The rise of the “non-traditional reserve currencies.”

By Wolf Richter for WOLF STREET.

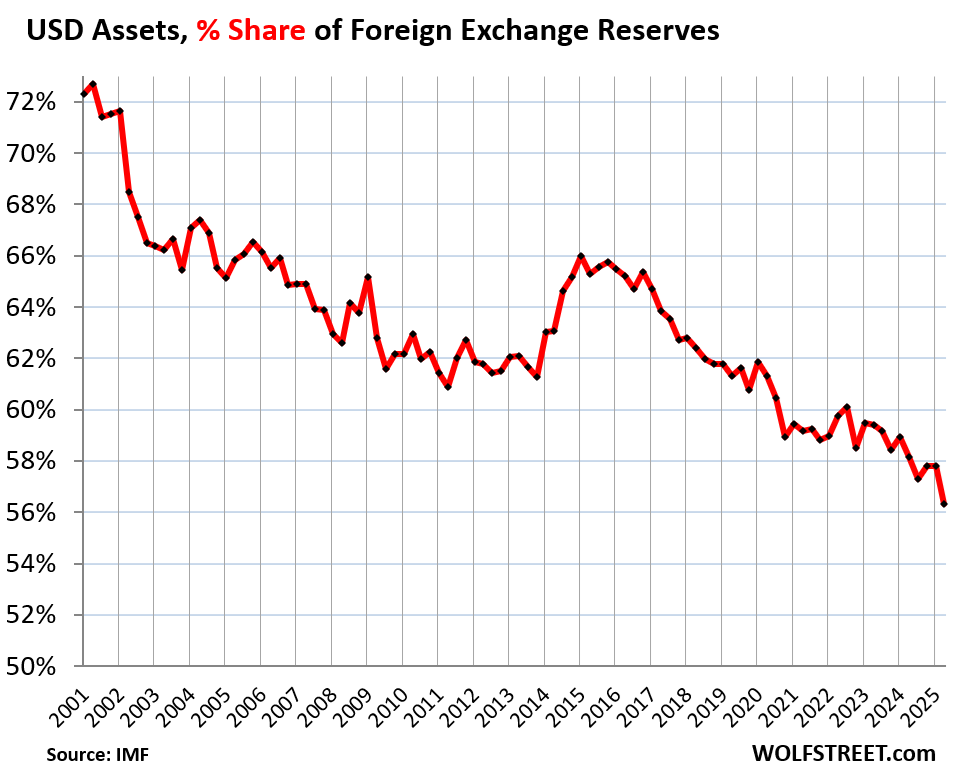

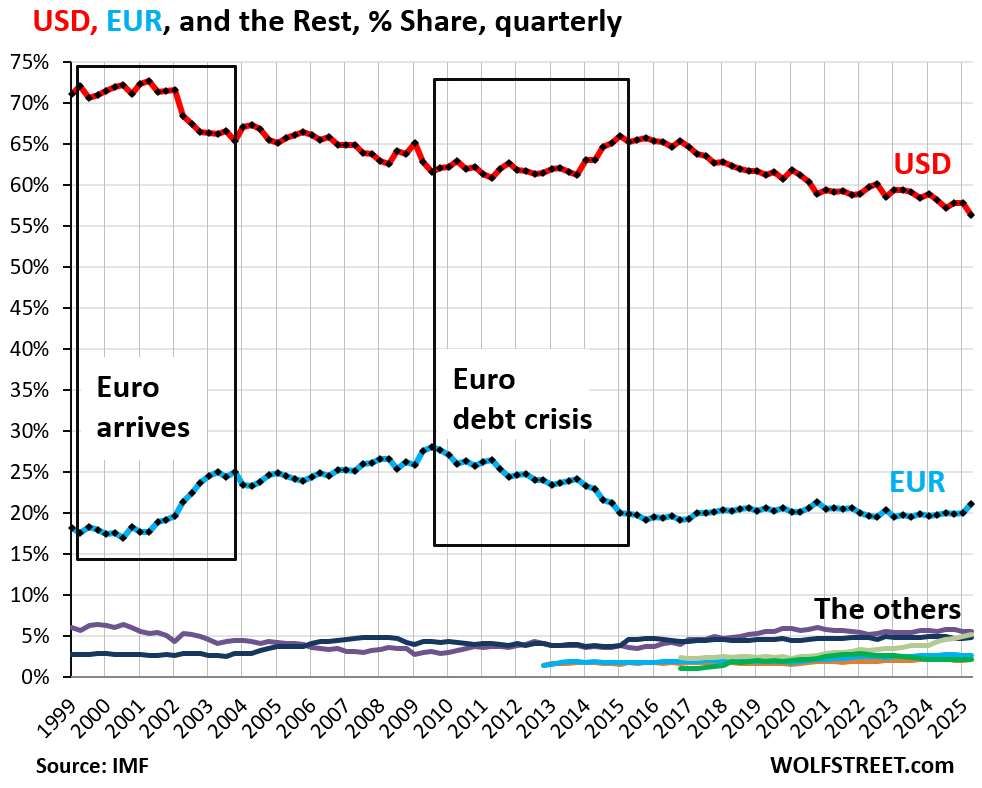

The dollar’s status as dominant global reserve currency just took another steep dive. The share of USD-denominated assets held by other central banks plunged to 56.3% of total foreign exchange reserves in Q2, the lowest since 1994, from 57.8% in the prior quarter, according to IMF’s new data on Currency Composition of Official Foreign Exchange Reserves.

At the pace of the past five years, the dollar’s share might fall to 50% in another five years. Even at 50%, the dollar would still be the largest reserve currency, as all other currencies combined would weigh only as much as the dollar. But the long-term trend is clear – and this has significant long-term consequences for the US.

