To prop up sales, 24% of home builders cut prices, others tried mortgage-rate buydowns or other incentives.

By Wolf Richter for WOLF STREET.

“Buyer traffic is weak in many markets as more consumers remain on the sidelines due to high mortgage rates and home prices that are putting a new home purchase out of financial reach for many households,” according to the National Association of Home Builders this morning regarding its survey of home builders.

Incentives: “In another indicator of a weakening market,” and a “soft market,” over 50% of the builders reported using incentives to prop up sales or reduce cancellations – more on those cancellations in a moment. Those incentives, the NAHB said, include “mortgage rate buydowns, free amenities, and price reductions.”

Price reductions: The percentage of home builders who reported cutting prices jumped to 24% in the September survey, up from 19% in August, and up from 13% in July.

Cutting prices and using mortgage rate buydowns (when the builder subsidizes the mortgage) counteract some of the effects of soaring mortgage rates – now over 6%. When the market begins to freeze over, price cuts is what needs to happen, because home builders cannot just sit on the houses they have started on or have completed. They must sell them one way or the other.

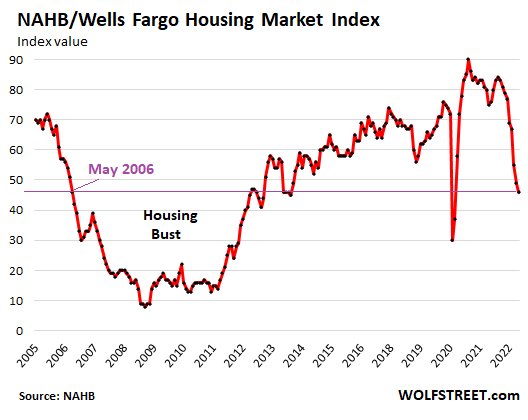

The confidence of builders of single-family houses fell again in September, the ninth month in a row of declines, “as the combination of elevated interest rates, persistent building material supply chain disruptions, and high home prices continue to take a toll on affordability,” the NAHB report said.

With today’s index value of 46, the NAHB/Wells Fargo Housing Market Index is now below where it had been in May 2006, on the way down into the Housing Bust.

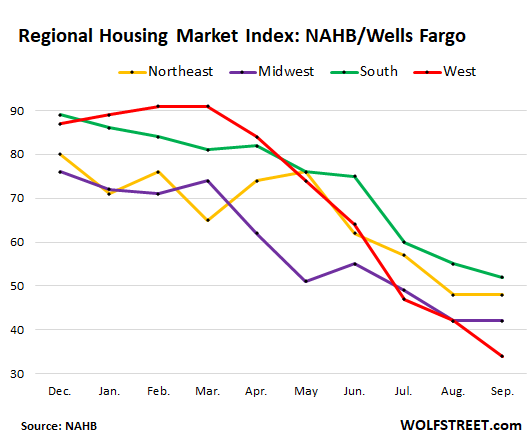

Home builder confidence by region:

The NAHB’s regional Housing Market Index plunged the most in the West (red line in the chart below), after still rising during the first three months of 2022. This is a stunning plunge from March (91), when home builders still expressed enormous confidence, and six months later, now at 34, the lowest since June 2012, as the West was coming out of the Housing Bust.

The index dropped the least in the South (green line), which is the only region with a reading still above 50, which marks the neutral line in the index. But even in the South, sentiment has been falling sharply. The chart shows from December through September:

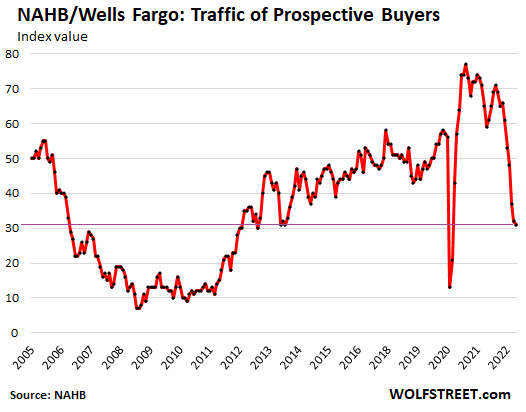

Traffic of prospective buyers deteriorated further.

The index for traffic of prospective buyers dropped to 31. Buyer traffic is a sign of interest among potential homebuyers. And many of them lost interest at these prices. Hence the price reductions and other incentives to get them to look and nibble:

The NAHB index for current sales has dropped for the seventh month in a row, to 54. This means that slightly more builders rated current sales as “good” rather than “poor” (50 is even).

The NAHB index for future sales dropped to 46, the lowest since 2012. This means that slightly more builders rated future sales as “poor” rather than “good.”

But then, what do these “sales” even mean, when 20% or 30% of those sales suddenly get cancelled?

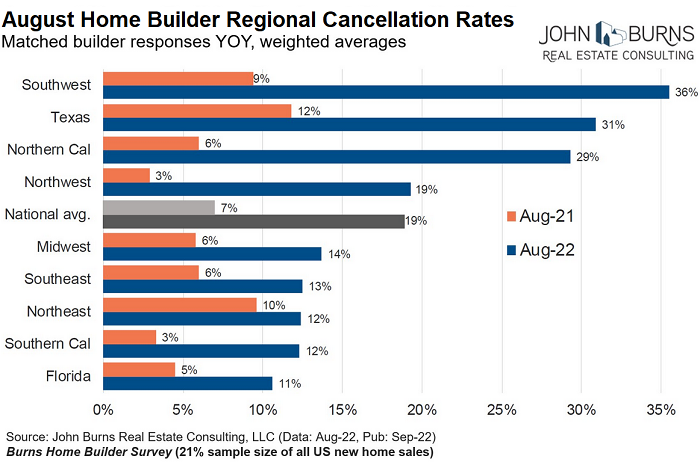

Cancellations jumped.

In the Southwest, home builder cancellation rates in August spiked to 36%, up from 9% are year ago. In Texas, the cancellation rate spiked to 31%; in Northern California, it spiked to 29%, based on the home builder survey by John Burns Real Estate Consulting. These are huge cancellation rates.

Across the US, the cancellation rate among home builders in August jumped to 19%, the highest in years, up from 17.6% in July, and up from 16.5% during the worst lockdown month, and up from 7% in August 2021 (chart via Rick Palacios Jr., Director of Research at John Burns):

I previously reported on The Boots-on-the-Ground Observations by 21 Home Builders about the Housing Market They’re Facing, also based on John Burns’ home builder survey. For example, a builder in Phoenix said: “Incentives continue to grow, with some communities pushing 20% in total discount packages. The positive is there’s light at the end of the tunnel for improving build cycle times. The negative is there won’t be customers on the other side of said tunnel.”

