Inflation far from over. ECB risks throwing fuel on top of it.

By Wolf Richter for WOLF STREET.

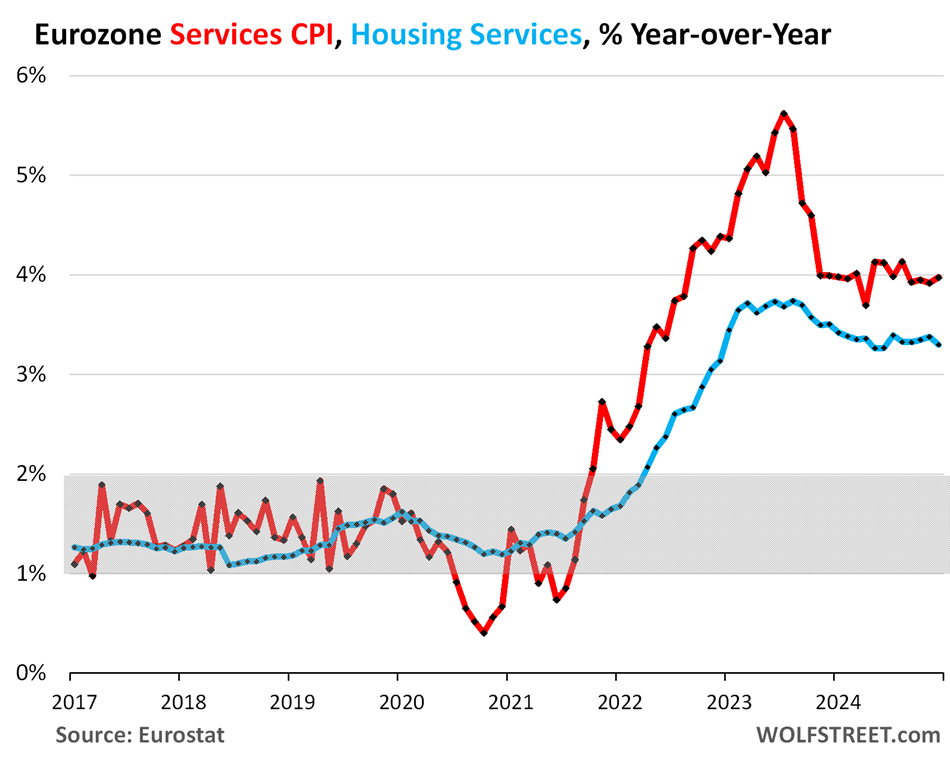

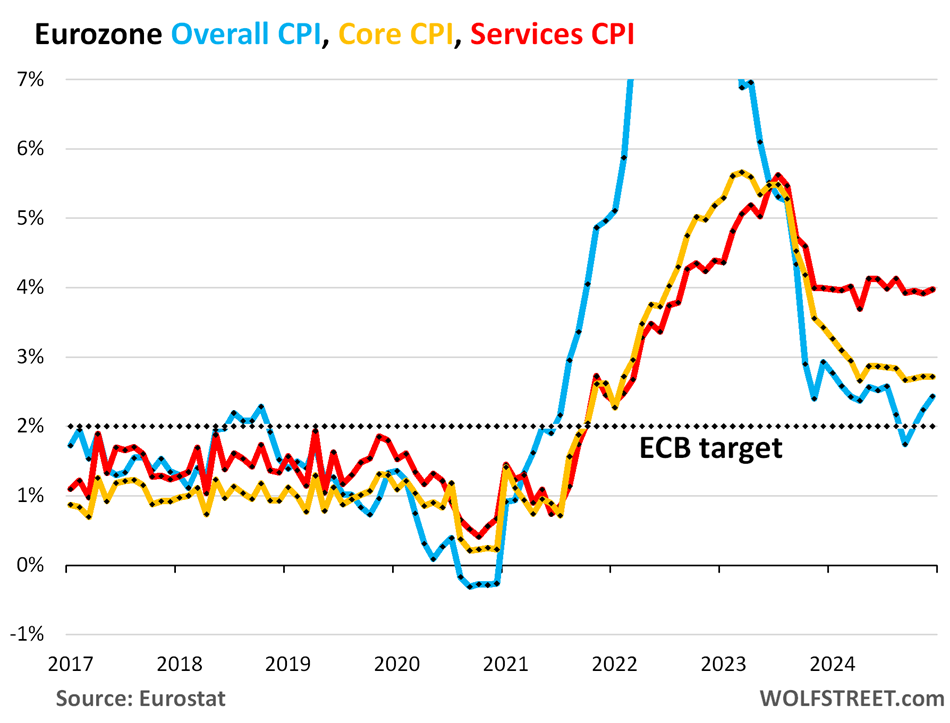

Services inflation in the 20 countries that use the euro accelerated to +4.0% in December, according to Eurostat today. This marks the 13th month in a row that the services CPI has been in the 4.0% range, roughly two to four times what prevailed before the pandemic (between +1% and +2%), and two full percentage points above the peaks before the pandemic and not making any progress at all (red in the chart below).

Its housing component, the CPI for “services related to housing” decelerated a tad to +3.3%. It’s other services that consumers pay that are not related to housing that keep the services CPI nailed to 4.0%. The shaded area indicates the pre-pandemic range.

