With US debt issuance threatening to blow all fuses, foreign demand is an increasingly important question.

By Wolf Richter for WOLF STREET.

The US government’s recklessly ballooning debt has now reached $37.5 trillion. High on our worry list: Will foreign investors continue to buy this debt, or will even more of it have to be absorbed by US domestic investors?

If there is lackadaisical demand for this debt, yields rise until enough demand materializes. The US government will always be able to sell this debt, but at what yield?

If foreign investors are less than enthusiastic about buying US Treasury debt, it will put upward pressure on yields. And these yields affect private sector interest rates, such as mortgage rates.

But for now, longer-term Treasury yields are relatively low – the 10-year yield is barely above 4% – despite the potential inflation trajectory and the flood of new supply coming on the market that has to be absorbed by investors. It shows that for now there is still plenty of demand for this debt.

But the risk of foreign investors losing interest in Treasury debt and even just maintaining their holdings, rather than increasing them, would put upward pressure on yields, and this possibility is high up on our worry list, which is why we keep an eye on it.

Some countries — including the two that used to be by far the biggest foreign investors in Treasuries — have either been reducing their holdings or roughly maintaining them. But other countries have taken their place and have massively increased their holdings. So here they are.

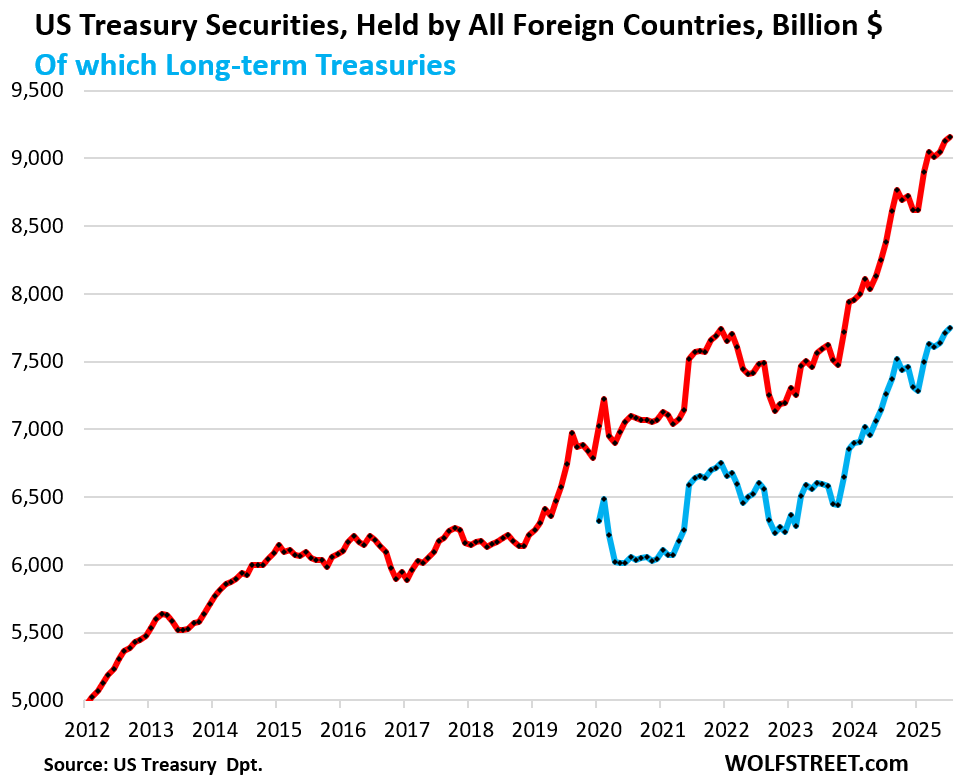

All foreign investors combined piled on another $31 billion of Treasury securities in July, to bring the total pile to a record $9.16 trillion, according to Treasury Department data today. Over the past 12 months, they piled on $778 billion (red line in the chart below).

Of that total, $7.75 trillion (85%) were long-term Treasury securities (blue), and the rest were short-term T-bills.

