Just when European banks need to inspire confidence more than ever.

By Nick Corbishley, for WOLF STREET:

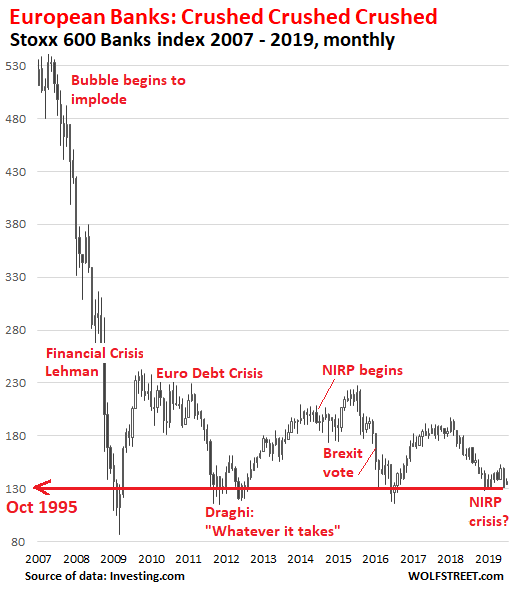

European bank stocks continue to get hammered near multi-decade lows by a slew of problems, including the ECB’s monetary policies, particularly its negative-interest-rate policy (NIRP), festering nonperforming loans, and a well-deserved lack of confidence by investors. This was just exacerbated by a scathing new report from the European Court of Auditors (ECA) highlighting a litany of problems and shortcomings with the European Banking Authority’s latest stress test. Among other things, the test ignored some of the most common factors that cause a bank to fail, excluded many of Europe’s most fragile banks, and used simulations that were a lot more benign than the last financial crisis.

Banking stress tests are supposed to gauge the resilience of a banking system by imposing a hypothetical shock — or “adverse stress scenario” — on a large share of the system’s banks. The problem in Europe is that the European Banking Authority’s stress tests have tended to ignore, rather than identify, many of the worst stress points in the banking system, which is probably why many of the Continent’s worst banking failures, including Bankia BFA, Dexia and Banco Popular, have happened shortly after the banks in question had passed a stress test.

Unlike its counterparts in the UK, the US and Japan, the European Banking Authority (EBA) does not itself calculate the impacts on banks of the adverse scenario; it leaves that up to the banks themselves. It does not even corroborate the information provided or conduct on-site inspections.

This is just one of the many problems the Court of Auditors has identified with Europe’s latest stress test. Here are the other main ones:

1. Some of the riskiest banks were excluded from the test. The number of participating banks has consistently fallen since the first round of stress tests. In 2011, 90 banks in 21 countries participated. By 2018 the number had shrunk to 48 banks in 15 (out of 28) countries. Some of the banks that have fallen off the radar are among the most at risk, including lenders that:

- Have recently been subject to restructuring or a merger.

- Are from countries where banks have considerable exposure to their own sovereign bonds (e.g. Italy).

- Have a high concentration of non-performing loans (e.g. Greece; Cyprus, Portugal and Bulgaria).

2. The adverse scenario did not even contemplate some of the most important systemic threats facing Europe’s banking sector. A financial stress test is only as good as the scenarios on which it is based. In its latest test the scenario cooked up by the EBA not only failed to reflect the risks posed by a likely future reality, it didn’t even reflect the risks posed by the current one.

In its latest stress test, the EBA tested banks against an economic downturn rather than a shock stemming primarily from failures in the financial system, even though it was this kind of shock that triggered the last major crisis. In fact, it “did not even use an event or a risk within the EU” as a trigger for the adverse scenario. “Nor was consideration given to an event or a risk from within the banking sector,” despite the myriad systemic risks (nonperforming loans, struggling Italian lenders, Deutsche Bank, …) that continue to linger there.

Here’s a list of the systemic banking threats the EBA’s last stress test largely or completely ignored.

- Non-performing loans, despite the fact they were the cause of most bank bail-outs after the financial crisis and remain a significant threat to financial stability, as the ECB itself warned just last month.

- Banks’ liquidity risks. The stress tests focused exclusively on bank solvency, completely ignoring liquidity issues, even though liquidity risks are rapidly rising across many different financial markets, as the Bank of England recently cautioned.

- Negative interest rates, which are seen as one of the biggest obstacles to banks making money and which are expected to become even more negative in the near future.

- Other adverse effects of central bank policy. Given that the ECB was heavily involved in the EBA’s scenario development, it’s perhaps no surprise that the ill-effects of its monetary policy decisions were not (and never have been) considered as a trigger for an adverse scenario.