USD-denominated foreign exchange reserves include US Treasury securities, US MBS, US agency securities, US corporate bonds, and other USD-denominated assets held by central banks other than the Fed.

Excluded are any central bank’s holdings of assets denominated in its own currency, such as the Fed’s holdings of Treasury securities or the ECB’s holdings of euro-denominated bonds.

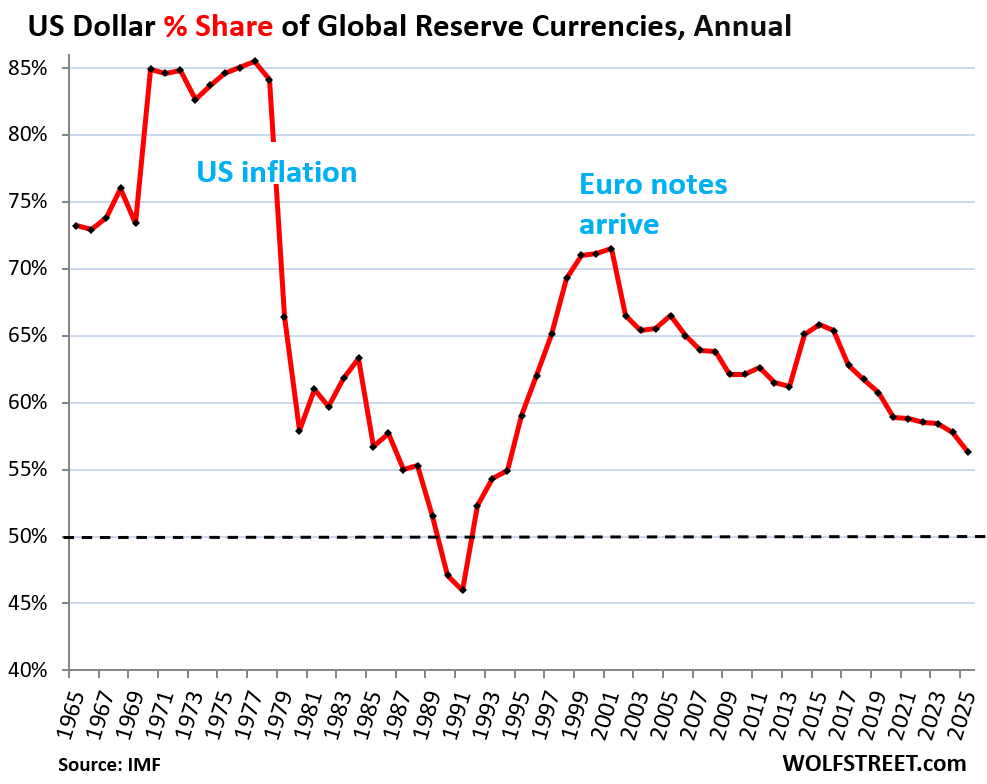

The dollar’s share had already been below 50% (dotted line in the chart below) in 1990 and 1991, at the final leg of its long plunge from a share of 85% in 1977 to 46% in 1991, after inflation had exploded in the US in the 1970s and into the 1980s, and central banks lost confidence in the Fed’s will to get this inflation under control.

