But the hot air was let out of pandemic-era gross margins, operating earnings, and net income. Sellers of existing homes should pay attention.

By Wolf Richter for WOLF STREET.

Homebuilder Lennar reported earnings yesterday evening, and along with its conference call today, aired out a litany of lamentations about the housing market: Revenues from homebuilding fell 8.8% year-over-year in Q3, incentives needed to make those deals jumped to 14.3% per home sold, which slashed its gross margin to 17.5% in Q3, from 22.5% a year ago. Operating earnings from homebuilding plunged by 49%, net income plunged by 50%, and earnings per share plunged by 46%.

Gross margins dropped “primarily due to a lower revenue per square foot [lower prices per square foot] and higher land costs,” that were only “partially offset by a decrease in construction costs,” the company said in its filing today.

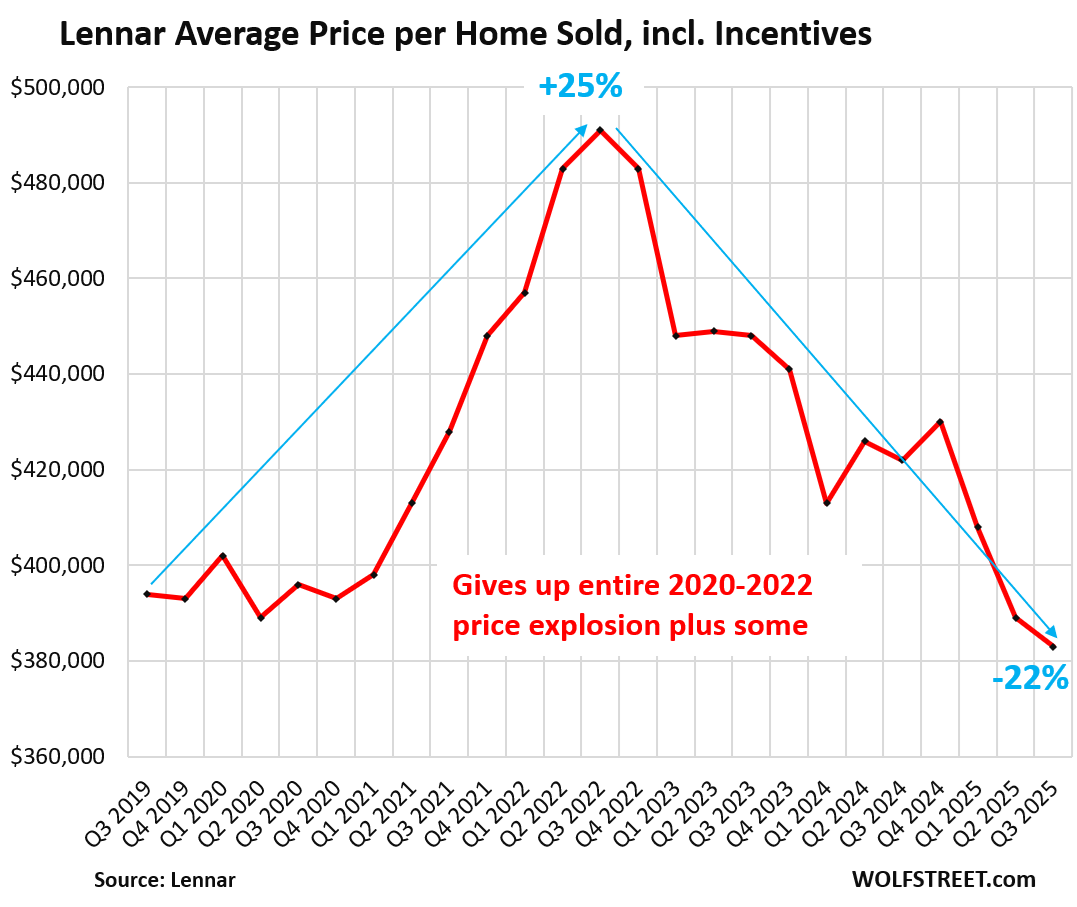

The entire Pandemic Free-Money price spike got cut: Lennar’s average selling price in Q3 dropped by 9% year-over-year to $383,000, below where it had been in 2019, and by 22% from the price peak in Q3 2022, when FOMO-addled buyers were willing to pay whatever because money was free.

Lennar targets the mass market. It doesn’t target the high end. People who want to spend substantial amounts on a custom-built home will likely choose a different builder. Lennar’s homes are mass-market products, they expand the supply of homes that people can more easily afford, and more supply and lower prices are exactly what this price-ravaged market needs.

From Q3 2019 through the peak in Q3 2022, Lennar jacked up the average price by 25%. Lennar has now given up the entire price spike plus some, and the average price is below where it had been in 2019.

As a result of the much lower average selling prices, sales held up: The company delivered 21,584 homes, which was up a hair from a year ago, and new orders jumped by 12% to 23,000 homes.

That message is lost on sellers of existing single-family homes whose sales plunged by about 25% from 2019 and by over 30% from 2021, because prices are too high, and sellers are loathe to budge. And homebuilders are now eating their lunch.

Hot air comes out of inflated gross margins. Lennar’s lower prices did the trick, kept volume up, and boosted its new orders – but they crushed the inflated gross margins from yesteryear:

- Q3 2025: 17.5%

- Q3 2024: 22.5%

- Q3 2022: 29.2%

That Q3 2022 gross margin of 29.2% was when money was still free, and when money is free, prices don’t matter, and homebuilders went on ahead and cleaned out these FOMO-addled homebuyers, generating huge profits for themselves and massive mortgages for the homebuyers, and a good time was had by all.

