Austin, Oakland, New Orleans, San Francisco, Washington D.C., New York City, Detroit, Seattle, Portland, Tampa.

By Wolf Richter for WOLF STREET.

We talk a lot about “home prices in the US” – rising or falling or whatever, as if the US were one monolithic market. But the US spans a vast number of housing markets that all dance to their own drummer, though they all share some underlying themes. The long-running Wolf Street series, The Most Splendid Housing Bubbles of America, currently charts 33 of the largest metropolitan areas with the highest home prices. Those metros are huge and diverse. Some cover parts of several states and comprise multiple counties.

So here are the largest cities – not metros – with the biggest price declines from their respective peaks in 2021, 2022, or 2023, for single-family houses and separately for condos and co-ops.

The double-digit decliners: For single-family houses, 4 of those cities have price declines between 15% and 19% from their respective peaks in mid-2022. For condos and co-ops, 6 of these cities have price declines between 12% and 21%.

These prices here are seasonally adjusted and a three-month moving average to iron out the month-to-month squiggles. They’re part of the Zillow Home Value Index (ZHVI) data, based on the Zillow Database of All Homes. These are not median prices.

The biggest cities with the biggest price declines of single-family houses.

The metrics include: price decline from their peak, change from prior month (MoM), change year-over-year (YoY), and increase since January 2000.

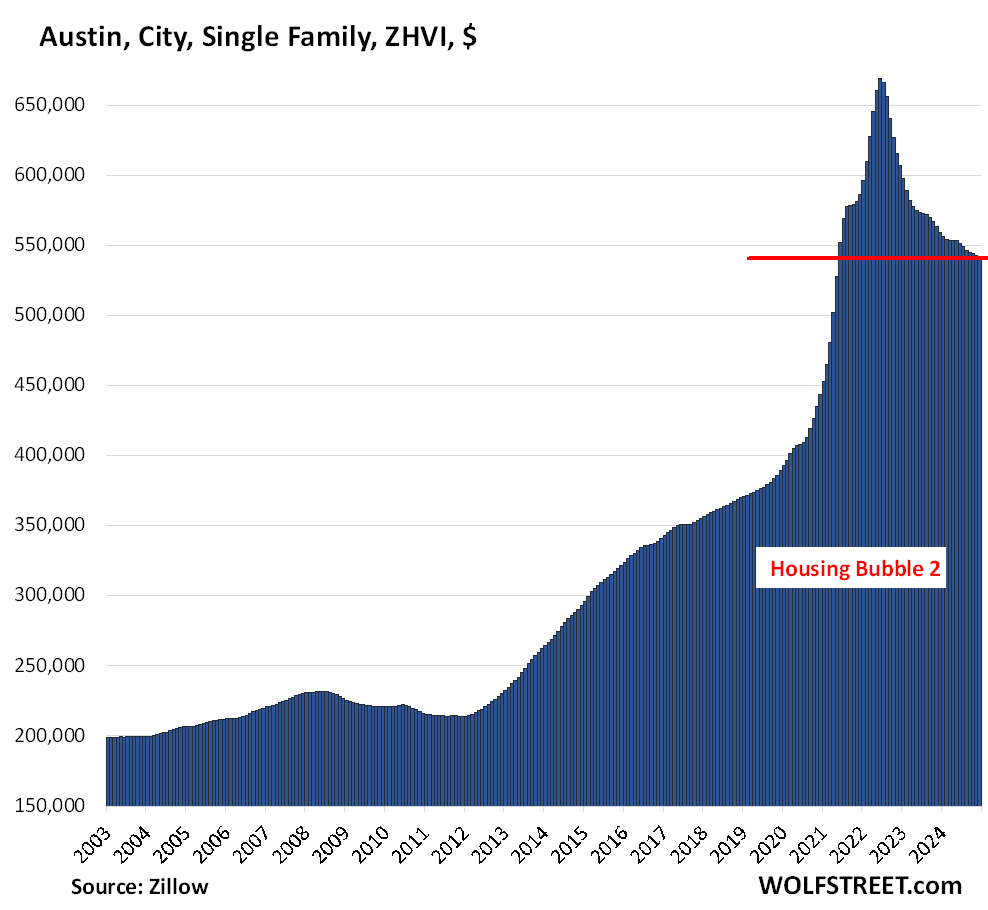

| Austin, City, Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -19.2% | -0.5% | -3.4% | 182.6% |

Despite this big fast drop, prices are only back where they’d first been during the price explosion in June 2021. Easy come, easy go here, but prices are downward sticky. They exploded by 38% in two years. And then, in two-and-a-half years, prices gave up only about half of that:

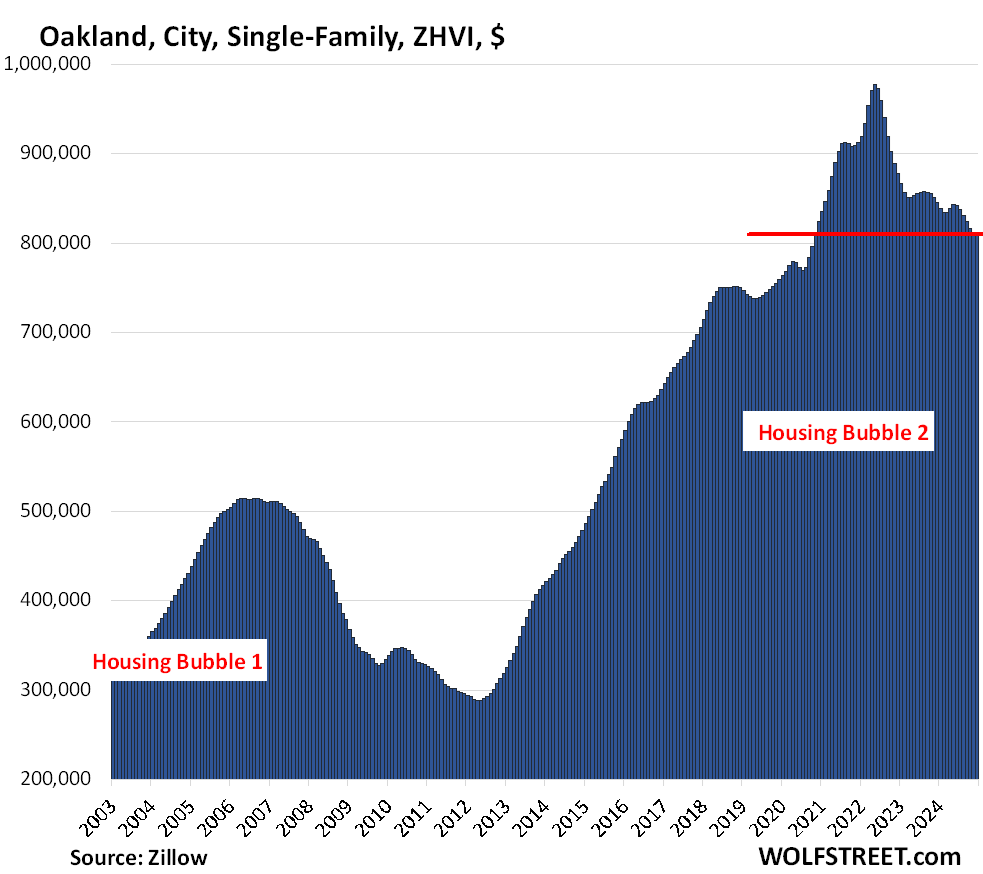

| Oakland, City, Single-Family Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -17.2% | -0.3% | -4.3% | 312.7% |

Prices are back where they’d first been in October 2020. Between June 2012 and the peak in May 2022, prices had tripled, which is nuts.

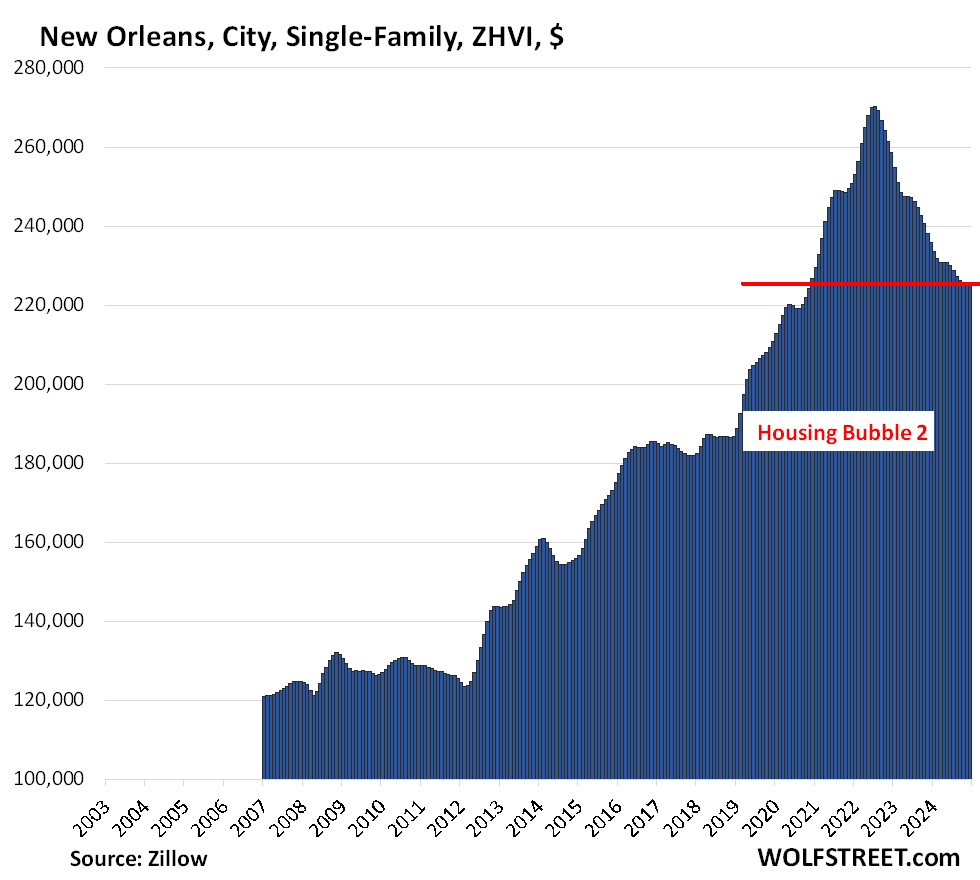

| New Orleans, City, Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2007 |

| -16.7% | 0.2% | -4.5% | 86% |

Prices are back where they’d first been in October 2020. Hurricane Katrina, which wiped out a portion of the city in August 2005, coincided with the beginning of the housing bust, and so we left this area blank.