But the Fed did bring inflation under control, though it took years, and by the 1990s, central banks loaded up on dollar-assets again, until the euro came along. The dollar’s share at the end of each year (2025 = Q2):

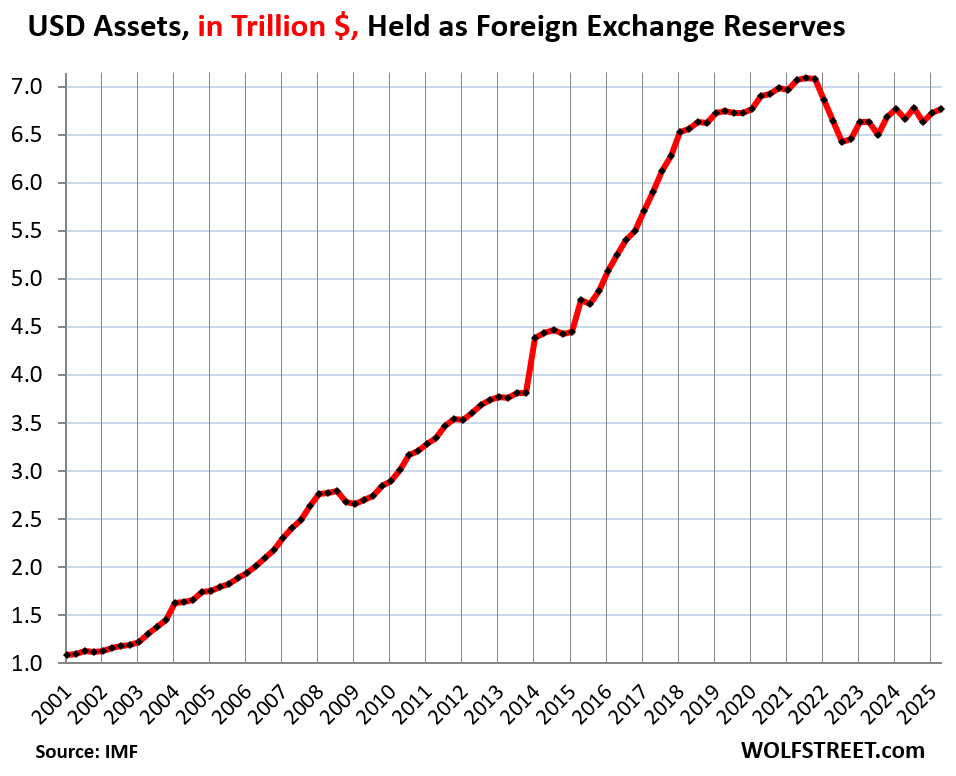

They didn’t dump USD-denominated securities.

Well, they did dump USD-denominated securities for three quarters in a row in 2022 when inflation exploded in the US; they dumped $660 billion in USD assets in Q1, Q2, and Q3 2022.

But when the Fed got serious about inflation and pushed up interest rates and started QT, the dumping stopped and the buying started again. And they increased their holdings of USD assets in Q2 2025 to $6.77 trillion, but that remains below the peak in Q4 2021 of $7.09 trillion.

Instead, what caused the share of USD assets to decline over the years is the growth in total foreign exchange reserves, driven by the growth in assets denominated in other currencies, including many smaller currencies, that outpaced the growth in USD assets, as central banks have been diversifying away from the USD.

So these are the USD-denominated assets – US Treasury securities, US agency securities, US MBS, US corporate bonds, etc. – held by foreign central banks:

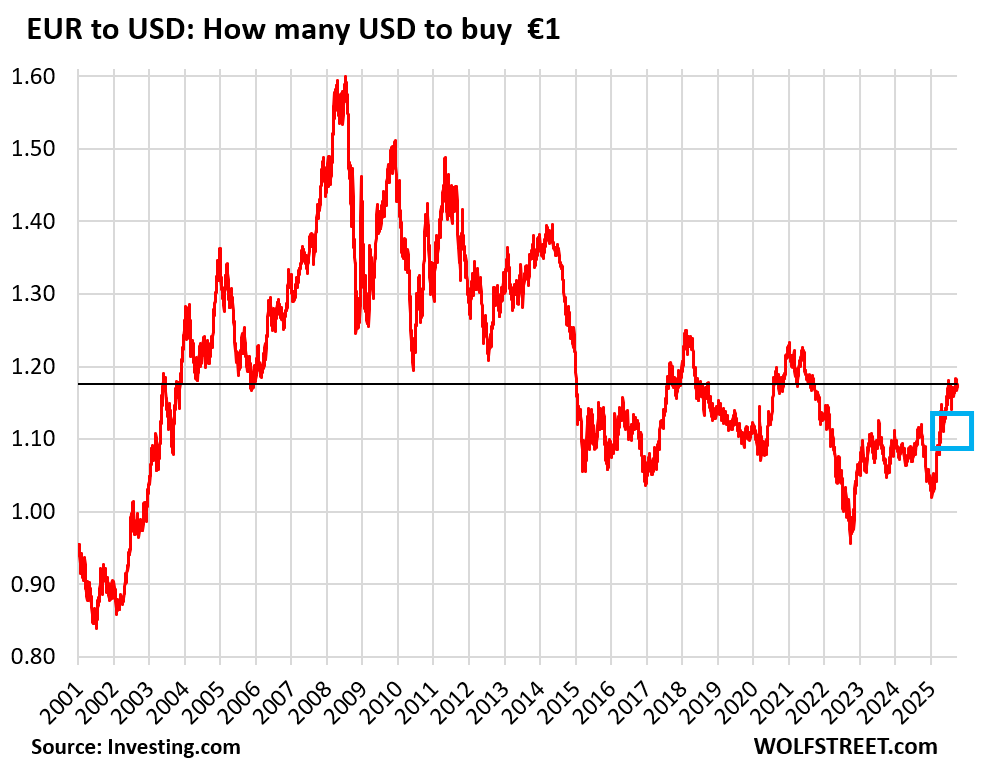

But the dollar tanked in Q2.

The IMF expressed all foreign exchange reserves here in USD. So all USD holdings are reported in USD obviously. But the value of EUR-denominated assets is expressed in USD at the current exchange rate; the value of all assets denominated in other currencies is expressed in USD at the current exchange rate.

Big movements in exchange rates change the value of the non-USD assets that are expressed in USD, but don’t change the value of USD assets. This shifts the share of USD assets against these non-USD assets.

The USD plunged 8.3% against the EUR in Q2 (blue box in the chart below). The euro is the second largest reserve currency with a share of over 20%. It moves the needle.

As the value of EUR-assets is then expressed in USD via that lower exchange rate, the value in USD of the EUR-assets increases, and the euro’s share of total exchange reserves rises while the dollar’s share declines.

Despite all the dollar-collapse theories, those exchange-rate movements were nothing special over the long term, with bigger and faster moves in the past, and the exchange rate between the USD and the EUR is in the middle of the range since the EUR’s existence (data via YCharts):

The USD also declined against the other major reserve currencies, but since their share is much smaller than the euro’s share (more in a moment), they had less of an impact.

The IMF estimated that most of that steep decline in Q2 was due to the drop of the exchange rate of the USD against the other major reserve currencies. If the USD exchange rates had remained unchanged in Q2, the dollar’s share of all global exchange reserves would have still declined, continuing along the trend, but the decline would have been much smaller.