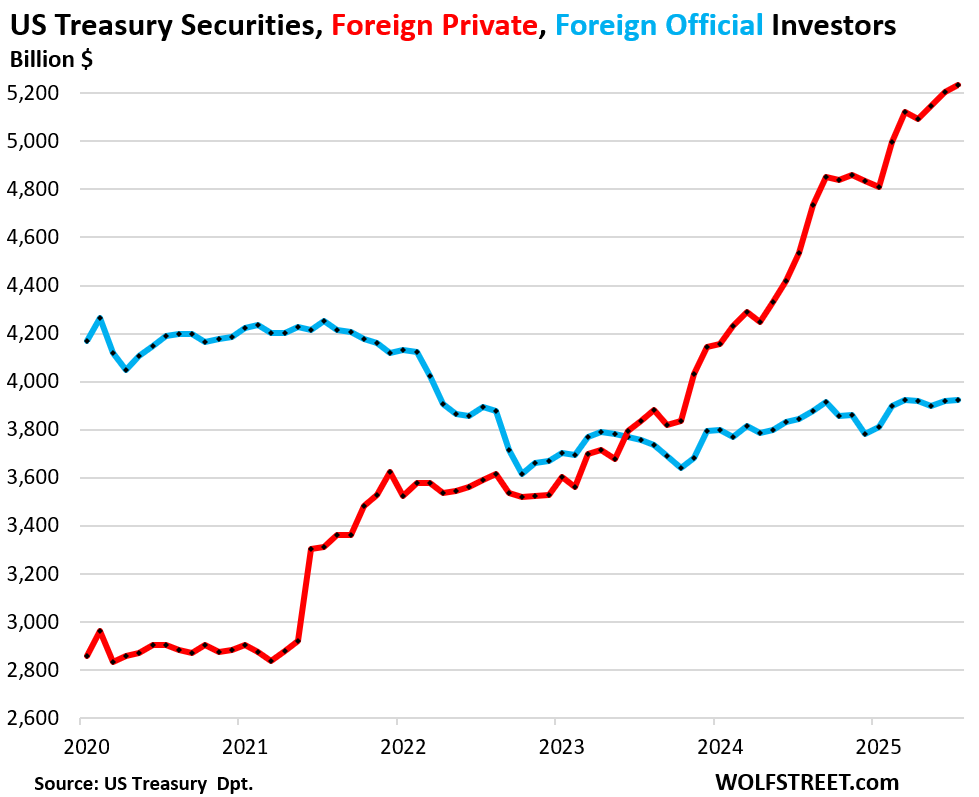

Private foreign investors have done most of the heavy lifting. These financial firms, companies, bond funds, individuals, etc., in foreign countries increased their Treasury holdings by $29 billion in July to a record $5.23 trillion (red in the chart below).

But “foreign official” holders, such as central banks and government entities, have shown less enthusiasm. Their holdings barely ticked up in July, to $3.92 trillion, and were down from years earlier (blue).

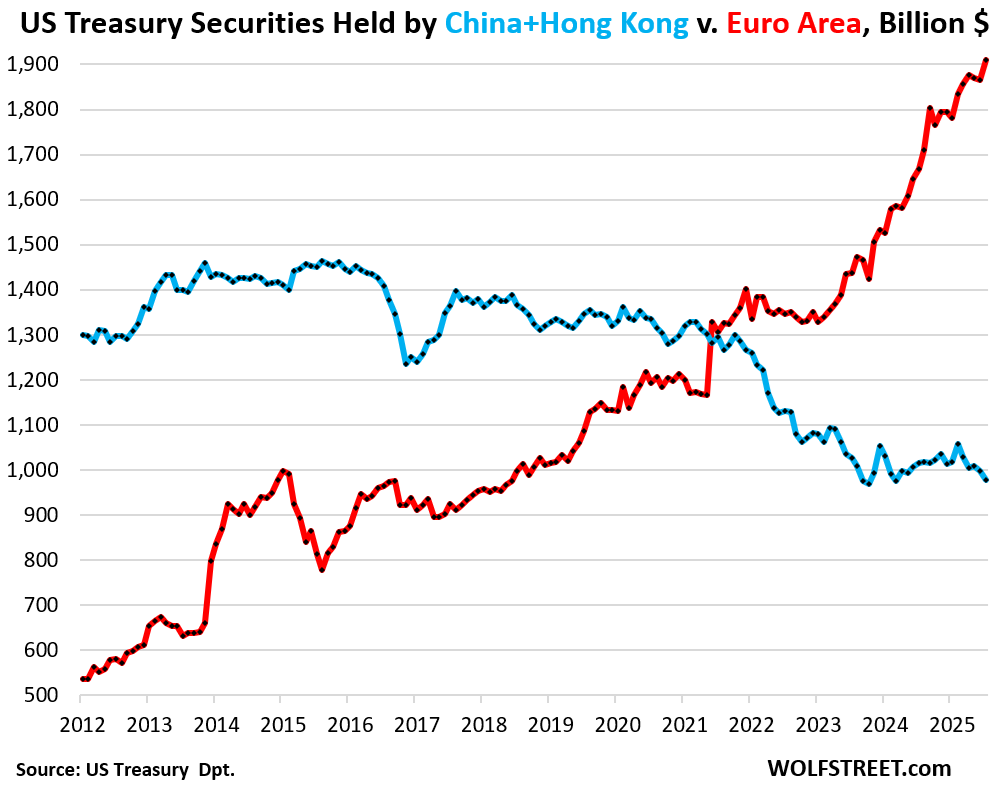

China and Hong Kong versus the Euro Area.

China and Hong Kong combined shed $20 billion in July, and $37 billion in the 12-month period, bringing their holdings to $979 billion (blue in the chart below).

The Euro Area continued to load up on Treasury securities, adding $44 billion in July and $242 billion over the past 12 months, bringing their holdings to $1.91 trillion (red).

The biggest holders in the Euro Area are the financial centers (Luxembourg, Ireland, Belgium) and France, whose banking system also functions as a global financial center. Their combined holdings accounted for 81% of the Euro Area’s total holdings. More in a moment.

