Lennar shocked the market by saying it’ll address this situation with further price cuts; its average price to drop by 16% from the peak in 2022.

By Wolf Richter for WOLF STREET.

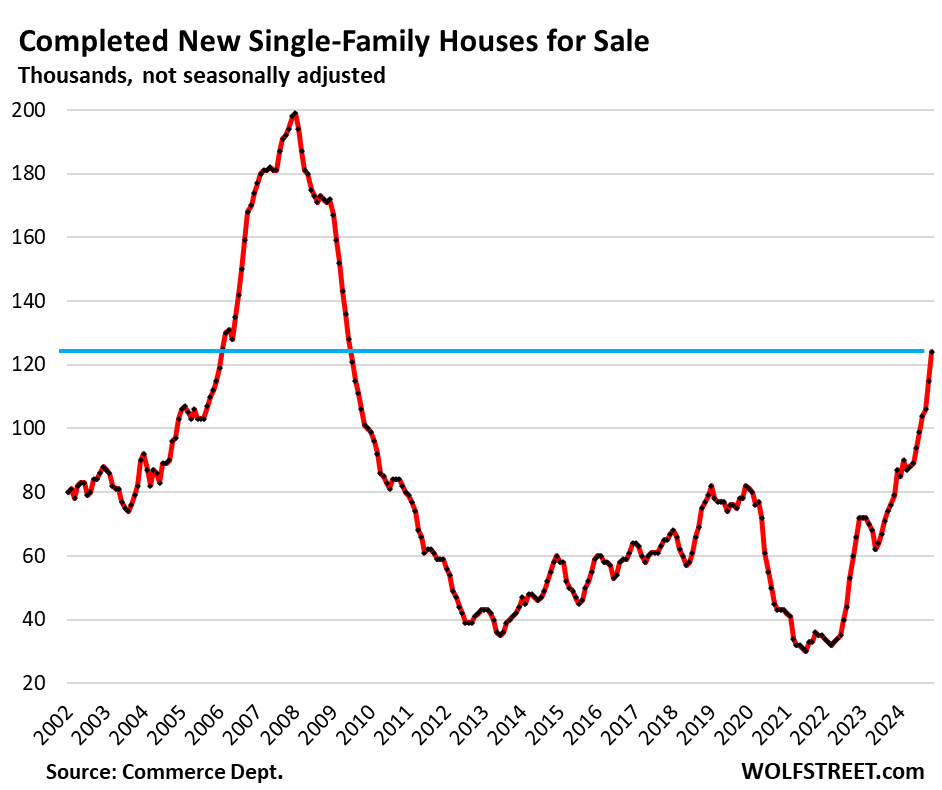

Unsold inventory for sale of completed new houses spiked by 57% year-over-year to 124,000 houses in November, according to Census Bureau data today, the highest since June 2009 during the depth of the Housing Bust when homebuilders, stuck with a huge pile of completed houses amid plunging demand, were trying to survive.

Homebuilders are trying to find buyers for these completed “spec” houses by piling on incentives, including costly mortgage-rate buydowns, and by cutting prices. But obviously, they haven’t done nearly enough to trim their bloated inventories, which continue to balloon, and they’ll have to do a lot more to bring those prices and payments down.

This surge of completed, essentially move-in ready supply is good news for the overall housing market, though not for homebuilders, and not for homeowners that want to sell an existing property. These “spec houses” will need to be sold quickly because builders have sunk a lot of capital into them, and because builders are continuing to build at a faster clip than they’re selling them – though they’re selling them at a pretty good clip – thereby adding to the pile on a monthly basis.

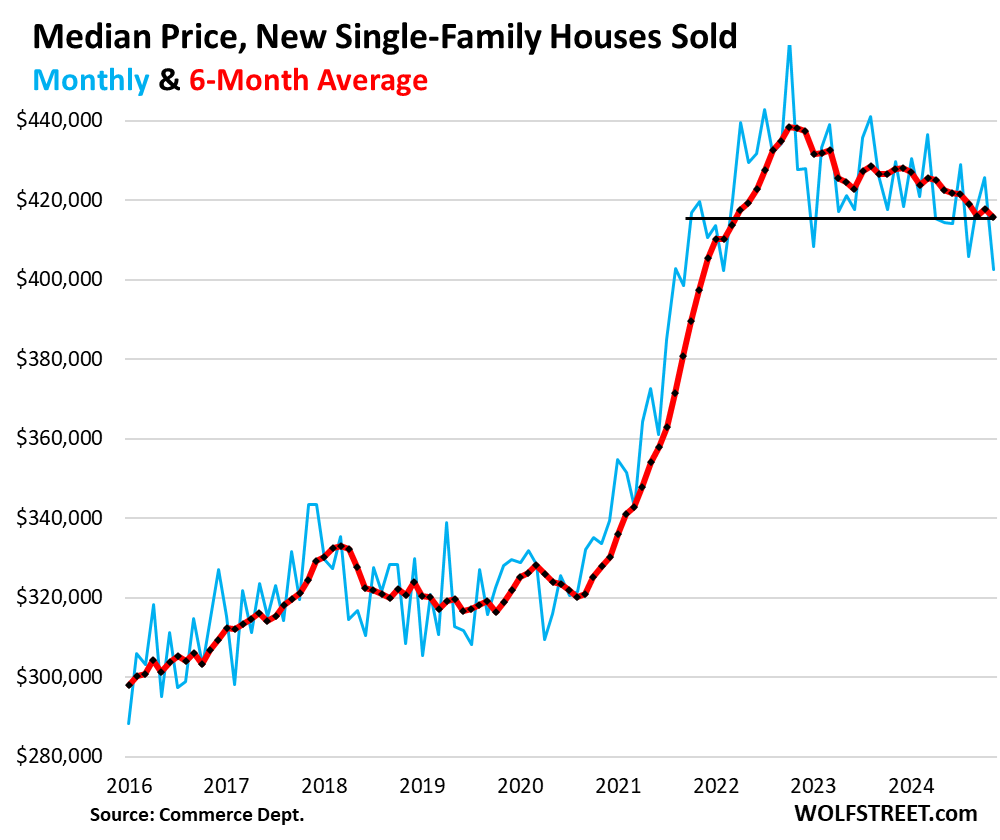

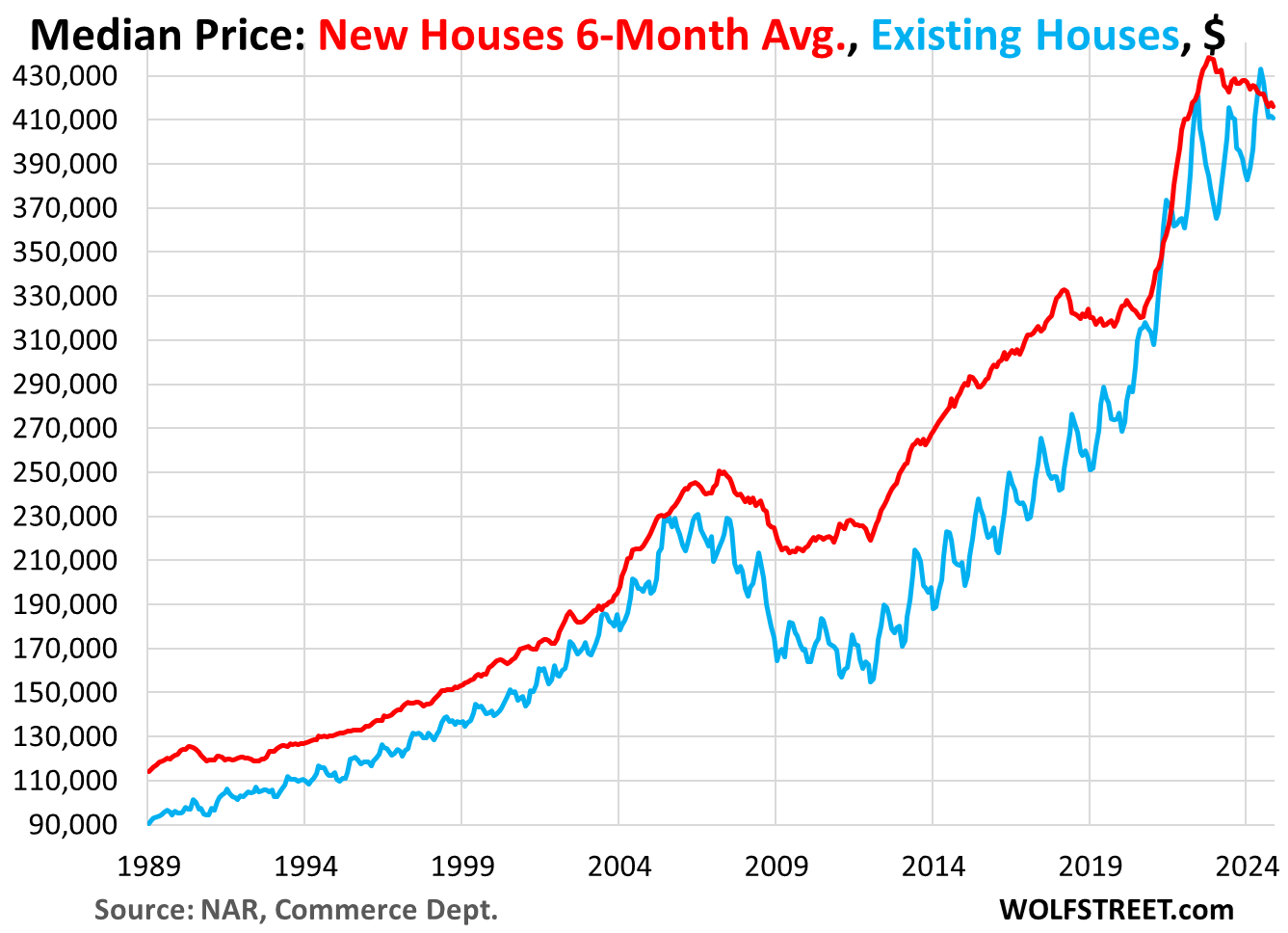

This is the situation that Lennar warned about last week. Homebuilders’ efforts to sell these completed houses will pressure prices down further. The median price in November, reported by the Census Bureau today, which does not include incentives, dropped to the lowest since 2021.