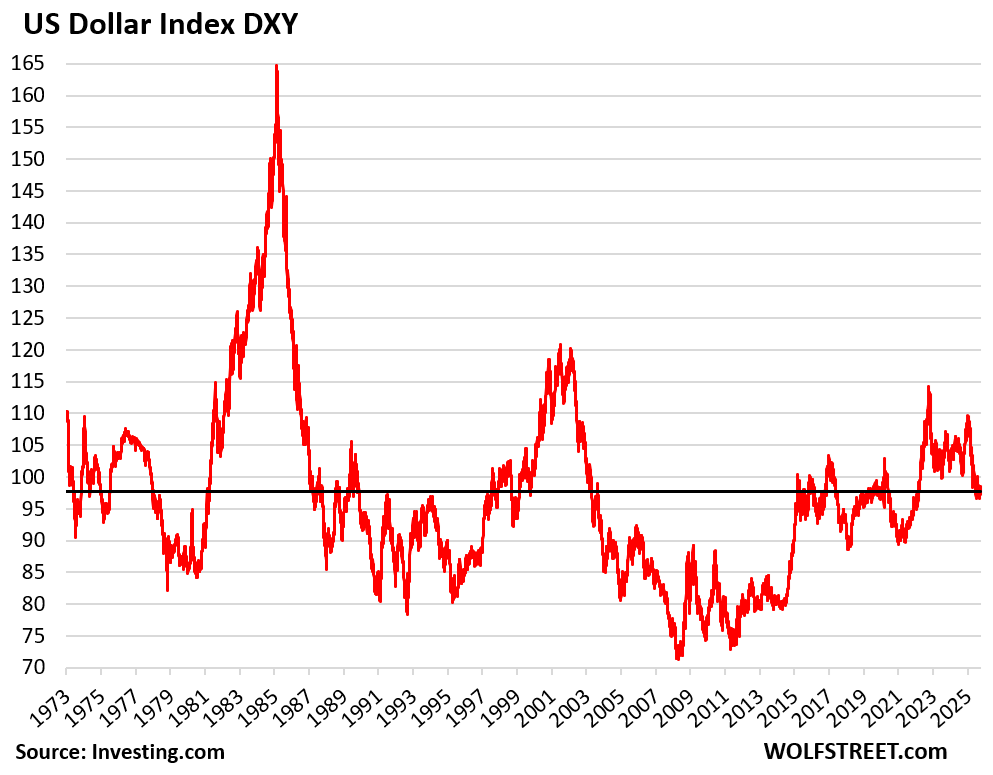

Over the long term, the DXY dollar index – it tracks the exchange rates of the USD against the currencies of the Euro Area, Japan, United Kingdom, Canada, Sweden, and Switzerland – has been, well, unchanged from 1973, despite huge fluctuations in between.

Also note the massive rally of the USD from 2009 through 2022, and how the recent decline of the USD has retraced only a small portion of that rally.

The other foreign exchange reserves.

Central banks holdings of foreign exchange reserves ins USD and in other currencies (expressed in USD), rose to $12.9 trillion in Q2.

Top holdings, expressed in USD:

- USD-denominated assets: $6.77 trillion

- EUR-denominated assets: $2.54 trillion

- YEN-denominated assets: $0.67 trillion

- GBP-denominated assets: $0.58 trillion

- CAD-denominated assets: $0.31 trillion.

The euro’s share, #2, jumped up to 21.1% in Q2. The entire surge in Q2 was due to the surge of the exchange rate of the EUR against the dollar, as the value of the EUR-assets were expressed in weakened USD (blue in the chart below).

