A cleansing process, long overdue, to whittle down the corporate debt overhang and clear out deadwood, at the expense of investors.

By Wolf Richter for WOLF STREET.

It’s turning into a banner year for corporate bankruptcy filings, after years of Easy Money that caused all kinds of excesses, fueled by yield-chasing investors, in an environment where the Fed had repressed yields with all its might. Those yield-chasing investors kept even the most over-indebted zombies supplied with ever-more fresh money. But that era has ended. Interest rates are much higher, and investors are getting a little more prudent, and Easy Money is gone.

At the peak of the Fed’s yield repression in mid-2021, “BB”-rated companies – so these companies are “junk” rated – could borrow at around 3% (my cheat sheet for corporate credit rating scales by ratings agency). Companies are junk rated because they have too much debt and inadequate cash flow to service that debt. In other words, investors risked life and limb to earn 3%, and now these investors are asked to surrender life and limb, so to speak. But that’s how it goes with yield-chasing.

These “BB” junk bond yields have risen to nearly 7%. This means these companies that had trouble producing enough cash flow to service their 3% or 5% debt, have to refinance this debt when it comes due, or add new debt, at 7%. That 7% may still be low, considering inflation running around near that neighborhood, but it puts a lot more strain on those companies.

So lots of overindebted junk-rated companies will restructure their debts in bankruptcy court at the expense of stockholders, bondholders, and holders of their leveraged loans. That’s how it’s supposed to work. That’s how the corporate-debt burden gets lifted off the economy. And it’s starting to work that way.

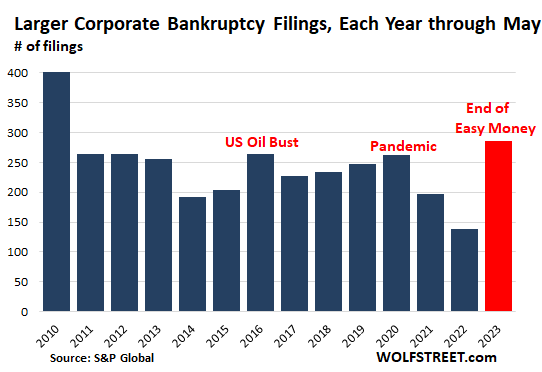

S&P Global has released its May bankruptcy statistics for companies that are publicly traded with at least $2 million in assets or liabilities listed in their bankruptcy filings, and private companies with publicly traded debt (such as bonds) with at least $10 million in assets or liabilities listed in their bankruptcy filings.

In May, 54 of these types of companies filed for bankruptcy, including notably, among the big ones:

- Envision Healthcare

- Vice Holdings and its affiliate Vice Media (a creditor group plans to acquire Vice Media out of bankruptcy)

- Kiddie-Fernwal

- Monitronics International

The May filings brought the five-month total to 286 bankruptcy filings, the most since 2010, more than double the filings for the same period in 2022 (138). And it even outran the 262 filings in the same period in 2020 when some companies faced enormous stress.

When the oil bust exacted its pound of flesh in 2016, and oil and gas drillers collapsed one after the other, S&P Global recorded 265 filings, but concentrated in oil and gas. To get a higher number of filings than in the first five months of 2023, we have to go back to 2010, when 402 companies filed for bankruptcy during the first five months.

Among the biggest bankruptcies included in this illustrious list so far this year that made it into my pantheon of Imploded Stocks were:

- SVB Financial, the holding company of Silicon Valley Bank that had collapsed into a big mess and was taken over by the FDIC;

- Avaya, the telecom, software, and services company that had issued $600 million in bonds just last year;

- Meme-stock ridiculousness of Bed Bath & Beyond, which is now liquidating.

The problem today is not a collapse in prices – such as the price of oil during the Oil Bust of 2016 when crude oil grade WTI collapsed below $20 a barrel that took dozens of frackers down; WTI is at $72 a barrel today!

And the problem today is not a collapse in demand such as it hit some industries in 2020 or during the Great Recession. This economy is marked by rising prices and resilient demand.

The problem now is that the debt got a lot more expensive, and that investors thinking of buying this debt have gotten a little more prudent. The problem is the End of Easy Money. Once companies get hooked on Easy Money by having piles of debt, it’s tough to get by without Easy Money.

In a way, the economy is normalizing with rates that were fairly typical before the era of QE. But companies that only made it this far thanks to Easy Money are now getting hung out to dry.

Bankruptcy filings will whittle down the corporate debt overhang. Many companies will emerge from bankruptcy with less debt, and they’ll be nimbler and more able to thrive. Others will be sold off in bits and pieces, making room for appropriately managed companies not encumbered by these issues.

