Will the bond market eventually wake up and scare the bejesus out of Congress? Is it already rubbing its eyes?

By Wolf Richter for WOLF STREET.

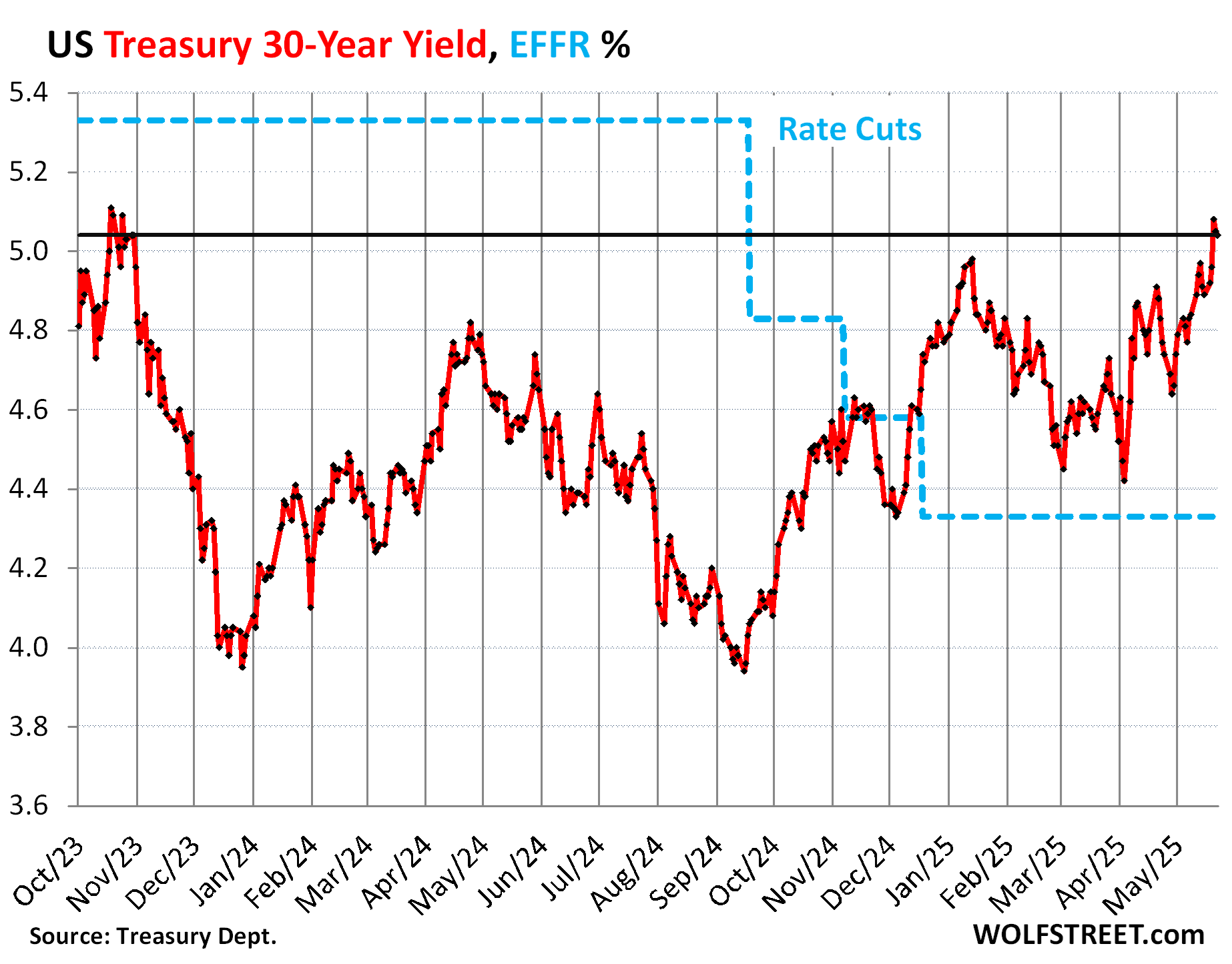

The 30-year Treasury yield ended Friday at 5.04%, after kissing 5.15% on Thursday. These above-5% yields are the highest since the debt-scare in October 2023. The 20-year yield has also been above 5% for the last three days of the week.

The Fed started cutting its policy rates in mid-September 2024, by a total of 100 basis points so far. The Effective Federal Funds Rate, which the Fed targets with its policy rates, has dropped by 100 basis points, from 5.33% to 4.33% (blue line in the chart).

But over the same period since mid-September, the 30-year yield has surged by 110 basis points, in a spectacular counter-move (red in the chart). The gyrations around “Liberation Day” now look just like some additional squiggles in a longer up-trend.

When bond yields rise, bond prices fall. With bonds that have many years left to run, prices fall a lot when yields rise, which makes them risky in terms of market price, and “bond bloodbath” once again made the rounds in the financial media.

But for future buyers, higher yields and lower prices are appealing, and those future buyers are sitting there on their hands, licking their chops. Someday, when yields get high enough, they’re going to buy. When too many of these folks or algos are just licking their chops and waiting for even higher yields, instead of jumping in and buying now, that’s what causes yields to rise.

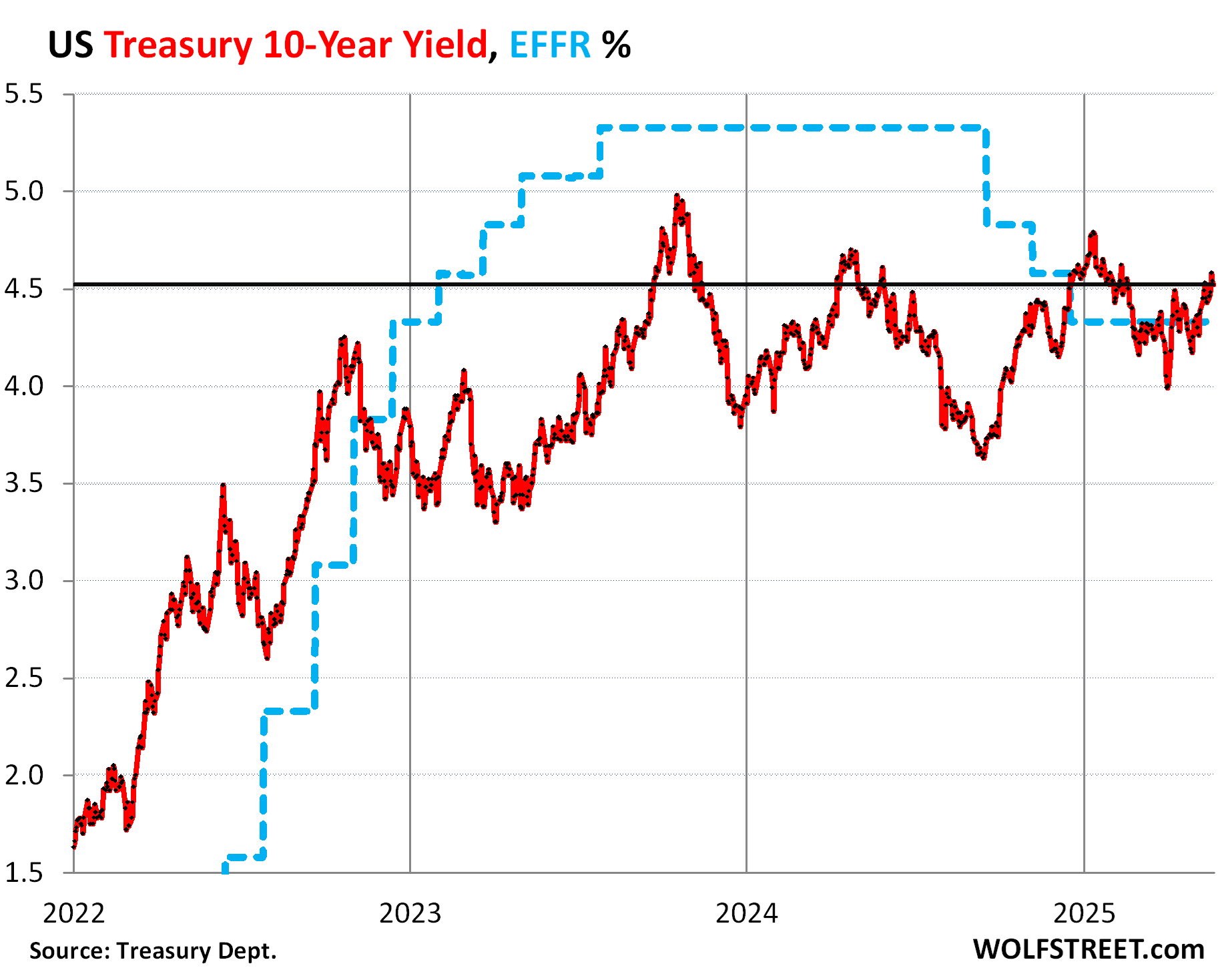

The 10-year Treasury yield ended Friday at 4.52%, after briefly kissing 4.61% on Thursday. So it’s back where it had been in February.

