Waiting for even lower mortgage rates comes on top of all the big issues that crush demand in the housing market.

By Wolf Richter for WOLF STREET.

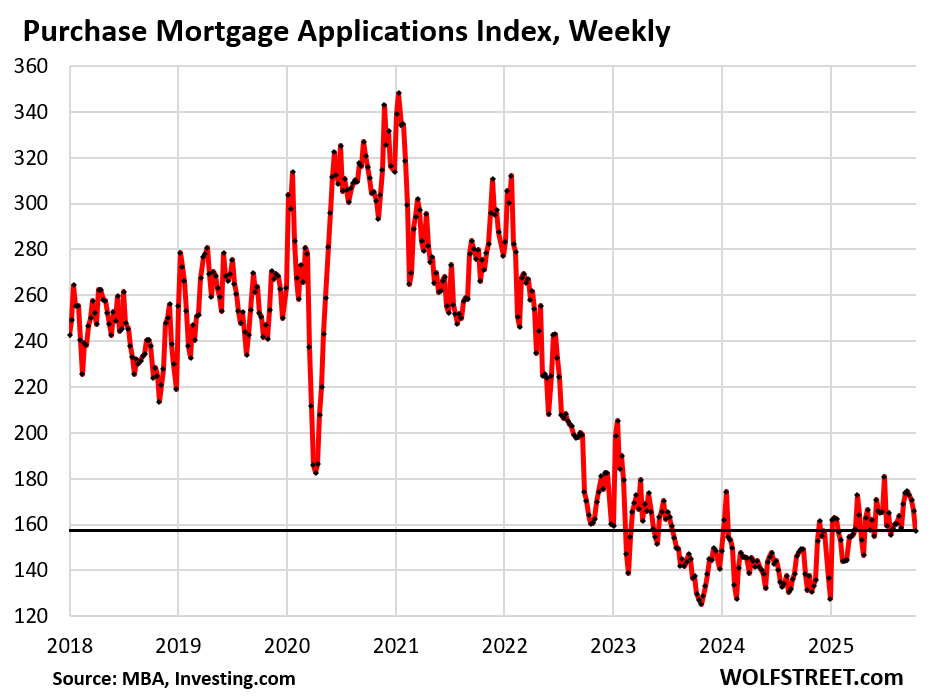

For the fourth week in a row, applications for mortgages to purchase a home fell, despite declining mortgage rates, and hit the lowest level since the week ended July 30, when mortgage rates were nearly 50 basis points higher. The much-ballyhooed idea that lower mortgage rates would unleash waves of demand is running into reality?

Demand by homebuyers began to plunge over three years ago and has been wobbling along very low levels ever since. Compared to the same week in 2019, purchase mortgage applications were down by 35%, according to data from the Mortgage Bankers Association today.

Applications for mortgages to purchase a home are an indicator of home sales in the near future.