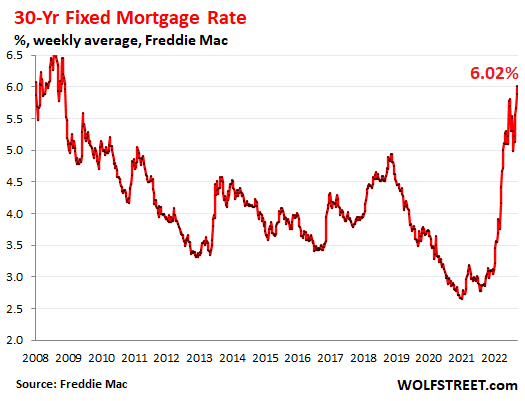

Holy-moly mortgage rates.

The average 30-year fixed mortgage rate rose to 6.42% today, according to Mortgage News Daily’s measure, which tracks mortgage rates on a daily basis.

The weekly measure by Freddie Mac, released last Thursday and reflecting mortgage rates earlier in the week, hit 6.02%, the highest since November 2008. It has now more than unwound the “Fed pivot” mirage over the summer, when it had briefly dipped to 4.99%.

“Holy-moly mortgage rate” is becoming a technical term based on what potential homebuyers say when they see the mortgage payment of the house they’re trying to buy at these prices and rates.

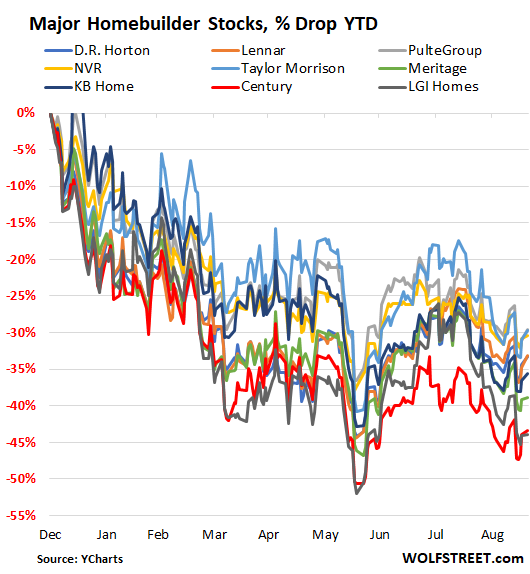

Homebuilder stocks, after the summer rally that ended in mid-August, are down between 30% and 44% so far this year (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’ve noticed that a lot of listings in Southern California are priced just under their Redfin estimates. As far as I can tell, Redfin generates then largely based on comparable sales, and any of those from June or earlier are trash. Maybe a drop in those estimates is what we need to poke a hole in seller delusion?

This will not stand! I will lower interest rates tomorrow!!!

Lol

Everyone who could buy a house has bought a house during Pandemic Fomo. Now there are only sellers and real estate agents.

Those who didn’t buy at 3% in 2020 rate have no reason to buy at 6% in 2022 at higher proce and higher risk of layoffs and price corrections.

Big layoffs have still not started as high inflation is masking the decline in productivity. Today’s 8% revenue growth = revenue decrease when corrected for inflation.

Corporations still expect aPivot, hence delaying layoffs.

GOOD

I want to buy a house because I didn’t buy one during FOMO and I need one. My attitude is this: I don’t buy clothes and things and real estate that I don’t need and like just because it’s on sale. I rather buy something I do need more expensive (even if it’s a lot more) when I need it and desire it. But alas there are very few of people like me…

During the years of the pandemic we had friends buy second homes left and right in places they never went to (like Idaho, in the middle of nowhere in FL, Tucson etc…). These are the same people that used to complain about how expensive their living in NYC was. These people didn’t move out of NYC, they managed to afford second homes by using magic investing thinking. I know at least one that used her whole Investment portfolio as a down payment. Go figure !

Now we have moved out of NYC (and not going back!) and I’m locked out of the real estate market, not because I can not afford it, it’s because what I want it’s not available. That’s ok, I can wait and I can move somewhere else again (the power of renting (!).

But my question remains, for how long can this people keep real estate they don’t need anymore (pandemic is over). 3% is still 3% on debt I pay to the bank. It just doesn’t make economically any sense, but maybe I’m missing something…

“To prop up sales, 24% of home builders cut prices, others tried mortgage-rate buydowns or other incentives.”

Until we get to 100% of builders are cutting prices, then we’re not in a real estate recession. Rather, it’s just builders still trying to maximize profit rather than trying to stay in business.

MND shows the 30YFRM at 6.42% today and there’s still not broad price declines after relatively high mortgages for going on five months now.

That should remind us all how much money is still chasing real estate. It’s like the broader economy. We’re not in a real recession until there’s broad job losses. At this point, there’s no telling if or when we’ll get to that point just like having 100% of builders cutting prices.

We are no where near a real recession.

We are for the bottom 70%.

Well, about half of that 70% owns a home, which has likely appreciated, so they are OK.

We’re nowhere near a recession overall, but housing sure is in a recession. The deterioration of the market in response to the modest increase in rates has been faster than many expected, but it’s really not surprising given the irrational behavior of market participants in recent years. The route has only just begun.

BenW,

You’re confusing a “recession” with a “collapse.” The home builders are already in a recession. But they’re far from a collapse.

Let’s make the definitions more logical:

1. Consumption is measured in Dollars and not in units for accounting GDP.

2. However society gets richer or poorer based on Consumption in units.

3. If inflation is so high that while Consumption in dollars is increasing and Consumption in units is decreasing, we are in recession on Consumption end.

4. However, real economy is based on domestic Production of goods and services and not on Consumption.

5. Domestic Production in terms of units keeps taking even big hits.

Prices have increased 50% sqft in two years, so they are still *way*ahead.

Builders are in the business of maximising profits. Why build if not for maximum profit?

The rationale is then to rather stop building than lower prices. To builders it is well beyond time to cancel new projects and building to match supply to demand.

Because they have to carry the land, ongoing overhead and sunk costs in infrastructure. It is amazing to watch a group of people sit around a beautifully polished table and believe their own bullshit. They will squeeze the subs and cut back on some quality upgrades first. The hard part is they have to keep nominal prices up. Anyone remember buyers getting a car in the garage of their new home back in the 1980s? Developers get paid to develop.

Re QQQBall, around here startup of new single family house builds are down 24% from last year.

That is, one quarter of the supply is cut off.

Interesting take by another finance blogger. He says folks who move would rather rent the original house rather than take a price cut. I have a feeling that strategy will backfire in the end.

WSJ article on exactly that today. Good luck with that.

During the mortgage crisis, small-scale investors were a huge problem, defaulting on multiple homes at a time. Without those small-scale investors, the mortgage crisis wouldn’t have been nearly as bad.

They’re the first ones to default because they don’t live in the homes, and they have no incentive to make mortgage payments when they’re under water and the rental income, if any, isn’t enough to pay the costs.

