Sky-high prices, today’s mortgage rates, property taxes on those sky-high prices, and spiking homeowners’ insurance costs create a peculiar situation that more and more people are taking advantage of.

By Wolf Richter for WOLF STREET.

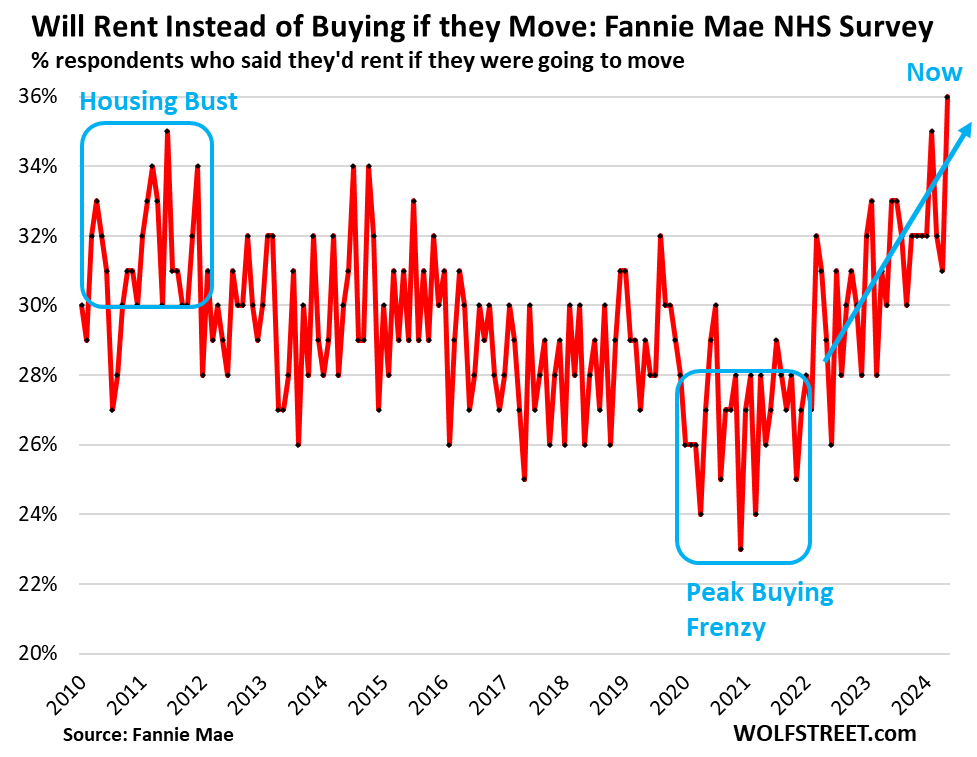

The share of people who said that they would rent rather than buy a home if they were to move spiked to 36%, an all-time high in the data going back to 2010, according to Fannie Mae’s National Housing Survey, up from the 23% to 28% range during the free-money buying frenzy in 2021-2022.

That 36% share has surpassed the highs of 2010 and 2011 during the housing bust, as home prices were in freefall. And the trend (blue arrow in the chart below) is promising to make renting an even more popular choice because it makes financial sense.

This is just another indication that the 50% explosion of home prices since 2020 – more in some markets, less in others, fueled by reckless monetary policies through 2021 – has created a peculiar situation where on a monthly cost basis, it is now far more expensive to buy a home than to rent an equivalent home pretty much across the country. And people are figuring this out, and they’re starting to engage in an arbitrage to take advantage of a price difference between similar products.

“One effect of the prolonged period of relatively high home prices of the past four years is that we are seeing a slowly growing preference to rent rather than buy on consumers’ next move,” Fannie Mae said.

“With rent growth expected to remain modest in 2025, more consumers may be seeking – and finding – attractive deals in the rental market as they continue saving toward a future home purchase,” Fannie Mae said.

But it’s not just too-high prices. Mortgage payments at today’s rates, for homes at today’s sky-high prices, plus property taxes on those sky-high valuations, plus skyrocketing homeowners’ insurance have seen to it that the monthly costs of buying a home today have far outrun the monthly worry-free costs of renting.

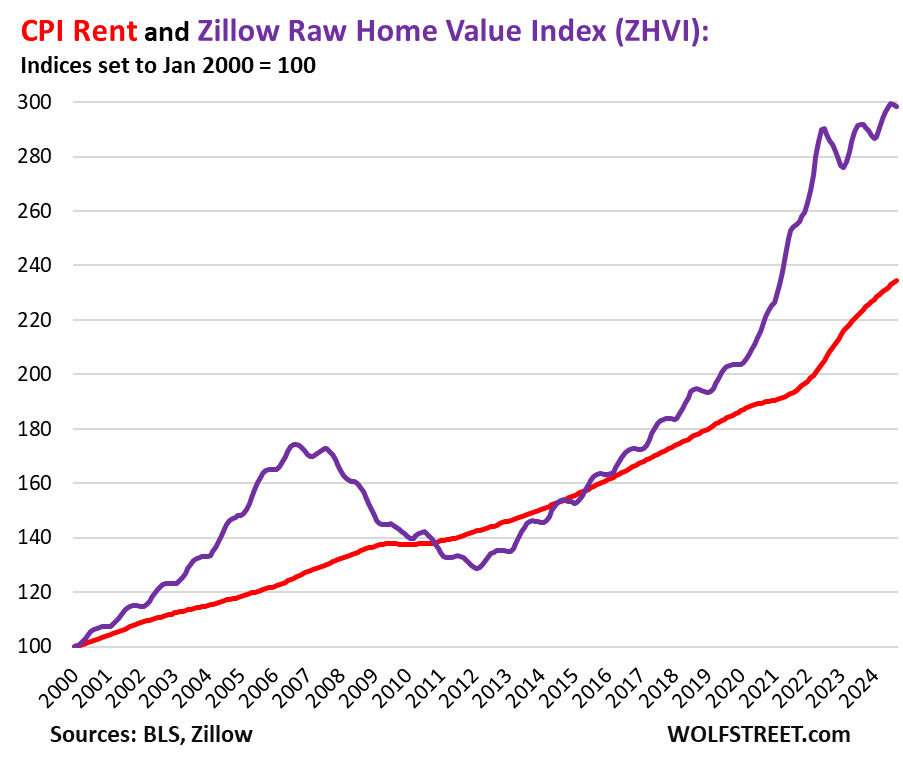

Simply comparing the trajectories of rents and home prices – excluding the effects of higher mortgage rates, soaring property taxes, and spiking homeowners’ insurance premiums – shows just how far home prices have gone out of whack.

For this purpose, we’re looking at the Consumer Price Index for Rent of Primary Residence via the Bureau of Labor Statistics’ CPI data (red) and home prices via Zillow’s “raw” Home Value Index data (purple) both set as index where January 2000 = 100.

And we see that rents have also surged, but not nearly as much as home prices. Again, this measure of home prices excludes the additional homeownership costs of higher mortgage rates, soaring property taxes, and spiking homeowners’ insurance premiums.

People are doing some basic math and are finding out that they’re getting ripped off if they buy an existing home now. If they buy, they will just make the sellers and Realtors rich, feed investors’ interest income from MBS, stuff local government coffers, and fatten up the revenues and profits of insurance companies.