3. The adverse scenario was a lot less severe than the 2008 financial crisis. For 23 out of the EU’s 28 Member States, the projected impact on GDP of the adverse scenario for the 2018 test was less pronounced than the financial crisis, with the UK, Malta, Belgium, Sweden and Poland being the only ones that fared worse. The projected effects on unemployment, credit spreads on sovereign bonds and banks’ capital levels were also far milder than those experienced during the financial crisis.

This begs the question: how is it possible to gauge whether European banks are better equipped than ten years ago to withstand a severe stress if the adverse scenario is a lot less severe than the last crisis?

4. Banks’ calculations remain a black box to the EBA. In limiting its role to broadly coordinating stress-test activities, the EBA “makes no genuine efforts to ensure reliability and comparability” of the results produced by the participating banks, many of which have grown so big, complex and opaque that it’s virtually impossible to form an accurate impression of what’s really happening on and off their books.

The EBA did not conduct any on-site inspections to verify the data provided by the participating banks. Nor did it take steps to ensure the relevant “competent authority” (either the ECB or the respective national central bank) was carrying out rigorous checks on the data provided by the banks. In fact, to handle the entire work load of the 2018 stress test exercise, the EBA appointed “around seven” full-time employees.

In light of all these glaring procedural flaws, oversights and staffing constraints, perhaps it’s no surprise that the EBA’s stress tests have failed so spectacularly to restore trust in Europe’s broken banks, as perfectly demonstrated by the never-ending downward spiral of their share prices. While some central banks may claim that the results of the last test demonstrated the resilience of the banks they supervise, investors are clearly having none of it. By Nick Corbishley, for WOLF STREET.

$30 trillion of assets globally are held by open-ended funds similar to the funds that just ran around. Read… Liquidity Crisis at Woodford Equity Fund Is Symptomatic of Systemic Problem, Bank of England Warns

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

“When things get serious, you have to lie” – Jean-Claude Juncker. The Court of Auditors did not get the memo!

“Sir, I take offense at your comment, Germans do not lie….”

“Ok, actually, I’m not German, I’m from Luxembourg.”

I have heard that the stock market is still being manipulated. I think that without manipulation, many bank’s stocks would be even lower than they are, because the derivatives gambling exposure of so many banks is so enormous. If the stockholders had any idea of how high the risks are, and how difficult it would be to bail out all of the connected entities in this gambling paradise of banksters, they would drop most banks’ stocks.

Be aware that there is “minor” manipulation is already publicly known to those familiar with the subject, so that do not be surprised if the collapse is later so great that other manipulation, e.g., by central banks like the banksters’ Fed purchasing the stocks of EU banks, may exist. As to the technical manipulation, watch a video called the Wall Street Code, before the banksters pull it off Youtube.

Be aware that dishonest brokers, and I would not identify who they are, prefer for you to make market value trades. That is online trades that are specified to be executed at whatever is the market price when executed. In a variation of what that Wall Street Code video describes, if I were a dishonest broker and you place a market value order for (e.g.,) AMD stock at $32, if I received 50 orders for that stock, I would buy the stock for those 50 customers at $32 from third parties then sell it to each of those customers at $32.20, for example.

Of course the profit from each individual trade would be minor. However, if I did this over thousands of trades for years, since the Society for the Encouragement of Corruption is as competent/honest as a decomposing, dead bovine, and would not act to stop it if I am “connected” as B. Madoff may be believed to have been “connected,” the profits would accumulate.

If I ran a major brokerage, the annual profits would be enormous. Of course, I would have to be of the right group, so that I would do this with impunity. That is the current situation in the U.S.

A form of organized crime, whether connected or not to other organized crime, whatever the rumors say, now controls our finances. The financiers have become a parasitic class that thrives on defrauding their customers.

The Furher of the rich just removed the requirement that financial advisors act as fiduciaries to customers. Thus, thousands of Americans in the middle class are among the gullible suffering for these frauds.

Why are crooked, poorly run banks still valued at all by the stock market? I wonder if gullible persons are being made to invest in these risky banks run by banksters by brokers and financial advisors. Most politicians and judges are beneficiaries of this system, so do not expect any action anytime or ever.