But the free money ended, and so there’s this litany of lamentations about “the continued pressures of today’s housing market,” and about the “incentives and price adjustments to match market conditions,” as Lennar said.

Lennar, like all homebuilders, figures the cost of incentives and mortgage-rate buydowns into the average price per home sold. So all of the costs of those incentives are included.

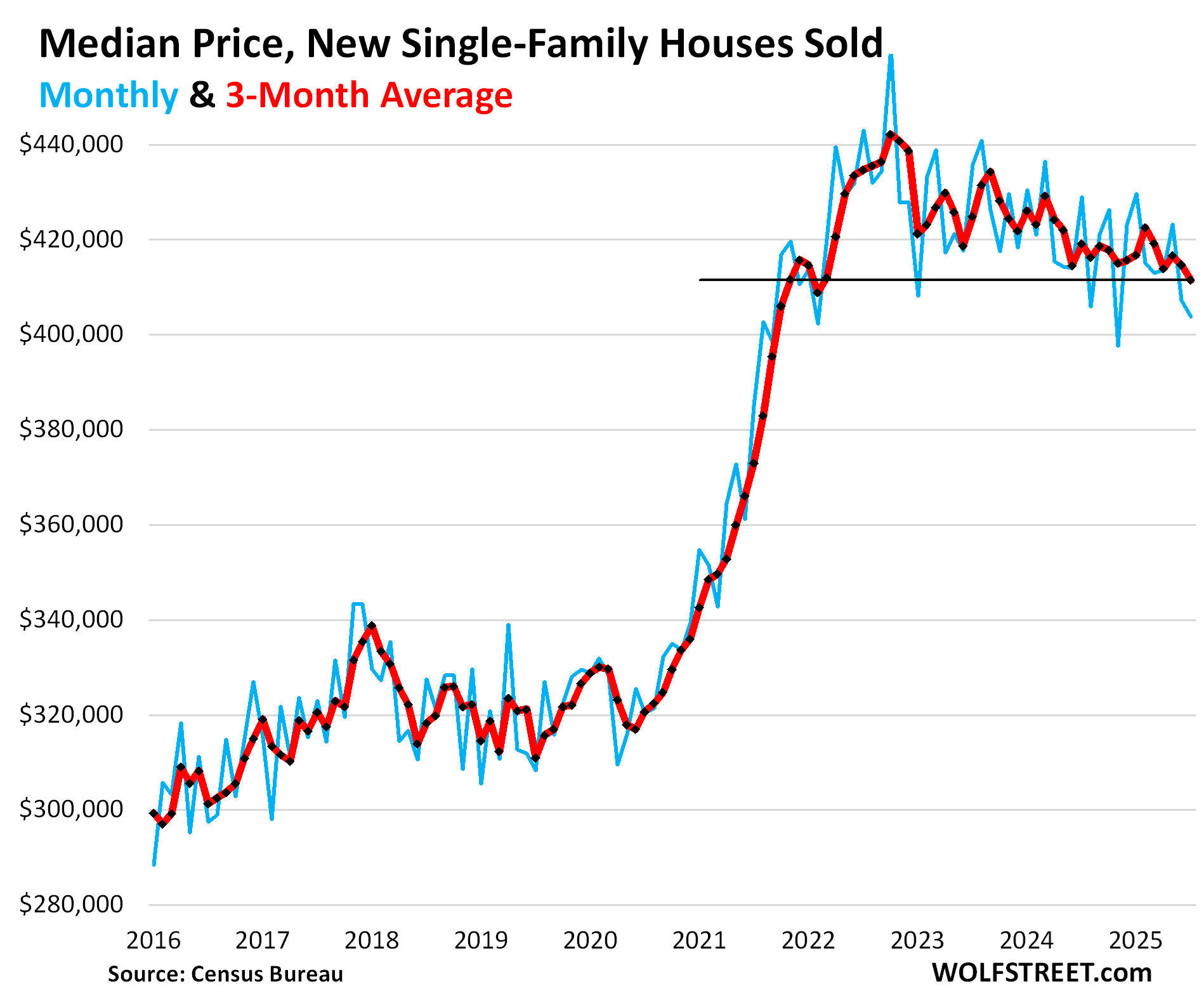

Incentives are not included by the Census Bureau, when it reports on new home sales, and bases its median price on contract prices of deals, and they don’t include the costs of mortgage rate buydowns and many other incentives, and without those costs, the contract prices have dropped far less than actual new home prices and understate the actual price drops.

As per the Census Bureau, the median contract price across the US by all homebuilders dropped by 5.9% year-over-year in July (blue in the chart below), and the three-month average (red) dropped by 1.8% year-over-year and by 5.9% from the peak in late 2022.

Lennar also cut its delivery expectations for Q4 “in order to relieve the pressure on sales and deliveries and help establish a floor on margin,” co-CEO Stuart Miller said during the conference call today (transcript via Seeking Alpha).

“Sales volume was difficult to maintain and required additional incentives in order to achieve our expected pace and to avoid building excess inventory,” he said. Sellers of existing homes should pay attention.

In case you missed it: Condo Prices Dropped by 12%-27% in these 25 Bigger Cities through August: Condo Bust Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Revenues from homebuilding fell 8.8% year-over-year in Q3, incentives needed to make those deals jumped to 14.3% per home sold, which slashed its gross margin to 17.5% in Q3, from 22.5% a year ago. Operating earnings from homebuilding plunged by 49%, net income plunged by 50%, and earnings per share plunged by 46%.”