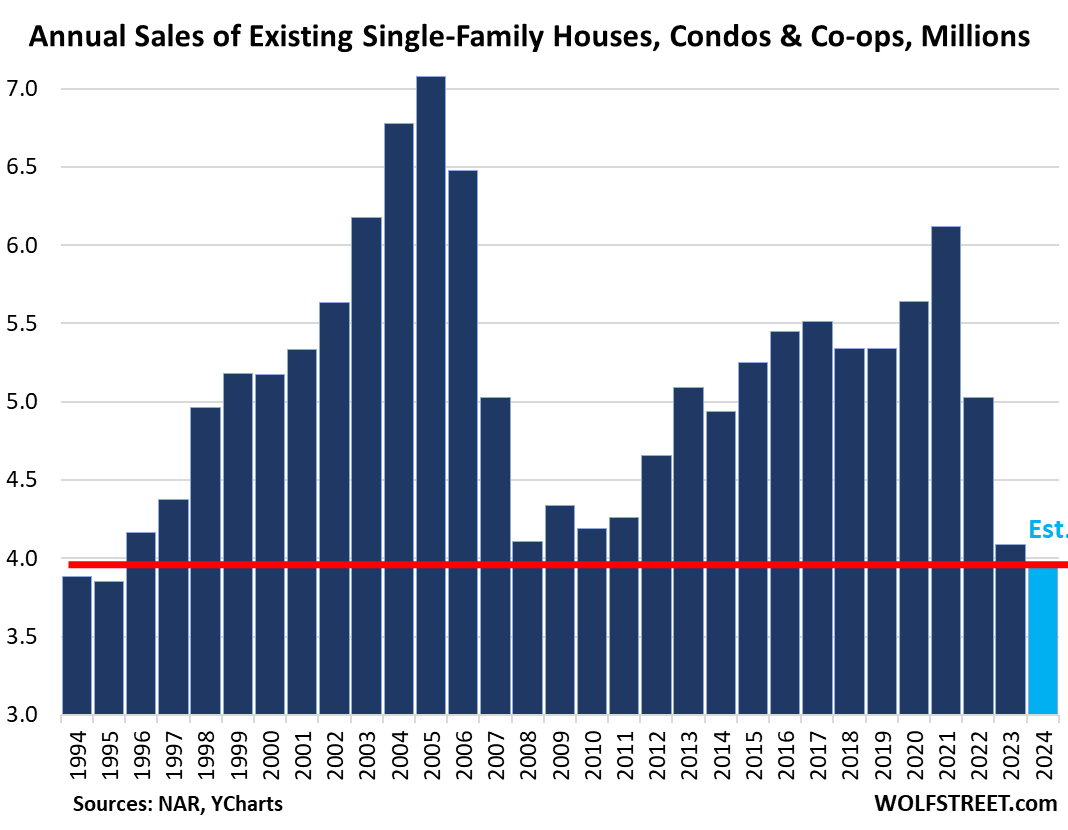

As more and more people have engaged in this arbitrage to take advantage of a price difference between similar products (renting v. buying a similar home), demand for existing homes has plunged to the lowest levels since 1995.

As demand has plunged, inventories and supply of new houses and existing homes have spiked, see the charts in the comments below.

And this growing preference for renting instead of buying will sap demand for home purchases even more, with sales having already plunged to levels not seen since 1995. Too-high prices destroy demand, which is a fundamental economic principle that even home sellers cannot escape (light-blue column = our estimate for 2024, historical data from YCharts).

If people rent a similar home, rather than buy it, they have more flexibility at a much lower monthly cost, they can save and invest this money or spend it, and they won’t be house-poor.

And with home prices now being targeted by higher mortgage rates and $2 trillion of QT so far – QT is in part responsible for those higher mortgage rates – these renters who choose to rent instead of buying have no risk of losing additional money when property prices head south, which they have already started doing in some markets, from our Most Splendid Housing Bubbles in America:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And what about inflation? 35 trillion in debt and no inflation. I do not believe it. It is great to rent, buy in the end you have nothing. No American dream here.

hard to see huge price decreases with 30-50% devaluation of fiat $dollar

why did gold go up 20% in 3 months??

expecting HUGE spending from our spendthrift run away govt

another $100B for worth less war in UKIE-VILLE

Devaluing the dollar is a loss in value, which is the same as devaluing an asset. Devalue the dollar and it’s easier to pay off debt, and your house is worth less. That’s the plan…

I agree with @joedidee, and I wanted to respond to @KGC below. KGC you have it backwards. When you devalue the dollar, you actually increase the value of assets that are priced in dollars. Drop the value of the dollar 10%, and suddenly your house that WAS worth $100,000 is worth $111,111. That is Joe’s point. Back inflation out of housing prices – particularly when inflation for the cost of shelter is running above overall inflation – and look at these numbers in real terms. Suddenly housing doesn’t look quite so over-priced, because the value of the dollar has fallen.

Sorry Greg, but until someone pays you $111,111 your $100,000 asset is only worth $100,000 (devalued) dollars.

Now you can borrow against that new perceived values, and a lot of folks do, but if there’s no buyers at that price point when you need to sell things get ugly. That’s why nobody really wants to see houses, etc. take a dive in sales prices.

The whole point is comparing the total cost of renting to the total cost of buying. To give a realistic example, a 3/2 SFH in the SF Bay Area might rent for $4000/month, while buying the same house might cost $10,000/month. Allowing for tax deductions and such, let’s assume that buying is 2X.

So now the choice is to spending $96,000/year on the house, with a large proportion of that going to interest and taxes OR spend $48,000/year on rent AND put $48,000/year into 4%+ CD’s.

But human nature being what it is, most will spend those savings on frivolities like new cars and Swift concerts. Buying, not renting is effectively compulsory savings which mature when later wisdom has developed.

We gotta stop talking about the tax deduction for mortgage interest. After the standard deduction was doubled in 2018, the majority of folks don’t itemize deductions and this isn’t the perk it used to be. It’s been six years and I still hear realtors carelessly using this line, completely unaware and uninterested in the real tax benefit implications.

I was just trying to be overly fair to the buy side…reality here is renting is probably 1/3 to 1/2 the cost of buying, but I’m too lazy to run all the numbers, and a lot just depends on the individual home (like repairs), landlord, and the future, which we don’t know.

To be fair to RE agents, in CA the MID + SALT can make a difference (although not as much as before), but on the other side home repairs can add a lot to ownership costs.

You are absolutely right, Tony. This is where the brains separate from the emotional stance of people. Those who take the time and think things through realize the situation as you’ve proclaimed it to be. It’s interesting, because I sold my condo in July and I’m in a roommate situation now saving up for my next house. Salute!

Mac Money,

Will be interesting what happens with new Congress. All the tax cuts you referenced and more expire end of 2025. Only big one that doesn’t is corporate tax rate. Wouldn’t be surprised if they try to do reduce corporate tax rate further and then bring back the others but time will tell.

@MikeB, yes the difference can be wasted. Or renting without additional savings could be all a family could afford.

But you can also throw money away when buying, including moving frequently, cash out refi’s with the $$$ going to frivolous expenses, doing unnecessary upgrades, etc.

So are their original purchase prices low and they are making money on $4k / month rent. Otherwise it would be a terrible return being a landlord in SF.

Cut and paste from article.

————————————–

San Francisco is also home to one of the highest percentages of residents who rent. At the moment, it’s estimated about 65% of San Franciscans rent their domiciles.

Not only is homeownership outside the means of affordability for most San Franciscans but renting is actually far cheaper still — even in the long haul. At current home and rent prices, you could actually save around $800,000 over the course of 30 years (assuming a secured 7% mortgage at present home prices, with 10% down, and a lease signed for a rent-controlled unit at the current market rate).

Agree with MikeB–the reality is most won’t roll the savings into other investments. There’s a reason that a lot of wealth is tied up in real estate equity and retirement accounts–they’re both set it and forget it. You live in the house and make a payment monthly. Before you get your paycheck, a percentage goes into a 401k, IRA, etc. It’s out of sight and out of most people’s spending ability. Wealth in America is generally a lazy process.

Hah – Every time we get a decent bull run in real estate some joker talks about the pending crash. I’ve been jacking rents 5% minimum annually. Over time real estate will continue to appreciate @ 4.5% like it always has. Keep renting and drive more demand!

You made my point, 🤣 . Rents increased nationwide 20% in three years while home prices shot up 50%+ over the same period, on top of already sky-high prices. And now it’s a lot cheaper to rent an equivalent home than to buy it, which is the arbitrage described here in this article. RTGDFA.

And as more people choose to rent, the inventory of homes for sale is starting to pile up, which I showed you in the charts.

Eventually, the arbitrage will end when rents increased enough and home prices fell enough to where there is not much difference anymore in monthly costs.

Appreciate your analysis as always!

Is there any data on increases in rental inventory? Anecdotally I’m seeing houses sit empty for rent for up to 6 months in Seattle.

If these don’t rent surely they will be put up for sale

Based on your research, when was the last time home prices were pushed down due to oversupply? I’m guessing the GFC, but correct me if I’m wrong.

Would you consider supply to be at those levels? The charts don’t seem to show that.

TheData,

The problem now is lack of demand. That’s why inventories are rising. Prices are too high and demand fizzled at those prices. That is kind of a new scenario in my lifetime.

Another factor in being a home buyer is the acceleration in property taxes and insurance costs.

I had a guy in Arizona – not known for Hurricanes or Earthquakes – tell me he’s seeing 20% premium increases. 20-30% increases in Florida and Kansas alike since COVID.

Property tax – the yearly tax on my modest Florida condo went from $800/year in 2020 to $1100 in 2024, and I don’t live in Miami or Tampa or Palm Beach.

My condo fees went from $320 to $460, and 80% of the increase was insurance on the building, only 20% due to trash, utilities, landscaping, etc.

Another wild thing is that 1200sqft 1960’s era 3bed,1.5 bath modest houses are still trying to get $270k, when you can buy 1600+sqft, 4bed, 2+ bath, USB ports built into the wall, new HVAC, new roof, 2 year warranty and builder 5.5% incentives for just over $300k.

The used car market is insane too, with 10-11% rates on 50-70k mile cars with several years old, but only 35% less than current prices on the current models.

There is no solution I can see except somehow getting years of low/no inflation + substantial wage increases (esp. for working class jobs), or pounding inflated asset prices back down.

