More rate hikes are on the table. “Overall, excess demand in the economy looks to be more persistent than anticipated.”

By Wolf Richter for WOLF STREET.

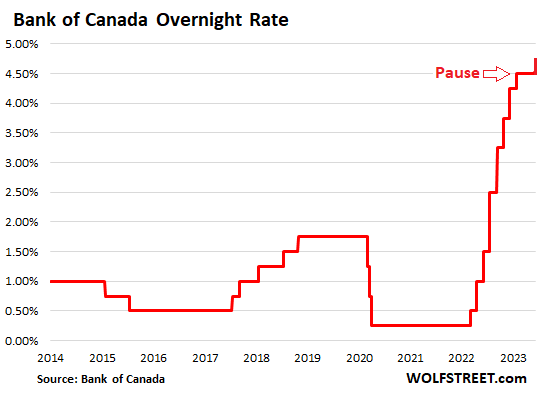

The Bank of Canada un-paused today, after having “paused” following the January hike. The pause had been widely ballyhooed as the end of the rate hikes and a pivot toward rate cuts. Those hopes have now been bitterly disappointed. Everyone is figuring out that this inflation isn’t just fading away on its own.

Today it hiked its policy rates again by 25 basis points, bringing its overnight rate to 4.75%, the highest in 22 years, in a move that surprised a lot of observers.

The Bank of Canada has now become the second central bank to pause and then un-pause, after the Reserve Bank of Australia, which had paused in April and un-paused in May, and hiked for the second time post-pause yesterday, on fears that inflation was getting entrenched via inflation expectations and surging labor costs that weren’t matched by productivity gains.

At its meeting in January, when the Bank of Canada hiked one more time and announced the pause, it stressed that it was a wait-and-see pause, not a pivot, though that message had been widely ignored. At the time, BOC Governor Tiff Macklem said in an interview, “the question really we’re asking ourselves is, ‘Have we done enough?’ We’re pausing to assess whether we’ve done enough.”

Turns out, it has not “done enough.”

The rate hike today reflects “our view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target,” it said in the statement today.

So, well, turns out, amid strong consumer spending, a tight labor market, and increased activity in the housing market, the Bank of Canada has not done enough. And it un-paused the ballyhooed pause.

The BOC pointed out that the “stubbornly high” underlying inflation rose for the first time in 10 months. The increases were broad-based across goods and services, “reflecting strong demand and a tight labor market,” it said in the statement.

The BOC is now seriously fretting about the resurgence of underlying inflation:

- “Overall, excess demand in the economy looks to be more persistent than anticipated.

- “The economy was stronger than expected” in Q1 with GDP growth of 3.1%

- “Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains.”

- “Demand for services continued to rebound.”

- “Spending on interest-sensitive goods increased and, more recently, housing market activity has picked up.”

- “The labor market remains tight: higher immigration and participation rates are expanding the supply of workers but new workers have been quickly hired, reflecting continued strong demand for labor.”

And it warned that, “with three-month measures of core inflation running in the 3.5-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.”

And the BOC put the possibility of more rate hikes on the table. It said, “We will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behavior are consistent with achieving the inflation target.”

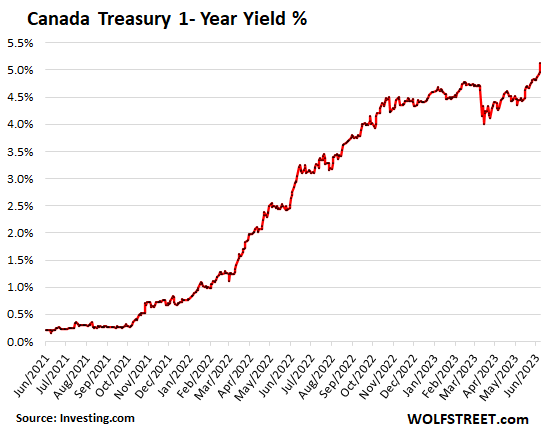

Yields jump on the move.

