Commercial real estate (CRE) loans on office and multifamily properties got further bludgeoned in October.

By Wolf Richter for WOLF STREET.

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked to 11.8% in October, the worst ever, and over a percentage point higher than at the peak of the Financial Crisis meltdown, according to data by Trepp , which tracks and analyzes CMBS.

CMBS are bonds that are sold to institutional investors around the world, such as bond funds, insurers, pension funds, REITs, etc. Banks that originated these mortgages are off the hook here, and investors eat the losses (see my discussion “Who is on the hook for CRE mortgages?” in the comments just below the article).

They were good until they suddenly weren’t. In October 2022, the office CMBS delinquency rate was still 1.8%. In the three years since then, it exploded by 10 percentage points.

Older office towers are getting crushed by a flight to quality and by corporate downsizing of office space due to continued working from home, as the much ballyhooed RTO has stalled. Even newer office towers are getting crushed by corporate downsizing and consolidation of their office footprints.

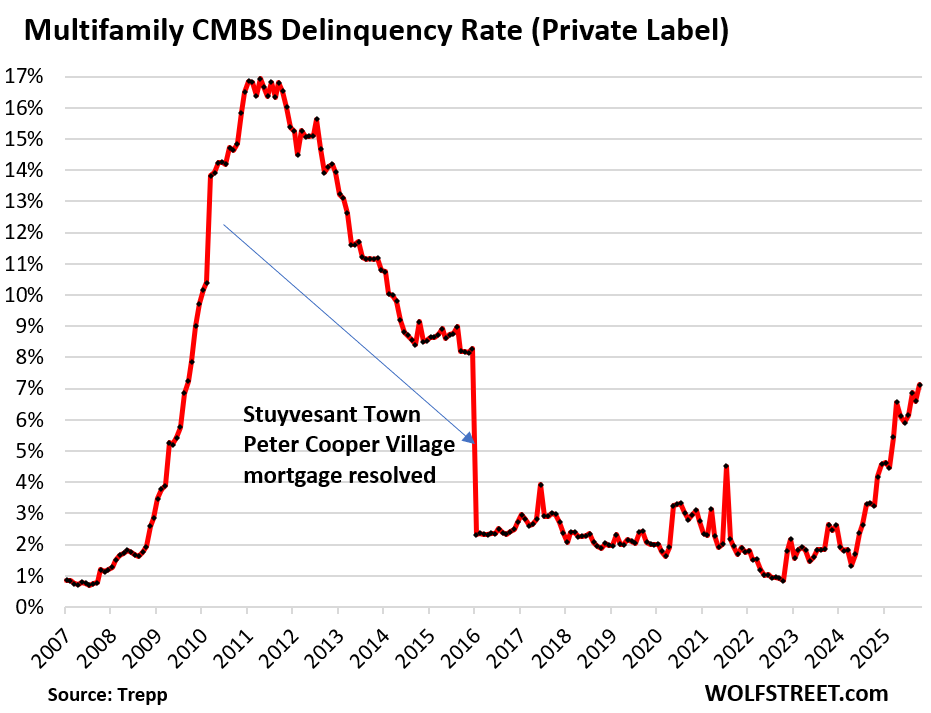

For multifamily CMBS, the delinquency rate rose to 7.1%, the worst since December 2015. Multifamily CMBS are backed by rental apartment property mortgages.

December 2015 was just before the defaulted $3-billion loan on Stuyvesant Town–Peter Cooper Village in Manhattan was “cured” through the sale of the property to Blackstone, which caused the loan to be removed from the delinquent list, and the CMBS delinquency rate plunged.

Newly delinquent office loans…

Loans become delinquent and are added to the delinquent balance when the borrower fails to make a loan payment or when the borrower fails to pay off the loan on maturity date (maturity default).

The $304 million mortgage on Bravern Office Commons in Bellevue, WA, was added to the delinquent balance in October, according to Trepp. The 750,000-square-foot complex of two towers, completed in 2010, is now vacant, but was once fully leased by Microsoft, which announced in 2023 that it would not renew the lease and has since then departed.

The property was purchased in 2020 by Invesco and Australian Retirement Trust from Principal Financial Group for about $585 million, according to Downtown Bellevue Network. In early 2020, it was appraised at $605 million. Two months ago, Morningstar valued the property at $268 million, a 56% haircut from the appraisal in 2020, and 12% below loan value.