Lennar expects that the average sales price (including incentives) of homes it delivers this quarter will be down by about 16% from two years ago. Lennar’s stock price has tanked by about 28% over the past three months. More on Lennar in a moment.

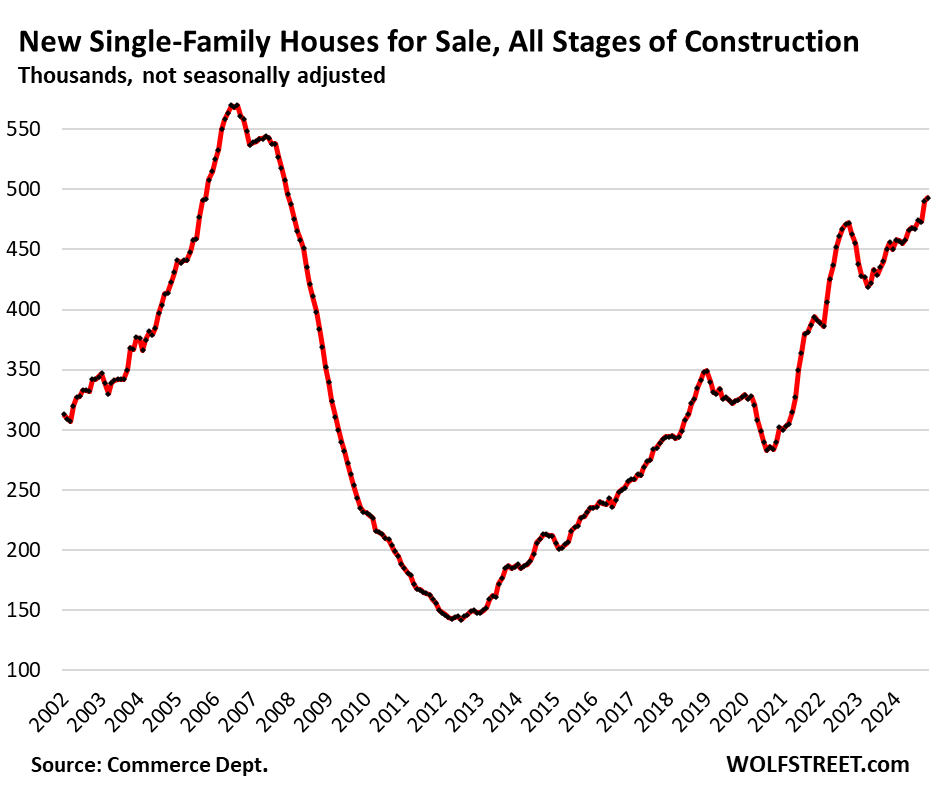

Unsold inventories for sale at all stages of construction – from not yet started to completed – rose by 8.1% from the already bloated levels a year ago, to 493,000 houses, the highest since December 2007. Supply jumped to 9.1 months.

Prices drop, incentives surge.

Big homebuilders cannot sit out this market, they have to build and sell homes because that’s their business, and they have to keep their businesses intact and keep their shares from tanking. So they’re building at lower price points, cutting prices of completed houses, buying down mortgage rates, and throwing in other incentives at a substantial expense to them – just to maintain sales volume by taking share away from homeowners that want to sell an existing property.

Despite the incentives and lower prices, sales volume is now below the targets that the big builders communicated earlier this year, while their incentive costs have jumped, and their margins are getting squeezed. The issue for them is that prices are still way too high, prices have come down, but they haven’t come down nearly enough.

The median contract price of new single-family houses sold at all stages of construction dropped to $402,600 in November, the lowest since September 2021 (blue in the chart below).

The six-month average, which irons out the month-to-month zigzags and includes the revisions, dropped to $415,800, the lowest since March 2022, down by 5.1% from its peak in October 2022.

These contract prices do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives, though they do include price cuts.

So here comes Lennar, one of the biggest homebuilders in the US. When it reported earnings on December 18 for its fiscal Q4 ended November 30, it dished up a mess:

“Consistent with our strategy of matching sales pace with production, we adjusted sales price, incentives, and margin in order to re-ignite sales and actively manage inventory levels,” it said.

Lennar reported for its fiscal Q4:

- Revenues from home sales fell 9.2% on a 6.7% drop of homes delivered and a 2.5% drop of the average sales price.

- Average sales price of homes delivered fell to $430,000 net of incentives, from $441,000 a year ago, and from $491,000 two years ago.

- Gross margin fell to 22.1%, from 24.2% a year ago, and from 25% two year ago.

- New orders fell by 2.7% to 16,895 homes, 11% below the “low end” of its guidance of 19,000 homes.

A 16% drop in the average sales price (net of incentives) from the peak:

- In fiscal Q3 2022, the average sales price was $491,000, the peak.

- Last quarter, the average sales price was $430,000.

- For the current quarter, Lennar sees $410,000 to $415,000, roughly a 16% drop from Q4 2022.

Gross margin guidance for the current quarter got slashed to 19.0%-19.25%, the lowest since Q2 2018, down from 22.1% last quarter, and down from 25% in Q4 2022, as incentives and lower prices are beginning to bite.

And Lennar said it will not provide gross margin guidance for its full fiscal year “until we have a better sense of market conditions as the year unfolds.”

Sales are decent, thanks to price cuts and incentives.

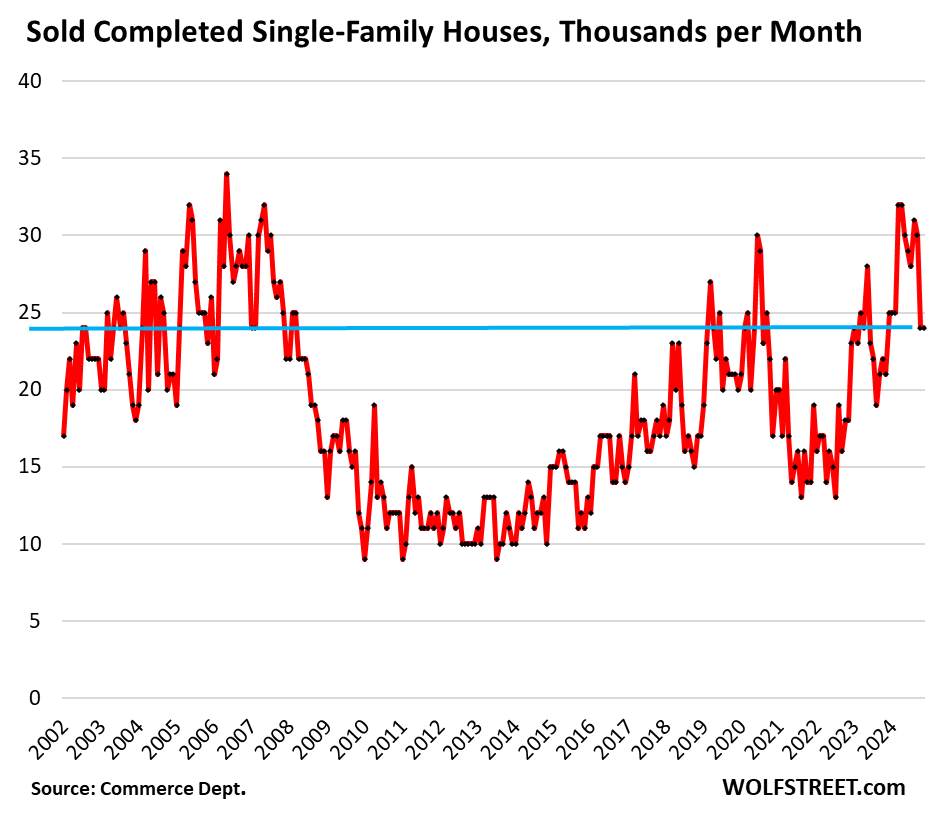

Sales of completed houses – supported by incentives, mortgage rate buydowns, and lower prices – are up about 14% from a year ago, and up 33% from two years ago, to 24,000 houses.