By the way, these schemes become more difficult to detect or punish if it is a group of crooked brokers that engage in this behavior. If one broker executes a purchase at $32.20 at the then increased market value (e.g., $32.20) after his crony bought the stock at a lesser value ($32) and offered to sell it at $32.20 via computer programs a millisecond later, they have captured their profit, these transactions can later be collapsed by the two brokers doing the trades and dividing the profits of their frauds then or later. My example above was simplified.

No covert meeting to divide profits need occur. To hide the division of profits disadvantageous trades can be made: e.g., the broker that got the profit from the transaction described above can then sell or buy other stock to the other crony broker, so that crony broker shares in the profit via computerized trading.

This type of civil conspiracy is closer to what actually goes on via computerized trading. Unless a competent programmer audits the code, all of it, or standard code is used by ALL brokers, this will continue for the foreseeable future.

These kinds of schemes are the use of math to make illegal profits like the 1930s numbers games or fixing horse races or boxing matches. I doubt that the society for the encouragement of corruption will take any effective action.

I predict that they never will. Read the story of Madoff and how his family members turned him in after it all collapsed. Was this done for the public good? You be the judge.

If he was not in jail, I believe that he might have been found dead later due to the anger of the persons whose funds he managed: e.g., if he was not safely in jail, he might have been found floating dead in some swimming pool.

By the way, I believe that schemes like this are being or are going to be used with computerized voting machines. The Junior Bush dispute about chads in Florida was one way to win in an election.

Through computerized voting, the theft of elections will be streamlined and made more efficient for the future. It is good to know that the crooks are becoming more efficient in controlling our government, is it not?

Well, I am happy to hear that an organization actually has a modicum of credibility left. Many orgs playing Liar’s Poker these days. What a show it will be if the CB’s cannot provide the massive liquidity if things start to degrade very quickly in the EU banking sector.

I watched a special on the 1929 crash on You Tube recently. The crash was attributed to lack of financial market regulation, causing a loss of faith in the banks, credit drying up, and thus the Great Depression.

I also watched a special on the 2008 crash. This resulted from bank deregulation. (Shades of the S&L crisis after they were deregulated. )

Now, we’re seeing problems in European banks where the regulators are taking the banks’ unsupported word that all is well (remember “liars loans” for home mortgages?)

We’re not remembering the past, so we’re doomed to repeat it.

Events are often over-determined. In the USA the Great Depression was related to the chestnut blight, the mechanization of agriculture and the immigration bubble of the early 20th century. It was the adjustment going from 50% in agriculture to 2%. The Fed was a relatively minor player

Now you all know why the SP500 is above 3000

Or must I draw the picture?

The SP500 has been climbing for many decades. It continues to do what it has always been good at. Sorry.

Decades! Right.

Sorry I missed that 2009 lowest.

Capital flight that’s what it is.

Dollar is the least dirty shirt and everyone knows it.

2009 was one of the best years for the S&P 500.

2010-2019 was good too.

Excellent Article!

Thank you John,

great article, bad news.

the EU is imploding, this has been the case ever since the Germans and the French decided to swallow the rest of Southern, Eastern European problematic Economies

( at the behest of the US)!

Was it to protect these countries from falling under the clasps of the ( bear)?!

Well it seems that didn’t work out, and we’re edging slowly towards the Europe that we know better:

( a fragmented Balkanized little democracies) groaning under the influx of Human waves coming from the south to claim their piece of ( paradise)!!

The Scandinavian School of Free for all Economics is proving very shaky day by day, the Germans are at their wits end due largely to the pressures brought on them From their allies across the Atlantic and the Brexit debacle.

The Italian Economy is No more!

The Core of the EU is now well and truly Rotten, France , Germany and Italy will succumb to the Credit Crunch quicker than your proverbial Hail Mary!

The result?

A fantastic opportunity for new restructuring of these countries on entirely new Model , a real diversity with no overbearing EU bureaucratic bs .

That should hearten the Swiss to make more cheese and watches to sell their Neighbors ( at discounted prices).

I was just chasing links about ECA and Dublin-based Depfa Bank and its owner Munich-based Hypo Real Estate and various bailout (guarantees) back in 2007 — and now see that Bank of America London is moving operations Dublin, because of BREXIT. It’s interesting that so many bailed out banks have amazing amounts of liquidity — after stealing trillions during the last decade! Who could have possibly guessed that these pirates would be doing better than the people that lose so much.

This was an interesting comment I came across FYI:

“While I understand what they’re trying to do, only the 5 per cent of the population in Dublin earning over €100,000 could get a mortgage equivalent to the average home price in the city,” says Murphy, referring to the Central Bank rule on most mortgages not breaching 3.5 times income.