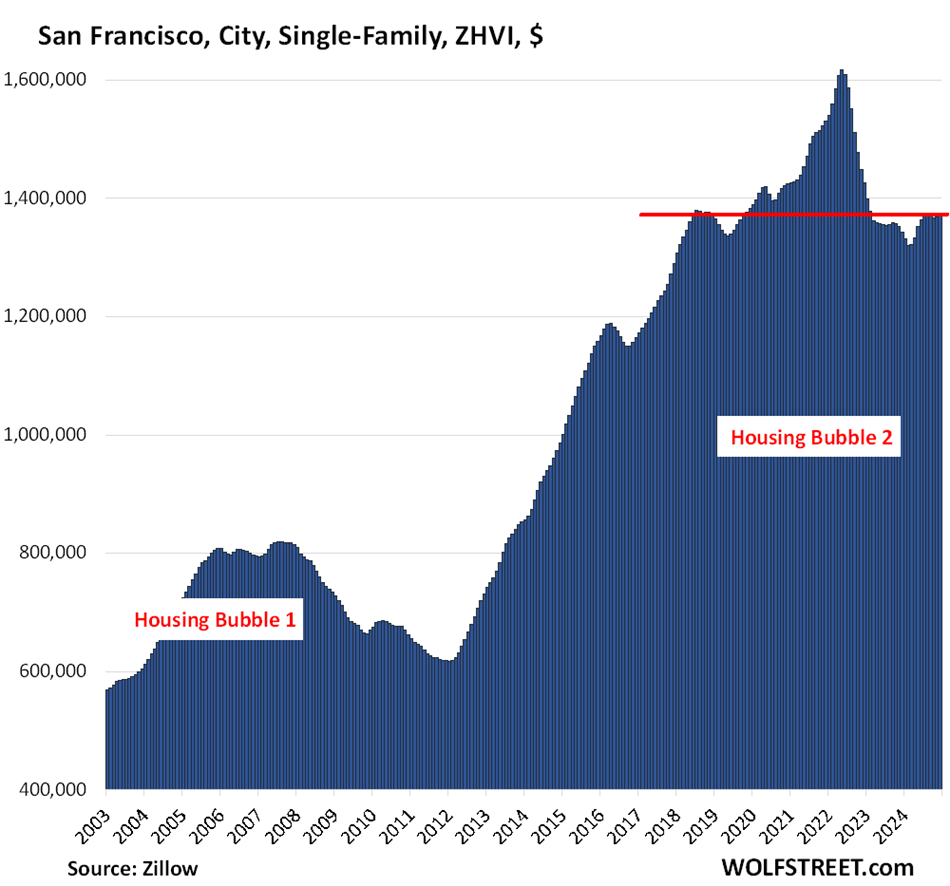

| San Francisco, City, Single-Family Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -15.2% | 0.3% | 2.1% | 237% |

Prices are now back to where they had first been in mid-2018. That was over six years ago:

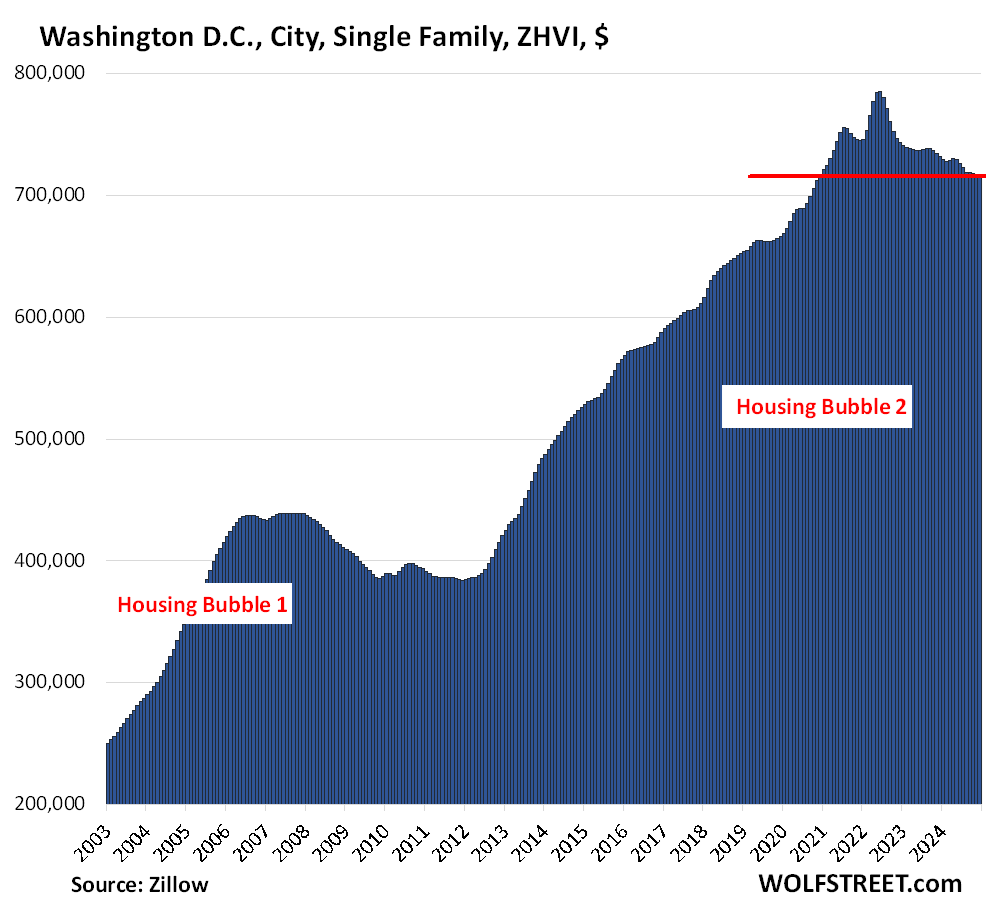

| Washington D.C., City, Single-Family Home Prices | |||

| From Jun 2022 | MoM | YoY | Since 2000 |

| -8.8% | -0.2% | -2.2% | 288% |

Back to December 2020.

The biggest cities with the biggest price declines of condos and co-ops.

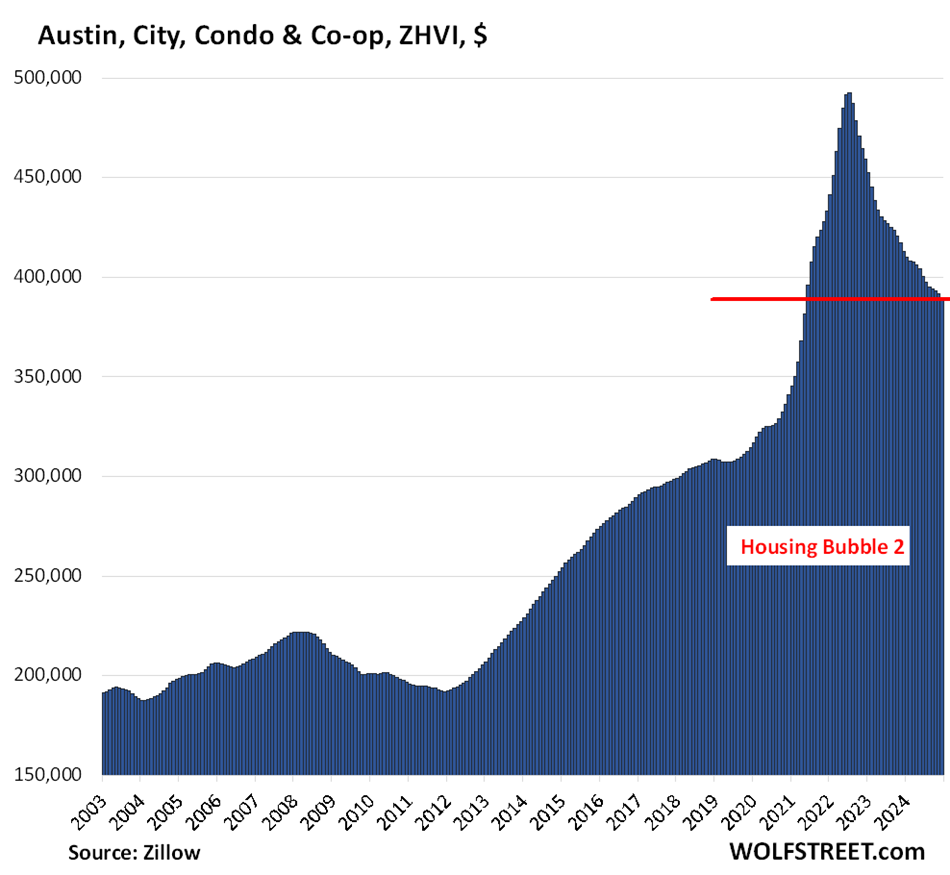

| Austin, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -21.0% | -0.6% | -6.1% | 124.8% |

OK, this is moving pretty fast, not very downward sticky.