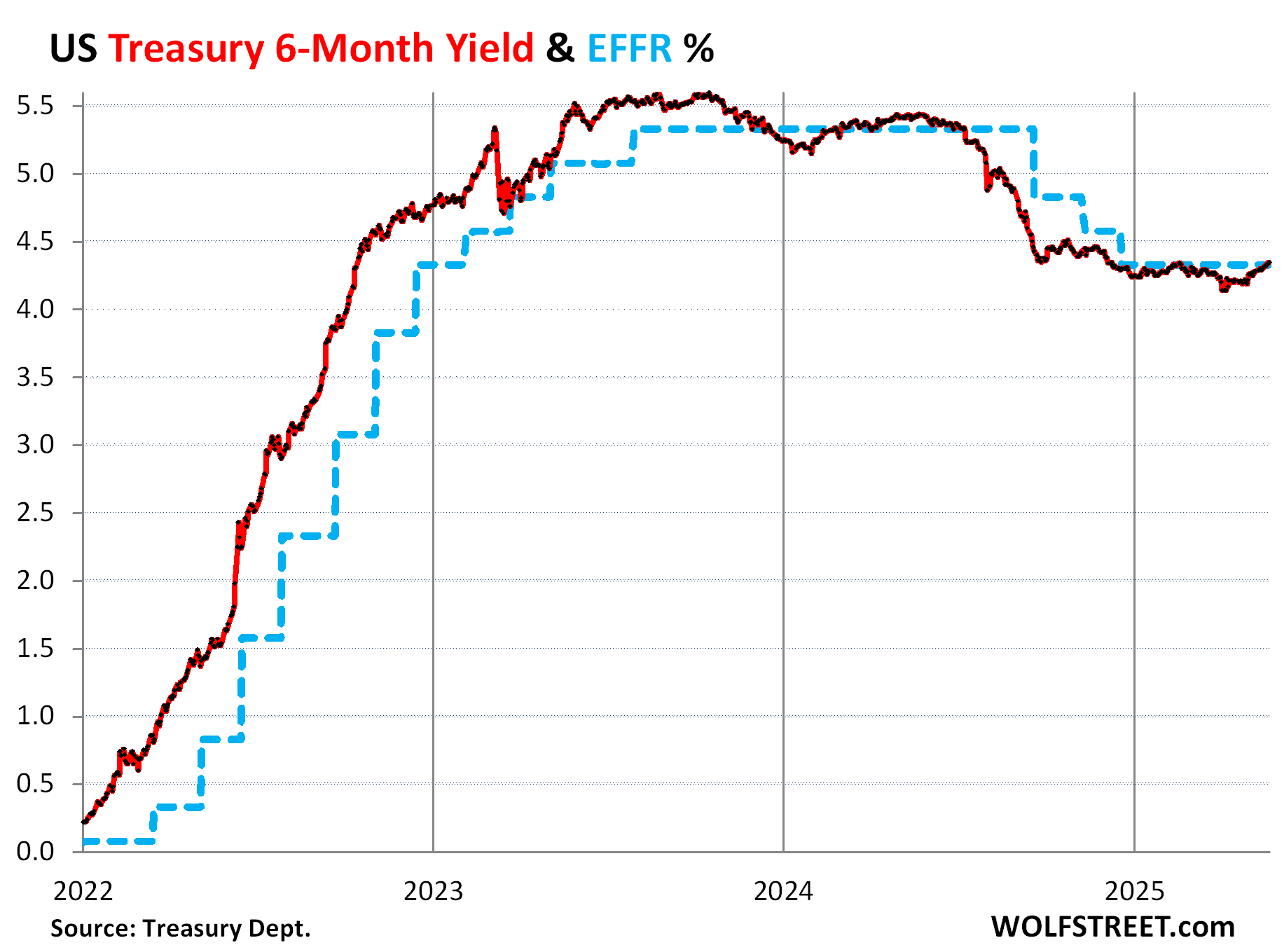

No rate cut for months: 6-month Treasury yield.

The six-month Treasury yield has taken rate cuts off the table within its window which extends to about three to four months. It normally does a pretty good job of anticipating rate hikes and cuts months in advance, as market participants listen to every comma the Fed utters or fails to utter.

It has ticked up by 20 basis points since early April and now hovers right at the EFFR, amid persistent chanting by the Fed and Fed governors of the wait-and-see mantra.

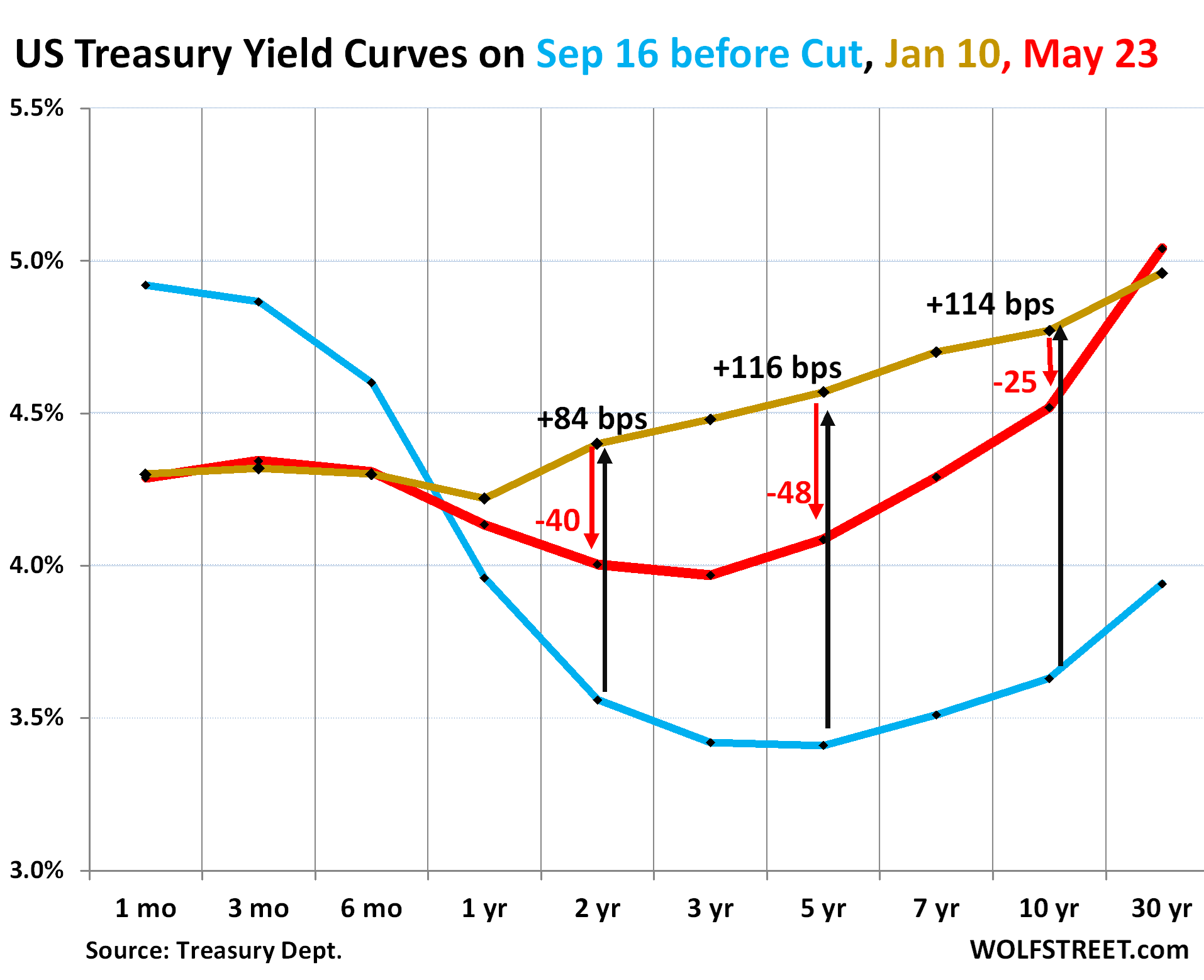

Yield curve steepened at long end, sag in the middle flattened.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed pivoted to wait-and-see.

- Red: Friday, May 23, 2025.

- Blue: September 16, 2024, just before the Fed’s monster rate cut.

The 30-year yield has snapped back and is now above where it had been on January 10. The 10-year yield is only 25 basis points from where it had been on January 10. The 7-year yield is right where the short-term yields are. Everything longer than the 7 years is now above short-term yields and that part of the yield curve has fully re-un-inverted, so to speak.

And the sag in the middle between the 6-month yield and the 7-year yield has gotten shallower in recent weeks as those yields have risen.