Sure seems like big corrections are bound to be coming to a housing market near you. I wonder what the real trigger will be for sellers to regain a healthy sense of reality when pricing their homes?

Needing to sell will provide reality or watching homes sell for less than 2021 prices may soften the market. Wolfe has described how it takes 4 years. Who the hell wants to pay 7.25% on a money pit, if your not buying a school system, it’s simply not a good investment and the well, ya gotta live somewhere ppl are locked into a 3% mortgage but chasing an asset w softening value at 7%, your an idiot. And i don’t want to hear about interest rates in the 80’s my parents financed their overconsumpti9n on the proceeds of two homes, all time periods are not analogues.

I’m waiting and collecting cash flow

of course my mortgage costs on rentals = $0

If I understand the implications of your comment, then I think it’s a point well taken. Rentals probably no longer work as an investment if they have to carry much or any debt.

But isnt that what we were told about the great reset, you will own nothing and enjoy it.

I find it hard to agree with Mr. Wolf that a big correction in asset prices is coming. At best things will stagnate for a number of years at the new higher level while incomes catch up. Only if there is a BIG spike in unemployment and incomes drop significantly will values drop with the 25% and 50% magnitudes people expect.

I can only go by my local conditions. Where I live, none of the things Mr. Wolf talks about in the housing markets is happening. But as they say in RE everything is location. Every market is it’s own story.

If incomes catch up to nominal prices then expected loss in real value already happened.

Keep collecting.

You sound like a good sheep hearder, you care for the sheep, give them some good grazing, and in return they multiply giving you, the sheep hearder, a larger flock….and you detail for us here your common sense approach…thank you.

Get a more masculine name like bullfrog or bone crusher, I was initially confused as to your gender….joedidee, joedee, Jodie.

But I think I liked you better thinking you were a female, out with the sheep, with your long flowing hair…keeping guard.

I hate to say it, but we need a good good recession/depression to clear out all this malinvestment.

And also we need some deflation to get the prices back down to where they should be.

The federal fed chair was asked point blank if we could have some deflation and he said the Federal reserve’s framework doesn’t work with deflation and we’re only going to have inflation.

Lack of buyers and rising expectations of declining prices are the usual triggers.

“I wonder what the real trigger will be for sellers to regain a healthy sense of reality when pricing their homes?”

Unemployment. You can’t keep things you can’t pay for. At some point defaults and foreclosures will begin to spike and at that point we’ll really start to see price movement.

sellers need to keep paying their mortgages on empty houses

year of that and they find discounting may or may NOT work

But Daddy PoWPoW will not let unemployment drop.

That’s WHY he’s cutting rates NOW to save our amazing labor market, don’t worry PoWPoW would cut rates to zero and turn the printer on, before he let any of his cronies assets begin to devalue.

Everything’s fine, carry on

Everyone gives the Fed far more credit than they deserve. Tthey didn’t even get the “transient inflation” thing right just a couple years ago, let alone all the other decades full of proof they suck at their job.

There is no stopping the boom and bust cycle as long as the Fed continues to exist.

The only real question here, as investors continue building rental properties, is how long these terribly built units will last. One the past twenty-odd years, the value of the built works has deteriorated so quickly that homes and apartments being built now have the shingles buckling within five years—and that’s simply a morsel example.

In my humble opinion, the final demise of these poorly built complexes will be the bitter end for a lot of investors. Who knows when the bandaids and slings will run out, right?

Do you invest in your 401k with the anticipation of it decreasing in value? To think homeowners that are selling need to do the same is hilarious.

I’m selling 5+ acres in north county San Diego. If want to take over heaven, you have to pay. If not, rent out a tiny apartment and languish with fomo.

For me, I want to move to be closer to family, but if nobody steps to the plate at my price, I’m not going to discount the property 100k, because it’s still peanuts mortgage wise. Why g8ve up my appreciation and 300k+ in improvements.

For that, I keep my 3% interets payment and rent out several bedrooms to family, covering my mortgage, and revisit selling at a MUCH HIGHER list price years later.

Either way, I’m not budging in price, nor should anyone else. Now, if you bought a house in an undesired area and jacked your price up ridiculously, that’s on you.

Some people are better positioned to ride out the storm and creatively get ahead regardless. Everyone else will continue to rent, and purchase brand new cars and huge TV screens because they are DUMB.

How many teslas I see in rental parking lots is ABSURD.

I’m #2!

Not when you count replies to #1. But you’re right about being a steaming pile of #2 if this is all you have to add to the conversation.

Go outside. Touch grass.

Thank you, Wolf!

So much excellent data!

Yay! At 36%, irrational exuberance and FOMO are dead with buying a house.

At least they are down to the levels below the darkest hours of 2012 during Housing Bubble I.

You included my favorite chart: CPI Rent and Zillow Home Value.

The current gap is 1.5X wider than the gap during the peak of Housing Bubble I in 2007. Just before everything crashed.

A good time to buy would be when the lines intersect again like they did in 2012.

From your excellent chart, this intersection could happen if:

1) Home values fall 30% and rents stay constant. This would be similar to the 2008 HB crash. With increased taxes and insurance putting upward pressure on rent, rent will likely not stay constant. Also, I believe the powers that be will not allow home prices to fall more than 20% to avoid the foreclosure disaster last time. You can’t have too many houses underwater from downpayments or refi/HELOC equity minimums without a disaster.

2) Rent increases 20%(to cover increase insurance, services, and tax costs) and home values fall 10-15%. This may take 2-3 years but the lines would intersect without too much pain.

3) A major job loss recession and stock market crash could cause both to fall.

I’m betting on #2 to re-ignite buyer interest above unless the Fed loses control.

Rents are close to peaking, if they haven’t already. They only appear

“cheap” relative to the high cost of owning.

Home prices already peaked and most of the future sales will be at much lower levels. Sellers are slowly reducing list prices – way too slowly. In many cases they’ve had multiple reductions and the houses still aren’t selling. This means they’ll have to reduce prices even more to sell.

What makes you so sure rents will come down?

If rents keep climbing then locking in a mortgage rate for 30 years seems like a no brainer, even if you’ll pay more than renting.

What will keep rents climbing forever?

– healthy or overheating economy leading to no recession

– inflation

– widespread war

Not sure the most likely trigger for inflation. Significant tariffs would either raise the cost of goods or disrupt supply chains. Extreme deficit spending could devalue our currency leading to an increase in commodity costs in dollars.

I never try getting last $ out of rents

being bit below with nice place gets better tenants

mine are usually 3-5 years in duration

I don’t usually raise rents once they’re in – no need to get them to think about moving

12 months rents v 9-10 = 20% annual cash flow + fixup + marketing new tenant

but I also kick out riff raff

I will share, do with it what you want.

I used to run the same script. Somehow makes you feel good about yourself. Had an epiphany a few years ago.

Was going to loan some money to my son and make him pay it back, but not raise the rent to fair market on tenants?

They’re strangers, and no matter what, have no reciprocal loyalty to you. That’s something we landlords create.

I raised and continue to raise rents as market dictates. Have not lost one of them over it and average turn time when someone moves away is less than a week.

Until you do it, you can believe under market rent equals better tenants, but it’s simply NOT true. It’s a false association because you already made the decision.

You’re losing thousands. I cash flow $2k more per month with absolutely zero correlation to the things you said, which I too once believed.

I want to see renters go on a massive rent strike, and just not pay.

If one person doesn’t pay they get evicted. If all don’t pay, then what?

You really get excited over a 13% sentiment rating fluctuation.

I think it means the irrationally exuberant speculation on housing as an investment is dead.

When things settle, people can buy a house as a place to live long term. Just like they did from 2010-2014 based on Wolf’s chart.

still lots of flippers out there

when I see them with deer eyes I know I ought to be buying

For like 3 seconds. They better be poised and ready before the next bubble. Your “normal prices” do not last long at all.

Or wait, what is most likely is that it will be a time when most cannot buy. Then they will fill these forums with their sad song. Boooo hoooo hoooo 🎻

The number of new apartments being built nationally is creating more supply and downward pressure on rent pricing in markets where there is land and reasonable local government. Real incomes after inflation have not kept up with inflation over the last 3-4 years so this limits demand for any type of housing be it rentals or purchasing. Nick Gerli is projecting 20-25% decreases in housing values for example in Florida as I see that trending in certain markets already. The large corporates that bought much of the REO’s from 2012 to 2017 and dumping their rentals at any cost as they see what is coming to create dry powder for the next cycle.

Have you heard of hurricanes and floods. This is why I live in TX. More businesses. More people. Most don’t want apartments. Rents up. Who wants flooded homes or areas flood prone.