The Canadian bond market was surprised by the move and is now adjusting to it. The one-year yield jumped by 17 basis to 5.13% today, now expecting one more rate hike and no rate cuts within the 12-month period:

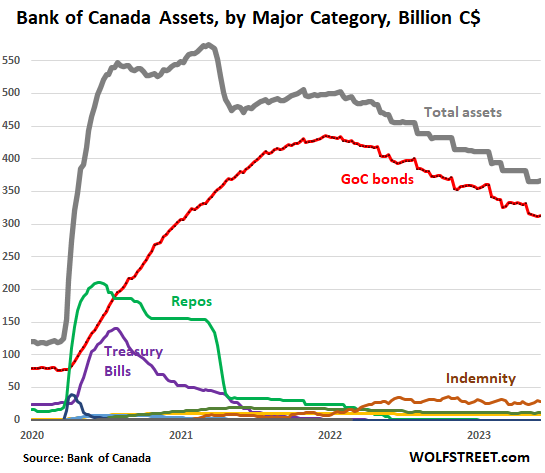

Quantitative tightening will continue.

“Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank’s balance sheet,” it said.

During its crazed QE starting in March 2020 through March 2021, the BOC piled on an additional C$455 billion in assets. As of the most recent balance sheet, it has now shed 46% of these pandemic QE assets, well ahead of the Fed and other central banks — though it’s behind the Fed on rate hikes, perhaps on the theory of faster QT and slower rate hikes.

It started early by starting to unload its repos and Treasury bills in 2020. It never seriously bought mortgage bonds and then stopped buying them altogether in late 2020. And it unwound most of its other small holdings.

Its largest remaining holdings today are Government of Canada (GoC) bonds: at C$313 billion they’re down by 27.4% (red) from the peak. The “Indemnity” reflects unrealized losses on its bond holdings, currently C$28 billion (brown), which it carries as an asset under an indemnity agreement with the Government of Canada, that, if it actually ever sold those bonds, rather than hold them to maturity, and thereby realized the losses, the government would indemnify the BOC for those losses.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Nobody talks about business investment anymore under the current interest rate environment. I wonder how bad it is now. BTW, commercial real estate vacancy rate is 15% in downtown Toronto.

Fed will still pause, because now it has to defend the stupid 30% rally on Nadaq that was based on

1. Decreasing EPS marked as earnings beat.

2. Fed Pause and instant Pivot.

3. Debt ceiling deal printing trillions.

4. AI taking over the world.

That’s a really interesting observation. I think it’s just way worse than we can see because things move slow and things move fast and then you have to factor in all the shady statistics. I mean there is just no way we are getting all the correct data.

The economy’s lifeblood is negative interest rates and inflation, I’m shocked at how it’s still standing, it must be because there’s so much printed money slushing around out there that we have no clue about yet, but eventually I believe it will show up somewhere.

Office real estate in Toronto is suffering but the rest of commercial real estate is holding. Retail is steady. Industrial is crazy. In the Greater Toronto Area, industrial vacancy is at 1% and net rent has gone up almost 200% (tripled) in less than a decade. Even with 6.95% prime rates leading to higher cap rates, industrial real estate market price is up over 50% from pre-pandemic per square feet.

my friend i took a five minute drive in my hood saw 6 new leases on mrkt,,, ,, my new driving game is counting how many retail/ industrial leases i see on my daily drive. best number was 18 leases ….. fyi i am 15 mins from the dwtn core

official is 15% but major players trying to offload and right size footprint,, my guess real number closer to 22%

Well does the fed have the guts to follow this one?

It depends on the movement of US inflation. Why not follow BoC? !

Blue Oyster Cult?!?!!!

Don’t fear the reaper.

25 basis points more would put US monetary policy at either mildly stimulative or around neutral, depending on which inflation index you use. Meanwhile, fiscal policy remains highly stimulative long term. Fifty basis points plus a statement that there will be no pause or skip until inflation hits the 2% target would convince Wall Street that the Fed wasn’t going to tolerate 4% inflation. However, the Fed will tolerate higher inflation because abusing the currency is the political and societal choice that has been made, and the Fed is part of government and society.

I’d rewrite this: “Abusing the currency is the political and societal choice that has been made, and the Fed is part of government and society.”

as

Abusing the currency is the choice which helps the elites and rich , that has been made, and the Fed does not work for common people but for its masters .

I don’t see FED being hawkish either in their action or their words.

there’s some legitimacy in that comment. and then. you’re better off having Banks than not having Banks. There is no Banking Perfect.

Why do central banks err dovish and abuse their currencies? Doesn’t inflation help those paying off debt rather than the rich elites?