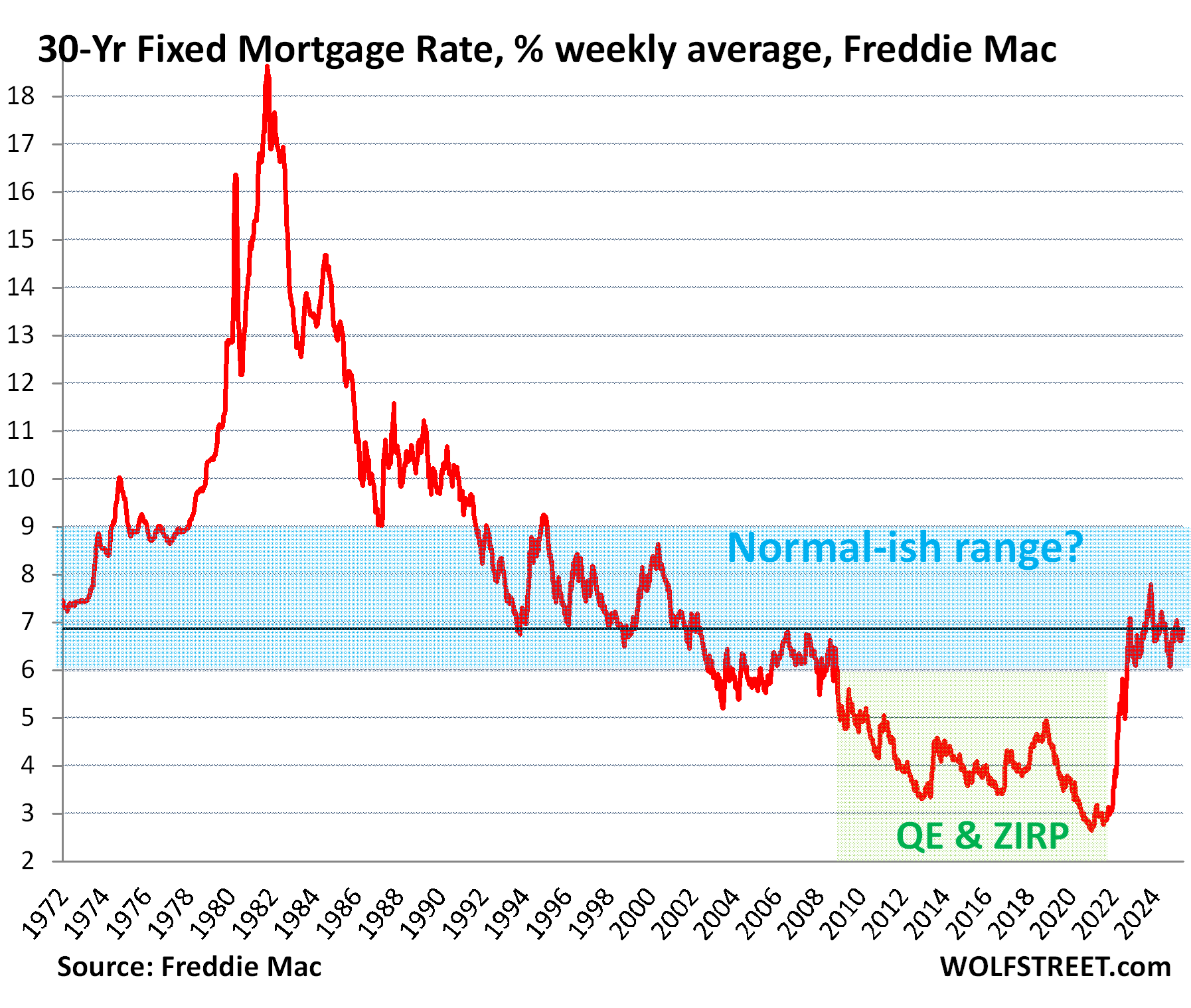

Mortgage rates again above 7%.

The average 30-year fixed mortgage rate has been once again above 7% for the last three days of the week, and right at 7% for the first two days of the week, according to Mortgage News Daily. It went over 7% for the first time in this cycle at the end of September 2022. The once unthinkable 7% mortgages have become the new normal? But they were the old normal, sort of.

By Freddie Mac’s measure on Thursday, the average mortgage rate for the week through Wednesday rose to 6.86%. This measure has been north of 6% since September 2022, and between 6.5% and 7.5% much of the time.

The average 30-year fixed mortgage rate didn’t drop to 5% until the Fed started QE in 2009, which included the purchases of ultimately trillions of dollars of mortgage-backed securities, which helped push down mortgage rates, ultimately below 3%, which triggered historic home price inflation. But in 2021, consumer-price inflation began to also rage, and the Fed eventually put an end to QE, and since mid-2022 has conducted QT, shedding by now $2.26 trillion in assets, including $570 billion in MBS.

The 3% mortgage rates were a brief aberration that created massive distortions in the already distorted US housing market and were the final act of the 40-year bond bull market.

Sleeping through the first innings of anathema.

For the people and algos that are waiting for higher yields before buying, the current yields, though up some, are still not a good deal.

At first it was the swirling fear of stubborn re-accelerating inflation and of a lax Fed: It cut 50 basis points last September just as inflation started to re-accelerate.

That fear is topped off by the fiscal mess: It appears likely that the Republican budget in the works will make the deficit even worse for years to come, increase debt issuance even more for years to come, thereby throwing more supply of debt on the market that then has to attract more buyers who need to be lured into the market with more attractive yields.

All three issues – fears of higher inflation, fears of a lax Fed, and additional years of unspeakable fiscal madness – are anathema for the bond market.

Except that the bond market has been sleeping through the first few innings of this anathema. It briefly woke up in the second half of 2023, but then dozed off again. And now it woke up again? Maybe just a little?

The last time the bond market was wide awake, nervously watching inning after inning of anathema, was in the late 1970s through the early 1990s, when the 10-year yield was mostly above 8%, and for some years much higher.

Eventually, the bond market scared the bejesus out of Congress and the White House, and they successfully trimmed the deficit. The bond market scaring the bejesus out of Congress and the White House for years to come – not just a brief episode that blows over – is likely the only force that can get them to trim the deficit. But that’s not happening right now.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Genesis had a hit in the 80s, with Land of Confusion. There’s a particular line that I think about often toward the end of the song, ” …Our generation will put it right, we’re not just making promises that I know we can’t keep”

Aged like milk as we keep kicking that can on down the road.

Except the debt super-exploded starting in March 2020 by close to $20 trillion, and it continues to super-explode, and lots of the people in Congress are now GenXer, Millennials, and GenZers, and the last $20 trillion of the $36 trillion of the debt is their decision and their debt.

Speaker of the House, Mike Johnson was born in 1972 and is 53 years old.

The median age of Representatives in the House is 57.5 years now. So half are younger than 57.5 years, and it’s their decision now.

The head of the Senate is JD Vance (VP), who was born in 1984 and is 40 years old.

Senate Majority Leader John Thune is a late boomer, now 64.

The median age in the Senate is 64.7 years, so half of them are younger than 64.7.

The boomers (older people before them) have long been on their way out, and in their footsteps come the younger people. That’s how it goes. So what happened over the past five years – the last $20 trillion of the $36 trillion in debt – required the younger people to get it done. And those young ones are by no means fiscal conservatives. They voted for this stuff. And they’re still voting for it, as you can see.

In section No rate cut for months: 6-month Treasury yield.

market participants listen to every comma the Fed utters or fails to utter.

Should the line above be a “comment” rather than a comma?

No, comma as in “,”

It was my kind of humor.

A friend of mine and me joke that CNBC and Bloomberg break down Powell pressers talking about whether he blinked wrong at the podium. The comma (,) joke make me laugh!

Every “coma” would work too!

In fact, they listen to every little fart, burp, and pause from Powell, and make their decisions accordingly.

Wolf

I may have missed but can you write an article explaining in numbers what congress and other branches of government will do if we have to cut this deficit in half and how long it will take. DOGE agency has been a complete failure and no one is talking about it anymore. I mean it’s not a rocket science. We have 3 big buckets of social security, defense, and Medicaid. Unless we make drastic cuts this is going no where. Our current approach is like using a spoon to empty a dam full of deficit.

My another fear, Powell term is up May 2026. New Fed chair is going to be a puppet of our president. What do you think will happen if new chair cuts interest rates drastically or make other rash policy decisions? Can you look into that crystal ball you have and predict and write an article? It will be an interesting write up.

Last, we will have to make sacrifices if we have to cut this deficit. I for one open to give up half of my social security if all of us decide to it. Why we even have it? Let’s stop paying social security taxes and phase the system out over 30 years. Those who have already invested, will get their share based on their investment. We literally stop program and you will get paid based on the years of service based on program termination date. I do not believe that 20-30 year old young working class cares of social security. They have plenty of years to manage their finances. I am only advocating to terminate social security payments. We will still need medical coverage from government since retirees cannot afford insurance. Like I said, at some point we will have to start making sacrifices. Giving up money is hell lot of easier than giving up life for a country and our soldiers did ultimate sacrifice in worlds war 2. Why can’t we sacrifice for our future generations?

“I do not believe that 20-30 year old young working class cares of social security. They have plenty of years to manage their finances.”

My google AI buddy says the median retirement savings balance in the US at age 65 is $88,000. Younger folks don’t think of Social Security because they don’t think of retirement. And Social Security exists BECAUSE of that. Young folks didn’t care at the turn of the 20th century and they don’t care now. That’s why the median savings balance is $88k.

Fixing SS, Medicare (et. al), and the defense budget are HARD. You have to actually raise taxes to fix Social Security. Willing to make that sacrifice? You have to actually ban hedge funds from charging exorbitant rent for the land they own underneath hospitals to reduce wasteful costs (and a million other absurdities in US healthcare), and you have to give up the fantasy that their is a country out there that has a powerful enough navy to cross the oceans and land millions of troops in the US. Willing to give up that fantasy? And, most importantly of all, you have to have elected officials be willing to give up “campaign contributions” from the military-industrial complex and insurance companies. Which can not happen.

These things will get fixed, but only when the pain reaches the necessary threshold.