They just try to rent them out, and when it doesn’t pencil out anymore, and home prices sag, they’re outa there, and they let the bank deal with the house and the mortgage.

A real estate buddy was trying to sell a bunch of us that we should all upgrade our homes. He said first get a fat HELOC, second rent out your home. Then go and buy another house since your new rental won’t count against your new loan, since it’s income. He says people do this all the time and we’re missing out. What could go wrong? I just hope this isn’t common.

Seems to me reasonable legislation could be enacted that anyone claiming property as income producing would lose the non-recourse status (in the non-recourse states of course).

This may quantifiably change the nature of housing bubbles.

There is incredible rental demand out there, and rents have increased substantially in the last five years.

The question comes as to the financial stability of the tenants. Went through twenty applicants before finding a decent non smoking applicant last month.

This is why in the aftermath, if you were an investor (at least here in TX) you were going to pay 20%-25% down to get a mortgage on an investment property.

A perfectly reasonable policy that offers some protection for the lenders as the buyer has some serious skin in the game.

I like running rent vs buy calculations with breakeven at 10 years and using 10 year as the opportunity cost for a 20% down payment.

I ran numbers for median price $428,700.

At 3.5% appreciation it was cheaper to buy if your rent was more than $1700.

At 0% appreciation it was cheaper to buy if rent was more than $2700.

A lot depends on what you can’t know.

And…what is the true cost to build SFH (vs. “exploit ZIRP for every penny” pricing that has ruled for 20 years) or, even more importantly, what is the true cost to build an apartment?

(There are a *lot* of apartments under construction and a ginormous number at the planning/permitting stage…apartmentdata.com has a lot of metro level info).

So long as the true construction costs pencil out at these insane rental prices, builders will continue to build, adding housing supply – via apts, undercutting the insane rental prices.

(Did costs to build really double or triple since 2000, like SFH prices…I don’t think so.)

cas127 wrote that there are a *lot* of apartments under construction …

Anecdotally, that is 100% accurate here in the Western suburbs of Chicago.

Driving about, doing our thing, we are simply astonished by how many HUGE apartment buildings are going up. Most of them seem to be in suburbs close to METRA commuter stations.

I thought WFH was the big thing going forward.

I really can’t figure out how they expect to rent out all that space.

I just relocated to the Chicago burbs from East coast…I just renewed my 3 month lease at a discounted rate. I am talkative to the management here which oversees tons of buildings and they admit demand has fallen off a cliff.

Try running the numbers for negative appreciation.

Home prices can never go down 😀

Jon,

Housing always exists on a “permanently high plateau” according to real agent agents, as they wave their hands and say, “this is not the crash you are looking for…”

I have noticed on my daily walk that several for sale signs have flipped to for rent signs. I have also some become AirBnB listings.

In Calistoga, Napa Valley CA, I see six luxury apartments that were recently completed now offered for lease. They were for rent for $5,000 a month previously.

“I have a feeling that strategy will backfire in the end.”

That strategy could work if home prices don’t drop too low and for too long. On the other hand if home prices drop and rental rates drop, the strategy might not work too well. The way things are headed you might be able to make as much money from a 2 year treasury as you could from a rental property, and without all the stress and work.

We’ll see if the new landlord class has cast iron colons when SFH sales start going off at 30%-60% off peak prices.

Ditto, when 25k new apartments open up in their metro this year/next year/year after that.

Thanks Wolf for this analysis of the report.

OF COURSE…. from CNBC this morning….

———————-

Homebuilder stocks moved higher on Monday after KeyBanc double upgraded the sector to overweight from underweight. Analyst Kenneth Zener said that homebuilders, which have underperformed this year, tend to rebound sooner and more sharply than the broader market. Shares of Lennar rose about 2%, while D.R. Horton gained over 2%, and PulteGroup jumped nearly 4%.

————————

OBVIOUSLY, the bottom must be in, after all KeyBanc “DOUBLE (secret) UPGRADED the sector.. lol

Hahaha, yes, and they’re still down between 30% and 44% YTD. According to the Wolf Street Mug Dictum, ” Nothing goes to heck in a straight line,” as you can see from the chart.

Never trust these banks/firsts/analysts. They have been wrong many times and have absolutely no clue about the market.

They are not wrong, and they know all about their markets. The people who pay them tell them to lie and they do. Quite simple.

Exactly, they are farming their market and their market is you and your perceptions.

I agree. What I meant is: Don’t trust what they put out. They are like realtors :-)

They actually have a clue. They know. But they have to be dishonest and play the optimism game to get the paying gig.

Cold winter ahead I guess. So says the farmers almanac at least. Wonder if they were talking about housing?

Local market here had an explosion of inventory at high prices. New listings have stagnated in the past month or two but inventory isn’t shrinking very much. Nobody is buying, very few are listing after the initial rush. Price cuts are common but very small. Prices still incredibly unaffordable for the local area.

Another interesting point: The local DMV and licensing agencies for both states here on the border of two northwest states have no lines for appointments for new out of state residents. It used to take two weeks to get a license changed. Not anymore.

Anecdotal evidence things are sort of on the right track at least.

“Incentives continue to grow, with some communities pushing 20% in total discount packages. The positive is there’s light at the end of the tunnel for improving build cycle times. The negative is there won’t be customers on the other side of said tunnel.”

That’s a great line! And is reflected in the third chart above: Traffic in Prospective Buyers. What a plunge!

Astounding times. Better buy now, there’s obviously little competition!

And the customers who purchased in the last 12 months are gonna be pizzed they didn’t get the same deal as the newbies!

I’ve been waiting since April for XHB to tank – and it stubbornly refuses to drop much below 60.

I think when it finally breaks it will be a waterfall, just like the junk bond etfs. Just have to be patient and short any crazy pops.

In my local I saw a ~2 acre lot with pad and water meter, looked like they were going to build but its for sale with a price cut. Looking at the price history, they bought exactly a year ago for 2x what the previous buyer paid just 2 years earlier. Even with the cut they’re asking 100k more than they paid but the reality is theyre going to have to cut at least 100k below what they paid to move it. And they’re out of state :) Ouch!

There was certainly an effort put forth by the powers that be to reignite the housing bubble and to amazingly make a house in Boise worth nearly as much as one on the coast.

All of the institutional buying that went on, it wasn’t like they really needed the used houses-but it propped up markets and buoyed them so.

Short term rentals didn’t exist in the 1st housing bubble, and if i’m a would-be Hilton and see the market going south on my rent out pride and joy, i’d want to maybe exit stage left and beat the crowd. It isn’t even as if you have to do all that much to get it ready for market, and what if a bunch of AirBnB types all got the same idea and inventory grew as high as Jack & the Beanstalk?

AirB&B rental owners are facing that now and they jacked up their prices to the sky. Similarly we see a high demand in the Hotel reservations, this year.