Housing-related services include actual rents paid by tenants; services for the maintenance and repair of dwellings; refuse and sewage costs; repair costs for furniture, furnishings, floor coverings, and appliances; domestic and household services; and insurance connected with the dwelling.

Worries about services inflation have for months cropped up the ECB’s announcement about its policy rates, which it has cut four times so far. This stubbornly high services inflation “reflects strong wage pressures and the fact that some services prices are still adjusting with a delay to the past inflation surge,” it said at its December 12 policy statement, when it nevertheless cut its deposit rate by another 25 basis points to 3.0%.

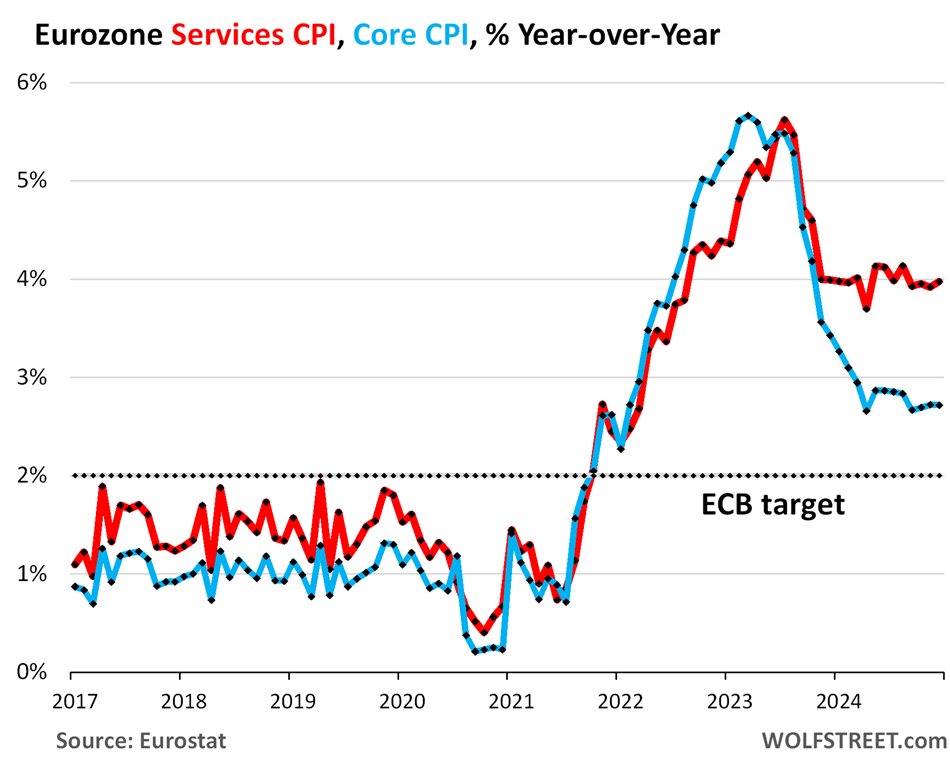

Core CPI – which excludes food, energy, tobacco, and alcohol products – rose by 2.7% in December and has been roughly in the same range for nine months and up a hair from April 2024.