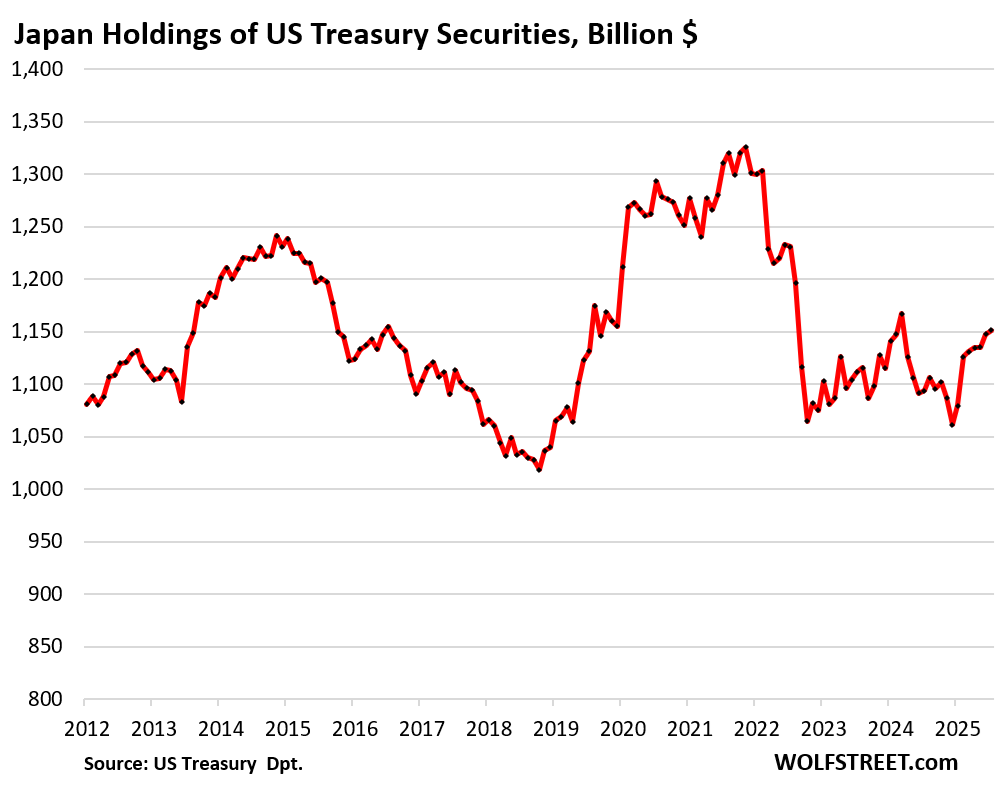

Japan’s holdings of Treasury securities rose by $4 billion in July, and by $58 billion over the 12-month period.

Japan’s holdings haven’t gone anywhere in 12 years despite the large fluctuations in between.

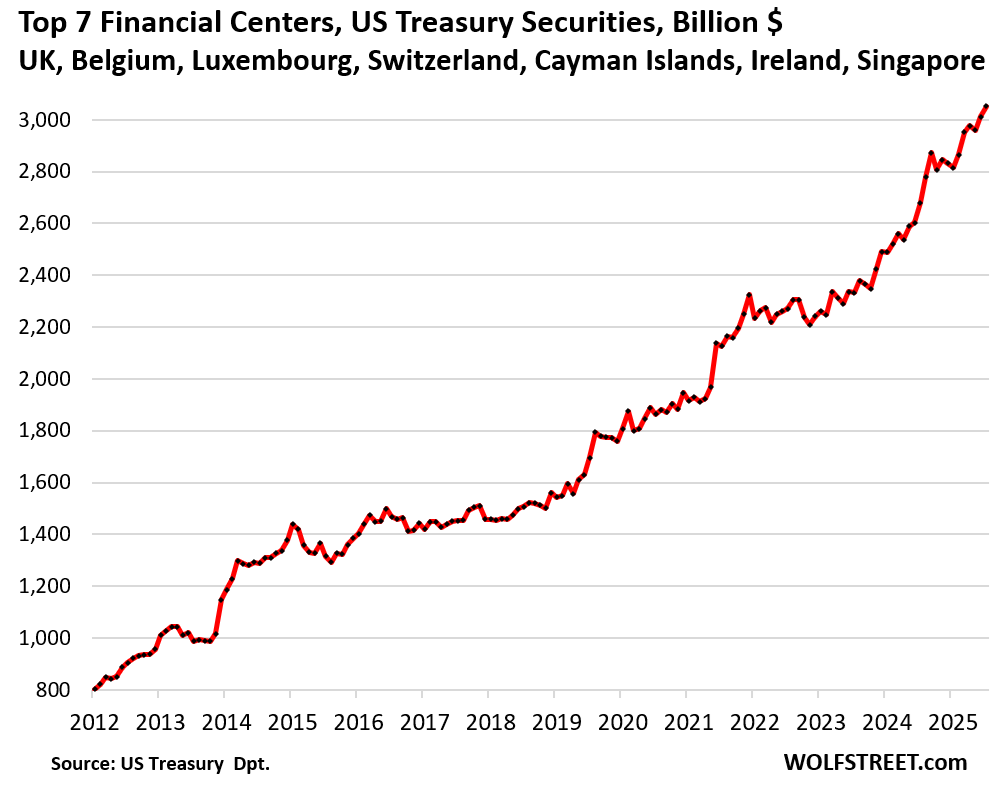

The seven largest financial centers have massively piled on Treasuries over the years, more than doubling their holdings over the past 10 years. In July, they added $41 billion, and over the past 12 months $373 billion, bringing their total to $3.05 trillion.