But same as restaurant that was packed last year, and no one is considering to seat in empty tables these days, the hotels and AirB&Bs will be suffering next coming year. I believe this is also a temporary demand. You will see a lot of inventory and high prices next year, at a time that inflation already wearied out the consumers. Basically no customer at the end of the tunnel. Next year is going to be ugly.

You would be surprised at how often those Airbnb’s need to be occupied in order for it to cover costs. One of my family members says if they have it used 1/4 of the month by renters it breaks even. Don’t expect a big rush of inventory.

Kurtis, you’re making the same mistake everyone else does, forgetting that each problem in the economy doesn’t happen in a vacuum. Your family member’s statement might be true, but that assumes an economy with healthy vacation spending. When people start losing jobs, they cut back on spending. Heck, even the people who haven’t lost jobs cut back on spending. So the days of people spending $500/night at an AirBNB could easily be over.

Also, while that 25% math might be true in places like Miami Beach, Greenwich Village, and Honolulu, there are many places where the nightly rentals aren’t nearly enough to cover fixed costs unless occupied for much more time than that.

Not to mention that many municipalities have banned or heavily restricted these types of rentals.

The point being, buying a property intending to use it as an AirBNB property for 30 years is a risky endeavor.

I have taken big steps to cut my expenses.

First one to go is big expensive airbnb rentals and expensive vacations.

Things are gonna get much worse and we’d see how long these airbnb stay afloat

home prices need to fall at least 50% or so to be affordable.

With the monthly payments now that mortgages are at 6.25, maybe not that much. 20-30% is probably more correct.

Mortgage rates are at 6.25 today.

Unless inflation goes down big Time

This won’t be the case next month or so

Paul Volcker is J Powell’s new hero. Look for fixed mortgage rates to go up to 18% like they were in 1981/1982. Variable rate mortgages will make a comeback as an alternative to the nosebleed levels of fixed mortgage rates. Half or more of the builders above will be going bankrupt. Blackrock will be warming up the Bullpin to pick up the pieces.

ENJOY!

“Look for fixed mortgage rates to go up to 18%”

Not going to happen SC. The Fed is targeting disinflation, not obliterating credit markets. Inflation is bothersome to the Fed, but their worst nightmares are #1 deflation and #2 a credit freeze. Our economy is now so thoroughly built upon debt that 18% interest rates would bankrupt a huge number of businesses small and large, cause massive deflation in asset prices, plunge us into a new great depression, and would also make it a challenge for government to pay for new debt moving forward in the face of decimated tax revenue.

Besides, the Fed doesn’t need to run particularly high interest rates… They have trillions of anti-dollars to deploy in the form of QT, a weapon Volcker didn’t have. They’ll pause around 3.5%-4% while erasing tens of billions per week from their balance sheet until something breaks. When something breaks in 6 months, or a year, or whenever, they’ll back off fast.

“Our economy is now so thoroughly built upon debt that 18% interest rates would bankrupt a huge number of businesses small and large, cause massive deflation in asset prices, plunge us into a new great depression”

Nah, it would mostly hurt large corporate debtors with variable rates and interest only loans that have impending balloon payments. It would cause massive deflation, no doubt. And that would create new opportunities for the little guy to afford to survive eith a family.

GIven the concentration in asset ownership, particulary in financial assets, I don’t think the little guy would feel much from 15-18% rated except the awareness that there be deals out yonder for earners with savings. You know, like it always was and is supposed to be.

Nah? An 18% FFR would affect all kinds of things for the little guy. Credit cards would become a huge risk. It would wipe out homeowner’s ability to borrow against equity that would evaporate as house prices get crushed. It would make car loans unaffordable. Opportunities for the little guy would be great, but not useful if the little guys are all unemployed after credit markets undergo cardiac arrest. As we learned in the last financial crisis, a lot of companies of all sizes can’t even make payroll in a credit freeze because they rely on credit for even their day to day operations. An 18% FFR ain’t happening in our wildest dreams with anything short of banana republic flavored hyperflation, and we’re not anywhere near that yet. 18% would actually be a death blow… There’s just so much more reliance on huge debt now compared to 1980.

Very hard to believe they’ll pause below 4%. Even if they do, rate sensitive markets like RE are already crumbling.

Rate sensitive markets already crumbling indeed. Exactly why they’ll pause. A pause has been mentioned several times by Powell, the Fed governors, and the minutes for a while now. The idea is to allow for the known lag time between the tightening of monetary policy and its desired effects. Coupled with QT, cracks in the system are showing up fast. Everybody is focused on interest rates while the Fed destroys tens of billions per week in QE-generated liquidity. They don’t need a high FFR because they have a huge amount of anti-matter to pump into the cancerous mass that they created. If the last round of QT is any indicator, something is going to break, probably credit availability, and probably sooner this time. And when it does (months, a year, etc.), the Fed will tuck tail.

Every indicator is red, inventory, price drops, days on market, number of sales, active listing, bla bla but sale prices of comparable homes are barely budging. I have been tracking South Bay Area price trends and I can assure you that sellers are not giving any deals. On paper you may see some price decline but thats because price is skewed by higher sale volume of compromised homes, likes those with weird lots, those on busy streets, those with plumbing issues, those with bad schools, those on bad streets, those in tier 3 cities, etc.

I have not seen a comparable home selling for more than 10% below the all time high in April. Sellers will just wait it out. Between home sellers and buyers and Fed, sellers will just out wait everyone else. So do not hold your breath for huge RE deals. If you do not agree with me, show me any good homes in a tier 1 city in good neighborhood that sold at more than 10% below a comparable home sold around April.

“I have not seen a comparable home selling for more than 10% below the all time high in April.”

Here’s part of the South Bay. Santa Clara County. Median Price, single-family houses, $1.65 million in August: -5.2% from July, fourth month in a row of declines, -15.4% from peak in April, -0.3% year-over-year:

https://wolfstreet.com/2022/09/16/california-housing-market-dismal-sales-prices-sag-in-san-francisco-20-fr-peak-silicon-valley-san-diego-orange-county/

Wolf, being from SoCal, when I read Kunal’s comment I thought he meant the South Bay cities down here. It makes sense you thought South SF Bay. Not really sure what area he meant. Perhaps he always talks about the SF Bay Area and I just don’t remember. Regardless, Kunal needs more patience, sellers have lives too and often can’t “just wait it out.”

OK, thanks, that explains the confusion of the otherwise un-confusable “jon” (his comment further down).

Kunal has been around here for a long time, a well-known figure, if you will. He always means the San Francisco Bay Area. Often he is very specific — as in “San Jose.” So we know.

@Wolf,

re “Santa Clara County. Median Price, single-family houses, $1.65 million in August: -5.2%”

is that “Median Price” really representative of market price decline? I mean, how do we know it is not more sales at the low end and high end sitting, or all/most of the declines at the high end vs mid/low end (which is the most common case in the bay area)?

