Includes mortgages already delinquent before they were swept under the big federal rug of extend-and-pretend forbearance programs.

By Wolf Richter for WOLF STREET.

The mortgage delinquency-and-forbearance mess keeps getting messier – in record-setting ways. At the same time, the record-low mortgage rates continue to push certain other segments of the housing industry toward ever greater exuberance. That contradiction became humorously obvious on the Bloomberg News Economics front page, where side-by-side these two headlines appeared:

The overall delinquency rate for mortgages on one-to-four-unit residential properties soared by nearly 4 percentage points (386 basis points) during the second quarter, and by June 30 reached 8.22% (seasonally adjusted), the highest in nine years, according to the Mortgage Bankers Association’s National Delinquency Survey.

This nearly 4-percentage point jump in the overall delinquency rate was the largest in the history of MBA’s survey going back to 1979.

Delinquencies started soaring in April. A month ago, CoreLogic had reported that the percentage of mortgages entering the early stages of delinquencies — from 0 days to 30 days delinquent — had spiked phenomenally in April beyond all prior records. What we’re seeing now is that many of these mortgages are becoming more seriously delinquent. This shows up in the stages of delinquencies, according to the MBA today. At the end of June:

- The 30-day delinquency rate fell by 33 basis points to 2.34%

- The 60-day delinquency rate rose by 138 basis points to 2.15%, the highest since the survey began in 1979.

- The 90-day delinquency rate jumped by 279 basis points to 3.72%, the highest since Q3 2010

The delinquency rate of FHA mortgages jumped by nearly 6 percentage points (596 basis points), the biggest jump in survey history (since 1979), to a delinquency rate of 15.65%, the highest delinquency rate in survey history.

The delinquency rate of VA mortgages jumped by 340 basis points to 8.05%, the highest since Q3 2009.

The delinquency rate of conventional mortgages jumped by 352 basis points, to 6.68%, the highest rate since Q2 2012.

Delinquency rates here include mortgages that were already at least one month delinquent before they entered into a forbearance program. So these mortgages are still delinquent, and the borrower has stopped making payments before entering into forbearance, but the lender has agreed to not pursue its legal rights for the agreed-upon period of forbearance.

Instead of the borrower either catching up, or the mortgage going into foreclosure, the mortgage is put on ice during forbearance. The borrower doesn’t need to make payments. And the lender, after putting the delinquent mortgage into forbearance, may no longer consider the mortgage delinquent, and may therefore still show the mortgages as “performing,” and may still show interest income from it, though no one is making payments.

There are now 4.2 million mortgages in forbearance, according to estimates by the MBA. Meaning 4.2 million homeowners have stopped making payments, in addition to the homeowners that have stopped making payments but are not in forbearance programs.

The delinquency rates here do not include mortgages that have undertaken the final steps: moving into foreclosure. But the current trend for lenders is to move mortgages into forbearance and put them on ice for as long as possible – “extend and pretend” – rather than foreclosing on the property.

The states with the biggest increases in delinquency rates at the end of June compared to the end of March were:

- New Jersey: +628 basis points

- Nevada: +600 basis points

- New York: +575 basis points

- Florida: +569 basis points

- Hawaii: +525 basis points

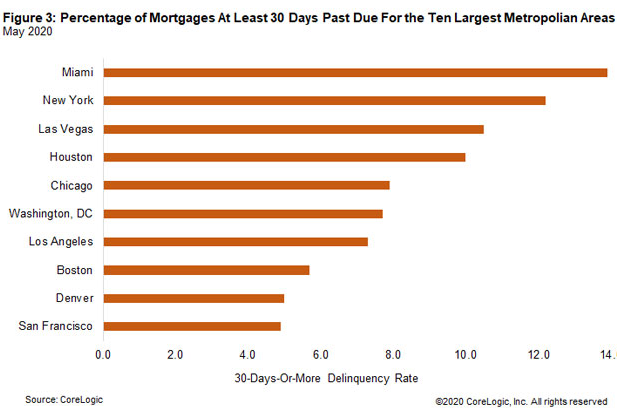

Last week, CoreLogic released a report that showed the 30-plus day delinquency rates in the 10 largest metropolitan statistical areas through May. So this lags by one month the MBA’s report, but provides insights by metros. These delinquency rates at the end of May ranged from 4.9% for the San Francisco metro, to 13.9% for the Miami metro. This data also includes mortgages that were delinquent before they entered forbearance (chart via CoreLogic):

Other smaller metros got hit hard too, with the sharpest increases in metros that are dependent on tourism – such as Kahului, HI, and Las Vegas, NV – and metros in the oil patch – such as Odessa, TX. And Houston, in terms of an oil-patch metro with a massive delinquency problem, is already on the list above, number 4 in the chart, with a rate of just around 10%, just below Las Vegas.

This mess playing out in the mortgage market has been largely swept under the rug of widespread, government-supported forbearance programs – to where no one really knows what will happen to those mortgages when these forbearance programs end. And the exuberance in other parts of the real estate industry, such as with homebuilders, and even with mortgage brokers and mortgage lenders that arrange refi and purchase mortgages, is a contradiction to what is going on with these swept-under-rug delinquencies that will eventually come to a head.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

home prices have been tesla-ized. More mortgage delinquencies = higher home prices.

LOL………I was going to say the exact same thing. The more things don’t make sense the HIGHER prices go…….my sister and her hubby were looking at houses over the weekend and she said “they are selling faster than we can look at them”

Worse economy in the history of the nation, 60-Day Delinquencies Hit Highest Level Ever, so any thinking person, using logic and reason, KNOWS that must mean highest home prices ever, highest stock market ever……

The old saying “markets can stay irrational longer than you can stay solvent” needs to be updated to mainstream 21st century thinking……revised: “markets can stay irrational”

In the search for the square root of negative 1, markets have the answer!

;-)

You can’t figure out why home prices are rising ? Your sister is the anecdote! She’s one of the reasons why home prices are rising.. for now.

Possible demand coming from people trying to escape the cities?

Long time lurker. First post :)

Thanks for the content Wolf.

“markets can stay irrational longer than you can stay solvent”

Agreed – on possibly the most enormous scale in history. If the consequences of these dynamics were not so dire, and the victims not real, I would be tempted say that witnessing them play out in real time is an amazing experience. These feel like exceptional times.

If you don’t have to pay for something you want more of it.

This is an analogy to the saying: “if you subsidise it, you get more of it”.

I bet they weren’t looking “downtown.” I suspect house prices in “the burbs” are going up as people are fleeing the riots and pandemic in the cities.