The $300 million mortgage on The Factory in Long Island City, NY, was added to the delinquent list. The loan on the 1.1-million-square-foot office property was originated in 2020 at the very low interest rates at the time. The borrowers exercised three extensions that had pushed the maturity of the loan to October, when the loan finally went into maturity default. Occupancy dropped to 73% by the second quarter.

The property was built in 1926 as furniture warehouse for Macy’s. Atlas Capital, Invesco, and Square Mile Capital Management purchased it in 2012 at a bankruptcy sale and invested $100 million to redevelop the property into creative office space with Class A amenities. In 2018, Partners Group purchased a stake in the property that valued it at $400 million, according to The Real Deal, which added:

“While Manhattan’s trophy towers have led a recent wave of leasing activity, outer-borough landlords have struggled to land tenants. Long Island City’s availability rate hovered just below 27% in the first half of 2025, according to CBRE, compared to Manhattan’s overall availability rate of 17.5%.”

“Cured” loans…

Loans are considered “cured” and get pulled off the delinquency list when the interest gets paid; or when a deal is worked out to extend and modify a mortgage that wasn’t paid off at maturity date; or when a forbearance deal was worked out between borrower and lender; or when the loan is resolved through a foreclosure sale; or when the property is returned to the lender in lieu of foreclosure. So this process of “curing” a delinquent mortgage can mean pushing the problem into the future or taking big losses now.

For example, cured through “Extend and pretend” was the $96 million office loan backed by the 378,000-square-foot HP Plaza in Springwoods Village, a mixed-use development in Spring, in the Houston metropolitan area. The corporate campus of two buildings, completed in 2018, is 100% leased to HP Inc. through 2033. So this is a newer building, not some 1980s tower, and it’s fully leased, and not mostly vacant.

The loan became delinquent in the spring due to maturity default, when the balloon was not paid off by the maturity date. The borrower, Northridge Capital, which had acquired the property in 2019, has now negotiated a second maturity extension to November, following an additional principal curtailment, and so the loan became current through extend and pretend. “Discussions around refinancing are ongoing, with life insurance capital sources in play,” Trepp reported.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Who is on the hook for CRE mortgages?

For office mortgages: A big part is spread across investors – not banks – around the world via office CMBS – discussed above – and CLOs that are held by bond funds, insurers, private or publicly traded office REITs and mortgage REITS. PE firms, private credit firms, and other investment vehicles, are also exposed to office CRE loans.

Banks hold only a portion of office CRE loans. Many banks disclosed write-downs and losses. Many have sold bad office loans to investors at big discounts to get them off their books. And their earnings and shares were dented. And some of these banks were big foreign banks that were aggressively pursuing the US office market in prior years, such as Deutsche Bank.

For multifamily mortgages? The largest category of CRE debt, with $2.2 trillion in mortgages outstanding at the end of 2024, accounts for 45% of the $4.8 trillion in total CRE debt, according to the Mortgage Bankers Association.

Over half of multifamily debt was securitized by the US government (mostly Fannie Mae and Freddie Mac which doubled their exposure over the past 10 years) and the CMBS were sold to investors; and state and local governments hold a small portion of it.

Banks and thrifts are on the hook for 29% of multifamily debt, life insurers for 12%, and private label CMBS – discussed above – CDOs, and other Asset Backed Securities for about 3%.

The relatively limited exposure by US banks to CRE mortgages indicates that CRE is not going to pose a systemic risk for the banking sector, that most of the losses hit investors and the government, and that the Fed can let it reset on its own.

I was walking around a Simons Property Mall in Clarksburg, MD the other day. All the stores were devoid of customers. The mall looked like it was in a death spiral. I wonder who owns the debt on this mall? There was nothing in there I would want to spend one cent on. The only few people in there looked like they couldn’t afford a cheap hot dog.

MY BEST IDEA FOR OLDER MALLS IS TO SEGWAY INTO BECOMING OUTLET STORES.

THEY HAVE TO REVISION THEIR PURPOSE AND ADAPT TO NEWER VERSIONS OF THEMSELF. THINK OUTSIDE THE BOX…

GONE ARE THE DAYS OF SEARS AND JC PENNEY…

We have outlet stores around here and they are empty most of the time and many are closing up. Let’s face it, mall retail is dying.

Bulldoze this stuff and build housing. Suburban malls are huge properties because they include so much parking, so starting over with a clean sheet of paper to develop housing on it is pretty easy to do. And it’s happening everywhere.

A problem arises when there is an old gas station on the property. In all likelihood, the soil surrounding the underground tanks is contaminated, and remediation adds to the costs.