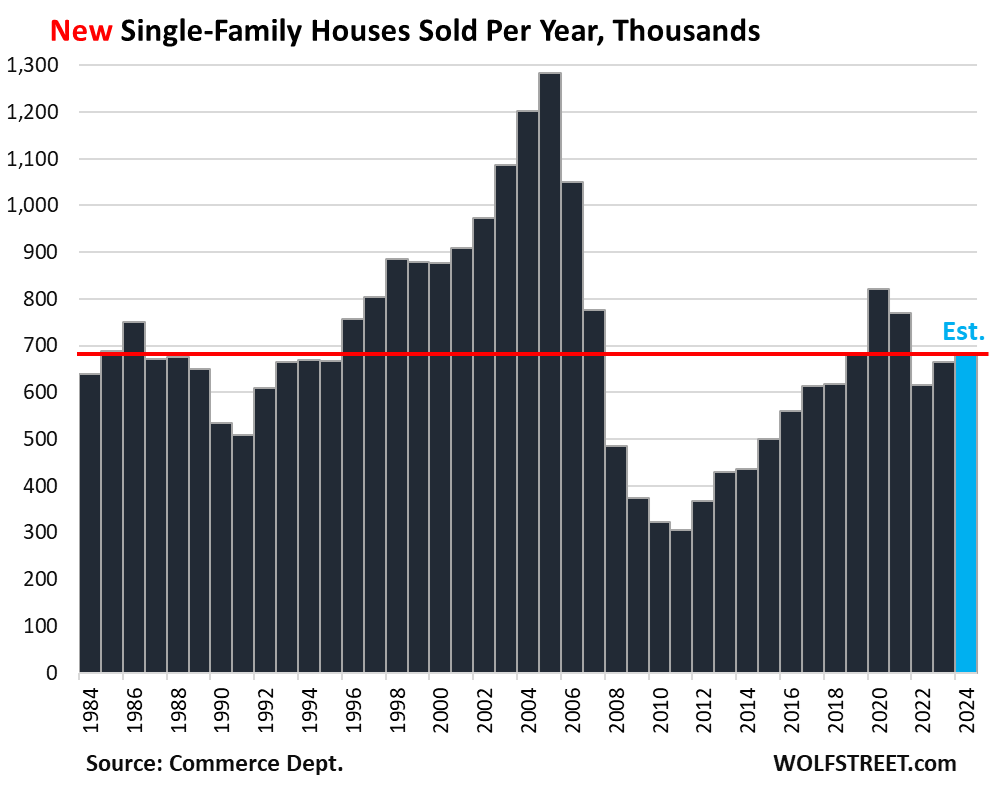

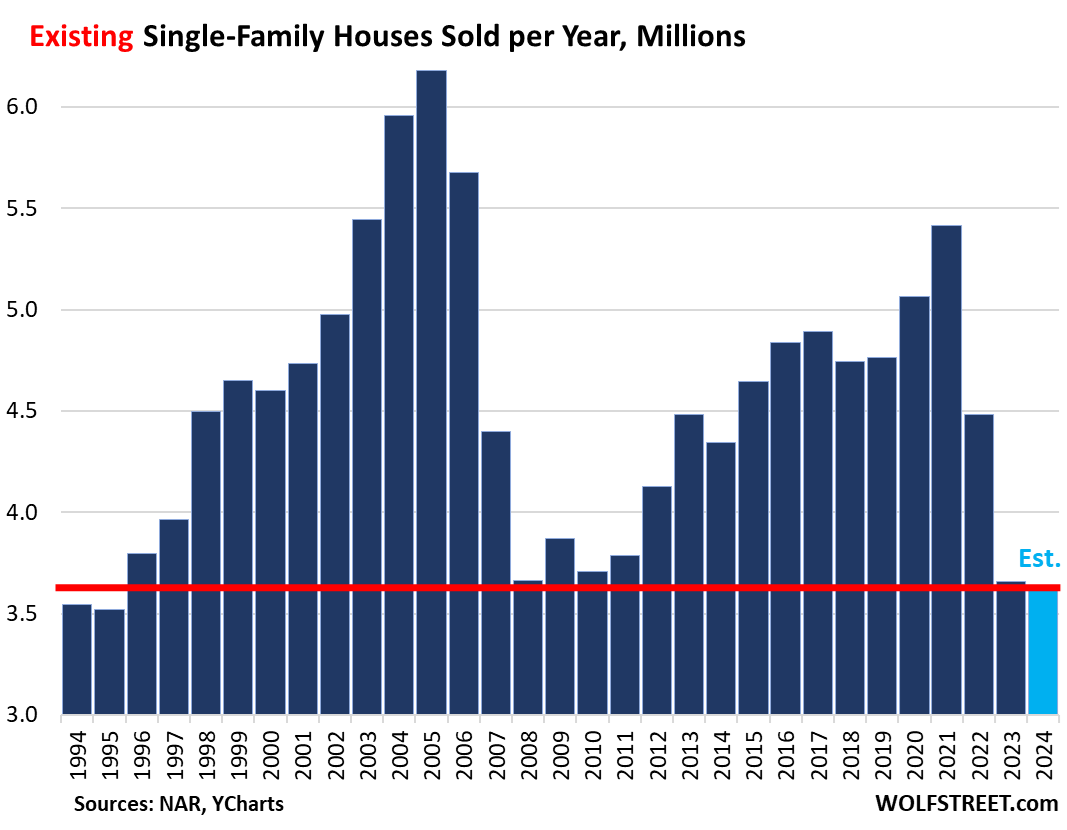

Sales of new houses at all stages of construction, from not started to completed, rose by 7.1% from a year ago, to 45,000 houses. Sales of new houses have been decent, unlike sales of existing single-family houses, where demand has withered because sellers are clinging to those too-high prices.

Annual sales of new houses in 2024 – based on the first 11 months of current sales data plus WOLF STREET’s estimate for December – rose slightly to 681,000 houses, a decent level and roughly on par with 2019, and higher than any of the prior 11 years:

By contrast, sales of existing single-family houses in 2024 fell to the lowest level since 1995, according to sales figures by the National Association of Realtors through November plus WOLF STREET’s estimate for December (historical data via YCharts).

Prices of new houses versus existing houses.

Over the past four decades, the median contract price (six-month average) of new houses exceeded the median price of existing houses nearly all of the time, with new houses being usually 10% to 30% more expensive than existing houses. This scenario has now changed.

And remember, for new houses, the Census Bureau collects contract prices which do not include the incentives and costs of mortgage rate buydowns.

But with mortgage-rate buydowns and other incentives included, the monthly payments of new houses are now out-competing monthly payments of existing houses, which explains why homebuilders’ sales have held up reasonably well, while sales of existing homes have plunged, as some buyers shifted from existing homes to new homes.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What does this information portend for the widely discussed housing shortage across the US?

“Housing shortage” is a BS propaganda term used by the RE industry and its trolls to drive prices higher. There is no housing shortage. There is no shortage of homes on the market for sale. But prices are too high – that’s the problem, and so demand plunged, and lower prices will fix that problem.

So ignoring for now the huge new supply of multifamily (condos and rentals) coming on the market or already on the market…

Here is the supply of existing homes (red line for 2024). Over the past 8 years, only Nov 2018 had a slightly higher supply. That is plenty of supply. There is no shortage:

https://wolfstreet.com/2024/12/19/home-sellers-home-buyers-and-brokers-getting-used-to-the-new-normal-old-normal-6-7-mortgages/

I guess that squashes the CRE conversion idea. Plenty of houses out there.

Conversions take many years, and they will create new housing supply, and new supply is always good in bringing down prices and rents. Particularly, this new supply will be in central business districts, which is great because central business districts are dead at night, and this will put some much-needed life into them.

Realistically speaking, only a small number of office towers can be converted to housing.

But malls are easy to “convert” because they’re easy to bulldoze and have so much parking space. Stonestown Mall in San Francisco is being redeveloped into 3,000 housing units and a walkable main-street type of shopping and restaurant area, with a multiplex and big supermarket (in the old Macy’s department store). This stuff is exciting, but it’s so slow-moving.

The impracticality of CRE conversions is what kills the CRE conversion idea. It is an extremely naive idea that some people seem to refuse to let go of

Same thing here with the basically-dead Sunrise Mall near Sacramento. The city plans to demolish and redevlope it into a walkable mixed use thing once they can find a developer who wants to do it. Still waiting for one though.

When will prices actually fall to affordable levels? I’ve been thinking about this…if new homes are too expensive to construct to make a real profit, that means that homebuilders need to build them for cheaper. To build them cheaper that means they need to pay less for their raw materials or pay less for their labor.

If they pay less for their labor, I think employees may balk and they won’t be able to hire enough workers to build homes. If they can’t build homes at a profit, they will go out of business.

If enough new home builders go out of business, that means there is less supply on the market. Less supply leads to higher prices. But the prices are already too high for middle class workers. This is where I get stuck. What happens at this point?

There are many ways of reducing the costs of building a house, including by shrinking the builder’s profit margin. And that’s precisely what they’re doing right now, just not enough of it.

They are still making like 20% margins. Automakers can live just fine on 5-6% margins and grocery stores on 1-2%. So I’m thinking they can get squeezed a bit more and still do alright. They’ve just been taking advantage of their pricing power that customers (home price) & workers (labor) have allotted them

When push comes to shove for the big homebuilders, they can stop buying smaller homebuilders, they can stop share buybacks, they can stop paying dividends, they can stop paying executive bonuses… they have all sorts of ways of trimming their own fat.