Idk why idiots like you think the riots are in an entire city. It’s literally like 3-5 blocks in a down town area with businesses only. In my city they had protests that never changed from peaceful Marching. The vast majority of protesting has been peaceful until they cops show up and shoot people.

My city has 5 million people in it. It’s not Portland but no where is as bad as Portland.

@Big City Gal………Riots may only be in a 3-5 block radius but that’s still enough for people to not want to come in or live the city.

If delinquent mortgages are in forbearance they won’t enter the market as forclosures, thus keeping the price inflated.

Justin:

You are correct. I think that keeping prices up is the main reason for these forbearance programs. My suspicion is that, as soon as the election is over, these programs will end. When that happens, prices will start to decline.

Will the price decline turn into price free-fall? We will find out in December.

My house will close escrow next week…

I’m moving out of state and plan to rent until there is a correction.

Have to believe it is going to be a big correction!

The federal govt has said nobody will be foreclosed on and nobody can be evicted by their landlord. And then people are SHOCKED that people stopped paying rent and their mortgages? This is rational behavior by people who know there are no more consequences to bad behavior.

Who are you claiming is shocked? Can you give some examples of people being shocked by this?

Any good person who used to have faith in government. Most people realize now how bad their elected officials did through this whole mess. Good people are still good, they just know better now.

Well I guess the people get what they elected: politicians in cities that allowed the mass destruction of large areas and crime running rampant. No wonder people want to ‘escape to the country’.

IMO the USA has the dumbest bunch of politicians in the world running the large cities and states.

The House and Senate are full of idiots.

Makes one wonder how they are even able to function in normal, everyday life.

And I don’t feel sorry one bit for those idiots who elected them either.

And the rot doesn’t stop there either.

Another story about another another spy ‘uncovered’ at the CIA (How the hell did he get and keep his security clearance?) ; the FBI lying; the DOJ covering up.

Things were bad with those three letter agencies a long time ago and they have gotten worse.

No wonder countries like Japan and Australia and others, even with all their faults and problems, are doing so much better than the USA.

Not sure how rational people would be shocked by the government mandated rules that lacks any real thought.

It’s a very perverse set of incentives targeted on people who have for over the last decade decided that there might not be a tomorrow, so it’s time to go YOLO.

But I suspect that there are a good number of people out there who still try to do the right thing and pay rent and such on time even though there is an awful temptation just to take advantage of the perverse government incentives.

I wouldn’t say I’m shocked, but yea a little surprised. I have this naive part of my brain that assumes that the piper must always be paid, I unfortunately can’t shake it.

Anybody who paid for their / their kids college without any loans, or has already repaid loans, would be a fool not to not take advantage of either temporary or perhaps permanent bailout on this. Sorry, I’m too old and cynical.

“no one really knows what will happen to those mortgages when these forbearance programs end.”

Will they end, at least in a reasonable timeframe (however that is defined)? While many people are legitimately in a tight spot, for others this type of forebearance will only reinforce their sense of victimhood. They won’t want to begin repaying even when they have the means.

That might sound mean, but…

A year from now that sentence will read “no one really knows when these forbearance programs will end”.

It’s always important to remember that it’s an election year, I would expect alot of the eviction suspensions, enhanced unemployment, and the like to last at least until after the election. The fact that Trummp’s extra 400 a week lasts until dec 6th (or until money runs out) only weeks after the election is telling. Alot of things will be extended at least until after the election up to a small length of time into 2021 and then it’s anybody’s guess.

Yes, maybe dec 31. Both parties are tired of spending on workers, IMO changes after the election.

But maybe they will instruct the gov mortgages to be modified with a new 30 year term and including the missing payments rolled in, as a one time event. Then what for those still unemployed?

When the landlords start going broke, and the banks can’t sell CDOs any more, forbearance will end.

I’m more than a bit suspicious of these stories of people choosing to spend the rent / mortgage money even though they remain employed. I expect there are some folks stupid enough to do so – there are always some stupid people. However, I expect most people not paying their mortgages/rent are either already in dire straits, or see the abyss in front of them and are putting away a nest egg for the even worse times to come.

Yes, consumer spending is up – but all that says is that someone is spending more – it doesn’t say who is spending. I’m still employed, and working from home means more money in my pocket even after paying all the bills. I expect I’m not the only lucky one.

I can guarantee you that in my area (an average sized Midwest city) where a 1 bedroom apt. with utilities is $600, that ALOT of people living in apartments simply chose not to pay. I know several landlords that own a bunch of small apartment buildings in my city. Most of the non-payers were getting unemployment (and getting much more than they are usually paid) or long term free money disability or something of that sort.

Those renting houses in my city were far more likely to pay. It’s important to note, the housing market is rated as red hot right now.

If you look at the articles about non-payers in NYC, you can tell that it simply became socially acceptable in many apartment buildings to not pay. If everyone’s doing it, you will feel less compelled to pay yourself.

There are of course, those who actually couldn’t pay as well, but most people in my area at least, simply chose not to.

It’s important to note, alot of those who weren’t paying claimed to be unemployed or barely working at that moment and were waiting on unemployment, but, he can tell through various ways such as them suddenly ordering a lot of new stuff, neighbours tattling on each other, and many other ways that they already were getting unemployment.

You can’t be this dumb. Are you literally saying people aren’t paying their mortgage and risking their house because they got month or two of forbearance. Do you have any proof of these insane claims?

Occam’s razor suggests that the largest unemployment in history is the fault of this, not the forbearance of a single month or two. Other countries cancelled rent and this didn’t happen for them but they also didn’t have mass unemployment because unlike our government, there’s isn’t stupid and they got the virus under control with mask wearing

I’m muling going into forbearance myself. Worst case is I have to pay the same money as I would otherwise pay. Best case is President Biden declares all the money forgiven. There’s really zero risk. Only downside is my credit would get dinged, but given there’s a 75% or greater chance that money won’t have to be paid back it’s probably worth it.

President Biden declaring all the money forgiven is less likely than Trump doing so.

Biden is the water boy for the banksters.

Didn’t DJT give a massive tax break to corporations and the 1% to the tune of TRILLIONS of dollars? I think Biden has a history of helping out the banks but to suggest he’s any more of a water boy than Trump is outright silly.

Have you not noticed corporate profits are at all time highs? The only reason banksters want rid of DJT are the obvious reasons that he’s going to keep crapping the bed (like he did on Covid-19 response) and they “may” prefer having some competent adults running things. Then again, maybe not…

Besides forbearance doesn’t stop the interest accruing. Just like all debts, it is the compounding interest that is the cost.. So not paying, just means you will pay more in the long run. If you have something to do with that money, and the interest is cheap, it may be a reasonable trade off.. Otherwise ?