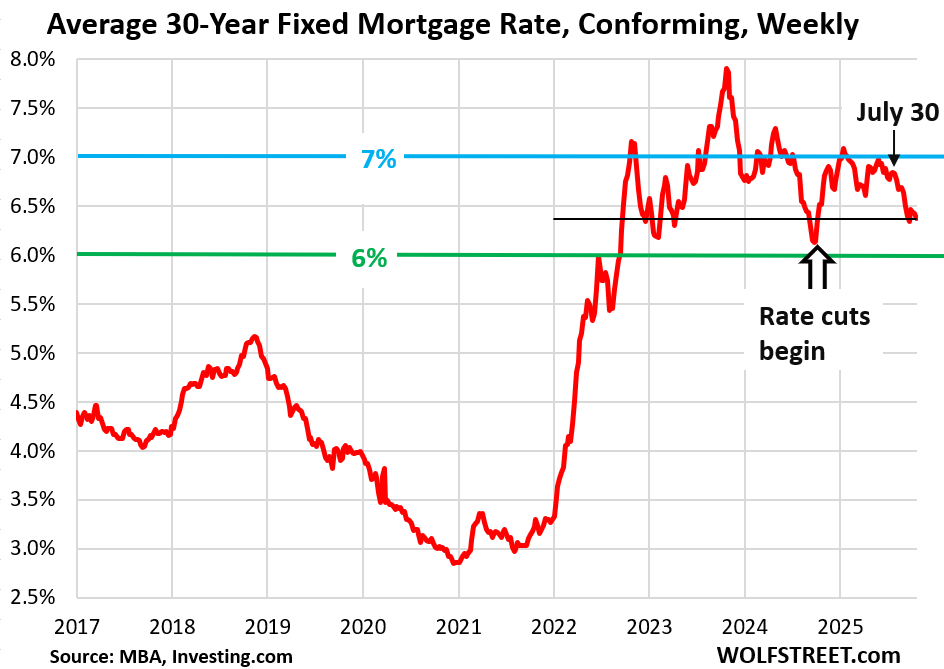

But the average weekly mortgage rate for conforming 30-year fixed mortgages declined to 6.37% in the latest week, according to the MBA today.

Since the reporting week ended July 30, mortgage rates have dropped by 46 basis points (from 6.83%); and since the end of May, by 61 basis points (from 6.98%). Yet mortgage applications are now lower than they were then.

Mortgage rates, according to this measure, bottomed out in September 2024 at 6.13%, just before the Fed started cutting interest rates.

Not so paradoxical. The phenomenon that already low demand for mortgages would decline further even though mortgage rates have fallen substantially is not so paradoxical.

Potential homebuyers – those not turned off by the too-high prices – see mortgage rates zigzagging lower, and they listen to the housing prophets promoting the notion that mortgage rates will fall further, and they add 2 and 2 together, and the first thing they do is wait for even lower mortgage rates.

Waiting for even lower mortgage rates comes on top of all the big issues that have crushed demand in the housing market – including way too high prices, though they have started to come down in many markets, and in some markets by a lot, for single-family homes and for condos and co-ops.

Waiting for mortgage rates to decline further is the opposite behavior of the FOMO-driven buying that had set in late 2021 and early 2022, when mortgage rates had started to rise from below 3%, as the Fed was making noises about rate hikes and tapering QE to deal with inflation, which had begun to rage.

Fear of rising mortgage rates at the time, and efforts by homebuyers to “lock in” the still low mortgage rates and buy before prices spiked even further, triggered a huge wave of demand and crazy FOMO-driven buying, which resulted in home prices exploding through the first half of 2022.

So now mortgage rates have fallen, and prices are falling in many markets, and people are waiting for still lower mortgage rates and still lower prices.