There is a cleansing aspect to this part of the credit cycle that needs to be allowed to do its job to get rid of the excesses and the deadwood at the expense of investors. This cleansing process that has now just started is long overdue.

Hilariously, the end of Easy Money is now called credit crunch. Which should be the name of a candy bar (Credit Crunch®) offered to the crybabies on Wall Street as consolation when they start clamoring for rate cuts.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The 30% rally on Nadaq is based on

1. Decreasing EPS sold as earnings beat to braindead investors.

2. Expected Fed Pause and then instant Pivot.

3. Debt ceiling deal for printing trillions.

4. AI taking over the world.

5. The perceived Fed and FDIC put on banks

These bets seem so solid. What can go wrong?

Not just Nasdaq, “investors” are now pivoting towards small cap stocks, Russell 2000.

The whole market feels like a Ponzi scheme. As long as money keeps flowing in, everything will be hunky-dory. The printing press is not going to disappoint and mess up everyone’s retirement.

New money isn’t being printed though. That’s where this analysis fails. It’s based on the bet of this happening in the future.

6. Pension fund pump.

Agree with all…but would like to get thoughts on easy-to-find/easy-to-digest metrics that spotlight overvaluation.

For all its GAAP-related shortcomings, I tend to use historical PE because it is widely available and I can grasp the linkages between the E in PE and DCF/NPV valuation models.

But I wonder if there are other simple valuation metrics out there that might be useful.

Speaking of which, I note that enormous SP 500 presences Microsoft and Apple are trading well above 30 PEs…despite the fact that they are so huge that we would have to find a duplicate earth to justify their PE-implied growth rates.

And don’t get me started on the triple digit PEs of Amazon and Tesla…

It is worth thinking about the engine behind these persistent overvaluations.

Competing investment returns from interest rates have hemi-semi-demi normalized…but stock equity is still trading in the Everest death zone, PE wise.

Why…and when will the balloon burst?

I’ve suggested 401k autopiloting (which demographics will undo…perhaps soon) and CEO option-driven buybacks (which depleted cash hordes will undo) but I’d like to hear other theories.

There may be a handful of undervalued stocks or sectors, but, when the market has a major set-back, almost nothing is unscathed. Look at 50-year charts by industry or sectors (SRC Green Book charts) and look at the deeper recessionary periods. Few things benefit although a few groups ride it out without much damage: tobacco, education/publishing, beverages – sin stocks, some staples. But nearly all assets are in bubble territory now. I’ve settled in with short term, interest-bearing stuff.

I think there’s a good chance that the price inflation for real assets will not tank and that a serious bout of deflation isn’t in the cards, least of all with the Fed now having the ammo to reduce rates if things get ugly.

I also think that there is ungodly number of people anticipating this scenario, so the deep-value-field-day ain’t going to happen.

Read pages 282 & 570 in the book Intelligent Investor. The whole book is worth reading but these two pages may give you some better insight.

7. They printed over $10 trillion in monetary and fiscal stimulus.

The US GDP was over $23 trillion last year. The effect of the stimulus is waning as the years go by.

They printed a new floor under all asset prices.

DC

QT coming

really , its coming

“”free beer tmorrow” too

Good list. This is hopefully going to reduce the number of managers in this world, although many of the bstds will clear out with plenty of money and probably go have an expensive dinner with others that were canned and make some deal and all will be back behind a big desk in a week.

BTW, on the good side, Wolf’s pal Logan at Seeking Alpha said “EVEN Jack Bogle [maybe THE inventor and for sure THE champion of buy and hold forever index funds] just sold stocks.”

When TIG welding thin-walled 4130 tubes together, I’ve always used Vice Holdings.

Vise?

Vise-grip?

…aka ‘mole-grips’ in the UK…(hm, how come we rarely read about something ‘trapped in the mole-like grip’ of whatever? Another instance of my gratitude for being a native speaker…).

may we all find a better day.

The jig is up.

Companies that are taking on debt to cover expenses, and that have been using debt that was at artificially low rates, do deserve to have their deadwood cleared out.

It’s one thing to borrow money in order to have what is needed to begin a business, but too many of these zombies have just had money poured into them without generating revenue from their operations.

Thank you for the report Wolf, “That’s how it’s supposed to work.” “This cleansing process that has now just started is long overdue.” That is an understatement.

Chapter 11 bankruptcy filings are reorganizations; the filer might survive and prosper under legal protection. Chapter 7 bankruptcy filings are liquidations; fire sales of assets and layoffs occur. Chapter 7 is where the wild things are.