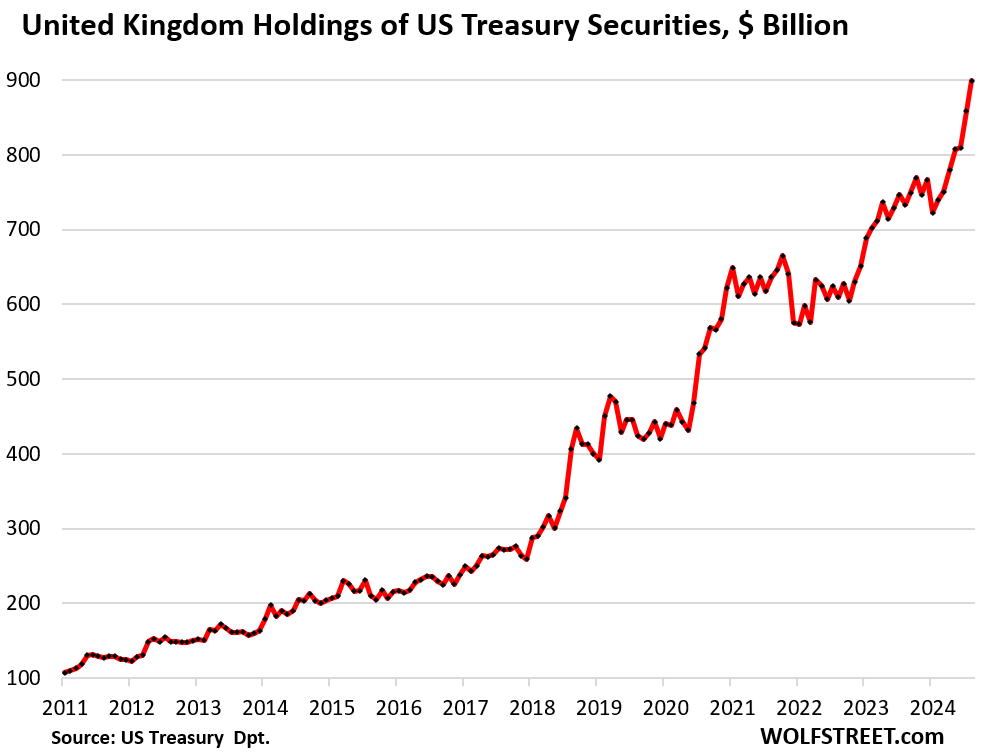

A portion of the holdings at these financial centers are held by US entities. These countries specialize in handling the financial holdings of global companies, individuals, and governments. Ireland is a favorite for US Big Pharma and Big Tech to store their profits. Belgium is home to Euroclear, which has $40 trillion in assets under custody for companies, governments, and wealthy individuals around the world. The United Kingdom here means the “City of London,” the top financial center in the world.

Changes in July, and total Treasury holdings:

- United Kingdom: +$41 billion, to $899 billion

- Cayman Islands: -$4 billion to $439 billion

- Belgium: -$5 billion to $428 billion

- Luxembourg: +$0.4 billion, to $428 billion

- Ireland: +$7 billion to $324 billion

- Switzerland: +$2 billion to $303 billion

- Singapore: -$1 billion to $254 billion.

The United Kingdom — so the “City of London” financial center — is by far the biggest financial center of the seven, and globally, and its Treasury holdings have spiked over the past two months by nearly $100 billion:

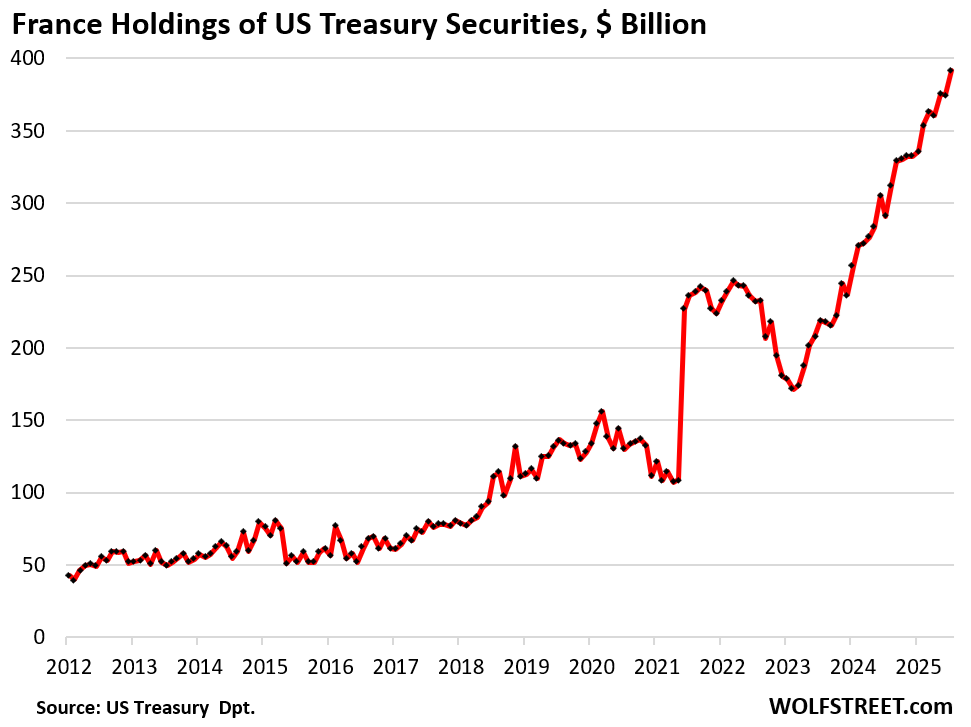

France’s holdings rose by $17 billion in July, and by $101 billion from a year ago, to a record $392 billion. France’s megabanks are global financial centers.

Canada’s holdings have been gyrating up and down all year. In July, they plunged by $57 billion from the record in June, to $381 billion.

