The 6-month PCE price index accelerated to 2.8% annualized, despite dropping energy prices. It’s been 2.7% to 3.3% in 2025, sharply higher than in the 2nd half of 2024.

By Wolf Richter for WOLF STREET.

The inflation measure released today for May – the overall PCE price index favored by the Fed as yardstick for its inflation target – re-accelerated month-to-month and year-over-year, despite the steep drop in the components for energy.

The “core” PCE price index, which excludes the food and energy components, also re-accelerated month-to-month and year-over-year.

The year-over-year readings of both the overall PCE price index and the core PCE price index moved further away from the Fed’s 2% target.

There are still no signs in the inflation data that the new tariffs are getting passed to consumers. If that happens in future months, and to whatever extent it might happen, it would add to inflation.

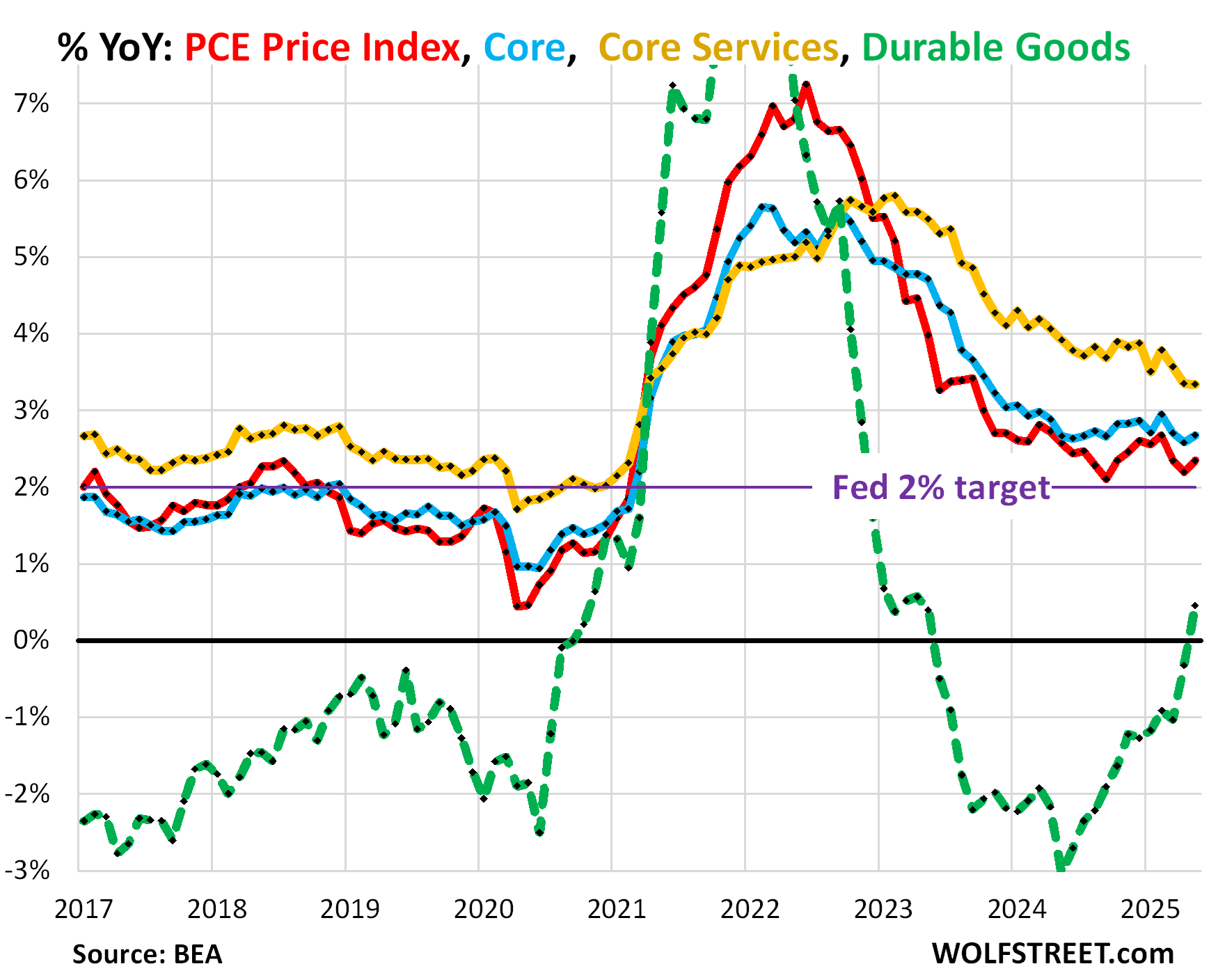

On a year-over-year basis in May:

- Overall PCE price index (red): +2.3%, despite the plunging PCE price index for energy. The Fed’s target is 2.0% (purple).

- Core PCE price index (blue): +2.7%.

- Core Services PCE price index (gold): +3.3%.