Occam,

Lots of Chap 11 filings end in liquidation, especially with retailers (such as BBBY). It’s very hard to restructure retailers because they have so few assets, and so much debt, and by the time they file, they’ve already ruined their brands. Some retailers were restructured, only to file a second time a few years later (the infamous Chap 22, LOL), and this time, for liquidation.

Prepackaged Chap 11 filings, such as Vice, are the smoothest to exit. And a lot of them work.

Chapter 11 tend to work best when the business model itself is solid, but the company has made some bad decisions in the past and needs to be released from certain obligations (whether a few expensive leases, debt, pension obligations, etc.). As Wolf noted, Bed Bath and Beyond didn’t have a workable business model by the time it filed.

Ouch! 😂

Yeah, Ouch. (But not my show.)

At least I got to post historically accurate (I checked) story on how Reagan was “transformed” in Wolf article about Australian Central Bank pause. Worth reading, believe me! I was around then, in CA, and never knew ANY of it. He just popped up as Gov.

Einhal,

You’ll just have to take my word for it. Businesses DO screw up a lot, not just government. In fact I’d bet since the people in business are generally greedier, they screw up MORE….pushing the limits. But that is just my opinion.

I think this is suppose to be a joke and it might just be funny if you would only allow a clue to the pun….

I was looking at the joke angle, but cannot quite see it. The welding part eliminates all the funny angles I might see.

Hell, I tried to use the word “jig,” as in welding jig too. Nope, two strikes on that one. “… eliminates all the funny angles …”

For “funny angles,” an ‘adjustable angle miter corner clamp’ works well. My tube-coping machine tool goes to a 60 degree angle.

But, it’s too late to, “Don’t quit the day job,” as I already have.

He’s giving MichaelEngel a run for his money.

Wolf’s trademarked Credit Crunch candy bar will have to contain an FDA warning- “Caution may contain moral hazard.”

I wouldn’t eat one.

You have to have done some table top/jig welding to get the joke….I did.

Let’s see if I bomb, too.

PS- Vice was a damn good channel but my cable company doesn’t have it in my cheaper package….or Speed channel. I hate them.

DanRo/Wolf – some ‘muricans say ‘vise’ (I do, but mebbe it’s a relict of Victorian sensibilities) and many don’t. My experience with Brits is that they use ‘vice’ (weird, given my parenthetical comment). Churchill’s observation of the USA/UK as ‘…two great nations, divided by a common language…’ remains, and mebbe in our case, ‘…one great nation…’.

may we all find a better day.

NBay – mebbe you have MAV or CNBC (yes, they carry some motorsports) or (ack!) FS1? (We gearheads remain underserved, in any event…). Best.

may we all find a better day.

Saw your comment with explanation of MOS (I wasn’t sure what yours was, either). VERY well done!

Suggest you change screen name to DUSTOFF, and with that in mind I THANK YOU for your service, and of course, not on behalf of the USA.

Yeah, I get some motocross (mostly indoor…not as good as out) and bike GP, some Indy Car, but no F-1 or AMA (San Jose IS/was The Mile…glad I was there a few times) which I love, and of course all the Nascar I can stomach…..But it’s still gear, tech, and whatnot.

NBay – happiness was a cold LZ, but you know that, brother.

No doubt San Jose was THE mile. Still have Sac, though (Too bad the Santa Rosa revival wasn’t successful, but there’s still short track around the Fairgrounds occasionally)…best.

may we all find a better day.

Lets hope so Mr Wolf. I would love to see Wall Streeters brown baggin lunch. With one of your candy bars for desert.

I would like to see some wall streetcars jumping from windows,they don’t open Hahaha 🤪

Instead of the mug from Wolf a box of Credit Crunches !

That’s a marvelous joke, Mr. Richter. Set aside a case of those candy bars for Professor Siegel of Wharton.

Thanks for your great work Wolf! Something got added or dropped in “debt got a more expensive”.

lot. Thanks!

and we have yet to feel the lag effects of a housing/ construction slow down, that encompasses a wide area of tradesmen, small contractors, buildng components, etc..

Homebuilder stocks are all time high

They have great margins, and the longer sellers of existing homes remain delusional and emotionally attached to the 2022 peak value of those homes, things will stay great.

Multifamily construction is booming, as are other commercial categories. What slowed down is SFH.

Slowed down is definitely not stopped though. I’m in semi-rural Oregon right now, across the street from a somewhat large SFH development where they just broke ground.

I’m ending my buyers strike as of this week. The lack of real effort by the Fed to squelch inflation has finally broken me, and I see no more incentive to save, but rather to spend like mad before money loses all value. I’m either the last bear to turn bullish, marking a top, or a sign of more spending to come as other bears come to the same conclusion.

Not me. I won’t play their game. I’m going to be patient. Something will break. I’m done buying crap anyway.