For Fed balance sheet size is the problem. They should prioritize reducing it rather than rates.

issue is negtive real rates,,,,,, inflation probably higher runnning around 6-7 range if you use 1980 metholodgy,,,,,, and rates at 5,,,, after 14 yrs of negative rates,, regardless of econ stats geo political war, natural disasters,,, prices climb,,,,,,,, make cost of capital mean something,,

The Fed rate is already over 25bps higher than the Bank of Canada rate.

came to say this, can’t believe CAD has held up so well.

the BoC “paused” because they know real estate is teetering.

yesterday’s raise tells me the Fed told the BoC they plain to raise in 6 days.

Do we really have to ask that question?

And it warned that, “with three-month measures of core inflation running in the 3.5-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.”

Just like Wolf has been calling it for months

“Overall, excess demand in the economy looks to be more persistent than anticipated.”

Translation:

“It’s amazing how much counterfeit currency we actually brought into existence.”

Just wait for BRIICS to launch a gold backed currency and see the price realization of phantom debt.

Fiat currency is the mother’s milk of big government; there is no going back to a gold standard. Using a gold backed currency solely for international transactions might not be a bad idea, except that there is probably not enough gold in the world to support it.

Real estate prices started climbing in Canada again, in my hometown Nelson BC $500k for something I couldn’t live in on a busy street. Everywhere you go people are spending like crazy. 50% of adjustable rate mortgages have hit the trigger point with 100% + of the payment going to interest. The Trudeau Government passed emergency legislation to extend amortizations. Some have seen them increase to 70-90 years. We have another 2008 brewing, this time Canada will feel the pain.

I have family in Nelson and likewise watch the market there, and I am as shocked by what I see in that tiny little middle-of-nowhere town as I am with what I see here in Nanaimo (a town that anything bad you can say about it…is basically the truth).

Prices are down here about 15% here from the peak madness (early January 2022 in The ‘Mo), but that represents a sizeable bounce off the -25% pricing of January 2023. Sales are off by quite a bit, too, and anything over a million just rots on the market, but the idea of million dollar non-waterfront houses in Nanaimo would have been laughable five years ago. It’s still laughable, but it has become reality. It’s not really a robust market, unlike what real estate agents are saying, but there’s sure a long way to go until we get back anywhere close to actual affordability.

TEMPLE

Not sure if you can comment on the situation north of Nanaimo, Parksville to Courtenay?

I don’t track it as closely as I track Nanaimo, so I don’t have much to say about price action north of here. The VIREB has a good archive of stats, which is very valuable to dig into because you see the actual numbers rather than the Realtor-Spin. Even so, seems to me that there has been a big increase in the number of listings north of here. That’s true of Nanaimo, where inventory levels are higher than any time since the pandemic started. Will be interesting to see what happens now that the bond market and the real-estate-or-die crowd have woken up and realized there’s no “pivot” coming.

TEMPLE

Have friend outside of Black Creek, bit N of Courtenay. 20 acres. She is a member of local nimby organization…..no more building. And an NDP member….go figure.

Sorry, forgot, Courtenay was exploding years ago.

We sold our house in Port Alberni April 2022. 2200 sq ft 1977 4 bedroom house. Got 780k, yes now it would be 680k

Not until the loonies currently in charge are replaced.

negative amortization was something we cdn’s laughed at at sllly cuz the usa offered them in up to crash,,, guess what, we have a spike in prices again,,,,, why,, 2019 no cdn bank had over 30 yr mort,, now almost alll have 30 -35% over 35 yrs,,,,,,, nuclear time bomb,

Wolf, can you comment on the argument that the #1 upward contributor to CPI (28.5% YOY) are mortgage interest costs from variable-rate mortgages (and rolling renewals of fixed-terms) adjusting to the rising benchmark rates? Don’t the hikes statistically exacerbate, not relieve, this surge?

If that’s what you believe, you need to argue that with the BOC, not with me.

The BOC said the opposite of what you say. It’s cited in the article. Read the article!

I’ve grown weary of this trickle of rate increases. Inflation is going to rage past 2024. Currency is going to be devalued significantly and everyone is getting significantly poorer.

The fed and government is going to drag out the inflation past the general election and then we may have a deflation/stagflation, whatever. I don’t see this changing until 2024 or later…

“Currency is going to be devalued significantly and everyone is getting significantly poorer.”

From what I observe, the wealthiest 20% or so of citizen’s are able to manage inflation in a way that actually increases their wealth. Tax policies help ensure that they prosper under most scenarios.

Rumors that Buffett bought crypto,when he’ll freezes over

– The charts remain in agreement. The FED could hike the next time but the charts are also predicting that rate cuts are coming.