There is another way to make homes more affordable: Make them smaller.

They’ve been doing that too.

DeuceSevenoff,

I think they call it “tiny McMansion” now, or mini-hacienda. As long as it has a stable to park the horse.

On a 400k house their margin was 100k.

Thanks to zirp and fed mbs they cranked up prices to nosebleed levels and made an absolute killing on a commodity. Fun while it lasted. It’s over now.

House prices stay high. In a strong labor market, you can’t pay tour people less. Supplies, well they may get bulk discounts, but costs are costs.

The question is, what are the profit margins? Can they cut off some of the profit and still be profitable? I believe so. Will they, who knows?

A major part of the ridiculous price increases are materials that were jacked up during Covid, and have not come down. Windows, for example, had a 100 percent price increase from Anderson and Pella. My distributor said they literally doubled their pricing simply because they could, and have not *yet* had to lower them–still enjoying the fat increases. Other materials have experienced the same. As builder inventory continues to build and they slow down construction, material prices have to come down. Another example, a 1000 gallon propane tank pre Covid was $3000, they are now $6,000. I don’t believe the price of steel doubled. It seems the only product that has followed market dynamics is lumber, which quadrupled, but is now closer to where it was in 2019, last time I checked. All this is near and dear to me because I am completing my house I started in 2022, and everything, starting with concrete, was jacked up to ridiculous levels. Two-three years ago you were lucky to even be able to order concrete. I think those prices have been coming down, but are still way too high. They will follow everything else when things truly start sliding. And the subs who wouldn’t return calls the past 3-4 years will be begging for new jobs.

Oh they can operate at smaller margins and they will. Same company operated at 5.8% in 2006 and -30% in 2007. So you can do the math and where that put the current 400k home pricewise. And that’s assuming they don’t shift how they operate or slash costs simultaneously. If you cut out their profits suddenly the new home only costs 320k. And if they take a loss, well….

I’ve seen some exciting stuff with 3D house printing that should be able to lower costs. Manufactured homes are also cheaper.

Really though, I think the big answer is to get developers to make smaller homes. They build these huge 3000sf+ homes to pad their margins when what we really need is starter homes in the 1000-1500sf range.

we sold 2 homes this summer – thankfully got market

today there is FLOOD of listings at prices 20% lower

issue is they still need 25% price cut from here

just closed on NEW HELOC for more fresh cash when time is right

IMT cash flowing income and putting into savings as fast as can

need couple more units for retirement income

as late boomer – never got PENSION and those 201k plans are for suckers

self employed and using the WARRENS plan

and glad I did

Is it available houses for sale or available houses for a sale at a certain price point? I’ve noticed that inventory is up in the area I live but still significantly higher than I want to pay.

I was a remodel contractor most of my life…framed and built several customs when I was young…shocked at prices for material . Many things twice there cost from ten years ago…bottom line fewer houses will be built..land prices and have to come down..

Government needs to sell BLM land and or select property on fringe of military base such as Camp Penalton near Oceanside California…just north of the harbor there…5 miles of beachfront property a third to a half mile deep… REIT will need to be limited in there Residencial holding…or be outlawed completlt 22% of sales during the pandemic went to REIT.like Blackstone…or it that Blackrock?

Musk and Ramaswamie can do a firehouse sale of potential properties..We must remember this is a land of We the People..as far as the illegals…the good ones…round them up and make them avaible as skilled,or unskilled labors…much like FDR did in the depression….

“bottom line fewer houses will be built..”

That’s just not the case. It’s just propaganda. Look at reality. They’re building more houses than there is demand for. 2024 was the third highest in new house sales since 2007, and inventory for sale still ballooned.

Do you have a geographic breakdown of unsold inventory for sale of completed new houses? If it’s concentrated in a handful of markets I would think it would be hard to make generalized conclusions from this data. I live in upstate NY where the national homebuilders are not as active and we haven’t seen the glut of new supply.

Marcus,

Yes, as you can see here, that’s always the case, there is never a glut of new supply in “my area.” Every housing article brings out those not-in-my-area comments. Never fails.

There are 29,000 new single-family houses for sale in the Northeast (from NJ and PA on up) in November.

obviously, in big dense cities, what gets built is multifamily, often replacing single-family. That’s the reality of the past few decades. New single-family development takes place further out. So if you live in Manhattan, you will never see any single-family construction, though they’re plenty of towers being built. That’s just reality. People who live in Manhattan choose to pay a huge premium to live there, and they choose to live in larger buildings, and they often pay millions and sometimes tens of millions for a condo or co-op.

But overall, even in the Northeast with its big dense cities, there is still 29,000 new single-family houses for sale, just not in urban cores.

You ramble like you sniffed too much lead paint back in the day

I don’t even understand half of the point you’re trying to drive home, I’m not so sure you do either

Lead paint is only dangerous if it’s eaten. Sniffing it has no effect.

That having been said, you do sorta have a solid observation.

But do you? What is the best size particle to snort?

“Housing shortage” is also a BS propaganda term used by developers and their YIMBY Millennial/GenZ trolls to push pro-developer policies through local/state governments while rent algorithms keep rental units off the market and prices high.

RealPage’s corporate motto: ‘Collusion is just an Illusion!’

Wolf’s explanation sounds more plausible. Sellers of anything would always want to show/cause scarcity to get people to buy stuff at a higher price. Basically, most news from RE people is fake news. Inverse it.

The charts tell a different story if you go back further. The furthest back Redfin goes is 2012, but they showed 10 months supply of existing homes back then. It’s still relatively low now at 3 months, even after a year suppressed by interest rates.

You are definitely correct that new builds are the best buy out there today with all the incentives. Existing home prices have inflated about 4-5% this year, right with the historic average of 3.5%, and are projected to go up at about average rates again next year.

Houses don’t cost too much and there is no housing shortage. There is excessive amount of capital looking for things to do (build, buy and rent) and an insufficient amount of wages to purchase basic needs.

There is absolutely a scarcity of existing homes. Philadelphia area

This is direct result of SFH homes being scarfed up by investors seeking yield.

Increased taxes on investment property would help alleviate, adding to inventory and cutting prices

The biggest single-family investors have become net sellers of houses. Just listen to their earnings calls. They cannot make those prices work with the rents they’re getting. Instead, their building their own build-to-rent developments, where hundreds of nice rental houses are in one development, with a central leasing and maintenance office, common amenities, etc. They’re super-popular with the renters of choice that have above median incomes and could buy, but don’t want to.

You are 100% right. My city’s market was hit hard by the Too Big to Fail institutional investors buying up 30%-40% of inventory between 21′ and 23′. We have never had a shortage, but the price of the 3br/2ba ballooned out of reach for the middle class natives. Somehow prices stay high while the average posting to close is starting to stretch past the 6 month-1 year range at this point (along with multiple price cuts before a contract). We are actually reaching a glut of supply, but it doesn’t matter when everyone wants $220k+ for a 3br house in a market with a median income around $45k/yr.

Well, it’s a bit like the labor shortage we hear about as well.

For labor, there’s a shortage of potential employees interested in the work available at the wages offered.

For houses, there’s a shortage of buyers interested in the properties available at the prices offered.

It’s a conundrum, a mystery, an enigma as to what the employer or seller should do (maybe free coffee at work or better cookies at the open house)? /s

Amazingly the peak to trough on new units chart…but we are an empire of bubbles, bubble economics, bubble reality, bubble fake scripted sports, another president who was an actor with a scripted career from birth…the elites same old scripted empire…MC.

The employer and seller should tell Congress to stop destructive policies like deficit spending and never again do QE. Let the economy grow organically, not through bad stimulus and that will give businesses the best chance at stability and longevity.

The height of the housing bubble had 199,000 units compared to the current 124,000 units. Bankrate reports the average FHA rate of 6.4% in 2006 & 2007 compared to current FHA average rates in the high 6s & low 7s, but, most builders are paying for rate buydowns with fixed FHA rates ranging from 3.99% – 5.99% and still covering some of the closing costs. The population is larger now vs 2008 and January is the beginning of the buying season and it runs through July. This “glut” of homes (75,000 short of the 2008 levels) will disappear by Feb. A lot are being gobbled up now. The analytical data is about 60 days behind. Get ready to see reports of “Inventory Homes cleared out in December 2024” around Feb 2025. It takes on average 4 months to builders to build a home, so get ready to see an increase in permits for Jan & Feb vs the last few months. There is a lot to unpack when it comes to housing, but it’s doubtful there will be a large price decrease due to the inflation we just went through (yes lumber is down, but everything else is up) and easy access to no cost 3.99% – 5.99% rates when buying new.

LOL, RTGDFA, that’s not what the big homebuilders are saying. You should listen to their earnings calls and earnings warnings and slashed guidance for the coming quarters. I told you Lennar’s outlook in this article. Why didn’t you read it? You didn’t want to pop your bubble? Obviously, you didn’t make it past the first word of the headline – “glut” was a troll trigger. Works every time.

Eggnog and rum for breakfast, huh?

You are out of your mind. Your own post contradicts itself.

Well, it’s a bit like the labor shortage we hear about as well.