Houston? Every time it rains it floods. Recently my daughter didn’t have electricity for two weeks and she lives in the city! My daughter rents out a house in South Austin – rents are down big time. She wishes she had sold the place when it peaked. Texas is a dystopian nightmare. The infrastructure stinks, crime and property taxes are through the roof. There is no water left. The electrical grid cannot handle the people who are here. We are all getting out as soon as we can!

LOL. I stopped reading when you mentioned click bait Nick Gerli. LOL

Will new home builders ever throw in the towel and stop construction. ?

Will they lose money? Will any go belly up?

I seem to remember that happening in the distant past.

Well the stripper in The Big Short bought 5 houses. Maybe they got tired of her calling. 😂

With home prices still at lofty levels, why should they stop building?

All their labor is about to get deported. Homebuilders costs are going to go through roof if they can even find labor. There’s a reason their shares dropped on election day.

Listen, I’ll explain market dynamics to you, because a LOT of people seem to have this notion that once the Mexicans are gone, nobody is going to plow the fields, nobody is going to build the houses, etc etc etc

YES, someone WILL replace them and YES that person will require more payment for their labor than Julio, and YES that will either be inflationary, due to wages going up, and/or cause the profits of certain industries to fall, depending on whether or not they can actually pass the costs onto consumers without losing business

Absolutely under no circumstance in any reality would there be nobody to fill these jobs the existence of illegal labor does nothing but devalue labor while propping up corporate profits

Throw in the towel of making money? Heard of stock market?

The big public homebuilders did not go belly up last time. They got a government tax bailout rule.

Lots of mom and pops home builders not big enough to take advantage of the government tax bailout did go bankrupt.

Result….in HB1 25% of homes were built by the publicly listed homebuilders. Now it is over 54%. Thus, they will get bailed out if anything bad happens. It is the American way. Get rid of the mom and pops and bailout the big guys. That is why it is important to grow and do M&A as fast as you can to get into the TBTF category. :)

During recessions home prices correct, but landlords don’t rollback

existing leases, only new ones.

And our very generous local governments gladly roll back property taxes /s

When rents drop, landlords lower rents for tenants they want to keep. If you haven’t seen that, they may not have wanted to keep you.

Oh yeah like any landlords like (whom they consider) the “Poor”.

They can’t shower fast enough when they get home.

We were building new subdivisions from late 60’s til late 70’s and boom , no kaboom:construction dried up!

Seems like the Pulte’s and the like are making a few more concessions that are not sustainable. Kaboom?

Here by the beach in SD County, i’ve been saving approximately $4000/month renting instead of buying. Starting my 5th year and that savings turns into real money pretty quickly. Also, I have a smart landlord that values a good tenant. Win/win for both of us.

In certain areas of California you would have come out ahead hundreds of thousands of dollars ahead renting and investing the difference in the markets versus buying over the last few years.

Owning a home is soon to become an opportunity afforded fewer Americans due to land use restrictions, urban growth boundaries, aversion to building condominiums or converting apartments to condominiums. However opportunities are always available for the buyer who works at it and makes some compromises to get on the home ownership track. The best time to buy a home is when you can. The best time to own a home is now, especially if you are retired living on a fixed income.

Or you could just rent something minimal and have extremely good saving and investing habits. Then your goal is to retire to a cheap area where you can have a house built to spend the rest of your days.

That’s a pretty simple and clean goal.

And also you could take up lots of hobbies once you retire. Hobbies are funnnnnnnn

And if you build one, make sure it’s something you can age in with relatively little maintenance.

… said Bill Brewer, the Realtor trying to sell homes to rake in the commissions.

The cost of renting is not just the rent, it is also the cost of moving. We have lived in several rentals in over a decade and the cost of moving is easily over $20K for us. Two of the moves were interstate. Renting gave us mobility but it was not cheaper overall.

While I do agree that rents are slowing dropping now, they are not dropping as fast as home prices right now. A couple of weeks ago, the for sale/for rent signs on two streets near me were 11, now the signs are down to 8. Home prices are falling faster than rents.

What are the costs of interstate moves when you own the home, including the costs of selling the home, and buying a new home, plus the $20k in moving expenses that you had, Petunia? Do you get free interstate moves after you buy a home? Are free interstate moves one of the benefits of homeownership that renters don’t get, LOL?

The biggest potential cost of renting is the lack of an inflation hedge and no appreciation.

This is a largely due to our corrupt FED/Bankster/Treasury/GOV money creation system and accounts for a good chunk of the wealth divide.

I think Petunia makes a valid point – renters as a group probably move more often than owners.

I admit I don’t have anything to back that up except my personal experience – but I rented 8 years and moved 4 times during that period.

For me, another risk of renting is insolvent roommates. Imagine being halfway thru your lease and having your rent effectively double because one of your roommates lost their job and suddenly “can’t” pay their share…

No you don’t get her point. She didn’t make that point you’re making. Her point was that moving expenses hit renters when they move, but not homeowners when they move. That’s the comparison she made to explain that renting is not cheaper than buying.

Wolf,

My point was that moving is more common with renters because leasing exposes them to more risk than owning. The risk was in the cost of renewing the lease which was generally higher than the rise in our income.

For many years renting was better for us because it gave us mobility, which we valued more than the cost of renting. In order to keep up with rent increases we moved to higher income situations. If we had owned a home, this would not have been possible because of the time involved in selling and buying.

Generally, we found renting was more expensive because we had to move to keep up with the costs. We recently purchased because a rent increase priced us out. That rental has been on the market for almost 6 months. The landlord priced us out and himself as well.

Renting is only better when you have some form of rent control giving the renters rent stability. Otherwise, your rent will always outpace your income.

Petunia,

Renters don’t move “interstate” twice because of issues with the landlord. That’s just bullshit. But that’s the point you used to say that renting is not cheaper than owning. Just BS. People move interstate because they want to or need to live somewhere else, renting or buying no difference, same thing.

I can pay for rent by investing the cost of the house in Tbills. No tax, maintenance, insurance, price risk. The latter is huge at today’s prices. So why should I buy this house?

To rent it. The deals are still out there. May not be the perfect home, but you won’t ever live in it, so size and school zone are irrelevant.

Staying facts, not bragging: I pay for EVERYTHING with OPM including food, gas, vacations, insurance, hobbies, utilities, vehicles, etc.

Renting for free is thinking too small. Live for free, then you can invest all you earn.

When the numbers work, it’s 12-16% ROI after expenses vs 4% after taxes. After approximately 8 yrs, you own it if you dump the profit back in to paying it off.

Then you moonshot your wealth building. At ANYTIME you can choose to make another 1500 per month. I currently pay cash for 2 homes per year.

I fund my entire lifestyle by buying a house instead of an expensive car. Get the car and another house for free and increase the cycle and net worth.

This is opposed to working for the money, then investing it, and waiting to earn more. You’re constraint is time and thus speed.

You can do the same investing several million as you suggested, but how long is that going to take?

I have wracked my brain trying to diversify, I end up buying another house. There is simply nothing that beats it except a lucky stock pick or having bought bitcoin in the beginning.

Funny bitcoin: bought $100k gold in 08. Had I put that in BC it would be $660 million!

Pilotdoc,

Do me a huge favor and add some (fake) alphanumeric stuff in front of your email. Your current (fake) email sends them all to moderation.

No, the best time to own a home is not now. Only a realtor would say that. Especially in the Portland, OR area. I just moved from there (Sherwood) to TN, because the OR prices are literally stupid to live in a place with such poor weather, such high income tax, and an almost non-functioning downtown. And the stupid urban growth boundary artificially restricting building. I rented a brand new, really nice apartment outside of Nashville for $1300/mo. I make $140k a year, and I’m not even buying here yet until the prices come down another 20%. My son rents a big house in the Bethany area (NW Portland) for $2600 a month. The nice area with all the tech people. Zillow says the place is ‘worth’ $900k. He makes 6 figures as well, and has a big down payment saved up, but he is also sitting on the sidelines waiting for the stupid to die down.

“in a place with such poor weather”

I don’t get this at all for the PDX area. May through October are pretty much spectacular, blue skies, and with a legit warm summer. The shoulder months are hit/miss, and only Dec-Mar are a bummer. But even that bummer is way better than the popular midwest towns.

You’re spoiled!

I’m not at all spoiled. I just hate the endless cloudy days. It’s oppressive. The only truly good months there are July-Sept. I lived in Portland for 40+ years. Being able to work remote gave me freedom to see sunshine. I tried Seattle too. It’s just as bad there.

I worked in downtown Portland for 35 years. I got to see it turn to shit firsthand. It makes me sad. It used to be a nice city.

And why should I pay $600k for a fixer house on the west side of Portland when I can get a great move-in ready place in an area with better weather and lower taxes for $300-400k?