The Canadian bond market was surprised by the move and is now adjusting to it. The one-year yield jumped by 17 basis to 5.13% today, now expecting one more rate hike and no rate cuts within the 12-month period:

“Everywhere you go people are spending like crazy.” – Flaming Anarchist

I agree!

As inflation rages, so-called: ‘inflation mentality’, sets in because people realize that what ever something (especially something real that has intrinsic value; e.g., Precious metals, Real Estate, etc.) costs today, it Will cost more tomorrow. This has happened in other periods in other places. As some see it: Inflation is too much money chasing too few goods; I do not fully agree, but close enough.

Just heard that April trade deficit grew 25 percent or so and I was expecting less which means in my option consumer and industrials were buying . Energy is a net exporter and I thought would suppress the deficit but that’s not happening. More hikes I think

Go Stop Go is the proven method for extending if not worsening the inflationary cycle.

We need to accelerate the balance sheet rolloff. $95B a month should be a standard. If the MBS rolloff falls short, more Treasuries should make up the shortfall.

“and corporate pricing behavior “…

Haven’t heard or read on this subject lately…

Mostly about workers receiving belated increases in wages…

Had a paper-route once, remember those days fondly.

More bloody nonsense written about inflation than any other subject around.

5% inflation, or whatever we’re handling now ( depends on which stats you choose ), is hardly ‘raging’ inflation….it’s simply, marginally more inflation that we’re comfortable with, and enough that we know to stay on the brake…..but, if we have any sense, stay on the brake…subtly, gently.

The increase in residential real estate prices has resumed in some areas of the Canada……..hello, no surprise, cannot possibly increase supply with any speed, over 1/2 million immigrants each year…some with big cash, many parents/extended families rallying around the kid(s) with cash to help them with their first home ( and govt incentives for first home )…….of all the demand/supply imbalances, that’s the last one that will be resolved.

Most product imbalances will be resolved from increase in supply…..suggest will happen to autos, trucks, appliances, electronic goods etc.

Service imbalances include things like trucking, flying (goods and people), etc will be resolved with increase supply.

Rent, a service, will continue to be problematic…..people can’t afford to buy…and no amount of interest increase will help 95% of renters, the shortage of homes is that severe in Canada…..so renters have no choice but to rent….and rents will continue to increase, though, in Ontario ( largest pop in Canada ) that rent increase is controlled by law, to just over 2%…..unless/until vacated.

In Provinces without rent control, huge rent increases are taking place…..and can only be stopped, artificially, by rent controls, or permanently, by building more homes/apts…..which is less likely to happen with high interest rates.

So, BoC not helping at all with latest rate increase….

“So, BoC not helping at all with latest rate increase….”

What is needed is big reset in all asset prices and CBs can facilitate this.

BoC should have raised by 50bps if they are really serious about taming inflation.

Home prices go down drastically, rents would follow as well

I would look for actual evidence in data on housing supply shortage in Canada before spouting about that. Best to know what you’re talking about before spreading misinformation. Housing supply in Canada is no worse than the US. It will indeed get worse at this immigration rate in a couple of years. Not there currently.

Virtually nothing is for sale and no one except the Chinese can afford to buy new housing in most of southern Ontario and the greater Vancouver area. Where I live in Markham, Ontario new townhouses start around 2 million dollars with no basement and no backyard.

So what about rentals with negative cash flow from adjustable mtgs in Canada ? Bankruptcy

“So, BoC not helping at all with latest rate increase….”

Crybaby 🤣

It was as obvious as a sunrise. What these ‘pausing’ morons were thinking?

Thank you Wolf, another great article !

Bank of Canada is smart to fight inflation, and defend their currency.

The Canadian Dollar (Loonie) use to be worth, about 1 to 1 to the USD.

Now the Canadian Dollar is worth only 75 cents to the USD.

When Canada raises their interest rates, it slows inflation and makes their currency more attractive to hold. While a 1/4 point does not do much….. frequent 1/4 point raises will have an effect while not spooking the markets.

Will the Fed follow suit in June ? I doubt it.

But I’m sure we will see several 1/4 pt. rate hikes in the future.

Mr Magoo, Canadian REal Estate prices are currently in out of equilibrium.

Agent99, real estate price are crazy high in most places.

Vancouver is especially crazy high due Chinese buying, one way of moving money out of China.