I don’t think there’s a problem with housing prices being high. If 65% of Americans own their homes, I’m sure they like these high prices. Or the 35% that left, many of them prefer to rent….no problem detected on that front.

As for the home builders, they’re still doing fine, selling and building, making money…laying people off isn’t a thing yet.

So the problem lies with the poor people who don’t have any money, the usual crowd.

Homeowners only like high prices if they can liquidate their home and fetch those prices. It benefits them and makes them feel rich. If they list their home at that price, and it never sells, they don’t win. So it’s meaningless. The only beneficiaries here of high prices are those locked into low rates. Everyone else is struggling with affordability, and high home prices also effect rent affordability. So if you’re cool with the situation, it’s probably only because you’ve paid off your home or have a low rate locked in. Otherwise, there’s an important factor that you’re leaving out here and it’s known as opportunity, sometimes referred to as the American dream. Most people would like opportunity to return for the average person. It’s more than just poor people who are uncomfortable with the current situation, it’s also the intelligent.

I think you’re overlooking the wealth effect and HELOCs.

Don’t forget higher property taxes and higher homeowners insurance. People really only benefit from the higher prices if they can sell without having to buy another equivalent at the same inflated prices.

And HELOC’s are debt, not income.

Exactly, fellow MM-er.

Higher prices = higher prop taxes. If I’m not looking to sell, higher prices *literally* cost me more money.

while our market has come down around 10%

it still needs another big correction of 25%

all wage increases went to buying food, utilities, taxes(make more pay more)

so in end mortgage payment needs to stay same as pre-covid $1,200 month

Agreed: ” Most people would like opportunity to return for the average person. It’s more than just poor people who are uncomfortable with the current situation…”

-I question what the actual profit margin new- home builders make after all costs and taxes. I thought it is well less than 20%, more like 9%. And risky variables, high rate of employee injuries in construction.

Maybe this democracy is failing the majority.

The middle class income is not middle anymore, and it’s shrinking. Middle and lower classes get a third of their pay taken in taxes and healthcare, in the most convoluted tax system ever created.

Also, I saw the biggest REIT’s pop up for sale signs on many existing single family homes in my small town about the time of COVID or just before. That’s a problem for availability and affordability on existing homes.

“I don’t think there’s a problem with housing prices being high.”

LOL. RTGDFA. But yes, homeowners like higher prices and for prices to go higher, and they like feeing richer every day when they look on Zillow, and they may be disappointed. They’re already disappointed in a bunch of cities but are still gloating in others.

This homeowner does not feel richer.

Property taxes, home owners insurance, are double digit increases

again for 2025.

bingo WOLF forgot that part

2024 brought 38% increase in insurance, 10-30% increase in property taxes

and repairs – $800 for water heater + installation

just did few repairs on home – lost 1 months rent and paid 1 1/2 months rent to do few repairs/upgrades

$3k

have new tenant which will likely stay the 3 years last one did

just lot $$$ upfront today

I am a home owner and having higher prices does not materially increases my quality of life in anyway

On the other hand.. property tax increases in general along with property insurance increase is a constant headache

I want homes to be affordable again

This homeowner also does /not/ like higher prices, and is in fact appeling his city’s recent re-assessment because there’s no way the damn house is worth that much!

So .. you all want your houses to be worth half as much…I don’t believe that….not one of you would volunteer for that…you just don’t like the higher cost of ins and taxes…. IMO

If people were more resilient and bold, they could take advantage of this rare opportunity, sell the precious house and get out of dodge, pocket the money and free yourself from your crusty neighbors and worn lifestyle.

Ok then, how about a game of pinochle. Love that game.

I would love to see my home value get cut in half. Because that would mean the bubble popped, opportunity once again exists for everyone else, and it changes nothing for me (I still will reside in the same exact box). It only changes my ‘net worth’. Boo fricken hoo.

I’m voting with ”Blake” on this issue!

NOT selling, property taxes NOT going up due to reasonable and rational ”cap” for homesteaded AND elderly, etc.

And while our next generation is benefitting from being able to inherit SOME of that, WAAAYYY too many of that gen is NOT,,,

Housing needs to drop AT LEAST 50% once again,,, sooner rather than later.

Trump could make his ”legacy” about reasonably priced housing ownable by EVERY ONE willing to work for it…

WE, in this case WE the Peedons who love USA and want it to continue, can and should Pray for him to do so.

@Home Toad – yes, I could care less what the market price of my primary residence is.

If the number goes up or down it doesn’t matter.

If it was sold I’d pay transaction cost and would be able to get something similar. High or low number makes no difference until you consider insurance and property taxes. My insurance has more than doubled in the last 4 years. Property taxes have gone up 40% over the same period. It sucks.

I bought this house to live in and to die in. I don’t care what anyone else thinks it’s worth.

If We sell for less than appraised Tax & Insurance Should be Forced To Replace our Loss Back To Us.

Many of us renters are forced to rent due to the cost of purchasing being so astronomically higher.

At risk of repeating what others are saying, I own my own home but do NOT like higher prices. I don’t go on Zillow every day, look up my house, and think, “wow, it’s doubled, I’m rich.” Instead, I get my property tax statement and my insurance bill and feel decidedly less rich. High prices impose COSTS on homeowners. This bears repeating: higher prices impose COSTS.

The only homeowners who benefit from high prices are people who sell an expensive house in one area and buy a much nicer house in a lower cost area.

Local governments, collecting those property taxes, also benefit. “Look at us,” they say, “we’re providing all these services and have not raised tax rates” (though nobody who pays taxes is actually fooled by this).

Locally the crap areas with run down houses are starting to break in price. No more does a tear down home 2 hrs from civilization demand nose bleed prices. There is no shortage of overpriced homes still. Cracks in the foundation maybe.

Time will tell. I’ve seen 2-3 houses in the past month or two I don’t immediately scoff at. But they are in low desirability areas and in bad shape. But the prices are at least starting to reflect that. Anything in a decent area is still way over priced for local wages.

I’ve been studying the market in the Dallas area for years now and starting to see softening, and seeing more and more back on the market listings and they are setting on redfin a lot longer.

I think we’re going to have a repeat of 2008-2010

One can hope

to much 1% cash out there

2008-2010 involved a full-on run on the banking system triggering the Great Recession and housing price collapse. We’re missing that ingredient for the moment at least.

I expect that ingredient to be a loss of confidence and pulling back on spending and purchases due partly to a stock market decline in 2025 that eventually becomes a new bear market for a longer period of time than we’ve come to expect in recent years, with all the attendant issues that can cause.

Yes but home prices are still going down over time albeit slowly

@Canazei Yeah that’s one of the obvious scenarios that even the MSM has occasionally been talking about.

I think the other one would be an insurance crisis. The increasing rate of natural disasters multiplied by increasing replacement cost is creating a huge amount of “negative value” in the system that everyone has an incentive to ignore until they can’t anymore – and then it becomes a case of trying to be the first one out the door. The new administration is going to do everything they can to worsen both of those problems because they too are in denial about it.

I can’t remember the source exactly, but there has been some recent modelling which says that if we don’t do anything about this situation the end result is likely to be a wave of municipal bankrucies as local governments are forced to absorb these losses without sufficient reimbursement. Even if your house survives that isn’t great for property values.

MW: 10-year Treasury yield ends at 7-month high to kick off holiday-shortened week

The yield on the 10-yr has not finished going higher. Let’s not forget that yield and price are inversely related, in other words bonds are in a nasty bear market after a prolonged bull market. Best guess, the 10-yr UST will hit 5.5% and perhaps higher before this is over. This does not include the possibility of Trump making matters much worse with his brash and unsophisticated approach to governing.

I heard banker selling CD to younger guy with couple $$ in IRA

pushing him into 5 year CD to get ‘higher’ rate

said they see rate cuts in 2025

—

fed can cut but when 10 year keeps going higher – oops

Lots of government debt piling up in short end of bond market where interest rates the lowest, but this is debt needs to constantly be refinanced. This is like a giant snow ball rolling forward in the US bond market because it is constantly being added to as we borrow more money. Low interest rates are a pipe dream. Interest Rates look a lot higher to me

What happens to US home prices if we see 8-10 percent again! Perhaps both housing prices and inflation will come down and we will have , heaven forbid, a depression.

@Andrew Prppr..

We thought the same when fed hiked the rates from 0 percent to 4.75 percent in historically fastest way

Nothing broke ..

We may get a recession which is part of normal business cycle

Wall Street cry babies have been scared mongering that higher rates are disastrous but nothing of that sort happened in last 2 years

MW: Stock market will find it hard to rally unless the dollar and bonds calm down

I purchased a house recently. I had the option of choosing a new build and and older 2000s house. My agent was an old friend so we were able to speak candidly about much of the process.

I will say that I opted for the older house based on what I saw in the new builds. The construction is quite simply shoddy. In one of the built homes we toured, I was able to lift the granite countertop of it’s platform with one hand. Doors were not level and floors creaked across the entire upper portion of the home.

I am not saying that the Housing Bubble 1 era homes are much better, but the craftsmanship of the new home was just atrocious.

I was going to ask about hedonic adjustments.

Here in South West Florida, new construction — shoddier or not — is subject to newer storm-related building codes. Is there an adjustment in stats (one way or the other) designed to neutralize the changing nature of the product? The decision between new-build and pre-existing home is muddy.