Come the end of this pathetic spring season, which is around now or July, you will see a huge slowdown in SFH sales and even more price drops. Builders are already offering huge discounts. I’m not buying at these prices.

Fed up

Agree with you.

WSJ, yesterday I believe, had a story 3 days ago about the apartment building boom hurting owners (REITS) in the South. Maybe the see MFR slowing down.

https://www.wsj.com/articles/sunbelt-construction-boom-threatens-top-apartment-building-owners-d009312f

Maybe not as relevant to your point, small investors- who they try to make look overly sympathetic by referring to them as small, when their modus operandi has been to flip existing apartments (sans tenants) in a fast easy-money way. -something the big guys are shy about doing – but calling them small makes them sound meek and innocent.

https://www.wsj.com/articles/a-housing-bust-comes-for-thousands-of-small-time-investors-3934beb3

I’ve been on buyers strike for several years, but at least now I’m getting 5% on the down payment I saved.

I’m OCONUS and SFH hasn’t slowed at all.

Big boom town with Canadian and US expats paying eye wateringly (up 300% in 2 years) insane prices for vacation beach homes.

Rentals went nuts too. My condo went from $1k for. 3bd/2/ba to $1,700.

I can’t wait for the bust!

I need price relief. 3% COLA on wages with 6% inflation is no fun :(

I should have been more clear: SFH *construction* hasn’t slowed in my area.

I believe sales have slowed

That multifamily boom is scary to us apt renters. Wish WSJ “good news” wasn’t behind paywall, although I’m not in the South.

It’s where the money is if a person wants to work. It’s where the money will stay because repair and upgrades are always needed.

I want to see how crawling under a house and fixing busted pipes during a Texas freeze can be replaced with AI!

Wolf, seriously, sell some 6 packs of “credit crunch” candy bars. You can have wrappers custom printed easily, and the sale of them is viral marketing. It’s a perfect summer intern or loyal wife project.

You could use Payday bars with red food coloring.

Ritter will make custom candy bars.

A fine and viable plan. In addition, let’s add a promotion to the release of this novel food product. We will place a Willy Wonka “golden ticket” in one of the bars. Any overleveraged zombie company that finds the golden ticket is relieved of their debt. Willy Wonka’s Credit Crunch bars.

The managements of these companies will buy them by the case. They’ve already been addicted to the sugar high of immediate gratification through ongoing low-cost loans. Perfect.

Kidding aside, these half-assed companies need to be flushed. Most would be gone by now anyway if not for the easy money environment. Cleansing is the correct word Wolf. Let the cleansing continue.

Lol

The credit crunch diss aimed at wallstreet genuinely made me lol 😆

I guess the SVB memorial candybar can be known as the “COF crisp”

Hmm, now the internet tells me that the ‘Coffee Crisp’ candy bar is a purely Canadian phenomenon, so I guess nobody (except any fellow Canucks on this site) will get my joke – all these years I had no idea. Maybe that is why Canada always ranks ahead of the US on quality of life indices, it can’t be due to real estate affordability, after all.

Those were my first pick out of the Halloween pillow case as a kid. Was surprised that the US didn’t pick up on the best bar of all.

Kinda looks like Wolf’s joke can’t be improved upon……but I’m only halfway thru comments.

1) China discount rate is 2.9%, osc around 3% for 25 years, stable. The 10Y is 2.7%. The 30Y is 3%. Chinese households saving is almost $2T out of $18T GDP. China will take us out.

2) The wholesale dollar debt became painful after Fed hikes.

3) China central bank raided in “other”people checking accounts, saving and CDs to finance ==> 600 millions apartment buildings and houses, global infrastructure, military, useless factories… for an hollowed IOU.

4) The gov raided in again when China was comatose, but China is not waking up.

5) Many of the 600 millions building are empty. The silk road countries are in financial troubles. A war with the west is not palatable.

6) China is roaring, marking territories like dogs.

where is my tin foil.

China’s # 1 task and hope: moving on from the CCP, or at least the CCP moving on from Maoism, to which Xi is a throwback. Why is Mao’s picture still on the currency? He destroyed the economy, starving millions, and society as he set the Party against the family. When will the CCP apologize to the Chinese for its reign of terror: The Cultural Revolution?

Deng, not Mao, is the man behind China’s real ‘Great Leap Forward’, which was accomplished by freeing business from the CCP, first in coastal areas. Shanghai etc.

If the Mainland could move on from the worship of totalitarianism, in time it might tempt more on Taiwan to think of peaceful reunion. Having seen the iron grip of the CCP descend on Hong Kong, this is not currently palatable to most Taiwanese.

1) Wall street want free money, savers like 6% and the zombies are paying 7%.