Yes, Montreal and other Canadian cities are out of equilibrium as a result of Ultra Low Rates for the last many years. The return to a more normal interest rate will be painful.

Chinese are buying properties because there banks steal the money,sounds familiar .Also could be a buyout home when SHTF,.Might be the reason US is experiencing the same phenomenon also Australia.

The BoC have overseen the total destruction of the middle class over the last ten years. They are behind the Fed on rates too.

The BoC have absolutely trashed life for regular people.

Labor productivity has no effect on labor compensation, or anything in this country, graphs of the two parameters diverged starting in the 1970s with real compensation as flat as a pancake. However, the costs of everything have exceeded the percentage increase of wages, so real buying power compared to the 1970s is nonexistent.

Old Soviet saying: “They pretend to pay us, so we pretend to work.” :)

Here are some quotes from the Bank of Canada:

“The Bank of Canada today announced that it is raising its target for the overnight rate by one-quarter of one percentage point to 4 1/2 per cent. The operating band for the overnight rate is correspondingly increased, and the Bank Rate is now 4 3/4 per cent.”

“Economic growth and inflation in Canada in the first half of this year have been stronger than expected. … The Bank judges that the economy is now operating further above its production potential than was projected … Both total CPI and core inflation have been higher than projected in April and are above the 2 per cent inflation target.”

Of course, this was from the Bank of Canada press release on July 10, 2007. By December of 2007 they were cutting rates and in less than 2 years, the overnight rate was 0.25%.

Time will tell how much things are different this time, certainly there are enough factors that are different (commodity prices were still ramping up in 2007, US housing was already in rough shape, there wasn’t the same flood of pandemic spending back in 2007 and inflation hadn’t been as high or for as long, house prices and debt levels are much higher now (in Canada), there wasn’t an ongoing wave of Boomer retirement in 2007, China was growing much faster back them, reshoring wasn’t a thing in those days, the US was a big net oil importer etc., etc.) to make a case that this time is different.

To be fair to the Bank of Canada, their July 2007 statement did say,

“There are both upside and downside risks to the Bank’s inflation projection. The main upside risk is that household demand in Canada could be stronger than expected. The main downside risks are related to the higher Canadian dollar and the ongoing adjustment in the U.S. housing sector. In the context of the Bank’s new projection, these risks appear to be roughly balanced.”

So they identified the right risk, just didn’t weight it quite right :)

You have to take into consideration that the inflation rate today is grossly understated which was not the case in the past.

How come there are never talks of a “pause” by central banks when they are cutting rates? Also, where are the “emergency meetings” to raise rates?… wait for it…(crickets chirping noise inserted here)…LOL!

If it’s true the market leads the Fed rate decision then it would look to me the Fed raises rates next week.

CME Fed watch isn’t there yet but yields seem like that’s what they are pointing to.

Also seems like the central bank think tank is alive and well except for Japan!

Maybe comes down to core CPI reading next week🤷

Canada desperately needs unabated deleveraging of its real estate market. Residential and commercial.

Any which way you look at it all of the real estate fundamentals are pushed into the Monty Python level of ridiculousness.

Canadian real estate market is killing off our young, they are voting with there feet by leaving Canada for greener pastures.

Canadian real estate is also killing off any other type of the investment or business since lease rates are outrageous and business owners are collecting percent of the tips in order to stay in the business.

Canadian real estate is killing off R&D (no money left for R&D and why do it when you can just by the houses and do nothing).

Canadian real estate is threatening fiscal stability of Canada since 75% of variable rate mortgages have hit “trigger” point and now amortizations are extended into the infinity (40-90 years). This has happened due to the T2 government leaned on the banks requesting that they do everything in their power to keep people in the houses(that they can not afford to begin with and had no business buying).

Canadian real estate is threatening Canadian banks since they lent more then they should have(take a look at loan loss provisions) and now they are kicking the proverbial can down the road by extending amortizations in the hopes that inflation will ease and thus rates will ease as well.

Bottom line Canada needs major, unabated deleveraging. People should not be afraid of it. Our financial system would not be any longer a hostage to the real estate industry and cartel. We can focus on building proper and real economy based on real GDP growth(per capita not aggregate) (and not by importing unsuspecting immigrants that get shocked at what is truly going on here and leave after they get passport).

Agree. Canada is singularly focused on real estate. The affordability metrics are absurd. Ponzi-like setup.

