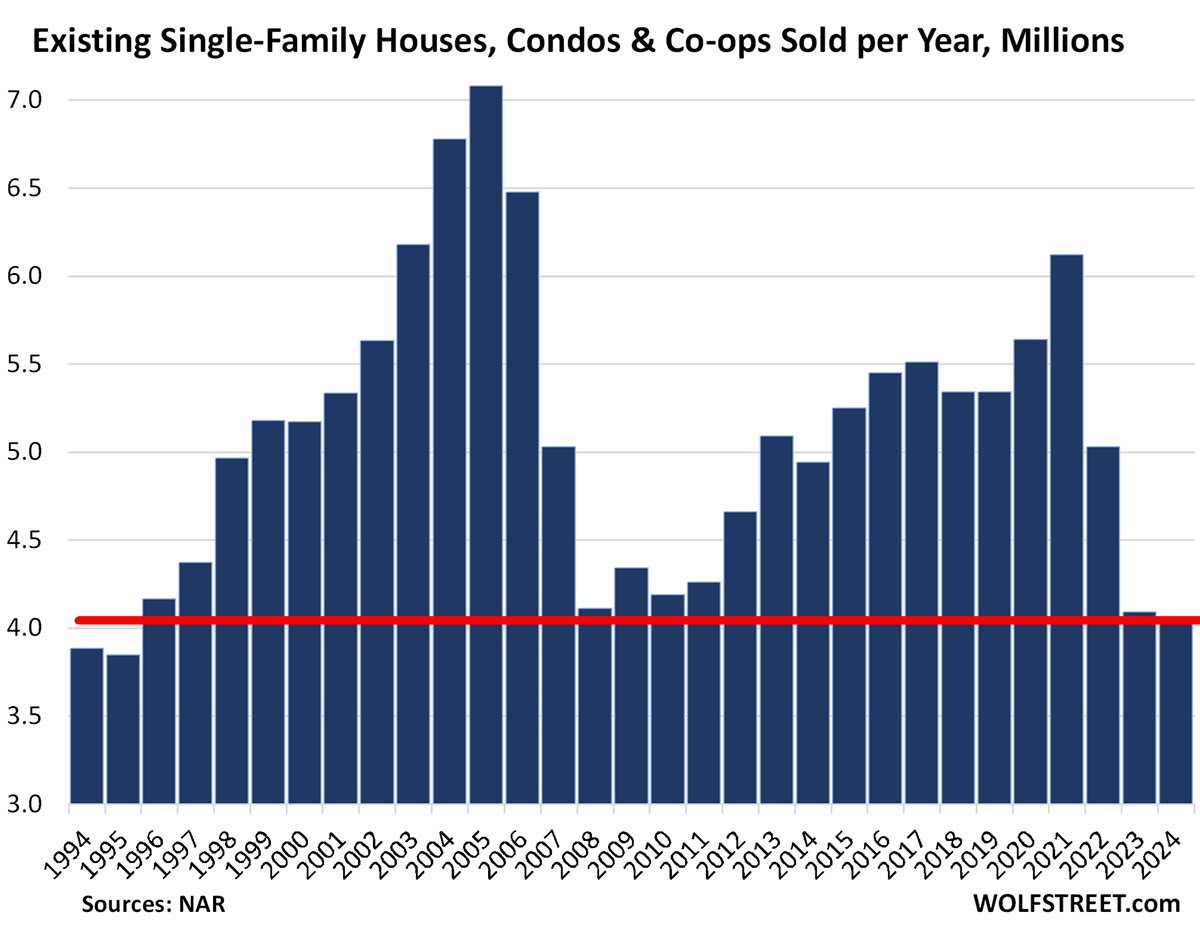

2024 was the worst year since 1995 for sales because prices are too high after the 50% spike in 2019-2022.

By Wolf Richter for WOLF STREET.

The market for resale homes has started to thaw just a little from its frozen condition as more buyers and sellers started getting used to the 7% mortgage rates, rather than waiting for them to plunge or whatever. And more “locked-in” homeowners are selling their homes to deal with changes in life, thereby giving up their below-4% mortgages. So sales volume ticked up a little over the past few months from the deep-freeze levels before, but remained still very low.

Sales of existing single-family houses, townhouses, condos, and co-ops that closed in December rose to 329,000 homes, not seasonally adjusted, up by 10.8% from December 2023, but still down by 36% from December 2021, testimony to the ongoing but slightly softening demand destruction.

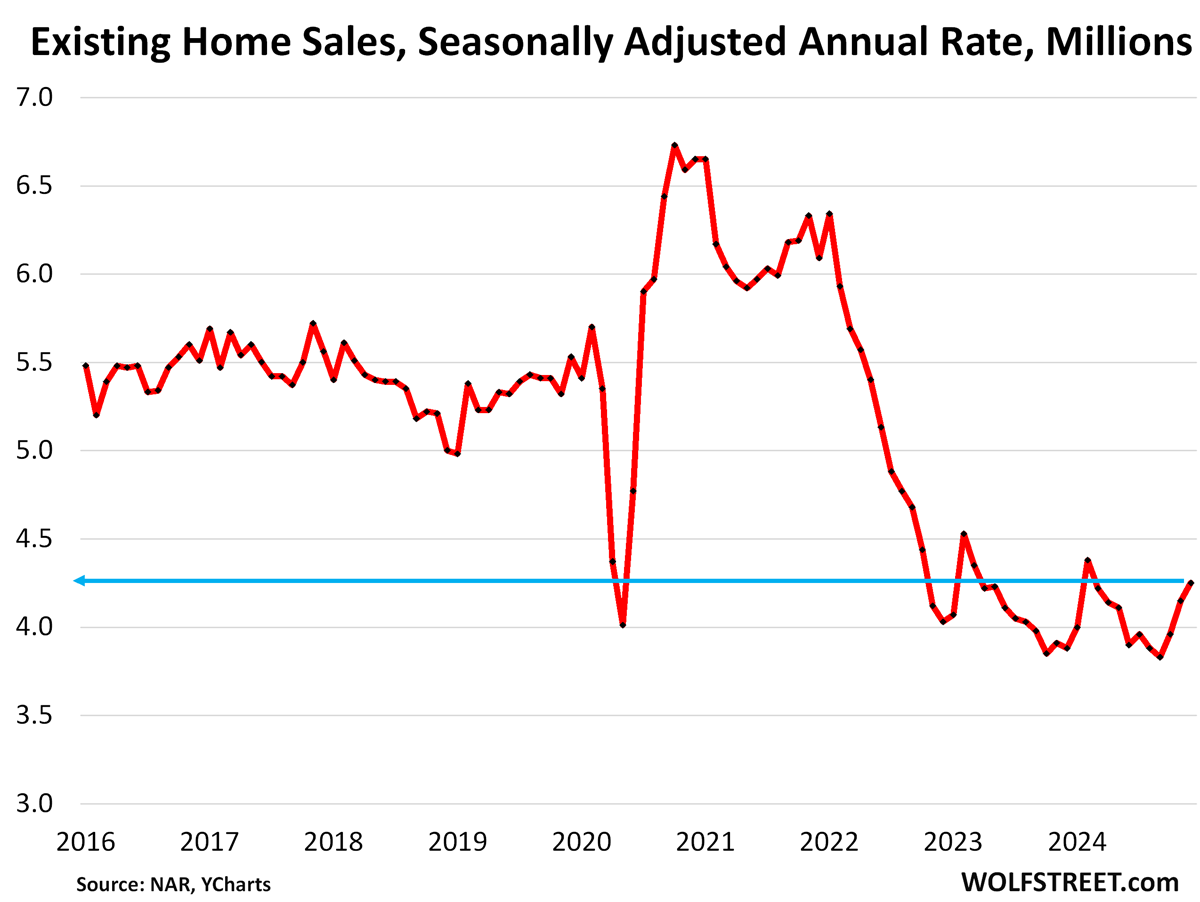

The seasonally adjusted annual rate of sales, which attempts to iron out the seasonal changes and multiplies this out to a 12-month period, rose by 2.4% in December from November to an annual rate of 4.25 million homes – down by 30% from the rate in December 2021 and by 23% from the rate in 2019, according to the National Association of Realtors today (historical data from YCharts):

For the whole year 2024, actual sales fell to 4.06 million homes, the lowest since 1995, below even the worst years during the Housing Bust, when demand destruction was caused by an economic and financial meltdown that followed years of reckless mortgage lending.

But in 2023 and 2024, demand destruction was caused by a historic spike in home prices in the prior three years, when the NAR’s national median price shot up by nearly 50% from June 2019 through June 2022 – which then collided in 2023 with mortgage rates that returned to the normal-ish levels before the money-printing era started in 2009.