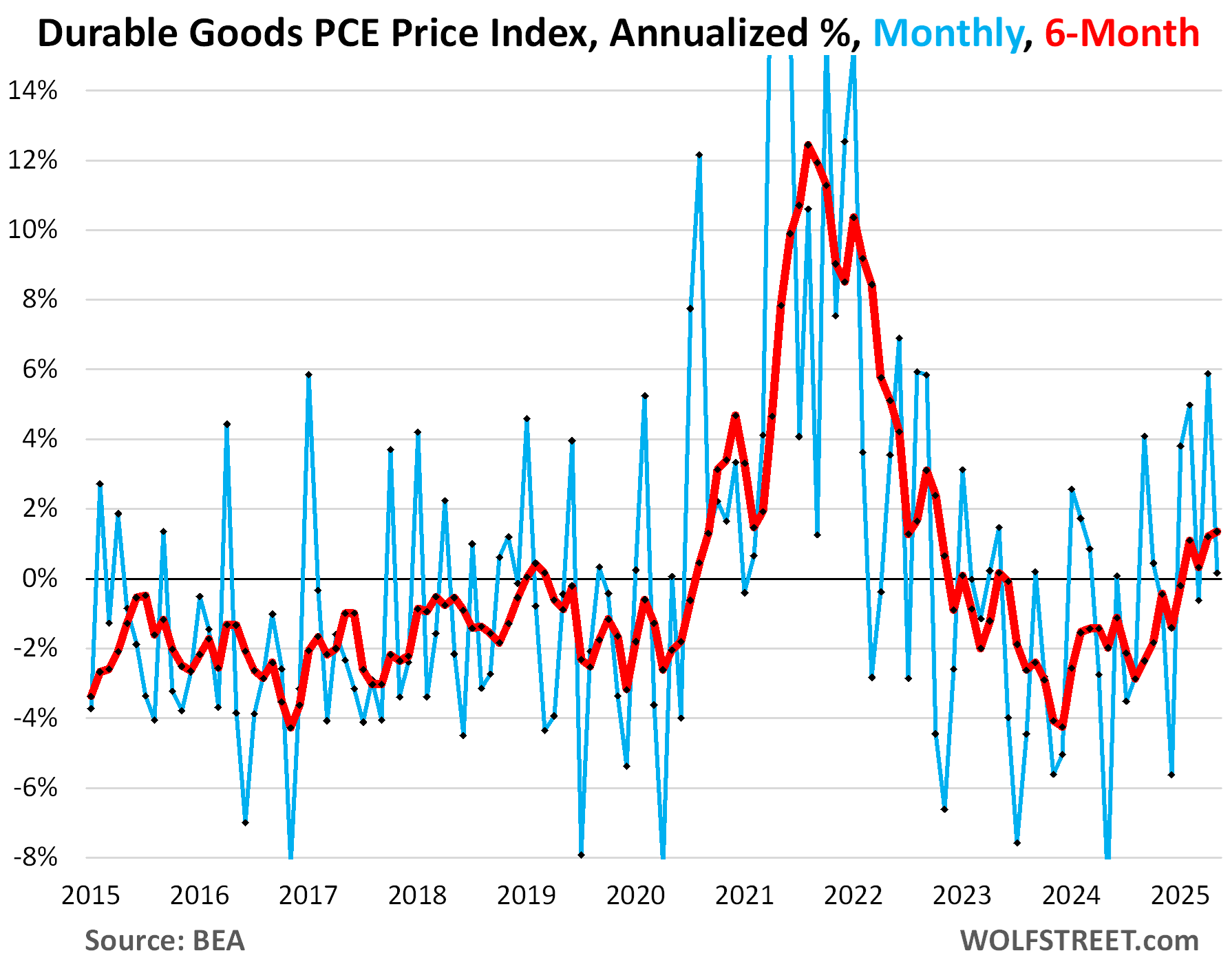

- Durable goods PCE price index (dotted green): +0.5%, first positive year-over-year reading since May 2023, continuing the bounce-back that started a year ago after the big plunge in 2022 and 2023 (but month over month, the change was 0% in May, indicating that tariffs have not yet been passed on to consumers. The CPI data for May had already pointed that out).

Month-over-month and on a 6-month basis in May:

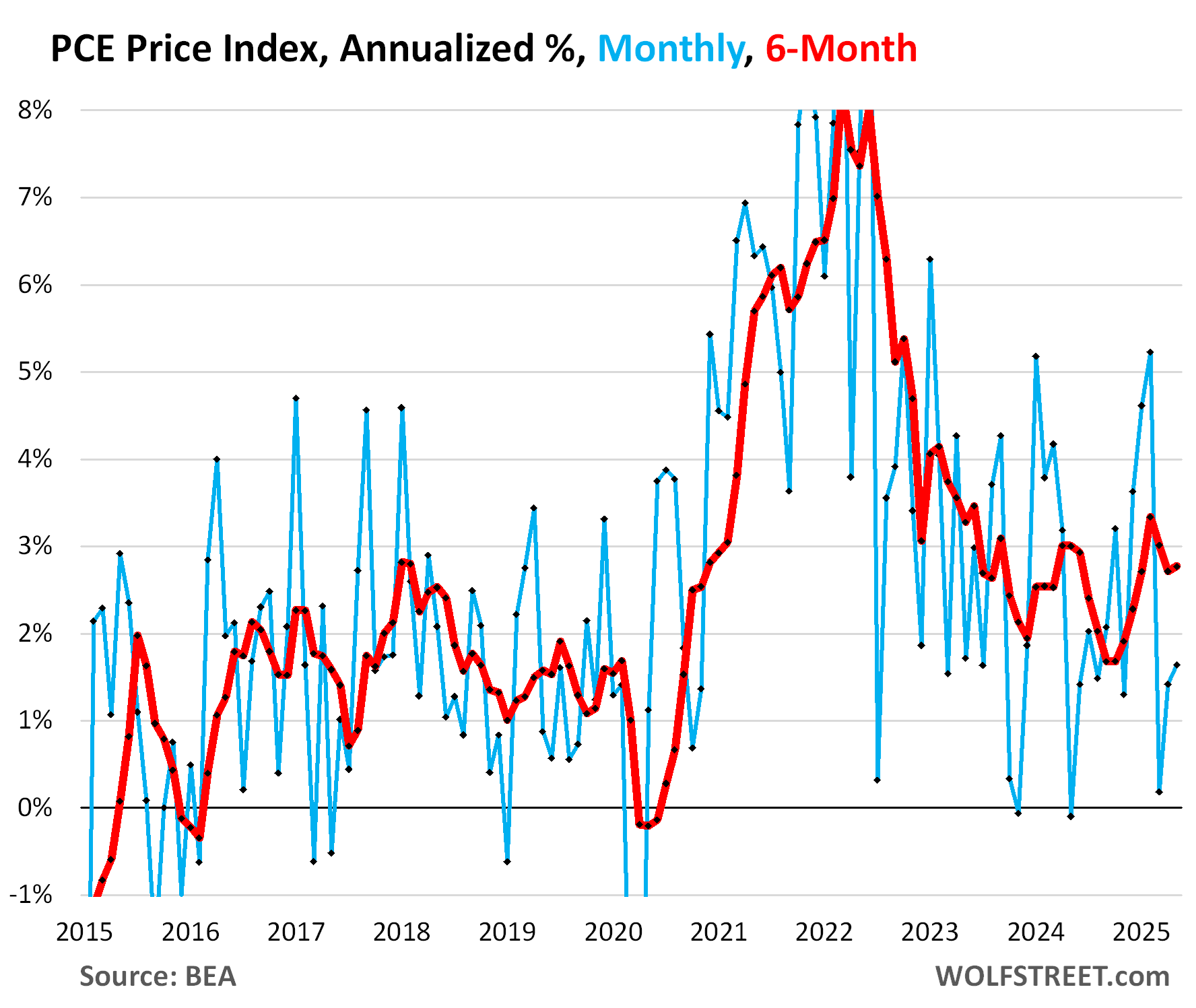

The overall PCE price index rose by 0.14% (+1.6% annualized) in May from April.