I have a friend in commerial real estate in SF, he claims things are getting better. I don’t know about that. Things still seem very quiet in SF core M-F. Also the lunch spots are still hurting and that one indicator I use.

Don’t known if the delinquency rate can be used to quantify the total amount of capital erased . Also question for Wolf . The math behind the delinquency rate.

As a mtg becomes delinquent how does that roll off the the delinquency rate calculation?

IE if delinquency rate was 10 percent monthly and rolled off the balance sheet then there would be 90 percent of the loans remaining to be in the pool. But I suspect that does not happen .

1. “As a mtg becomes delinquent how does that roll off the the delinquency rate calculation?”

See the section under “Cured loans…” which explains the various ways that delinquent loans come off the delinquent balance, and it gives you an example of a loan that was cured in October.

2. The delinquency rate = delinquent loan balance ($) in October divided by total loan balance ($) in October.

3. Delinquent doesn’t mean total loss for investors; it means there are problems with the loan. The losses for investors (landlord and lenders) come in different flavors over time.

I’m just a blue collar worker although I saw this coming. If we keep allowing WFH our economy will suffer and never recover.

Why would anyone stay in NY, NJ, SF, Chicago or any major area if they can work anywhere in the country or world? I’d move to the cheapest area possible and avoid expensive housing costs, property taxes, and exorbitant living expenses. These areas that are trying to do away with office buildings and replace with housing can’t shoulder the tax burden that successful businesses once did. This also eliminates small business that existed off the presence of employees being in their offices.

I’ve worked in many office buildings that have been reconfigured for housing in NYC and north Jersey. Most are struggling to find renters or buyers now.

for 1st time in 10+ years we are experiencing vacancy issue in multi-unit apartments

one factor is there are few ILLEGALS now that Trump/ICE making it difficult

another is poaching by newer large apartments offering massive concessions

2-3 months free rent, no deposit

lost 3 tenants who said they got deals they couldn’t pass up

and yet when it comes to pricing on these rentals

the FAKE ROI cap rates of 5% still flood market

gonna be interesting 2026

I’m an owner and dealing with the office buildings I know all of the office market lost its value, will not be able to refinance and we all will end up in default we all lost our investment the market is down over 30% and that’s where our down payment went. It’s time for the banks to release the true numbers it’s much worse then it’s being reported. Don’t know why the fed it’s sleeping and not doing anything and ignoring it.

Banks are relatively thin into office CRE. It’s mostly global investors that are on the hook for office loans, such as the CMBS holders discussed in the article. And banks have been cleaning out their office loans that they do have, often by selling the loans to specialized debt investors at a loss. This has been going on for two years.

The decline in occupancies far outweighs any up tick in deals. At this rate they will have to rezone most of these properties to residential and hope they can revive their use.. Big companies are downsizing, look at the layoff numbers !!!

A question about finances of blogs. Several ads for local commercial real estate accompanied this post. Does the site receive any revenue or does the carrier of the blog get it all?

My company, Wolf Street Corp, owns this site, leases a dedicated server that I control, and gets revenues from the ads. But between Wolf Street and the advertiser (the company you see in the ad), there are thick layers of other companies (“ad tech”) that exact their pound of flesh, and by the time whatever is left over reaches Wolf Street, it is just a small portion of what the advertiser paid.

For publishers, such as WOLF STREET and all others, including all those that went out of business already, internet advertising has been the road to hell, even as the big ad tech companies get huge and fat by sucking the bejesus out of the money flow from ads. The amount that publishers get paid per 1,000 ad impressions has been going down every year, but this year has been particularly bad (AI?). I guess sometime in the future, they expect us to carry the ads for free? This is why more and more websites go behind a paywall and still carry ads.

Instead of hiding WOLF STREET behind a payroll, I ask for donations. And it works; regular readers are generous (thank you!!)

https://wolfstreet.com/2025/11/02/dear-readers-please-donate-to-wolf-street-fall-2025-reminder/

As a regular reader and regular contributor, I SAY WONERFUL on WOLF,,, and plan to contribute each and every year until I am called…

OK, will only add that after many years of study, I am NOT any kind of religionista, but keep trying to understand why ANY of ANY ability think it IS or MIGHT be OK for GUVMINT to take from some without their agreement for any reason…???

I wonder if this could be one of the (many) reasons that the Federal Reserve is cutting interest rates even while inflation still appears to be very warm, as well as simultaneously announcing the end of QT on Dec 1.

I would like to think they keep an eye on these types of problems (or at least read Wolf Street). LOL.