I thought we could all work from home.

Did they not get in on the zoom meeting about the normal?

– @W. Richter: The homebuilders ETF (ITB) reached a new (all time ??) high. Was the Bloomberg refering to that ETF in that article ?

No, the article was referring to a monthly sentiment survey of home builders by the National Association of Home Builders (NAHB) and Wells Fargo. The survey asks home builders about how they feel about current conditions and how they feel about conditions in six months. Classic sentiment survey.

So is the other home builders ETF – XHB!

The magic of easy-peasy money spigot from Fed!

Supposedly Home Builders are super bullish. Aren’t they like the smart money?

I mean what reason do they have to be bullish?

Homebuilders are the biggest idiots I know.

fwiw, banks knew this was coming and have been saving money to cram down this portion of debt. Its also why the F/F .5 surcharge is a good idea despite lenders have been getting cut off, but the lag there takes several weeks until it shows up in data. My guess by September, the MBA index will crash………by the 4th quarter, the homebuilder index will crash.

Oh those lags. Retail Sales will contract in August, NFP will contract in September. Lag lag lag lag.

Builders in my area, like myself, well remember the great housing depression. They may be bullish, but they are not idiots. In my area, the days of spec. homes ended in 08.

It is mid August in flyover. We know/believe a slow down is coming.

But the phones have not quit ringing. It has been a long time since we have been this backlogged.

what type of person or corporation is buying your homes? How many are foreign buys?

Lynn

No corporate, or foreign buyers out here. These are families.

I have several large cities within a 2-3 hour drive. Their city govt. has failed them miserably. Covid & leadership siding with looters is the driver. But the roll out of fiber across flyover is what makes it possible to live & work from your chicken scratch hollow road hideout.

I would think corporate buyers will wait for a bottom and buy were money wants to live or vacation.

I know the Property Appraiser for Pinellas County, FL (the most densely populated county in in the state).

He told me years ago that every developer goes bankrupt sooner or later.

They aren’t idiots…nor are they geniuses.

MB,

I’ve posted this on a previous comment section, but it bears repeating. My son is a rural electrician and he has a one-man electrician business. He has been suddenly overwhelmed with requests for bids and work (won bids) on new installs. That is, homes to be built or currently being built. And this is all of a sudden. Last month, just the usual work — new panels, repairs, wiring new additions, etc. This month, almost all new builds. He says it’s like a switch was thrown (great pun!). He has more work than he can do in a timely fashion.

Anyhow, I can see why builders are bullish, at least for the short term.

I know common sense does not make sense these days otherwise with 20% unemployment rate, how come the stock market is going up and up.

Same thing can be said for housing as well.

Although a lot of low paying jobs are obliterated, there would be a domino effect on rentals as well as higher priced homes as well.

The stock market is making some sense at least i.e. the Fed’s been pumping money like crazy. Stocks are easy to buy and sell. They are very liquid.

Homes on the other hand depend on location, location and the generosity of a couple of bankers. Once you buy a home, you are basically signalling that you’ll stay there for a short while at least? That makes you less mobile if you ever lose your job, and then again depending on location, you might have to take a price cut.

“Same thing can be said for housing as well.”

Jon, viz. my son the electrician, this flood of new home builders are monies urban escapees, mostly Portland and Seattle, with a smattering of ex-Cal. They’re often buying the property sight unseen.

I dont know if this qualifies as smart money…

MiTurn,

My wife in her endless redecorating of our house bought some new light fixtures. I need an electrician to install them, since anything involving wires or pipes, I do not touch myself. I called around a few places, 1-2 week availability. This is for a 1-2 hour job. Anyone in the trades right now has more work than they know what to do with.

As a counter point to the electrician viewpoint. My wife works in a large water and wastewater agency. They interact with homebuilders at two times in the process. One when a development is planned, sewers are installed in the street and development fees are charged, the second time is later when the house is built and needs to be connected to the sewer. The first stage ( new developments) is dead as a doornail, but the second stage ( connections) is rolling along just fine. No one is dumb enough to start a new development, but anything they have started has so much sunk cost they are rushing to get it done so they can find a sucker to sell it too before it is too late.

Thanks for this very interesting info. It makes a lot of sense, actually. If this is true on a broad scale, there will be big changes in a month or two, I guess.

I don’t doubt the claims made by people here that homes are selling fast and all electricians/plumbers etc are super busy.

But no one can deny the fact that we now have 30 million people un employed and economically things are not looking good unless Govt keep printing money and keeps sending $$$ to people. In this case Gold and other PMs would skyrocket.

@Jon – They have to keep sending the money. Otherwise their most likely will be more riots.

A lot of people remember Obama bailing out the hedge funds and banks in 2009. Main street will demand to be bailed out this time.

If the CEOs of speculative companies in 2009 were bailed out and could keep their jobs….why can’t the CEO of a home (homeowner) be bailed out too?

Obama set the precedence.

I think forbearance will continue to people get back on their feet. Most mortgages are owned by the GSEs. They printed to money to buy the Mortgages so no harm to them if there are no payments.

I mean it could be the case that homebuilders are building inventory because they think that it will be business as usual come next year.

It could also be the case they are forecasting higher than usual inflation, so hei, let’s build NOW.

As per MiTurn’s comment,

My son is also an electrical contractor with two part time businesses and one full time job as a maint electrician. One business is in Alberta and one is in BC. He is going flat out with new builds and renos. He mostly does the estimating and pulls the permits under his ticket, with journeymen electricians doing the work and in partnership. They bill out at $90 per hour per man, plus materials. On firm contract bids that rate is used with an additional contingency cushion. With smart phone technology he is able to troubleshoot problems from 1500 miles away. Busy busy busy. This new reality is accomplished by phone videos.

I live in west coast logging country that supplies 27% of the US softwood lumber needed for this new construction. Logging here goes on 12 hours per day/7 days per week, and sorting and grading runs two shifts per day in order to process the 2 million cubic meters of wood harvest from just this one area, by January 1. There are hwy billboard advertisements for fallers, machine operators, and logging truck drivers. The price of lumber in the US is still climbing due to demand.

These are high paid union jobs and require a pretty sophisticated skill set compared to the past.

Give away free money through low interest rates and this is what happens; unrestrained building and unrealistic optimism. When forclosures meet up with empty new builds, look out. I’ve seen the woods around here shut totally down within one week. I used to run an aviation company that supplied remote logging camps for crew changes and emergency parts. Full booking sheets can evaporate into nothing, overnight. I expected this a few years ago, but like the stock market, nothing makes sense anymore.

“Full booking sheets can evaporate into nothing, overnight.”