The 6-month PCE price index, which irons out the month-to-month squiggles, accelerated to +2.8% annualized, in May from April.

So far in 2025, the 6-month readings have been in the 2.7% to 3.3% range, a sharp acceleration from the second half of 2024.

The core PCE price index, which excludes food and energy items, accelerated in May to +0.18% (+2.2% annualized).

The 6-month core PCE price index (red) accelerated to +2.9% annualized.

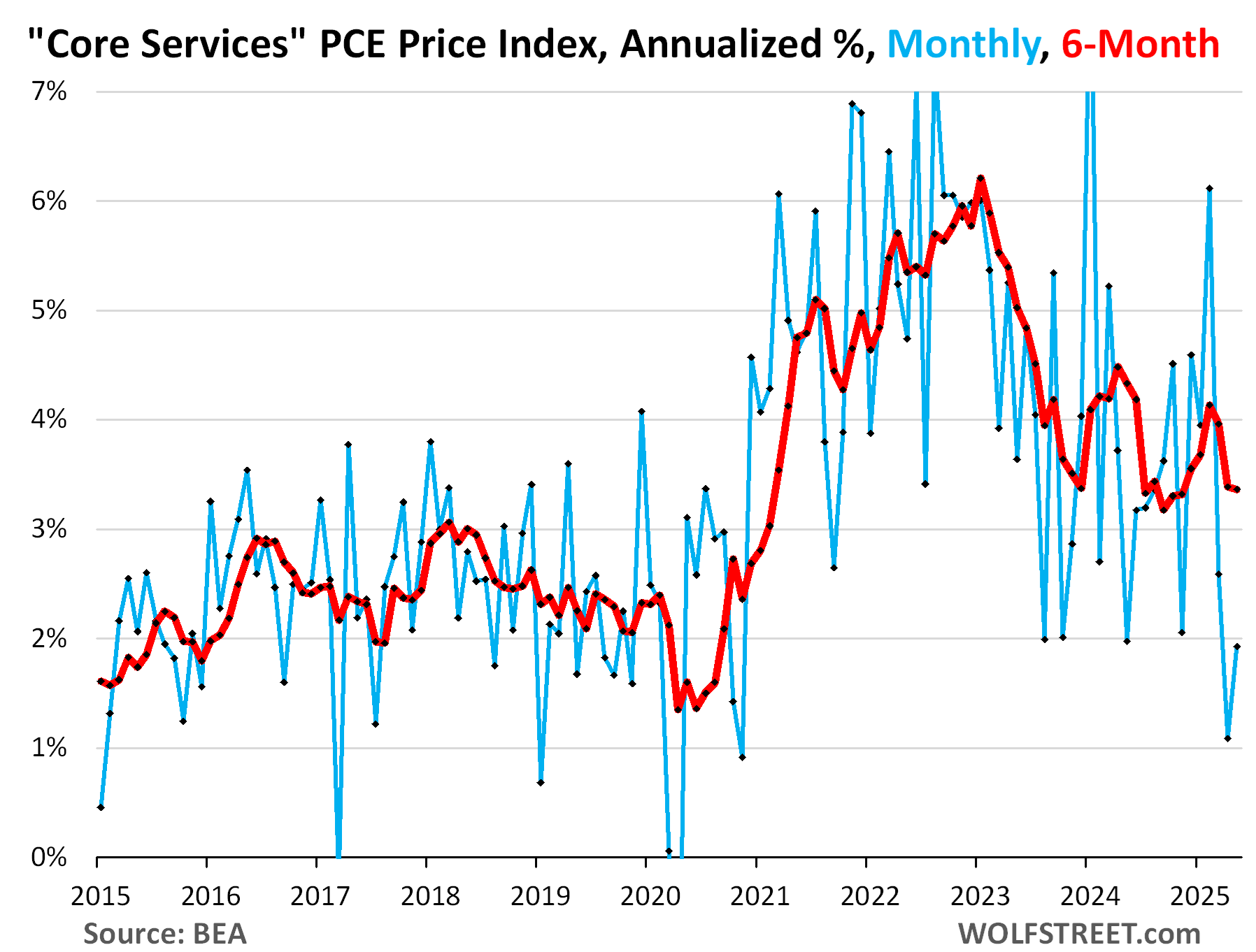

The core services PCE Price Index, which excludes energy services, rose by 0.16% (+1.9% annualized) in May from April.

And April’s freak low reading reported a month ago was revised higher today. That low reading in April was caused by a massive month-to-month negative reading in Financial Services, due to the plunge in the financial markets in April, and a historic cliff-dive in Recreation Services (we discussed this phenomenon at the time).

The month-to-month plunge of the index for Financial Services in April was revised higher today from the originally reported -1.69% (-18.6% annualized) to -1.33% (-14.9% annualized). And for May, both Recreation and Financial Services bounced off their lows.

The 6-month core services PCE price index was essentially unchanged at +3.4%.