Thanks to anyone who has insights.

The two key expenses in Florida is the ground floor has to be concrete block construction if within a certain distance from the ocean or a river, all roofs have to have the rafters attached to the frame (or block) in a way that it won’t detach in high winds, and all roofs have to have some type of plastic sheeting between the roof and shingles so that if the shingles blow off, the water won’t penetrate the house (as much). These things will add thousands to the price of a new build, and a roof replacement, but in the context of the overall price of a home, it’s not that much. $10,000 is a big deal on a $60,000 house, not so much on a $350,000 house. As for shoddy construction, I’ve lived in Florida for 60 years, and it’s always been shoddy. You’re paying for 70 degrees in January and the beach, not quality construction.

I was down in Florida right after Andrew. I toured the devastation. It looked like a neutron bomb went off. Every home was gone. Driveways ended at empty lots. All the roof s blew off, because they were not secured to the house with metal braces. and the homes followed suit. Went back again 10 years later. Saw the same shoddy construction at a relative’s new home. Every door wouldn’t close, every cabinet was crooked, Windows same. How could any educated person buy such a piece of s$hit.

No, there is no “adjustment in stats” (prices) for changes in building codes, storm or seismic improvements, build quality, etc. It is what it is.

My wife and I are looking home in SW FL, either buying here or somewhere back north (or halfback). But family is here, so probably here.

For the life of me, I can’t decide if it’s wiser to buy DR Horton crap with impact windows and a rate buydown OR buy something older (but post 1995) that might be built better – albeit at an overinflated price with higher interest rates.

There are some crazy stories about DR Horton builds… do some googling before making an investment.

Where I live in SoCal, SFR prices have basically doubled over the 5 to 6 years. As far as I concerned prices need to drop by close to half to make sense for most buyers. One of the huge problems in the local market is the number of short term rentals and corporate owned homes. In some neighborhoods, short term rentals account for 25% of SFRs, and the percentage would be higher if not for city zoning.

DM: Veteran hedge fund boss reveals America’s fatal flaw ‘that will lead to a crash next year’… and why parabolic prices are a red alert

A market expert has warned that America’s ‘fatal flaw’ could lead to a market crash in 2025. America’s ‘addiction to government debt’ is its fatal flaw – and could lead to a stock market crash, an expert has warned.

Ruchir Sharma, who is an author and fund manager, said attempts to rein in the debt – now at a record $36 billion – will eventually weaken economic growth.

Sharma, who is chairman of Rockefeller International and worked at Morgan Stanley for 25 years, made the comments in a column for the Financial Times.

36 billion is a drop in the bucket.

He obviously meant 36 Trillion.

Yep, $36 trillion.

Did you mean to say 36 trillion?

My

I don’t know his reasons, but have read that apparently Warren Buffett has a larger than normal proportion of his portfolio in cash lately. Things may be getting frothy in equities.

“Things may be getting frothy in equities.”

Um… yes. Yes, it’s frothy.

Based on just about any longstanding stock valuation metric, we’re in the midst of the 1st or 2nd bubbliest US equity market ever. (Potentially 2nd behind only 1999.)

– Buffett Indicator (1st)

– Shiller PE Ratio (2nd)

– Trailing Price-to-Sales Ratio (1st)

– Equity risk premium (2nd)

– Among others…

We’ve blown WAY past 1895. WAY past 1929. WAY past the Go-Go 1960s. For some metrics — we’ve even blown past 1999.

And no, it’s not the Mag 7 skewing everything. Across the US equity spectrum, valuations are at or near all-time highs. Mag 7 gets the attention because their valuations are particularly extreme. As just one of many many many examples: Sherwin-Williams — a 158 year old PAINT MANUFACTURER — has a 35 PE.

Why is Buffett overwhelmingly cash?

“Be fearful when others are greedy, and be greedy only when others are fearful.”

But, but, just think of the new paint colors AI can think up for Sherwin Williams!

There are companies that are at historically low valuations currently (low p/e’s etc) even though the market is hyperventilating.

The problem: if you look at S & P charts, by industries, charts of 50 yrs.+, you’ll see that almost every industry gets kicked in the arse when there’s a big market decline. Just a few industries, e.g. tobacco, alcohol, education, get by with very small declines.

Oooh.

A fund manager AND an author? I actually like Sharma as a comtrarian thinker, but he’s exactly that. Wouldn’t you know it, his fund encourages ex-US investment.

Similar to auto mfg. Prices went straight up and now inventory sits. Nothing that lower prices won’t fix.

Lower prices might fix one thing but break something else. I was messing with some old plumbing and next thing I knew everything was leaking.

But lower prices seem to be a step backwards, a bit depressing actually.

But for the sake of affordability, I wish Santa will lower prices for homes and cars.

Merry Christmas!

Ticking time bomb. So many facets of the housing market have already crashed. Only matter of time before prices become un-stuck in the stratosphere.

Interesting to read. Falling house prices could be one of the negative factors for the market sentiment in 2025.

We had near all time record valuations in the market in December 2024. I am curious if we will see some selling in January for tax reasons.

Merry Christmas!

I live in the extreme Northeast, so big builders are not a thing here, something that just exists in theory to me.

Our good land up here around our cities was taken long time ago. Granted there is a lot of wide open space on the map in other parts of the country, but people buying these new homes need to be near cities that people want to be in, and by all appearances these are large tracts of housing at the fringes of already sprawling urban areas. Could the fact that old home prices are not pushing down in line with new home prices also mean that there’s some kind of lower desirability of new home locations? That builders are just pumping these things out but there’s some diminishing returns in location quality?

Just asking a question and hope that somebody that lives in one of these areas can expand on that. Again, I have no specific knowledge of this situation. Very happy to live in a rural area far away from this garbage construction.

If you look on google maps at suburbs of any flyover city, you’ll see entire new neighborhoods being built. This is what the big builders are building – not single properties scattered across existing neighborhoods.

But up here in New England, we don’t have that kind of space. Everything is already built out, or protected forest or other conservation land. Sure you could easily build a new neighborhood in the middle of nowhere Maine, but where are you going to find buyers for them? Rural parts of ME / NH / VT aren’t exactly high-income.

Unfortunately, areas like this just aren’t seeing the same downward pressure on existing home prices – at least not yet.

Just change some laws and free up more land to build homes

The solution is simple

Even San Diego is seeing price decline though slow

Socal is epitome of no land per real estate agents..

Earlier this year I toured homes being constructed in southwest Dallas, about a 30-min drive to downtown with no traffic. Close to 1+ hours with traffic. It did not have the northeast feel whatsoever. I would’ve preferred to live closer to the city, but the existing home prices were more than a new home.

There were some additional benefits of the locations of the neighborhoods I toured. Not in a 5-mile radius of a landfill, not in a flood plain (actually a couple were the top elevation of local topography, so they never would flood), and at the fringes of the metro area—such that a 5 mile drive south would bring one to cattle ranch after cattle ranch. Quiet. Great for what I thought would be raising kids. Things didn’t pan out with the lady, for the better ultimately.

There was high desirability in those neighborhoods. People touring left and right back in March 2024. Sales closed left and right too. Great deals relative to existing homes.

The value proposition of DFW vs elsewhere is totally different. That’s what most people miss. If you compare dollars, then you’re misguided. $1 in one location is totally different than the same $1 elsewhere. What is needed is equal value dollars, which is impossible to decide because everyone values different attributes differently.

In central Nj there is zero new construction in about 4-5 years now.Those that I have seen are for 55+ or smaller 5-10 houses in a stretch/plot of land which are gone before you hear about them.

In the Ny tri state + philly surroundings new SFH construction is not happening for the last 4 years

Yes, as you can see here, that’s always the case, there is never a glut of new supply in “my area.” Every housing article brings out those not-in-my-area comments. Never fails.

There are 29,000 new single-family houses for sale in the Northeast (from NJ and PA on up) in November.

obviously, in big dense cities, what gets built is multifamily, often replacing single-family. That’s the reality of the past few decades. New single-family development takes place further out. So if you live in Manhattan, you will never see any single-family construction, though they’re plenty of towers being built. That’s just reality. People who live in Manhattan choose to pay a huge premium to live there, and they choose to live in larger buildings, and they often pay millions and sometimes tens of millions for a condo or co-op.

But overall, even in the Northeast with its big dense cities, there is still 29,000 new single-family houses for sale, just not in urban cores:

I truly commend your effort and patience to reply to these ‘not in my neighborhood ‘

People live in their own echo chamber

Happy holidays and merry Christmas to all

Chetan,

I lived in Central Jersey during high school, college, and 10 years after college. Watched the build up to Housing Bubble 1, watched Bubble 1 Pop, bought a short sale, and sold short sale back in 2021. Growing up, we watched farm land get turned into single family developments by Centex Homes, DR Horton, and others.

One 2 minute search and I found lots of communities being built by DR Horton in NJ. These are not communities with 3,000 homes like you would see in other places in the country. Space is at a premium in NJ, and there are 600+ towns all with their own codes and regulations.

The homes are there. What you may not like is the location, build quality, and/or price.