“You’re creating another bubble, not in the property market this time, but a bubble in rents and social inequality and political inequality, which is a bubble in itself. When you press down hard on one sector, you’re going to create something on the other side. You just need to get that balance and they’re definitely not getting that balance now.”

That’s from a Irishtimes article about “the day the banks stood still” published last Sept

Didn’t US stress test pass DB?

DB’s US arm passed the stress test. If the total of DB was stress tested, my guess is the results would be different.

The entire European Banking Index seems destined for zero, as it is very difficult to fund your operating costs in the wake of NIRP forever.

Well the model is to keep foisting debt onto the ‘little people – ie, the model is usury.

A family member of mine (UK) has just been given a 6 month lease on a new VW 4×4 – that’s how desperate things are getting, they’ll lease you a brand new automobile for 6 months. After that it’ll quite possibly go into storage, ‘cos who’d lease a 6 month old one when a new one will only be a few pounds a month more?

Got gold? You betcha.

Still don’t buy into the gold thing. It’s not “coin of the realm” in the USA, and here is where I must buy food and shelter, and all the other pretty much mandatory services/needs,. Plus I have no secret place to hide it until everybody has forgotten about it. So, being in the bottom 90% net wealth, albeit towards the higher end, above median 10-20%, I think, I guess I’ll stick with a CD ladder, and just plan on looking into joining up with a good warlord like in Somalia, if the worst happens. I suppose speculating in it (or anything else) would maybe help with net wealth, but I don’t have the info, or skills to play those games.

If only I had a room sized 100K farad capacitor that I could slowly fill….sigh….

I should imagine that the three things keeping European bankers awake at night are ZIRP, NIRP and that €45 trillion column in the DB Balance Sheet.

Banks have had a cushion for the last 10 years where their loan book and borrowings were at much higher rates of interest than at present, but that cushion is less comfortable now as 10 year paper expires and to quote Buffett “when the tide goes out, you can see who is naked”

The “notional” DB derivative exposure wot causes many to blink and check if the figure is in Millions and then look again when you realise it is in Billions, is supposed to be mostly hedged according to DB.

By whom?? The problem 10 years ago was when it was suddenly realised that those on the other side of the hedge could not pay, and then we were talking about a $200bn problem. When we are talking about problems that begin with a T, everybody fails, because everybody is interconnected. All those warehouses which supposedly hold physical metals will suddenly be shown to be a couple of filing cabinets in the corner stuffed with IOU’s

The downfall will not be because DB suddenly fails at close of play on a wet Friday afternoon, but because one of the supposed insignificant fringe banks will fail and light the fuse, just like Bear Sterns did.

I sometimes wonder if some of the crazy Guns and Canned Goods fellows over on Zero Hedge might have a point.

As one of the nutters over at zero H, all I can say is: “What me worry?”. Nope, just watching.

Hopefully, most people will have their physical metals in their OWN safe place if they want to keep it.

Many moons ago in the mid 70’s when I was a young Army Logistics officer, I was taking over as Technical Officer for the British Army unit in Germany which held all the armored vehicle reserves.

I was asked to sign that I had taken possession of XXX vehicles, but was surprised to find that 50% of the vehicle stock was “notional”. and had been so for years. Were a conflict to have taken place with the Soviet Union, my “fleet of notional main battle tanks” might have cut quite a dash!! The difference between theory and reality.

London, Amsterdam and Munich were identified as cities with property bubbles. Could the hinterland be in any better condition? Sydney was a bubble. When it popped so did Australia. I do not know Euro banking laws. Self-guided stress testing might mean anarchy as you have pointed out.

You’d think the profits from loan sharking and creeping fees would be plenty to cover the gambling losses and executive “bonuses”, but that would depend on all the other “expenses”.

Wolf could almost recycle this article yearly ECB/EU banking “Stress tests” are and always have been Pseudo stress test, that it is impossible for the tested bank’s to fail.

They do this for the simple reason that they do not wish to upset the whole rotten house of cards that is Eu banking, in particular club med banking.

Pretense everywhere, whether stress testing or underwriting.

Saw today that BNP Paribas and Standard Chartered were underwriters on a $300M bond deal back in March for Indonesian issuer Duniatex, a textile manufacturer. Due to the trade war with the U.S., China is flooding Indonesia with cheap textiles. S&P downgraded the bonds six notches to CCC- this week (Ouch!). Those Duniatex bonds which sold near par in March are now trading at 37 cents.

This particular bond issue may default before even a single coupon payment goes out.