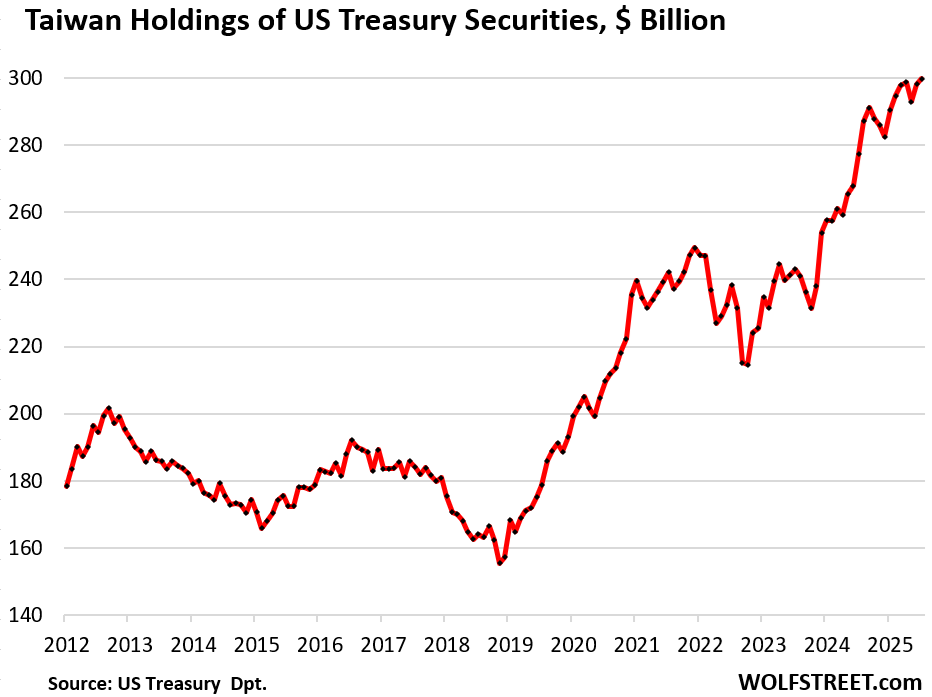

Taiwan’s holdings rose by $7 billion in July to a record $300 billion, and were up by $22 billion year-over-year:

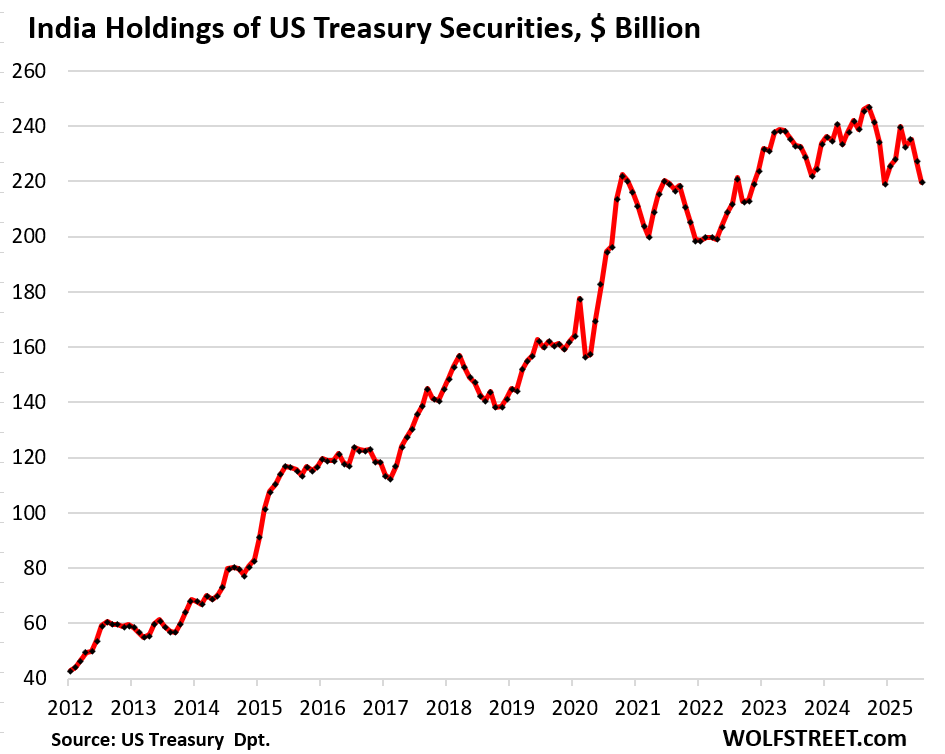

India has been unloading for the second month in a row. In July, its holdings dropped by $8 billion and year-over-year by $19 billion, to $220 billion. The high was in September 2024 at $247 billion:

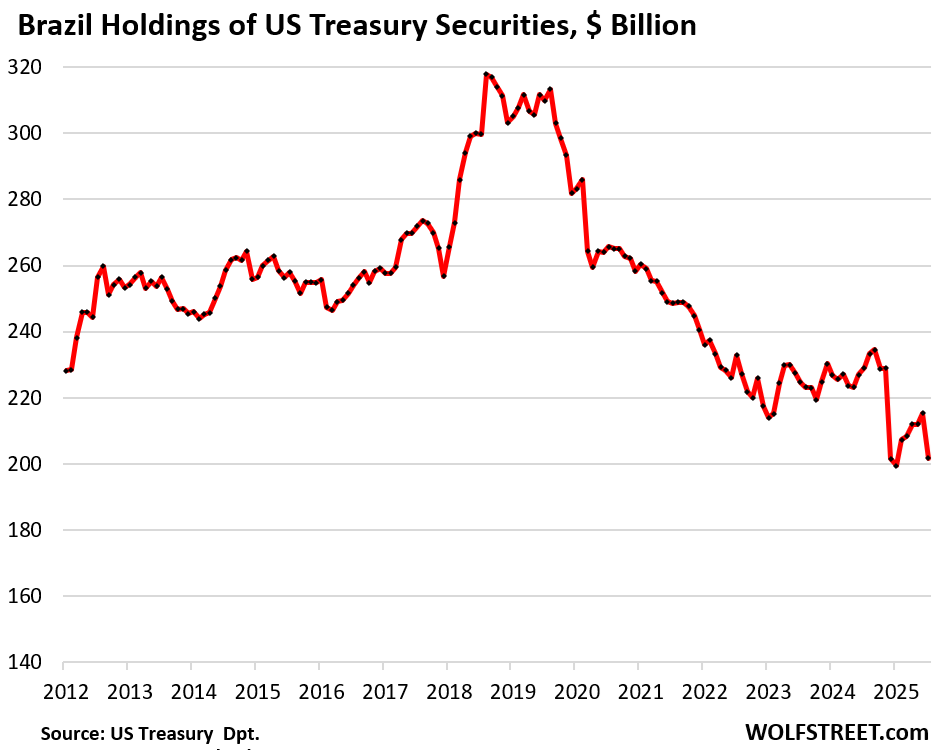

Brazil’s holdings have long careened lower and in July plunged by $14 billion and year-over-year by $27 billion, to $202 billion. Since the peak in 2018 ($318 billion), Brazil’s holdings have dropped by 36%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: Treasury yields rise after Fed rate cut, with Powell’s FOMC in no ‘sprint’ to loosen policy

U.S. debt is too big to fail?

The US debt cannot fail by definition because the US controls the currency in which the debt is issued, and in theory, it can always print more to services this debt.

The issue is yields and inflation.

Thus when foreign investors have had enough, the Fed will buy what they have to.

By this logic, Russia or Argentina couldn’t fail either, but they did.

Good lordy, they NEVER defaulted on debt issued in their own currency. They defaulted on debt issued in foreign currency (USD mostly), because they can print their own currency and thus will not default, but they cannot print foreign currency. So when they ran out of foreign currency to service their foreign currency debts, they defaulted on that foreign currency debt.

The US has no foreign currency debt.

Alku,

Wolf is right about the point he makes…

But you are right in terms of how *controlling/lowering interest rates by printing money* can destroy an economy pretty effectively (as you say, see Argentina and a long list of other countries).

1) Countries in perpetual fiscal deficit (banana republics and cough, cough, US)

2) naturally see a rise in their interest rates (as lenders watch the national debt-to-GDP number relentlessly rise and demand a higher return, aka interest rates).

3) To “fix” their perpetual deficit/spiking interest rate problems, (rather than *ever* limit Gvt spending) these banana republics (see also, US) print essentially unbacked money via their central banks,

4) with which to buy their own Treasury debt – at whatever lower interest rate they are aiming for (substituting the central bank for independent, economically oriented private lenders.

5) But there is no free lunch – printing money to obscure the consequences of perpetual fiscal deficits simply converts a “too high interest rate” problem into an *inflation* problem,

6) Because the ratio of real assets-to-printed money definitionally worsens every time a central bank simply prints money.

The dishonest MMT’ers like to say “Countries can never go broke” (because they can print an infinite amount of money to buy infinite amounts of government debt).

But the Wormtongues of the MMT *know* that what people really mean when they object to MMT is that national economies can be ruined through money printing/MMT) – not just in the narrow sense of “bankruptcy”.

The banana republics destroyed themselves via money printing/inflation very effectively.

On the inflation front, supply or lack of it invents inflation. To few goods chasing a higher demand. The U.S., private and public investment should be looking to increase the long-term available supply, be it in goods or services.

Overabundance of supply lowers the cost to the end user, not a bad thing for Treasury yields. Yields are lower when there is abundant savings investors want in save keeping. The U.S. bond and Bill holdings are about as safe as it gets in our world.

The Federal Reserve Bank is the buyer of government debt as the final security in the trust in the dollar. The F.R.B. can roll off/ destroy that U.S. “debt” at will, making that debt more attractive to private and foreign investment.

“Overabundance of supply lowers the cost to the end user,”

Overabundance is exactly what reigns in the US economy: shelves are full, warehouses are full, trucks are constantly delivering new stuff, services have unlimited supply, there is unlimited amounts of streaming and health insurance you can buy. The US economy has always operated on overabundance, and marketing and advertising have to be used to push sales. The only broad exception in my lifetime was during the pandemic when a bunch of goods were suddenly in short supply. In a very limited way, there was a shortage in the early 1970s during the oil shock, but if you lived in Oklahoma and Texas at the time, as I did, there was no oil shock either, because crude oil was produced and refined there, and money was gushing everywhere because the price of oil had spiked, the pot holes in the streets were filled with cash. Those were the good times.

“The F.R.B. can roll off/ destroy that U.S. “debt” at will, making that debt more attractive to private and foreign investment.”

There is no such thing as a free lunch.

How exactly does the FRB *acquire/buy* that ever-engorging US fiscal debt – which magically disappears?

By printing incrementally unbacked money.

So the ratio of US “money” to US real assets (from real estate to a can of peas) definitionally increases.

*That* is inflation.

And it isn’t harmless – particularly when it is perpetually used to enable the perpetual delusionary deficit spending of a government.

If deficit spending “worked” in an economic (sh*t, even Keynesian) sense then the economy would *grow itself out of deficit spending* = as the “stimulated” economy’s faster GDP growth would increase tax revenues – balancing the Gvt budget.