Core CPI is dominated by services, but also includes goods other than food, energy products, tobacco and alcohol. Prices of durable goods plunged off the pandemic spike and by early 2024 turned the year-over-year CPI of durable goods negative, this plunge in durable goods prices pulled down the core CPI.

But durable goods prices stopped plunging and over the past five months have ticked up again, which has been whittling down the year-over-year declines. If this trend continues and moves the year-over-year durable goods CPI into the positive, while services are stuck at 4%, then core CPI will accelerate away from the ECB’s target, rather than cool toward it.

Core CPI (blue), which has been running roughly in parallel with the services CPI (red) since April and not cooling any further, remains well above the ECB’s 2% inflation target for core and overall CPI (black dotted line). The ECB has been preaching for many months that core CPI would go back to 2%, while core CPI has refused to do so.

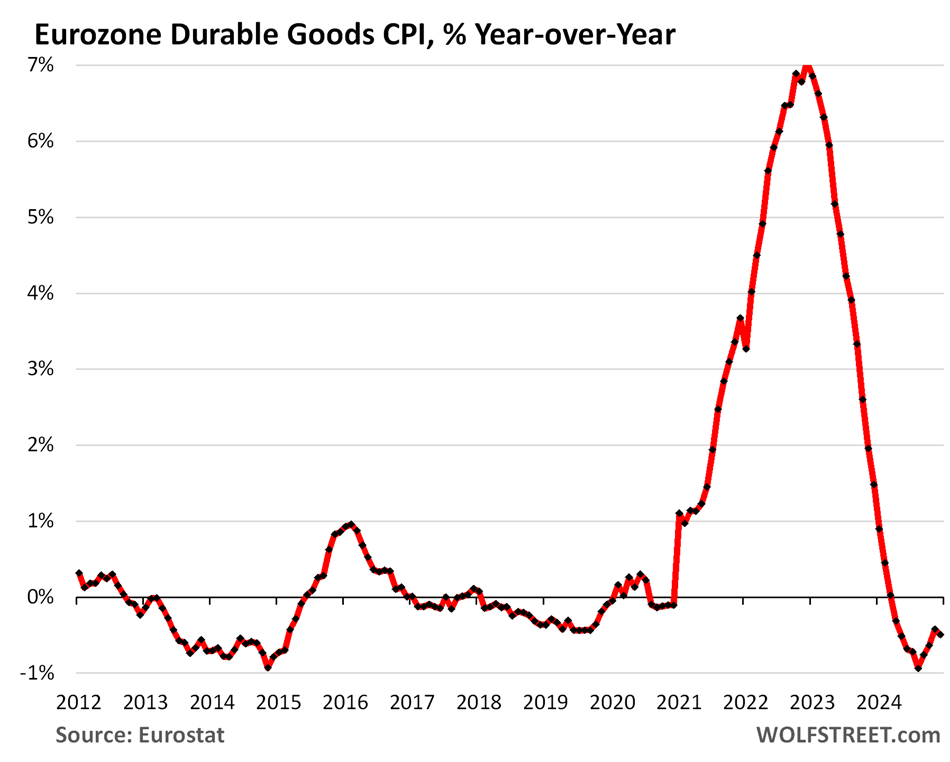

What had caused overall CPI for the Eurozone to cool substantially between mid-2022 and October 2024, were the plunge in energy prices off the huge spike, the drop in durable goods prices that had surged during the pandemic, and relative stability in food prices at very high levels. But now that honeymoon of cooling overall inflation is over.