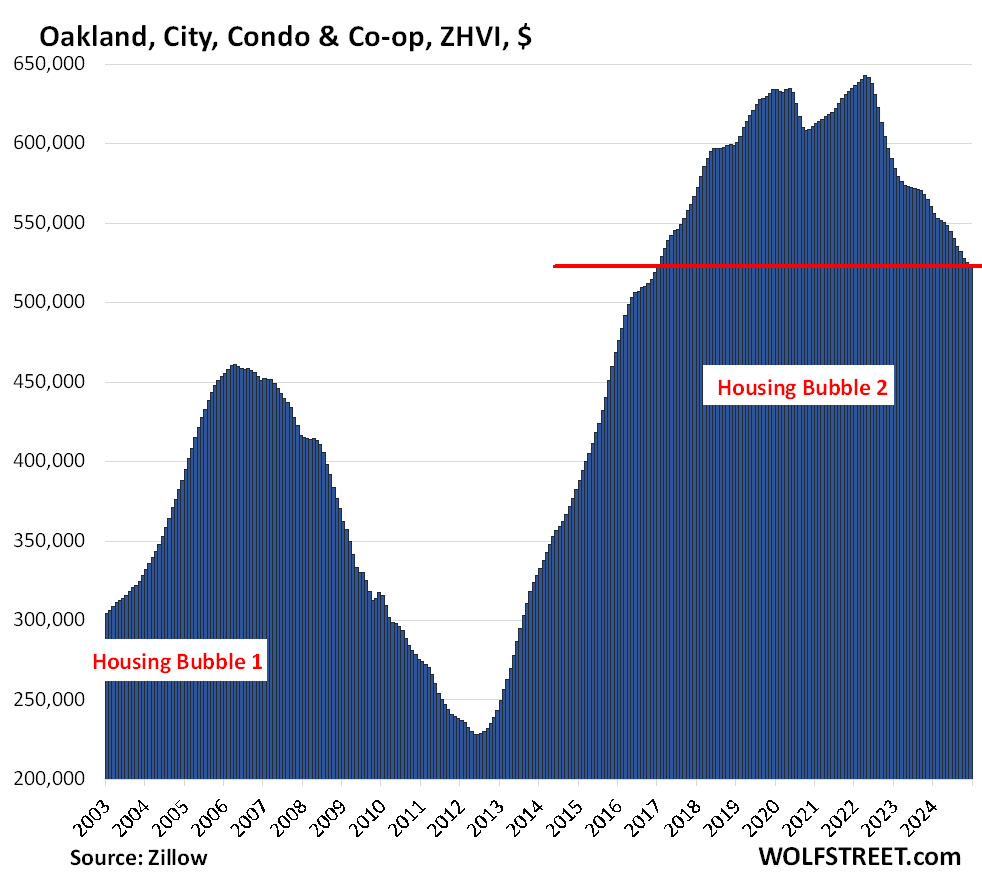

| Oakland, City, Condo Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -18.6% | -0.5% | -7.1% | 186.1% |

Back to 2016.

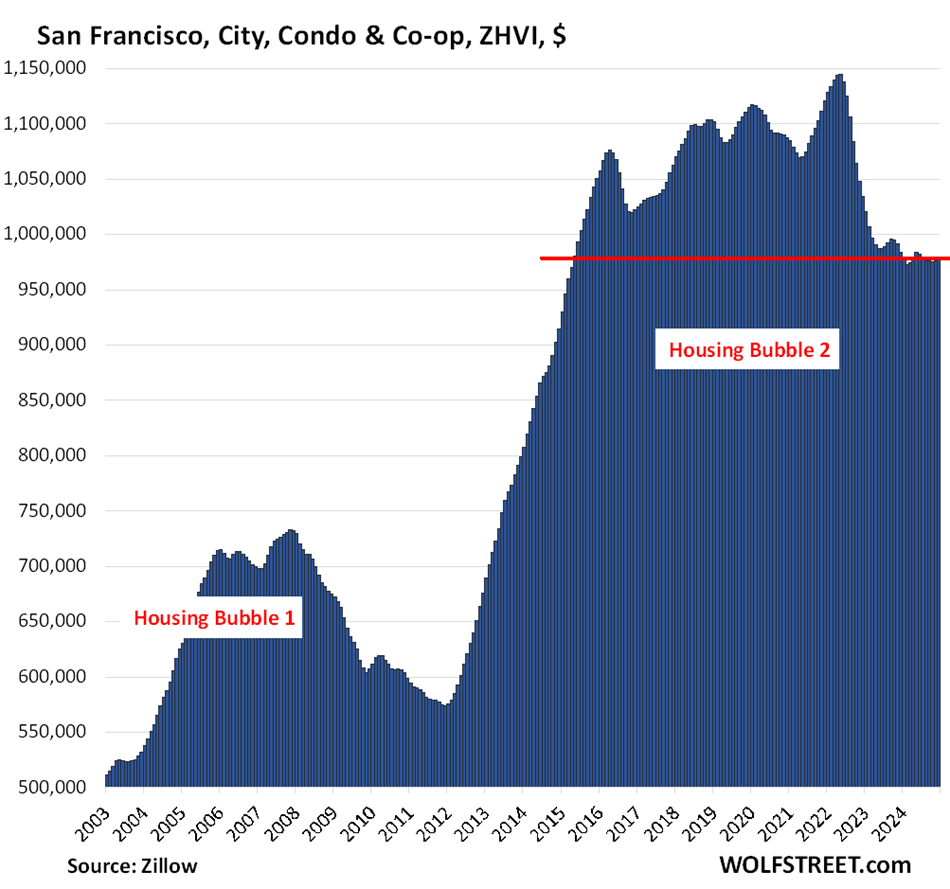

| San Francisco, City, Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -14.6% | 0.1% | -1.5% | 144% |

Back to April 2015. Condo prices had doubled in the four years between 2012 and 2016. But the sky is not the limit, not even in San Francisco. In the City of San Francisco, condo sales are the majority of the market.

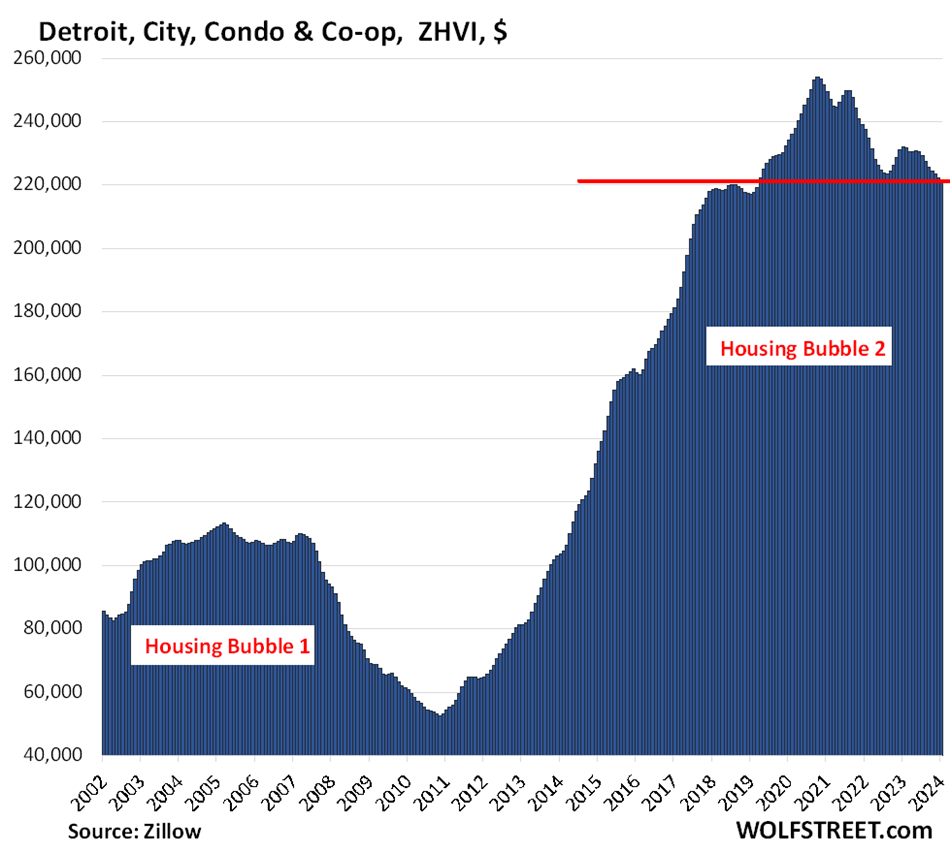

| Detroit, City, Condo Prices | |||

| From Sep 2021 peak | MoM | YoY | Since 2000 |

| -13.1% | -0.6% | -3.8% | 273.7% |

In the process of revisiting 2018.