Paulo,

Yeah, my son expects this windfall to end as quickly as it started. He’s holding his cards pretty close to his chest. Not banking his future on it.

“Give away free money through low interest rates and this is what happens; unrestrained building and unrealistic optimism.”

Yep, it’s called malinvestment, and it’s what the Fed, through it’s easy money policies, specializes in.

MonkeyBusiness,

“Supposedly Home Builders are super bullish. Aren’t they like the smart money? I mean what reason do they have to be bullish?”

Low mortgage rates. SOME people are using them to buy new houses. OTHER people are massively delinquent on their mortgages. Not the same group of people. But there are a lot more of these OTHER people.

In normal times I would understand, but surely there’s the question of affordability as well? Richer people are never the issue, but how many are buying because of the wealth effect?

Home builders serve a specific set of demographics – very unlike the regular population.

I wouldn’t be surprised if some home builders are doing well: those serving the 1% and 0.1% – their core constituencies are fine.

Its everyone else who is suffering.

In the DFW area, building is off the charts. But the price points are the $250k – $450k, not exactly the 1%er rangees. These are middle class homes.

Seems highly speculative given the current economic environment. Unless they are hoping for an explosion of immigration if Harris/Biden wins in Nov.

In Denmark, the home builders that last, they all have a holding company which owns a corporation for each project and ‘services’ the execution of the build – of course for a charge:

A.K.A. They siphon all the profits off from the ‘satellites’ and into the ‘mothership’ (There is a very handy tax-structure specifically for that). When something goes ‘PoP’ for them, it’s not the ‘mothership’, it’s within the ‘satellites’ and whoever extended credit to them.

After a good, long, run in there home building markets, optimism is rampant, especially amongst the late-entries, the contractors who formerly worked within the satellites of the Old Ones and now kick off on their own – often to their doom, of course, because they are too late in the cycle and they don’t have the sophistication and the manpower to really run the company structures that the Old Ones do. Thus, they get nailed in bankruptcy court (and whoever bought a house from them loses their warranty).

Another effect is that home prices between Copenhagen and The Rest differ by a huge amount (this in a country where the longest possible drive is about 400 km).

Outside of Copenhagen, the same quality homes can be 4 – 10 times cheaper than Inside of Copenhagen. When people of a certain age in Copenhagen smells that a recession is coming, they will unwind their Copenhagen home and move to, say, Ebeltoft or Vejle, leaving them with maybe 1-4 million tax-free DKK in the bank and within cycling range of a boat-club and a golf-field. Then they will do ‘consultancy’ work.

This “cashing out, moving out” drives a lot of the home-building and home-renovations in “the provinces” that we often see just before a recession really kicks off.

I.O.W., Builders Optimism is a Bad Omen: We have the ‘Sell Side’ Old Ones who are Professional Optimists (they lie!), all of the upstart yahoos (who don’t know any better), and the cashing out from the well-paid Copenhagen crowd driving real business, making things look on the up-and-up!

Brace, Brace, Brace!

Thanks for your report from boots on the dirt in Denmark FJ, please keep telling us how it is going there going forward.

Retired now from construction industry, by seen the same sort of ”out of time” optimism several times in FL, CA, and OR over the last 50 years or so,,, followed by RE selling less than half a few months later.

Will that same thing happen this time? Of course not, ”it’s different this time.” ya, of course it is

Meanwhile, developers go bankrupt once again, and make their sub contractors pay or do likewise because they trusted they would be paid…

I suspect most forebearence agreements with a ballon payment will end up in foreclosure.

Why can’t we let markets clear?

What’s wrong if average Joe can finally buy a house he can afford?

Are there still any adults left running things in this country?

This is because the value of things that people who have spent money on will decrease, the majority of money spent is by people who have money to spend money.

There can no longer be a drop.

As Wolf mentioned in his podcast, we have socialized the owner class, our SYSTEM perpetuates the VESTED money, it needs this perpetuation.

The people with the most money to lose, also have the most power, therefore, the system will be manipulated tirelessly, to avoid having any drop of “value.”

The system is also, now, more corrupt than it has ever been, which is why there CANNOT be a drop.

It is the third corollary to the saying: owe the bank $1000, its your problem but owe the bank $10M – it is their problem.

What about 5 million people owing the banks $1 trillion?

Its the debt. There are so many assets leveraged so heavily. Many loans have no actual assets backing them, just hope and prayer. To allow the system to clear means that these assets will be revalued at a lower price. A true Mark to Market can not be allowed. That scares the bejesus out of the financiers. When so many loans are based upon the value of assets and that value falls, then there is no longer any security.

Generally this is referred to as deflation. It could be a huge spiraling down the drain and leave many (most) of the Banksters, Hedge Funds and PE groups totally insolvent. The PTB will do everything possible to prevent this.

The market and the economy are fundamentally sound.

It’s contained.

Everything will be fine just as soon as the temporary blip caused by the corona virus passes us by, a golden age of peace and prosperity is on the horizon!

Horizon: An imaginary line that recedes as you approach it.

Wonder what percentage of these delinquencies are due to landlords being unable to collect rent and therefore not pay their mortgage? As the moratorium on rents continue, we can expect this number to go up. Landlords will never recover the months and months of rent that is due them.

In the south there is a postal work slowdown going on that is not helping people pay their bills. Bills and checks are not getting delivered. This will push even the landlords with paying tenants further into the red in August.

Packages are averaging about one a day, if any at all.

Thanks, Nancy Antoinette.

I would like to see your supporting documents.

Anecdotally, this is happening. I had to scramble to pay my car insurance because the check took too long to get there. My insurance company says it’s happening quite a bit.

I’m experiencing the slowdown personally, just spent $35 on a stop payment because the check hasn’t gotten to the next town in almost 3 weeks. You can read about the slowdown in any southern city news site, even the democratic liberal ones.

I’ll send you my US Cellular bill showing a $5 late payment fee. They claim I paid 4 days late, even though I put a check in the mail the day after the invoice arrived.

Destroying USPS is now a profit center for scumbag cell phone companies! Ain’t capitalism great?

I don’t have any supporting documents but I’ve noticed the slowdown. I’ve used the USPS quite a bit over the last 30 years and the slowdown is noticeable.

Have you not seen the photos of the blue boxs piled up behind the various post offices (there weren’t many left anyway, sort of like pay-phones).

Have you not seen the photos of the large mail sorting machines that have been yanked out and are also sitting beside/behind the various post offices?

They deliver 143B pieces of mail a year. Pulling those machines, pulling overtime, changing rules all equal one thing: a massive slowdown in the service. Occam’s Razor as to why.

