houses.

Winter in Phoenix – finally got some rain. There are open houses and lots of cars in front of them. Houses are still selling. It’s going to be a slow grind of price/time until everything is in balance again. Mortgages aren’t going under 6.5 for a long time. Each individual house will change hands at exactly the right number for that buyer and that seller. It may be $550 today, or $525 today, or maybe $545 in a year, or $585 in three years. Or sure – maybe things will crash and it will be $385 in three years..but are you willing to rent and wait to find out? Some people will I suppose.

Rent prices are dropping all over the southwest/mountain west. Here in Denver we got a 5.4% yoy decrease in rent prices as of December. This typically is a leading indicator of a bust.

Rent is already significantly below the cost of a mortgage and now it’s going down further. There’s 4 thing propping up the housing market currently:

1. FOMO crowd that watched housing prices runup over the last decade due to artificially low interest rates. They’ve gotta buy before prices double again (I hear this a lot out of people in their early 30s)

2. Airbnb’s distorting local markets – as travel continues to return to more normal levels booking and nightly rates will drop and as the costs of operating goes up these should start to end up back on the market

3. Buy downs – no one’s paying sticker price and thus comps and median prices are artificially high

4. Vacant properties

“FOMO crowd that watched housing prices runup over the last decade due to artificially low interest rates. They’ve gotta buy before prices double again (I hear this a lot out of people in their early 30s)”

Sadly FOMO doesn’t seem to ever subside in our society until perhaps external factor force the FOMO peeps from spending.. you see that with other stuff too. Right now there are lines of people camping out Microcenter waiting for a 5090 video that will cost $2k to $2.7K a pop and people are lining up as if this is food ration. This is one example of people’s willingness to buy no matter what as long as they think they still have the means

No kidding Phoenix_Ikki. There is plenty of money still sloshing around in the U.S.

Restaurant stocks are on a tear today. EAT (Chilli’s) blew away earnings and of course a bunch of other restuarant stocks took off too. People are eating out a lot I guess.

IN my hood, if you buy a home, your monthly outlay is 12K plus, if you rent the same home, it is ~$6K / month.

It’s a no brainer to rent and wait as prices are falling albeit slowly.

That new build chart in the Northeast is the problem here. Anemic new builds numbers since 2006.

Everytime a new build project here comes up, the NIMBYs come out of the woodwork.

But sales are even slower, and months supply is the highest in the nation.

What about exisiting homes in the NE? Whats that months supply?

Where do you propose they build more homes? Bulldoze the state forests and wildlife sanctuaries?

Maybe they could build homes out at sea, like Stiltville in FL.

We had two projects come up in town.. small townhouse projects maybe 12 each time.. and both were knocked down because of “Character” Also a apartment complex that was fought tooth and nail.. like 50 units. Still being fought.

“both were knocked down because of “Character””

That is pretty stupid.

@ShortTLT

It’s totally dumb, the towns current density is 850/sq mi. For example Dedham has a density of 2150/sq mi and Wellseley has 2900/sq mi.

My understanding is that only small home builders built spec houses and they do great in market booms and go bankrupt in market busts.

So I am really surprised there is that much inventory of new homes.

I was under the impression the big guys do not build spec houses.

Is the inventory ballooning because new home buyers are backing out of contracts with the large builders?

In my little slice of flyover

GFC ended spec homes.

Starting around 2020 BnB

Became the craze. That has now cratered in my area.

The multi family developments are now in the process of grinding to a halt.

Keep building. We have 8 years to remove from the average age of first time home buyers to get us back to where we were.

If a 30 year old cant afford a home, we need to build more.

The next recession will solve all these over-priced housing problems, the stock market bubble, and general inflation problems. Don’t worry, there will always be another recession. Of course we don’t know when it will occur, but it will happen.

We are betting on within the next two years. Mr. Market hates instability and this administration is serving up a lot of it, making the house of cards even more precarious. Luckily, once we sell we can rent for as long as we need to.

Sorry but the recession has been forever canceled as we have seen so many “predictions” fail miserably in the last couple of years. Tough pills to swallow for the bears but maybe this is the new paradigm and this time is different..

Couple with the threat from the top guy on gunning after interest rates cut and more juicing of the market, any inflation be damn…Yeah I know that supposedly Fed Chair can’t be fired but his term is up soon enough and also I get the feeling that rules and law aren’t as much of a showstopper as they once were…

If you read my comment, I was not predicting when we would have a recession, only that we will have one.

Long time reader. First time commenting. I know everyone likes a good real estate story and this may be common but when it happens in your family it is different. My Aunt passed away a year ago and lived in Raleigh NC. She bought a ranch house in the 70’s for around 55k inside the beltway. House was put on market for 900k. The house was sold for the lot because the builder that bought it was going to demolish the house and build one for his family. (So he said) After he bought it, his wife (So he said) decided she did not want to move. Builder sold house to another builder for 1,350k with in a month. The executor in charge of the estate trusted a real estate friend of my Aunt’s when trying to price the house/lot. I think the executor got taken advantage of. There is probably a lesson to be learned from this story.

Home prices are not too high! Median household incomes are too low. Since 2001, rents have gone up ten times faster than renters incomes. Between 1985 and 2022, median home prices have gone up by 423 percent, while the median household income went up by 216 percent. This is why Generation X is not happy. End the Fed!

I disagree – home prices are indeed too high.

If incomes go up, the prices of everything *else* will go up too. You still need to afford food while saving up for that down payment.

They have to move inventory with all those hard costs already in the ground in their subdivisions…discounts will become larger and passed on to their finance arms, but those margins are shrinking rapidly…maybe breakeven soon with higher borrowing costs…

Hey Wolf, I am interested in better following along with the data. Your charts cite Commerce Dept. data – is that the same as the “newressales” excel on the census .gov website? If so and I am understanding correctly, then your first chart should be using the data in worksheet ‘Table 1 – Sold and For Sale’, Table 1B, For sale at end of period (South)? Thank you very much and interesting article. I’m sure the listings vary substantially at the state level too (FL vs. NC, for instance).

Nope. I should use no such thing. You can download all the data here from the Census Bureau’s interactive site that lets you choose time period, category of data (SAAR or actual), by state of construction, sales/sold, for sale, by region, etc:

https://www.census.gov/econ/currentdata/dbsearch?programCode=RESSALES

Wow, thank you!

I am very interested in the geographic differences in the housing market. This analysis is much appreciated. Pretty much read my mind after I read the last one. We made some money in 10-11 in central FL and have watched it ever since we sold. I evenly invested here in the Midwest and hold some of them still as long-term rentals. Huge differences in those markets.

How closely does the housing market follow supply and demand, can a strong correlation coefficient be derived?

My guess is it is less than 70% correlated… but somebody prove me wrong or wolf do your bs rant thing 😀