Plumbers faced with a backed up toilet first address the clogged pipe, to get the “stuff” moving again, cleaning up the bathroom is last.

Builders and maybe even auto manufacturers might take a lesson from plumbers. Unclog the pipe and then don’t do what caused the clog in the first place.

I know, this is dumb, but it somehow seems to fit in a sense.

Happy and Safe Holidays to all!

Sorry, this reply of mine above was meant to be to Kent’s post above regarding the “missing ingredient”. Somehow I messed it up on my phone browser when I used a back button and it appears I replied to the wrong comment here.

WSJ: Insurance and Taxes Now Cost More Than Mortgages for Many Homeowners

Ballooning expenses rewrite the math of homeownership

Soaring costs for home insurance and property taxes are busting homeowners’ budgets.

Insurers have pushed big rate increases because of losses from natural disasters and rising costs to repair homes. Surging home values in recent years, meanwhile, have lifted property taxes for many homeowners.

These ballooning expenses are rewriting the math of homeownership. In September, 32% of the average single-family mortgage payment went to property taxes and home insurance, the highest rate ever for data going back to 2014, according to Intercontinental Exchange.

Nationwide, taxes and insurance make up more than half of the monthly mortgage payment for 9% of single-family mortgages. That is up from less than 4% at the end of 2014.

Rising taxes and insurance premiums intensify the lack of affordability home buyers already face because of record-high home prices and elevated mortgage rates. Those deterrents have led many home shoppers to give up this year, putting sales of existing homes on pace for their worst year since 1995.

I’ve seen some of the new developments Lennar is building. They’re tiny, packed in cheek to cheek, and on basically no lot.

What are you complaining about???? First you complain that you cannot afford a house because it’s too expensive; and when someone builds a house that you could afford, you complain that it’s too small, that the lot is too small, yada-yada-yada. This whining sense of entitlement really gets old. What you want is a beautiful mansion in an expensive area of an expensive city without commute, and it has to be cheap. OK, keep wanting it.

Same here. Seen some of the homes Lennar is building in San Diego…..packed in communities like sardines right next to a freeway. Not cheap either. Move in ready for 1.2mil dollars; 1900sq feet. Sure putting a dent in those San Diego home prices bwahahaha.

That home here in south Texas would be $250 K.

Yes. But you can’t drive for a peaceful hike in the Sierra (or if you don’t want to go that far Gorgonio or San Jacinto) or drive twenty minutes to the coast to go surf, dive and catch lobster, or whatever else you want to do. To each their own.

Why?

And adding to the already biblical traffic. So glad I left years ago

I am in San Diego own a house with decent size front and back yard

If I can I’d move into a house with little yard

Big yard big lot looks good on paper but the maintenance is too much 😑

This is what young people want. A large lot just increases property taxes and landscaping maintenance costs. No one wants to hang out in the yard. They could care less how close they are together–none of them have kids anyway so noise not as issue. Density just means feasibility of convenient services like food delivery.

Lot of boomer mindsets on this thread.

So with selling prices higher than marginal cost to produce, production rises, thereby squeezing prices until marginal revenue equals marginal cost for the marginal home builder. Econ 101.

So many home owners complain that higher home prices mean higher insurance rates and higher property taxes. Fair point. But how much of this increase can you guys offset by tax breaks ? Also, if you got a 3% or less mortgage rate, then is your mortgage + tax + insurance – tax breaks LESS THAN mortgages at 5% or more ? If yes, then you are not so bad off compared to others.

PS – If you take tax breaks on your home payments, then you are really taking govt hand outs i.e. you are not really the capitalist that you think you are. You are just another govt dependent. The tax breaks you get have to be made up elsewhere either by higher taxes on someone else or by issuing more debt i.e. inflation.

Your “PS” is “BS”!

What do you mean “BS?”

Of course tax breaks for homeowners and landlords shift tax burden onto other taxpayers.

Specifically — they shift the burden onto future generations (with interest) via the federal deficit.

In other words, it’s a federal government handout — a transfer from future generations to current homeowners / landlords.

“But how much of this increase can you guys offset by tax breaks ?”

None. Your comment is complete nonsense.

A few points.

Yes, rising insurance and taxes impact homeowners, at least they do right away. However, as soon as possible, depending on local rent price restrictions, tenants will foot the rising bill in their monthly rent payment. Eventually. I just walked by our rental, which we price very very low, and thought I might have to pass on an increase this coming spring depending on our property tax assessment. In cities large landlords also play with parking fees, above and beyond the housing costs. Absconding with a damage deposit is common as most tenants cannot do the fight to get it returned.

I have been building on and off for most of my working life. I get a decent break on price from one lumber supplier but nothing like the big contractors get. In fact, major players have their own captive suppliers and even do their own trucking to save on costs. This reduction is never passed on to purchasers, instead goes to pad the profits.

And last there are the specialty crews. A large company has their own sub-trade divisions and they move them around from project to project. Often, living away expenses are borne by the crew (workers) themselves.

Houses are far too expensive for many reasons. In addition I blame agents and the selling process for a lot of this. Sure, it’s a market economy, but I know kids who got into an RE agent career in their early twenties and think 6 figure incomes are normal. Many know absolutely NOTHING about construction or building quality and the buyer pays for it all in the price.

When I bought my first home 45 years ago I paid 2X my yearly salary for the privilege. My down payment was an affordable 15% which was easily saved on my very modest income. The same house today would cost me at least 10X of what an adjusted for inflation salary is for the same job. We all could buy houses back then. Yes, many many things have changed to increase sale prices, but I do know for certain my wages never increased 10X adjusted. Maybe…..maybe 3X, but definitely not 10X. Inflation clouds everything, and the increasing zeros on money cows expectations. People need to lower their expectations on housing, no doubt. Granite counter tops? Really? Start with something affordable, even a shit box and fix it up….then pay it off asap. Make it your home, an affordable home. Start small and modest and live within your means, especially with housing our biggest single living expense.

Hopefully, housing will become sane and affordable. once again

If there are so many homes, how come there are so many more advertisements on TV saying they’d buy any home?

scam?

Yes .. i called up one of these guys for fun and they told me they can write me a check tomorrow and I was delighted

But the problem was.. they would write you a check 30 percent the market price

All real estate is local. I think there’s a housing shortage in some of America’s most prosperous cities like NYC, LA, and Wolf’s backyard of the bay area. Because local governments make it illiegal to build new housing artificially. Combine government mandates scarcity with fancy tech jobs that pay average workers what CEOs make in some countries and you have skyrocketing prices of even decrepit homes that would get bulldozed anywhere else in the USA.

But all real estate is local. And clearly in the states where housing is legal, like Texas and Florida, builders are matching housing supply with demand. In those localities, everyone is just being too greedy to match their sales price with what the buyer can actually afford in a 7% mortgage environment.

I agree but WR backyard, city of SF has seen big drop in prices. This would not be true if the inventory is super low and buyers are rushing to buy in.

I hear two things refuting WR price drop articles.. not in my neighborhood and real estate is local. WR does a better job of explaining these myths away.

Alpha Poodle

“I think there’s a housing shortage in some of America’s most prosperous cities like NYC, LA, and Wolf’s backyard of the bay area.”

🤣 Here in the city of San Francisco, we’ve got housing coming out of our ears, and they’re still ADDING a few thousand new housing units every year, and the population has dropped, and prices have dropped to levels first seen in February 2018, that was nearly six years ago. Why do people keep spreading stupid “housing shortage” BS? This data is out there, it’s not a secret.

There’s plenty of housing. The problem is that prices have been manipulated up to levels that are not sustainable, and now they’re not sustainable:

And here is the San Francisco Metropolitan Statistical Area:

There is no shortage of housing. This has been disproven again and again. Whether it’s the supply argument or the demand argument, neither holds water. Why do people keep peddling this? I’m not sure.

Here in Texas prices have dropped. I have zero skin in the game, I’m an outsider. Locals will not buy. Outsider see an arbitrage opportunity. I sit in what some call “mortgage jail” with a 2.75% mortgage. Others cry. To each their own.

Let’s not forget that by 2029…just four years away…the entire baby boomer population will be ages 65 to 83…20% of the population.

Average life expectancy is 77. Point is, many boomers will die, live with children, or go into senior care/nursing homes, forcing home inventory higher. Throw in deportations and less immigration and it’s a lot of existing home inventory to come on the market. Also consider that generally speaking, more than one person in gen X and millennial (married, cohabiting, possibly with children) buy homes…but as a couple ages, it’s usually one person selling (i.e. the surving spouse/partner). That spells big inventory of existing homes hitting the market in the very near future.

The base price for any house is the cost of the land and the cost of permits and fees for the builders. The cost will never go down.

LOL. Illusory. The base price of a house is what a willing and able buyer will pay for it. Here is a recent example:

But the prices are already going down

By the way .. I don’t own two homes and want prices to be down for other people to own and live a decent stable life

Cash is always king. The consumer is very pliable, but there are limits. It seems like the limit has been reached in certain markets. Monthly payment is king to most consumers.

It is really nice that Wolf kept this forum open to the public, instead of a paywall. It reminds me that there are truly, truly stupid people in the world and their lack of self-awareness keeps them where they are, no matter the nice nuggets of advice and thoughts shared. I said this before, there are really wealthy and smart people here and occasionally they share.