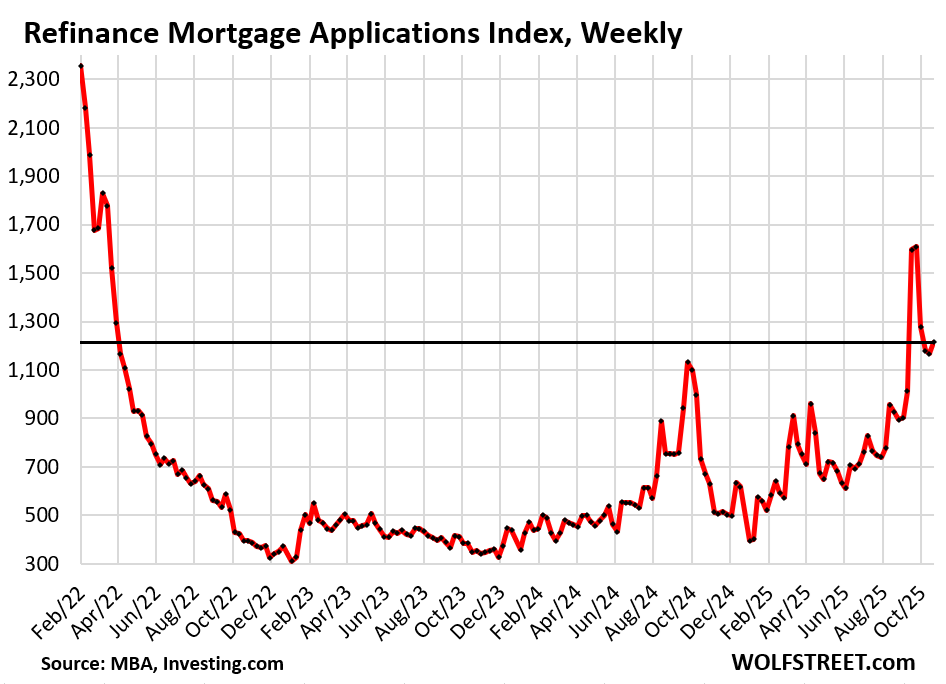

But the lower rates increased refis. Applications for mortgages to refinance an existing mortgage ticked up in the latest week, and for the past six weeks have been higher than any time since March 2022. But that spike last month took a lot of pent-up refi demand off the table, it seems.

The September 2024 spike in demand for refi mortgages occurred when the MBA’s measure of the 30-year fixed mortgage rate was even lower than today.

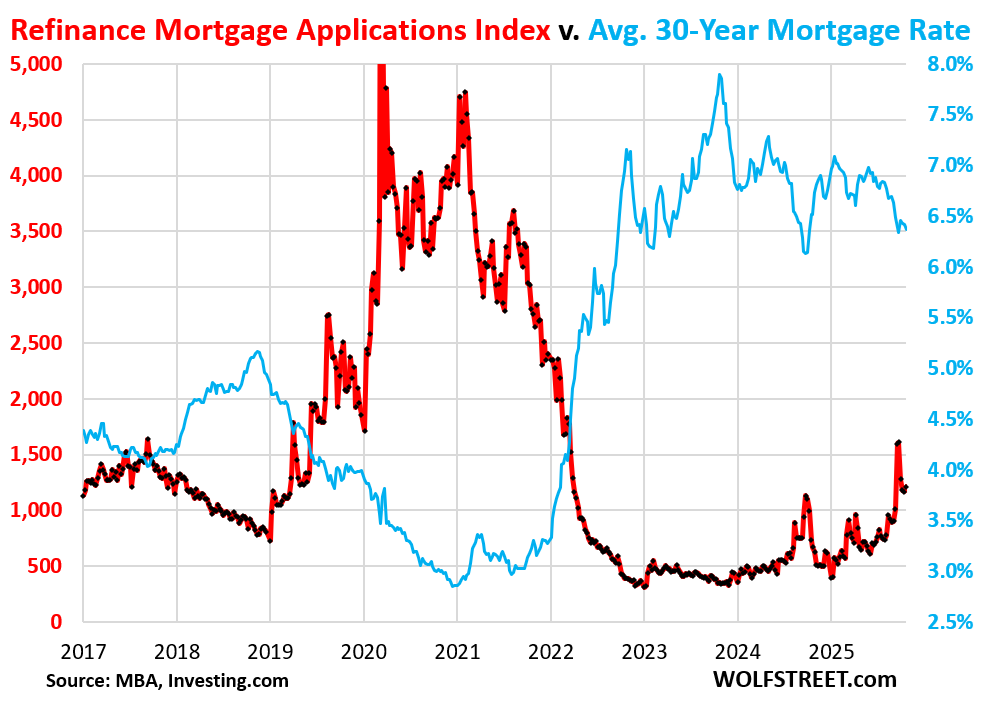

Refi mortgage applications (red in the chart below) rise when mortgage interest rates (blue) fall, and vice versa.

That spike of refi mortgage applications in September was small compared to the boom years of the 3% mortgages that everyone was trying to refinance into. But the current level of demand for refi mortgages is in the middle of the range of three years before the pandemic.