Think VAT tax. But remember that when this balances the budget, all governments will overspend and go into debt again. So think firing every elected official if they overspend by more than 3 percent a year, and hold a national election. These solutions are not mine. They come from the Wharton Model, and Warren Buffett.

We don’t need “drastic cuts”. We need repeal of the irresponsible Bush and Trump tax cuts, returning taxes to past levels with which the country did just fine.

We should also reinstate the regulations prohibiting stock buybacks, another thing we used to do quite nicely without. Corporations should distribute their profits as dividends, taxable as income. This would also reduce the fraud being committed with many buybacks, and the bizarre overvaluation of stocks driven by the buybacks.

@jm

Exactly. We need a combination of repealing of previous tax cuts with spending cuts. We need to get in deficit spending lower, so as Wolf said in the past it’s a manageable amount.

Social Security is not part of the Federal Budget and is not included as part of the deficit. It is a stand alone, self funding program payed for by social security deductions.

The fallacy that SS is the cause of the deficit is the pablum fairy tale that is served up to the gullible so they willing agree to give up their SS benefits to continue to pay for the party they’re not even invited to. Sheesh !

For approximately 27% of Americans on Social Security, it’s their only source of income and for 47% it represents 3/4 of their income. Infuriating to read this nonsense. Social Security didn’t cause the deficit, bloated military spending and tax cuts are the problem. Novel concept, Raise taxes !

Can anyone cite an actual law that prohibited share buybacks?

kramartini

Section 9(a)(2) of the Securities Exchange Act of 1934 (the Exchange Act) prohibits various forms of market manipulation, making it unlawful to conduct securities transactions with the intent to deceive investors by controlling or artificially affecting the price of a security.

From 1934 (when the SEC was established) until 1982, the SEC judged open market share repurchases to be one of these forms of market manipulation and deemed them to be illegal.

In 1982, the SEC issued Rule 10b-18 which provided corporations a “safe harbor” to buy back their own shares under certain conditions. This safe harbor is huge, and it unleashed share buybacks.

This comment is as sloppy as Wolf’s surprisingly-out-of-character misstatement that the deficit could be increasing.

You can literally go to the DOGE govt site and see that they have saved $170B annually, and they post daily/weekly savings. Now, congress needs to codify it to keep it from coming back, but that’s the age-old problem with congress and those who keep re-electing swamp monsters.

Medicare/Medicaid (not just Medicaid) and interest on the debt account for $2.7 TRILLION of spending, which alone is more than the annual deficit.

CommonCents

Seems you’re living in fantasy land. But OK, deficit projections are hard. For example, deficit projections by the Congressional Budget Office, as dismal as they have been, have turned out to be too low for years. So forecasting what happens to the deficit is hard, and if you believe that it’s not going to increase, fine, we’ll see, but believing the stuff on DOGE’s website, before they walk it back, is easy.

There are some things on the positive side, including the tariff revenues. But tariffs are in flux, and it’s impossible to predict what that revenues from tariffs will look like over the next few years.

BTW, when the deficit grows more slowly, that’s not “cutting the deficit.” It’s still growing, but more slowly than it might have otherwise.

Cutting the deficit means that the deficit in dollar terms actually shrinks: it is smaller in 2026 than it was in 2025, for example.

We need to increase the velocity of money that’s locked up in assets, then capture them with taxes. Tax finance markets into the ground so the only way to make money is to make products. Overbuild on houses so corporations can’t rent seek and hedge fund types go to work producing something.

We have plenty of wealth, it’s hoarded under inflated assets waiting to be rented out. If we then broke up monopolies, all these businesses would have to compete and keep prices low. People would build and buy, feeding the tax man and keeping the debt low. Low prices would spur new innovation and small business that would raise up the lower classes and build out the middle.

The guys who are keeping things stagnant are the wealthy people in the government.

Everybody wants to cut the deficit until their benefits are in the cross hairs. It all circles back around to the question, “How are we going to pay for it?” When the the masses are convinced that it should come from the “Rich people who aren’t paying their fair share,” then you are already doomed. He we are. Cutting spending won’t happen until someone decides that they”ll take a pay cut.

It being Memorial day, good questions.

The American veterans are the American everyman. The foundation of our belief system who believed enough to serve in the armed forces.

Being a WW2 baby, I remember WW2 veterans, like my Dad, humbly rebuilding a peace time economy and society.

We forget what we owe to the social democratic warriors that secured our freedoms. IMO they would not agree that the current situation was worth the sacrifice.

It seems even if congress and voters don’t decide to take a spending, pay cut, the real value of the benefits will decrease, so there’s no escaping it but better to do it willingly and structured.

@Wolf

My theory on this is that people only learn from what has happened to them personally.

The majority of the Congress today were too young to actually remember the 1970s, and do not think about inflation very much. They do not understand that deficits have consequences.

This situation looks like inflation and high interest rates for the next five-ten years.

Yes, that’s a big part of the problem.

The band Genesis’ song Land of Confusion from their 1986 album Invisible Touch is a song worrying about the state of the world, especially under the leadership of Ronald Reagan, who liberals regarded as a dunce and a trigger happy nut who wanted to start a nuclear war

Who said that out loud during the past 30 years? As a self professed social democrat, I would vote for the Reagan that actually governed over any Republican and most democratic candidates today.

Reagan actually raised taxes when needed. Reagan actually changed course when he saw what he was doing was not working. Very few modern politicians would do the same.

Reagan tripled the debt in 8 years. No other president, try as they might, has more than doubled the debt in the same time span.

@ Goldie

Reagan had a Democratic Congress, it was a bipartisan effort

For approximately 27% of Americans on Social Security, it’s their only source of income and for 47% it represents 3/4 of their income. Infuriating to read this nonsense. Social Security didn’t cause the deficit, bloated military spending and tax cuts are the problem. Novel concept, Raise taxes !

“All three issues – fears of higher inflation, fears of a lax Fed, and additional years of unspeakable fiscal madness – are anathema for the bond market.”

Sums it all up. The interest rates, IMO, are 200 bpts too low and buyers of long term bonds from any country are likely to lose 30+ pct of their nominal value. T bill and chill.

The bond market is not rigorously logical, but neither is it *quite* illogical. It follows its own rhythms and rhymes, loosely connected with the larger economy. Today’s economy is, basically, good, so the bond sellers are happy…

I disagree. I think the bond market is inherently logical and one of the most rational measurements of financial equilibrium devised by man in his search for meaning in a universe in which he is not important.

The interest rate structure has a much bigger impact than contemporaneous memes.

I guess yield may come down due to tariff revenue.

Canada, Mexico = 25% non USCMA

China – 45% on most goods

EU – 50%, but I see eventual settlement to 20%

Steel, Aluminium – after deals will avg 20%

Cars – after deals will be 20%

Pharma – wil be 15-20%+

Phones, Semi conductors – 15=20%

Will take avg tariff rate to 22-23.5%, netting over 3.5 Tn in 10yrs. Weak currency will increase offshore profits and I see tax revenues remain unaffected

Let us for a moment see the other side – Isn’t Trump playing well?

Our tax cuts total 4-5.5 tn additional expense, but low taxes +weak currency + slight decrease in trade deficit is higher GDP still.

I guess we end up 10 yrs at 5.25tn – 3-3.5 tn tariff rev = 2-2.25tn additional debt.

The dark horse here is interest expense but I see yields for 30yr can come down a percentage point if he gets a friendly fed to do 3 tax cuts, and there is a bank SLR rule adjustment

Treasury may borrow short term over next year.

Tariff inflation is one time, but also helps companies price up goods and eventually increase tax revenue

Wow. You have interesting calculations !!!

So called “Unfriendly” FED did 4 cuts (100 BP in 3 meetings) and 10,20, 30 year yield went up by 100 BP. Wolf has been saying this for entire 9 months now. Even FED is asked about this and they have been giving their reasons.

Aren’t you that cute MAGA supporter who can give any BS to convince yourself? The tariff numbers you are giving couldn’t even stand for one day in April 1-9 drama.

In your own theory, you are saying Companies can price up goods and increase revenue. Isn’t that phenomenon called “Inflation”? And yet you want FED to cut rates?

Cute that the FED got “spooked”

Into cuts late into an election cycle.

Memo to SSK. The FED (as in Federal Reserve) does not have anything to do with taxes. Taxes are a government function.

For what it is worth, Social Security is not part of the government budget setting process. At one time it was not even included in the Federal budget. Before 1969

the Social Security Trust Fund was not included in the unified budget. But there was a war going on, and someone got the bright idea to use the Social Security Trust to help cover up a wartime deficit.

A weak currency is not a cure; rather it is a symptom of a weak, noncompetitive economy. In time, the protracted decline in the dollar will eliminate the deficit in our balance-of-trade. But the price exacted will be a sharp decline in imports, and the purchase of foreign services, reflecting our relative poverty and inability to compete in the international economy.

Spencer,

I tend to agree, but it is very important to emphasize (which you do initially) that the weakening of rates allows a nation to return to a semblance of equilibrium/health – if those FX rate adjustments (see USD-Yuan 1995-2025) are artificially foiled then cancerous imbalances build up. This is manifested in China’s nearly 4 *trillion* in FX reserves.

The Yuan has been manipulated for decades to keep it undervalued – to perpetually supercharge Chinese capital investment and export growth – at the cost of Chinese consumer demand.