Incredible !

Thank You for Your professional observations and reporting W.R.

Have a fantastic weekend ! 🍻

Good news for everyone, except homebuilders, their stockholders, homeowners looking to sell, etc.

Good news for folks like you and me.

Margins tell the whole story.

From 2002 to 2022 (with rare breaks), ZIRP likely empowered builder margins to explode – making them and affiliated parties very, very rich for a very, very long time.

If they have complaints, they can come back in 2042.

Another big shout out to the Federal Reserve.

Lennar is giving them away in my area. Offering 3.99% financing right now for 30 years (PMI on top of that), plus big discounts. Low income buyers are snapping them up (homes starting at $205 K)

I follow them in my snowbird area. They are now @ or below $160/ft2.

35% cut since I started tracking price.

Which area

Is that detached single or town house?

I was driving down I-90 about an hour east of Sioux Falls and saw an ad for homes starting at $120/sf. Granted it’s in the middle of nowhere, but prices are coming down.

Now I can’t imagine what kind of ICF and PEX and monolithic slab and laminate sheet crap it’s built with, but if the rural folk need cheap shelter, the deals are there.

All this and the real bubble crash hasn’t even happened yet.

What ought to freak out real estate investors is that pricing may never again hit their 2022 peaks in real terms. It took until 1970 for a real estate investor who bought in the 1929 bubble peak merely to recover the nominal value of their investments. With slower population growth and much less immigration you may never have real estate hit these prices again in real terms.

I’m going to laugh when the people who bought in to the stupidity go bankrupt – and especially so since many of the people who bought into it are also propagating it.

Solid analysis as always Wolf.

With multifamily there is at least some pretend and extend. You also have the ability to collect rent. You may never hit your IRR or equity multiple but you can still make a solid cash on cash if you hold long term. The problem is that many of those people jumped into multifamily during the free money era and know jack shit about how to operate a property.

Source – me, in multi-family and unfortunately know the jackasses who jumped in

Lots of people also did this with SFH. And all of them going to lose their shirts because you simply can’t make it work unless you can afford to staff maintenance personnel yourself (plumbers electricians etc.), have zero debt, and can afford to lose all your investment (I.e. no insurance). This is true of both SFH rentals and multifamily rentals.

That is a very very small group of investors. And for those who aren’t in that bucket, selling now to avoid even greater losses later is your only option.

This attitude is quite common and continues to show a lack of understanding of the goals of “real estate investors” It’s not about the value of the property going forward, only that it works now. If I buy a home to rent and in ten years it is worth only what I paid for it, or maybe even less, I could care less. I’m getting the house for free. Someone else is paying for it and I get to keep it.

I bought a rental home in 2011 and another in 2019. Both have doubled in value but if they were worth the same I still made out like a bandit. The 2011 became a free house 3 years ago and the 2019 is about one third free so far. If prices drop enough I’ll buy another one, even if it never appreciates in value.

Keep laughing, I do too, all the way to the bank…..

You’re not buying now for a reason, genius ! You can’t cash flow unless you’re just buying outright with cash, and getting a terrible cap rate.

The foolish investors that bought into this market in late 2021 and beyond aren’t looking too good now as costs to maintain are increasing and rents are falling.

It includes investors who bought in housing investments 2012 through 2019 if they still have debt on the books, or investors who can’t make their cash flow work if they get 2012 rents but 2025 expenses.

That includes nearly everyone who bought into this insanity after 2008. It also includes nearly everyone who can’t do maintenance in house, meaning you have to hire plumbers, electricians, etc. from outside instead of having such people on your staff and those who could afford to lose their rental units without insurance.

Only the very largest commercial investors will even be able to try. But if you do meet all these conditions, you’ll still make some money – just not as much as you do today.

I’m thinking that only a cash buy works as a rental now. Rentals today can hardly afford to carry any debt.

As for the low cap rate that everyone points out. I suppose it’s true but a cap rate always has to be compared to something and that something would seem to be whatever the risk free rate is.

The risk free rate today is 3.75% and going down.

If I have 500k in cash and buy a rental outright, I can generally expect to earn 3%-4% net in actual cash flow unless I really press the rents to 1% more. That does not sound so good in cap rate terms. But on the other hand, that 3% return is mostly tax sheltered so I actually get to keep that cash flow and not hand 28% over to the government.

People will tell me I can put it in the S&P and earn 10% per year. But I measure risk by how well I sleep at night. To me the S&P is less of an investment and more of a hedge that is subject to the government policy.

However, I get the cap rate argument. It boils down to what let syou sleep at night.

A house that provides an actual good to people – housing at a reasonable monthly cost – where a young family might want to actually raise kids, it also benefits society.

If I carry no debt, I’m somewhat indifferent to if the price of the house goes up or down from year to year. I can always hold it through the down turn even if that period is 10 years.

If I eventually sell it at a loss then that probably means asset prices in general are also down.

I’m in the process of buying a house. I expect that even now, I’m paying more for it than it will be worth in 1 or 2 years. On the other hand, it’s a house in a location we like and we know to be attractive going forward and where houses rarely come to market without being sold privately. We know this because we watch this area very carefully. The opportunity is now, so we buy now – pay cash and plan to hold it for many years . I grant you, that from a wall street point of view, it’s a low cap rate but I dont live on wall street.

Given your name, I can see why, but that is a Florida problem due to natural disasters, insurers bailing, and the vast influx from less friendly states largely over. I would say most metro areas don’t have those problems.

Sadly, none of us own our homes even if we paid cash. We rent them from the local tax authorities.