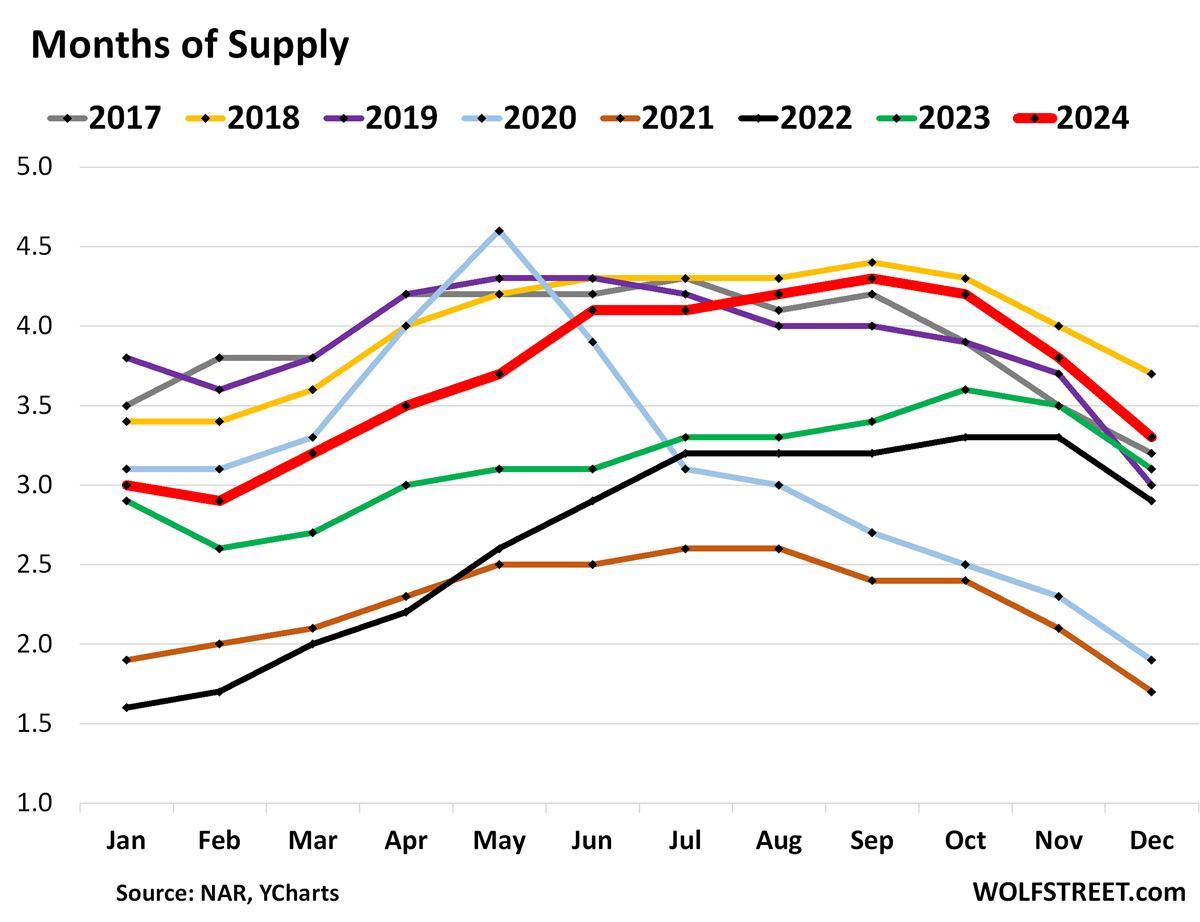

Highest supply for any December since 2018.

Supply of unsold existing homes on the market, at 3.3 months (red line in the chart below), was the highest for any December since 2018, and higher than 2017 and 2019-2023.

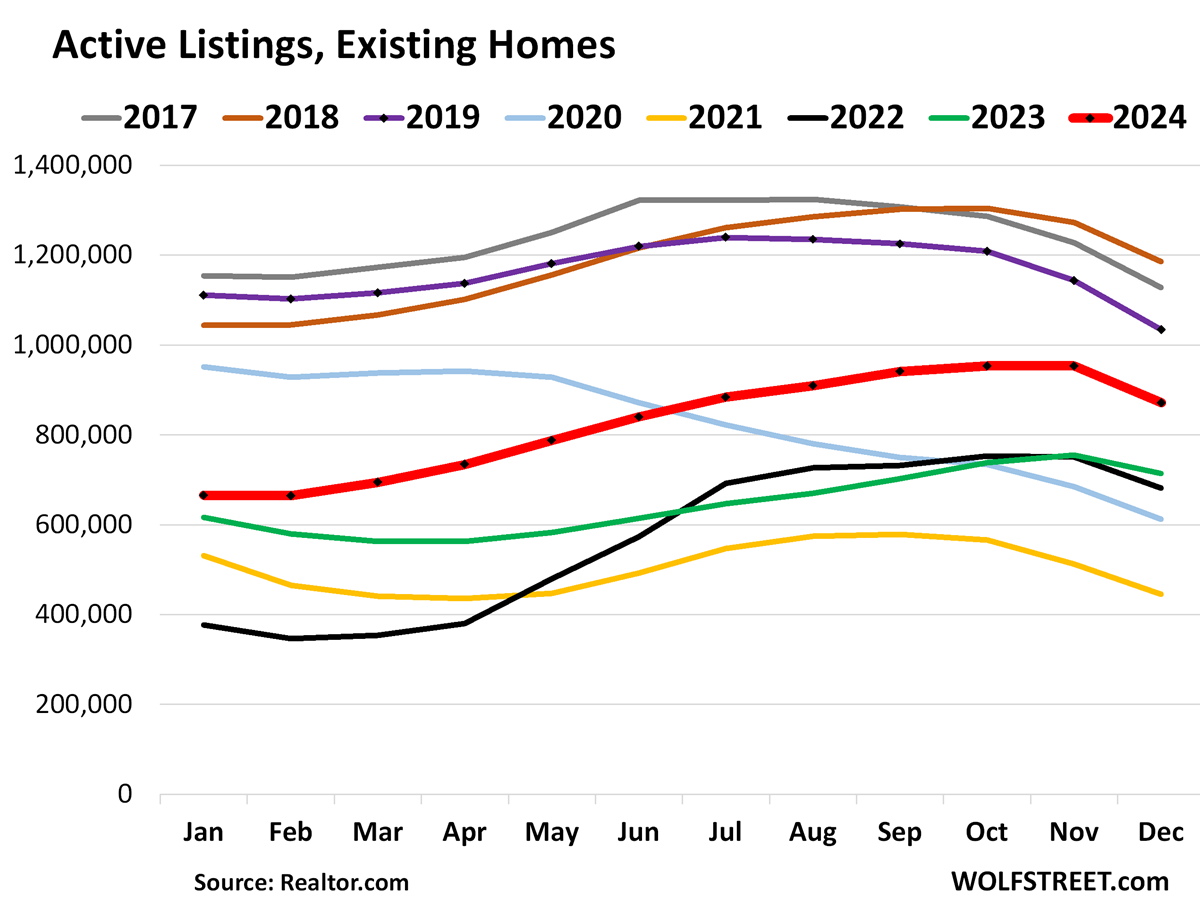

Active Listings doubled since 2021.

Active listings – total inventory for sale minus homes whose sales are pending – at 871,500 in December (bold red line), were at the highest level for any December since 2019, having nearly doubled since December 2021 amid the plunge in sales.

Unsold inventory, at 1.15 million homes, was up by 16% year-over-year. Over the holiday period in December, demand dries up, homes get pulled off the market, new listings dry up, and what is on the market, sits there longer without selling.

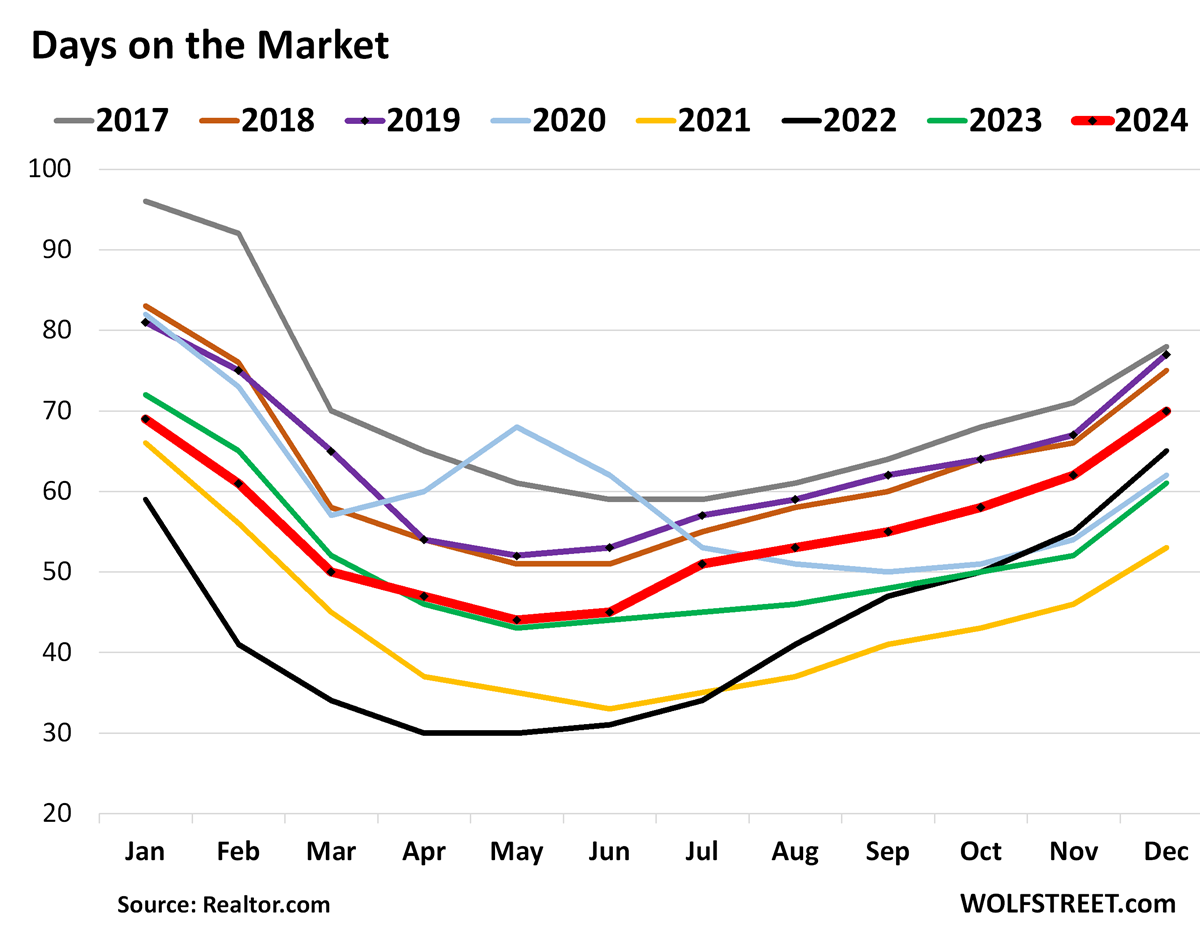

Days on the market lengthen to 70 days.