And for 30 years, US “leadership” has ever more farcically found ways to avoid labelling China a “currency manipulator”. History will view this as civilizational suicide.

We can by like Argentina then…

Wolf on the daily Treasury statement could you point out the lines that identifies tariff revenue. Is there any other additional lines besides customs and certain excise taxes. The numbers seem funny.. Daily $16,539, Monthly $22,304, Fiscal YTD $92,874. The numbers reported are in millions.

Are revenues being slow walked because aas the DHS attempts to manage cash flow and unbudgeted expenses. Given the freeze on borrowing. Tariffs do not seem to be a big and beautiful funding sourse just like DOGE.

This is the first time I have ever looked at the daily statement.

Where to begin. It is an unusual situation where one country, the United States of America, plagued by poverty and the world’s most punitive legal system, is reliant on the Chinese Communist Party for a majority of our manufactured goods.

In that light, I agree with the concept that Adam Smith elucidated in his treatises about the free market was too never allow the merchant class to make policy.

Great point about the deficit and Congress . The problem is not with baby boomers . If there is a problem now. There was one before with the raging inflation that still is sticky . There could be a bounce in the bond markets as the downgrade and the deficit maybe has bonds oversold but that most likely be short lived . I read someplace that the short bond trade (betting on higher rates and lower bond prices ) is one of the highest on record . They so far are proving to be right ! I personally have cash in the 5-7 year range vs money markets or longer term bonds

50% retracement of the 40 year move, puts the 10 year at 8% ish. Impossible you say? Yet….

…”For every action there is an equal, opposite, reaction”.

Keeping all my funds in 2-6 mo T-bills.

Lending money to the Treasury so they in turn can pay my Medicare and Social Security. This cannot last forever.

Well, yes the problem is the Republican Congress. They think the problem is the marginal tax rate. The dark humor about the mid west hicks being flushed down the drain to fund Trump’s tax cuts for the rich.

They, we, are about to pay for what we bought. And it ain’t good. More sacrifice.

All you do is have to look at the actions of Congress to know that the debt is something at best will give lip service to. Their salaries are adjusted to inflation so even protected from that. Tax cuts, endless and pointless wars, increased military spending are of course the easy to point to evidence. That said, lip service seems to be all run of the mill Americans need along with fictional and fearful false narratives. It isn’t like America’s problem are unsolvable but when the millionaire political class and billionaire donor class are in charge, the most vulnerable will of course pay the price

On the positive side, perhaps yields will climb so my children’s children can work to pay for them in an ever declining political and economic landscape.

Feels just like yesterday the all-knowing bond market was buying 10-year treasury yielding 0.5%. Same geniuses are now buying Mag 7.

I sure hope so, and I’ve got some money in TLT which would be at risk if long-term rates continue to rise.

I don’t see how Congress doesn’t get the message unless annual interest expense stays above $1T and moves towards $1.5T sooner rather than later.

As this $7T continues to roll over, one has to wonder if things will get nasty as we approach $40T in debt. I’ve been saying for about 5 years now Treasury auctions will start exhibit longer tails well before $50T which is the number everyone seems to think is when it will start to fall apart.

TLT monthly charts are at an inflection point to possibly breakdown hard to the next level of long term support at 75. Support levels are 82.5. 80. Gap at 78 then 75. If 75 fails then on to 65. Hedge your TLT.

No reason to get too crazy with hedges IMO. High interest rates cure themselves in a debt ridden economy. The higher interest burden promotes recession, and stocks likely decline as interest shifts to bonds.

The more predictable event is a drop in interest rates when the next recession hits hard, whenver that is.

That’s the progression I would expect. My TLT costs basis is sub $95. It’s just a paper loss with higher yields. When the recession hits, I’d expect TLT, at a minimum, will break though $120 which at would lead me to sell out.

Gambling in the stock market is a fools errand for the amateur.

The house vig.

Rates up, but trade weighted dollar down, although off it’s lows I think. Usually a sign of a confidence problem ?

What happens when the debt ceiling is raised and Treasury is fully back in the market ? I can’t help thinking the current TBond market is not fully itself until that happens.

I read the GENIUS act today. That seems like a perfect scheme to absorb a lot of Treasury demand. Still a lot left undefined in the legislation. One thing I did find interesting is that the law expressly forbids coin issuers from offering a yield on their coins but explicitly encourages them to back the coins with Treasuries.

There was some language about not requiring coin issuers to list their coins as liabilities in a balance sheet. I might not have read that carefully enough to understand exactly what it is getting at.

But it seems like an invitation to players to buy Treasuries, issue coins and keep the spread. Seems like a useful vehicle for perhaps allowing Treasury to focus more issuance on the short end under the shelter of renewed FED yield curve control efforts.

I’d love read an article from Mr. Wolf with his take on it.

After reading the act, I’m actually less opposed to it than I was. It’s clearly meant as a tool to underpin USD by creating a new bubble asset but doesnt appear to be a new kind of skynet or anything.

No article coming on crypto. Let it burn. In terms of stablecoin, backed by Treasuries, the thing is, people need to buy the stablecoin for it to have the cash to buy the T-bills. Stablecoin are used for transactions within the crypto system, and if they don’t pay interest, that’s all they’re going to be used for. So people who want to earn interest in secure assets will keep their cash in T-bills directly or in money market funds, and people who want to do transactions within the crypto environment want to use stablecoins. So I don’t think stablecoins are going to be this huge source of demand for T-bills. Some sure, but not huge.

Try the FED, they can always do QE and buy the treasuries T-bills. This would be a HUGE source of demand for T-bills. Sort of one hand of the government shaking the other. Just kidding, but knowing our government, this might not be a joke soon.

If the Fed restarts QE in an inflationary environment, we will cause MASSIVE INFLATION. Disruptive, debilitating, destructive double-digit inflation. They know that by now. They saw the beginnings of it in 2021 when they continued QE, and inflation spiked to 9%, forcing them to backtrack and start QT. Lesson learned.

Inflation and currency collapse are the two things that force a central bank’s hand.

What the Fed will do, however, and they already talked about it, they will replace maturing notes and bonds (2-30 years) with T-bills = a reverse of “Operation Twist” that Bernanke did in 2011/2012 to push down long-term interest rates. It currently has almost no T-bills ($195 billion out of $4.2 trillion in Treasuries). So if the Fed wants to bring its T-bill holdings in line with the total share of T-bills (around 25% of marketable Treasury debt), it would have to add $800 billion in T-bills and shed $800 billion in notes and bonds if the total remains unchanged. But for now, the total is declining due to QT. If the Fed goes ahead with replacing maturing notes and bonds with T-bills, it will likely put upward pressure on long-term yields.

As a side note, I realized at least one of the sources of the strong opposition to CBDC’s (Central Bank Digital Currency): it’s competition for private cryptocurrencies.

Second, as I was reading an article about ransomware, I realized that a source of demand for crypto is in the underground economy: The cryptocurrency platform Bitzlato, involved in more than 15 million USD of ransomware proceeds, was seized in January 2023. Another example is the darknet cryptocurrency “mixing” service ChipMixer, which had laundered 3 billion USD worth of cryptocurrency since 2017.

Finally, it’s another source of poker chips to be used to gamble against other players in order to obtain more currency, like non-voting, non-dividend-paying stocks.

It’s simply astonishing to me that the perception of risk has not shot to the moon long before now. Thank you Wolf. Our donations to Wolf St are the best $ we spend as a firm. Hands down.

Thank you!!

I agree. As I said before, risk is the only undervalued capital asset available.

“It’s simply astonishing to me that the perception of risk has not shot to the moon long before now”

Until the Economic Apocalypse actually occurs, most people use its lack to tell themselves (and each other) that the Economic Apocalypse is impossible…because it hasn’t happened yet. It is like being on the Titanic, while the iceberg is still out of sight.

Plus, we have a “government” whose primary desire has been to foil every warning signal effectively forestalling fundamental reform.

– Also blame the Trade War(s). US has an “exorbitant privilege” (EP) because it uses the USD in its economy. But this privilege is NOT unlimited. This “privilege” is – more or less – the size of the US Trade Deficit (TD) or the Current Account Deficit (CAD). As a result of the Tariffs Wars imports into the US have been shrinking ==> shrinking TD ==> shrinking EP. That means that the US sees less foreign demand for T-bonds and needs to sell more T-bonds domestically. Rising US rates here we come.

– If there is a MAJOR sell off of T-bonds then I actually expect the USD to go (much) higher against a range of other currencies.

Imports = cash goes overseas and circulates overseas. If some imports are replaced with local production, the cash doesn’t go overseas but stays in the US and circulates in the US, and gets spent and invested in the US, and some will end up buying Treasury securities. That’s ALL GOOD for the US. Bizarrely, you sound like that’s bad.

Keyenes fanboys romanticize the thought of US dependency on imports and trade deficits because, of course, we cannot reach our full growth potential without it. 🙄

MrFoo,

Very perceptive – in hopeless pursuit of some imaginary “economic optimum” Keynesians will mortgage every existing US asset in order to finance the endless purchase of Chinese trade goods.

They wiil/have created a wasteland and called it Paradise.

You can’t live inside your iPhone.

You can’t breathe through your iPhone.

You can’t physically travel anywhere, for anything in your iPhone.