Agreed. I believe every property owner should be able to claim one primary residence exempt from property tax. This would allow for true ownership.

Yes, you do own it.

It’s like saying, there should be no permits needed to do whatever the home owner wants on the primary residence.

Just because it’s primary residence doesn’t imbue it special qualities.

Absurd. Who will pay for the services that give the prop value? Water, sewer, streets, cops, fire, etc.

If you think you can do without these frivolities, there’s lots of rural props for you to move to.

BTW: I’ve had some experience with props on well water. My word to those on municipal water: never bitch about your water bill. When that big tanker truck rolls in to boost the well, it’s bringing about a week’s worth of water used by an urban gluten.

Without property tax, how is the local government going to be funded? Without a local government, you have no protection of your land rights and it can be taken from you by someone else if they wanted. That’s how I look at it.

I don’t understand this from a numbers perspective. BTW I have 3 rental properties as well which I am or have sold.

I think you are saying you bought a home with a loan and say 20% down?Have been renting it above the monthly mortgage. So you are paying off the mortgage and maybe any repair costs?

With the mortgage paid off. You now get the rent minus expenses. So you’ve effectively created an annuity. With the risk of not getting rent if the renters leaves, or the rent goes down, or major repair costs occur which the home is a depreciating asset.

From a total return perspective you would have made more money on alternative investments like stocks. By a wide margin and then just park the money in treasuries, dividends, and eventually bonds. That’s why I’ve cashed out of the homes at the peak and now have greater dividend based cash flow then rental income even with a home paid off. The tax is also less.

Stocks are at least as overvalued as residential real estate is.

Not all stocks are going to fall, but unless you bought a large amount of US-manufacturing stocks that risk is very much open to you. This post-2008 environment has made stocks with prices thousands of times earnings and you can’t tell me that is anything other than a bubble.

Sure, if all you care about is cash flow you’ll do better. You’ll certainly do better than rental real estate. But what people are going to find out is that there is no safe investment. If you can invest your money in something you can lose the value of your investment. And people being reminded of that is no bad thing. The destruction of that sort will correct the excesses of the free-money era.

A lot of investors have merely left their housing investments vacant, not even bothering to rent it out.

This is particularly prominent because the costs of mortgages and maintenance is currently above the income you can get renting out housing, which is absolutely not how it should be.

Just because you didn’t do this doesn’t mean that a million other investors didn’t, because they did. And when they realize that the capital gains are nonexistent, they will panic-sell and bring down prices even further.

To bring American housing down to affordability you have to have housing at or below 2012 pricing. That’s all there is to it. If you can’t make money renting at 2012 rents but 2025 expenses, you too will be forced to sell to limit losses eventually.

Agree Doug. Some people always want to see the world burn. They don’t see that duration matters. They just see the top tic and think everyone bought there. In reality, they more than likely bought there once and will be angry forever. Meanwhile we eat oysters and drink all the champers. It’s a hard life. :)

You don’t seem to be considered the opportunity cost of your capital. If you have $1 million locked up in real estate that is slowly declining in value (paying taxes, insurance, cost of maintenance, depreciation, etc) versus having that same $1 million in tax-free munis earning $45,000 per year after taxes… I know which one I’d choose.

I don’t understand your post. “It took until 1970 for a real estate investor who bought in the 1929 bubble peak merely to recover the nominal value of their investments.” As an active real estate investor your making me nervous. I’ve done well and been cautious. Do you have any data or source material for your comment?

When Houston went into an oil and gas depression in 1983. Home prices did not recover until 1992. Condos sold for cents on the dollar. Single family units hit the skids. Job losses fueled foreclosures.

Bought a 3400 sq ft vacation mountain hse. in NC in 2012 for $280m for cash from a mortgage company. Sold it in 2023 for $925m.

Lesson, keep your powder dry.

The Fed always screws things up.

I hope I’m making real estate investors like you nervous, because you lot need to be nervous.

The ultimate point of my post is that we’ve had a national real estate bubble before and its pop both contributed to the Great Depression and kept prices low for decades, even with strong population growth. A bubble pop now is likely never going to be recovered from in real or nominal terms because we’re entering an era of slow population growth. Prices for things like houses have to get very low to make them cheap enough for young people to raise large families. That is going to screw investors out of a lot of money. Don’t count on income growth either since you’d need a lifetime of income growth to make the nominal price even begin to make sense. More likely 2.

My source for this previous 1920s bubble is “Real Estate Prices During the Roaring Twenties and the Great Depression”. I would post link but usually that results in problems. It’s authored by Tom Nicholas and Anna Scherbina, and online at Harvard Business School. One of the other depressing facts (for real estate investors) the study leads with is that stock market investments had 5.2 times more return than real estate, even including rental income, between 1920 and 1939.

My ultimate point is, real estate is a bubble and it’s about to pop far worse than anyone else thinks it will. If you’re a real estate investor you better sell now or you’ll never be able to.

“I’m going to laugh when the people who bought in to the stupidity go bankrupt – and especially so since many of the people who bought into it are also propagating it.”

Lol, you are silly and jealousy and we are rich, keep trying and work hard, maybe in the future you will get there too.

Many of the older homes have larger lots, better location, zoning not allowed in compact builder HOA type projects. I see 3,000 square feet homes with no land in the 650 to 800K range. In my cul de sac, people have 2k sq ft to 5k sq ft homes going from 750K to 1.5mil all with land as in .9 of an acre to 2.5 acres with no hoa, and in the county right on the border to the city with radically different zoning advantages on my end and the complete opposite 1 block from my home where it becomes city although we both have the same town on the address. The point here is the complexity of each real estate situation always has exceptions of great value. People live here 10 to 50 years straight for the reasons stated. Schools excellent, shopping all over, freeway convenient, and the ability to build extra home, shop, barn or ?????