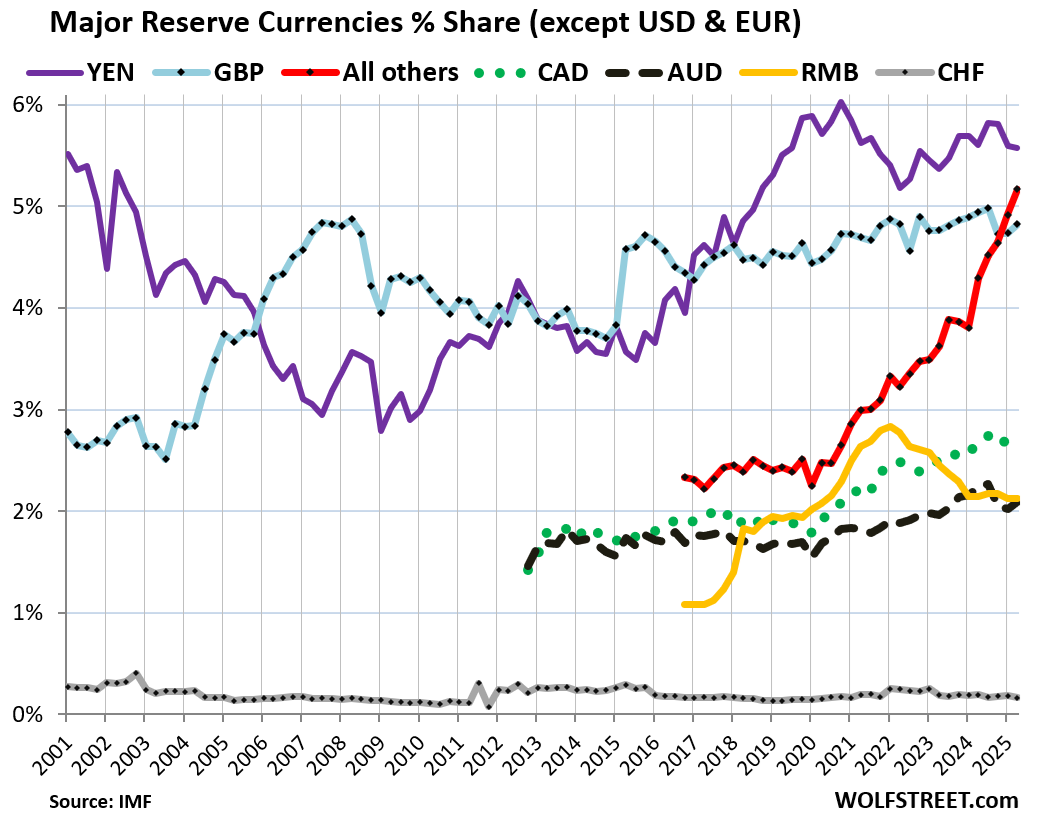

The other currencies are the colorful tangle at the bottom of the chart (more in a moment). Combined, they have gained share over the years, at the expense of the dollar, while the euro’s share has remained roughly stable since 2015.

The rise of the “non-traditional” reserve currencies. What is stunning in this tangle at the bottom of the above chart, once we look at it under the microscope, is the surge of “nontraditional reserve currencies,” as the IMF calls them (red line in the chart below). These are dozens of smaller currencies, and central banks have been gobbling up their assets.

What is equally stunning is the decline of the Chinese renminbi (RMB, yellow), that became an official reserve currency in 2016 amid immense hoopla and was supposed to catch up with the USD. It made a little headway early on. But starting in 2022, its share has plunged amid ongoing capital controls, convertibility issues, and a slew of other issues.

The two currencies that gave up share to the “non-traditional reserve currencies” are the USD and the RMB. The world is diversifying away from them.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

For the first time in decades central banks own more gold than Treasuries as a percentage of reserves.

Gold is “reserve asset” on a central bank’s balance sheet, not a “foreign exchange asset” (securities denominated in foreign currency), which are a subsect for reserve assets. So gold doesn’t fit into here since this is about foreign exchange assets.

But yes, some smaller central banks have been buying lots of gold (not the Fed, ECB, and BOJ though)

Why dont central banks diversify to silver platinum palladium? Do you see this trend coming up

The US did maintain a strategic silver reserve until the 1990s.

Copper is still king. We live in an electronic extension of the Bronze Age.

If any central bank is interested in metallic collateral for its credit issue, it might choose to construct its official headquarters with a few hundred thousand tons of solid brass.

diversify? in fiat system

idea is to use paper(and trust in govt) assets as currency

value lies in govt use/abuse

only fiat alive are ones in use until they implode

Clouds with gold lining: The Central Banks diversifying into Gold has been the best news ever to a gold investor. After living the 1970s inflation, reading Roman history of debasing currency, etc. all over the world throughout history, leaves the conclusion people had halfway to the Ice Age of what to invest in. Gold to $6,000 a troy ounce; and going to a gold standard would put it in the 10s of thousands. Looks like time to roll up to a country club community in a tax free state.

There is NEVER going to be any ‘gold standard’ again. The last time that was tried it was just a brief and very failed experiment from 1873 to 1933 and the total amount of gold in the world is about the size of two olympic swimming pools comprised of around 190,000 metric tonnes worth less than 1% of global assets.

Brief. 60 years! I agree we will not go back to a gold standard, but that does not mean there will not be more choices than the dollar.

I calculated gold would need to initially be $100k oz

and easily double/triple/x times

economy to large

Complete BS. First, it is very easy to a maintain a gold standard. It’s the PRICE that matters. Second, there will be a new “gold standard” but it will involve a basket of metals/commodities. What that basket looks like will be what everyone goes to war over. Regardless. The world is going back to mercantilism. If you don’t work/produce, then you won’t eat.

🤣

😂

We will never go back to Gold because under it GDP crashes result in 25%+ unemployment periods for extended periods of time. Workers and their lives and lives if their families get crushed for too long.

Why return to that just so a small rich group of billionaires can get even richer?

You get a de facto gold standard when gold preserves its value, and the major currencies don’t.

Likely for many years to come. Eventually the moneyprinting will stop and budgets will get balanced (and/or the currencies we trade with today will cease to exist). It’s a very big cycle that takes about a century to play out.

According to what I read in project 2025, the destruction of the dollars value is a feature not a bug.

Ben Around The Block

I have been betting against the dollar since January. While the S&P 500 is up 14,4% this year, my 4 biggest holdings are VEU up 26.1%, GLD up 44.6%, SLV up 57.9%, and VGK up 28.0. I guess I have lots of company around the world!

Yes, you do. Company at home as well. I hold the same as well as B and AG, but taking some profits now. Nothing new under the sun and humanity has been here before.