The house of cards “should” come tumbling down but mass delusion is real and no-one in power is willing to provoke a reset.

It’s not real-estate per se. The exact same single family home in the middle of Toronto would be worth far, far more than a home in the middle of nowhere. Why? The location value / land value.

Canada is running a land pyramid scheme by:

1. making it very hard to build outside approved zones

2. constantly setting immigration numbers above known build rates

The only policy change Trudeau has made in the past 12 months was to double immigration rates from 500k to 1mm.

When people start losing their houses at renewal time there will also be a lot of boats, trailers, truck and SUV’s for sale bought with HELOC’s.

Real estate is a religion here – too big to fail, or so most believe

I thought that mortgage rates touching 6% would deflate real estate but Toronto’s real estate market seems to walk on water. Questionable suburban semidetached homes in working class neighborhoods are still selling in a week without conditions for C$1.4 million (US$1.05 million). Everyone is looking to have a basement rental or two in their newly-purchased properties to afford these mortgage payments.

It is the land of paper millionaires, massively indebted gamblers, money launderers – all but the latter living like paupers.

Can someone tell me: how does me paying more towards my variable rate mortgage every month lower the price of groceries?

It’s the worst of both worlds: I pay more towards my mortgage AND pay more at the grocery store.

As you run out of money because you have to pay more for your mortgage, you spend less on other stuff, and where you do spend money, you’re doing a lot of smart comparison-shopping to get the best deal, instead of just paying whatever, all of which reduces demand, which reduces inflationary pressure — that’s the theory.

But yeah, inflation hurts. And the crackdown on inflation hurts. That’s the price to pay for years of Easy Money. During Easy Money, everything was easy. Now we’re back to normal.

And if you cannot pay for your mortgage, you overpaid for your house – that’s a sad truth.

But you still have to eat, and all food across the board costs more now. So even if you’re careful with what you choose, you’re still gonna pay a lot. So therefore, the theory doesn’t hold up. Raising the rate just punishes people, without the benefit of stopping inflation.

What to say savers who for 15 years lose the purchasing power of money so that borrowers can use the free money?

Of course it holds up. Substituting to cheaper product in aggregate has the desired effect.

It helps push companies to make different decisions on pricing / volume tradeoffs.

At the individual level, for 95%+ of the population it also works because most people don’t optimize their spending along primarily price vs sustenance considerations. Most can indeed shift down to other less expensive alternatives (brand, product type, etc).

Or, in the case of today’s environment, shift out of some categories altogether (travel).

In Canada, due to prevalence of variable or “semi variable” mortgages, you might expect an even more significant shift. But these things take time. Especially when the psychology is so entrenched that “things are fine” and that assets (almost exclusively homes in Canada) will resume an upward price trajectory into perpetuity. It dampens the near-term effectiveness until/unless a real breaking point occurs. Like a sharp rise in unemployment.

Been buying cereal &1.48-1.99 a box ,on sale .Give to food bank.Good for the soul

The answer is while money/mortgages were cheap the money that was available for eating out, new wardrobe, vacations, new phones, whatever should have gone towards paying down debts and saving for the inevitable return higher interest rates. So now that debts have real costs people need to tighten their belts to just the necessities and if that still isn’t enough they have to accept they borrowed too much and make very hard choices.

Lev,

Higher interest rates WILL stop inflation. They’re just not nearly high enough. For interest rates to stop inflation, they need to be MUCH HIGHER THAN CORE INFLATION.

What we have now are interest rates that are still mildly stimulative.

“Higher interest rates WILL stop inflation.”

You mean higher interest rates WOULD stop inflation, were they to be implemented. But it’s extremely unlikely that they will.

Me, a crybaby, nope, not the way I see it Wolf.

Sitting high in the water, can handle a storm.

For BobbleheadLincoln, i know what I’m talking about brother, thank you, my income is from that sector.

House prices may well slip, as recession, rate hikes, take their toll, but the radical shortage of housing at prices that are affordable, and the high and rising cost of new builds, will constrain any downturn….with eager first timer’s stretching to the max, with family help, to buy.

Rental prices, in most mkts, will not follow….the shortage of rental accommodation is so extreme.

In mkts where there’s rent control, mine, in Ontario, rent’s will ‘show’ increases for the next many years, as landlords take the opportunity to raise a rent dramatically when a unit, finally, becomes vacant, often after years of being under rent control.