2) XLI was rising, MSFT was plunging, AAPL tried to move up but lost it’s

grip. NVDA might partially close a gap, before turning up to test the highs.

3) The regional banks are on sugar high, but DG is asking : where are my cookies.

4) BRK/B daily close Renko $1 is waiting for the exterminator in July.

Hi. From the chart it looks like a time when Credit Spreads should be screaming high. But that is not the case. Any thoughts on that? Thanks

5% short term rates feel normal to me, whereas 0.001% always felt odd. I imagine there are a lot of younger folks who have the opposite feeling…

Agreed!

Wolf is like having a brother who runs an equity fund and makes clear what is in fact occurring versus the spin.

In a class on persuasion and compliance, in the first chapter was a sentence that was amazing saying that in relation to the execution of persuasion “…facts don’t matter.” I already have a graduate degree in Strategic Communication which originally is a Department of Defense communication policy done to “persuade and control” in the realm of military objectives not inform and enlighten. In the world of war this is not a problem to this writer understands the basis of all power is effectively violence that those in the military do to keep order over chaos.

My point is that the readers here are so hungry to be informed and enlightened and most know almost all the info now presented is mostly sewage not worth a XXXX.

Wolf made this statement:

“There is a cleansing aspect to this part of the credit cycle that needs to be allowed to do its job to get rid of the excesses and the deadwood at the expense of investors.”

and this cuts to the heart of the matter that people like us all have been waiting to see happen but now the outcomes are not the same with all manner of manipulation and deception. What is most telling is how tech allows a small subset of people to know what is happening in real time every minute and can make decisions most here would love to be privy to so investing would be a breeze. To make matters worse, now business, government, and tech seems to be in control of everything be it concealed, apparent, or “an understanding” between all the big players in our entire system.

I too have wanted to see all the benefits of being able to take advantage of good deals but this seems not likely for most anymore. So, are we all here just fooling ourselves to think anything like we once knew will exist ever again? I think not….

When younger, I went to school to become a CPA/Tax Attorney. I worked in accounting firm with ex White House Alumni from the Republican Party. Then, went on to audit federal and state grants to nonprofits….stunning what things done with this money we all pay taxes for.

So 35 years later, my old boss has been my CPA. I asked him to answer a question about 401Ks because I was always hearing about people cashing in all the money in their 401K for one reason or another. The question was “What percentage of people you have seen start a 401K and stay with it to the end and collect retirement from this source?

His answer was 5%, 1 out of 20, wow. So, the IRS gets all the tax avoided plus a ten percent early withdrawal penalty, and if it is much more than they normally earn in a year they are taxed at much higher rates than normally. So the government knows this is a scam (that they make good bank with) whereas how many here actually knew that?

I can barely read the news, I haven’t watched TV for 30 years, and I think most of us will be toast due to inflation….

What Wolf does here is found in the definition of lucid: “characterized by clear perception or understanding; rational or sane: a lucid moment in his madness. shining or bright. clear; pellucid; transparent.”

Appreciate your execution to inform and enlighten.

Kudos, Adam!

Dark. I agree on much of what you’ve said but I think there’s some serious distortion. The author of that book that wrote, “facts don’t matter” is probably doing what your course was intended to do: shock your sensibility to persuade and make readers (students?) compliant. Facts do matter, but, when the herd turns into a mob, all bets are off.

The 401K scam isn’t a scam. It’s a good idea and sensible; prudent people will use it to their benefit. The trouble is that we have a vast number of stupidisimos in our country and they’re inclined to do stupidismo things with the money they get. I think that 95% is probably too great a percentage.

I used to babysit when I was a teen. I’m losing sympathy for the multitude of idiots that would rather have a tattoo on the forehead than use matched employer contributions, etc., in their 401K. When should babysitting end? At the age of puberty or after by-pass surgery? Use of a 401K is not a long-term problem; AI will have them on welfare soon anyway.

Screwed up that second sentence: meant to say “…shock your sensibility: by persuading and making readers (students?) compliant.”

Thank you, Adam. That was the most informative summary of how ethics based people feel, for several decades now, about the problem of institutionalized mendacity that we have been assaulted with.

Wolf is doing a lot of good by telling it like it is.

Adam, great post. Just trying to discern what you said about 401k being a scam…is it a scam in the sense of if you keep it to full term (retirement) you get sacked in the head with taxes? Or is it if you cash it in early the govt gets all the taxes avoided right then and there PLUS the early withdrawal penalty?

I’m assuming you are talking about the latter. I’ve seen a ton of people pull out of their 401ks to buy a home or a new car or something else with depreciating values…

You have two good options that Iknow about.