Your iPhone *may* reduce the need to do *some* of these things…but it far from eliminates it.

Kudlow made a good point this past week we all need to think about. Does more Federal Debt increase yields or decrease them? In my humble opinion, rates are going much higher and we all need to prepare for it.

IMO, not on the margin. However, the Federal budget that was passed by the House of Representatives, proposes to double the deficit before cutting spending in five years.

A budget that proves that the MAGA electorate was played as fools, all the while they celebrate their losses.

Do we expect the US to grow faster than the interest it pays on debt in the coming decade or two??

Wolf, do you think the great reset will be from 10 year yields nearly 10% causing a major crash on all the crypto nonsense and forcing congress to cut deficit?

Oh goodness, I don’t think in those terms 🤣

In the terms that I’m thinking in, scaring the bejesus out of Congress and causing it to trim the deficit took about a decade last time. So no, Congress isn’t suddenly going to trim the deficit overnight.

Especially since they either believe (or are deluding themselves) that this combo of tax cuts and tariffs will spur growth and pay for themselves and narrow the deficit. So no, they will not do anything directly about the deficit. Come next election, they’ll say that’s next up on the docket, but we’ve heard that every election cycle for….a long time.

Yes, it will take a while to get through to our powers that be. See the 50 year long chart above of the 30year and notice how long it was over 10% in the late 70’s. Apparently congress is full of very brave souls and it takes a lot to ‘scare the bejesus’ out them. We have not gotten close yet.

Ok, you are running for POTUS…please tell us your plan to cut the deficit??? What core program do you start with first?? Who takes the pay cut? Let’s hear it.

Whomever makes the decision to cut spending, is going to get dragged for it and will enrage a massive portion of the voting block.

Someone is going to have to martyr their political careers (maybe even life) to cut spending even a little bit.

Look at the panic and outrage from the DOGE situation alone, now imagine that x100 when millions of voters have some benefit cut. There will be riots and chaos.

So please, candidate Gattopardo, tell us who takes the pay cut??

Of course they are brave, dougzero, very few of them have to worry about being re-elected. The voters have been picked for the maximum number of safe seats with only a handful of competitive seats. My congressman is almost universally hated but he can count on 60% plus from now until eternity.

@MrFoo,

Debt was 106% of GDP during WW2, and 10 years later the ratio was cut in half. The playbook has already been written for how to get out of the current mess, put Congress feigns ignorance of literacy as an excuse not to read it. Somehow, that makes in all ok, nowadays.

Mr Foo (love the handle, BTW),

It’s really not that hard*. Don’t extend the tax cuts, and you’re half way there. Trim 20% from defense. Skip the Golden Dome. You’re about 3/4 there. Keep tax on tips and OT, and some other small things. Whatever gap remains, which is likely around 5%, trim uniformly from everything except social security. I hate that method, but since a group of 535 can never agree on who should take cuts, the only way to solve it is the old fashioned way, everyone takes a cut.

*Mathematically it’s not that hard. Politically, as you note, it is. This solution requires Trump/GOP to go back on their campaign promise to extend tax cuts. But that’s way less difficult than campaigning on the above budget/tax plan.

“Apparently congress is full of very brave souls”

Behavior indistinguishable from drug addicted sociopaths.

An interesting point is that the current Congress-path Rep only has an average career of 8 years (pretty sure it used to be markedly longer 30-40 yrs ago).

So, on the one hand, pretty short time before the Congress-path is cast back into the outer darkness with the rest of us, enduring consequences of crappy, crappy policies.

On the other, pretty short time to effectively sell out to highest bidder for later personal “security”.

Of course, these people could live within reasonable means and lead lives of greater integrity – but then they wouldn’t be sociopaths.

Require states to pay 50% of their share of Medicaid expansion under ACA, institute work requirements, repeal the IRA, don’t extend SALT deduction to 40K or change treatment of overtime or tipped income, cut defense 20%, no golden dome, roll SNAP rules back to 2019, and limit tax deduction for employment related health insurance. No deficit, very minor tax increase based on limiting deductions instead of increasing marginal rates. Fixed it for you. States that want ACA expansion can raise state taxes to fund it, those that don’t won’t be bribed to do so. People keep more of their earned income and there is finally some pushback on the ever increasing leviathan of Federal spending.

Tariffs at this level is enough to reduce 300bn annual deficit. Medicaid cuts another 150bn

Not much to worry, 30 yr should be back to 3.5-4.

That’s $450B, chief. Just another $1,5T to go….

what about the yield curve steepening? False signal or was the 20% draw down the big show or are we currently in a recession? My stupid big money market position wants to know

We’re not currently in a recession, far from it:

https://wolfstreet.com/2025/05/08/recession-watch-time-to-dig-out-our-favorite-recession-indicator-again/

Like Wolf shows below, UEC have to move above 2M and then start rising towards 2.5M for there to be a recession. At this point, there’s no telling how soon or far out the next recession is. One thing seems for sure though and that it’s not right around the corner.

Is there any reason to think that the current US treasury bond rates are being driven up by events outside of the US?

Japan’s QT, or possibly Germany’s new debt laws could be changing their yields, and pulling their domestic investors back “home”, and thus out of the US?

Actually, it is unlikely that any routine sovereign bond issuance in the world would effect the 10 yr treasury. Now, a financial collapse would surely disrupt the normal functioning of the bond market.

It is, at least, a market that is at least pseudo normally distributed, then calamity is likely.

On April 9th the PBOC asked state banks to reduce dollar purchases.

China imports a lot of dollars, many of which end up in the treasuries. Many countries buy treasuries:

– Japan – $1.13 trillion

– China – $784.3 billion

– United Kingdom – $750.3 billion

– Cayman Islands – $417.8 billion

– Luxembourg – $412.5 billion

– Canada – $406.1 billion

– Belgium – $394.7 billion

– France – $354.0 billion

– …. many more …

It makes sense to buy treasuries because the US pays for its imports in dollars.

Treasury prices and yields move based on demand: high demand leads to higher prices and lower yields, while low demand leads to lower prices and higher yields.

If China and other countries decide to curb their treasury purchases, I expect higher yields.

Similarly, if tariffs reduce US imports, I expect to see higher yields.

As we know from the Treasury’s Allotment report, foreigner entities have been buying at the auctions just fine (allotment data through May 15).

America First: It is better those foreigners use their money to pay the tariffs and not buy bonds. Keep the bonds and their interest right here at home in the USA.

This may come as an added effect once imports are reduced by tariffs.

On the other side, tariff will significantly reduce issuance.

One thing I dont know is – Does foreign demand numbers include only foreign govts or also foreign private buyers? The later would be impacted by high global yields, and i expect demand drop there

Foreign demand is all foreign entities: “official” (central banks and governments) and private (corporations, banks, etc.)

Thanks for response – so the global bond yield surge is yet to impact the auctions.

I see it coming soon

Thanks. The Allotment report looks normal through May 15th. A handful of news reports said the May 21st, 20-year $16 billion auction was weaker than usual.

It does make sense that foreign buyers would slow if exports slow.

I may be jumping to conclusions, as one auction does not make a trend.

We’ll see in the next allotment report how the 20-year went with foreigners.

20-year auctions are always kind of funny. For decades, there was no 20-year bond. Then in 2020, the Treasury Dept. revived it, and so now it’s here, it’s kind of an oddball creature, the auction sizes are relatively small ($13 billion in March and April, $16 billion in May due to lack of demand), there is little liquidity in trading it because so few exist, and it often has a yield that is higher than the 30-year yield due to the liquidity issues when trying to sell it.

The PBOC issued currency is not capable of sustaining the financial transaction volume that the dollar routinely does.

A ban on Chinese products is extreme. It would be like the Chinese impose on American products.

One wise man has this opinion: ” … The Federal Reserve is up to its old money printing games once again. Earlier this month it quietly purchased a cool $43.6 billion in U.S. Treasuries. This included $8.8 billion in 30-year Treasury bonds on May 8. Several days before that, it bought $20.4 billion in 3-year Treasury notes and $14.8 billion in 10-year Treasury notes … The Fed’s stealth QE is merely warming up the printing presses. Later this year, when overstressed credit markets frost over like the Alaskan tundra, the Fed will be called upon, once again, as the lender of last resort. Jerome Powell will be forced to crank up the printing presses to full tilt … “

“One wise man has… ” LOL, That guy is an obliterating ignorant idiot who is clueless about how bonds work, how any investor with a bond portfolio has to buy bonds to keep the portfolio from vanishing before his eyes as bonds mature and are paid off, leaving a pile of uninvested cash behind.

Ask anyone here with T-bills on auto-rollover. They all understand that they’re buying new T-bills when the old T-bills mature. And T-bills mature in 1 month, 2 months, 3 months, 6 months, and 1 year. So if you have a big portfolio of T-bills, there is stuff that matures every single week, and you have to buy T-bills every single week to re-deploy the cash you got paid when they matured. Same thing with longer-term notes and bonds. The Fed has a $4.2 trillion portfolio of every type and maturity of Treasury securities. EVERY WEEK, a huge amount in securities matures, and the Fed gets paid cash for them, and has forever. To maintain the bond portfolio at a certain level, the Fed has to buy (“reinvest”) every week at auction the amounts it got paid in cash from maturing securities.