Houses are money pits. As a renter, when something breaks I laugh and call the landlord and tell them to fix it pronto – and to not hesitate and annoy me lest I get itchy feet and decide to let them twist in the wind as I vacate the property, causing them many sleepless nights and emotional duress.

*duress = distress (still dreaming of that edit button)

Depth we don’t have Reddit money around here. ;) hehe jk

It’s like a bunch of dudes renting a ski cabin, if it’s jankey you deal.

Just so you know, many landlords wouldn’t lose sleep over losing a tenant. In general, we own property because we already have money.

This. There are other tenants waiting in the wings to take your place. If you get itchy feet you’ll have to find some powder for that until your lease is up. Then don’t let the screen door hit you where the good lord split you.

that’s a gross oversimplification. in certain bubble markets, like austin, nashville, miami and fort lauderdale, san diego, and i’m sure several others, rents skyrocketed in the last 4 years. some of it is reversing as work from home is decreasing, and a lot of owners would not be able to fill their rentals with the rents they’re getting today. if you got $1,500 in rent in 2019, and are now getting $3,000, you may not be able to find one for anywhere near $3,000, especially if you don’t want a gap month or two.

Franz, if I was renting at $1500 in 2019 and now I’m getting $3000 that extra $1500 is pure profit since the rental was cash flow positive at $1500. Lowering the asking rent, if necessary, is no problem. As for gap months any landlord who knows what they’re doing has a plan to handle a few of those here and there.

mustbeaduck, sure, but that isn’t really the point. what he said was that if the landlord annoys him, he can leave.

in my example, say the tenant is a good tenant and says “ya know, mr. landlord, the market rents have dropped a lot, i’m only willing to pay $2,500 for next year,” and the landlord tells him to pound sand, then he’s much worse off if the tenant follows through and vacates. that’s my point.

Franz – if market rents have dropped to 2500 why would any landlord tell a good tenant to pound sand? I think you’re conflating house sellers, who want their aspirational price to sell their house, and a landlord. The landlord should know they’re not going to get more if the house goes back on the rental market. It makes no business sense to lose a good renter in that situation. Regardless of the emotional reactions of DC’s original comment a landlord probably doesn’t care if you feel like you’re “sticking it to the man”. It’s a business transaction, nothing more.

And landlords hate hate hate spending money on the property. I’m pretty sure most see it as a vending machine where they turn the wheel with a satisfying click and $3500 just pops out.

You call with a water heater issue or the fridge stops working and they are working the phones like a ross Perot election volunteer to get the bottom basement most crusty service they can find. Some service living under a bridge for $99, “fine that will work. Our tenant doesn’t need much. Just get it working.”

mustbeaduck, with all due respect, you are assuming that most landlords are like you. that is not the case.

there are many that are delusional about what their properties will rent for, just like there are many sellers who are delusional as to what they will sell for.

this is especially true in markets that were greatly distorted by the pandemic.

I feel like I know you, and your maiden name is Tina E. At any rate, the house I rent is not your cookie cutter rental. It is a custom home with impeccable, heated solid wood floors and all sorts of amenities which the owners are terrified of having damaged.

Franz G,

I had exactly that scenario play out – I was just asking the landlord to resign us at the same rent (not increase it) because I felt he was overcharging.

Even when I told him I signed a lease at a much nicer place, for $100/mo LESS than what he wanted… a much nicer place that was literally (not figuratively) seven houses down on the same street… I still got this defensive email reply about how he’s been in the business for 20 years and knows what he’s doing blah blah blah…

Needless to say, I saw the place sit empty for five months after my roommate group & I left… and yes I saw the place sit dark every day; again, seven houses down on the same street…

There absolutely are landlords who let ego get in the way of rational market decisions…

…and in Canada tenants don’t even have to pay the rent.

Enough welfare cheques pooled together means the landlord will always get paid. Always buy a bungalow with a separate entrance to the basement.

…or you could do what I did, and offer to fix it yourself for a couple months of free rent.

DC

Definitely your silliest post ever.

“Still crazy after all of these years,” huh?

Since you are a master craftsman/handyman/hammer wielder, it seems you would do the upkeep and maintenance yourself and bill the landlord.

A man with your magnificient mechanical skills should be all over those tasks.

Psycho much?

Sure you do big guy.

Landlords tremble at the mighty power of the unlanded masses.

Don’t forget his annual Christmas bonus or he may raid your fridge while you’re out working the fields.

Letting your emotions get to you, huh? What are you afraid of? Because your fear is palpable….

The landlord passes all expenses plus profit onto the renter. It would not be a profitable business otherwise.

The landlord controls the renter’s living space, and all that entails.

There’s a time and place to rent, but it has financial as well as noneconomic costs, the latter can quickly become onerous if the landlord so chooses.

Many big landlords have already gotten wiped out this year, with lenders taking possession of the properties, billions of dollars’ worth of debt has defaulted and lenders are licking their wounds. Being a landlord means that you have costs on one side and rents on the other, but rents are set by the market, and the market doesn’t care about your costs, and if you try to pass on your costs beyond what the market will bear, your units will be empty, and you make no rent, and you cannot service your loan and you default, and the lender takes possession of your property either via foreclosure or deed in lieu, and whatever money you had in the property is gone. That’s reality for landlords. It’s a risky business.

Another element here is the 2017 tax changes, which raised the standard deduction to a level that lets only the wealthiest itemize deduction. This means most people get no added tax benefit from paying mortgage interest.

Or, said differently, renters now get the same deduction that used to be reserved for homeowners. The gap began widening on that CPI/Zillow chart at about that time.

Yeah, it’s a pretty tough deduction to get. Have to fill up that 750,000$ bucket. And have a high interest rate.

It may cover your property taxes.

Something, but not much.

how do you figure? the standard deduction is $29,200 in 2024. let’s assume that your property taxes and any state income taxes hit the maximum of 10,000. you need mortgage interest to exceed $19,200 for itemizing to make sense.

obviously, interest as a percentage of the monthly payment decreases as time goes on, but a $275,000 30 year loan at 7% will have interest payments of roughly that $19,200 threshold the first year. that would be lower than the average home price in america now, assuming a 20% down payment. so it wouldn’t be anywhere near just the wealthy itemizing.

and of course, this assumes you make no charitable donations or other deductions that are allowed.

But see anything you get over the standard deduction is just Pennys.

Say somehow you had 50,000 in interest deduction. 50,000 minus 29,200 = 20,800 (you can’t take both the standard AND itemize)

That’s $20,800 deducted from your AGI, so let’s say you get a third back in the form of cash, 20,800 divided by 3 = 6,933. (You’re getting this back in addition to normal amount you would get without itemizing. So say 29,200 divided by 3 = 9733)

So see covers your property tax maybe. AND you’re getting straight reamed on interest payments a year.

And I think it behooves most people under trump tax cuts of 2017 and I guess 2025? To be married.

forgiveness asked from accountants if I got that all wrong. Haha

PatrickW,

That used to be true and is true for homeowners who purchased or refi’d with 3% mortgages. Renters saw a large decrease in taxes with the std deduction.

Today, the std deduction for married filing jointly is 28K with a cap of 10K for SALT but no cap for interest paid.

With a 400K mortgage, you will pay 28K/year in interest alone. You can itemize.

It is likely you have property taxes+state taxes that are capped at 10K so after deducting that, you can deduct anything over 18K in interest.

At 7%, that is 18K in interest on a 260K mortgage.

My point is that if you have a 7% mortgage on any reasonable house today, you should probably itemize and not take the std deduction.

Axis for the chart of annual sale of existing homes are deceptive and blown out of proportion that is not a huge difference between annual sale of 5 million versus 4 million it’s just a 1 million difference but somehow it is being shown as huge bars because it starts at 3 million instead of 0.

This may be true, but 1 million is still 20%. If prices dropped 20%, this whole article wouldn’t have been written because sales would be normal.

Element – “That is not a huge difference” Are you serious??? It’s a colossal difference!

That’s about $25 Billion in real estate commissions if the average transaction price is around $400k.

For perspective, the total outlay from Social Security payments is $100 Billion annually.

This is not a recession in the industry of real estate agents. This is a depression in that industry.

You got stuck on the graph axis and completely missed what the graph is telling you.

This is our family. We are saving at least $500/mo by renting and our square footage is double what we could afford to buy. Plus we don’t have to worry about repairs or mowing. And NO property taxes. But it’s never a guarantee long-term so that can be unsettling when renewal comes up.

I rent for about a quarter of what I would pay if I bought the house I’m in. That’s an extra 3k plus insurance (owner vs renter) and property taxes I can spend on other things. Yeah, I’m in no rush to buy :)

As long as you’re making an informed decision, so be it.

That said, my 10 year old home has a mortgage of $1100/mo. It would rent for $4500 if I didn’t own it… (mortgage monthly payment has gone down over time with refis, while rents have gone up)

Right a different time, when homes were affordable. I think if home prices become reasonable again many will buy.