1. You can retire at 55 with a 401K at your last place or employment penalty free, but not tax free. But you can pull 3 – 5% out each year and spend it.

2. you can retire at any age with an IRA and follow IRS rules with substantially equal payments. I did that at 49 or so and it worked for me. It’s a little bit of a leap of faith.

You appear to be a conceited AI

The financialized US “mickey mouse” economy is a joke. It has been supported by the “dollar” abroad, on the backs of the rest of the world and been “maintained” by our heavy handed military which is no longer involved in defending our country as much as “projecting power” around the world to strong-arm support.

To add to that mess, our society’s values have gone down the sh****ter. The rest of the world that has to really work for a living and continues to support us cannot believe the pure nonsense that America now stands for.

These corporate zombies, private equity monsters and all the other players in this game are shameful.

Well said. Light on words for such a large subject. It’s important because some people don’t see the bigger pictures. It can be intricate until you work your way back to the source and step back to see the true size of the pile of garbage that it is. What these pirates have done is destroy values and the ability to assess and hold values. economic and moral.

The Fed should just stay put (no pun intended) with rates that encourage some old fashioned savings. That, by itself, will create deflation and a more conservative oriented population. Demand will decline, in other words. Now, if we could just tax the bejesus out of the Oligarchs so they can’t bribe every politician on the street.

I saw a graph of what the rates would have been in recent years if Fed simply followed the Taylor rule.. Fed definitely waited way too late to raise rates according to the Taylor rule and Taylor rule indicates rates probably need to go higher, but there are different values you can plug in for inflation that determine if 5.25% is enough.

Maybe Fed interest rate policy should follow Taylor rule unless Fed goes to Congress explaining why they feel the need to throw out the rulebook.

It all started when the Fed began to fund the government by monetizing the debt. This will end of course with out of control inflation and the demotion of the dollar. Anything else is politically impossible. But, for now, we’ll have an intermission with deflation. As soon as things start to crumble they must restart the printer.

Interest rates are nowhere near high enough after years of disastrous ZIPR and QE, then $10-12 trillion of pandemic (over)-stimulus and still very inadequate QT. If anything the Fed should be raising rates by 50 bp in the June meeting–inflation is absolutely crushing Americans right now. Rents are still soaring and homelessness across the US is exploding, shops are having to close down or change policies to fight the worst theft and shoplifting on memory, the US birth rate is collapsing and the rest of the world is de-dollarizing much faster than expected, so much that even Bloomberg is reporting it.

Quiet quitting is crushing US productivity and the writer’s strike is breaking the back of Hollywood–it’s the first of many, and it’s a direct result of inflation piled on top of inflation. The 2% target was never legitimate but it needs to drop down to more like 0.2% now given all the inflation that’s pushed up prices without wages to match. Americans can’t survive this inflation for much longer, Powell needs to go full Paul Volcker or the US and the US dollar will be facing an even worse reckoning than we already are.

Wolf,

I hear a lot of talk about all this easy money still floating around from Covid stimulus.

I made the following calculation

M2 has increased by 34% since February 2020. From the article in the Journal of Applied Corporate Finance (hhttps://www.independent.org/publications/article.asp?id=14307 ), I took -1.7% for the change in velocity (ΔV). Real Gdp has increased since Feb 2020 with 6%.

Both numbers I multiplied by three because it has been three years since covid stimulus. Therefore, excess money equals 22.9% ( 34% minus 6% minus 5.1 percent) (Quantity theory of money). I also subtract the inflation that we have already experienced, caused by the M2 explosion.

I guess this to be 15%. (I think that the inflation from the COVID stimulus started in February 2021 because, at that moment, M2 YOY took off) This leaves me with roughly 8% of M2 unused.

This is about one to two percent above the trend (Money growth has been 6%/year on average since 2008). SOOOOO not that much money from covid stimulus left.

“Both numbers I multiplied by three because it has been three years since covid stimulus”. Correction, I multiplied the velocity (1.7%) by three (3 years). Gdp is just 6% since Feb 2020.

“Once companies get hooked on Easy Money by having piles of debt, it’s tough to get by without Easy Money.”

….

Once governments get hooked on Easy Money by having piles of debt, it’s tough to get by without Easy Money.

Both are BAD right? Or am I missing something here?

Still a drop in the bucket? Maybe your headline should be, “economy proving highly resilient”. What percentage of companies are filing for bankruptcies. What percentage of people are having to forfeit or panic sell their homes. What percentage of people have lost their jobs.

You completely missed the topic of the article. Did you accidentally forget to read it?