The median number of days before the home is either sold or pulled off the market because it failed to sell rose to 70 days in November, the most for any December since 2019, and up from 61 days a year ago, according to data from Realtor.com.

Days on the market track the mix of how motivated sellers are by letting their home sit on the market when it doesn’t sell right away, and how quickly homes sell that do sell.

Prices are too high.

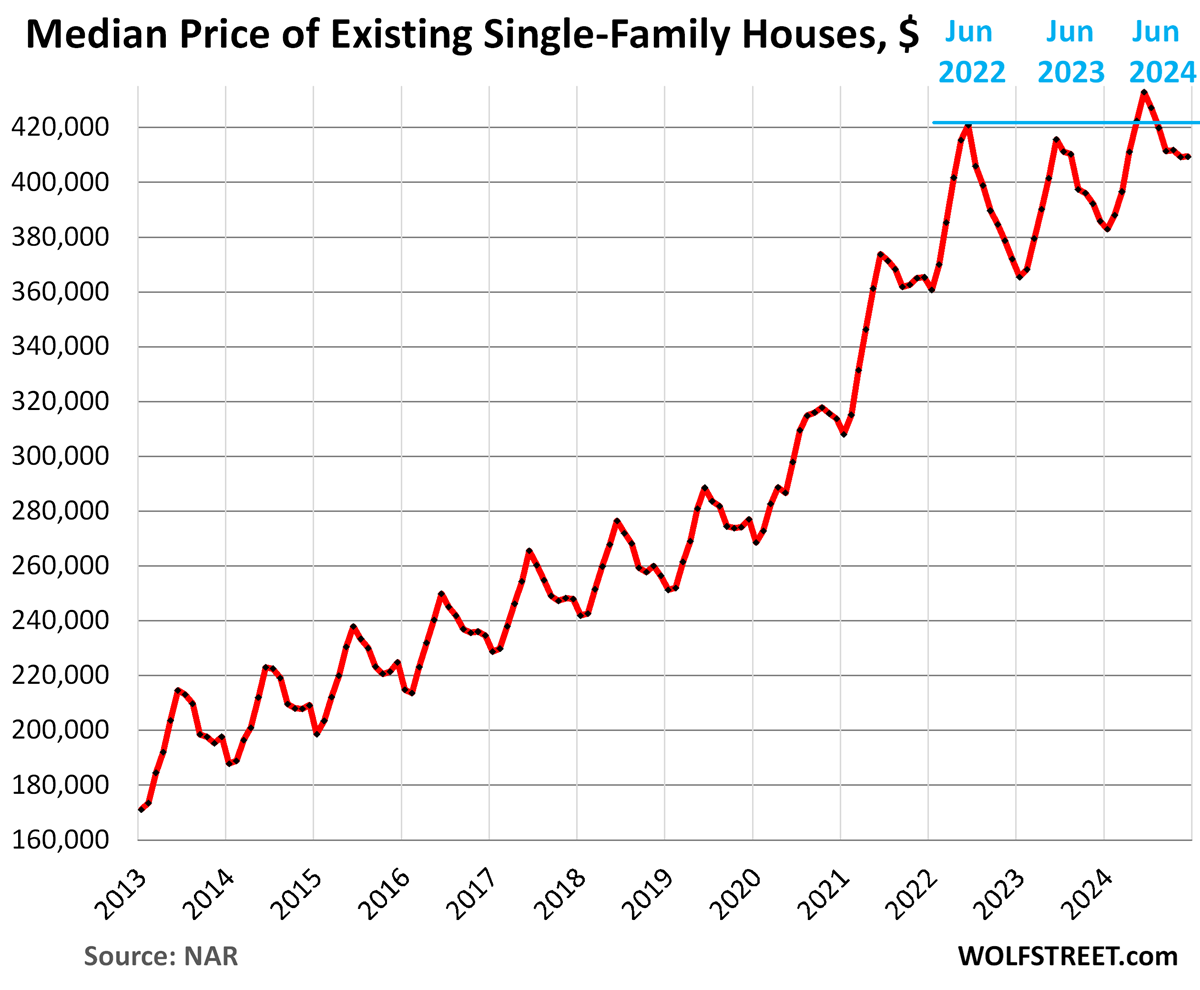

Single-family house prices. As has been the case for months, the median price of single-family houses was revised down for the prior month, which also reduced the year-over-year gain for that month. For November, the median price was revised down to $409,200 from $410,900 originally reported a month ago, which shaved the year-over-year gain for November to +4.3%, from the originally reported +4.8%. These downward revisions keep happening. I bring this up because the December year-over-year gain was an outlier of +6.1%, the highest since October 2022, but when the December median price gets revised down next month, the year-over-year gain will be back in the range of other year-over-year gains in 2024.

Based on the pre-pandemic seasonality, the median price drops sharply in January, and January-February mark the seasonal low points.

The 50% price explosion between June 2019 and June 2022, on top of the large price gains in the prior 10 years, was driven by the Fed’s interest-rate repression and money-printing schemes which have created the #1 problem in the housing market today: Prices are way too high.

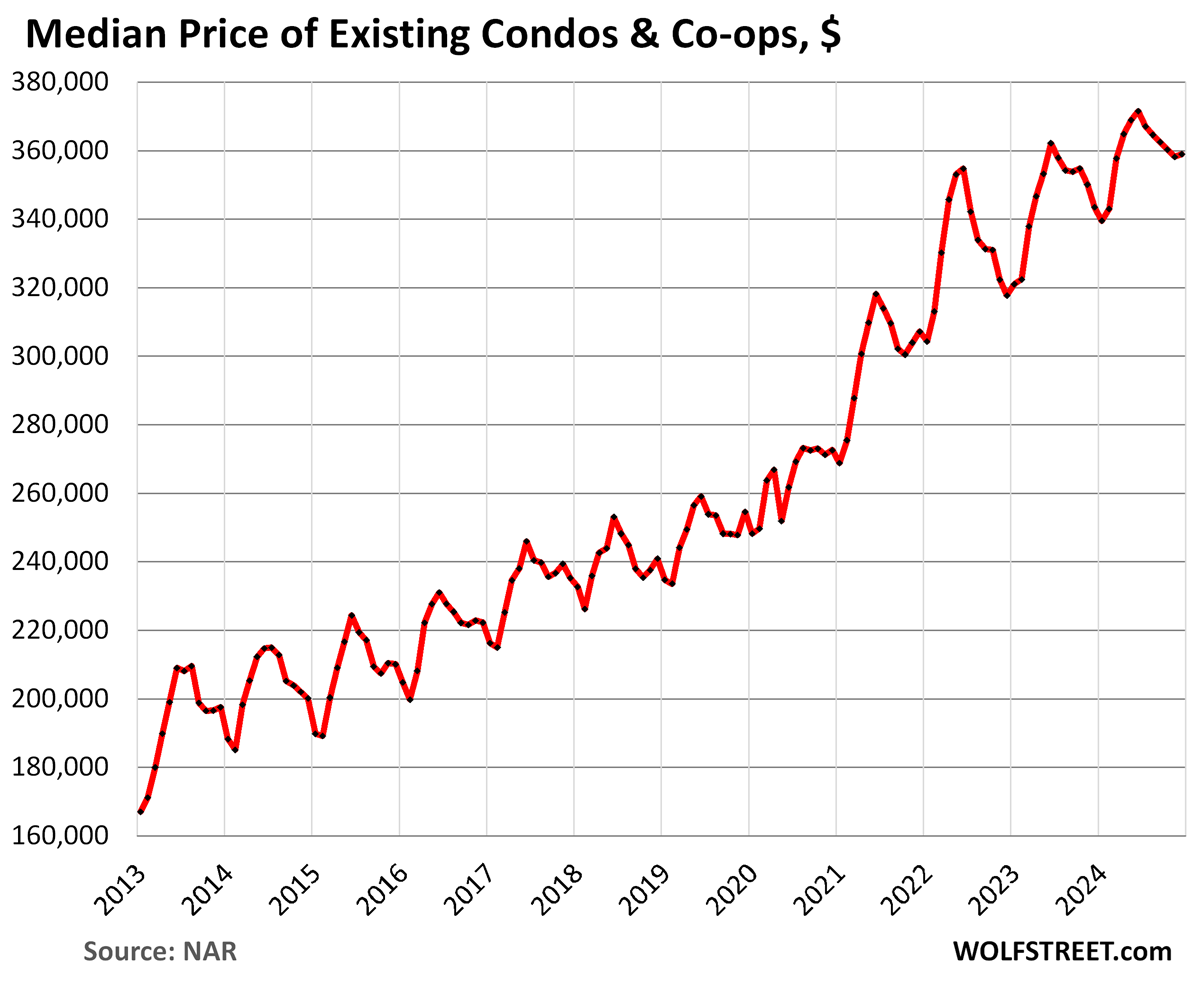

Condo and co-op prices. Here too, as has been the case for months, the median price of condos and co-ops was revised down for November to $358,200, from the originally reported $359,800. This shaved the year-over-year gain to +2.3%, from the originally reported +2.8%. And so we can expect that the December median price will also stick with tradition and get revised down as well.