1. It’s -15.4% from April.

2. It’s the median price – I explained a gazillion times what a median price is. There is no such thing as an absolute “market price” in real estate. There are different ways of estimating price movements.

It could very well be that the high end is still selling, because buyers in that realm still have money and don’t have to rely on mortgages, but that the bottom end is not selling, and that therefore the mix has shifted, thereby skewing the median price up. In other words, the “market price” that you mention might have declined by 20% or more, if that’s what you mean.

Definition of cognitive dissonance

: psychological conflict resulting from incongruous beliefs and attitudes held simultaneously

Examples of cognitive dissonance in a Sentence

“I have not seen a comparable home selling for more than 10% below the all time high in April. Sellers will just wait it out. Between home sellers and buyers and Fed, sellers will just out wait everyone else. So do not hold your breath for huge RE deals.”

Clearly Mr. Kunal would fit in perfect someplace in the DC Swamp!! Just pick a color, Red or Blue, and go for it

LOL- when have we seen this before?

AirBnb crash dead ahead!

Ok, then we watch everything slide 35% down, and so many people will continue to pay their mortgages, because a new house will have the same monthly payment as their underwater castle.

That is going to be the hard part- higher mortgage rates are going to be a housing killer, no matter what.

Until wages rise, or enough cheap houses miraculously appear in tight markets. I expect rents to finally soften next year. A bit. The high end will continue to be expensive, because finance will take a much bigger bite.

Now in resort areas, the airbnb crunch is going to be much more damaging.

Someday this war’s gonna end…

Factually, Kunal is right.

I see lot of red signs but no meaningful price decline as such.

A 20% or so real decline in home prices wont any dent materially when the price increased by 50% or so in just last 2 year.

At the same time, my feeling is: home prices need to crater. I have been wrong many times before though.

Also, in California, especially in coastal CA, real estate is like a religion hence I can relate with Kunal’s feeling as many of my friends feel the same i.e. come what may real estate in CA can’t go down as we have limited land, lot of rich people, every one wants to live here, year round gorgeous weather etc etc.

Home prices move slower. We need to revisit this thread after a year or so.

“Factually, Kunal is right.” Well, no, duh. Wolf just showed clearly, with boldface print, Mr. Kunal’s “haven’t seen anything drop below 10% since April” to be an alternative fact (also known as an untruth). Maybe Kunal has a special talent where he puts on blindfolds very quickly, as necessary, and makes that work for him. Driving with blindfolds on can be dangerous though.

jon,

“Factually, Kunal is right.”

No he’s factually wrong. I just gave you the numbers, including a chart.

“I see lot of red signs but no meaningful price decline as such.”

I doesn’t matter what you “see” in San Diego, where you’ve been saying you are. Kunal is talking about the “South Bay” — meaning San Francisco Bay Area’s southern part. AFAIK, it still doesn’t go all the way down to San Diego.

“…everyone wants to live here …”

Everyone wants to be a comedian.

Last time I checked, ~30% of homes in my area of interest had price reductions. My guess is the average drop is around $30K, but I’ve found a couple with $400K reductions (>25%). I’ve bookmarked them b/c I’m interested to see what the final price will be.

North County San Diego 3500-4K sq ft tracts homes selling for $2.5 to low $3 mil range in the spring are now closing at around $2.1 mil. Even throwing out the top $$ $ 3 mil+ sales of buffed out primo properties, you are still left with spring sales in the $2.5 mil range now closing at $2.1. You do the math.

Not surprising. That’s a huge annualized rate of decline, and it happened during the summer. It’s amazing that there are still deniers out there given how quickly this is happening.

Renters collapse imminent. Guaranteed by Powel. You do know the ramifications of that.

Real estate prices can be sticky. For the time being price cutting is still modest. I was positive the crash was coming in April 2020 and then the market took off like a rocket ship. I was a fool. It makes me more humble about predicting the future. It may take layoffs and forced sales to bring a measure of realism to the sellers in this market. Meanwhile expect that a lot of denial.

I was right there with you in 2020. I was on the sidelines with a bunch of cash ready to start buying used boats, jet skis, cars, you name it. I failed to predict that the government would just print a bunch of money and bail out all the people that have always lived beyond their means. I wasn’t raised that way and now I’m the fool.

No one hits a home run every time they step up to the plate. Catch the bargains on the next dowturn.

The Fed is trying to avoid a crash by engineering a controlled demolition. Is it time to pay the pandemic piper?

Don’t feel bad. Markets have been manipulated so long that they are ruled almost entirely by irrational expectations, aka hype at the margins. Wait, earn, and buy when you know you are getting a steal.

I made the same mistake for years expecting fundamentals to matter, like i was taught, in markets deliberately separated from fundamentals by powerful kleptocrats with the ability to create unlimited credit with no accountability and a propaganda machine like the World have never seen backing them up.

I was about to buy a renovation ready house in my neighborhood for 120k in late 2019. I work in the trades and have done this for years. One of my retired know-it-all neighbors, an engineer, jumped in at the last minute and offered 150k. He proceeded to overimprove and put 200k into the house, a house which would not have sold for more than 325k. I was ready to let him learn a lesson and take a bath. It hit the market mid 2020 and went for 425k. He stepped in s-&t. He then bought another piece of land and built and average house, probably for 400k, which sold for 550k. Those new prices are in line with what all houses have done in our town, which has become a nouveau retirement favorite in the last 3 years, unfortunately. This jack&#s, who never could have made squat pre-pandemic, gambled a bunch of his retirement funds, and now thinks he’s a builder, and has a couple hundred thousand more to show for it. Until that money and thensome is wiped out of the economy, inflation will not slow down. People like me, who thought we learned something from the last recession, now look like fools for sitting on the sidelines.

My only hope is that asset prices crash so hard that the winners of this inflation mania get hurt so bad that they voluntarily leave the housing market for good. Personally, I think the Fed has a major political problem with inflation and it’s going to have to get ugly for them to solve it.

Dave, it was the same during HB1, as I gather you recall. Things are turning really quickly right now, maybe even faster than last time, and this time the fed can’t bale out the parasites. They will get crushed unless they’ve already cashed out.

Thanks, Dave – for illustrating & articulating just about perfectly the frustration Ive had with being the doofus who opted to save & hold off buying anything the past few years.

Back in ‘18, I knew a bartender who was going around hat-in-hand to solicit family members — some estranged — for help with a modest down payment for a 90 year-old, 900 sq ft shanty in Lockhart TX she was trying to buy for under 200K. I didn’t discourage her, but I think my advice at the time was to just keep saving. Well, she just sold it a couple of months ago for nearly 400K. Couldn’t have happened to a nicer gal, but I use this to illustrate that there is likely a lot of such lucky money out there sloshing around. Maybe it never boils away and we have a *new* generation of nouveau riche, which keeps prices elevated, but I tend to doubt it. Free money tends to have an evaporative element built-in.