In case you missed it:

The 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September

And:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

ROFL…you mean my trusted RE agents and NAR has been lying to me about rate cuts = roaring FOMO demand? I am shocked…..

I am sure they will tell you when they say rate cut, they are thinking of less than 3% 30 yr fixed :/

Rates won’t cross below 5% for at least a decade (if ever). Good luck on your real estate investments. 🤭🥴

My neighbor took out a million dollars in a refi in 2022 and put it in the S and P. I think he has made a ton of money. Timing is everything.

Did he sell and cash out his gains?

+ and pay off that loan?

Is person using the yields or profits from their investment to pay down the loan or are they making their monthly payments using some other source of money?

Could it be that the rate of home sales will just remain depressed for a long period of time because of high prices + mortgage rates or what will force the market into further price declines? Does it have to be a recession?

There could be foreclosures and forced sales when the “interest rate buy downs” on the previous new builds run out and the rates reset to the current higher rates.

Regarding the spike in refinancings a few months back, doesn’t it confirm that some people are highly leveraged on their mortgage? There isn’t much benefit to refinancing your mortgage every .5% drop. The origination costs eat up most of the savings. It tells me some recent buyers in the 2021 to 2025 time-frame might be struggling to make payments and don’t have the luxury of waiting for larger rate drops to refinance.

@Bobber I have never actually originated a residential loan or worked for a residential lender (I was in commercial lending for a decade) but in the real estate lending world I have seen that more often than not people refinance to get cash than just to get a lower rate.

I did a refi in 2021 or whenever the rates went real low. I refied to a lower rate in house with the same credit union that the original loan was with.

Because it was in house, the only real cost was an appraisal for $800. They said it was just a technicality because they knew I owed about 1/4 of any appraisal value.

It was during covid and the appraiser only took 2 pics of the front of the house. He asked my wife to take all the pics of the sides and back and the inside. He then complained and asked my wife to reformat the pics several times, and then asked if we could write a description of what we told him he saw. I asked him if there would be any discount.

He said Covid, he was’nt working. (As he was on the job)…haha….

Ironically, I paid him $800 for two pics and an appraisal that was cut and paste exactly from all our work and an exact price that matched Zillow to the dollar.

Oh well. Paid him $800 to save over $30,000 in the long run.

Don’t trip over quarters, to save a nickel, and end up losing a dollar I guess.

So FOGS (Fear Of Getting Screwed) by interest rates dropping after committing to a mortgage is now a factor.

Personally, since refi is an option if interest rates plummet, I’d be more concerned as a buyer in many markets of overpaying for the house right now.

One market in the MidWest that I’m following still has lots of houses back on the market after having last sold in 2021 to 2023. Over many months they slowly drop the price with no takers — and are now at a price that means that the current owner is, after xaction costs (RE commissions, “spruce up” costs, loan fees, etc), underwater and still no takers (albeit they probably lived in or rented the place during the time they owned it so they may not actually be underwater when looking at the whole picture).

To a potential buyer, it feels a bit like trying to catch a falling knife if you don’t _need_ to buy.

I feel this right now. I am watching so many homes that are languishing on the market up here in Sacramento. Many homes aren’t selling because they are still too high. Others are selling but have many times come down 10-30% from the original list. Granted, the original list may have been in 2023 with the whole list/delist game. So when you actually look at the selling prices, they aren’t going for 15%+ under list. One home I have been following was bought by one of these appreciation LLCs in the 2021 era for 920k, rented for under 3 years with a listed rent between less than 3.2-3.9k a year, and then listed for sale for $1,455,000 in 2024 with almost no upgrades, but they did list the sqft as 350 sqft more than the last time it was sold (they were at least smart enough to include a “buyer to verify square footage” on the listing). The home has languished on and off since and is down to $1,350,000. Granted if they were actually able to sell it at that price, they would still do great, considering they bought it for 920k. But I think there’s a great chance that if someone were to buy it at that purchase price or even 50k, they would still be overpaying by about a 150k. This is just one example but there are many of these examples across the Sacramento and surrounding markets.