QT is when the Fed buys LESS than the amounts that mature, and so its holdings decline because it doesn’t reinvest all the cash from the maturing securities but destroys that unused cash instead. Under QT, the Fed set limits as to how much in Treasury securities it would allow to mature without reinvestment. At first the limit was $60 billion a month for Treasuries, where it would not reinvest $60 billion in cash that it got from maturing Treasuries. Last year, it lowered the limit to $25 billion a month. And last month, it lowered the limit to $5 billion. Any amount over $60 billion, then over $25 billion, and now over $5 billion in Treasuries that mature the Fed reinvests via purchases at auction.

And there is nothing “stealth” or “quiet” about it. The Fed has announced and re-announced this every time it discusses its balance sheet, including in the FOMC statement and implementation notes after the meeting. And I’ve discussed it endlessly for years in my Fed articles.

That ignorant idiot just doesn’t ever read any of the Fed’s publications or press releases, or anything on this site. Instead he makes up stupid-ass lies. And then the WSJ and MW allow him to publish these lies as an opinion piece to pollute the brains of all the clueless readers.

And then I have to waste my time on this BS, when people could just read my articles instead, and ignore that ignorant idiot.

Note that the MBS roll-off is not limited. MBS don’t mature off the Fed’s balance sheet, they shrink because the Fed gets the passthrough principal payments.

Those are the times I feel Wolf St should be paid service. The knowledge is sometimes ignored because its free.

I am not saying we all have to agree to Wolf’s view points. But we have to agree on basic mechanisms on how FED is doing QT. It is well published, documented and seen in FRED numbers as well as 3 years of QT articles published monthly (First Thursday of Month after FED releases its monthly balance sheet). Right from QT started, Wolf has been writing about how QT works.

I was completely clueless about how FED works until I started following Wolf St. But just reading his articles I have more knowledge. I am sure many people here say experience. But I READ his articles. I didnt take it lightly because they are Free.

SRK – …when it comes to economic issues (and freely-admitting that I don’t pretend to play in high-finance sandboxes), Wolf has been my longtime Law of Gravity, diligently-reaffixing the license numbers on those particular runaway trucks (among the many others) that can imperil one’s individual life on our spacecraft…

may we all find a better day.

Agree completely, with the exception that we don’t just read the articles, we RTGFAs.

Just a quick tip to those who use the autorollover option with Tbills bought at auction at Schwab. You lose a week of interest at each autorollover event. It is best to buy Tbills manually at Schwab. You can time it so that you buy a new Tbill exactly when the old Tbill matures. Three month Tbills always settle and mature on Thursdays. Call Schwab’s bond desk to confirm. If you do not have a lot of money to play with, it probably does not matter much. If you have enough where you would kill for one basis point, it matters a lot.

In my comment about Tbills at Schwab, I am referring only to Tbills bought at auction.

Not sure why anyone uses Schwab or any other platform to buy T-Bills.

I use TreasuryDirect. dont lose any day interest. You can buy in advance in multiples of 100.

SRK, you cannot sell Treasuries through Treasury Direct. You have to transfer the bill, note, bond, to a brokerage account. I don’t know how long it takes to do this, but I am sure it is not instantaneous. If you always hold to maturity, it doesn’t matter, but I like to keep my options open. Also you cannot buy (or sell) Treasuries in the secondary market at Treasury Direct. So you are limited to buying at auction and holding to maturity.

Yikes, Wolf and I responded at almost exactly the same time and said almost exactly the same thing.

No problem, I deleted mine.

After the first round of QE, pundits from the popular financial news talked about~ QE Lite”:

This refers to a type of QE where the focus is on managing the composition of the balance sheet rather than massively expanding it. The Fed might buy new bonds while letting others mature, keeping the total assets relatively stable.~ the pundits thought QE lite was stimulating,. For the past 14 years I thought QE lite was stimulus, too. Honestly, I don’t know. Smart people(traders$) love the expression, It’s all at the margins!

“persistent chanting by the Fed and Fed governors”

nice visualization!

If Congress does not pass the Big Beautiful Bill, on January 1st everyone will get a tax increase. The income tax rates will revert back to the 2017 rates. I would argue that a “Cut” is reducing an existing tax not keeping the tax rates at the current rate. Words do matter. Notice that all of the Never Trumpers loudly call the bill a tax cut.

Your forgot the additional and new tax cuts in the bill.

With interest payments headed towards 1T and higher congress will be forced to cut deficit one way or another they cannot afford the treasury yields to go higher as interest payments will be much higher

Why does everyone believe Congress will need to take action? Over half of Congress are millionaires, make a healthy salary that stays ahead of inflation and get solid pensions. Congress does what it does to try to get and stay elected. Expecting that a magical number will change the behavior is unexpected and if it does change it won’t be the donor classes that are impacted, but a continued rollback of New Deal and other programs. What can be given can just as easily be taken away and we are seeing that now.

I’m old and cynical, and I agree with your perspective. When Congress takes action it tends to serve itself first.

https://www.irs.gov/retirement-plans/weighted-average-interest-rate-table

“The bond market scaring the bejesus out of Congress and the White House for years to come – not just a brief episode that blows over – is likely the only force that can get them to trim the deficit. But that’s not happening right now.”

Looking at the surplus/deficit to GDP curve, it appears that this process would take ~10 years of the ratio being around -5% or worse before we would see any Congressional and White House response (based on the late 1970s/1980s followed by the 1990s):

https://fred.stlouisfed.org/series/FYFSGDA188S

But then if we look at the period ~ 2010 – 2025 (~15 years), the average deficit to GDP has been a lot worse, so whatever metrics the bond market was using in the past–are they the same today? Or maybe there was less intervention in the bond market historically, and over the past ~15 years, we effectively have had bond market manipulation by the Fed (although I guess we do not call it that when central banks do it)? We have a moral hazard feedback loop, where the Fed will intervene in the bond market, and so it can be complacent?

Long-term interest rates are largely determined by inflation expectations. The expectation that price levels will chronically increase injects both an “inflation premium” and added “risk premia” into longer-dated maturities.

Under these assumptions, the present supply of loan funds would decrease (in both a quantitative & schedule sense). I.e., lenders as a group, reduce the volume of loan funds offered in the markets, & refuse to loan any particular volume of funds (except at higher rates that will compensate for the expected default risk, and future projections of inflation).

I.e., higher inflation expectations generate higher inflation premiums. The higher the expected rate of inflation, the higher long-term rates will climb. This is the kind of economic milieu that perpetuates stagflation.

The disparity between the rates paid by the federal government as compared to private sector rates will widen.

The inflation premium is currently being held down by a supply demand shock in oil.

Standard and Poors last U S downgrade was August 5 2011 when the debt was 15 trillion.

With 30 trillion debt now on the way to 50 trillion you might speculate that they will cut another notch.

Would that raise interest rates and what would the U S interest payment be for 50 trillion.

When too many of these folks or algos are just licking their chops and waiting for even higher yields, instead of jumping in and buying now, that’s what causes yields to rise.-wolf

you stated that foreign demand has been just fine for the bond market. But what about the domestic demand? Are bond holders in the U.S buying less/selling bonds outright? Any specific data on domestic bond holders?

Also, when the treasury general account gets refilled after the debt ceiling gets suspended (possibly in august stated in your previous article) what type of effects are we going to see with significant less liquidity to refill the TGA. Stock market falls, Reserves fall and yet apparently, we seeing people waiting for higher yields.

Thank you!

I update this quarterly because a lot of the specific data comes out quarterly. Here is the last one:

https://wolfstreet.com/2025/03/18/who-holds-the-ballooning-us-government-debt-even-as-the-fed-and-foreign-holders-unloaded-treasury-securities-in-q4/

Mutual funds seem to be the largest bondholders domestically. In that article you state they bought 335 billions of t-bills in Q4. Do you know what percent are t-bills, notes and bonds of 335 billion? Any information on Q1 in 2025 for those mutual funds?

I think there is a misconception here.

A T-bill with 3 months left to run trades like a 30-year Treasury bond with 3-month left to run. They’re essentially interchangeable. Money market funds only buy notes and bonds that are near the maturity date (within one year, and most often less than that). So they have T-bills and they have longer-term bonds, but they all mature within 1 year, and most of them much sooner.

When you want to buy a 6-month Treasury security in the secondary market through your broker, they will present you with a list of all kinds of Treasury securities that mature in about 6 months, including 30-year bonds.

I believe the only way govt. spending will get in control is a complete crash of the current system,till then feel pols will kick can down the road ect.

Enjoy this long weekend and lets all take a few moments to think about ALL who have died in wars,wars mostly due to bankers/mic ect.

Right now there is a sweet old grandma who wants to buy her grandkids a U.S. EE Savings bond, which doubles in price over 20 years, earning 3.55%

But why should Grandma do this quaint American ritual passed down for generations when the 30 year & 20 year is at 5%?

They killed a great American tradition. Time to end U.S. EE saving bonds for poor people?

Maybe keep the I bond?

Asking for poor people. I think we’re all getting closer & closer to the poor house.

EE bonds used to be guaranteed to *at least* double within 20 years. In practice, they paid much more than that pre-2005. The post-2005 EE bonds are abysmal, and the USA is practicing a form of usuary by issuing them. Perhaps that can also be said for the 10yr and 30yr Treasury, given current interest rates, bond issuance levels, and government fiscal spending philosophy.