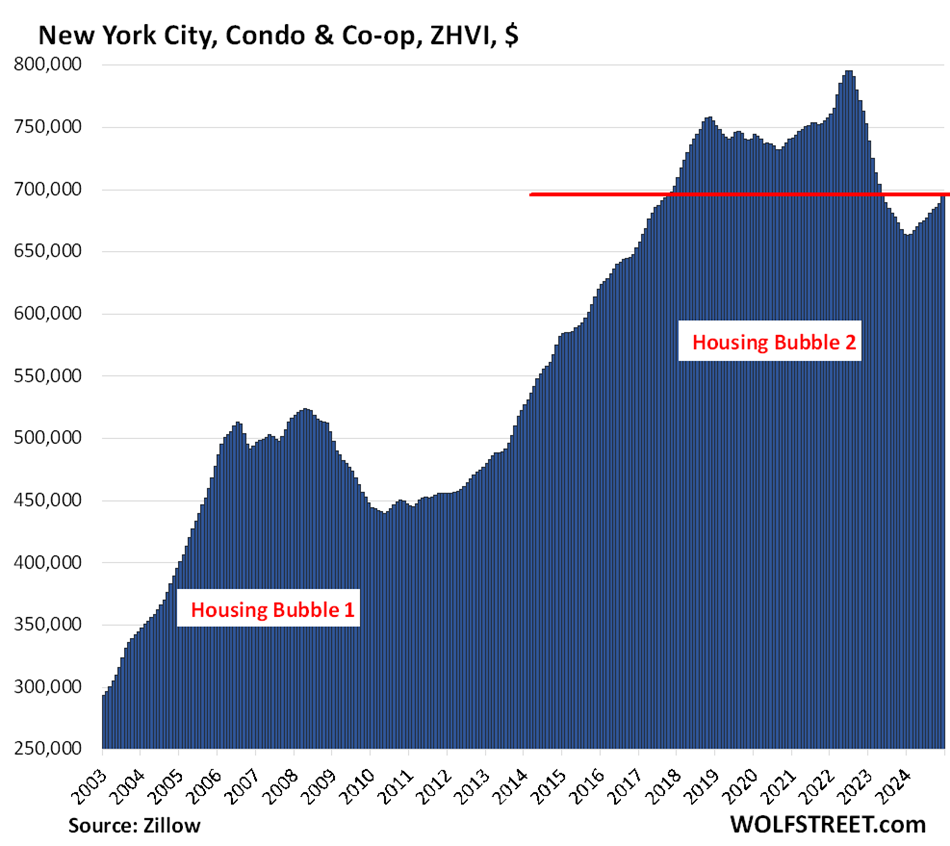

| New York City Condo Prices | |||

| From Jul 2022 | MoM | YoY | Since 2000 |

| -12.7% | 0.8% | 3.1% | 219% |

Got a little bit of excitement going on in here. Maybe the huge stock market rally, the surge in bond and leveraged loan deals, and all the other things that produce huge bonuses for Wall Street workers.

A price level first seen in 2017:

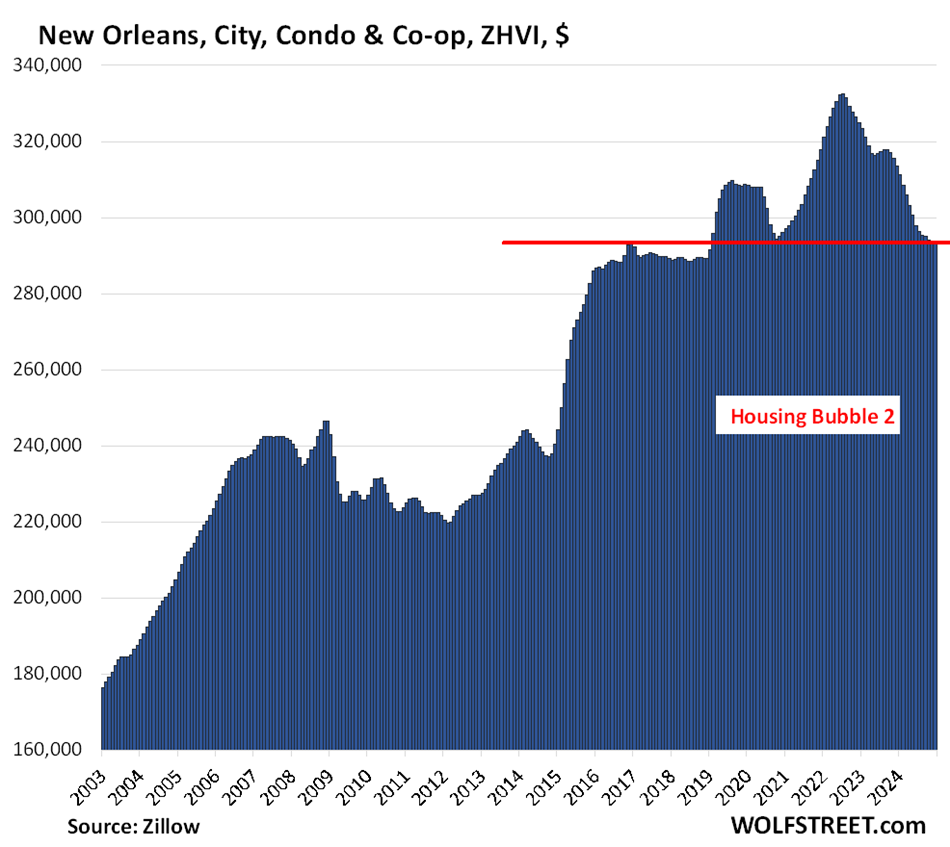

| New Orleans, City, Condo Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -11.7% | 0.1% | -7.0% | 101.6% |

A price level first seen in 2016:

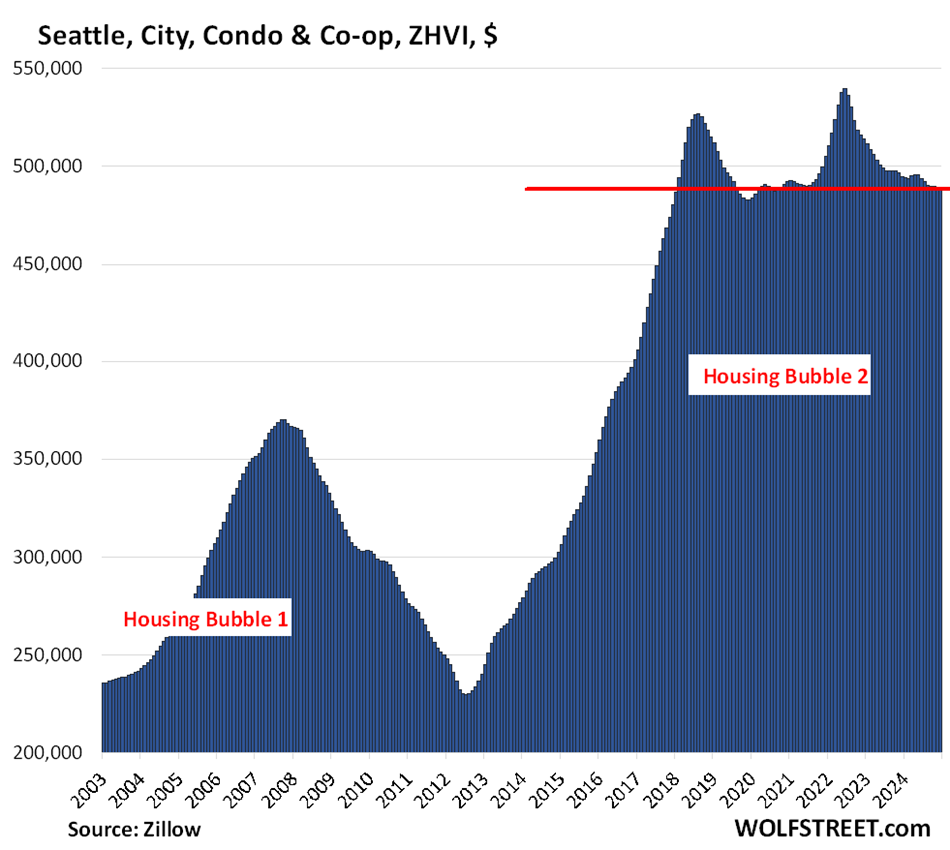

| Seattle, City Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -9.5% | -0.1% | -1.6% | 148.4% |

Back to November 2017.

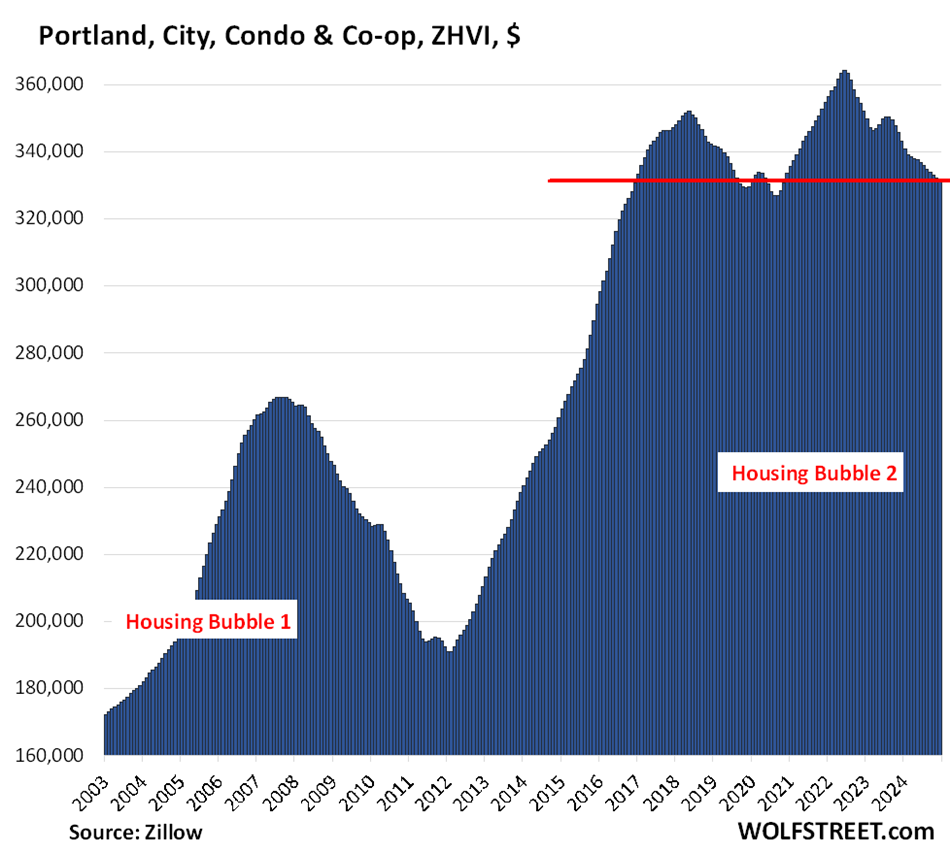

| Portland, City, Condo Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -9.0% | -0.2% | -4.0% | 119% |

Back to 2016.