Does anyone actually pay by cheque (note correct spelling) anymore? Those days went out with the Pony Express.

BTW, I have no doubt of the results of the ‘New Plan’ of the new PMG. I am just looking for actual numbers, not political bias.

Well, only speaking personally, I sent my 2019 extension to the state of SC on July 15 by certified mail. It arrive in Columbia, 100 miles away, on July 27th …….. good luck with that postal voting…..

I ordered something online from Ca 8 days ago, 1 day after ordering it’s status was marked delivered to USPS for shipping. Now, 7 days later, it’s status is ‘Waiting to be accepted’, whatever that means. The USPS is essentially at a crawl.

You are utterly kidding right. Nancy. Try Trump. Next time pay your mortgage. You were bankrupt before correct. Trump virus, Trump USPA destruction. Wake up. Your posts are hilarious.

Yup, I was going to post something almost identical to what you wrote. I would only add to your comment that it would be nice to know the breakdown of old school landlords who are getting screwed by these insane laws (that, by the way, don’t apply to Target, Shell, Vons, the water dept, etc) vs short term vacation rental types.

Since when did it become ok to steal from landlords? I suppose we’re an easy target as we’re the biggest chunk of change people have to dole out each month. How about landlords who solely depend on rent for their income? This is pure and simple theft…legalized rioting/looting I suppose, not dissimilar to Portland and the rest of these rundown blue cities.

One of the big retailers here in Oz has refused, yep, refused to pay rent to their landlords.

They announced record earnings as a result of an increase in online sales, ‘reduced rent’, and a huge amount of subsidies from the government.

Of course, with the A$ falling like a rock and the imposition of a 10% on overseas purchases from places like eBay, it has also helped them………….

It’s not exactly right but since sanity went out the window, does anybody care about landlords right now? No. That’s why you rentier capitalists should dump your properties now and buy gold.

To The Bob who cried Wolf says

Since Henry George …

Wolf, do they include Philly as part of the NY metro? Thought we were still a top 10 metro.

Philly is not included in the NY MSA. But I think they combined the SF Bay Area’s two MSA’s into one, which makes sense and is done a lot, which moved it into the top 10. They might have done something like that with another MSA, which might then have moved Philly out of the top 10.

Financial disturbances are piling up. Nevertheless everyone’s happy and music goes on. Who will be left without chair when music stops? When does it happen and what is the straw that brakes camels back?

“There are now 4.2 million mortgages in forbearance, according to estimates by the MBA. Meaning 4.2 million homeowners have stopped making payments, in addition to the homeowners that have stopped making payments but are not in forbearance programs.”

So what is the total for mortgages not being paid off? That is, the sum of forbearance +nonforbearance loans that are mentioned above.

Or is that number not available?

Robert,

Just ball-parking: There are about 70.5 million in total residential mortgages outstanding. If 8.22% are delinquent, that would amount to about 5.8 million delinquent mortgages.

My step daughter may be one of the ones that’s not paying her mortgage. She won’t say she’s not paying, but she has been unemployed since February 2020 from her oil & gas accounting job here in Houston. She’s 50+, divorced, one child at home (not working either) and probably has run through her megar 401K funds by now. (she went through some of them last layoff)

She made $120K/year up until layoff (two months severance). Maybe it’s time for her to turn in her leased Mercedes? I know that will sadden her.

No job on the horizon and UI until the end of Jan 2021.

i think its time you call your daughter and see if she needs help.

Contractors busier than usual? The Refi mortgage money can’t go to travel because of travel restrictions and covid risk, so it reverts to renos. This also explains higher suburban and exurban home prices. This is anthropologically stupid, cramming people into houses beyond, say, 12 months, as we also find these same houses stuffed with dogs living in the kitchen onsuite, precious browser we’ve been trying to humanize since QE. So either Kim gets the dog, or one or two of us humans go back to bunk in the garage or vehicle. The neighbourhoods money is on me barking in three octaves by Halloween.

I think it’s perfectly safe and recommend for you to go outside!

I’ve been working from home, social distancing, etc. and I go outside as much as possible, every day!

I think its best if they tell the mortgage people to go straight to the Banksters as it is they who have caused them to forfeit the mortgage… After all they caused the problem why should they profit by getting ordinary people houses and wealth….

Let them keep their bits of useless paper, , all ways the same they blow it up then crash it and scope all the properties and assets for their useless paper…

People enter into contracts to purchase a house willingly – they don’t have a gun to their head making them sign the paperwork… they’re as much to blame for stretching their budget, not having savings, and thinking that man multiples price to income is “normal” as the paper pusher realtors and bankers. It’s been all about cash flow for too many years – no paying attention to safety nets, total costs, etc. Sometimes a painful lesson imparts the best education – it’s time some people start learning.

The rich get richer for real.

While the middle class gets to “extend and pretend” that they aren’t getting poorer.

lol

Listings of SFH in San francisco are up 96% YoY according to Zillow.

I suspect one reason for that is that SF has a reputation of being friendly to the Homeless.

And with 21 Million Americans facing eviction there may soon be more Homeless in SF than voters in Colma.

“And with 21 Million Americans facing eviction there may soon be more Homeless in SF than voters in Colma.”

Nobody is facing anything. Stop with the hysterics. You know very well the feds will bail out renters and pay their back rent.

At least once a day, and now sometimes even twice a day, the old Marty Zweig rule is disasterously & disingenuously ignored (to everyone’s amazement & astonishment & tish/rushing): don’t fight The Fed…PJS

Hear! Hear! I learned my lesson after losing my shirt and betting against the FED for 3-5 Years! Stupid, stupid, stupid!! I finally admitted defeat over a year ago and gave up all my inverse ETFs after losing 90% of my stash. Only god knows how much longer this all can keep up. Maybe decades??

There was a report during the first week of August about over 30% of Americans being behind on their mortgage or rent payments.

I am still trying to understand – if the landlords are not allowed to evict, are they eligible for some kind of support like PPP?

Alku,

You make a good point. Some landlords are facing their own problems with making mortgage payments on their rentals. What does a renter do, who isn’t making rent payments, do when the rental goes in foreclosure? You could argue that, in some idolated cases, that the renter brought this on his or her own head.

Point is, many landlords are not faceless corporations with some financial connections but ‘little people’ dreaming big.

I think it is a taking without just compensation being paid to the landlord. Also, the moratoriums are a taking of the bank’s property without just compensation being paid to the banks. Anyone need a lawyer to assert a claim against the gov’t for violating the 5th Amendment’s takings clause?

That was not and advertisement for legal services. It was a comment.