So many products tied to real estate cash flows. No idea how that’s going to turn out locally or globally because inflation with higher interest rates has kicked in. And explosion in housing prices just prior.

Everything bubble!

Seems odd that only 24% of builders have cut prices. IF they don’t cut prices, houses won’t sell. They’ll have to lay off employees. They’ll lose relationships with contractors. And…..they’ll be sitting on inventory, watching it decline in price.

The last house I bought was from a builder that kept prices high for too long, then suddenly gave me a fire sale price amid rumors he couldn’t make payroll.

Yes, but as the article says, over 50% are offering various incentives.

If I was a shopper in this market, I would demand a price reduction instead of the incentives because property taxes (everywhere that I have lived) adjust to the sales price and gradually go up from there.

Of course, I ain’t shopping. Just sayin’…

Right now it’s not so much about home prices and how much they are moving. Rather, it is about declining transactions and how they are going to affect the economy. The economic decline will then spiral back in and affect housing.

Mortgage brokers are already being affected due to rates – both purchase mortgage and refi. Where do they go to replace that boom-time income?

As RE transactions decline everyone in the commission line is affected.

Eventually, RE agents will find themselves out of work but not qualifying for Unemployment insurance (no PUI benefits this time around). Agents will eventually be the cheerleader for lowering prices in order to get the transaction through.

Construction workers as new projects are canceled.

Anyone else that is tangentially hired or provides supplies for an active housing market.

The list goes on.

Just the month of August in greater Nashville was down 673 residential sales compared to the same month in 2020 and 2021 or about $ 19 million in commission flowing back into the economy. July was similar.

Nashville used to be the hidden gem of the south. Fantastic place to live with zero state income tax.

But, the population has exploded in this century and the infrastructure cannot keep up. It’s a logjam now.

Times they are a changin’

Mortgage rate buydown: Seems to me this is a purchase price discount that the seller passes to the mortgage company instead of the buyer, so as to maintain the fiction of a higher sales price.

This is fraud, IMO. How can this be legal? Does FHA, FNM, FRE allow this?

this is a very common practice.

Last thing builders would do is outright price cut. They want to disguise price cuts in many ways: free upgrades, buy points, etc etc.

But if I am wise buyer, I’d ask for outright price cut which is lower basis for property tax.

We just had a hold placed on an order for 15 homes in the Denver area, as a supplier. This happened last week, and is our first.

Also, I’m noticing For Lease signs for Industrial space where I didn’t before. It might be that I’m just being more observant.

1) Higher rent/ more evictions. New evictions and 6% mortgage rate might dislodge owners rent.

2) Dislodged tenants and millions of new “comers” might dislodge sticky wages.

3) Yahoo : between 5M and 8M tenants might be evicted within a year.

4) After fixing it, legal, and commission, millions vacant units will come to the market.

5) Inflation backwardation : the current inflation is higher than the front end of the yield curve, but future inflation is lower than the long duration. The CPI Y/Y, next year, might be : (-)6% with 6% mortgage. US 1Y is higher than every other rate.

6) Rotation : Santa Clara median prices down sharply, but the flyover RE is up.

7) Builders sentiment is so low, MSFT breached June low……

This is like the department store that “lowers” their price 15% after having raised it 100%

Nothing is cheap yet. You have to wait until April to get a deal on down jackets. Builders are still fat and happy to sell at these prices. Another 250+ basis points in fed funds and we might start seeing some deals … 2024 maybe

And if you’re not buying or selling, it doesn’t matter anyway. I could sell my house for 6x what I paid for it but I’m not moving, so who cares what “book value” is.

Is there info on the average size of homes being built (or perhaps not, as it were)? As a sidelined buyer, it’s driven me bonkers there are no sanely-sized, 1,200-1,400sq ft 3BR, 1-2 bath homes that aren’t 60+ years old and decaying. Its either those, or $600k+ starter castles, although I can’t tell if this is a local problem.

Yes there are the zoning laws and nimbys, but its also been reported that builders make more profit off a handful of these suburban palaces than putting in a full qiaint neighborhood of smaller homes. Given builders are losing customers, wouldn’t it still be more profitable to put up functional-sized homes for the masses desperate for basic home ownership instead of not building at all? Or is the country really that hell bent on three-story vaulted ceilings and 3-car garages to (not ironically enough) park their EVs in?

Few people want to buy a house that size.

Apple, if you build it, they will come. Plenty of side lined millenials are fine with a normal-sized home, or a starter home if you please, if it means actual ownership. For a generation painted excessive, many of us prefer lower utility bills, less maintenance, and less excess. Its seemingly discouraged to not want a giant eyesore full of useless junk.

Michael, perhaps ‘they’ are changing the system by not paying top dollar for McMansions. One can hope.

Lily Von,

instead of crying they should innovate, change the system.

1)Instead of crying

2)They should innovate

3)Change the system

@Lily – me too. The high land costs dictate larger homes. retirees are faced with a condo (hell no!), too-big newer home or an older, smaller home. a nice 1,250 SF to 1,600 SF 1-story newer home would suit the bill nicely.

“The typical American home being purchased these days is 1900 square feet in size and has three bedrooms and two bathrooms. As of December 2020, according to a study of the mid-Hudson counties by Pattern for Progress, the average size of all homes built in Ulster County since 2015 was 2245 square feet. Except for a paltry few government-assisted units, the small amount of new housing being built has been for the upper end of the market.”

– article from this week found in local paper HV1. Answered my own question, locally anyway. If I sound bitter, you must see the giant houses currently being constructed here, well over 2245 sq ft and tacky as sin in what I suppose is a display of opulence or HGTV trend (suburban farmhouses dime a dozen). Wouldn’t mind these folks having their big, fleetingly popularly-themed homes if basic starter homes were an option, but thanks to these folks and their builders, starters are not an option at all, for anyone.

The land is too expensive to build smaller homes.

I have had 2 sellers back out in so many days on RE deals. One was waterfront other a super desirable location fixer-upper. Dont care except affordability on those myself. They were to live in.

I think the main issue in housing is that for many sellers, they have 2-3% interest loans, and are wise to the fact climbing up the property latter right now will murder them on payments. So until prices are down from today at least 20% they have no threat of negative equity.

I think the economic secter is having its own sort of stagflation. Little movement/ growth and increasing cost.

The builders are pinched because unlike eatablishes housholds they HAVE to sell.

The fix will go in, so it will be funny money bailouts by way of stupid loans; the only way i see a big true correction is either prices drop enough to budge sellers even at high mortgage rates (so price goes down so much that 7% no longer hurts and staying put hurts. Like 40% or so) OR and this is so contrary to the system design… New houses start to out compete old ones on price.