Savings bonds are tax-deferred for 30 years or when redeemed before 30 years. This is their main attraction, imho.

DM: Trump insiders explode over Big Beautiful Bill… as bond market issues chilling warning: ‘Prepare for punishment’

Trump administration insiders are worried that Republicans are in a no-win situation when it comes to the Big Beautiful Bill. A major donor of President Donald Trump and his crypto czar think Congress is flubbing the president’s promised tax and budget overhaul and warn the final version will likely hurt the middle class.

The CRB commodity index is up 16 percent since September 10, 2024. Inflation expectations are high. The supply side shock in oil is holding rates down and the inevitable change in SLR will keep rates masked.

“The US is facing an interest expense problem approaching

5% of GDP – by far the largest of any other major economy.”

As the interest expense becomes the largest component of the deficit, the increase becomes exponential.

Great article. I think most of us agree taxes going up is necessary. My problem is that why would I trust these people? Look at our history of spending.

I’m 38. Just in my lifetime I have seen the iraq and afghan war, the patriot act, wall street bailout, cash for clunkers, auto bailout, Ukraine war funding, huge defense budget with over runs for every single new ship or plane, 2023 or whatever year bank bailout, inflation reduction act, etc etc etc.

There is zero trust in these people. They are not serious about the future.

The core issue is that the U.S. is sliding towards oligarchy. Political influence is easily and openly bought (from both sides of the isle), there are no apparent alternatives due to your ingrained 2-party system, and our checks&balances are being hollowed out at an incredible pace. Income and Wealth inequality are steadily rising, and it’s being felt at every level. People, like yourself, are tired and angry, but our attention is masterfully drawn away by populists. We are being bombarded with ads/propaganda more than literally any other country on earth, every day of every week has a new ‘HUGE THING (trust me, it’s huge)’ telling us to be outraged about something else.

Until people start holding eachother responsible for disengaging from political life or blindly following whoever is shouting loudest instead of critically thinking what would be best for society as a whole, jackshit is going to happen. Get informed (like on this site, good job!), talk to your friends & family about what’s happening to this country and how it’s affecting all of our lives. Democracy can only work if the People put effort into it, otherwise we end up being ruled by the few.

Thanks Jorg – Well said. I agree that this site with its focus on data and analysis – rationality over BS – is a good example of how we should be operating (I include myself in this, in that it is easy to get caught up in drama). I think you are right that there is already enough amplification in capitalism, where those who have spare money can make more just because they have money. But then if the government adds more amplification versus serving as a regulator of capitalism, it’s not good. Then we end up with a few people with more money than god who call all of the shots. Add in deficit spending as a tool in government amplification without broad-based GPD growth (where everyone benefits) and it’s a time bomb. Time will tell.

“holding each other responsible”

And that right there defines the political systems that resulted from the last couple of hundred years of human experience.

Be careful what you wish for.

I am about the same age. My observations throughout my life have led me to believe our Federal government and the Federal reserve are both abject failures. I will throw in the MSM as well. A bunch of self serving liars that can never be trusted.

It’s OK to say…

End the the Fed

Idontneedmuch: The grade all depends on the grading criteria.

If the goal is to gut “democracy” and wrangle capital markets to fuel inequality?

A+++

Some fundamental problems include: nationalism and conditioning.

We “all know” that our country is the best (GOAT!), that democracy is the best (no other system is fair and regulated like mine!) AND capitalism is the best.

Also: that America WAS great… and must be made that way AGAIN.

The FED is obviously concerned about the upcoming fiscal deficits. They are going to eliminate the SLR this summer prior to refilling the TGA.

The next Fed Chair will raise the inflation target. Trump and Bessent think they can outrun inflation.

If the Fed raises the inflation target, the 10-year Treasury yield will spike, and mortgage rates will spike, because all this stuff trades off inflation expectations for future years, and if the Fed is happy with 4% PCE inflation (=ca. 4.5% CPI inflation), and obviously allows it to run over a little, the 10-year yield might hit 6.5%, and mortgage rates 8-9%. Are you ready for this?

Everyone at the Fed and in the Treasury Dept., including Bessent, knows that.

Meanwhile, in JGB-land, unrealized losses are influencing liquidity and adding instability to the zinga towers:

“For example, Nippon Life – which is Japan’s largest life insurer – just reported a tripling of paper losses on domestic bonds to ¥3.6 trillion ($25B) last fiscal year because of rising rates crippling the bonds on their portfolio. Thus, the firm recently announced plans to cut its sovereign debt holdings (meaning even less demand for JGBs).”

“Badgering” Powell to lower rates wouldn’t backfire like last September at this point because of N-gDp level targeting smooths the short-term money market fluctuations.

Wolf great article. The long end is at a very important tipping point.

The bond markets around the world are becoming sensitive to deficits. Bessent is very aware of the situation and will definitely do something with the SLR. I’m not so sure other than a knee jerk reaction will help the long end. As far as I’m concerned I think it will increase inflation expectations. This would be a perfect time for the bond market to make its point about getting serious about the deficit while the Senate is hashing out the budget.

Despite growing pressure from bond markets, governments continue to resist spending cuts. The United States leads in deficit spending, with a deficit that was equivalent to 6.4 per cent of GDP in 2024, according to the U.S. Congressional Budget Office. This is compared to other larger economies, according to Trading Economics, such as France (5.8 per cent of GDP in 2024), the United Kingdom (4.8 per cent in 2024) and Germany (2.8 per cent in 2024). Canada’s deficit to GDP ratio was two per cent, according to the government’s 2024 Fall Economic Statement. Interestingly some countries have moved toward budget surpluses, such Norway, with -13.20 per cent of GDP in 2024 according to Trading Economics, showing that fiscal discipline is possible despite global headwinds.

From Financial Post

Norway is a special case because of its massive per capita revenues (and taxes) from oil. The oil industry accounts for over 20% of GDP. Norway has had an average budget surplus of over 10% of GDP since 1995. Norway has certainly managed its windfall well, but it isn’t comparable to the larger and more diversified economies you mention.

This is a cut and paste from FP, not me. Agree Norway different.

Another difference apart from not being a major trader, they have world’s largest Sovereign Wealth Fund. They could pay off their national debt tomorrow.

You’ll amass a large sovereign wealth fund if you run budget surpluses of 10% of GDP, on average, every year for 30 years.

Is there any need for the Gov to sell that many 20-30 bonds? Most debt is short term and they dont seem to have a problem funding the gov especially with rates over 4%

Otherwise when the debt bubble bursts is anyone’s guess? Just like the .com bubble or Japan’s housing bubble

“I think there is a misconception here.

A T-bill with 3 months left to run trades like a 30-year Treasury bond with 3-month left to run. They’re essentially interchangeable. Money market funds only buy notes and bonds that are near the maturity date (within one year, and most often less than that). So they have T-bills and they have longer-term bonds, but they all mature within 1 year, and most of them much sooner.

When you want to buy a 6-month Treasury security in the secondary market through your broker, they will present you with a list of all kinds of Treasury securities that mature in about 6 months, including 30-year bonds.” – Wolf

So, what you’re saying is that mutual funds aren’t the active bondholders that actually buy long term bonds for the whole duration until maturity? But does selling 30-year with 3 months until maturity have an effect on yields at all? Wouldn’t that have an effect on the 3-month T-bill yield?

The other question is that who are these bondholders that are increasing the yield by waiting on the sideline? From your article, the next one would be U.S households and non-profit organizations. It states that they shed 229 billion? Is shedding defined as selling them outright or letting them mature and reducing overall treasury securities? And do you have the data on how it was broken down by T-bill, notes, bonds?

1. “So, what you’re saying is that mutual funds aren’t the active bondholders ..”

No, that’s not what I was saying. What I was saying:

— You can’t go by what is a T-bill and what is a longer-term security. What matters is when they mature when you buy it. If you buy a 10-year Treasury with 6 months left to run before maturity, it’s like buying a 6-month T-bill.

— I was using the example of money market funds — they’re a big part of the bond mutual funds, and they constantly buy because they only invest in securities that mature in less than 1 year.

2. “…who are these bondholders that are increasing the yield by waiting on the sideline?”

Me 🤣

And a gazillion other people.

3. “Is shedding defined as…”

It’s defined as “reducing your holdings,” and it doesn’t matter how with bonds, unlike stocks. You actually have to sell stocks to liquidate your portfolio. But with bonds, to liquidate your portfolio, you just sit on your hands and watch it happen as they mature.

4.44% should be the sell the rally for $tnx, maybe people will hit orders above that or right about now people will sell the 10 year! $vix hit support now and buyers came in. Ball is in the bulls hands to fumble,

Yesterday risk on Pop was fueled by 1.3ish% drop in the yen. Carry trade is at risk to create global risk off; or will it be continued risk on for few more days? Bitcoin was unable to make new highs priced in the major world currency. Sure, bitcoin made slightly higher high prices in $usd but was unable to carry the ROW fiats to new highs. Sellers came in priced in other currency and got their shirt money back!! $tnx should march higher, the great algo is on hold until fed minutes. Hopefully, fed minutes are exciting and will give Wolf an article to write about.

For many reasons, but mainly because risk is being repriced, interest rates are going up. It’s not personal, it just MATH and risk…