*Perpetual* fiscal deficits indicate that something has gone horribly, horribly wrong.

and exchange rates.

What are they purchasing, Wolf Man? I’d call it lending the town drunk money, hoping they’ll get paid back in scrip that someone else will accept as payment for good and services, and hoping that the scrip isn’t completely devalued.

In a way, aren’t they ‘purchasing’ risk?

The US 10-year: Return free risk – Grant’s Interest Rate Observer.

Coined during the non-inflationary ZIRP/ NIRP era, before the yield hit the all time low of 0.33% (on the chart) in 2020.

Even after rising by 10-15x since then: If the shoe fits…

“Risk free” refers to the credit/default risk. Treasuries are “risk free” in that sense because you WILL get your principal and interest, and there will not be a default.

But bonds have other risks:

Interest rate risk, which is where interest rates rise and the market value years before the bond matures drops substantially. But the market value rises again by definition as the bond approaches maturity, and on maturity date, market value = face value because the holder gets the face value plus remaining interest. So if you hold bonds to maturity, you don’t feel the interest-rate risk because you get paid your principal and all your interest.

Inflation risk, which is where the coupon interest that you get may not be enough to compensate you for the loss of purchasing power due to higher-than-expected inflation.

There are other risks, such as liquidity risks, call risks, etc. depending on the bond. 10-year Treasuries have zero call risk because they’re not callable, and low liquidity risks. Callable bonds are a special breed, and the call feature is always disclosed.

It’s an interest-paying store of wealth in US dollars. If you live in a foreign country and you have income in local currency, but financial obligations (or aspirations) in US dollars then you need to store your income in US dollars. If you live in Turkey and don’t trust your local currency, then you need a better shell hole. It’s not just the yield, but the currency that matters.

“If you live in Turkey and don’t trust your local currency, then you need a better shell hole. It’s not just the yield, but the currency that matters.”

Agreed.

Now, if you don’t the US government (35 trillion federal debt after 55 years of deficits) you…

“You don’t understand. Those were trading sardines, not eating sardines”.

A huge conundrum is the absurdity related to investors viewing U.S. Treasuries as the world’s most secure asset — as the U.S. admin is working nonstop in engineering global instability and uncertainty.

This entire game of trading sardines isn’t making sense, because, in theory, yields have been declining as issuance explodes — and the nuclear radiation of issuance spreads wider, yet, the sardine traders are happy to pay higher prices for a chance to grab treasuries that have less future value.

The magic hype of stablecoins potential may be creating a mutated secondary mkt dynamic — but I see that as nothing more than sardine cans spinning in circles at a circus. There eventually will be some institutional digital transactions, but widespread adoption on main street is unlikely.

If traders are accumulating treasury inventory to play that game, maybe it stimulates short term demand, but if the supply of treasuries is being diluted by more issuance, then, I assume lots of bag holders will get burned (stablecoin bailout warning).

The 4-d checkers game here is crazy — seems that lingering, drifting tariff impact in the next few months will be inflationary — which seems like yields go up, but then maybe more rate cuts push yields lower.

And, backdrop of slowing overall economy, as AI explodes — friggn confusing puzzle!

” I assume lots of bag holders will get burned (stablecoin bailout warning).”

Which touches on the question that has been bouncing around.

IF there is a Crypto crisis, does the Fed intervene……and how?

Cryptos must currently be involved in collateral and leveraging. A few things could cause a domino tumbling event. Should the Fed intervene or let the chips drop where they may?

Micro mackerels?

US treasuries are not seen as the safest asset in the world. Many bonds issuers have lower rates.

Crypto, like the tech sector, is one of those perpetual bubble machines. There have been boom and bust cycles of tech throughout all stock market history. Some were absurd on their face (like the *coin replays, others absurd on valuations.) No one can predict when they’ll pop as they depend on fools and there are a lot of fools with money.

Overall the broader tech bubble continues to inflate. It always feels like forever when you are in one.

Redundant,

Stable coins are not hype. The combined total of stablecoin transactions has already exceeded the combined total of Visa and MasterCard transactions. That crossover happened last year.

Nearly all of those transactions are trades within the crypto world, to get in and out of other cryptos, because it’s hard to convert crypto back into dollars. Almost none are commercial transactions, though if you google around long enough you might find that someone actually did buy something with a stable coin and then that made the national news? You will also find reports of illicit transactions, but also withing the crypto world.

Why are there so many fees and runarounds to sell a crypto in a secure wallet?

It’s like 20% or more of the crypto transaction is in fees, and another 10-25% in premiums, regardless of amount in many cases.

And people complain about a $2.00 convenience charge on a $200 withdrawal.

2 of the BRICS are selling

The BRICS are already irrelevant with regards to Treasuries except the C.

Europe is worried about a Russian invasion, Taiwan about a Chinese invasion. If I lived in Europe or Taiwan I would want a big chunk of my money overseas. Note that Japan, India, and Brazil are a lot less interested in buying Treasuries.

I live in Europe and definitely don’t want more than 20% of my wealth in the US (dollars). Today everything is OK. Tomorrow i can’t get my dollars back over here, because of what my government might have done wrong in the eyes of the “almighty”. And as i do, so do many others.

You can’t bully others into submission and expect they like you for doing it.

Quietly they will seek other, more reliable friends.

Meanwhile the US dollars buy 10% less Euro’s than last year. So that’s no good to me too.

And that talk about a Russian invasion is just talk. If the Russians had the ability to do so, there would be no Ukraine today.