But here in Easton PA the prices are up way over 25%. So even a 30% correction won’t budge them if interest rates are only 6% or so. And the baseline dollar is inflating.

Sellers wont care they cant sell easily unless they really really have to.

Renters collapse imminent. You do understand the ramifications of that. All those fake jobs(pandemic boom) the media and such purport will be vanishing. Giant liquidity squeeze imminent. Investors in denial thinking renters will always be there. Layoffs took em down in 2008, and it will that way go again. Imho just a tad slower as this time 3x more wealth to milk down. None of the R.E. bubble has any sustainability to it. None.

There isn’t 3X more wealth. It’s fake like the artificial economy and from the same source.

Last time the proximate cause was mostly mortgage credit. This time I’m placing my bet on corporate credit and sovereign debt defaults.

Junk bonds highly correlated to stock prices too. When stocks take a big enough hit across the board, job openings at public companies will not only evaporate but large scale layoffs with it if the decline is big enough.

Homeowners who tap equity early may “milk their wealth”. I do agree with that but much or most of their financial asset wealth will disappear. Still also looking for more mortgage forbearance and foreclosure moratorium again if it gets bad enough.

Very odd post. It’s normally hard for sellers to back out where I’ve lived. Also, this is another one of those wacko rationalizations in which it is assumed that the sellers can always choose to not sell. Sales happen for many reasons. And it is only transactions that determine valuation. If your neighbor decides to sell, your house value is affected, and you have no control over the sale price.

Lots and lots of comments above on rent ramifications from this collapse of the sales market. Did these people just flat out back out of the market or are they waiting to see what prices do? Seems if prices go down but interest rates continue to go up the payment would be the same. My suspicion is that they’re gonna continue to rent for a while and the rental market will stay tight. I suppose if each market (sales and rent) collapse, then they’ll come off the sidelines and buy, but one has to wonder how far prices can fall given all the trillions printed in the last two years. It’s not like they can unprint the money.

The rental market will stay tight until employment weakens noticeably and that’s coming later.

Rents are ridiculous in much of the country and not much if any more affordable to many Americans without an artificial economy either.

QT should pull excess out

“It’s not like they can unprint the money.”

—————————————-

They claim they can do exactly that with QT.

1) Suppose the housing market will not deflate. Innovative builders will

assemble new houses like lego instead of on site. New apts/ new SFH targeting entry level customers. Making money by selling starving lower income people without commission and in a more efficient way.

2) If the next 10Y the average house will rise from 430K to 500K it will appreciate at 1.5%/y.

3) If the average inflation rate in the next 10 years will be 3.5%, the

average house should cost 600K.

4) Seinfeld Motorola cost 3.5K in the 90’s, new IPhone 1K in 2022.

My guess is you’re wrong. I think smaller

homes would be extremely popular with singles and couples w/o kids.

I sent a letter to the city housing planning department where I live in Eastern Washington detailing a subdivision of modest sized homes, 700 to 1200 ft².

I put together estimates of costs: land, land prep, house structure, etc. I mentioned that I wasn’t very knowledgeable about such things. But what did he think ?

I never heard back. When I called later I basically didn’t get any useful info.

A manufactured housing rep told me in spring 2021 they can’t build in Spokane County because of zoning restrictions.

Its not the 1% that bother me Bernie.

It’s the middle class and upper middle class especially and their influence on politicians and other businesses.

Age old story.

These same people will then

Whine about sprawl.

I’m in eastern Washington, mid sized cities here.

Most new construction, detached single homes has been in the $400k to 650k range from what I’ve seen. Mostly 2000 to 4000 ft².

I just would have liked to see some new construction subdivisions in the suburbs go for 200k to 350k, much smaller homes, small plot of land, no frills but quality. I’m pretty confident some builders could have done it profitably, but they wanted greater profit (yet) building bigger more fancy homes. Yes I know the land is expensive, but again I did a little research and I believe it could have been done. But all emphasis on maximizing profit to the exclusion of anything else. Interesting eh.

As others have said, no starter homes for the lower middle class… all used homes on the low end are sold instantly. Not many available to begin with.

As for sprawl, I’m no expert on that. I’m sure there are valid concerns there but NIMBYism is part of it too.

I blame politicians left and right as well as builders. Its been laissez-faire and we’ve seen that some segments of society haven’t faired so well… this is dependent on where you live of course. I live where many west coast transplants have driven up the price of homes considerably for about 6 or 7 years, last two especially. Naturally, existing homeowners complain about the influx (a little) all the way to the bank.

We now are having wildfires here (Washington state) and surrounding states ((Idaho, Oregon, B.C) consistently August and September… quality of life issues.

We only average 15 inches of precipitation here annually so drought concerns are starting to get a little more real here though no where near as bad as California, Nevada, Utah, Arizona, and I guess even Texas this year. I’m sure some folks are moving to the Northeast, South or Midwest.

Most places east of the Mississippi River average 35 to 40 inches of annual precipitation. Canton. Ohio about 40, Atlanta 49.

As mentioned in Eastern Washington we average 15 to 16. Seattle is about 36 to 37. Olympia, the capital 49.

Richland in South Central Washington state only 8 inches annually. That is not a typo. Check it out at Wikipedia or elsewhere.

One last update !

My reply should have said:

“east of the Mississippi River average

35 to 50 inches precipitation annually,” not ” 35 to 40″. Most cities in Tennessee for example are 40 to 50 inches.

The plain states maybe a little closer to 35, I’m thinking Nebraska.

For me… I like a dry climate in Eastern Washington but no free lunch. Wildfire concerns now quite real. Idaho has had a ton of fires this summer.

Counted over 50 a few weeks back per Air Now website.

We all know what AQI stands for here that is sadly true !!!

Air Quality Index.

Back east, grew up in Ohio, nice rain and thunderstorms… but humidity is the price one pays. Occasional flooding in some areas no small thing either.

Trade offs indeed.

This year’s fire season was nowhere near as bad as 21s or 20s. Even in Montana which seems like a smoke collator only had a very very smoky days. Last year it was smoke walls from July to October.

But yeah, Spokane and the surrounding area, especially Idaho are completely detached from what the local economy can support. But what place in the US isn’t? Duluth, Minnesota? Detroit?

When I lived back East it was county ordinance for most counties to limit new houses to a minimum of 1600sqft, some kind of masonry facia for the front of the house, and minimum lot sizes of 1/4 acre or more. There won’t be anything affordable with those being the minimum requirements paired with a speculative market. Unless the speculative bubble bursts. Then you can get a shotty built mcmansion that’ll be a teardown before the mortgage is paid on the cheap.