Where?

Woodcrest ca

Woodcrest is a census-designated place in Riverside County, California, United States. The population was 15,378 at the 2020 census, up from 14,347 at the 2010 census. The adjacent city of Riverside lists Woodcrest as an area for potential annexation.

Bro thats Lake Elsinore a living hell

Not anywhere near Lake Elsinore.

The potential of Woodcrest is awesome.

NO HOA

LOWER SALES and PROPERTY TAXES

Much more freedom with building codes

Address is Riverside but Woodcrest will never give up its advantages of being in the county. Everyone is aware of things like I can now have 5 horses on my property. If Riverside City took over it would be 2 horses.

Larger lots are good on paper but bad to maintain and take care of .

Ideally I’d like to move into condo once I get older.

I just retired 3 weeks ago. Sold my three bedroom. Two bathroom home with a large yard in NJ. Moved into my condo that I had rented for the last 11 years. We renovated the entire 1500 square foot condo. Where about 5 mi from the beach in New Jersey.

Also built a home in Northeast Florida by the beach when covid was raging in 2021. I think I got lucky. Now I just need to start living the dream after 45 years of hard work.

😎🏝️🍀

Good for you

I am living my dream right now instead to wait for me to retire then live my dream.

I have no debt and all my $$ is slated to charity I intend to donate once I am dead

My children would not get anything other than college expenses as I don’t believe in passing the inheritance.

Hope they do well.

I dont have any dog in this race and I just want to sleep peacefully and die with absolutely no money .

@Mark, Congratulations!!

Great for you Mark!

Enjoy your freedom!

We see this a lot on the outskirts of Sacramento, especially in Placer County. Most of Roseville has already been transformed over the decades, and so the 6,000 sq ft lot with a 3,000+ sq ft home with an HOA is very common. They are having a hard time selling at current prices in this market, and I am seeing prices softening in real time (consistent with the articles on this website for that market). In the luxury community of Granite Bay, there are many list/delist games being played and 6/9 month lease games, where they are hoping to rent in Spring 2026 after having failed to sell in the 2025 season at their insane list prices. Also, digging into high-end homes that are currently on the market and looking at places like home. com where they list mortgage history and make the already public info easily accessible, the savvy buyer can see exactly who bought what and when for how much. I didn’t realize that so many small named LLCs bought 1 mill+ homes and either flipped or held for appreciation and are now listing and not getting bites on their astronomically priced homes. This will sort itself out eventually. There are only so many buyers in the Sacramento/Placer region willing to pay 1.5 mil for an old flipped home on 2 acres of fire-prone land. Especially when one zoning change could mean that your neighbor with the flat 5 acres behind you may sell and you find yourself bordering a new development and 20+ new neighbors along your fence line. But hey, I guess that is always the risk of buying big lots of land in desirable places.

Re:” Sales volume was difficult to maintain and required additional incentives”

That sales volume problem is a bit like cellular degradation with a disease — or the recent mutated virus stages with Covid. LEN is trapped, or overly reliant on dosing-out incentives, as their profit margin evaporates, as home prices all experience repricing, due to nonsensical expectations. The volume decline seems like it will continue as inventory grows. I assume building materials and labor costs will add pressure as well.

I disagree that the “message is lost on sellers of existing single-family homes.” They know that all that the need to do is to reduce the price and the home will sell. The real story is how so many home owners have the luxury of choosing not to sell. Past housing bubbles were burst by homeowners being forced to sell, recession, job loss, etc. If one can post a home for sale, pull it, repeat, for months… they are not in financial stress.

I heard the excuse here in FL and boy were they wrong. If it’s unaffordable and overpriced, then buyers will stay away.

There are always forced sellers – death, divorce etc. Unemployment won’t stay historically low forever – it will continue to increase.

“The real story is how so many home owners have the luxury of choosing not to sell.”

I think this is a fair question – how have investor-speculators hung on for 3+ years of unZIRP?

SFH investors-speculators with even a smidge of knowledge understand that it is all about interest rate changes/cycles – yet this generation of investor-speculators (who witnessed the post 2008 housing apocalypse) have somehow managed to white-knuckle it this go round for over three years, presumably praying for a rate pivot.

Should be required to disclose all incentives included in a purchase and adjust the comps accordingly. These games to prop up the market need to stop

That could well create a panic – or a riot… because in many of these communities they are now selling homes (after incentives) for less than what they sold them for in prior years. Imagine a 1000 home community that is five years old and half built out… and then suddenly word gets out that the builder is selling the new homes for less than what people paid for their new home two years ago.

It’s ironic, but one could raze entire cities to the ground – Oakland for instance- and rebuilt them better for half the price of what the current housing inventory is allegedly worth on paper.

Alot of the “value” in these older neighborhoods is in the lot/land; primarily location and nearby amenities. In Charlotte, where we lived, close in neighborhoods with mature tree lined streets and solid infrastructure, older/original houses were sold for $1M+ and promptly torn down. The new house would almost assuredly be more costly than $1M since it is being built on a $1M lot.

Your understanding of land value vs improvement value and cost of construction is wrong.

Example: 2500 sf house on 5000 sf lot, market value $700,000, land value is $400,000, new construction cost $250/sf fully loaded.