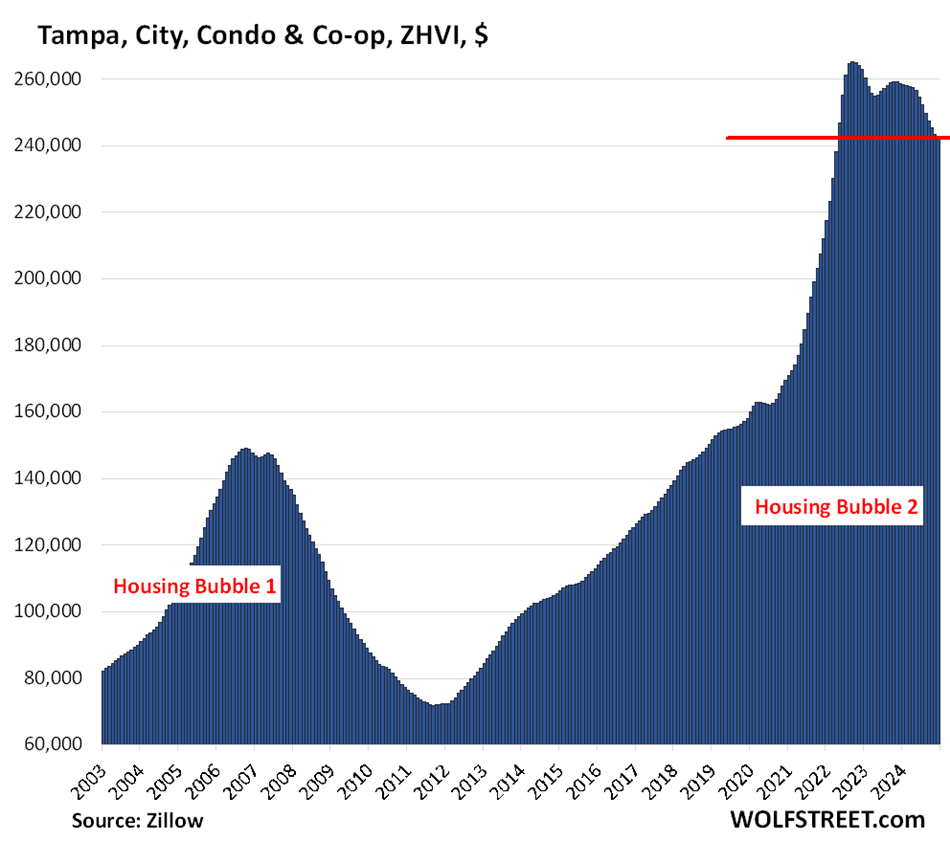

| Tampa, City, Condo Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -8.8% | -0.6% | -6.1% | 301.0% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Once the economy goes into a recession depression they’re going to come way a lot further down.

I told Wolf to buy $TRUMP coin yesterday and he would be up 200% today if he did. We are nowhere close to a recession buddy, keep dreaming.

I will buy crypto after hell freezes over.

Interestingly the crypto reserve the Trump bros want the US to create, is not about anything strategic from the US perspective, but rather to create a price floor for crypto. Of course many of them will be thrilled to have someone to take their bit coin off their hands too.

Well considering the activity currently in the mantle leading to a new mini ice age (polar vortex activity biggest sign) you may be buying crypto soon!

I hear you. NEVER invest in a ponzi scheme.

Thank you Wolf! Someone with some senses on crypto . A travesty that our leadership and government has been willing to regulate these products.

If, as I think, the crypto scene (or at least most of it) is Tulipmania 2.0, Trump has put himself at some serious political risk when the bubble finally bursts.

When people lose their money, they won’t say to themselves, “maybe I shouldn’t have put my life savings into Fartcoin chasing after my neighbor who made a 30x return in a month with that coin.” Rather, they’ll look for someone to blame. And they’ll start at the most visible proponent of crypto, at the top.

Of course, it could all be different this time. It might. Just maybe.

Another reason I love Wolf.

IDK Florida panhandle looking pretty frosty today ;-)

Wolf, please be so kind as to post the Portland Single Family Chart, I think I (only) see dead condos

“I will buy crypto after hell freezes over”

It did. And so is large parts of the US at the moment.

But I would not recommend to buy any fake coin as currently advertised and hold it except for Musical Chair purpose :

when you sell something and be paid in some fake coin, you immediately sell those or buy something with value and do not ‘HODL’ a.k.a. speculate .

I have been making fun of fake coins from the beginning but the fact they don’t have an intrinsic value might actually be a blessing especially to solve the trade imbalances.

Currently we buy something in e.g. China or Europe with USD and the receiver will keep those USD for a rainy day or turn them into treasuries. But they do not buy anything at this moment resulting in a trade inbalance.

Now say we pay them with utterly worthless $Trump coins. The seller may accept them but will be very motivated to get rid of those things as soon as possible. So will immediately buy something with value or a future value like a delivery of oil or gas or a 10 year subscription to netflix, whatever. So the worthless $Trump coins will bounce back and the receiver of those will exchange them immediately for something useful and not HODL them.

So the bottom line is that those fake coins may afterall have a use to facilitate group bartering between multiple parties.

We have all been blinded by the rediculous hodl and ponzi speculation of those things but as grease for trade it may have a future.

Your thoughts?

Yes, I like you, have imagined the possible outcomes like something with a needle that pricks the engorged asset bubbles.

The most common aspect of all these big city markets seems to be Blue…they all range from mild to extremely liberal political strongholds. The economic effects of politics on business policy, employment and income plays out in the housing market in real time, in that homes tripled in value over about a 10 to 12 year window, in a unsustainably optimistic economy. Based on a very similar scenario in the late 70’s to the early 80’s, I’d say all these places are going to see dramatically declining prices over the next few years. Where the US is right now reminds me of the oh crap scary feeling on a roller coaster, right when you crest the highest drop, and are just picking up speed going down, and the bottom is still down a lot further away!!! I hope I’m wrong, but it appears a lot of these folks will be economically devastated in the near future.

They probably all have a 3% mortgage. I’m sure they will be fine.

I wouldn’t count on that. Blue areas are now a refuge from the retrograde social agenda currently in play as of this morning. Housing may be cheaper elsewhere, but that cheap tends to come with all sorts of restrictions and outright hostility at the state level that half the country isn’t interested in living with. Large portions of the country are voting with their feet, which sets up some ugly dynamics when you look at national policy and provides some real heartburn for national manufacturers (see also California emissions standards).

A balkanized country is not a united country.

The people who will get crushed are speculators who overbought and aren’t reading the room. Price declines for STR will make anyone too close to the edge fall off, if your rental equation can’t handle a decline in either price or volume, you’re in trouble.

I am going to be following this type of internal migration story with interest.

I read on some political boards that many Dems feel trapped in their red states, which they hate in many ways, because either they can’t afford to move to some of the more expensive blue states, or family obligations and such keep them there.

But as the screws tighten in the coming attempt at implementing the handmaid’s tale and xtian nationalism in the silly states that are receptive to that nonsense, I expect to see more migration of this type from those who can afford it.

California may become interesting that way – the less expensive central valley and far northern counties that are currently red or red leaning may get an influx of Dems from other states who cannot afford housing in the blue urban areas, but may be able to in these areas of California.

Just a hypothesis that could be wrong, but which I’ll observe to see what unfolds.

I agree with a lot of it. Not a bad narrative, chronicling the repetitive behavior of human beings across centuries.

in a unsustainably optimistic economy

That is one answer to the question that requires continuous updating, but not currently the official view. According to my favorite WWF president, again. Donald Trump.

America is about too enter a golden age? if I remember correctly , is a gift that is given when the day is done.

America is the best we have right now. In fact, the world’s wealth agrees. America is the least dirty shirt in laundry pile of monetarist experimentation, that failed.

The roaring 20s redux coming to a country near you. Elon and Jeffy and Mark!

We’ve seen before what follows, but history is apparently not Americans’ strong suit.

Canazei, Following the roaring 20s came the stock market crash of 1929, the Smoot-Hawley Tariff of 1930 and the failure of the Kreditanstalt Bank in Vienna in 1931. Can anyone guess the major political event in Europe in 1932? I definitely agree that history is not America’s strong suit.

I think you’re just saying large metropolitan areas are statistically more democratic . Which is just pointing out a rural vs urban divide and doesn’t really have anything to do with anything here.

Not sure the politics of these towns is germane to the real estate market, these towns just got particularly bubbly in the recent past.

What is clear to see in most of these charts is that prices almost tripled in most places from their lows in 2011-2012 to their new highs in 2023. That is insanity. We’re talking housing – a basic human need. We’re not talking cryptos or some other speculative investment. This makes working class people much poorer and the recipients of home payments and property taxes richer. Housing so far has made a very minor correction back to sane valuation levels.