But, BUT: I just read an article about the coming housing BOOM!

It included all the facts: mortgage rates are way to high, and the boomer wealth is flowing into the pockets of the next generations, making for great down payments!

Be interesting what happens come this next Spring. If employment holds up and a 3-4 more 25;point cuts happen it could create some movement. Obviously too many variables to really predict anything at this point, especially as data is thinner to make those decisions.

If Employment holds up, why would we get 3/4 cuts? Then FED will be crushed with surging inflation. Its already 3%. Still they are cutting rates because they are worried Labor market has started deteriorating.

Sure FED can be pushed into cutting rates with more Trump-PRo governors. Even if FED rate cuts happens, long term rates including Mortgage rates will stay same or go higher. We have seen this story from Oct 2024. Even if QT stops, FED will not buy more MBS. This is accepted even by dovish Governors. So whoever is going buy MBS, they will expect higher spread to make sure they stay profitable and adjust their Interest rates risk.

So unless we see lot of Price corrections, not much will change in coming 12 months.

If person is is RE Business then YES!! Good Days are coming.. just around the corner.

Bond market will punish the Fed for cutting prematurely. Powell knows this.

well, of course demand drops in the fall after kids are back in school.

is the data or you know analysis adjusted for a seasonality?

It’s seasonally adjusted.

It’s down 35% from the same week in 2019, as I pointed out in the text.

Is there any data on how the NAR settlement that went into effect in mid 2024 had on seller/buyer agent commissions? Sales are down but there has still been a lot of transactions.

Hopefully people remember what rates were early to mid 2010’s and refuse to take these ridiculous current rates

They are not ridiculous. They are low normal rates. ZIRP era was an anomaly its time to wake up.

It’s not the rates but the prices and insurance costs. Sellers are still pushing that their house has appreciated 50-90% in 5 years and buyers are calling BS. When I bought in ’06 interest rates were 6.25% but prices were not through the roof as much as they are now. Insurance costs have also gone up 30-40 percent. It’s about the carrying costs for would be buyers and the reason the market is frozen is because the numbers don’t add up. At least here in the Bay Area where I am It’s cheaper to rent and wait this bubble out.

This is a bit akin to a ‘buyers strike’ as I see it, and for the right reasons, rates are traditionally in a normal range (but falling) and house prices are too high (and falling).

However, with the stress in the funding markets, we could see a not-qe qe pivot from the Fed soon and that will immediately flip the calculations:

Rates will be coming down sure, but prices will be doing up!

So it may not be bad to jump in, lock in that ‘low’ prices at a ‘high’ rate in the expectation that you can refi that rate down while the house appreciates…

I agree that future expectations of rates is having an influence on home buying. If rates are dropping, why by now if they will be lower tomorrow? Especially if there is a chance house prices will also be lower tomorrow? I think future expectations of house prices are also playing a small part in the drop of new mortgages applications.

However I think there are two bigger influences than either expectations of future mortgage rates and expectations of future house prices. I think economic security it one of the biggest influences in the drop of new mortgages. Consumer sentiment is down. While people are still spending because the culture among the last two generations of home buyers is more directed towards experiences than assets. So while people will gladly spend every last dollar they have in order to experience a nice trip or some other once in a lifetime experience, they are reluctant to make a 30 year commitment to having a large portion of their income go to a mortgage.

There is a huge difference between spending money on something that will leave them broke for a few days and spending money on something that will leave them broke for the next 30 years.

The 2nd important factor is the newer generations lack of commitment. The younger generations are less likely to get married or have kids. Both of which require commitment. Furthermore, their attitude towards jobs is different than those before them. Most recognize that jobs are just what they are doing now and probably will be very different a year or two from now. Everything is much more temporal to them now. They recognize that things will likely change.