1. This is corporate not consumer bankruptcies.

2. A bankruptcy doesn’t mean that the company shuts down. It means that the ownership of the company gets transferred from stockholders to creditors in a process that is supervised by a court. Vice Media will continue to be Vice Media, but under new ownership.

3. Sometimes everyone loses their job and the company is liquidated – retailers often end up that way. But that’s not the rule for corporate bankruptcies.

4. These are larger publicly traded companies or larger private companies with publicly traded debt (such as bonds). There are only a few thousand of them in the US. These bankruptcies here are not by the gazillion small businesses.

5. You need to compare the current period to the prior periods to get the trend, and the trend is that the Easy Money is gone, and bankruptcies are higher than they’d been when we had the Easy Money, and higher even when things got rough, such as during the oil bust in 2016 and during the first few months of the pandemic. I cannot believe you missed that. That was the core topic.

6. Consumer bankruptcies are still hovering at record lows. This has nothing to do with corporate bankruptcies.

wall street doesn’t need credit crunch bars it needs ex-lax!

How fortunate, Nestlé produces both!

Now allow that student debt to be bankrupted. Lets see what happens.

That would be consumer bankruptcies not corporate bankruptcies. Nothing to do with this here.

Warning, Credit Crunch® may cause anal seepage.

Bankruptcies are a healthy part of a competitive market. The bankruptcy rate was artificially subdued for a while, so we should expect an uptick for a little while (3-7 years) which will likely cause an over swing of the pendulum before it comes back toward a stabilization. The zombies need to be cleared from the market, and right now there are far too many of them.

Pardon my ignorance, as I’m fairly new to this scene, but are zombies a reference to homes that are not habited?

*typo= homes that are inhabited

Zombies are companies kept in existence only by borrowing more money when their existing debt comes due.

Thing about a corporate zombie is they might employ many people.

They might produce large quantities of product.

They may have great value to society.

The problem is the balance sheet is not happy, and that is the only genuine distinction.

The 10Y indicate that inflation is falling. Gravity with Germany, which entered recession, pull it down. The front end attract private money, global money, to US gov.

That money finance US gov debt.

Higher rates –> stronger dollar. Stronger dollar –> lower commodities prices, lower inflation and lower stock markets.

“The 10Y indicate that inflation is falling.”

The 10-year yield never indicates anything other than speculation. In August 2020, the 10-year yield was 0.5%, and people back then said that it indicated that rates would go negative in the US like they’d done in Japan and Europe, LOL. Major banks collapsed because they took this BS seriously.

In 2008 the fed became more powerful than ever. It had the power to suppress the front end and the long duration rates. Until 2008 the Fed controlled only the short term rate.

By doing so it controlled the gov debt rates and mortgage rates !

1.5 Trillion Commercial RE loans have to be refinanced in the next year alone. Many were interest only loans. So their interest costs will go from zero to current market rates. At the same time office tenants are abandoning the big office towers in droves. Look for more bankruptcy filings and more small and regional bank failures.

CRE defaults may not normally involve a lot of bankruptcy filings. Most of the commercial mortgages are either non-recourse (lenders only get the building) or are backed by a standalone entity (lender gets the standalone entity which holds only the building). And the borrower just walks away from the mortgage and lets the lender have the building — no bankruptcy involved. I have already posted a bunch of stories on this very topic – and none of them involved bankruptcy filings. Landlords are smart.

I have always had a negative feeling towards Chapter 11. “…We borrowed all of this money, it didn’t work out, so we’re not going to pay you back. We’ll try again, hopefully better managed this time – Don’t hold us to it though”. I guess the investors in the “junk” accept the premise in advance, but still, it seems somebody gets off scot-free at investor and supplier expense.

A bankruptcy means that the ownership of the company gets transferred from stockholders to creditors in a process that is supervised by a court. Vice Media will continue to be Vice Media, but under new ownership. The prior owners lost the company, and their shares became worthless.

In other words:

1. The owners (stockholders) normally lose their entire investment (sometimes they get a little consolation token).

2. The creditors get the company or assets, with some creditors losing some or all of their investment, and others getting made whole, depending on seniority in the credit structure.

I think the money now is a lot easier than then.

interest on CDs and treasuries.

“Hilariously, the end of Easy Money is now called credit crunch. Which should be the name of a candy bar (Credit Crunch®) offered to the crybabies on Wall Street as consolation when they start clamoring for rate cuts.”

Excellent.

Nope. It’s all the new businesses that were set up to receive PPP and other goodies during the pandemic that are closing down. Economy is booming.

The qualify for a PPP loan I thought it required the business to be operating (and loan was based on money flow) from a few years prior to the pandemic I believe? 2 years prior?

Was there a work-around to this?

Yes, it was based on self declaration to avoid too much paperwork.