Durables goods CPI rose over the past five months on a month-to-month basis, by 0.5% combined, which whittled down the year-over-year declines from earlier in 2024 to 0.5%. The spike in durable goods prices during the pandemic was caused by shortages and the accompanying price gouging, particularly with new and used vehicles, same as in the US:

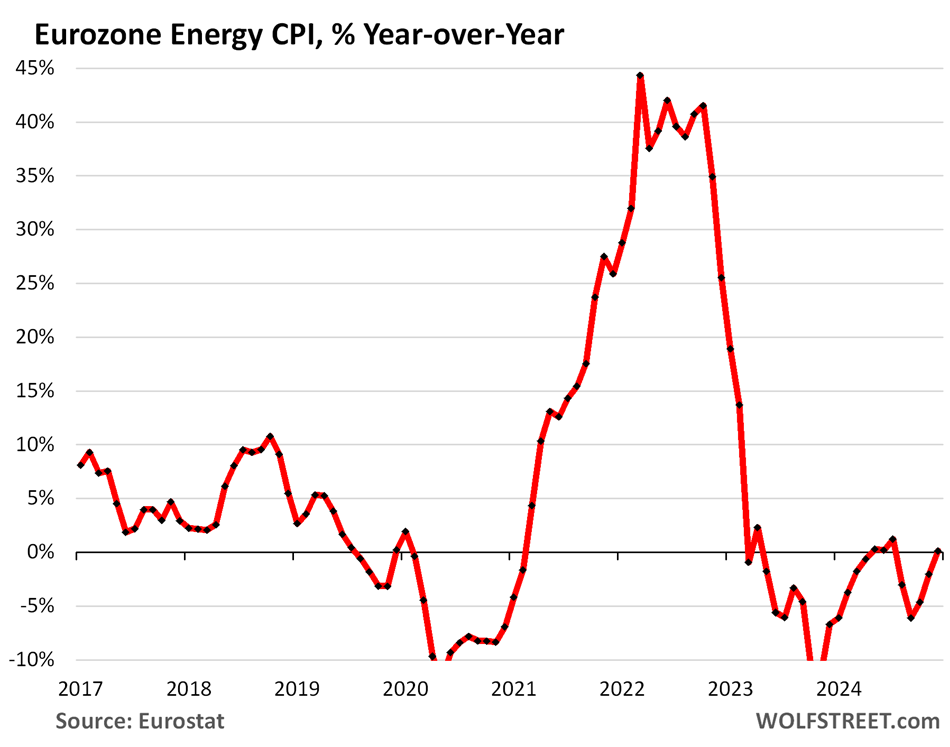

Energy CPI, which tracks prices for gasoline, diesel, natural gas, electricity, heating oil, etc., rose for the past three months, on a month-to-month basis, by a combined 1.5%, after sharp declines in the prior months. On a year-over-year basis, it is now unchanged.

Note the 45% year-over-year spike in mid-2022. This caused overall CPI to spike as well. Then came the plunge. In late 2023, the energy CPI was -11% year-over-year, and the negative readings mostly continue through November, but getting smaller.