As reported today, the median price in December, at $359,000, was up by 4.5% year-over-year, and we expect tradition to continue with a downward revision next month. Unlike single-family house prices, the median condo price didn’t experience year-over-year declines in mid-2023.

But home prices vary widely by metro.

In a number of the largest cities, prices of single-family houses and condos have been dropping for over two years.

Double-digit price declines of single-family houses from their respective peaks in 2022 or 2021 occurred in four of the biggest cities:

- Austin: -19%, to lowest price level since 2021

- Oakland: -17%, to lowest since 2020

- New Orleans: -17%, to lowest since 2020

- San Francisco: -15%, to lowest since 2018

Double-digit price declines of condos and co-ops from their respective peaks in 2022 or 2021 occurred in seven of the biggest cities:

- Austin: -21%, to lowest price level since 2021

- Oakland: -19%, to lowest since 2016

- San Francisco: -15%, to lowest since 2015

- Detroit: -13%, back to 2018

- New York City: -13%, back to 2017

- New Orleans: -12%, first seen in 2016

- Seattle: -10%, back to 2017.

Here are all our charts and data of the big cities with the biggest price declines from their respective peaks years ago. And here are our charts and figures of home prices in the 33 biggest metropolitan areas, from steep declines to ongoing increases, documenting the divergence in the US housing market.

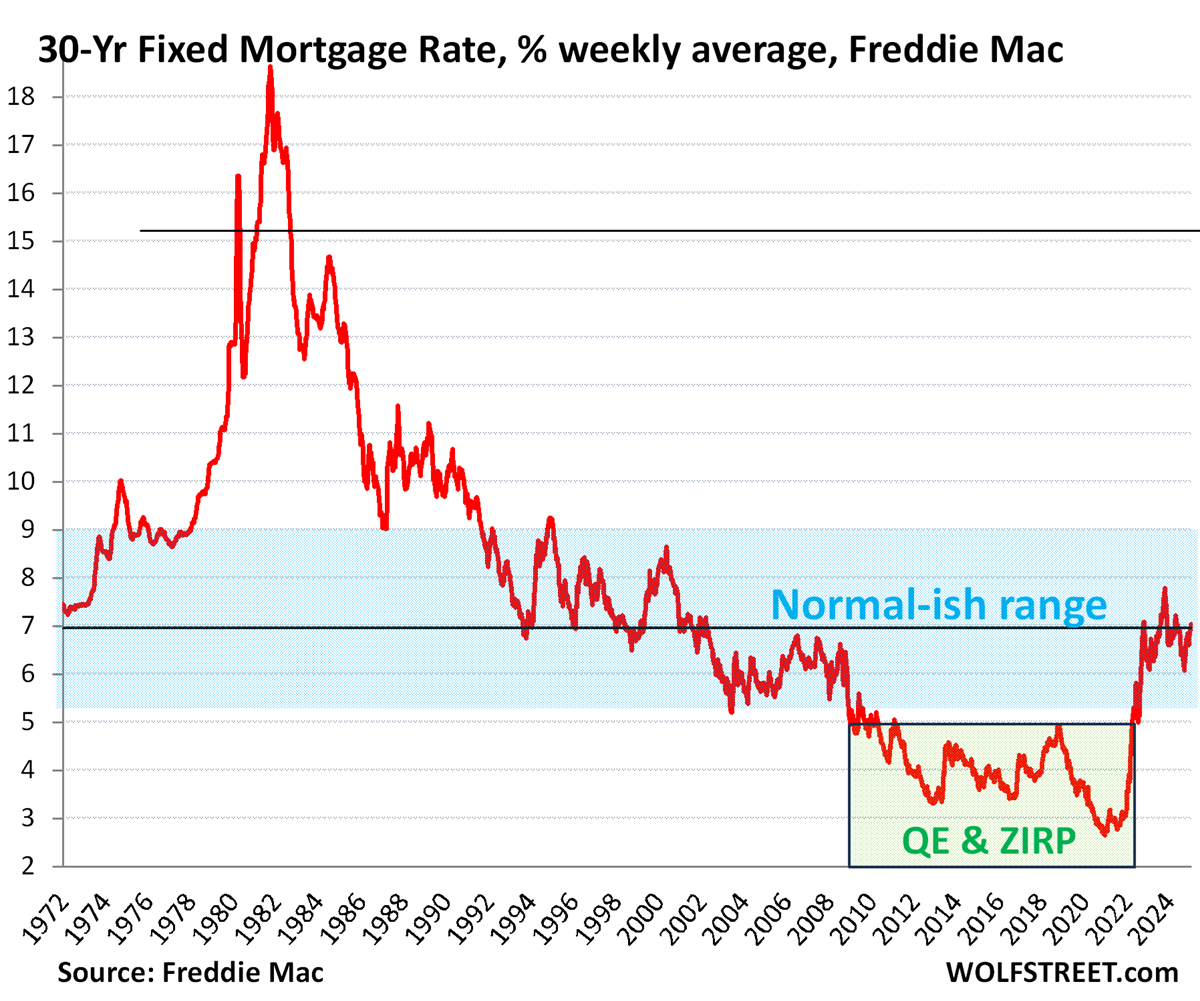

Slowly getting used to the old normal 6-7% mortgages.

The average 30-year fixed mortgage rate has been above 6% since September 2022 and above 7% on and off since October 2022. The daily measure by Mortgage News Daily is today at 7.11%. Freddie Mac’s weekly measure, released yesterday, of the average 30-year fixed mortgage rate was 6.96%.

The real estate industry has now given up waiting for mortgage rates to plunge to wherever and is encouraging sellers and buyers to get used to “a new normal of mortgage rates between 6% and 7%,” as the NAR had put it, which are the old normal rates that prevailed before the money-printing era started in 2009..

The CEO of Fannie Mae, the largest Government Sponsored Enterprise that buys and guarantees mortgages, also encouraged buyers, sellers, and everyone in the industry to get used to these 6% to 7% mortgage rates.

Before the money printing era, the average mortgage rates had been well above 5%. The Fed’s QE and zero-interest-rate policy, which started in 2008 and, with some interruptions, finally ended in 2022, had created an anomaly:

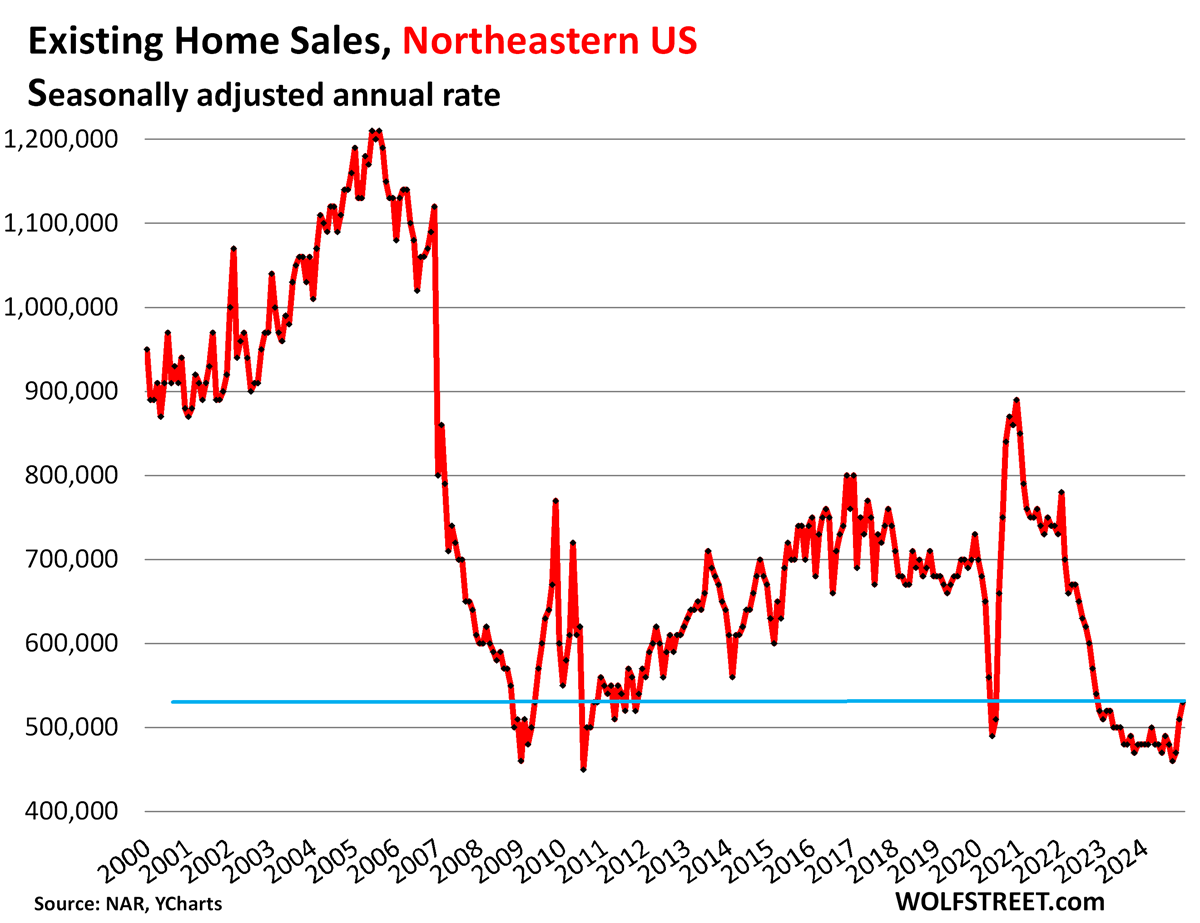

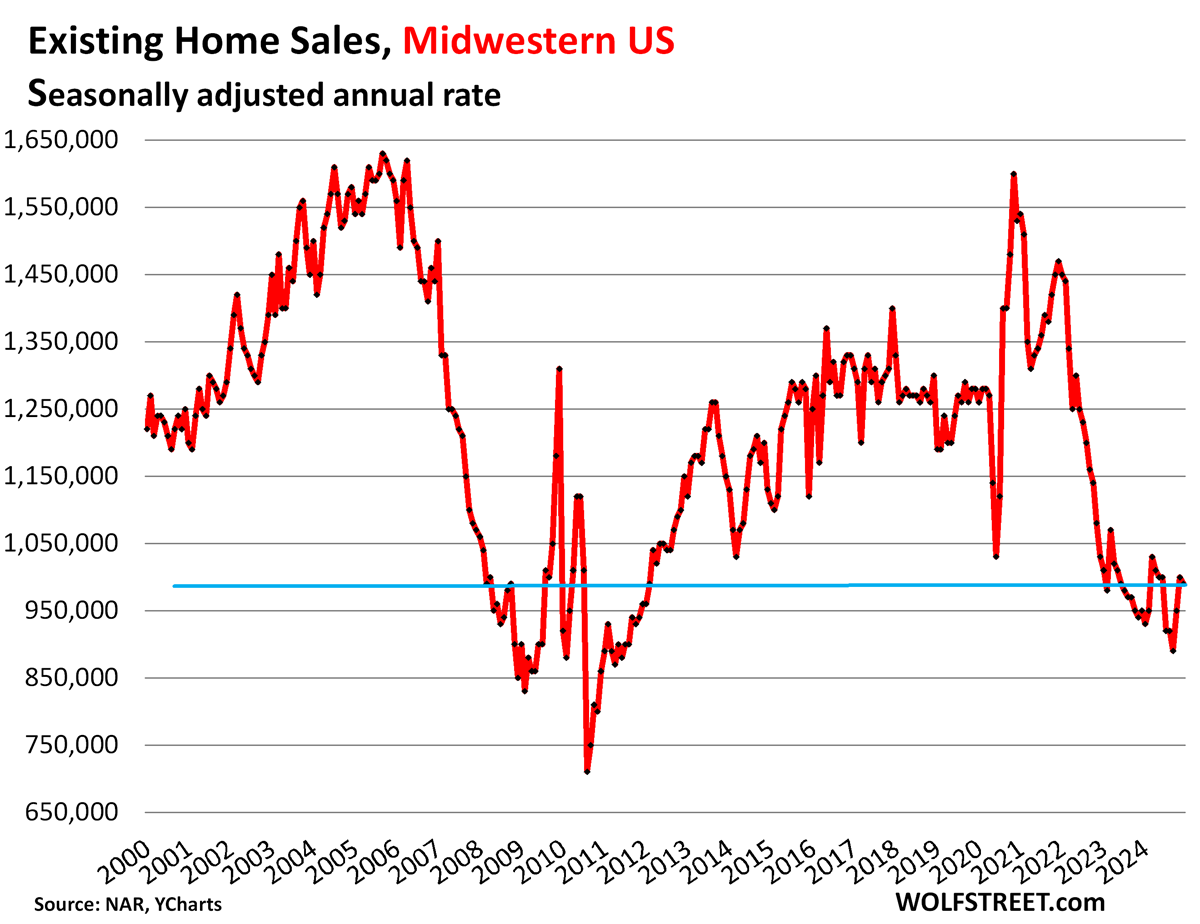

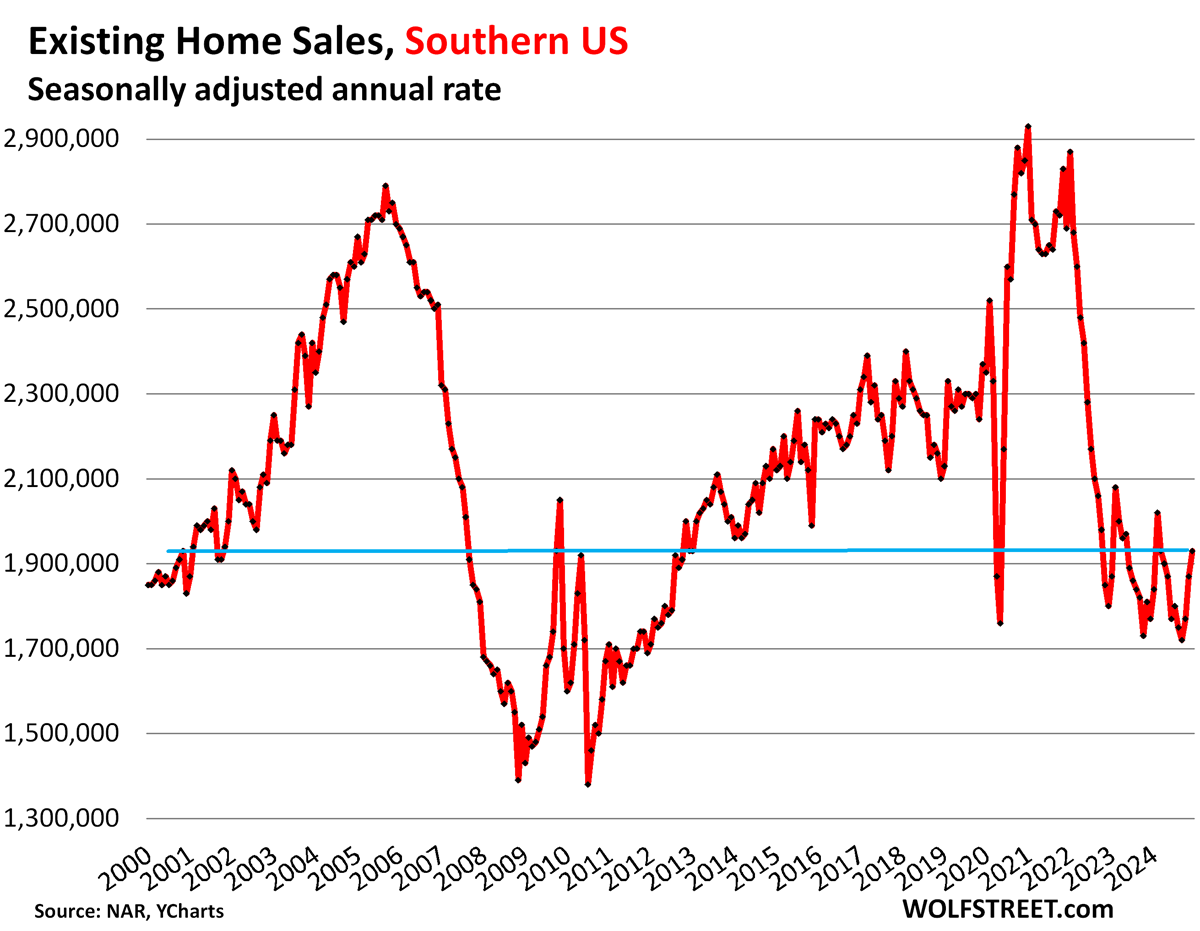

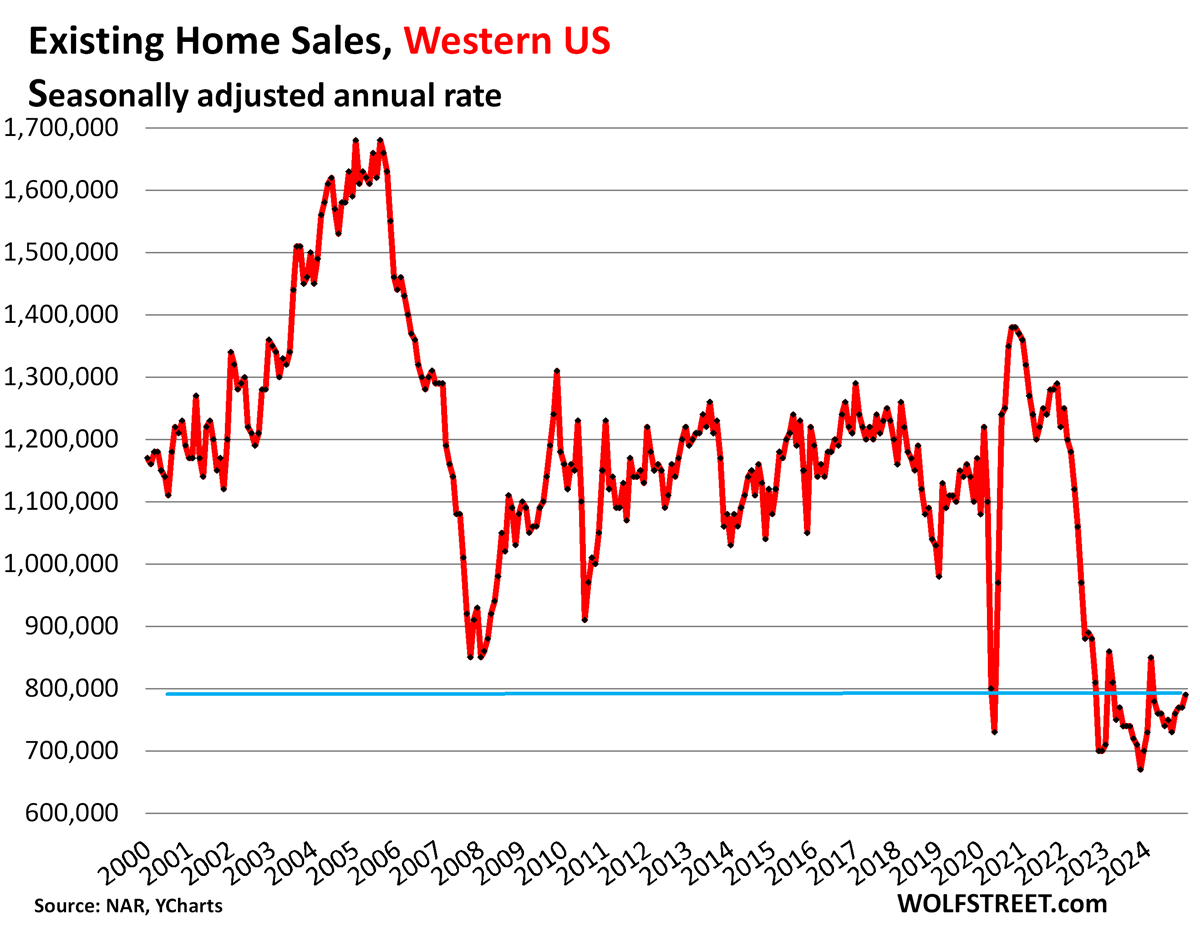

Demand destruction by region.

The charts below show the seasonally adjusted annual rate of sales, released by the NAR today, in the four Census Regions of the US. A map of the four regions is in the comments below the article.

Northeastern US: The seasonally adjusted annual rate of sales rose to 530,000 homes:

Midwestern US: The seasonally adjusted annual rate of sales dipped to 990,000 homes.

Southern US: The seasonally adjusted annual rate of sales rose to 1,930,000 homes.

Western US: The seasonally adjusted annual rate of sales rose 790,000:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As promised in the article, here is the map, showing the four regions of the US:

Against my recommendation, my mom bought a condo 3 years ago instead of renting an apartment. Seems like the condo association raises HOA fees the max amount legally possible every year. If Zillow has readily available data on HOA increases that could be really interesting. It seems like a large variable in condo prices and resale value- a beautiful condo at market price will have less demand when you can rent a similar apartment for 50% more than the HOA fee alone. If this keeps up I could see condo prices plummeting over the long run compared to similar homes or rental prices

Oops, you’d think I could figure out how to reply to the base article instead of the wrong vomment by now. Apologies. And thanks as always Wolf for the excellent analyses

Exactly what happened to my mothers condo when we went to sell it in 2011. The fees were so high relative to other associations that it lopped a good 20% off the value. We took a bath unloading it.

Here in CA it is getting harder and more expensive to find anyone to do decent work on apartments and condos. Most CC&Rs require anyone doing any work is licensed bonded and insured and that makes it even more expensive. I got a mailer from a realtor selling a couple condos near my cabin in Olympic Valley (near Lake Tahoe). The tiny 758sf condo had a MONTHLY HOA of $1,595 and the bigger 1,777sf condo had a MONTHLY HOA of $2,899. With the CA wildfires HOA insurance costs are going to increase even more.

i don’t know where your mom was, but if insurance is an issue, like in california and florida, it can be even worse.

Well, I think that acceptance is not a substitute for truth.

Which is the basis for the micro-economic formulation for the market’s machinations.

THIS SAYS IT ALL –

“ 2024 was the worst year since 1995 for sales because prices are too high after the 50% spike in 2019-2022.”

Worst year in 30 years! That says one thing…THE BIG ONE is COMING!

How do you know that terrible sales year wasn’t the “big one”?

Oh, no, no…the BIG ONE isn’t the SIGN(S) of a disaster, the BIG ONE will be the MASSIVE COLLAPSE of the housing market. It will be felt around the world.

Think about it – the lowest level in 30 years!

It’s a massive headline in the WSJ. The national piggy bank/ATM machine is about to be blown to smithereens.

You had me until WSJ!

What they may be referring to is a recent article titled “Wall Street Thinks U.S. Homes Are Overpriced

Housing could be overvalued by anywhere from 10% to 35% based on how investors are acting”

I can’t read the whole thing because I refuse to subscribe, but my back of the napkin is about $200k – $300k in excess price in California drawing value trendlines when I can find pricing data going back to at least 2016 on Zillow – which is not always.

Since we had a huge spike 2019-2022 , then we have flat prices or slightly down from 2023-2029, to smooth out the 10 year . Why are flat prices a bad thing? People like stability.

flat prices are the best case scenario, in my opinion.

Indeed. A housing market with a prolonged sideways movement could be its own recession. It would essentially be the soft landing the fed has been looking for.

Because there are not enough buyers at these prices. Incomes have not gone up relative to housing prices. The only thing sustaining these prices is a decade of underbuilding from the Great Recession. When supply catches up (which will be a least a couple of years or longer depending how much economic damage is coming our way as lots and lots of people lose their jobs and a bunch more leave before they are escorted out) that will bring prices down just through competition.