The turnover on my units is way down……

And I’m saying, increasing BoC rates will not help the real estate mkt….not any sector of it…..will not reduce rents….will only reduce prices moderately……and will make new builds more expensive, and less likely to be built.

Won’t do any huge damage either……possibly as MrMagoo suggests, it’s about the rate of exchange v the U.S. dollar……or maybe anticipating a U.S. raise, this time or next, and jumping ahead.

I advise you to go back and read the Wolf statistics for Canadian real estate in April.

For the month of May, Toronto deals are still down year-over-year even by a little bit, but it’s the spring season after all, so it’s normal for prices and deals to increase. Yesterday BoC winked at you again. I see prices falling for the first time in 11 years in the Atlantic provinces. In Montreal for May you are at – 8 pr. deals per year and a drop in prices on an annual basis.

Nah, tannin is correct. The market remains red hot. I don’t think sustainable but it is a market in rebound at the moment. The BoC decision, if followed by more and if it has a broader economic impact (ie employment) may cause resumption of a down trend (which I personally view as necessary). But today, right now, the market remains hot.

Today, the market is hotter than April but cooler than May 2022 across Canada.

You’re completely wrong. Real-estate rose as rates were cut.

Ergo it will fall when rates are raised. And it is.

I know several people at work on variable who were all very, very aware ahead of yesterday’s BoC decision about the meeting. These are regular people who would have had zero clue about BoC meeting dates under normal circumstances. Why are they aware? Because their mortgage is killing them.

Next up big 4 Canadian bank layoffs. After that forced sellers into a downward market where banks won’t lend.

Funny all this talk about Canadian real estate excesses, with only a few commenters mentioning the role of immigration, especially Chinese immigration driving up prices. Canadians seem a little too politically correct. Sometimes it is necessary to recognize the reality that penetrates the thin veneer of civilized discussion.

The last of the rich Chinese emigrated to Canada in 2016. The rest of the immigrants coming to Canada earn a lot less than the average Canadians and very few come to Canada with significant wealth. Rents are increasing in the places immigrants emigrate to.

After Australia and Canada unpaused last meeting and increased rates by 0.25% in June meeting, the lame good no good Indian central bank (RBI) governor paused TODAY like last meeting . Moment he said “PAUSE” ,I switched off the video not willig to listen to his bull story of inflation decereasing !!

When is it going to sink in that Keynesians are in full denial of Gibsons ‘paradox’. Which was an explanation for why prices rise with increasing rates and wasn’t called a paradox until Keynes decided to call it that. He didn’t understand it, or it didn’t fit his models and narrative.

Followers of Keynes are very religious in denying reality when it doesn’t match their models

Gibson’s ‘paradox’ explained in short: “Raising rates raises the costs of doing business. Those rising costs have to be paid for … by higher prices.”

No paradox there. Just common sense.

But Keynesians believe that raising interest rates will ruin the economy, causes unemployment, make people having less to spend, takes demand down, and that will force prices lower.

Is that how we want the world to work?

Or are we accepting reality that raising rates will raise the costs of everything and then ruin peoples spending power, then causes demand to go down, then weak businesses will go under, supply will go down and the remaining businesses can freely raise their prices … again.

Some basket components will follow Gibson’s paradox, like food or durable goods, but others will take a disproportionate inverse effect, like shelter.

But you can sense between the lines that monetary policy is about causing pain, politely called “demand destruction”, unemployment, increase in mortgage payments, defaults etc. This incentivises wage slaves to trade their blood and sweat labour for tokens created out of thin air.

This theory of higher-interest-rates-cause-inflation is beyond dumb, it’s a total misrepresentation of how an economy works.

Prices are set in the market by the maximum amount that buyers are willing to pay. Overindebted companies that cannot lower their costs simply fail and vanish (so now we have a surge in bankruptcies for that very reason). There is no paradox. Just everyday reality of running a business: the high-cost producer loses.

The willingness by buyers to pay higher prices determines prices, not the costs by some over-indebted seller (over-indebtedness is a company specific issue).

The only exception is when the company has a monopoly, such as a regulated utility that applies for price increases based on a cost-plus formula; they can pass on higher costs without being crushed by buyers unwilling to pay those prices.

Inflation is in part psychological – the inflationary mindset, and when it takes off, something drastic needs to happen to tamp down on it. Higher interest rates and/or an increase in unemployment can accomplish this “drastic” event that causes that mindset to shift, causes buyers to be reluctant to pay higher prices, and causes demand to fall, all of which put downward pressure on inflation. But we’re not there yet.