Something that surprised me when looking at houses in the Spokane area is how terrible the new construction is. It has had every corner cut and every expense saved to just meet building codes. No trim except base boards and doors/windows. No return vents for the central air. All the walls are gross spackle popcorn off white to hide garbage sheetrock work. Vinyl “tile” in the bathrooms and kitchens. A tiny section if hardwood floors in the foyer. All the cabinetry is apprentice grade work. The second cheapest carpet option you can find at home Depot with minimal padding. Etc. All for 1.2 million on a 1/4 acre lot for a 1500sqft single level. And people were getting into bidding wars for this trash.

Of course if you want to buy anything under 400k in Idaho your options are trailers with 400/mo minimum lot fees or Early Clyde’s prepper shack that’s off the grid and you need a dog sled to access it 6 months out of the year. All for the low low price of 325k. Don’t all bid at once! If there’s one thing I’ve found, it’s that Californians who hit the housing bubble lottery are easy come easy go with their spoils when they move.

I was looking at the similar issue purely from the buyer’s perspective when I was in the market for a new build – here in NC my builder was offering 8 or 9 possible floor plans. The cheapest ~1900ft ranch started at $310k back when I started looking, while almost 3000ft 3-floor 5BR 4BA house, probably the biggest they could squeeze into a 0.14ac lot, started at $340k. For the price difference of less than 10% it was a no brainer for me.

That said, if they started offering 1000ft houses for $150k or even $200k back then, I would probably look at those, but something tells me they would’ve slapped a $280k price tag on a tiny 1000ft house making it a very strange choice given other alternatives.

Discounted new homes killing 1-2 year-old resales.

Based on the trajectory of mortgage rates north of 6%, it wouldn’t surprise me to see a relative burst of buying in the next month or two as everyone who rate locked 5% tries to snag a home. November into the holidays the impact of sustained higher rates will be more apparent (esp if they hold above 6%) and will likely lead to a total collapse of sales volume. A family member of mine just sold a house with 35 interested buyers and 11 offers (mid 300k price point, which does exist in NH). Likely the final mini-surge before higher rates force the housing market into a prolonged winter hibernation.

Here’s a email I received this morning from a builder here in Utah:

“Join us for a fun taco night event hosted by Pax Home Loans this Wednesday, September 21, from 5 to 7 pm at the Orchard Heights model home.

Tour the beautiful model home, preview quick move-in homes, and enjoy delicious tacos on us! Ice cream sandwiches and beverages will also be provided.

$12,000 back to school promotion to be used towards closing costs and free window blinds now available!”

If they throw in a free tank of gas I might just drive up there to kick the tires

now this is how you beat inflation, dinner and a free show. drive 65 and heckle the comedians.

You can buy a portable sawmill for $5000, cut your timber on your own land (close to free), and build your own house. Let’s say it costs $125,000 for ten wooded acres. Homes cost $400,000 now. Does it really cost $200,000 in labor to build a 1500 sqft home? What am I missing?

Plumbing,electrical,appliance hvac roof,the list goes on

Insulation, gutters, drywall, paint, dirt work, permits, concrete, garage doors, septic, windows, doors and trim, flooring, carpet, cabinets/counters….

“Does it really cost $200,000 in labor to build a 1500 sqft home? What am I missing?”

NO, absolutely not. It costs way MORE than that unless you build a shack, or cobble together a mess of cheapest possible junk components.

Depends on SO many factors, but especially how good a skilled manual laborer you are or can become quickly for the various trades needed.

We started with 1000 SF cabin for our previous home in ”flyoverstan”, gradually built out to 1800 SF ”heated” then added decks and porches to end up with 2500 under roof.

Cost of purchased materials was about $50K, ”paid labor” over 10 years about $10K, hours of labor by us and family about 1,000 hours—just for house construction, not counting greenhouse, sheds, fences, gardens, etc.

We were paying 40-60 cents per board foot for lumber, $80/CY for concrete, $2/SF for metal roofing, so your experience WILL be different, at least for now.

Dems was the good ole days, VVNvet. Must have been fun, sort of, to build it.

To PilotDoc, well done. Depending on the state, apparently not TN, you can be down $30k just in city/county fees for even the smallest house (sky is the limit for larger). Throw in another pile of money for the architect, structural engineer, civil engineer, survey, soils report, etc. Just school fees are $5/sq ft+ and in our area the parks/rec charge is around that. Water meter $15k+. It all adds up.

Middle TN. Son just moved in Friday to the home we built him. No land cost mind you, I gave him 1.5 acres. 1800sq ft home, 3BR, 2 BA, extra large utility room, no garage (will add free standing shop later), shingle roof, metal siding, granite counters, vaulted open floor plan…beautiful. We contracted it ourselves and got it done for $190k=$105/sq ft. Not bad even with lumber and electrical tripling in last 2 years. We painted and did the flooring and trim work ourselves.

As a comparison, 3 years ago we did the same for the other son. His was a 3br, 2ba all brick 1600 sq ft home with a 2 car garage. That was done for $165k.

I know a lawyer in San Diego who’s practice is now nearly all evictions. San Diego has an eviction moratorium for people who claim they can’t pay rent due to Covid-related financial problems. Property owners are going to battle to get these people out, this guy says he is overwhelmed with cases. Obviously there is an ongoing shortage of rentals due to all the deadbeats who are not paying rent. Eventually these people will be cleared out, perhaps all the way out and into another state or region.

RE values are coming down, rents will be going down, job openings will be going down and income will be going down. Oh and the stock market will be going down further. Brace yourselves this is only the beginning.

A few days ago I finally saw a post in one of our local FB groups (NC) – a lady told that she had signed a purchase agreement back in June (aka almost at the very peak of the market), made a huge deposit and is now watching her builder offering massive discounts to new prospective buyers YET still massively delaying her build (with estimated completion of “some time in 2023”). She was wondering what she could do, especially if discounts keep getting better and better.

She didn’t mentioned the specific location or a price point, but judging by her previous posts, she was looking at houses well above median price (close to 1MM which is … quite a lot for this market even by mid-2022 price standards).

It brought me back to my usual thoughts that I have every time walking around our actively developed community in the evening – back in 2020 I signed the purchase agreement when prices already started to go up, but were still within some reason. Then massive construction delays came in and my completion date first moved from August 2020 to October and then finally from October to February this year. Yet folks like me were in a pretty weird boat because there was absolutely no point in walking away and looking elsewhere – everyone knew that if we walked away, the builder will even thank us, because they will be able to sell the house for WAY more than our agreed price.

It all looks quite different now – now, if market keeps going down, people WILL have an incentive to walk away even forfeiting their deposits. Lots of people will become very upset. But the point I totally don’t get is that there seem to still be massive delays!!! This absolutely blows my mind – not only builders should be interested to finish already started builds asap, with the overall slowdown of the market, there must be some excess capacity (contractors, materials) easily available, YET I still see what I’ve been seeing all year long – semi-completed houses standing there with SOLD signs for months without any apparent changes.

It’ll sure be an interesting to watch how things would evolve here on the ground over the next 12 months.