Prices cannot remain flat when there are people who NEED to sell and appreciation has slowed to a crawl. Stalled appreciation pushes the investors out of the market, declining STR revenue pushes them further. So, there is no reason to buy a house unless you plan to live in it.

As if California doesn’t have enough problems, Trump’s lunacy complicated the supply of Federal funds to support the victims of this natural disaster.

All feds told to RTO this morning.

Wonder how many people are going to be forced to sell and move back to DC or wherever else their office is. In these cases it is a forced sale so we will see what the true market price is rather than the sellers listing and pulling the same house five times.

From the graphs every region shows the same pattern, interesting WR.

I will keep waiting…it’s still too high…patience is required!!

Agreed! How are prices still holding up so much? I know markets have fallen but the overall national trend is still up, which means that there are other markets out there that have gone up even more than those markets have fallen. That could be a good future post.

Actually, overall market trend is down, albeit little bit.

YoY may be up, but 6 mos average is down.

With very little sales volume, this does not make much impact.

Because stocks are still worth ~60T or ~200% of GDP. People have net worth. Even the great 1989 asset bubble of Japan, before the lost decade, they only reached a piddly 140%. Weak.

Japan has finally returned to the highs of 1989 ; that’s 35 yrs to get back to the highs of the Nikkei ( more like lost 3 1/2 decades ) !

While prices are clearly still far too high which is most of the problem, I can’t help but think there’s another contributor that people are underestimating. Perhaps the dollar is worth less than everyone thinks and it’s rearing it’s ugly head in RE, stocks, and meme investments moreso than groceries, goods and services, wage inflation, etc. Will home prices correct down, or will everything else correct up? Maybe something in the middle.

It’s been a refrain in the comments section for years that the housing market takes years to correct. Looking at the median price chart, one could make the argument that it corrected in just six months, between June 2022 and January 2023.

Since January 2023, we have seen a higher seasonal low in January 2024 and we will see another higher seasonal low in January 2025 (unless the bottom drops out within the next month).

Based on seasonal lows, the trend in prices is up and we may look back on January 2023 as the low price point for this cycle.

This is the national median price that throws all markets into one bucket and takes the median out of it.

But market by market, there have have been some big price declines while prices still rise in other markets. I linked this in the article, of the biggest cities, these are the double-digit decliners in terms of single-family house prices. Condo prices look worse.

https://wolfstreet.com/2025/01/19/the-big-cities-with-the-biggest-price-declines-of-single-family-houses-or-condos-from-their-peaks-from-9-to-21/

Prices are back where they’d first been in October 2020.

Prices are back where they’d first been in October 2020.

Prices are now back to where they had first been in mid-2018.

Agreed. Unfortunately, I’m in the Seattle area where the price chart looks similar to the national chart.

If I were in the areas you point out above, I would feel good about waiting to see how things unfold.

In terms of single-family, the index is back where it had been in February 2022, down 5% from the May 2022 peak, but rising recently. And not a huge improvement, for sure.

But condos down 10% from peak, and back to November 2017.

How about Honolulu, by chance? Single family and condos if you have it. Thanks in advance!

There is an overall chart for Honolulu’s urban area here, houses and condos combined, as part of my series on the 33 big metros:

https://wolfstreet.com/2025/01/12/the-most-splendid-housing-bubbles-in-america-dec-2024-in-21-of-the-33-metros-prices-have-now-dropped-below-2022-peaks/

I’m waiting for prices to return to 2009 when they started the money-printing bullshit. I rent in Oakland, patiently waiting for the time to buy. I won’t buy in Oakland. The place is a shit hole.

I feel ya bro! I been waiting for prices to go down to where they were when we went off the gold standard. One day we’ll get there!

Don’t hold your breath.