Just listen and reflect very carefully. Good luck.

As a hypothetical point of curiosity, I’m wondering what an affordable is — is it a percent of family income or related to savings?

Additionally, the cumulative inflation we’ve all experienced since 2020 really distorts one edge, of the rubber-band, while on the other edge, we’ve seen an explosion in wealth effect from insane equities and the everything bubble,

Affordable housing is confusing, partly because there’s no realistic baseline anymore. Sellers want unrealistic high prices and buyers want unrealistic low prices,

Maybe I’m wrong, but equilibrium isn’t in the horizon — until prices crash.

The classic measure of affordability compares household income to the monthly costs of the mortgage (assuming x% down-payment), insurance, and property taxes.

The Atlanta Fed has a “Home Ownership Affordability Monitor” for the US, and by metro (using local income and costs).

https://www.atlantafed.org/center-for-housing-and-policy/data-and-tools/home-ownership-affordability-monitor

Great resource, thank you for sharing. It seems that starting around 2020, the unaffordability index went up to a similar level to the housing bubble #1

Merry Christmas!

I look at the Fed index for affordability, but seems they’re being extremely generous in their assumptions regarding the reality of costs over the past four years — they seem to be suggesting that there was just a brief period when homes were unaffordable — and during the msft several years, the affordability factor has been a cake walk.

I’m increasing inclined to believe the vast majority of government data is overly subjective and unreliable.

I seriously get a better interpretation of real data by visiting Planet Wolf and your overall balanced insight.

I’m deleting my Fed charts, they’re useless.

Below 100 means it’s unaffordable, not above

19% is still a crazy good margin. On top of it these big builders operate their own mortgage companies that are only interested in packaging then as MBS to be sold on the market. When times get bad like this, they simply start packaging more mortgages to sell. They aren’t going under even in times like this that would put small builders under.

A general rule of capitalism: after the shortage, the glut!

Even diamonds are going down in price after the laboratories pierced the de beers cartel. The Saudis couldn’t wipe out shale oil producers.

Why it’s a bad idea to buy with borrowed money during a run up. Risky. Hopefully wage inflation will fix the used housing market over time but considering our corporate overlords will even engage in illegal behavior to keep wage inflation down, I would not count on it.

Wolf,

We know many locked in low rates, and that is having an impact on inventory and sales (The Fed has said so).

This time is certainly different in that respect, I don’t know if that scenario has occurred before.

Is there any published data showing the current breakdown of mortgages on Existing Homes by rate?

i.e.

X number of Existing Homes have a current mortgage between 2-3%

Y number of Existing Homes have a current mortgage between 3-4%

Z number of Existing Homes have a current mortgage between 4-5%

etc.

I’m a landlord and have been investing in real estate for nearly 30 years. I’ve found there’s 2 rules.

1) in supply constrained environments (Bay Area California and similar), price/rent is what matters.

2) in unconstrained areas (Orlando, and similar), price/income is what matters.

Everything else is noise.

It’s a bit depressing reading the “soak the landlords with taxes” comments here. Y’all really, really don’t get it.

FWIW, here are some realities about buying an older, nominally affordable home in a flyover city, fixing it up, and renting it out.

First, two rules: 1) Don’t lose money. 2) Must have cash flow.

Let’s use the Kansas City MO/KS SMSA as an example. Most of the more affordable properties are on the Missouri side. Not that since 2022 most of the median income folks could afford to buy one of them. A significant majority of folks in KC MO, Independence, and the regional smaller cities rent. We’re looking at 2 and 3 BR homes, most with one bathroom, some with a single car garage, but many without. Most of these homes date back to the 1920s to 1940s. They are wired with copper wire (good), but usually only 100 amps. (Not good. With all the electronics in homes today, a house basically needs to be at 200 amps.) So, right off the bat, a rental owner will be upgrading the electrical system, significantly. Especially as codes have changed. Must have GFCI protected circuits and in some cases, outlets, now. Electrical redo on such a home going to cost between $10K and 20K. Unless the roof is less than 15 years old (way less), you’ll need a new roof. Why? Because no insurer will insure your roof if it is older than 15 years old. (Yeah, even if it is a “30 year roof.”) There goes another $12K-15K. (Note, these are smaller homes, not McMansions. Hence, reroofing costs are more reasonable.) Odds are, the older home has an older HVAC – maybe on its last legs, and almost certainly undersized for the home. You’ll be putting in a new HVAC. $8-10K for a decent system. Is the kitchen a mess? Super dated? Going to need to redo the kitchen. Also, almost certainly you’ll be putting in new appliances. Call that $20K total if you are lucky. Paint it all (primer plus two coats of interior on the walls and one, maybe two coats of ceiling paint). Couple of $K, mostly for labor. Probably need window blinds all around (a few $K). Scope the sewer lines and if you are lucky, you won’t need to jet them. Maybe you are not lucky, though. Call that another $20K. All in now at about $75K to bring that cute 1920s prairie craftsman style home to solid rent-able standards. You know, to compete with the new build stuff. Even if you paid $125,000 for the home, (and yes, you still can find some homes around KC MO for $125K that aren’t in the ‘hood) you are now into it for $200,000. Let’s say you put $100,000 into it. You’ve got a 7.5% fixed rate 30 year mortgage. Why 7.5%? Because this is not your home. It’s a business. You pay business rates, and they are NOT cheaper that a personal home loan. No, siree. Even with reasonable flyover country taxes and insurance, you are paying $1,199 (call it $1,200) a month for PITI. Must have cash flow. Say, $200/month minimum. That does not include any set asides for maintenance and between occupancy repaint and repairs. Call that another $100/month. Your rent is now, because it has to be, $1500 a month. Will your house value out in an appraisal at $200K? Maybe. Maybe not. Maybe you only hit $190,000 in your after rehab appraisal. You bought a $125,000 house, put $75K into it, and you are negative ($10K) right off the start. It will take just over four years of $200/month cash flow (50 months), to make up that loss of $10K. During that time, maybe two, maybe three renters? So, that $1200 a year in additional rent for make ready and between occupant repairs? You’ll want a full house interior paint job each time, even if just a single coat. (That’s the law in California, incidentally.) There will be some stuff to fix. Most likely plumbing related, maybe flooring, too. Thank goodness for luxury vinyl planking, but still. Labor costs and some material costs. Nope, that extra $100/month gets eaten up fast.

As it turns out, $1500 a month rent is about average for the KC MO area these days for a house like that. It is an “unaffordable” home for the renters. They cannot come up with enough money to buy such a place, even at $125,000. With 15% down ($18.8K), and a 6.8% 30 year fixed loan (current market rate), same taxes, same insurance rates (except, they’ll have higher insurance rates, because they have not yet done any of the repairs you did – like that new roof), their monthly mortgage payment (PITI) would be $1,222. That’s without mortgage insurance (which if they are lower middle class folks, with typical lower middle class blue collar incomes, the lender will almost certainly insist on). AND, that is for a beat up, NOT fixed up nicely, almost 100 year old house. For $278 bucks a month more, they could be living in a much nicer place, fully updated, and not ever have to worry about maintenance costs. And still have that almost $19K down payment AND the closing costs (several thousand bucks, for sure – we didn’t discuss those costs at all) in their pockets still.

So, the “greedy” landlord is $10K in the hole, won’t start breaking even on actual cash flow for over four years, and assumes all maintenance costs and between occupancy costs. Of course, the “greedy” landlord does own $90K equity in a $190K valued property. And has a $100,000 30 year mortgage to pay off. If that “overvalued” property sinks in value to say, $150,000, the “greedy” landlord now has only $40K in equity (remember, the “greedy” landlord dropped $100K of actual money into the property at the start of all this), and still has a $100,000 mortgage to pay off. On the other hand, there are tax write offs associated with rehab costs, and depreciation, of course, and write offs on the interest cost of the loan. But some of the readers think those should be taken away, too.

Of course, an attractive prairie craftsman style older property has been saved for several more decades of life. And the rental residents have been given the opportunity to live in a fully remodeled, solid home – something they were proud to come home to – rather than just a trashed out slumlord property. But there’s no “cash value” to that. (Other than that rent, which, as we’ve seen, is barely enough to make doing the buy, rehab, hold and rent operation even remotely profitable.)

When those housing costs plummet, which some of the readers are hoping for, well, maybe some of those older homes will become slightly more profitable to buy, rehab, hold and rent. Or maybe not. It’s still going to cost about $75K to get them fixed up. If inflation does not continue to drive up those costs.

Oh, and good luck trying to find any lender who will cut you a mortgage for any sum under $133K loan amount. That’s right about 70% of $190,000. Basically no mortgage lenders will loan less than that these days, and they sure want any commercial buyers to have at least 30% equity in the deal.

And remember, I haven’t covered closing costs in any of this. They eat into any profits very rapidly, too.

It’s all too easy to blame “greedy landlords” on “too high” rental costs, or on “driving up the price of housing.” Until you actually start to pencil out the real numbers. Looks different from the other side, when silly things like facts get thrown into the mix.

And please remember, this example is for a basically sound, 80 year old house that cost $125,000 before rehab. And is NOT in a “bad neighborhood.” The median cost of a home in the Kansas City MO area last month was $275,000.