Wolf’s last name is one used to measure the intensity of earthquakes. Sadly, it’s going to be another sort of Richter that will measure the

massive quake that eviscerates the housing market.

Absolutely agree.

The elite billionaires and Forbes 500 millionaires are the 21st century “Marie Antoinettes” running the country and they are completely clueless about the real state of our economy. I fear things are going to get much worse.

Yes, indeed. I always say, it’s going to have to get a LOT worse before it gets better.

Things are going to get worse?

Then things are going to get better?

What says the drunk sailors…the vigilantes. And what says the fat lady…. what does Engelburt Humperdinck think.

The early 2010s were known for QE, and the pandemic response was almost zero interest rates, leading to asset inflation.

Up here in Canada, policy is designed in a way to enrich the property investor class while putting working class and lower middle class Canadians at a huge disadvantage.

The owners of Toronto and Vancouver property vote against more housing supply, yet vote for increased “population growth” in order for them to pack several families into a basement charging extortionate rent.

Houses which went for C$300,000 in the middle of York Region were selling for almost C$2.3 million at the early 2022 peak.

Toronto’s housing supply has increased considerably in the past quarter century but it has taken the form of condos and townhouses. The central city was built up years before that. If you want to buy a single family home there, you will pay up. The house I grew up in came into the family in 1929 for C$1,250. In late 2023, it was listed on a real estate web site for C$1.7 million. I recognized the exterior but not the interior which had been totally upgraded. Toronto residents do not get to vote for or against new housing. But the high cost of housing in Toronto and Vancouver has helped bring down Justin Trudeau’s political career.

I don’t believe so for reasons I posted earlier.

I still think this rise was the result of slow building recovery, zoning restrictions limiting construction, population increases, and the rise of Airbnb slowing taking millions of units off the market and turning them into hotels.

It’s never just one thing, it’s a storm that comes together.

Cities in Florida because of changing building codes and the insurance crisis have had to make expensive upgrades just for hurricane mitigation. When you add renovations to old bath and kitchens it is big bucks. I picked up a cheap cash out in the fall of 2020 and spent easily $250+. And I already had a new tile roof. My neighbors across the street just completed new tile roof, new hurricane windows, front door and paint for $110k. For a two story 2600sq foot house.

Zillow pricing is totally inadequate in Florida’s market because they have no way of pricing upgrades when comparing identical models. I did all of the above upgrades plus 3 new baths, kitchen, flooring and built ins. My house it priced 400k under current market price when comparing resent sales.

I would love to downsize and sell my family home to a family. But capital gains on primary residence are holding many people back because they have no place to go. Single story ranches are very over priced.

I think it is the capital gains TAXES not the capital gains that are holding people back. The exemption from capital gains taxes has not increased since 1997. Two of my very senior neighbors are now in assisted living facilities or nursing homes. Their prior homes remain empty. When they pass on, their former homes will transfer to older relatives with no estate or capital gains taxes.

Well, on the bright side, it is a problem that affects us all which generates potential political energy that may have prevented the tragic message of the asset inflation charts. Prices for overpriced assets have not noticeably come down, yet. I sense they may be hanging on by their finger nails

A decade-long central bank policy of rate repression resulting in a decade-long moonshot in real estate prices (at least in these metro areas), peaking when the monetary authority takes 3 of its five fingers off the scale.

That (un-elected) policy-setting committee is one powerful group!

Oops – Cities, not “metros” as I mistakenly stated above.

Imagine how much worse it would be if we left it up to an election by the ignorant proletariat.

Here here! Let’s have sound money and we don’t need the Fed.

I agree and suggest that the discrepancy between the cost of living and the median wage is not just political but constitutionally against the common defense.

96 pct of the people we interact with have less than the 400K income level that the group think DC Congress has determined is at the verge of economic inconvience. As a matter of fact, most of them make less than 40 dollars per hour which computes for an annual salary of about 80 grand.

This is America. Gave me an opportunity.

The New Orleans single family homes are priced at the level of NOLA condos. Is this an outlier? I don’t see this happening in the other big cities.

Never mind… looks like the same chart was used for both single family and condos for New Orleans

My apologies, and thanks for pointing that out. That was my goof-up. The condo chart for New Orleans is now posted.

Thanks, that is surprising condos are quite a bit more expensive than single family homes.

Condo fees in my town are often around $1000 per month on top of the $1000+ in taxes per month.

It can be very hard to sell a condo, I suspect, and especially when people know these fees are soaring. Who keeps what is not spent? Does someone get a fee for setting up and keeping the fund where these funds are held?

My first apartment, 20 years ago, was $650/mo.

HOA fees also apply to houses that are in a HOA, and many developments have a HOA. But houses without HOA have homeowners insurance and property taxes. In some states, insurance is the biggest problem (Florida, California, etc.), and that affects HOAs as well as houses without HOA. Insurance has gotten so expensive because of the risks, and because of the replacement costs for insurers that have shot up by 50% or more over a few years, and doubled over a few more years in many places.

Many HOAs in my area also cover exterior expenses like painting, roof repairs, and roof and window replacement. Of course, a buyer needs to know what the age and state of those covered components are, and what reserves have been banked to cover them, and when.

Without examining these HSA issues, the monthly fee level is relatively meaningless.

My main issue while not wanting a house within in HOA was the often had unreasonable and often abtritrary rules. No cars overnight on the street or garbage cans are not bad guidelines but unreasonable if militantly enforced with high fines. The deal breaker with me was noise which wasn’t connected to city or county laws but if somebody complained. I do see where an HOA can keep home values up and add value so to each their own. It is nice to not have any of those fees and just have property tax and home,/flood insurance which is about 10K a year on a 600K house.

I wouldn’t mind the fees if they were reasonable, it’s the rules about paint colors, window treatments, landscaping, solar, wind chimes, flags, parking, and 40 other nitty things.

If I were running the HOA the only rules would be around basic maintenance of yard & house and no RV, boat, or toy parking for longer than a week.

That’s what makes a market, Sandy. I like those detailed rules to keep others from trashing the ‘hood with poor taste and clutter. I live where there are no such rules, and it would be awesome if there were some fairly strict standards.

Utterly baffling to me how Americans are so prideful in individual freedoms but will live somewhere that will force them to pay money and won’t let them paint their front door a different color or they potentially get a lien placed on the very home they live in and pay for.

I rented a room from a guy for a year or so in an HOA community. Never, and I mean never will I live on an HOA again. I’d rather be living in a camper pulled by my truck and stuff my few things in a storage unit than do that again.

Busybody boomers with nothing to do but legally stalk and harass people over the dumbest bullshit ever.

It snowed while you were at work and you didn’t have the snow shoveled off your driveway within 2 hours? FINED!

You opened the hood on a vehicle to fill your washer fluid? FINED!

You mowed the grass and some of the clippings didn’t get completely vacuumed up into the bagger and turned brown? FINED!

A windstorm came through and blew your garbage can over in the middle of the night? FINED!

Water bill is expensive so you set the sprinklers to water once in the morning and not twice a day? FINED!

The old fellow I was renting from paid 550 dollars a month as a base HOA fee. He got popped for 100-150 dollar fines every month if not more often. The gated community was full of people flying Gadsden flags from their trucks and would have 3% bumper stickers and regale the world with the coming communist regime in the US.

It sure seemed to me like they were living in a communist dictatorship as it was. Nevermind the 1.5mil dollar home made with spackled walls because the dryrock work was so poor you couldn’t paint it smooth or the HOA blowing 100k dollars every summer to “seal the asphalt” so it looked new and shiny black instead of like dull asphalt. Anything to keep up with the Jone’s.

Again, utterly baffling.

Please sign me up for your newsletter!

Apple,

Are you talking to me? If you would like to get the WOLF STREET email updates, you will get an email each time I publish an article. The email has the headline and subtitle of the article and the link to the article. It’s free.

If this is what you want, please sign up here at this signup page:

https://wolfstreet.com/sign-up-here-for-wolf-street-email-updates/

Trucker Guy,

Facts! With an HOA you don’t really own your home, the HOA does. You’re just a tennant.

“I do see where an HOA can keep home values up”

If that were true, I should be able to lower my assessment by trashing the front yard. But I don’t think it works like that.

The HOA is like a lean holder on the property with rights that, at the extreme gained possession of an incalcitrant homeowners home.

Soon we may wake up and realize that it is the unregulated judicial branch that is the constitution’s worst enemy.

Add landscaping too. And as you’ve said, reserves for maintenance, which many people don’t put aside for say their single family home.

A lot of folks think of HOA fees as something completely additional to owning a property. In reality, depending on the HOA, they can cover a lot of what a single family property owner would have to pay for out of pocket anyway.

“they can cover a lot of what a single family property owner would have to pay for out of pocket anyway.”

How is that different than renting and having the landlord fix stuff?

I don’t mean the legal difference – the practical, everyday life differences. If you see some rotting wood under your siding, can you fix it yourself or are you required to call someone? Can you smoke on your property and have overnight guests? Many leases I’ve signed have these restrictions a do many HOAs.

Nothing wrong with renting, I did so for 8 years. But “owning” with an HOA seems like the worst of both worlds. A bunch of rules to follow and you still have to mow your own lawn.

Even a small HOA payment now can become a large HOA tomorrow. I can see old people ready for the grave doing an HOA because an HOA is similar to a grave yard, may as well be dead, you aren’t allowed to do much unless the cemetery or grave digger approves.

But some people are comforted knowing they are safe in their coffin.

There’s not a more depressive feeling than driving past the abandoned assets in your neighbors yard with no one to tell them too clean it up. The only motive that would induced American citizens to agree to pay for the HOA service. They also manage the subdivision common garden.