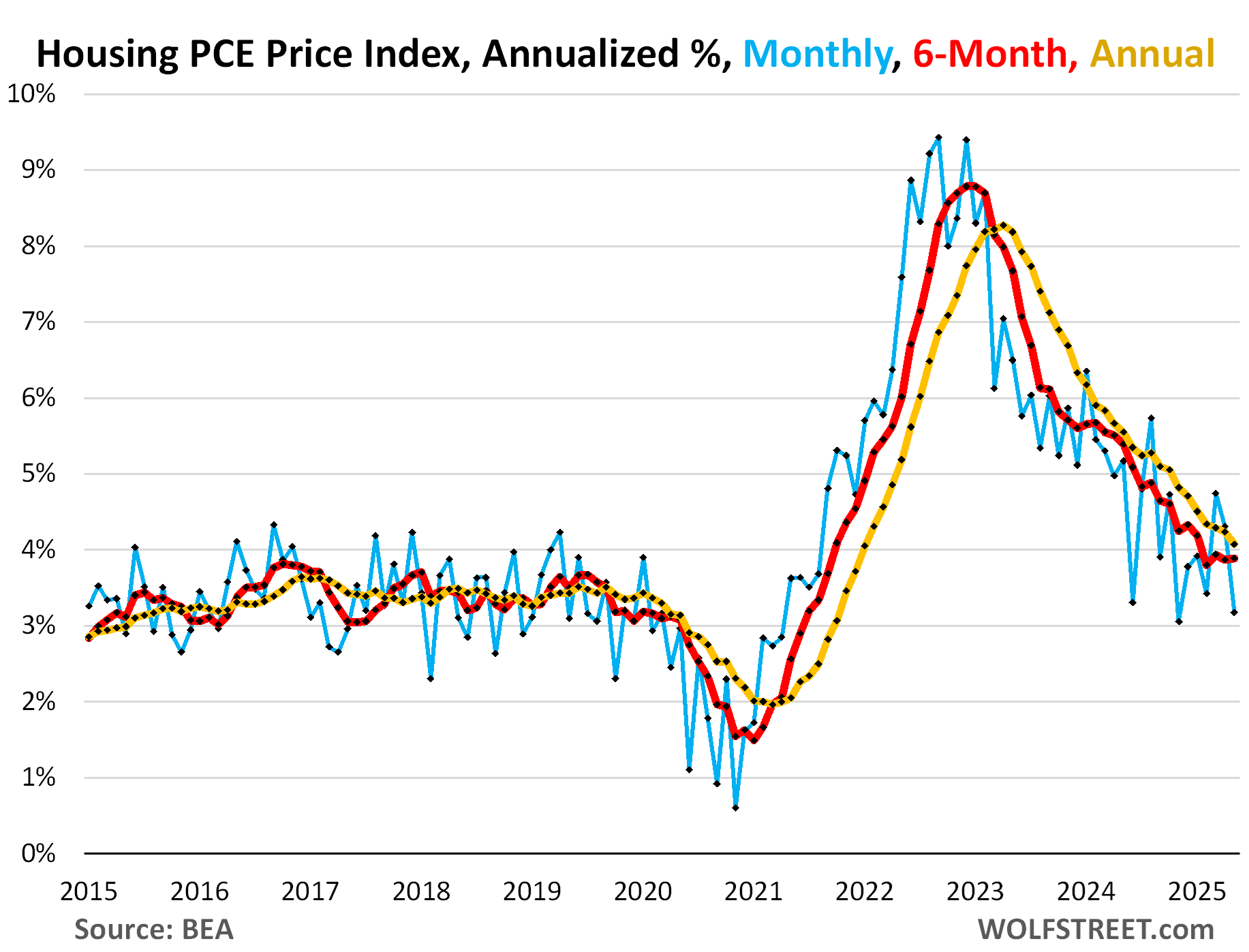

Housing inflation has wobbled around in the same range for nearly a year. The PCE price index for housing, based on various rent factors, rose by 0.26% (3.2% annualized) in May from April (blue), about where it had been in June 2024, above November, and below the much higher readings in March and April.

The 6-month housing index (red) rose by 3.9% annualized, for the fourth month in a row in that range.

The year-over-year index decelerated to +4.1% (yellow).

Clearly, rent inflation has ebbed, though it remains slightly above pre-pandemic levels:

Durable goods prices continue zigzagging out of the hole, a trend that started in 2023. Durable goods include motor vehicles, appliances, consumer electronics, furniture, etc. Many of these products or their components and materials are produced overseas and are subjected to new tariffs. So we look at them carefully.

In May, the PCE price index for durable goods was unchanged (0%) from April (blue).

The low point, in terms of the month-to-month declines off the majestic spike came in May 2024 (-8.8% annualized). Since May 2024, month-to-month price drops became smaller, interspersed by ever higher month-to-month increases, and the pattern has been higher. We have discussed this phenomenon here since last August, when used vehicle prices started to rise again.

The six-month PCE price index for durable goods has been slightly positive for four months, and in May accelerated to +1.4% annualized. It had bottomed out in December 2023 at -4.3% annualized.

The plunge in durable goods prices was one of the big factors that drove inflation down from mid-2022 into 2024. Now services inflation has cooled, but durable goods inflation is no longer negative, but slightly positive and as such is still pushing down inflation, but much less so than from mid-2022 into 2024.

This is what the Fed is waiting for: The portion of tariffs that gets successfully passed on to consumers, if any, will be visible in durable goods inflation. Many of these goods are imported and tariffed, or their components are imported and tariffed.

The Fed has said repeatedly that it wants to see to what extent the tariffs add to inflation, and to what extent companies eat them, and they can eat them without indigestion as they piled on record massive profits during the high-inflation years.

If a portion of the tariffs get successfully passed on to consumers and thereby make it into inflation, the Fed wants to see if it leads to just a “one-time bump” in the price level, or triggers persistently higher inflation rates as consumers start tolerating sharply rising prices again.

None of that has happened yet. It all depends on consumers. If they refuse to buy goods whose prices have been jacked up, companies will have a hard time raising prices without gutting their sales and losing market share.

The free money is gone, consumers are once again prudent and no longer willing to pay whatever. Demand growth is tepid. Consumers’ walking away from high prices is exactly why prices of durable goods plunged starting in mid-2022. Consumers have had it with high prices that go even higher. Price increases once again have consequences on sales and market share.

But how consumers will react to price increases remains uncertain. Consumers might once again tolerate bigger price increases, and if they do, inflation will accelerate. And the Fed is right in waiting to find out how this develops.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yet the market today is rallying again today because somehow the market is thinking Pow Pow will cut rate soon regardless of what the PCE or inflation is looking like….so glad to see we can forever live in La-La land as if all the problems has magically gone away now and hopium just keep us going higher and higher..

Enjoy it buddy, when the Music stops make sure you’ve got some of that LA la Land stuff stashed away

Completing the 5 Elliott wave.

Could be that the market priced in more inflation impart from tariffs

*impact

Durable goods are now flat, whereas the last 2 years these were negative. I think you have a point.

It’s very simple. Over the past 15 years, “buy the dip” has worked so well that it’s an ingrained emotional response. You buy stock, there’s an almost 100% chance it’s higher in one year. Why wouldn’t this influence behavior, especially if it looks like the government and media are taking steps to ensure it continues?

Look at the media headlines, “America’s stock market did 180.” They present it like it’s “our” thing, when in reality it’s just a trading vehicle for the rich.