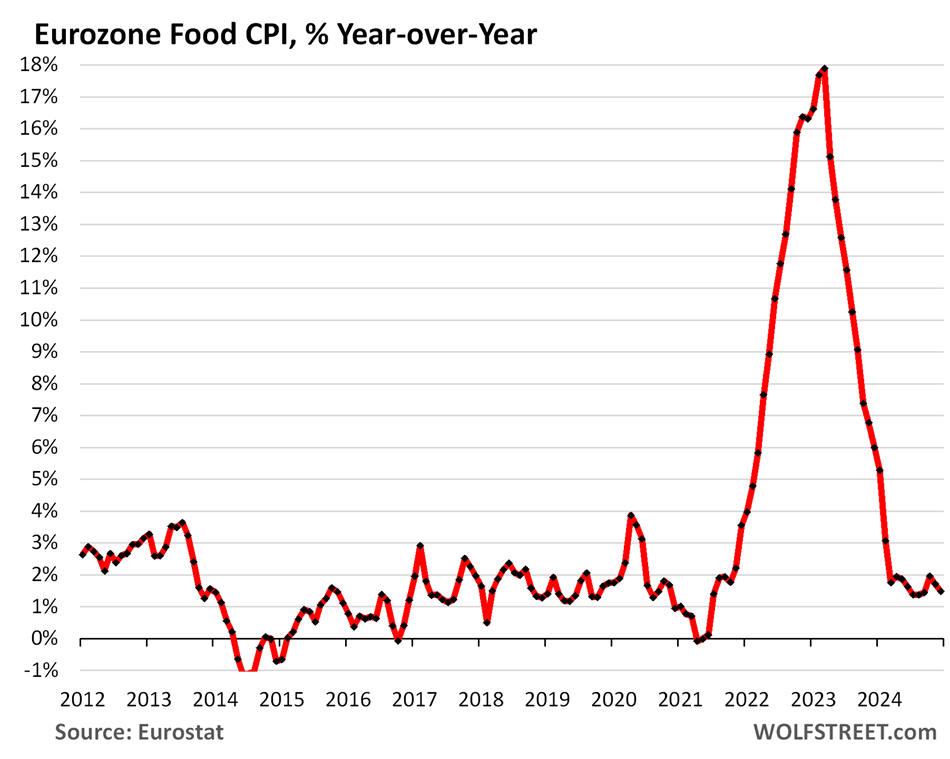

Food CPI, after a, 18% year-over-year spike into early 2023, has cooled substantially, rising by 1.5% year-over-year in December. This cooling of food inflation (the year-over-year rate of increases slowed form +18% to +1.5%, with prices at very high levels) has contributed to the cooling of overall CPI. But that’s now over too.

Overall CPI rose by 2.4%, the second acceleration in a row and is now roughly back where it had been 13 months earlier, in November 2023.

It had been pushed down by the plunge in energy prices (deeply negative year-over-year readings), the drop in durable goods prices (negative year-over-year readings), and the stabilizing food prices after the spike. On a year-over-year basis, all these three elements are in the process of ending or have already ended, which is why overall CPI has accelerated.

The chart below shows overall CPI (blue), core CPI (gold), and services CPI (red), along with the ECB’s target (black dotted line). Everything is above target, and not making any further progress, on the contrary.

The problem the ECB will run into is that further rate cuts will push the policy rates below the core CPI and overall CPI inflation rates, which is like throwing gasoline on a fire.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

so the way I read these numbers, slightly worse than the situation in the u.s. it’s almost as though the central banks are acting in concert to ensure the misery is spready equally throughout the world…

Well… they acted in concert to spread free money during COVID so no surprise I guess….l

As you can see this money wasn’t free.

“it’s almost as though the central banks are acting in concert to ensure the misery is spread equally throughout the world…”

LOL!!!

Ya think? Bankers of today are not the stewards of capital and the economy they once were. Less and less money-good collateral behind all that currency that these fuckers create from NOTHING on a keyboard. Of course those digits are used to buy very real assets…

Good gig, if you are in the club…

Interesting times Franz!

The bankers are not colluding to drive inflation! The economy is, at least partially, global and therefore inflation is, at least partially, global.

It really ISN’T a conspiracy.

LOL! Bankers control credit. Yeah, shut down the flow of credit and let’s see how the economy does.

That’s totally irrelevant nonsense.

It’s not acting in concert. It’s reaction and front-running. Search for “beggar thy neighbor” to understand the reactions that currencies have to each move.

Let’s face it, we are a global economy whether you like it or not.

Energy CPI is done cooling. The floor for crude (wti) seems to be $60. The house of Saud wants $75. Of course every producer wants as much as possible.

Same with the rest of the commodities space. The spike was overblown by numerous factors and has worn off to settle at a “higher normal.”