However, if they have determined that you have no juice and are in violation against the limit of weeds that volunteer in my wife’s never chemicals long term experiment.

I just don’t know when, if ever, economic gravity will catch up.

It’s insane.

Just to pick a random city for example: per the charts in this article, the mean price for a SFH in Oakland CA was pushing $1MM in 2022. Per google, the median income in the same city in the same year was $94k and change.

That means in oakland, the ratio of average home price : average salary is 10:1. How does this math make sense?

In my mind the only explanation is the speculative purchase of homes by whoever (individuals, investors big and small, etc). At some point, this has to stop making sense.

Dr L,

“home price : average salary is 10:1. How does this math make sense?”

A big part of it is the buyers are not 10:1. They aren’t average salary earners. Meanwhile, lots of retirees who bought ages ago for a fraction of this price may appear to be 10:1 or 30:1, but they’re more like 3:1 (or whatever) vs their cost to live there now. My dad is one of those, approx a 40:1 ratio.

Too many people focus on this average income / average price ratio. It isn’t meaningless but it’s not a very good measure of anything.

I think a better measure would be whether workers with say 10 years of experience can afford an entry level home.

I’d argue that income based indicators have less applicability in desirable areas. On the coasts, it’s more about how much savings and wealth you have. Cities are gentrifying.

Wealth has concentrated as a result of monetary policy, including QE and rate repression, tech boom, business consolidation, rise in executive pay, ongoing trade deficits, etc.

“The federal government made $2.6 trillion in funds available to respond to COVID-19 and spent $1.6 trillion of that in fiscal year 2020.” That is a total of $4.2 Trillion.

After the new money went out, where did it go ? It did not just go “poof” and disappear. The money ended up in somebody’s bank account.

Pity the poor souls who now have all that new money? What are they supposed to do with it? Of course they are going to go out and buy assets (like houses and stocks).

Ooops. Found new numbers on how much was spent on covid.

“In response to COVID-19, the federal government authorized an unprecedented $5 trillion in pandemic response spending. The majority of the prime recipients of this funding were located in the United States, however, approximately 2,000 prime recipients in 177 foreign countries received a total of $6.4 billion.”

Source was “Pandemic Oversight by US gov.

Wow. Those 2,000 foreigners did pretty well. If my math is correct, that is about $320,000 each. They did way way better then I did.

” 2,000 prime recipients in 177 foreign countries received a total of $6.4 billion.” what makes them 2,000 foreigners?

yeah, i don’t care how much it has come down in the bay area. Could say -50% for all i care its still unaffordable. Also this isn’t even the truth of reality in the bay area. You’re crazy if you think that a single family house in the bay area is comparable to a single family house in any other city. Literally talking about a house that has to be torn down and completely rebuilt to live in the thing. And 10:1 ratio, just to be clear isn’t a thing. If you’re in any ratio of 3:1 or higher then the truth is you can’t afford a house cause you’ll never beat out any of these cash buyers (Contractors, Big Tech Stock Options, or tech companies just buying up land to own it). So tack on another $300k for remolding it. My manager used to laugh at me when I told him i was saving for a house in the bay area, he said the prices of houses were going up faster than my salary.

“Could say -50% for all i care its still unaffordable”

Unaffordable to who? Everyone likes to make these judgments based on their situation. To everyone who buys (and there are plenty who have been), it is by definition “affordable”. Everyone who can’t buy declares them “unaffordable”.

My guess is this statement has to do with median salary to median home price. Yes there’s always the rich who can buy anything.

MM1,

Probably. But the median to median is a bogus and unrealistic expectation. See my other post on this (if you want).

Sounds like Gattopardo has either a rainbow with a pot of treasure at its end, or he just doesn’t see a major trend that has been developing in this country – that MOST working class people CANNOT afford a home in Californi, never mind the Bay Area. Go check out the median home price of a home in California and report back to me. The massive bubble

has done extensive damage to the real estate market. A tripling in price in twelve years, and you wonder “who” can’t afford to buy a home? Of course, the uber-wealthy will spend money like they got it from a Monopoly game, because with today’s economy, Monopoly schemes abound (ie – Crytos, stock options, and more). We have become a country of haves and have nots, or rich and poor.

So, in response to your insensitive question of ‘Unaffordable to who?’ I’d answer ‘unaffordable to MOST Californians.’ Wise up, wise guy.

Of coarse it is hardly random which sounds the alarm that economic mischief is afoot. Especially given your evidence of the inequality in our society which exceeds all previous episodes of concentrated wealth in the nation’s history.

Great work! Really important information for people to see and understand.

Double and triple tops in some of these markets and others, and some look to be rebounding again. Real estate speculation is bad for humanity. Something needs to change. A lot of things.

DC. Things will change when there is finally a recognition that a house is actually a financial burden and not an investment. A financial burden accepted by millions and millions of folks who desire a place to provide shelter and a place to build a nest for the raising of their offspring. Only in recent times, due to the nonsense put out by the National Association of Realtors and equally nonsensible programs that show house flippers getting rich has it been thought of as investment grade activity. The conduct of our fellow citizens falling for this nonsense is best described in Charles Mackay’s famous book “extraordinary popular delusions and the madness of crowds”.

Maybe, but like everything it depends on where and when you bought. Selling my house 20 years ago and downsizing away allowed me to retire in my fifties. As I write this I am looking at trumpeter swans floating by on the river I live on. This place has never been a rental and never will be. Our last place was the home that my children grew up in. The people I sold it to had a young child when they moved in. I see she is driving now.

A house is much more than an investment in the same way that a meaningful career is much more than just a job. It’s important that you enjoy and thrive in a place where you spend most of your living hours.

My daughter and son in law have paid off their modest home this year. They are in their mid forties. This will set them up financially for the rest of their lives. They would have had to pay rent, anyway, so instead they paid off a home along the way for about the same monthly cost. Sweat equity was donated, of course.

i think you’re making the same point. housing wouldn’t have gone up the way it has if people were buying it to raise families, as you did and as the couple you sold to did.

how many houses sat vacant during the 2021-2023 madness as people didn’t want to sell and lose another 2% of appreciation each month?

that’s the mentality that needs to change. nobody should get rich buying residential real estate.

The math is simple and irrufutable. The ability to pay, the important variable, determines ones social status.

The question I have is whose paying the mortgage on all those, overpriced, for sale vacant homes.

Somebody is supporting the price,

Louie-

Love that Mackay book!

This quote applies to the current real estate markets, IMHO:

“Men, it has been said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one. —Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

This quote of his on the futility of predicting the future (and yet, we persist at the endeavor!):

“It is happy for man that he does not know what the morrow is to bring forth; but, unaware of this great blessing, he has, in all ages of the world, presumptuously endeavoured to trace the events of unborn centuries, and anticipate the march of time. He has divided it into sciences and systems without number, employing his whole life in the vain pursuit. Upon no subject has it been so easy to deceive the world as upon this.”

—Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

Regardless of Mackay’s beliefs about predicting the future, another timeless quote abides:

“Nothing goes to heck in a straight line.”

— W. Richter

Be careful with statistics. If 100 goes up 38% to 138 and then drops 19% you have lost about $26 and are only up $12.

That’s not even statistics, that’s basic arithmetic.

After four long years of waiting for prices to come down, my spouse and I have decided to stay in our current (paid off ) home. In most cases, we would be trading down, paying more and getting less if we bought a home right now. Prices have come down, but not nearly enough.

Me think the “Weimar Boy” lost control of 10 bond yield…I expect mortgage rates will stay above 7% long enough for the drunken sailor to realize spending 2/3 of their net income on house mortgage, maintenance cost, insurance etc is not sustainable…

Exactly the reason boomers aren’t leaving there existing homes

Well, that and a bunch still have adult children living with them because rents are so high. We’re selling 24 hours after the last one moves out.

That’s one of the main reasons I am still in a family sized house, living in less than a notable portion of the available area calibrated to compensate for the dour propensity of age,

I am in the same boat. Been looking for a house to buy but prices are still insane and my rent is only $500/month.

Where does Old Guy live for 500 a month ? Maybe Tulsa ?

God’s country, Northern WI.

Just like the circumstances that led to the fires in LA were a designed failure, so too is the US economy and markets being set up for the same type of conflagration.

The scum running this country have done everything to make the cancer patient look like a super model and only the most foolish are buying it.

People who once bought bonds, bought houses instead.

Yes, and the funny thing is that speculators are now all over bonds with complex highly leveraged risky trades.

Everything got twisted.

Is there a searchable database showcasing these same datapoints/dates across the top 100 U.S. city SFH and condo markets?

Sure. You can download it from Zillow. It has many thousands of markets in it, by state, by metro, by city, by zip code, it’s a huge pile of data.

Seattle and Portland graphic….it looks like a double top to me…

Per chart, we might go down to 2008 top…about $375 K….

Yeap, I would love to see that…

Looking at the same charts, what strikes me is how far the prices have too fall to entice buyers. And how refractory to a price decline that the housing market is.

I’m in Oakland, CA, and I’ve noticed that the house flipper has taken one of the properties off the market. It just sits vacant, and I walk by it every time. The property next door is the next flip; they probably bought both houses at the same time—I should do some research on that. They asked for $1 million in a neighborhood with an average value of around $750,000. Our house is valued at $800,000, but I think it’s worth at least $600,000. Rent. Prices are too high. This neighborhood is quiet but far from the 1m dollar range in value. I would rather live in a small apartment in SF than a single-family house in Oakland, but here I am. Oakland sucks. If you buy in Oakland, you are a sucker.