We can apply for a forbearance but are still on the hook for utilities, maintenance, taxes, insurance, etc. Instead of making some money we’re told to pour money into the place so someone else can live for free. It’s a known fact among landlords that once a tenant gets a month behind they never catch up, never. If we get a forbearance it only delays the fact that you lost money because it’s still owed (tacked onto the end of the note). Tenant still doesn’t pay, we’re out the money. It’s an illegal taking of another’s property without just compensation. Gee, didn’t someone put something like that into the constitution to keep these politicians from doing just this; fifth amendment perhaps? It’s a real stretch and more of comic value than anything else, but, I suppose one could also make a third amendment argument that we’re being forced to house the soldiers of the welfare army that seems to be growing by leaps and bounds this year.

Per my understanding, small businesses can get PPP loans that will be forgiven if used to pay the workforce. Many landlords are pretty much the same small business. No PPP analogs in this case seems unfair.

They can always try to get forbearance from THEIR lenders :-]

This part I understand, but if the property is paid in full?

Yeah, that’s a problem.

Never buy real estate with your own money. Like the oil business: never drill with your own money.

I suppose we are seeing a lot of trickle-down effect now, just not the best solution. Everybody wants to be like the bankers and corporations during the great recession, we all learned well from those heroes, right?

Students have stopped paying loans betting on loan forgiveness. Renters are taking advantage of eviction moratoriums. Many people see home and auto loan forbearance as an Option, thinking this thing could stretch out for many many moons.

Today is not like it was when a lot of us older folks usually made it with some hard work. I think A lot of the younger people see no hope for their future under the present corporate zombie job rule-us-all Metropolis.

If we learned this dog-eat-dog attitude anywhere, it was fed to us from our government.

If people are allowed to take a “basic human need” (shelter) from another person (their landlord) when will they be allowed to meet another “basic human need” (food) by taking it from the shelves of their supermarket? Or is that too “socialist” for the USA?

Econ 101. You can control the price of something, or control the supply of the same thing, but never both at the same time. As bread in the USSR was deemed to be for free, it was unavailable. If people take food from stores for free, they will close very quickly to avoid negative cash flow, then the food becomes unavailable. The same will eventually happen for rental properties, it will just take a longer time, as landlords quitclaim their deeds. Upkeep then disappears, and tenants leave while the rats infest. It happened in the city where I live in the 1980’s.

Nonsense. I lived in the USSR. Bread was very cheap, good and plentiful. The issue was with more complicated consumer goods, such as televisions, for which the technology did not quite match production capacity or stuff got stolen in the production process and so your television did not work and as the state did not care about consumers, so you had no recourse. Military and space stuff worked really quite well because the state cared. Oh, and then there was that time a central planner accidentally erased a line for toothbrushes in the planning doc and then there were no toothbrushes. For a year.

I was about write the same comment, but then it occurred to me that he might have referred to the USSR’s early years :)

Ultimately, any system works well, or well enough, when people give a shit and try to do the right thing. Any system where people (and that goes especially for government) are corrupt and act immorally, creating injustice and unfairly applying rules, or creating/allowing perverse incentives to run amok, or worse, intentionally rewarding wrongdoing, that system will collapse on itself either in revolution or under it’s own unsustainability.

People debate the whole capitalism vs. “socialism” vs. communism thing as if they have some ultimate one true virtue. In reality they are generally all smeared with the ineptitudes common to any human social structure. There is no partially good reason other than human nature why any of them could not theoretically work well with a just society.

Being a landlord right now is the worst financial move anyone can make. You are taking a 40% chance that you will need to pay 100% of your expenses while earning $0 income. The federal govt for all intents and purposes has eliminated landlord/tenant contract law. This will have enormous consequences down the road.

Don’t they already do that in San Francisco where shoplifting is no longer treated as a crimeor basically ignored?

Not just SF, all of CA. Any theft under $950 is not longer prosecuted as a felony. So thieves now casually walk into a store, take $600, 700 worth of merchandize and simply walk out the door. Nobody stops them because they know there’s no point. There are tons of videos on YouTube showing this happening all across the state.

I saw that happening myself at the Walgreens down the block. Three people with three big suit cases coming in and cleaning out shelves (hair-care stuff), and customers taking videos of them. But I think if they can stick them with some kind of organized crime charge (that’s what this was… a commercial operation), it’s a felony.

Well, I think that’s just Price Discovery: Industrialisation will eventually drive the price of any manufactured product towards Zero.

There is a Frederick Pohl story, ‘Midas World’ about a time where poverty is directly measured by how much one has to consume annually “to save the economy”.

The extremely wealthy have small homes and can chose what to consume and when, whereas the poor all have huge estates and are also forced to burn through a mountain of consumer goods every year, produced by automated factories.

They can’t skip the middle man and recycle the goods that nobody want or needs or even tell the robots to produce less stuff, because “that would collapse the economy”.

This is where we are going, IMO. The poorer one is, the more garbage one owns and consumes! All is “for free” because the stuff’s real value is negative!!

Link: https://archive.org/stream/galaxymagazine-1954-04/Galaxy_1954_04#page/n7/mode/2up

The Midas story is already happening. Minimalism is for the rich.

https://www.themaneater.com/stories/opinion/column-minimalism-is-for-the-wealthy

NATIONAL DEBT STRIKE

People stop paying anything but personal debt owed to people that they like and honor, such as a decent landlord, if you can still afford it.

Corporate landlords? Mortgages? Credit Cards? Utilities? Car and Student Loans, Insurance? Not one payment from now on until–

The Federal Reserve treats individual taxpayers the same way they treated corporate America, which if I recall, would equal a payment of $9,000 to every man woman and child.

If there were ever a time when this could actually work, it is now. Taking a cue from Rahm Emmanuel, “Never let a crisis go to waste.”

The powers that be are terrified of this. It would not take a large percentage of people doing this, I bet that less than 10% of the population taking this step would be enough to get National Healtchare, a Postal Savings Bank and a smaller defense budget to pay for it.

County sheriffs would not enforce mass evictions, nor repossessions, nor would there be any way to stop this.

The great thing about a debt strike is that “Inaction is action”.

Wolf,

one way to look at this is that C19 is a great equalizer. It brought out all of the weirdo things that our government can do. Forbearance, eviction moratoriums, insane stimulus, limitless money printing… The government is basically reacting like an animal on instinct, no real thought about the consequences of action.

People are hurting, throw money at them, and as you say, that money then lines the pocket of the uber rich and make the situation even worse. Or make up some emergency laws that basically begins the abrogation of property rights, eviction moratorium without ever considering what this will do to both renters and landlords (the smaller ones) down the road. Nothing except a vague comment that the rent is still due at some point in the undefined future or loans won’t hit your credit scores.