There is also way way way more money being traded now than ever before. From 401ks, to retail, to foreign investment. It is why looking at past PE ratios is useless

Saw a stat that there are almost 25% fewer names traded on NYSE today vs 20 years ago. To your point, more money chasing fewer names

I don’t agree with that. 401(k)s were solidly established by the 90s. Retail was always there, although I will grant you that it was harder to trade without the modern internet and apps. Foreign investment was also always there.

The difference is that all of these people believe that there’s no risk. It’s a matter of psychology. Retail and foreign investors would not be dumping money into overpriced stocks if they thought there was any reasonable chance of losing. But they don’t. The last 16 years has made them all feel invincible. It’ll take a prolonged downturn that doesn’t almost immediately recover to change that.

Look at the index charts in 2023 and you can see the psychology of the market.

Things were coming down and as soon as the Fed and gov’t stepped in to bailout the rich clients at SVB the market sky rocketed based on hopes and dreams. It became clear the Fed put is still in play and the gov’t will do anything and everything to keep it going up.

Look what happened two years later. Trump implemented his tariffs and the market went down. Less than a week later Trump pulled the TACO move and we are up 20% again in less than three months.

The gov’t will never let the party end so everyone just figures that they should throw money into the market. Fundamentals mean nothing.

I agree with this. At some point, the government is going to have to pick between asset bubbles and protecting the bond market, but that time hasn’t come yet.

I saw Trump doing his expected “that guy knows nothing because he is not a businessman (and VERY successful like me). If he knew what he was doing he’d cut rates to 1% NOW!

Forcing poor bastards back into the casino where the clientele of his luxury branded hotels and golf clubs can afford to go.

I don’t know much about DC hard or soft power games (other than selling weapons of war), but I am sure the squeeze is on Powell. Especially as Trump has “consolidated” things in DC.

I remember when he told Macron Napoleon’s big mistake was “failure to consolidate”, I’m sure Napoleon was aware of what Trump means…..get as many important/powerful people by the balls in one way or the other as you possibly can.

Having no shame, empathy, loyalty, honesty, or anything resembling ANY morals whatsoever (and being short on knowledge and brains….except some RE sales ability) makes it all MUCH easier for him……a BIG advantage.

I sorta doubt Powell wants to put up with his vengeance….Mueller didn’t……

Bannon, Hannity, et all, delivered the talk show fan “deplorables” (Hillary’s word, not mine….most of my relatives are included) to him.

But if it wasn’t him, it would be some other stupid low life.

He is a symptom of an uneducated country.

Senator Warren has been just as hard on Powell as Trump. She loathes Powell even more than she loathes Trump. Powell must be doing something right.

She is likely most indebted to the insurance cartel and any side benefactors…..health is probably the biggest. We got ACA mess instead of single payer….go ask Pelosi, she’s your neighbor and she likely told Warren what to do….I like her rants on lobbyists because I knew the BEFORE SHE DID!!!…….but it’s better than nothing for many folks…(I know one guy who’s life was literally saved and he STAYED MAGA!!…..Almost $1M??!!…..after a botched stomach tie….dangerously overweight out of work “biker”we finally got rid of at our coffee thing)…..and the health and insurance folks.

I’m sure I don’t know fully why low interest rates are important to that bunch, because as I have said, financial stuff and bean counting/chasing bore the living shit out of me. Like writing code would. We are evolved to use brains, body and hands and it feels good….till I got old.

My parents and therefore my life was best when unions were strong and they used to support Dems is what I hear….Reagan’s masters ended that, and almost ended me…..saved by pure chance job test discovery luck and my vet’s points….(kinda ironic to me, the country (more likely the P/O,as they are all military and run the place that way) DID sorta appreciate what I did even though I had NO choice and deeply regret it ALL.)

If we are not going to have a more fair fiscal policy (through taxes and regulation) and just play this all out capitalism shit, then as long as the Fed effect is there, I’m for higher rates, as I am NOT an investor/trader/gambler….even if I had the money.

Being able to kick anyone’s ass or bring the entire show down means we can print all we want….the rich will still buy and all that can will live HERE (where else are they gonna go?……and stay secure AND rich? And for how long is this whole show going to go on, anyway?

We are leaving our kids with a lot worse mess than a pile of books that don’t balance.

With the asset bubble pumper in chief in the WH, did you think it was going to go down? He will do anything in his power to make everything go straight up and to the right, including his newfound love crypto (thanks to his kids and donors).

In this one case, I disagree. Trump was certainly an asset bubble pumper in his first term, but I think he saw that a stock and housing bubble doesn’t help the president. If it did, Biden wouldn’t have had 70% of people saying they thought the economy was bad.

Bessent said a month or two ago that he didn’t care if tariffs caused stocks to drop. It was the onslaught from the Wall Street bankster controlled media that portrayed the stock bubble popping as being the worst thing for Americans, and America, when in reality it was only bad for the top 5% or so.

The TACO trade thing was nonsense. He never intended on the tariffs existing in their original form. That was always a starting point.

Probably right. All the REALLY rich are in PE of one kind or another….not enough room for total us household net wealth in (public) stock, bond, and the personal RE they own.

Should look it up….broke 100 Trillion long ago, I imagine. all my rich relatives are in it, you know, the minimum $1/2 M buy in funds or corps and various rules on getting any/all of if back out when you might need it.

Kinda like the Bullion buried under the Aspen, Tahoe, Sedona ,etc “cabin”…as AI refers to his place.

$169 Trillion as of Jun 28, 2025…….and that is ONLY what the FED knows about……..What’s Powell worth?…..$30-40M?

NBay,

That “$169 trillion” is that supposed to be PE (private equity) assets under management? Or is that total assets of all categories combined, such as stocks, bonds, real estate, loans and loan securitizations etc all combined?

If you think that PE has $169 trillion in assets under management, if that is actually what you think, you’re hallucinating in drug-induced AI-fueled stupor.

PE assets under management were $3.1 trillion (three trillion and one hundreds billion) at the end of 2024.

https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/4/us-private-equity-aum-hits-3128-trillion-in-2024-88099590

No, $169T is total USA household net wealth (known to fed) Where is it?

That is just a list of some hedge funds…….like Powell was supposedly a “Partner” in Carlyle. Whatever that is?

Many rich individuals run their own “hedge funds”, (maybe with a savvy friend of their uncle or someone advising…..maybe hold some PE corps, some listed corps, some ETFS, hedge funds or maybe high net wealth bank divisions do it for them. Honestly didn’t read list.