Wolf reported at that time on all new start ups , I bet the decline no is proportional but Wolf has the data.

Nope? Did you read the article? The article is about the bankruptcy of publicly traded companies or private companies with publicly traded debt, i.e., large corporations. It has nothing to do with new business set up to engage in PPP fraud.

Just about anyone can look like they’re making money with ever decreasing interest payments on increasing piles of debt. Glad that scam is over for now.

They’ll need to wash down the Credit Crunch Bar with Copium Cola.

LOL that’s a keeper!

It’s not a credit crunch until the zombies have to pay well north of 10% to refinance.

I looked at some Carnival bonds – unsecured senior debt maturing in 2028, Yield to Maturity around 10%. That’s only 500 bps higher than a 1 month treasury bill.

No thanks, I need a lot more yield than that to compensate for the very real risk that bloated debt zombie restructures or files bankruptcy in the next 5 years.

Carvana tried to float something like a billion at 9% but not enough takers. No matter, its stock heads to the moon, just like carnival. The market is a perfect reflection of the sick, degenerate society we have today

Another .25 needed this month. Badly.

I am thinking they will raise the Fed Funds rate another 0.25% this month so the Fed Funds rate is increased to 5.5%.

They have nothing to do to keep increasing while the stock market has not crashed, and unemployment is low.

The greater they increase the Fed Funds rate the more margin or room they have to decrease rates without returning us to a zero interest rate policy (ZIRP).

Assuming about 20% inflation since February 2020, the S&P 500 has only had approximately a 6% real or inflation-adjusted gain.

Looking at the heat map for the S&P 500, and most year to date gains are with big tech.

Healthcare and energy has cooled off, and banks have lingered.

These are not big gains in the S&P 500, so I don’t expect it to increase inflation, plus it looks like bitcoin is down about 15% from its most recent high.

Recent years in California show an ecological version of this: whole populations lived in a semi-suburban pretend-nature where wildfires were suppressed, and kindling thus built up until, in a hot-dry year (I’m thinking withdrawal of liquidity), it doesn’t take much to spark off super-fires threatening whole (even green, healthy) forests. The deadwood will be cleared sooner or later, one way or another. Leadership is choosing a policy and getting buy-in with the trade-offs involved, or I suppose, waiting until a set of outcomes just tumbles in and resets the picture. I’m not sure whether this sort of scenario is brewing more generally across corporate-land (a very narrow set of super-meme AI stocks holding up the tent concerns me). The data-Wolf is the role model!

Phleep – like many of the myriad issues Wolf has addressed over the years (sound money, the abandonment of honest GAAP and price discovery, for example), ‘leadership’ believing the business cycle is something that can be constantly-dodged/manipulated is another. Another problem being that that cycle is an apparent unknown to many of the newer players…

may we all find a better day.

The o/n rrp award rate is lower than money market rates (rates < 1 year). An increase in t-bills should keep short-term rates higher than the award rate. Thus, funds will come out of the O/N RRP.

This is great news! One can only hope this helps lead to a recession.

I can’t think of a worse investment than buying stocks at today’s prices versus buying t-bills at 5%

Commodities are cheap vs snp, they are ripe for scaling in, biotech heating up also with triple top breakout, 10 % gains available

Some people are already in a depression,lost jobs living in tents . This is crazy so 1% can have more than yhey can spend in 100. Lifetimes = Warren Buffett

Do credit crunch bars come with a free helicopter?

I van vouch for bk filings we provide some of largest firms in country credit reports, are busiest sector volume wise

Re: There is a cleansing aspect to this part of the credit cycle that needs to be allowed to do its job

Not going to happen because sanity is only a temporary disruption of the customary behavior of the Central Banks.

Just a quick comment on Junk bond terminology:

If I remember correctly from my early fixed income days, the key difference between investment grade bonds and non-investment grade bonds (aka junk bonds) is the probability of default.

While IG bonds have a 5-year default rate below 2%, NIG/Junk has over 10% defaults.

There is a huge jump once the bonds moves into junk territory, therefore the name.

Assuming a recession gets underway, the question surrounding corporate junk and lower-rated muni debt becomes how high is high? Based upon the aftermath of 2008, it would not be surprising to see corporate junk in the 9% to 10% range, and muni junk yielding in the 5% to 6% range before things get better. If proven true, this will thin out the herd!

Muni junk may be a great investment once the recession gets under way. I like that 6% return free of Fed taxes.

Meanwhile, student loans remain essentially impossible to discharge.

Nearly 60% of all borrowers had stopped paying ever before the pandemic, that will increase by a LOT whenever they resume payments.

Disgusting.

Totally useless site! Please do the world a favor and die soon Wolf!