Given that outlook, why would they want to sign on to a 30 commitment to live in the same place (or face huge frictional costs to move)?

My 28 year old nephew recently bought a house. He makes good money and can easily afford it. However so many if his peers (working at the same job making the same money he does) look at him like he signed on for a 30 year jail sentence. They look at renting as a positive. It provides easy mobility (i.e. less commitment). They can move around, try different lifestyles and live in different places. Why would they want to tie themselves down to living in one place?

It is a different attitude.

@JimL great post, things are changing with almost all my parents friends married by 30, close to half my friends married by 30 and not a single one of my friends kids married by 30 today.

That attitude isn’t different. I moved and changed employers many times and bought/sold houses every move. You can’t rely on one employer to pay/promote you and the way to the top the fastest is to be a free agent. Buying a house doesn’t tie you down to anything, being comfortable with your current job often does.

With people thinking that rates and prices will be lower tomorrow, and lower still thereafter, it’s the beginning of what could develop into housing depression psychology. A housing crash preceded Great Depression.

Buyers are waiting for rates to go down when they should be waiting for prices to go down.

Right action. Wrong reason.

It seems like rates are controlled by a small number of major institutions, while prices are controlled by a large number of individual owners.

Which of those is more likely to act in a rational, coordinated and publicly disclosed manner that produces the sort of predictable outcome that would draw buyers back into the market?

I would guess it’s the small number of institutions.

Buyer’s cost of entry is the product of Price and mortgage interest rate. And mortgage qualification is as well. Also price drops can be much more locale related, so certainly for first time buyer’s holding out from the market would be dominated by the product. That said, assuming the buyer can stay employed (a big question mark) , mortgages can be refinanced wheras purchase price can’t be renegotiated. So It is hard to argue that the job market does not factor into buyers decision, meaning this is a multi factor calculus and not just a single factor.

Yield is yield. If T Bills yield continue to drop then folks like me will cash out and shift directions.

I’m looking at a 5% 15 year w/ half point fee refi(offered to me this week). The great thing about the 15 year is that principal is rapidly paid off vs. a 30 year.

If you are waiting for home prices to decline you might have a long wait. Building costs are through the roof and so is labor. Add in a shortage of skilled trades and home inventory, I don’t see a drop anytime soon.

If interest drops, prices will climb as the pent up demand to get a home will bring the market back to life.

In case you missed it:

https://wolfstreet.com/2025/09/19/what-it-takes-to-sell-homes-lennar-cuts-average-selling-price-below-its-2019-level-and-its-home-sales-held-up/

The facts are opposite to your statements, except for building costs.

There’s a huge amount of inventory, the “not enough houses” is completely debunked. See Melody Wright (she has a substack). Currently 500k more sellers than buyers.

Look at data from 2006-2012, house prices vs interest rates. Just like we are seeing now, rates dropped and house prices dropped. Deflation occurs when people expect prices to go down, so they do…

Osbourne Effect

Waiting to buy a home when rates drop lower is a loser strategy and thought process. Marry the house and date the rate. Rates are currently in the low 6% range for a 30 year fixed mortgage. That’s below the historical average. Buy now lock in a fair price and you can always refinance if rates go lower. Also, typically when rates drop, home prices increase. Additionally, most new home builders are offering extremely low rates similar to post COVID, that can lower your monthly payment significantly, compared to an existing home at par rate.

People who buy now marry the high price of the house, and they marry the historically normal mortgage rate. They’re married to both. People have done this for two years, and they’re still married to both. They can never shed the high-price wife, that’s a lifer; it will always and forever be their cost basis. Maybe they can divorce the normal mortgage rate someday to something slightly lower, and maybe they can’t because mortgage rates over 6% are historically on the low end of normal, as you pointed out, and inflation is at 3% and has been heading higher, and that is what determines long-term bond yields over the long run, which is what determines mortgage rates.