Russia is not going to Europe.

They’re heading south.

Agreed.

This is scared money getting out of a Europe that is about to go sideways.

Japan is the largest foreign holder of US treasuries, and they’ve held over $1t of them for over 12 years.

How do you think they replenish their maturing holdings for the past decade if they are not buying more?

The cleanest dirty shirt in the laundry?

Just pay no attention to all the holes in it or the fact it is being altered from size XXL to XXXXL.

Not so much these days

US treasuries are not seen as the safest asset in the world. Many bonds issuers have lower rates.

Crypto, like the tech sector, is one of those perpetual bubble machines. There have been boom and bust cycles of tech throughout all stock market history. Some were absurd on their face (like the *coin replays, others absurd on valuations.) No one can predict when they’ll pop as they depend on fools and there are a lot of fools with money.

Overall the broader tech bubble continues to inflate. It always feels like forever when you are in one.

Here’s what’s happening in the UK

The yield on 10-year bonds rose two basis points to 4.70%, while the 30-year rate rose three basis points to 5.54%.

Kinda related to yesterdays rate cut post and the way foreign buyers of treasury debt is the following curiosity:

As of September 19, 2025, the Bernanke-Taylor rule implies a target federal funds rate result of approximately 4.5% to 5.0%. This contrasts with the Federal Reserve’s current policy, which recently lowered the federal funds rate target to a range of 4.0% to 4.25%.

In my mind, the more uncertainty and confusion about the level, price or rate, everyone will be more cautious about what’s real and what’s reliable — what’s safe, accurate, stable — if all our financial metrics become more chaotic, buyers will be far less willing to part with cash for investing. The safe haven of treasury instruments or dollar is definitely more suspect today.

Maybe I missed it in the article, but percentage wise, how much of new issuance has been absorbed by foreign VS domestic?

This is the real question I also got from this article: “how much of new issuance has been absorbed by foreign VS domestic?”

The foreign participation in the auctions has been fairly typical over the past two years. You can look this up on the Treasury’s website and download the Auction Allotment reports.

In addition, foreign investors are heavy buyers in the secondary market because their needs don’t necessarily match with the auction schedules, and they can buy what they want in the secondary market. This buying in the secondary market is why holdings have increased.

The dollar amounts purchased have remained roughly stable. As US issuance has increased, the percentage share has fallen over the years.

I only have the data back to 2022. But so don’t take 2022 as normal. During pandemic mega-QE, the Fed (SOMA) bought huge amounts at auctions, and so that caused the foreign percentage of what was sold to the public (non-SOMA) to shoot up, even though the dollar purchases didn’t change much. See both charts below. If you compare to 2019, today’s percentages look more in line.

Here are the last few auctions in the most recent Allotment report. Foreign purchases as a percentage of issuance:

Since very few people read my articles foreign purchases, I stopped writing them. People don’t like to hear that actually, foreign participation is OK.

Wolf,

Big fan of your column and also big fan of discussion board where we see vies from folks all over America and your answers to questions. Is it possible to modify discussion thread such that it becomes First Come First Publish. It is very difficult to track comments when folks reply to comments from other members. I hope there is a better system out there where comments can be filtered or some way of segregating so you are not reading same comments again. I like to read comments as they come and not wait for 3-4 days. Just a suggestion to further enhance the experience of your website.

AR,

What you see is what you get, LOL.

But…

1. I encourage all commenters, and I try to remember it myself: always add the screen name of the person you’re replying to. This makes it easier to figure out who this was a reply to.

2. There is a time stamp on each comment under the screen name, so you can tell what’s new, and which came first.

3. Note the nested replies: The original comment and then three levels of replies/replies-to-replies deep.

AR,

If you read through the comments under an article on 9/19, return the next day and Ctrl F “Sep 20.” The next day, “Sep 21.” It makes it easier to filter new responses. I do this all the time.

I am a bit baffled about international purchases of US government debt. The bonds yield somewhere around 4 per cent in US$. The dollar has been dropping in value, so the yield would seem negative in many cases. What do I not understand?

One would expect the BRICS to be diversifying their reserves to safeguard against sanctions ala Russia. Seems the rest of the large developed world is still finding more security with the US$. This divide could suggest a currency war. It would be interesting to know how much of the reduced Treasury buying is being channeled into gold reserves.

The huge inflow of money from the UK and Cayman islands makes me wonder if this is “fast money” they may sell their Treasuries the second their algos tell them to, vs. the previous investments by foreign central banks. Will we see more turmoil in US Treasury prices going forward?

Darn good thing they don’t live here, you know as to know in what the real shape is of what they’re invested in. Because you couldn’t possibly spend as little as a day in this nation and reasonably invest long term in it. There is much heartbreak for many of you reading this, because you know it’s true, not just a random chime in. It shows up in every stat the Gov will still allow to be made.

An interesting question will be on the ballot in the most populous US state, a question which may become more and more important and seen in more states going forward.

I’ve spent a lot of time in Taiwan the past two years. Taiwan’s interest rates have been around 2%. So, many banks were offering great CD rates (5%) on USD accounts. Money was also flowing to ETFs with US equity exposure. In early May, the New Taiwan Dollar was devalued dramatically (>10%) over the period of a week following a meeting with the current US administration. A lot of people and businesses got hit hard. However, if you weren’t part of this camp, it’s now a great time to by long term US debt!

To put it in context, one should also look at what’s happening in the dollar.

It’s gradual, but this is what actual decline of the nation looks like relative to its peers. America First. What a joke.

what decline of the dollar?