Good stuff, wolf.

Thanks

That is a clear trend downward that one might expect to begin to accelerate. I saw a Visual Capitalist post today that showed how stable coins are starting to really buy up treasuries. One really has to wonder how that might work out once the holdings become considerable enough and there’s a run on stablecoin holdings. A recession might just be the spark that could cause some stablecoin vs treasuries instability.

It’s funny, people buy stable coins and get zero interest and are exposed to the risks of them — and the middleman that gets the interest makes a ton of money — while they could just buy the T-bills directly and get the interest and have no risk.

Same argument applies to holding money in a checking account. Come to think of it, stable coins are the checking account of the crypto world.

I’d argue that “stablecoins” are the new money market fund. Stable? not so much…

Same as in the movie ”The Wolf of Wall Street”.

Investors have to stay on the sidelines without cashing in their profits and brokers spend real money on commissions, haha

I will say again have a fair amount of (in hand)metals,I do not want to see dramatic rises in the price of gold and silver though glad to have a diversified nest egg that started with a years preps for trying times,man made or natural.

The price of gold, etc. is more or less the inverse of the deterioration of the currencies. As they say, $100,000 a year is the new $42,000 a year.

OK, but the price gold dropped by 50% from 2011 to 2015. What does that say, per your theory, about the currencies?

With tariffs and much action to bring all forms of manufacturing home what might the outcome be in terms of who we would trade with?

Selling military hardware? China is using the economic for warfighting and for now seems to be close behind????

Many of the forms of making money will change with a high degree of knowledge and sophistication will preclude many here with good choices available in the past.

Amazing will be how the Baby Boomer 19 trillion wealth transfer will occur….

Baby boomers (and I’m one) will spend their trillions on nursing homes.

Correct. Healthcare in general.

Genosurbro,

The US excels at ensuring geopolitical issues so it can sell weapons. Who knows why department of defense was rebranded but perhaps marketing campaign. Can’t exactly keep selling weapons when countries have stockpiles so need to fan the flames a bit. We are the ultimate lord of War arms dealer.

I would expect the dollar will continue to fall, but slowly. There will be more options to chose from with gold, etc. may be some of them. All it would take for gold is an exchange outside of US control.

It is all digital now and units of anything could be traded. It is all about trust and the dollar is not doing so well with our spending and use as a weapon.

1945: major powers UK, France, Germany, Japan in ruins. US & CN not only intact, but super-productive. No wonder the dollar was the reserve! But other powers are rebuilt now, with currencies (and stability) again worth having.

So does Morgan Stanley. In August they wrote:

Morgan Stanley Research estimates the U.S. currency could lose another 10% by the end of 2026.

Despite a recovery of 3.2% in July, the delayed impact of tariffs on growth and unemployment – besides policy uncertainties – are likely to keep negative pressure on the dollar.

Foreign investors have been adding hedges to their exposure to U.S. assets, which will likely further weaken the dollar.

I wonder if there is a stock vs flow issue here re $ status. Reserve $ holdings indicate decline, but is there evidence that $ role in settling transactions is down?

The measure for trade currency is a different measure, unrelated to reserve currencies. These are the three measures of a currency:

— Reserve currency (USD securities held by other countries)

— Trade currency (international trade by foreign countries settled in USD)

— Financing currency (international projects get financed with USD).

In terms of trade currencies, the USD and the EUR have been neck to neck for many years. The EUR has been a very strong trade currency between EU and the rest of the world, in part because of the EU’s huge exports and generally big trade surplus. The YEN is a strong trade currency. The RMB is growing as a trade currency.

The US doesn’t benefit in any way if the dollar is used to settle trades between two foreign countries, so this is kind of irrelevant.

But the US benefits in a big way from being the top reserve currency because it creates demand for its debt by foreign entities which helps fund the huge twin deficits (trade deficit and budget deficit). Being the top reserve currency has enabled the US to run these huge twin deficits. Funding the twin deficits is why reserve currency status is important. And as the status declines, funding those twin deficits is going to get tougher.

Interest rate will have to stay high. The Fed, regardless of the chairman, will make up excuses to keep it high, just like Greenspan did to keep rate low after 9/11 which caused 2008 crash. CPI, GDP, and unemployment don’t matter. There’s a bigger threat that the elites dont want the public to know — de-dollarization. When the music of Bretton Woods inevitably stops, people will be scrambling for a chair.