I don’t want to argue this (so, unless you will argue snare proteins and micelle construction used in COVID mRNA drugs/vaccines with me)….nahhh…. let’s just call it a straight total verbal loss, with proof, as you defined it, so you win and I am in an AI stupor…..on top of TDS and seriously financially impaired. I’m not running a website, anyway…..too lazy…..think that was established before, Sorry.

NBay

Household wealth is the wealth held by all households, including you, me, and Musk. It includes investments in hedge funds. It includes “family offices” which are hedge funds set up by rich families for their own family members. These private hedge funds are part of households wealth. Household wealth includes their pension funds, and those pension funds invest in hedge funds, and so even these hedge fund values held by pension funds are part of household wealth. In the end, everything is included in US household wealth except if it belongs to the government or a foreign entity.

OH.

The market continues to rally because Wall Street has “animal spirits” about the current administration.

The CRB index has been climbing since last September:

https://tradingeconomics.com/commodity/crb

In fact, it has recently hit new highs. Inflation is idiosyncratic. It still feels abnormally high when we go shopping no matter what the indices say.

Isn’t well over a third of that index energy related? The recent, but short lived, spoke in oil would have a very large effect

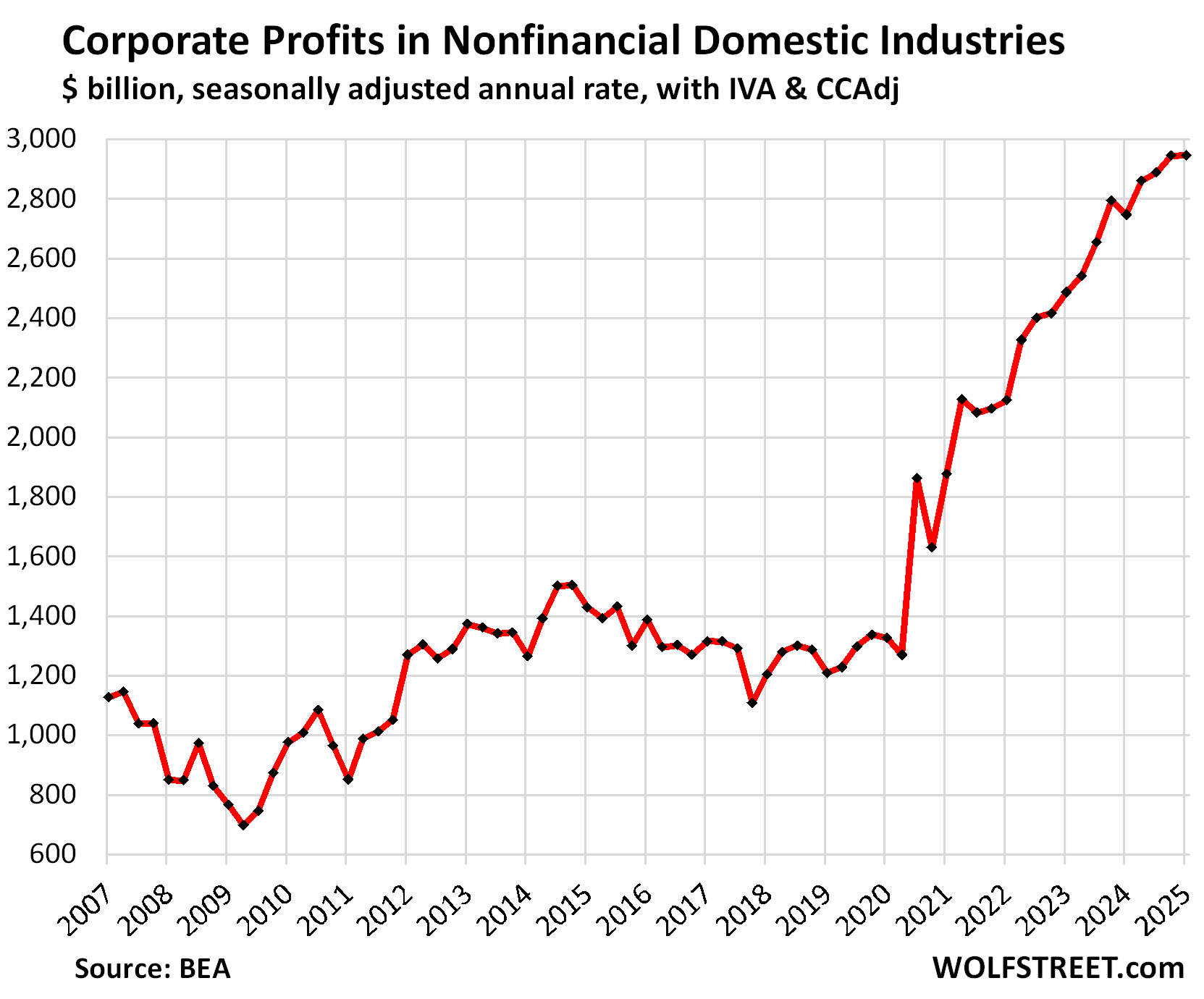

That corporate profits graph is close to disgusting. It’s almost the peace time equivalent of profiteering.

The sleeping lion is the Trump BBB should it be passed. Is there an appetite for $2T more bonds at current rates?

Powell or his heir can cut all they want…that doesn’t mean buyers will buy.

A chunk of those increased profits are simply due to inflated dollars. Not all of course. This is the insidious downside of inflation. What are things worth? If I’m making more profit, is that real or inflation adjusted??

So inflation was about 23% over this period, and those profits spiked by 122% over this period.

https://wolfstreet.com/2025/06/26/the-corporate-profit-explosion-stalls-in-q1-on-the-eve-of-the-new-tariffs/

The freeze on tariffs ends July 9.

There is no general “freeze on tariffs.” The baseline 10% tariff on all countries is in effect, as are specific tariffs on steel, aluminum, and on some goods from Canada and Mexico, as are other tariffs, as are the tariffs on goods previously exempted under de minimis loophole, etc. etc. Hard to keep up with this stuff. The only tariffs that were paused were the specific country-based “reciprocal tariffs.”

You can see right here that the tariff cash is rolling in — preliminary figures for May indicate that receipts from tariffs in May are even bigger, around $30 billion (update coming next week):

Re: “Consumers have had it with high prices that go even higher”

The 90 deals in 90 days tariff framework that hasn’t produced a single real deal, is being extended into September — but, the failure of Bidenomics, was the cumulative compounding impacts of inflation, that continued grinding down consumers and voters. Supercharging Bidenomics in 2025 seems curious.