29% margins…. back to 17%.

this is what I still look at; all these companies whose margins “magically” doubled during/after covid, presumably due to their own “genius management”. Not Lennar, but most are clinging to those margins with a death grip; willing to try anything to grow that margin, but is that realistic? Can’t fault them for trying, but it just seems a little ridiculous to have a step function like that and expect it to stick. Whatever.

And to the Real Estate Bros who say that prices never come down because “my cost is now 300 a foot” or some other inflated number, please let the peanut gallery know “what your cost is” now.

Lennar home listed at $350k. No info on lot size, but it’s in a densely packed subdivision, where the only amenity is a small playground. But only a $50 HOA monthly.

1,700 square feet, with a single large room on the first floor (Lennar markets this single large room as a family room, breakfast room, and kitchen, but it’s just a single room). 3 bedrooms upstairs. 2.5 bathrooms.

What are you griping about? Lower priced nice new homes? And then out of the other side of your mouth you’re griping about affordability? The elitist BS is so tiring!

Many people love these “great rooms.” I do too. My condo (1,800 sf 2-bed 2-bath, 23rd floor) in Tulsa was that way, a wide-open space with kitchen, island, living room and dining room all together. Someone had spent a lot of money combining two condos into one by taking out the separation wall through the length of the two condos, plus some other walls to create this “great room” with a balcony and glass doors across its entire width (they also created a large master bedroom suite). It was stunning, and I loved it.

The article tells you that most of the price decline was due to the price per square foot coming down, and it also tells you that Lennar targets the mass market, not higher end. And always has. It didn’t go down-market, it stayed where it was, but cut prices to where they had been, and those price cuts came mostly out of its obscene pandemic-era profit margins.

I have to point out the new home incentives to sellers and show how much it affects the buyers payment. Some sellers get it and some don’t. I also forward all the New homes in their area that go pending. In areas with new home communities the ratio is about 3 to 1 as far as sales. Buyers that bought a new home in the last year or so are going to have a rude awakening.

I saw their net margins appeared to go up slightly from what I saw vs the prior quarter. 8.9 vs 9.2% now or something. Did they go into any details about they were able to achieve that? I don’t follow them close enough to where I could decipher that also not sure I can say I 100% fully understand the difference gross vs net to be completely honest.

Lennar does not always, or at least DID not always ignore higher end housing. They were right in the top mix when the US Rep got a large tract in the south end of Manatee County address changed to Sarasota Co…

Lennar, and ALL the large residential builders I have dealt with over the last 50 years or so would change subcontractors for a dime,,, sometimes even less, so in a declining market such as these days, they could usually find a new sub in every trade to make that dime profit.

Does the house suffer? DUH!

The home needs a significant price cut (or incentives) to be affordable. Very rough affordability calculator estimates $110,000 household income for a $350k house to be affordable. Where this house is located, that is an abnormally high income. Even nationally with median household income around 75k, the house is not affordable.

Regarding you having a great room, if we’re talking about “how we grew up” being the ideal, I grew up in a house that cost about 61k (inflation-adjusted to today). My parents never paid a mortgage payment. Some of the money that would have gone to the bank was instead but into mutual funds for the kids, and we benefited enormously from that.

“if we’re talking about “how we grew up””

OK, I didn’t grow up with a great room, I grew up very modestly, with us three siblings in one small room (bunk bed and fold-away bed).

I bought that condo as an adult in my early 30s, when I was single. A developer had bought the whole 23rd floor of 12 condos at the peak of that local housing bubble and had made 6 condos out of them in the late 1980s at a very high cost, including those stunning great rooms — which was the latest and greatest concept back then. But he went bankrupt, the bank ended up with the condos, and I bought it from the bank at less than half of what it had lent on it, and then the bank collapsed, and two of my neighbors, including the one across the hall, whom I’d known since high school (and who shared the figures with me), bought theirs from the FDIC for about 20% less than I’d paid.

Great rooms have become very popular, and many high-end homes have them because they’re very social and make a lot of sense. They’re great for families and couples, they’re fun for entertaining, and it was awesome for me as a bachelor who was dating a lot and had dinner parties from time to time.

In a single-family house, great rooms require additional structural elements to span the large size without loadbearing walls. My condo tower was made of concrete, and the structural parts where columns and coffered ceilings, and the walls were not load-bearing, so taking them out didn’t affect the structural integrity of the building.

In the 80s when homes were cheap, they were like this. 1200 sq ft 3 bed 1 bath, 1 car garage, simple kitchen, laminate counters, linoleum in kitchen and bath, wall to wall cheap carpet. No AC, zero landscaping, shaped like a perfect rectangle, simplist roof possible, 1 small window per room. That still wasn’t a starter home, a starter home was a similar home just 30-40 years old and never updated, probably wearing it’s original roof. I think we need more really basic homes. There is nothing fancy about most apartments, but at least with a home on an apartment footprint you dont share walls and can build housing security.

Coming soon to many of the other big ticket items you purchase. “Sales volume was difficult to maintain and required additional incentives in order to achieve our expected pace and to avoid building excess inventory,”

The auto industry has been saying that for over two years, after the huge pandemic-era price spike, which is precisely why it cannot pass on the tariffs.

We are pretty much back to pre-pandemic business strategy. Bigger discounts, more incentives. Manufacturers are producing volume and creating more supply than demand. I was dreaming they would keep production low to keep margins high. Sell less, make more. Sigh. Dreamers can dream!

The classic car market has been slumping for a little less than a year. At least off 25%

Not with BMWs and Ferraris which are bringing record high prices these days.

Ha….. Interesting Point!