This dedollarization stuff and subsequent collapse of the dollar or whatever have been posted here in the comments ever since I first opened the comments about 12 years ago. Dedollarization is taking place slowly, and it makes sense, why should the #2 economy (China) deal with dollars, and the euro is a hugely powerful trading currency, given the EU’s trade surplus, and none of those developments matter to the US. What does matter is the amount in US securities held in foreign countries. If they lose interest over time, yields in the US will rise, but higher yields bring in the buyers, and so yield will solve that problem.

Something that is actually scary and worrisome are the gigantic asset price bubbles everywhere we look in the US and elsewhere – and the attitude that investors have about them, and their denial of the existence of risk (or even an understanding of risk). That’s scary, not the dedollarization.

This is not solid timing with my desire for international travel! One happens to the days of 2 euros for $1!

“But starting in 2022, its [Chinese renminbi] share has plunged amid ongoing capital controls, convertibility issues, and a slew of other issues.”

Perhaps the USD share of reserves is also plunging because of capital controls (ask US expats about FATCHA), tariffs and reciprocal tariffs that create convertibility issues for multinational corporations, and “a slew of other issues” that I’ll summarize for the US as a decline in the quality of governance. These governance issues include being a one-party state, socialization of large businesses, political pressure on the Fed, and cutting rates into a trend of rising inflation.

Seen through this lens, demand for reserve currencies is driven by the perception that the issuing nation does not have incentive to resort to money-printing or currency controls – either of which can reduce the utility of reserves. Thus the best performing currencies of the past year have been from countries with low debt/GDP ratios and perceived-honest governance.

A similar flight-to-legitimacy can be seen in interest rates / demand for debt. Greece, of all nations, is borrowing more cheaply than the US because they’ve subjected themselves to fiscal guardrails and are steadily paying down their debt/GDP ratios. The US and UK are on the opposite path, and are seeing their long-term rates increase with every pro-inflationary cut to the overnight rate.

Doing the wrong things suddenly matters for countries/currencies with debt/GDP ratios over 100% and no real desire or pathway to turn the trend around. Yet for countries like Italy and Greece, the market is rewarding their pivot toward responsibility.

I think the company that makes Charmin should release a new brand of TP – ‘Benjamin’…made to look like $100 bills. Luxury at it finest. Wiping your behind with $100 bills.

💵

You can already buy that, been around for a long time, in all kinds of varieties. They’re around $10 a roll though. And I don’t know how soft they are.

The US Dollar is a kamikaze plane in WW2. It’s 50 feet from the ship’s deck. Won’t be long before contact. We all know what happens next.

Sayonara!

So far, so good. Take a look at the long-tern dollar charts in the article. Nothing special happening with the dollar.

I guess we suffer the consequences of bad leadership. Again.

I blame Cheney “deficits don’t matter, reward the base!”

So it started, and it will be a long time until the end. I was expecting this crisis in the 2030s, and it started after the election. Ah well, here we go.

Measuring anything in a changing base currency is slippery. A stable coin tied to a sinking asset (USTs) is a loss maker. If the Swiss National Bank issued a gold stable coin that paid 1% in gold interest per year, money would pile into it. That alone tells the tale.

Epiphyte corp is the destiny, and was seen 30 years ago by N.S. in cryptonomicon It is simply to remain how long it takes to hit the mainstream.

The bezzle of finance is immense, and the really fun part of AI will be when it strips the lies from reality, and flenses our floundering society of the lies that sustain our dismal reality.

Welcome to the new world, the kids will get it quicker than us, as usual. The failures have been interesting, especially watching Zuck, with billions, fail to make farcebook money.

Most of it is the wild and wooly frontier finally coming out of the shadows into the light. Remember, the largest use of bitcoin was on Silk Road websites for criminal activities.

Wolf,

Excellent article. Would like to suggest a follow up dealing with the ramifications of the decline in the $ as a world reserve currency to the USA. It would be interesting, especially with the multiplicity of smaller currencies taken hold of central bankers interest.

I can say this in one sentence: It will put some upward pressure on long-term Treasury yields.

A decline in $ will reduce the value of US’ debt and US may gain by its exports .

A weak $ will reduce US’ Financial hold on the Global system.US Citizens will pay more “weakened $s” to buy things, in general

The trend line appears to be solidly down. Best guess – Trump’s fiscal and trade policies will hasten King Dollar’s death.

US plans to devalue $ to reduce the value of its Debt. Mr.Stephen Miran has some ideas, as follow up, one of which is, not allowing other nations do the same by some form of coercion.