Living in Oakland around 2011 was a great experience. Jobs were hard to come by but housing was cheap and plentiful. The city was clean and (relatively) peaceful and the residents were happy. Then the range rovers started to move in and I left soon after. Now I go back and the whole city looks like a warzone. It’s unbelievable how much can change in 12 years. But at least we have AI

If there was ever a time to buy property in Oakland, it was 2011. At that time, I was too focused on starting a family and did not understand finance. Had I known better, I would have purchased a rundown home in a good neighborhood and made it my own. Now that my ability to afford a home has diminished, I am stuck renting. I struggle to see the value in buying overpriced properties in this city. There are areas with homeless encampments where hygiene is clearly lacking and visible drug use is every day. I’m not blaming anyone for the city’s conditions, but it has been mismanaged for several years. As a remote worker, I wonder where to buy or relocate. AI is hype for shareholders. It was already here in one form or another. AI will accelerate crap to crappie. No one will survive…

The cause of all this seems to be the 2% mortgage free money bonanza in 2020-21. But why did that tidal wave of cash wash over every market except for San Francisco and New York that barely registered a blip? Shouldn’t the money supply & inflation impact all markets somewhat equally?

no, because it wasn’t solely 2% money. it was also the belief that people would be able to work remotely forever. there were always a lot of people who wanted to live in idaho, denver, san diego, honolulu, miami, but they couldn’t find jobs there.

then the pandemic happened, and people took their high salaries from chicago, new york, d.c., and the bay area and brought them elsewhere, driving up prices. people saw what was happening, and refused to sell, leading to the “low inventory” meme. basically, prices previously were based on the incomes in the area. after the pandemic craziness started, the “law of one price” i learned in university years ago kicked in, and housing prices in desirable markets like the ones i named up above reset to the incomes from the highest cost of living areas, and the bubble was born.

as people are realizing fully remote is not here to stay, this is reversing, but it happens slowly.

This is also partly about remote work, people taking their big city salary and buying a home in Boise or Austin or Park City. The Fed inflation of home values from 2020 to 2023 was very broad, but the spike hit biggest in the “Zoomtowns”.

haha, i beat you to that punch. but yes, places that were appealing to a lot of people, for whatever reason, but didn’t have the incomes to sustain high housing prices.

These prices are not inflation-adjusted, which makes the situation look worse than it actually is. There was a large inflation about 4 years ago, including a general increase in both prices and wages (because wages are prices). If you printed those graphs in real terms then the increase would be much less dramatic.

As one extreme example, condo prices in San Francisco are only up about 7.5% in real terms since late 2003. A 7.5% increase over 21 years is not that much.

Bear in mind that the minimum wage in California has increased by more over the same period. If you’re a fairly low-wage worker making 20% over the minimum wage, then a condo in San Francisco is much CHEAPER now than it was in late 2003, before any of these bubbles began.

1. BS. The other way around. If you inflation-adjust falling prices they look even more terrible. We had close to 20% cumulative CPI inflation since Jan 2021. So the price fell by 20% and there was 20% inflation, you lost close to 40% of the purchasing power of the house.

2. These home price charts ARE INFLATION INDICES. They measure how many dollars it takes to buy the property. They’re measures of HOME PRICE INFLATION. It’s conceptual nonsense to inflation-adjust inflation indices. CPI measures consumer price inflation, it measures the rate of change of consumer prices, which are dominated by services. Houses and condos are not consumer items; they’re assets, and these charts ARE INFLATION INDICES of home prices.

There have also been large swings in mortgage rates over the same period, which also affect prices. Most 1st-time homebuyers take out a 30-year mortgage and are looking for a monthly payment they can afford. After adjusting for both mortgage rates and inflation, the monthly payment for an SF condo is not much different from what it was in 2016, and there hasn’t been much of a decline.

If you adjust for both inflation and mortgage rates, then you’d get the following prices for a comparable SF condo:

2004: $4,442 per month assuming 20% down

2007: $6,334 per month

2012: $3,604 per month

2016: $6,047 per month

2020: $5,705 per month

2024: $5,808 per month

These figures are approximate because I estimated some prices by looking at graphs visually.

Of course you can argue that we shouldn’t adjust for inflation and mortgage rates. However, the point I’m making is that the situation is not the same as it was in 2007. In 2007, prices had shot up despite increasing interest rates. That degree of unaffordability has never been reached since then. The graph showing a housing bubble which is dramatically larger this time (2016-2022) is partly an artifact of inflation. The recent dramatic decline in prices is largely caused by increasing interest rates, unlike 2009-2012 when prices crashed despite declining interest rates.

There has also been a 19% increase in median household wages since 2004. If you adjust for this also then prices are only 9.9% higher now in SF than they were in 2004, before those bubbles began.

I agree with you that there has been a second bubble, but it’s not as bad as the first. Affordability has not gotten as bad as in 2007, and people can pay their mortgages to a much greater extent. The situation is not the same.

There are AFFORDABILITY INDEXES out there. They use a formula of price, down payment, mortgage rate, insurance, property taxes, and local wages. If affordability is what you want, go look at that. The Atlanta Fed has an interactive model you can go play with. And it has ZERO to do with CPI.

Good points Tom, affordability really is the ultimate driver of home prices, with temporary peaks due to greed and valleys due to fear thrown in. I look to experiences at car dealerships for some insight into human nature and how that translates to home prices. Many times dealers will try to negotiate in terms of monthly payments rather than the price of the car or the price of the extended warranty, why would they do that if it didn’t work? You want that shiny beautiful car that you think you can’t afford, no problem, let’s get you an affordable monthly payment and it will come with an extended warranty for just $x more per month! It works because they know you want that fully loaded beautiful truck that you think is out of reach, and they provide an option that can make it a reality for you. Same with houses, people that want to buy a house will buy it if the monthly payment is affordable, and if the affordability gets better due to perhaps lower interest rates or higher wages, then they will buy a nicer house because now they can afford it. And if you provide them a negative amortization loan that cuts their mortgage payment in half, then they go for two or more houses like in 2005-2007 and become “real estate investors”, or buy a Mc Mansion on a hill and feel on top of the world.

Getting ready to list a home in the OKC metro this spring for my mother in law that died Nov 2024. Sooner we get it listed the quicker we can sell . The suburbs is Edmond ok the home is 50 years old but well maintained on 1 acre in town no HOA . About 100 usd a square ft . Good prices in OK for those wanting to retire in a lower cost area .

Prices range from 100 a sq ft to 200 a sq ft for higher end homes.

Go OKc Thunderb NBA and the tallest building in the USA has been proposed for OKC downtown . Disclosure I live in Texas. Would like to sell the house quickly for market value. That’s a difficult thing to decipher with few comps .

Bloomberg: Home sales stall with 7% mortgages…

I’m surprised to see these price declines in Washington D.C. If it’s true I think its due to the lack of affordability since mortgage rates went up after June 2022. Nothing more. With government workers now being forced to work back in their offices (new Executive order), I believe a lot of them will think twice about suddenly incurring a long commute. The new administration’s employees may like to be closer to the employment which should boost demand for city housing.

“I’m surprised to see these price declines in Washington D.C.”

Here is your comment about this topic from Jan 13, 6:03 PM, regarding an earlier version of this chart:

https://wolfstreet.com/2025/01/12/the-most-splendid-housing-bubbles-in-america-dec-2024-in-21-of-the-33-metros-prices-have-now-dropped-below-2022-peaks/#comment-621919

Washington DC has been hit hard by the pandemic aftermath. About 40% of the small businesses have closed. WFH has decimated the downtown area businesses which depend on foot traffic. Crime is out of control. I’ve never seen a decline like this in my entire time here. No one wants to go downtown unless you have to. With the changover in administration a lot of Federal appointees, 5000 in all, will be losing their jobs. Most of them are Dems many who who prefer city living. The new employees, mostly, Republicans will move to Virginia, and the exurbs in Maryland. So look for a housing glut in DC to materialize further depressing RE prices there while the suburbs will flourish. Any metro-wide average price data is very misleading as Wolf’s data is already showing.

I’ve had a change in heart since my last post. I would bet that with the new administration pushing for Washington D.C. to be a model city, removing the graffitee, lowering the crime, hiring more police, reviving the small business community, the decline in the city will now be over. We’ve definitely reached rock bottom here. It has nowhere to go but up. While most of the new Republican appointees will chose to live in Northern Virginia vs Washington D.C. there are still a lot of contractors and people who are not connected with the adminstration, and even some who are, who will chose to live in the city once things turn around, which I predict they will.

Swamp Creature,

I’m still waiting for an example of a new-issue CD with a 5% coupon. You’ve claimed these exist but I can’t find them. Please share.

ShortTLT

My Credit Union, NorthWest, just rolled over my 1 year 100K CD this week. I will go in and ask them what the new rate is. The old one was 5%. I think it’s 4 1/2% .

The other day I went on Zillow for the first time in a couple of months. My focus is in the Coachella Valley (Palm Springs – Palm Desert area). The market in the Valley has been on fire for the past 5 years, with many nice but still affordable homes (previously around $300K) now selling for 2x+ from just a few years ago. The Valley attracts a huge amount of tourists and became a hot spot for AirBnB property owners and SFR REITs and hedge funds. With that said, I was somewhat amazed to see a lot of listings with large price reductions.

The housing market here in the desert is opposite that in most other US markets, since the winter is our busy season due to tourism. I found it interesting to see numerous $20K and even $50k price cuts. It will be interesting to see if the number of NOD and foreclosures will start climbing soon. BTW. We are now tracking another small mid-century hotel in Palm Springs with a recent NOD.

Of the cities that matter the most, thinking Manhattan, which one is performing the best in terms of a steady upward progression?

Thank you.