It’s hard to believe that consumers that were stressed by inflation for the past three years, are going to blow off tariff impacts 3 months or a year from now.

Corporations may have had nice profit margins lately, but are shareholders going to accept lower share prices and absorb the shock — or will consumers be counted on for their nonstop Teflon resilience and pirate-like habits?

I don’t see happiness ahead — but happy is overrated.

You don’t understand the most fundamental economic principle: If consumers refuse to buy at high prices from a company, that company’s revenues and market share will fall. It doesn’t make one effing iota of difference what stockholders want. They have no say in this. Stockholders don’t matter. Consumers do! These stockholders’ shares will just go to zero, no problem, Bed, Bath & Beyond and hundreds of others just over the past few years, happens all the time. Adios shareholders.

Companies go out of business all the time because their revenues drop and their expenses are too high and their debts too high, and their losses are too high. C’est la vie. Better-managed companies take their market share and thrive.

FYI, Uomich survey is an example of people still amped up on Extended Bidenomics+tariff anxieties — which are now extending like a Pinocchio nose mutation with a side dish of TACO.

““About 59% of consumers spontaneously offered comments about tariffs, down modestly from about 66% last month. Still, tariff mentions continue to come from a broad swath of the population and reflect ongoing anxiety that the threat of inflation remains real, even if consumers are no longer bracing for a worst case scenario as they appeared to do so in April and early May.”

Consumers were hit by the ceaseless massive onslaught of toxic idiotic lying bullshit in the media and social media – owned by Corporate America and the billionaire class — about tariffs. I experienced this onslaught of bullshit and lies first-hand here in the comments. I have never ever seen anything like this. This tsunami of manipulative lies and bullshit about tariffs polluted people’s brains. But eventually people see through it.

Do they eventually see through it? Does any president have the balls to actually push back against this coordinated aparatus?

I read a book “Three fund portfolio”. Essentially an index funds of VOO/BND/VXUS at 40% 40% 20%. This will beat any other wise guy. If this is true, we can simply invest in the bonds and index funds and get great benefits right?

Do these data capture shrinkflation or choice reduction in durable goods?

Tariffs might filter through to consumers in the form of getting less for the same price, or having fewer choices among products. Both could protect margins.

Would data focused on prices capture such changes?

“Would data focused on prices capture such changes?”

Yes. People have a simplistic notion of how inflation data are collected.

In terms of items you buy at the supermarket, inflation data goes by weight or volume, dollars per ounce, dollars per pound, etc. This is all part of the cash register data, which the government buys from the private sector (Nielsen).

Durable goods such as cars or laptops have improved massively over the years. And inflation measures take that into consideration. All tech products get vastly better over time, not worse. There are specific criteria that are measured. For cars, for example, fuel economy, performance, features (backup camera, hill-start aid, adaptive cruise control, 400 hp, 10-speed automatic transmission, etc.), safety measures (# of airbags, side-impact protection, crumple zones, etc. ), and on and on. Measuring inflation is a highly complex process.

A lot of the detailed data is acquired from private-sector industry data firms, such as from JD Power for cars, from Nielson for supermarket data, etc., and layered on top of other sources of data, including in-person visits of stores. The BLS uses this “multi-source” approach to data gathering.

What about quality though?

Companies using cheaper parts instead of raising prices.

Or at the grocery store I have to buy three watermelons because all the produce is poor quality

Don’t see how that could be factored in without massive work

There are dudes here who say, “my 1989 Buick was the best car ever, and I still drive it,” and good for them to live in their dreamworld, but that’s total bullshit. People just make up BS to suit their fantasies, such as your watermelon idiocy.

I’ve had good luck picking the watermelons with a sizable field spot, a yellow or cream colored patch on the bottom that indicates having sat long enough to ripen.

…American-you must remember that ‘quality’ perception must be learned and personally-embraced, whether goods OR services, and that that requires a significant time-investment by an individual, even to gain the level of ‘common sense’. Perhaps an easy slide down linked to cases of: ‘just in time’ being yoked to: ‘just good enough’ (though a new baseline ‘quality’-level may very well be an improvement on a prior generation’s ‘best’…)…

may we all find a better day.

Thank you. So this is why there was some alarm about reducing the government workforce collecting inflation data. Sounds like it is more complicated and labor intensive than getting just the prices.

Yes. What the BLS did under pressure from DOGE is to cut out some people who did in-person visits to stores in some smaller cities. So in a handful of smaller cities (Buffalo I think was one of them), the in-person visits are no longer taking place, but they are taking place in other cities, at least for now. So for those cities, the BLS still gets the cash-register data and the other data, but no longer the in-person visits to layer on top.

When people like that get cut, and it hits the press, this is when we realize that the government actually does things, and that those things are complicated, but have value, such as accurate data. For example, they’re gutting the IRS staff so that billionaires and big companies can no longer get audited. Etc. It makes sense that this was Musk’s idea.

…many dollars spent in order to demonstrate that pennies could be saved (or in the case of physical pennies, dispensed with). A conundrum of the disbursement of public monies which have required a significant (and growing) percentage of same to be expended just to make sure they are being properly, and legally, awarded, directed and used…oh, wait…

may we all find a better day.

That’s headache stuff dustoff. Won’t even try a reply, but glad to see post from ya….bit worried……but…..aww hell, at our age we are total winners even if we don’t wake up tomorrow….both the time era and the lifestyles. Now if I can just start looking at everything going on like I once did the Sat AM cartoons.

Later!

…just surfin’ that movin’ hourglass sand with a little less fluidity in my motion and wind in my shout. Best to you, my friend…

may we all find a better day.

You gotta love the corporate profits chart illustrating where the trillions of stimulus and government spending ended up… more than doubling in size, while GDP grew by perhaps 30% since 2019, barely keeping up with inflation. Asset holders love “Modern Monetary Theory” – it pushed income inequality into overdrive. In the context of MMT, governments should control inflation by hiking taxes, but that never happened under Biden. Funny how things always end up benefiting the wealthy, no matter who is in the White House.

” Funny how things always end up benefiting the wealthy, no matter who is in the White House.”

Almost always far damn shore Jason:

With the exception of a couple of decades after WW2, during my lifetime the rich have benefited from the vast and continuing political corruption they have paid for!