That is what is referred to as a gamble. Patiently wait for what exactly ?

A decline in the asking price of homes ?

Likely to happen, eventually. Without inflation.

Washington D.C. has hit rock bottom, and can only go up. The new administration wants to clean this place up. Get rid of the Graffite, the homeless problem, and infrastructure issues. This is a good time to buy in DC. , even though most Republicans will chose to live in Northern Virginia. The critical infrastructure is all there and intact. We just need some better management of the city. The mayor wants to work with the new administration.

Good luck with that.

Swamp Creature,

Need another Marion Barry to swoop in and set it right!

Glen

I was here when Marion Barry was Mayor. The city was run much better than it is now. He had the respect of the residents of the city.

Nope. DC is toast. Federal workers are going to be cut. Do not buy a home in the metro DC area. There may be other cities that will also suffer from less federal workers, but I do not know which markets those are.

I thought the new admin was going to ax all federal workers, that wouldn’t be great for prop values in DC….

This may seem obvious or obtuse to some, but I believe that the RE market is less a reflection of what people are willing to “buy” and more a reflection of what people are able to borrow. I see three possibilities: (1) we have a pretty weak RE market for years until wage inflation puts homes within the normal percentages of affordability for their respective local market, (2) lending goes brr due to interest rates dropping & deregulation, and/or (3) recession and some people cannot service their mortgages with some price collapses in some but not all markets.

Current CAPE levels have me still thinking (3), but Keynes said something about solvency and rationality once. We may not have seen the peak of this cycle.

I would say option 1. It’s too pricey to build so they’re building smaller and cheaper or not at all. Materials are up, labor supply is down due to aging out, dumming out, and soon to be kicked out, and the thing about natural disasters is they both destroy supply and stimulate demand.

To me, this is a supply side problem with few solutions, and in a down market, it’s driving by death, divorce, and debt, and the last one doesn’t count that much. That, and we don’t seem to relocate that much anymore.

Hi Wolf, you wrote “year-over-year gains in 2004”. Did you mean “year-over-year gains in 2024”?

I think so too. Later in the piece, one other small typo: “plunged to wherever” should be “plunge to wherever.”

Love the substantive analysis here, though, great stuff!

Yes, thanks.

This is the title of an article on CNBC yesterday…

“Only 28% of Americans who planned to buy a home in 2024 actually did-young buyers feel ‘trapped between a rock and a hard place’“

not surprised they feel trapped. everyone is telling them that they should buy something and get some stability for their families, but poor government policy has made it so that the market is completely out of whack. they’re justified in being angry.

Worse, they’re only being told half the truth. They’re told that buying a home is the only way to build wealth – which is just not true. A dedicated saver invested in low cost index funds can have a comfortable sum to retire on. The true cost of owning a house includes all the maintenance, the interest on the loan, and property taxes.

I ran the numbers for the kids last year. A $400k house with 20% down and a 30 year loan will ultimately cost a million dollars when you factor in maintenance costs.

You can also take your 20% and invest it, adding regularly over 30 years and at 6% return you end up with…a million dollars.

To be fair you haven’t calculated the cost of renting for 30 years in your latter calculation. Not that I’m pushing real estate at current prices.

Bought UWS, in the 80s, Condo, primary residence, in December.

6.23% mortgage on half of it.

Miami metro according to Redfin Data 14 Months of supply vs all Redfin Metro 5 Months, Price still too high, IDK how long could be

Purchasing a house in current market conditions holds a substantial risk. Difficult to believe that residential RE will continue to maintain current price levels in the long run.

Each time I look at it, the conclusion is the same. Prices are not good. They are only slightly less bad. Better have your scuba gear at the ready if you pay even close to today’s list prices. You may easily wind up underwater.

Probably the most factual article I’ve seen regarding this ridiculous housing market. I’ve been looking for 3-1/2 years now and do not see the value of buying considering all the risk you take on.

Where I am looking they are selling 30 year old houses for $300 a sq.ft. which is ludacris considering everything in that house is original! How much more life do you think that roof/those windows/hvac/etc have left?

Also don’t forget when you want to sell said house your closing costs on a $500000 home could be as high as $48000 which basically comes out of your bottom line.

Do your math before buying at these inflated prices.

@ Wolf

“Sales of existing single-family houses, townhouses, condos, and co-ops that closed in December rose to 329,000 homes, not seasonally adjusted,”

——————————

I remain confused by seasonal adjustment. How do seasonally adjust an absolute number? The number sold in December was 329,000 ….. no?

I said that 329,000 in December is “not seasonally adjusted.” It’s a raw figure of actual sales. What’s your problem?

The next paragraph discusses the “seasonally adjusted annual rate” in December (4.25 million) which is the figure that you see in the press most often. It’s a rate, representing how many sales there would be in an entire 12-month period at the seasonally-adjusted December pace of sales.

I did this to give you both figures, the raw actual sales in December that you don’t see anywhere in the media, and the SAAR of those raw actual sales in December that you see everywhere.

Thanks. Good job.

Here comes trump to the “rescue”? I knew he was going to go after interest rates. Will the Fed successfully resist? I hope so, but the exchange rate movements today suggest the market thinks he wields enough power to potentially make it happen.

Let’s keep in mind that the last time the Fed cut, long-term rates (and mortgage rates) rose.

Haha exactly. Lets let them go ahead and do more cuts. Burst this bubble even faster.

As I understand it (perhaps poorly), mortgage rates are set largely by expectations on the interest rate trajectory for the next 10 years or so, given the average mortgage lifetime is about 8 years.

Mortgage rates rose because the cuts happened more slowly than expected, and inflation is proving tougher than expected, which means higher rates in the longer term as well *if* the Fed continues acting in line with current wisdom.

If the Fed can be coerced into modifying their behaviour to setting rates lower than they think is sensible, would you not expect the market to react by lowering long term rates? Presumably the absolute mess it would create means they’ll eventually return to a sane path, but you’ll have 4-5 years of heavily suppressed rates first.

I’m cautious betting against Trump, however ridiculous the suggestion. Particularly this time around given it’s his last shot. (Although I’m sure he’ll try his best to prevent that, too! I’m *just about* willing to bet against success there)

“..setting rates lower than they think is sensible, would you not expect the market to react by lowering long term rates?”

If the bond market sees these lower rates by the Fed as the Fed’s willingness to tolerate higher inflation, or eagerness to create higher inflation, long-term rates will react to inflation expectations. No one wants to buy 10-year Treasuries at 3.5% yield when they expect inflation to be 4% or 5% over the next 10 years. So if expectations rise that inflation will be higher due to the Fed’s stance, then long-term rates will be higher as well, and you end up with a steeper yield curve. This happened before.

it’s not so much that mortgage rates are based on the interest rate trajectory for the next 10 years, but the inflation trajectory of the next 10 years.

the fed cannot control long term rates without printing money.

He wants lower interest rates in order to explode the debt to cover tax cuts for his buds and family. Housing and affordability for citizens is not even a thought for those people.

If this could be successfully done, every leader in the world would keep rates low for happy subjects. Even Putin can’t do it. The Fed is independent.

“He wants lower interest rates in order to explode the debt to cover tax cuts for his buds and family. Housing and affordability for citizens is not even a thought for those people. ”

thecon dot tv

Free education can be beneficial sometimes. Pretty much defines who “those people” are.

Aw shucks! Here I thought he was going to make my grocery bill go down. Are you going to tell me the Easter Bunny doesn’t exist? What about the Tooth Fairy?

If the fed gives in and cut rates more aggressively then I see mortgage rates shooting up

It would be like shooting yourself

The thing is .. they fed doesn’t control long rates without risking inflation

The FED’s interest rate suppression, QEs, consisted of long-term securities not T-Bills. This lowered mortgage rates and changed the elasticity of demand.

https://www.stlouisfed.org/publications/regional-economist/third-quarter-2017/quantitative-easing-how-well-does-this-tool-work

C-19’s SOMA current portfolio consists of a larger volume of short-term securities thus holding mortgage interest rates higher.

https://www.newyorkfed.org/markets/soma-holdings

Typo?

“consists of a larger volume of short-term securities” should be “small volume”?

There have only been $195 billion in T-bills on the balance sheet, unchanged since about May. The rest of the $6.4 trillion SOMO portfolio are longer-term and long-term notes, bonds, MBS, TIPS, agency securities, CMBS, etc.

Interesting to watch how the tax situation worsens in California over time. Lots of factors seem to be coming together to turn an already high tax state and go up from there. This will just add to costs and while home owners / flood and property taxes don’t hurt too bad in my area (9K combined or so), they will only increase especially as the state turns to bonds to fund the deficit versus the real purpose of bonds(infrastructure and so on).

California obviously not only state with this challenge but where I live so all I know. Don’t think any type of death spiral is in the making but clearly nothing to be optimistic about.

State taxes burden – California is towards the middle.

But its income tax really sucks for the highest income brackets.

“State taxes burden – California is towards the middle.”

Correct.

9k annual prop taxes for what kind of house I pay nearly 7k for a 960sqft ranch on a fifth of an acre in NH. My monthly prop tax is coming close to exceeding my monthly mortgage payment.

Probably the only “deal” that CA residents get but I digress…

“As of now, bills have been introduced in several states to block corporate ownership of single-family homes.”