On the flip side instead of buying the equivalent $500-600k town house/condo. I’m saving about 30k a year. Which after 4 years is about $140k assuming a 7% market return. Plus some interest in the $100k or so down payment so maybe close to $150k profit by renting.

On $500k house purchase right now you make about $74k assuming the historical appreciation of 3.5% a year which when you deduct realtor fees to realize that $74k is only $44k now deduct repairs and improvements. Obviously principal got paid down a little so maybe you net $40k after 4 years.

The last 10 or so years in housing was an anomaly funded by cheap money. But yay for everyone who bought in the early 2010s. Just because it was a good financial choice then doesn’t make it one now.

There will be a price correction. Just like there was in 2010. I remember thinking that I’d never be able to afford a home back in 2006-2008.

In 2015 I was able to buy the home I’m in now for $250K. Mortgage payment is about $1,100 a month. Redfin’s estimate says it’s worth $436K. Even with a 25% drop in prices, I’d still be sitting pretty.

So keep saving up money so that you’ll be ready when prices inevitably go down.

Aptly said.

In my neighborhood a house would have an ownership expense of almost 12k per month

But one can rent the same home for 6k.

This is in socal.

My mortgage payment is $980/mo. All in PITI, utilities, etc is about $1800/mo.

If I were buying this same house today, my monthly costs would surely be a lot higher. In fact, I doubt I could afford to buy my own home today.

The housing mkt is SERIOUSLY out of wack.

As a tenant, you ARE paying the property taxes, it’s just that the landlord is taking care of the paperwork.

Rents will almost always cover the landlord’s costs including mortgage, upkeep and taxes.

Rents do cover landlords’ costs, considering most purchased their rental properties during normal times at a fraction of current prices and have locked low-interest mortgages.

Right. In a normal world, renting would cost more than owning the same property. You’re paying a landlord to do something you could do yourself.

Kind of like paying a mechanic $80 to change your oil & filter, vs buying a 5-qt jug and oil filter for $40 at autozone and doing it yourself.

depends on when you bought. if you bought a house as an “investment” in a bubble market in 2022, you almost definitely cannot cover your costs with rent.

rent is set by the local labor market, not the availability of credit and speculation.

Yes but this doesn’t imply that property tax hikes can be passed on to a tenant. In general tenants are already paying what the market will bear. Until property tax hikes go high enough to depress supply, they will be eaten by the landlord.

One of my friends bought a house to rent recently

His monthly outlay is 12k and the rent he gets is 6k.

He is losing money but he believes home prices only go up

That’s the big question, where do you want to lay your head. There’s some piece of dirt awaiting its new owner.

If people were more friendly, together they could team up and…share together the payments….enjoy each other’s company while making “buying a house”very affordable.

But people don’t get along too well…

We moved cross country 2 years ago and have been renting since. I like to look at the houses for sale, but at these prices I’ll keep renting and saving the difference. The risk of missing out on home appreciation seems lower than the risk that prices could drop. When the math makes sense again, we will purchase again.

So they just elected a guy who won because the poor non college grads do not like being poor.

Wouldn’t it be bad if he also made the asset holders (like himself) poor as well?

prob more likely real estate is going from the moon to mars in the next 4 years.

But we will see!

I am hardly a Trump supporter, but didn’t house prices skyrocket during this administration? 🤔

Politicians – Many Ticks

That’s how the non college grads thought as well.

They were bleeding in the water, instead of calling beach rescue, they called in a great white. 🦈

“They were bleeding in the water, instead of calling beach rescue, they called in a great white. 🦈”

No, they were already consumed like chum.

Of course they did because he has a vast real estate holding so does his brother-in-law. Time to start buying up the homes.

@ sufferinsucatash –

How would it be better for the poor non college grads if Kamala was elected ?

@ Wolf – before you delete, this is an economics question, not a political one.

Durrrrr well let’s see one party is for the rich and the other party protects the poor.

Non college grads in the US are the Poor! And apparently dumb too because they were convinced to vote for the party of the rich.

Just telling you straight up.

Take the names out of the equation.

Being poor sucks no matter what.

Now they believed a convicted felon, narcissistic lier, low IQ / idiot, unstable, easily taken advantage by rich and enemies etc etc. What can go wrong?

Biker,

I spent a lot of time in 2017-2020 blocking and deleting the daily barrage of anti-Trump comments, and then I spent a lot of time between 2020 and now deleting anti-Biden/Harris comments, and now for the next four years I’m going to be spending a lot of time deleting anti-Trump comments. It’s almost funny how this stuff comes in waves. Censorship wastes my time, my friends.

I left your comment up as a good example of what not to do. All future comments of this type will be blocked and deleted.

So a reminder for everyone: These kinds of comments are in violation of commenting guidelines #3, #4, #10

https://wolfstreet.com/2022/08/27/updated-guidelines-for-commenting-on-wolf-street/

@Wolf

All was already said I guess.

I will try hard not posting such anymore going forward.

I’m a (relatively) poor non-college grad single male renter, and yeah the housing situation is a disaster but up until now I was at least happy to see it starting to swing back in the right direction – a soft landing so far, abandoning QE, more construction etc.

The polls are saying that voter’s priority is the economy, but I can’t make any sense of what they’re hoping for here. The right’s policies are probably inflationary on like 5 different axis, as well as being socially and economically disruptive which could have all kinds of unpredictable consequences. The mainstream estimate just for the direct costs of his ideas is $7T, max of like $15T, with what I see as an enormous potential for additional indirect costs.

If someone can make the economic case for how this ends well for someone like me, I’d love to hear it. (That’s not sarcasm.)

@Matt B

I get what you are saying. I see 2 ways forward:

1. Join the new rulers party circles. Get connections in MAGA etc, so maybe you can get some $ from actively preaching the new set up. They are good at that.

2. Limit your spending, save and invest. Wait few years and there is a chance that at the right moment you will have asset to jump and buy your place. You are just starting, everything in front of you.

A free gift of $25,000 just eluded you now that Trump is the president. Well I guess no one wanted that money anyway so they voted for Trump.

Your up a tree, a suckatash tree. The educated just got beat with the stupid stick.

I know that’s a bit harsh but I’m looking at what you just started. Now biker is going to have to put on his training wheels again.

But your vision of the possible future home prices “to the moon and Mars” and beyond is not too far fetched.

Ground control to major tom…report on Mars home prices……..can you hear me major tom….

Yes yes, let them eat cake. We’ve been here before. Yawn

🇫🇷

The only affordable homes here in the Swamp that have any hope of being a good investment over the medium and long term are in high crime neighborhoods in the fringes of the downtown and work centers near the Capitol. If you buy here you are nearly guaranteed to make out OK if you can hold out for a few years and don’t become another crime victim. I saw a yard sign the other day on one of these townhouses which was handwritten and said “Stop killing people”.

Sounds like you’d be counting on gentrification. Seems like a risky bet.

I bet the vast majority of this shift is explained by the homeownership demographic shift. Older people are fine to cash out home equity and rent and younger people who have more incentive to settle down and buy are taking longer to buy.

“Opposite,” a lot of people here would say.

Cash out and then what, overpay to downsize? I can see if your moving somewhere or to better your lifestyle but just to buy a smaller overpriced box in a similar kood seems like more trouble than it’s worth.

Wolf, I like how you describe the difference as an arbitrage – that’s exactly what it is.

But like all arbitrages, the difference will disappear. Things that do the same thing, eventually sell for the same price.

Over the comig years, home prices will be pulled down and rents will be pulled up until equilibrium is reached.

Great point – arbitrage undoes itself.

Prices in real estate are very slow to react, but this rent-buy arbitrage pulls demand out of the market. Eventually prices and rents will come back in line though some combination of rising rents and falling prices.

I am a homeowner (bought in 2017) and even I am fine with house prices coming down.

i think it’s more likely prices come down than rents go up. there just isn’t enough income for rents to go up that much more, unless wages increase dramatically.

After I sold my home bought in 1999 and sold in 2021 I moved to a smaller 1964 manufactured home in a small rural town with only 500 year round residents. Why the downgrade? Because my age was 72 and I chose a County where the RE taxes could be easily contested (& reduced).

My “home” cost $78,000, taxes are less than $400/year & I do’r have nor need insurance because I paid cash!

I also am building an “off-grid” pumice 1,200 sq ft. house in an adjoing county in southern CO and the 2024-25 RE taxes were LOWERED from

$350 to only $65 for the whole year!

What’s not to like?

What will those prop taxes be once construction is completed?

Is there a hospital nearby, James? Because that sounds dangerous a f for an old person.