I know you’ll totally disagree with this, but MAYBE the auto manufacturers got advanced notice of the tariffs, and decided to act early by raising prices, therfore being able to say ‘the tariffs had no effect.’

LOL, this goofball conspiracy theories are really hilarious. Automakers CUT prices since the price-peak in mid-2022 when Biden was still President, and no one gave advance notice of tariffs then because no one was thinking about tariffs back then.

I posted this chart only a million times, roughly, most recently on Sep 11:

https://wolfstreet.com/2025/09/11/cpi-inflation-dishes-up-another-nasty-surprise-as-it-tends-to-do/

They can’t set their prices to anything they choose, they can only set to what you and everyone else will pay. And we basically figured out what that was and it’s now dropping with all the incentives coming out of the woodwork.

It’s a 100k for an H1B visa now. Possible RE market tanker in the SF Bay Area? I know a lot of owners are already entrenched in paid off homes or low mortgages, so I can’t imagine the impact will be too high.

That’s an interesting development to watch, in terms of the housing market. The $100,000 fee will not end high-end H1b recruits, but will likely slow the flow of people brought in on lower salaries that are hired to replace Americans as a cost-cutting measure. That’s not just a Bay Area phenomenon, but lots of companies do that, including utilities in their tech divisions. All kinds of scandals about that for years. Not sure if these lower-end recruits are a significant factor in the housing market.

I work in tech and was in f1 opt and h1b visas

Most of the h1b visas are to replace american workers with cheaper foreign workers and is heavily abused and lot of frauds and scams beyond a normal people’s wildest imagination.

Its a good first step but much more to do.

H1b is for best and brightest but it is not absurd by average tech workers to replace american workers.

They are, if you calculate how many housing units the the H-1B workers take up.

If this gets applied not just to H-1B but also to other visas you should expect a complete collapse in demand.

USCIS clarified, It will applicable to New H1B in 2026. It wont impact for existing H1B holders.

I’ve managed teams in the Bay Area and worked with employees who, in my view, were hired under h1b to replace American workers at lower salaries. For companies, it made sense: lower costs and higher retention. But at my current workplace, we no longer consider h1b applicants, even for transfers.

Looking ahead, I see two possible outcomes. First, reduced competition for American tech workers, which is great. Second, companies may increasingly move entire teams abroad, leading to more U.S. layoffs. It’s hard to predict which effect will dominate.

I think if it’s tech that can be handled by someone in India it most likely can also be handled by AI.

Outside of the freemoney era, should homebuilders generate double-digit margins?

I don’t know enough about the industry to know what a historical normal margin “should” be, but are double-digit margins typical? My first thought is “it seems high” as the barriers to entry into house construction aren’t that high.

That might imply that there might be room for a further ~10-15% discount just by reducing Lennar’s margins. With more room for further final sale discounts by squeezing the profits down for Lennar’s suppliers. (I’d assume if Lennar is making 17% margins, their suppliers are creating something similar, so room to squeeze them too?) So plenty more room for lowered sales prices from here?

Isn’t that entirely for the free market for housing in the US to decide?

Sure, pending the price of money.

If interest rates go higher, then housing prices have to go lower to get the sign-off for the mortgages to do the deals. (Payments vs income being what they have to be.)

Lennar having such high margins suggests that there’s plenty of room for discounts to move inventory if mortgage interest rates climb.

Interesting that…

Yes, there is room for bigger discounts, as you can tell by Lennar’s profits, they’re down, but they’re still substantial.

Next thing you know they will want profit margin similar to META or Apple.

I don’t consider Lennar a builder, so yes the barriers to entry are extremely low. Digital marketing, land purchases, design/architecture, and project management are their forte.

I can’t wait until there’s an app that connects buyers with subcontractors, and coordinates the project management with the bank for draws. “Builders” like Lennar already charge a hefty fee for this service and deliver shoddy homes.

Let the app figure out pricing with the bank instead of having a middleman like Lennar tell the bank one price, the subcontractor another price, and call the difference profit.

We are living through the

Great Housing Abomination, which will make ‘Housing Bubble 1” look like child’s play, or a walk in the park. We are only beginning to see the fallout of this monstrosity.

The way things are going, they are going to be praying for another crisis to jumpstart the industry

Curious, anyone know what Lennar’s return on capital employed is at their current 17% margin rate?

Better review Finviz or some scanner for what you need, but I see RIOC @ 12.05%, with operating margin @ 11.26%, gross margin @ 20.60% — not sure if that’s updated??

Bonus: The recent trend in Lennar’s operating and gross margins suggests that its EBITDA is likely decreasing, which would cause its EV/EBITDA multiple to increase (meaning the company’s enterprise value is higher relative to its operating earnings).

Redundant

“…suggests that its EBITDA is likely decreasing,”

LOL…

1. What did I tell you in the very first paragraph???? You should at least read the first paragraph before you comment here. It says:

“Revenues from homebuilding fell 8.8% year-over-year in Q3, incentives needed to make those deals jumped to 14.3% per home sold, which slashed its gross margin to 17.5% in Q3, from 22.5% a year ago. Operating earnings from homebuilding plunged by 49%, net income plunged by 50%, and earnings per share plunged by 46%.”

2. Do you ever look at financial statements — instead of “scanners”? My figures are from their financial statement. Their financial statement says that EBIT plunged by 47%. All you have to do is look at it.

Re: Do you ever look at financial statements

I gave that up a long time ago — also bypassing the golden rule to RTGDFA: but, I did initially read it (all) then, blew it by not re-RTGDFA.

I’m a slow learner — no doubt about it!