Crude, copper, wheat, sugar… all being stubbornly high. The reset comes from an economic downturn only, which is probably even more painful than the current inflation?

I’m guessing that is also the mindset of the central bankers. The 2% rule stems from this anyway: rather erode the currency than the economy.

Eventually the entire ship sinks (good thing we have a “crypto executive order” to look forward to.) It’s not a great sign when the captain is shoring up the lifeboats (for the executive staff only?).

They would rather have inflation than unemployment at this time. But that could change.

This isn’t the ECB’s “problem,” it’s their SOLUTION.

It’s incredible their ChiefEconomist Philip Lane was saying there’s a risk they go ‘below target’ when service inflation is WAY higher and has been for indeed a year +. And Headline and Core are rising again. I get the ‘forward looking’ , but a year of no change also shows somewhat of a (nondecreasing and sticky) trend…

The tricksters in the ECB who are playing themselves fools are the governors of the French, Greek and Italian banks. They are the drivers for further interest rate cuts. And this is normal because, as always and now, these are the countries with the largest deficits, respectively, and the largest expenses on their debts.

Fairly unrelated but persistent inflation will likely just create more political pendulums in Europe where some concerning things are occuring. Voters will simply assume a big change is needed and that rarely, if ever, is the secret sauce. Basically same thing happening in US but doesn’t matter what party you install, the core problems will persist.

I have never understood the huge difference in the weights of housing in EU inflation vs. US inflation. With housing prices skyrocketing in EU and those costs being so largely underrepresented in the CPI, what is it that is really being measured by it? Definitely not what the average European is spending its money on… Moreover, what sense do ECB interest rates make if they’re being guided by an unreal measure of inflation? The lie is so much bigger than in the US…

Home PRICES are not included in the US CPI either. Home prices are considered asset prices, like stocks or bonds, and they’re not included in consumer price inflation indices. What is included in the US is rents (same as in the EU) and Owners Equivalent of Rent, which is a stand-in for all the costs homeowners bear, on the assumption that homeowners would want to recoup those cost increase through rent increases. In the EU, these costs — homeowners insurance, maintenance, Homeowners Association Feeds, etc. — are included directly as different line items under the segment of “housing services,” blue in the first chart.

Yes, I think the big difference is in the Owners Equivalent of Rent, because that has a significant weight in US CPI, but not in EU CPI

Rising services CPI simply reflects wage growth of about 4.4%. Thus, most Europeans are gaining purchasing power for goods. I would have liked to see this data point.

https://tradingeconomics.com/euro-area/wage-growth

As in the US, inflation previously exceeded wage growth and now wages are catching up. That’s a good thing, but it is reflected in the higher cost of services. The people working for less are the Asian exporters (see CPI for goods).

Regarding earlier comments about central bank intentions, it does seem like rate cuts are flying straight into stubborn inflation. In theory, a rising unemployment rate was expected to arrest wage growth, and central banks were trying to get ahead of this trend before wage growth flatlined. However, rising unemployment seems not to be happening, undercutting their expectations.

Regardless, western countries need more inflation plus lower government deficits if they are ever to dig out of the boomer generation’s national debts. The alternative is disruptive collapses as in Argentina or Türkiye’. For a country the size of the US, there is no hope of an external bailout as in Greece a decade ago.

Voters seem blissfully unaware, and that’s the really unfortunate thing. When the inflation or sudden devaluation happens, they’ll buy the politicians’ excuses again, and form the old familiar circular firing squad. They’ll blame each other while the predators enrich themselves.

“I would have liked to see this data point.”

In the wage-growth chart you linked, Q3 was the last entry. I covered wage growth through Q3 two months ago when this data was fresh, you just didn’t pay attention?

https://wolfstreet.com/2024/11/20/ecbs-own-measure-of-wage-increases-blows-fuse-sets-off-alarms-about-stubbornly-hot-services-inflation/

“ECB risks throwing fuel on top of it.”

Like Jerry recently did here?