We were looking at a home where they were asking $1.3M. It wasn’t right for us and they did not get any offers. Eventually, they pulled it and tried to rent it. After 6 months, they finally got a renter at $3500 a month. They pay $14k/year in property taxes. Insurance is about $7k/year. I guess they are waiting for the good times to come back. They could sell it for half the price and make more in treasuries.

Imagine doing all that work to landlord and maintain a property, only to lose money on it.

This is why rents are way too low and will have to come up.

Rents don’t have to accommodate this landlord. He’s describing a home with 21k in taxes and insurance that rents for 42k. Whether that’s profitable depends on the price where the landlord bought the home. The market doesn’t care about your entry price.

Based on the very high price and insurance I am guessing California. California has had very low cap rates (rent / price) for decades.

No one is going to get into the business of property management if they aren’t going to make money. Long term, this will push up rents.

Would you take a job if you had to pay your employer to work instead of the other way around?

Rents are as high as someone will pay. When they cannot be paid you will read a lot of articles about young couples moving in with the in laws.

Well said.

I keep telling my realtor friends to find me a 3 million worth of real estate rentals with a cap rate of 7% and I’ll buy them all. Cash.

(Crickets.)

All I hear.

I have friends dumping their rentals for MM accounts paying 5.5 or even 5%.

Living in Florida, I can see the argument for renting. Now dealing with replacing a roof and other storm-related expenses from the Hurricanes, increasing insurance costs, etc. Neighbors had extensive roof and fence damage – they’re renters, they don’t have to worry about any of that!

We lived through 5 hurricanes in Florida, don’t miss it, wouldn’t ever buy there again. But it is a nice place to visit.

The situation you are describing has existed in most large cities in Canada for years. When you factor in all the costs of home ownership it is often 30-50% cheaper to rent rather than buy. And yet for some reason Canadians don’t do the math and still prefer to buy if they can qualify for a mortgage. In fact we are so addicted to home ownership in Canada that even people who do the math still want to buy, presumably because they believe real estate is always a good investment.

Development is so restricted in Canada that owning is a better choice. They have more land than the US and only 5 major cities, the rest is mostly Crown Land. The artificially restricted supply is what keeps the prices high. Their immigration policy is also geared to investing in real estate.

There is lots of supply in Canada, currently over 4 months supply overall, much more in Toronto metro, the biggest market.

https://wolfstreet.com/2024/10/15/the-most-splendid-housing-bubbles-in-canada-september-biggest-drops-in-toronto-vancouver-victoria-even-calgary-gives-amid-surge-of-new-listings-condos-get-hit-hard/

And of course the biggest market, the Toronto metro, catching a falling knife:

With Trump winning the election instead of Harris this means the Yuan will crumble and no new money will come into Vancouver real estate and eventually the same thing will happen to Victoria, Richmond Hill, Markham, Unionville and Stouffville. This means Canadian real estate could fall all the way down to what the locals earn in a year which would be more than a 50 percent drop in prices.

In the area I live a similar sized condo is $500-$600k. At the lower end with 20% down that’s $3k month + $350 hoa + utilities. I save a little over $2k a month renting and have no maintenance costs. Like everyone I’d love to buy, but it just doesn’t make sense. Prices need to adjust to reality.

So essentially a ~20% house price correction is needed to find the equilibrium again

This is all very interesting. Thanks Wolf. But I don’t think that you should call this arbitrage. Renting a house is not the same as buying a house. They are entirely different products. When I was younger I moved from job to job and from one apartment to another, for the most part. Moving was a hassle and they raised the darn rent every year. Then a brown eyed woman rocks your world and she wants a rose garden! I’m sure that you understand.

Then you don’t profit form the arbitrage, but you pay what you have to pay. This arbitrage is not for everyone, thankfully, or everyone would rent and no one would buy, which would cause rents to double in about 1 second, which would shut down the arbitrage for everyone.

That’s how arbitrage works; eventually, when enough people it brings prices into balance. In this case, it means higher rents and lower home prices over the years until they’re roughly in balance.

Van Morrison I mean HappyBoomer,

The fact that rent vs own doesn’t include identical, overlapping demographics, doesn’t preclude it from being an arbitrage.

Here’s an example: my favorite current arbitrage is oil vs nat gas in USA. The former is very expensive relative to the latter. Not everything can be switched to burn NG since they’re still different fuels – but the price difference is so large that eventually, it motivates a change in behavior (burning more NG, converting engines, converting NG into diesel/gasoline via chemical processes).

Things that do the same thing will eventally cost the same. We burn hydrocarbons to create heat to do work. And regardless of whether you rent or own, you presumably do so because you’d rather not sleep outside.

Here in flyover Ohio, too many sellers continue to overprice their listed residential properties. The “high price entitlement” attitude is still very much in play. The agents may be complicit with that – knowing full well the seller will eventually drop the price after a property languishes on the current market for a period. The agent can then blame the market (“things have changed since the property was listed”) instead of their deliberately optimistic assessment of what the initial listing price should be.

Renting right now is a comparative bargain. I have a spacious, quiet 2BDR apartment in a newer building with a convenient location in a safe area. It rents for $1700/mo. That rent payment would service a (roughly) $252,000 30-year fixed rate mortgage loan at 7.13%, just as an example.

Assuming you put down 20% on that house, that would have been a purchase price of (roughly) $315,000. What can you buy for that price in southwest Ohio now? Very little. Usually, a dumpy house in a not-so-good area. Not nearly enough of a return to take on the headaches of home ownership along with parting with a (roughly) $63,000 down payment.

The conclusion is always the same: residential RE prices need to decrease substantially. The value (and arbitrage) proposition at current prices just isn’t good.

Are we finally returning to a balanced market? This would be good for everyone, but I remain skeptical. Prices still need to drop, but local governments have gotten use to the fat tax revenue.

Interesting times.

This seems like a situation that cannot exist for long. It will be fixed by housing prices going lower and/or rents going higher.

Absolutely 100% agree with this article. In many places, even highly desirable ones, it is now dramatically cheaper to rent than own. And it’s not just about mortgage interest rates, taxes and insurance… it’s maintenance too. The total cost of say replacing a central air conditioner or any of its major components is now almost twice what it was before the pandemic. Hiring a plumber, electrician, or any other trade is a lot more expensive now as well. Why deal with it when you can have it be the landlord’s problem?

The buy vs. rent equation is slanted towards renting more than it has ever been probably. From a historical perspective it is way out of whack. The interesting question is how does it get back to a more reasonable balance over time? Will rents increase, will house prices fall? So far in most places rent increases have been more subdued but house prices aren’t really budging much from their lofty levels. Not sure how long this situation can last.

i think the home prices not budging may finally reach a tipping point. here’s why. so many sellers have held out thinking that once rates drop, a swarm of buyers will come back in and they’ll be able to sell for peak 2021 or 2022 prices again.

problem is that mortgage rates haven’t really changed much after the fed funds rate dropped. so now it’s not just “wait until next year,” but “wait indefinitely until 7% rates drop back down to 5%.”

but how long will that be? how long are sellers willing to hold out paying carrying costs and taking on price risk to try to get the one idiot buyer looking to overpay.

once the prices drops start, it creates a snowball effect.

Let’s talk about the suggestion/argument that an additional 2, 5, 11 million people take up a lot of housing space and create buy/rent competition for everyone else.

Assume that starting in January the border is “sealed” and net illegal immigration drops to almost zero. Combined with some targeted deportations (it’s not going to be 11 or 25 million or whatever) the actual US population stays “flat” for a year or two. Can the housing and apartment construction industry catch up? I’m back in Phoenix now, I can’t believe how many old strip malls or car dealerships or cruddy single level apartment complexes are being leveled and turned into four story modern condos or rentals. And other places small 15-20 house developments shoehorned into a former single house rural properties. This metro is probably going to have another million people within the existing radius in a couple decades. I think it’s 4.5 million now.

Without getting into the politics too much (people certainly voted for it) is it safe to say that net zero or even a slight reduction in the US population will greatly reduce pressure on rents and housing prices?

Nope.

See the definition of Greed for answers.

Deflation can only go down so far as what it now costs to build new houses. Prices will only fall as QT removes enough reserves so as to limit the expansion of the money supply.

How is this ‘arbitrage’, more like hedonics or chicken for beef. Investment funds are still working the rental market, and for buyers there are alternate ways to secure financing. My big snarky question would be “and you’re going to SAVE money?” I leave it to your readers is anyone out there saving money? The other matter is location, renters need to be close to their jobs. I would call that no 1 issue.

Big institutional investors have become net sellers of single-family rental houses, even in Florida. They’re selling the houses they bought out of foreclosure in 2012 at huge profits, which is why they’re selling them. They’re adding to the supply or single-family houses on the market. And they’re building entire subdivisions of rental properties, nice new houses, built to rent at lower costs, for renters of choice with incomes over $100k that want to rent instead of buying a similar house because they can save thousands of dollars a month. Which is who they add to the supply of rentals — they’re building them. That’s the deal now. All you have to do is listen to their earnings calls and look at their 10Q filings.