The basics of today’s financial statements are really easy to read. You skip all the verbiage and scroll down to the tables. They have current quarter and the same quarter a year ago, for all line items, sometimes they include the percentage change, and sometimes you have to figure it yourself. They also have a lot of other interesting stuff, such as average home prices in the quarter. You can download the financial statements from the company’s site or from the SEC’s Edgar database (which is what I use), which is searchable by ticker (Lennar = LEN).

Kile, ~15% thru full business lifecycle. Recent years’ ROIC is at https://www.gurufocus.com/term/roce/LEN

It is all about location, location, and location! If you don’t live in an anthill, you have many choices and renting can be a sweet deal for both parties.

Screw dei, I chose guys with good skills and have an understanding if you don’t bother me, I will not change the rent or worry about details.

Around here there is zero unenployment for guys willing to sweat and acreage means you can hunt.

I expect out of the city limits to gain in value. Can you walk around your home at midnight and feel safe? Can you walk in your yard and not see another home?

All the talk about boomers is bs. Sure I could take a dirt nap today or 20 years from now! Kids could sell or keep paid for rentals that will go up in value!

Seen several new homes in Dallas last week. Quality could be problem. You may want to know how are they cutting costs?

A “home” is a building whose eventual value = $0. And only the land has value. That’s why these homes that were built decades ago get sold for land value, razed, and replaced by new construction. The structures are worthless. People who complain about “quality of construction” today should know that. The entire housing stock gets renewed that way over time. Only a relatively small number of historic homes are maintained at a very high expense. I understand that your house is different, that it’s timeless and will last forever, but that’s an illusion. Only your land has lasting value.

So you think a 3500 sf lot in San Fran is worth $2 Million? 🤬. What variety of Mary-Jane are they smokin’ in San Fran these days?

It’s worth what a buyer will pay for it.

The office tower on 201 California just sold for $57 million, a 75% discount from the last transaction price before the pandemic. So it sold essentially for land value. It sits on about 0.41 acres, or about 18,000 square feet. So land value pencils out to be about $11,080,000 per 3,500 square feet — to use your lot size. And yes, someone was willing to pay that. Location, location, location.

If that tower gets torn down and redeveloped, it won’t be into single-family housing. It’ll be another tower for multifamily housing. Another option might be converting it to multifamily at a huge expense. They’ll do whatever is cheaper. Another option is to spend a huge amount of money to fix it up as an office building, and rent out for less current rates to fill it up, but that too is a tough project, given vacancy rates of over 30%.

Location, lot, structure, in that order.

In response to Wilf’s reply above – your calculator is broken. At that price (the price you quoted for 3500 sf lot), i would be driving truckloads of federal reserve notes up your way to buy all the land I could! It should say

$11,176,470 for a 3500 sf lot! You need to multiply your number by $1000.

Do you need a fresh cup of coffee, Wolf? 😂 (I based it on the numbers you provided.)

F that, I’ll go check out real estate prices on Mars!

Nah, I don’t need a calculator for this stuff, I do that in my head. I crunch numbers likes other crunch cereal. I do need typo-control because I write these comments very fast, and stuff gets dropped.

My comment that you reference:

“The office tower on 201 California just sold for $57 million, a 75% discount from the last transaction price before the pandemic. So it sold essentially for land value. It sits on about 0.41 acres, or about 18,000 square feet. So land value pencils out to be about $11,080 per 3,500 square feet — to use your lot size. And yes, someone was willing to pay that. Location, location, location.”

18,000 square feet sold for $57 million = $3,167 per square foot. A 3,500 square foot lot times $3,200 per square foot = $11,080,000

But as was clear from the context – to which I replied….

“So you think a 3500 sf lot in San Fran is worth $2 Million?”

… that I did forget to write down the last three digits in the heat of the battle, should have been “$11,080,000 per 3,500 square feet”

Which I now corrected.

Any idea of the average age of existing homes? A relative lives in Longbeach and his million plus 1000 sf shack has to be from the fifties.

Someone is going to buy it eventually and tear it down.

This is good. Responding to market forces.

In the Phoenix metro all the new neighborhoods are around the far periphery. Only MFH is being built within 20-30 miles of the downtown cores of Phoenix, Tempe, Scottsdale. There is a lot of new employment going in around the edges too, and if you work there and your kids go to school nearby then maybe one of these cheaper new builds makes sense. If you work in downtown Scottsdale you either pay the “better located used house” price or you drive an hour each way every day. America is the land of choices.

I was listening to a guy who does internet videos, and he said exactly what I think – we DO NOT NEED interest rates to come down, we NEED HOME PRICES to COME DOWN. So true.

Sure, when prices are low or normal, having attractive interest rates will make homes more affordable, but now that we are amongst the mother of all housing bubbles, lower rates WON’T FIX ANTHING. It will be interesting, moving forward, to see how this housing monstrosity does respond to lower rates.

The creation of this current housing monstrosity is a lot like creating a Frankenstein monster. We have seen the good side of the housing monster – (previous) boom in construction, and overall wealth effect with homeowners. We are now seeing one of the bad personality traits – homes have become unaffordable for most people. We may wake up one day soon and find that this franken- monster housing market has become our worst nightmare.

People who have vested interest in real Estate are clamoring for low rates and they don’t think high prices are the problem.

People who are on the other side are clamoring for lower prices saying high price is the problem.

Many people who are objective know that high prices not high rates are the problem.

A lot of people here, who are invested in real estate have a one more take: Prices won’t go up but wont go down from their historic highs!

Those guy’s who do internet videos have a tendency to say exactly what you think, careful with them.