All that means is that sooner or later, there is a day of reckoning coming, and everyone has to pay up. Whether it is through the dollar declining in value, or the craziness we are seeing in the streets now. This is what we get for having twenty plus years of ever more screwed up concentration of power in the two parties, and division in the country where one party rule now prevails in most areas. The current Dumbo in charge is just the latest manifestation of this nuttiness, kind of like people are used to suffering along with the common cold, and tolerating it, and one day they suddenly wake up and find they have SARS.

No wonder people are buying guns and gold.

Sort of off topic but related:

As well as all the conspiracy stuff on ZH there is some good stuff including now then from our host on WS. Remember, one oz of gold per ton of gravel is a very rich vein.

As I was shoveling gravel into the rocker , I came across this:

An ‘Unexpected’ Systemic Crisis Is Assured’

You will have to wade back through a day of uh, tailings but the guy Alistair McCloud talks a good game.

He says the big European banks e.g. Societe Generale, Deutsche, and Santander are zombies just waiting for the head shot, with SG number one. No large North American bank is anywhere near as bad.

It’s a long closely argued piece that I don’t pretend to fully or largely understand, but worth a look.

Just don’t get too close to the tailings pond.

nick kelly,

The thing with SG is, the French government will never allow the bank to fail. A low low level trader will get blamed for a $5 billion loss and go to jail, and the bank will get a bailout. That’s how it is in France, never any doubt about it.

The mining imagery is beautiful.

Nick Kelly, The man who buys all the shovels is the smartest miner of all. Sam Brannan did just that in San Francisco, then, he ran up Kearny Street waving a money bag with a few coins in it shouting:

GOLD!, THERE’S GOLD IN THAR HILLS!

I see that Hawai’i came up on the numbers board with a big increase in problem mortgages.

Buy, why Kahului?

Toursim in Kahului? There isn’t anything there or maybe they are misnaming the SMSA as it includes Lahaina – the tourist area of the SMSA.

I wonder what Honolulu’s numbers are like. They are having a huge increase in the number of cases of the virus and no hope for any kind of rebound in tourism for a long, long time it appears.

The overall rate isn’t so bad, 5K people infected out of 1.4M population. Not even 1%. But the economy is going to be wrecked.

I often wondered which state is going to be forced to declare bankruptcy first. Up till now, I always figured IL to be the first, but HI seems to be a contender now.

But perhaps this will finally put paid to that idiotic HART project that they have going and that’s so overbudget that it makes CA’s high speed rail plan look like a model of efficiency in comparison.

Well Honolulu did need some kind of public rail transport system, but it seems that spending some $US9 billion on whatever the hell they have now or will have is absurd.

I remember waiting for the bus when we were in Honolulu and seeing bus after bus go by without stopping as they were full. I imagine that since the last time I was there is has become even worse.

All the polls that were connected with the RR project were basically dumped in the recent primaries and there will a couple of newbies running for head honcho in the upcoming election.

Given the political situation in Hawai’i and Honolulu I wonder if they will be able to make any difference……………

Hawai’i (Oahu) was very, very nice in the late 70’s and so so nice even up until the late 90’s, but something happened there after that and ruined the place.

Maui was still nice in the early 2000’s, but I haven’t been back there since then so don’t about it now.

Here in Melbourne we had a better day than yesterday (25 deaths – 22 from aged care) with ‘only’ 22 deaths and a couple hundred cases.

Total of 17,000 some case in Victoria so far and most in Melbourne with 351 deaths (Australia total is 438) and a majority of those recently and in aged care.

Melbourne population before all this started was around 5.3 million and Victoria around 6.3 million – a comparision for Hawai’i.

We are 2 weeks into our stage four lockdown/curfew with 4 more weeks to go. That is on top of the previous lockdown that started way back whenever.

The economy here is being totally destroyed with lots of stuff completely shut down. You can’t get your car serviced except for an emergency and you can’t buy a car from a dealer. Can’t visit your family members or friends either.

The state is borrowing billions and billions to give bucks to gvive a way to everybody (except me it seems!!!).

And then the federal government here is doing the same, but the share market keeps going up and the A$ along with it.

I can tell you what happened. One party rule.

Give one political party the run of the place, eventually they feel entitled, and then, every bad idea is good.

Problems are blamed on outsiders, Hawaii’s homeless problem exploded in the 2000s, and grew steadily worse over time. Instead of trying to solve the problem, the leaders there first blamed all the mainlanders for dumping their homeless in Hawaii with one way tickets. Then it was a matter of putting them out of sight so the tourists don’t see them. Instead of figuring out what else an isolate set of islands could do to enhance its economy, Hawaii tripled down on tourists and useless projects.

Now there are no tourists, lots of debts, and no plan. The governor locked the place down, all but banned tourists. (not that it’s a bad thing or that it would’ve made any difference in the world of C19) And the result, still cases happening there, with more increases recently.

When there is lack of creativity, there is the will to print more money. Someone eventually has to pay for this, but not the present generation.

Lee,

I would think the way Kahului got their attention was by having the highest delinquency rate in Hawaii.

Yes, but given the characteristics of Kahului, it makes no sense so as I said in my post I think that they just used the ‘Kahului’ name as the SMSA which includes the tourist area, Lahaina.

The two places are on opposites sides of Maui!!!

Possibly the Filipinos employed in the hotels that haven’t been able to operate since March. Lots will probably move elsewhere, Like vegas. I’ve read Maui has the highest percentage of them and that they’re primarily located there

When I see things like the following:

“Hearing implant giant Cochlear has posted a $238.3 million net loss for 2020 as costs piled up from coronavirus shutdowns and it faced a long-running patent litigation case. As it expected, it will not pay a final dividend.

Nonetheless, the company is soaring in early trade, up 6.6 per cent to $211.56. It earlier touched a more than five-month peak of $214.50.’

Makes me wonder what is going on in the markets these days. Maybe people have lost their minds all over the place……………….

The deaf leading the blind?

I’m still going to argue that going out and buying a house with the maximum amount of money a lender will lend for 30Y is a very rational decision right now.

There is no way fiscal and monetary policy won’t devalue the heck out of the US dollar over the next few years. In 10 years, the debtor still has a real asset and pays the loan back with Monopoly money, while the lender ends up the biggest fool lending for 30Y at 3%.

That lender is us – our pension funds will buy our mortgage bonds :)

re: “As well as all the conspiracy stuff on ZH there is some good stuff including now then from our host on WS.”

With QAnon taking the conspiracy crap to the stratosphere, ZH almost looks tame these days.