Chicken vs beef could be an arbitrage for some – if you’re just trying to consume protein to fulfil nutritional needs, for example.

Arbitrage is when things that do the same thing don’t cost the same.

The best thing that could happen is it becomes clear that rates during the massive QE period will never return.

I live in San Diego and know a bunch of people who want to sell and either move to a bigger house or retire and leave the area. Every single one for the last two years told me they’re waiting for rates to drop and bidding wars to come back. I know three coworkers who paid peak prices at 7% interest rate because they were sure that once rates dropped that the boom would start again.

As for rent, the SD market hit it’s peak two years ago. People have a rental price limit just like they have a purchase limit. Supply and demand applies to renting just like buying. I know people who decided to either not move to SD or they just stayed in their current rental until this market is figured out.

My current rental is $4500 a month. It was originally posted at $5K for over a month with no takers. My neighbor is trying to rent her house out right now and it is much nicer than mine since it was recently remodeled. She is trying to get $4500 and has no takers after a month of listing it. It looks like we are finally returning to some sense of normalcy.

That’s what I do not understand about re modeling your home.

Financially you are throwing out items you paid for when you bought the home. Say you paid $50,000 for the kitchen in the purchase. Then you buy a new kitchen for $75,000. You threw out your old $50,000 kitchen. New buyers are only going to buy 1 kitchen, not 2.

You bought 2 kitchens.

I get people like nice new things, but it seems like a poor move looking at the long term net worth numbers.

In the very big picture, The Dotcom Bubble took a full 8 years to play out — almost symmetrically, 4 years up, 4 down.

Here we are at post pandemic super highs — now at a stage for super post bubble supercharging — with all time highs in stocks and housing — awaiting new far higher glorious upward spikes in the election Santa clause pump.

In terms of arbitrage — or leverage, I’m not sure the vast majority of Americans have a choice in being able to make a choice about renting versus buying — the aspect of unattainable unaffordable home prices are a clear matter of income reality.

I think the buyers strike will continue, because of price and it’s highly unlikely income is going to materially change that equation — even with election euphoria. I think the same can be said for overvalued stocks as well— but maybe the unaffordable home prices will stir up animal spirits, and convince more people to speculate on stocks — because that’s the only path to homeownership.

The Buffett Indicator suggests excessive mass speculation doesn’t outperform cumulative GDP growth — and usually isn’t the best way towards wealth appreciation.

The dollar and yields and Buffett Indicator strongly suggest we’re almost exactly at the same place as we were at height of Dotcom Bubble — except, this time is different with The Deficit Bubble expanding at an accelerating dangerous, unsustainable rate.

It’ll be interesting to see if homeowners become more optimistic about raising their prices because of the anticipated, projected, promised booming growth ahead. Clearly, the explosion in inventory will be grabbed up by speculators getting ahead of higher rents, because everything is going higher!

It’ll also be interesting to see how The Everything Pandemic Bubble behaves as it gets supercharged from here on out — somehow I think inflation plays a role as does real GDP.

Whatever arbitrage is happening now, won’t last.

wage and debt and rent slaves

In my misspent youth I owned 2 5 unit apartment buildings during the course of 30 years. I’ll skip the part where I owned here. I sold by owner with classified ad in suburban paper (2002) and flat fee mls listing service (2017) within days each time. Sold both times to Eastern Europeans. In both cases within a year, some within weeks before the lease expirations, they ejected 4 out of 5 tenants and moved their own people / themselves in. For my part I’d have better off not having them in the first place, but that’s on me.

It’s hard to lose on real estate when rates are lower than appreciation, which I believe was the case for about 10 years before the 2022 rate hikes.

Talk about rents increasing to be in equilibrium with mortgage/taxes plus upkeep based on current housing prices is nonsense. Renting is a cash business, and there is only so much people can pay regardless of what landlords want. You can see the consequence of this when a single family rental has 4 cars parked in front.

I lived in New England for many years, and there were many stately turn of the century (1900!) homes which had been turned into multi-families. All of the new tract houses have enough bathrooms so they can get filled with roommates when rents get too high.

Something is going to break eventually. It will probably be something unexpected as the math hasn’t made sense for a long time.

Do hold your breath for home costs to drop. But it will take many years and will most likely be the same price or more and look cheaper due to inflation.

Owning a few rentals is a sweet scam and a great way to charge off everything you buy to a rental, making all the income all but tax free.

Right above your article in my news feed on Google there was an article about Open door has never turned a profit and they went from 18 billion to 13 billion and they lost like almost 2 billion in the last 2 years and now they’re laying off employees.

I don’t want to see anybody get laid off but at the same time it brings my heart Joy to no companies like that or starting to go under. To me companies like that are a part of the problem the reason home prices are unaffordable for a lot of Americans.

I know the root of the problem is the Federal reserve and federal government out of control spending and QT and zerp, all that does is transfer wealth from the poor and middle class savings to the rich.

Tariffs and deportation-driven labor shortage point to inflation.

Homebuilders losing their labor drives new construction costs higher, decreases supply.

Deportation efforts, wall-building costs and tax cuts point to worsening fiscals.

Deportations drive low-end rents cheaper.

All signs point to increased demand for slum rentals, stagflation for single-family houses.

Wolf, thank you so much for just sticking to the numbers without any political comments. It is a shame some of the commentators here can’t stop themselves from blaming one side or the other.

Anecdotally, we have some friends who sold their homes and are now paying rent instead. That’s not our style but it makes them happy.

I enjoy the numbers as well but important to recognize that political and economic systems are intricately tied together in reality. We are somewhat programmed by institutions and media to view these as separate and of course that helps to setup the us versus them victim mentality. Americans, based on approval ratings, have no belief in the system but continue to buy the narratives. No sign of any of that changing but does provide late night hosts with endless material.

Clearly prices need to come down but that is a factor of mortgage payment, which of course is significantly influenced by mortgage interest rates. If those do move down, rather than what has been happening lately, I could easily see home prices remaining relatively flat and in some areas even increase. My house has gone up about 60% since 2016 when I purchased it. It is probably down 20% from the ultra high point but I don’t tend to look at the highest peak. I am only applying this to the one specific area I live in however in California so not necessarily a good generalization even one you drive South over the grapevine or in the Bay Area. Of course, people coming from those areas don’t tend to blink twice when they can get a decent sized house in a decent school district for 500-600K.

I concur with the assessment. As a landlord in the Midwest, I’m down to three single family rentals in the area. The property taxes are going up by about 33% on Jan. 1st, insurance keeps going up and 5% annual rent increases are becoming a tough sell now. I’ve already sold three houses in the last 5 years and the case for running this small business is getting harder and harder to make. If I couldn’t write off all the expenses of upkeep, interest, insurance, etc., plus take depreciation, there’s no way it would be worth doing. I’d be losing money, which is what any potential buyer of these houses would be doing if I sold them. I’m down to 4-5% return on the value of the houses now, which I could basically make on treasuries. My equity capital has doubled for sure, when you factor in the sweat equity, but I was better off as a landlord when the houses were worth 1/2 what they are, rent was 30% less, and I could find people to work on them for 1/2 the hourly rate. And so were my tenants. At least they seemed happier. Or neither of us noticed because the rent only went up 5% every three years, instead of annually. This isn’t fun for anyone.

Curious that no one happened to mention that about 55%-65% of American adults can’t even afford to pay a monthly mortgage on a home.

Ya can’t do it with millions forced to work part-time, low wage jobs. Along with monolithic costs by Creditors, Banks who now have most Americans w/ Personal DEBT to the tune of 12$-17$ TRILLION Dollars

No one mentioned it because it’s ignorant stupid bullshit: 65% of all households are ALREADY HOMEOWNERS, duh!!! 40% of them own the home free and clear without mortgage. The rest are making their mortgage payments just fine.

Only 35% of all households are renters, and many of them are renters of choice who could buy but want to rent for a variety of reasons, including those mentioned here. The big single-family landlords are building whole new subdivisions of brand-new hoses for rent, and those are marketed to people with incomes over $100K (“renters of choice”), and that’s been going on for years, and it’s a hot thing because people are tired of overpaying for a house when they can rent a brand-new house for a lot less.

I live in a home right now that would sell for $3M at today’s prices. To buy this home would result in a mortgage payment of nearly 16k and then with taxes and insurance (not counting maintenance) the cost of ownership would come to 23k per month. The rent is less than 8k. It’s just dumb.

Hi,

We have a similar feudal situation in Kuwait. High demand – low supply (most in hands of few) – out of reach prices (avg. $1.1- 5 million)

People either rent or wait for gov. housing which takes an avg 20+ years to get.

Only citizens are permitted to own a house.