Yes, higher interest rates cause some pain for some people, obviously. And that’s what it takes to tamp down on inflation.

Only free money is painless money. But free money is a gift from hell, as we now see, because eventually, you end up with this massive bout of inflation that we now have.

EARNING higher yields (more cash flow from fixed income investments) can stimulate demand a little by those that get this cash flow, but it’s a relatively small counteraction to the much larger action of higher interest rates reducing demand.

“The only exception is when the company has a monopoly, such as a regulated utility that applies for price increases based on a cost-plus formula; they can pass on higher costs without being crushed by buyers unwilling to pay those prices.”

Monopolies/Oligopolies can raise prices by edict or in suit, but higher prices still face elastic demand curves and less will be consumed.

Less consumption, lower GDP, prices fall. Even if it means falling somewhere else, including layoffs in the Monopoly.

Thanks for taking the time to go through this, Wolf. You have burst apart several widely held fallacious beliefs here. Excellent!

Very well said Wolf!

Am aware, William Leake,, that some of Canada’a immigrants, often Chinese or Indian, come with considerable wealth, and of course buy homes……….should we forbid them to do that ? Or forbid them, but allow immigrants from the U.S. and Germany to buy homes ?

Silly stuff…obviously, if you’ve immigrated, you’re entitled to buy a home.

Gov. of Canada has stopped homes from being bought by people/companies living/registered in other countries, with broad exceptions, Provinces, BC and Ontario already had extra purchase taxes, think 15 and 20%, for those buyers who are not living here, people and companies.

So moves being made to stop those, minor statistically, but still part of the problem, purchasers from buying.

Contrary to your understanding, there’s nothing politically correct about ‘not discussing’ the subject….it’s been discussed at provincial and federal levels, and laws have been passed by at least two provinces and the feds to try and help.

Canada is a very large country geographically, but the “living zone” is a small strip along the Great Lakes/St. Lawrence plus Vancouver/Lower Mainland.

It is a moral insult to invite more people to crowd into the tiny living spaces left in Canada.

Nice article that captured the essential standard presentation of the Central Bank of Canada. First off, the idea that the Canadians are battling a 4% rate of inflation is flatulent. I suspect it is one standard deviation beyond the US measure of 5.2% and at the upper end of the probable outcomes at 7%.

Thomas Jefferson and Zachary Tailor, among others, warned that:

Inflation is one of the cardinal sins that have the potential to destroy Democracy.

The laisse faire attitude toward such a fundamental oppression of the God given opportunity and right of future generations to succeed offends me.

They seem afraid to say that the world wide inflation is completely anchored and that there will be automatic increases in the interest rate as long as prices increase.

Inflation is similar to an insect infestation that generally requires killing it all. Always better when the hive is small.

Maybe keeping in mind that:

Life is a beautiful struggle with it’s own rewards.

That being said, laying the groundwork for the takeaway that I would like to leave is that what their selling is us, without paying for the privilege.

Silicon Valley has stooped to the level of peeper to stay relevant. Spying capitalism like the USSR had.

Love is my most painful memory which I didn’t anticipate.

Because the commitment required a lot of hard work, a couple of jobs, which seems obvious now, 50 years later.

One can only remember the life one has lived. Imagining something that might have been should be returned to the rejection bin that houses the fantasy that often motivates human beings.

All those comments and not one person EVER said anything about the imploding quality of life while real estate prices have exploded. Notice how government benefits while families can’t cope increased costs. A healthy society doesn’t need high levels of immigration which is simply used to mask inept management at the national level. As always morality is crowded out by greed and no capacity for long term thinking.

What has kept the Canadian economy alive is HELOC’s. You can borrow 65% of your equity. I had a HELOC for years at 3%. I used it to buy a new ( used) vehicle every 10 years. You can pay for anything with it and the bank sets it up on your Interac card. $200 dinner hit savings ( instead of chequing) and it goes on your HELOC. Make the minimum interest payment. Only problem is HELOCS are variable and rates have doubled to 6%

I haven’t heard any mention of the debt Canada carries. Federal Gov over 2 trillion, Ontario over 500 billion, consumers mortgage and credit card 2 trillion, City of Toronto 1.5 billion with a huge budget deficit. And that’s just for starters, the other provinces and cities aren’t in much better shape. Canada heading towards Mexico and Greece eye opener soon