The article you linked is nonsense, and it says so near the top:

“These are generally just filed bills. There is a long way between where these are now and being signed into law. But, here they are…”

These kinds of bills have been “filed” in state legislatures for eons. They never go anywhere. They’re complete clickbait BS with which some individual legislators are trying to get some publicity in the social media and blogosphere. And it usually works.

i can’t see the article for some reason, but they never go anywhere because they’re completely unworkable. besides the potential constitutional challenge4s that would hold these laws up in court for years, what constitutes “corporate owned?”

most landlords buy properties in limited liability companies to protect their personal assets. are they corporate? does it have to be a public company? any company with a certain dollar amount of assets under management?

if these places passed such a law, investors would find ways around it.

“i can’t see the article for some reason,”

I deleted the link as I delete most links because I don’t want to promote these articles on my website.

What will happen when the likes of Blackrock and Larry Fink start moving into the fire ravaged areas on LA and starts buying up lots from distressed former homeowners who have left? I would bet that legislation will be introduced to prevent corporate ownership of lots of which were formerly occupied by single family homes.

Not to worry

“About 1,600 policies in Pacific Palisades were dropped by State Farm in July, California Department of Insurance spokesman Michael Soller said in an Thursday email to CBS MoneyWatch. An analysis of insurance data by CBS News San Francisco last year found that State Farm also dropped more than 2,000 policies in two other Los Angeles ZIP codes, which include the Brentwood, Calabasas, Hidden Hills and Monte Nido neighborhoods.”

I think the payout per home is like $3m tops so I suspect a lot PP homeowners are in for a shock.

“The report indicated that the median home inside the Palisades Fire zone had a value of $3 million.” So half the homes are over the cap.

The current administration and Congress? Legislation to benefit individuals and families over corporations? You’ve lost your mind.

With GOP control of congress, I fully expect bills to facilitate and promote corporate ownership of SFH’s, and limit rent control and liability on same.

And it will be sold to the peasants as being beneficial for families, somehow.

@Cold in the Midwest “if you pay even close to today’s list prices for 99% of the things for sale today, like cars, trucks, TVs, appliances or furniture you WILL wind up underwater in a year”.

I’ve been investing in real estate for the past 40 years and I’m not “investing” now (since I think cash in a money market will outperform every real estate “investment” I have seen in the past few years).

My advice to people looking to purchase a “house” (they want to live in) is if you can afford a home with a 30 year fixed rate loan and have a stable source of income go ahead and buy one.

I like to own homes and cars since I keep them for a long time and like to work on them changing things so they work better for me, but I have many friends that lease homes and cars and never need to deal with any of the problems of home and car ownership that I do.

When I finally put roots down in Hawaii(after renting on two other islands) it was 1983 and jobs were almost non-existent. There was a USDA farmers home loan program that would cover 100% up to 65k for a new build house lot package. The problem was scraping together the closing costs(about $1,200) and having regular qualifying income. Interest rates were 10.5 so the payment was $650 but if you couldn’t afford the full payment then USDA picked up the shortfall and the difference was added onto the balance. I thought to myself, ‘everywhere I’ve lived that was nice I have seen prices go up as it becomes “discovered’ so I’d better get a steady job and buy one of these’. I did but during the 3 years from making the decision to when I actually closed on the lot, every person I told about my plan said “It’s cheaper to rent! You’re nuts!”

Today, I am financially set despite making a ton of mistakes along the way. I still see those that scoffed at me and that are still here and many never bought and the rent has gone for $200-$500 to $4,000 to $6,000. Many retired at 62 only to return to work at HD, Lowe’s etc.

The Fed and it’s medieval inflationary policies is bearing rotten fruit for many workers. Many locals have moved 1.5 hours out of town, commute to work every day($4 for regular) and pay rent in the boonies at $2,500/mo. Imagine that lifestyle in your 70’s.

Those that still live in town to avoid the commute live apt style in SFR and pay $1,500-$2,000 for a bedroom(+ utilities).

Bottom line? If the location is nice, there seems to be an less line of folks just waiting to move there. I see Californians not even blink an eye to pay 1.1 mil for a home I sold 35 years ago for 99k. One just closed with an $8,000 payment. Then they complain when the local appliance repair dude wants $70 an hour to fix their fridge on a moments notice. Crazy world.

At Kukio, 2,000′ PUD’s that were $2m are now $10M and one new owner just gutted his and is spending $8m on new interior. Most sales in Kukio and Hualalai are “sold before print” as the demand by the billionaires is endless.

To quote Wolf:

“But market by market, there have have been some big price declines while prices still rise in other markets.”

i tell people the same. only buy a house today if you are very confident you will be in it for the long run, and you are okay, mentally, with the idea that you’re likely overpaying. in other words, don’t buy a house today for 500,000 dollars if you’ll wake up upset every morning in a year or two if the house is only worth 350,000.

I’m not sure what “long term” means for younger folks these days.

I think it is hard for them to say, even. Gone are the days of putting down roots because you work for a company that will give you a job you can work for 10, 15, 20 years. If your employment is in flux, where you don’t know if you will be working for the same company or even in the same field 10, 5, or even 2 years from now, it’s hard to focus on the long run.

With all the natural disasters occurring one after another, and all the insurance shortcomings coming to life, Real estate prices will be affected dramatically by the climate and weather considerations going forward. For example, people are not going to pay top dollar in hurricane prone areas. Hurricanes are affected by the warm gulf water temperatures which take a decade to change. Insurance companies hire climatologists to assess risk in underwriting policies in these areas. Same with flood zones. All you have to do is look at the recent insurance premiums in Florida and Louisiana to get the picture of what the cost of home ownership will be in these areas. Of course don’t look for Realtors, house flippers, or builders to tell you any of this.

Perhaps the new admistration will clean up the RE mess by limiting commissions and holding them to truth in advertising.

That is a huge part of the problem.

Hilarious. They will do exactly the opposite.

The main business of most advertising is to sell product. Truth has very little to do with it.

Surprised to see banks and mortgage companies have not rolled out and extensive financing options such as 40 or 50 year mortgages with 4% interest rates. It would be a hot commodity right now among the younger generations. Agree the West Coast wildfires and the Gulf of New Mexico hurricanes has reconfigured normal insurance rates. After going through several hurricanes in Louisiana, including Katrina. The last 10 years of living in Colorado have been pretty sweet, no insurance claims filed, no mental anguish.

“… such as 40 or 50 year mortgages with 4% interest rates”

Why would banks want to lose lots of money on these mortgages? Just to make young home buyers happy?? 🤣

Where in CO? Lots of people in my zip code are getting dropped by insurance or have had their rates more than double in the last few years. This years Hogback fire was very close to residential properties and could have been a disaster. The Marshall fires were over $2B in damage. We had a wildfire, up on North Table in Golden last year really close to a lot of residential properties had the wind conditions been right there wouldn’t have been enough time to warn a lot of people to evacuate. It never made the news because the fire dept is so close by it was brought under control quickly, but it was big I could see the side of the mountain huge and glowing as I drove home and quickly packed what I could in case the wind direction changed. The Goltra fire in clear creek/golden also could easily have spread and taken out a lot a of new $1M homes is Golden and West Arvada. There was also a fire somewhere near Green Mountain across 470 that could have been pretty destructive 2 years ago. There was one up by Lyons and Fort Collins this summer that luckily didn’t get too close to housing. They don’t even make the news anymore unless there’s a lot of devastation….

Summer is now just fire season and I hardly notice anymore except that air quality is terrible. For CO it’s only a matter or time before we have another Marshall fire. I wouldn’t say it’s a safe from spiking insurance or natural disasters.

Southeast Aurora Blackstone Golf Community. Gods country without the forest, some call this the beginning of the Eastern plains. Easy access to airport E470 shopping, tech center, Castle Rock and I-25. Mountain dwellers may continue to pay the price as it was proven a few years ago it only take 2 rednecks from Alabama starting a campfire 🔥 to ignite to biggest fire Colorado ever seen and just walk away. The are more idiots that have moved to this than ever before, just as the Marshall fire begin that religious cult was burning garbage with 100 mph winds. No one ever talks about that anymore. Just like the migrant gangs from Venezuela 🇻🇪.

Burning garbage? Don’t get me started!

I’m in Tucson, Arizona, we’ve had a dry winter, and what should my idiot neighbor decide to do on Saturday afternoon? Burn garbage in the backyard of the rental property that he and his family have been turning to (shhhhh!) since 2020, that’s what!

Well, I tried, believe me, I really tried, to report this to the city. I called 311 to ask if backyard burning is illegal.

Yes it is.

But, unless I can see WHAT they’re burning, (smelled like garbage from here), the 311 guy wouldn’t roll the fire trucks.

Mind you, during the afternoon of Saturday, January 25, the National Weather Service had issued a Red Flag Warning for southern Arizona.

Oh, I did report these neighbors to the city’s code enforcement office. Suffice it to say that a decent inspector could find all sorts of violations over there. That is, in addition to the backyard garbage burning. I took a picture of that — and I added it to my report.

And, lo and behold, in this mornings email comes good tidings from code enforcement. They’ve accepted my report and will investigate it.

Ummm March 24, 2024 there was a wild fire near Aurora, small 127 acres. But it’s as dry in Aurora as the rest of Colorado.

Favorable wind conditions and quick action seem to be the what determines whether they’re controlled or not.

Lots of comments about pricing and where we all think prices are headed. I would love to see a range of where we think prices should be as I try and sell my MIL home in Edmond Ok this spring. Built in 1968 3000 sq ft new hvacs 1 acre not updated 3 br 2.5 bath well water in town . 1 acre lot subdivision. No HOA

My guess is 350000 ? New homes nearby sell for 200 a sq ft