Due no doubt at least in part to serious fears of the possibilities of millions of battle tested veterans coming home to socio-economic inequality as had clearly been the case prior to the war, the rich ”allowed” the workers, AKA WE the PEONs, both at home and in our military, to enjoy a fair share of the benefits earned by the victories of that war, while also allowing their paid political puppets to tax the rich much more than currently to pay off the financial costs of that war…

Probably/maybe going to take some similarly traumatic situation to pay off the current debt.

Trump Tax Bill Could Add Over $4,000,000,000,000 to Debt

Under current policy it’s not spending anything at all lol … The BS politicians try to pass on to justify their evil deeds.

Like saying well my $800 car payment just ended so getting another $800 a month car isn’t taking on any new debt??? Lol what!?

Assets=liabilities+owners equity…so pathetic

One more inflation feature that has not been mentioned: the decline of the USD. To the extent an importer buys goods, whether denominated in USD or FX, the likely impact is that imported goods will cost more. This pain is different from the financial statement impacts on FX moves. I hope Wolf can provide some commentary on this in coming months if there is some data to show that offshore sellers want US importers to pay more for goods.

I don’t believe that the US or any other country on the planet will ever pay off its debt. MMT is right in that no state with a fiat currency actually has to do that. All money is just an IOU and as long as you can produce it without causing substantial inflation, you can just keep on doing it. The problem is money must be backed by labor to have any value at all. So what they are actually doing by printing more money without a resulting inflation, is to devalue labor.

Yes, that’s the fundamental problem. When people “give up” and stop laboring, the system stops working.

I believe that’s what is behind the so called “laziness” from Gen Z. They’ve given up. They feel the social contract has failed them.

…see history of the Roman plebeian farmer/citizen class…

may we all find a better day.

Trump has ‘outsmarted all of us’ admits backpedaling economist who bashed President’s bold plan.

Torsten Sløk, a chief economist at Apollo Global Management.

Maybe the administration has outsmarted all of us,’ he wrote

Torsten also just posted, about a day ago:

“… In particular, debt-servicing costs are rising rapidly, and the US government currently pays a record-high $3.3 billion in interest payments every day, and for every dollar the US government collects in tax revenue, about 20 cents go to paying interest on debt.”

Outsmarting us all, by increasing the deficit will be his biggest win ever!!

He said that on June 21, then June 24, he said:

“Lower GDP growth and higher inflation is the definition of stagflation”

So, we’re waiting to see reality play out very slowly — but as it plays out, the upside of tariff outcomes next year seem reminiscent of the tariff outcomes in his first term. I contend, that the slow transitory implementation will be overshadowed by slower economic growth.

Nike was talking about upcoming price increases in Fall and they were suspiciously moderate with $5-$10 on select footwear (https://eu.usatoday.com/story/money/2025/06/27/nike-prices-trump-tariffs/84387186007/) I strongly doubt that this is enough even if they manage to shift some sourcing as there are across the board tariffs and the USD index dropped 10%. Additional hidden hikes will be there like less sophisticated features and fewer price promotions. As in pharma a lot of the cost is in marketing so I would expect those budgets to be hit as well. It will certainly take time for whole picture to emerge.

Manipulative press release bullshit spread by a German troll that hates the US tariffs.

Nike just announced in its earnings call that it will eat $1 billion in tariff costs this year, not pass them on, and that profits would drop further and that sales would drop further, LOL

Nike’s sales declined by 12% yoy in the quarter through May 31, and its net income collapsed by 85%, so how is it going to raise prices when sales are already falling because prices are too high??? No, it’s going to have to CUT prices to get sales to grow again.

If Nike cannot figure out how to increase sales by cutting prices, and bringing its costs down by, for example, firing the top three layers of executives and replacing them with AI, its shares will just keep sinking (despite the 15% spurt on Friday, shares are down by 60% from their 2021 high).

That’s exactly how tariffs work. GM announced that it would eat $5 billion in tariffs this year because it cannot raise prices either, because people will just buy a non-GM if it does, and Ford announced that it would eat $1 billion in tariff costs, and they issued profit warnings. Other companies did that the same.

Even if tariffs are passed on to consumers, that is not inflation, but rather a tax increase. That should not drive monetary policy.

In any event, two Federal courts have already ruled most of the tariffs to be illegal. While the tariffs are still being collected during the litigation due to stays issued by higher courts, they will be refunded sometime in 2026 if the Supreme Court applies its centuries old precedent that the power to regulate does not imply the power to tax.

With all due respect, with hundreds of federal judges, it’s not hard to find a few in every issue who are part of the “resistance.”

I think it’s very unlikely SCOTUS will uphold their decisions on this.

So far SCOTUS has been actively overruling down these activist Judges that think they have greater authority than the executive branch.

Out of deference to the President, and so as to not disrupt ongoing negotiations, SCOTUS will stay any lower court orders until its final decision next year. But, eventually, there will be a 9-0 decision striking down the IEEPA tariffs (but not others).

For the next step, look for the Federal Circuit sitting en banc to overturn US v, Yoshida when it rules on the V.O.S. case this summer, thus eliminating any basis for the IEEPA tariffs. Oral arguments are July 31. Stay tuned.

Tariffs are one of the better “taxes” if theyre being placed on companies with huge profits. Much better in my opinion than the inflation tax that devalues the dollar. What’s your preferred way of how to pay for the govts overspending, and the trade deficit?

(One of) the Elephant in the Room is the chart for Housing. After the massive rise in costs it continues, “above the prepandemic trend”

This is cumulative!

Add in the fact that spend 2/3 on services ( also running hot), who cares about goods? The American Way is to be overloaded with cheap plastic crap. Cars and computers are similarly excessive in most people’s personal lives.

The inflation problem has not subsided, and the “numbers” only bounced off the “target.” At least now there’s yield.

…many dollars spent in order to demonstrate that pennies could be saved (or in the case of physical pennies, dispensed with). A conundrum of the disbursement of public monies which have required a significant (and growing) percentage of same to be expended just to make sure they are being properly, and legally, awarded, directed and used…oh, wait…

may we all find a better day.

…apologies, not sure what caused this to post earlier in the comments, then vanish, then post twice with different time hacks…

may we all find a better day.

Happens quite a bit. Not sure why. I think it has something to do with your browser keeping your comment in memory, and when triggered, somehow posts it again, but not as a reply (like the original) but by itself at the bottom. It’s always the same pattern. So I usually delete the duplicate that’s dangling out there by itself.