We were actively shopping in the San Diego are when Covid broke out. We pulled out of a negotiation at the time given all of the uncertainty. What we have seen in the market here since then has been dumbfounding. Every home we have been interested in since has been a multiple offer situation. Homes rarely last on the market for more than 2 weeks. We have officially been priced out of the area where our kids go to school now. Every single concern about the housing market I have had has been met with massive government support. So now we have jumped in and are in contract again. Part of me feels certain that we are going to top-tick the market. But you can’t ignore the trend. And you don’t fight the fed.

Only buy a house you can afford even with a 6months lay-off. If you can’t afford don’t buy. Don’t overthink buying the top. A personal home is a utility/consumable and your nest.. not a speculation on price.

All that being said.. if you don’t like the monthly payment then maybe it’s time to move to Arizona or Nevada.

Yup, this is the case here and it seemed to start in or around May. San Diego compared to the rest of the coastal cities in CA is one of the only ones left that hasn’t totally gone off the rails (we’re on our way but it’ll be several years before we’re the likes of SF or LA).

SFR’s in San Diego are going like hotcakes and there seems to be no end in sight. Once the good stuff in the good neighborhoods goes folks start looking at good neighborhood/bad street stuff, then fringe and after that bad neighborhoods. Won’t be long before the stop gentrification crowd starts peacefully protesting here. It’s coming…there’s nothing left to buy and folks are desperate before they get totally priced out. Condo’s are much more available but what’s the point in going from a rented cube to an owned cube with a shared elevator and sticky gym/pool/sauna.

It’s tough times for buyers here; I wish you well in your search and hope you find something soon.

Regarding “no one really knows what will happen to those mortgages when these forbearance programs end” —

I’m treating that as a serious question. I worked in a bank’s IT department for several years in relation to a mortgage modification application in the wake of the Financial Crisis and the Making Home Affordable program, which also included a forbearance option.

Per what I was told by a more senior co-worker, someone who took a forbearance option and then reached the end of their term would probably just refinance the loan. So yeah, thousands of dollars are suddenly due on the final day, but they’ll get another payment plan.

Of course this is an extraordinary situation and the banks will suffer from all the extending, forbearance, refinancing, and (yes) foreclosing. Maybe that won’t be an option.

My understanding is banks don’t own most of the loans they originate but rather sell them to investors or Fanny/Freddy. They may keep the best loans from wealthy clients that have ample liquidity and assets.. but not the majority by a long shot. The banks just service the loans for the bag holders thus making forebearance a pass through liability.

Not in the USA, but all very interesting reading. It shall not be long to Zero.

The whole world is f….. u.

I’m off to buy a boat.

Y’all have a good day

Housing starts and permits to the moon in july. Not shocker to us.

Seems as if the sport of our times is spotting the bag holder, while the obligation to pay is passed from entity to entity. Somebody, somewhere, in the end, will not be getting paid, or will be paid only with monopoly money, which is the same thing. It’s too easy to say it will be the taxpayer who will pay in the end. At some point there will be too few taxpayers, not to mention too few tenants with the ability or the self-respect to pay their bills, and too few small-time landlords still standing.

I’d love for someone to convince me this doesn’t end in revolution and war. Or at least show me how it is possible for this carriage to creep along for another decade so that I can enjoy a few years sipping wine in Portugal before it all goes to heck.

People sure have short memories. It was only about 12 years ago that another period of irrational exuberance and buyers falling over each other to bid up houses and condos ended very suddenly. And badly. Very badly.

This time will be much, much worse.

This time is different. Didn’t you hear?

Buy now or be priced out forever!

Hi Richard,

From someone who has thrown his economics books as junk and irrelevant and taken years to unlearn what crap I got taught in school and university and now learning how the world actually works.

Both the heading are possible.

Most delinquencies and house builders looking at good times. Why read below

Most delinquencies: Simple and expected people do nothing jobs, in gig economy and have high debts. So any time ball stops rolling they will fail. That is the basis of profit for people working in financial industry.

Note I said people working in the financial industry not the finance company itself. There failure has no repercussion to house builders.

House builders looking at good times: Absolutely, interest rates are low if not negative. Asset appreciation is main goal of all central banks and governments and there are enough suckers who will pile in with anything they have or even a last throw of the dice of what is left with them. Few of them will get lucky for the herd to follow. You will also find there are billions of benefits given to house builders in UK and US.

US: Fannie and Freddie mac take away the risk factor of unsold property from house builder. Ill thought out home rebuilding insurance where you can build any where and the govt will pay for rebuild means you can build poor quality anywhere and be safe.

UK: Govt makes the deposit payment for home owners, and also takes the risk of mortgage failures from bank who it authorises to give unlimited NINJA loans to prop up the market.

Either way they will keep the market going at whatever the cost to the rest of the economy.

We have heard about Zombie companies who just exists. We will see Zombie people who will just exists to pay for the losses of the rich.

I thought it was extremely easy for any SFR to get forbearance. 1-4 unit properties were mentioned. Does this mean multifamily and SFR are lumped together in these stats? Are multifamily loans usually commercial which are not readily eligible for forbearance?

Why are all these delinquent properties not being listed for sale? If owners truly thought they were not going to catch up or be given an easy out, wouldn’t they be selling in this hot RE market with low inventory to avoid foreclosure?

The only reason I can think they wouldn’t sell is perhaps they would have nowhere to go if they sell. Lots of friction to move.

FHA forbearance extended until 2021. Sigh.

https://www.politico.com/news/2020/08/18/hud-foreclosure-evictions-ban-397960

Yes, through the end of the year 2020, and it only covers FHA mortgages, not those backed by Fannie Mae and Freddie Mac. At least for now.

FHA mortgages are the ones that have the biggest delinquency problem after years of loosey-goosey underwriting. So it’s just trying to keep the mess swept under the rug until after the election, it seems.

I really wish they’d managed to re-privatize Fannie/Freddie since it looks like the public is going to be bag holders again. So tired of the game, especially since I’ve been property shopping through the last few years of madness.

What difference would that make? The government bailed out the commercial banks too.

It would allow price discovery and debt discharge, which would help reinvigorate our system. Constantly bailing it out “everyone’s a winner” keeps the system going and people feel good, but we all sink further faster as the debt weight drags us further underwater.

I had a fairly nice rental house occupied by white trash. It was a heck of a lot better than my dwellings of their age.

Many people now are lice or when walking in the swamps, the leeches that are nimble enough to attach to an ankle.

Go to the law to collect. That is a joke of some sort.

It was a pain to clean out their last crap to deliver it to them on the snow covered lawn. My wife was kind enough to help me deliver their stuff at no charge, almost like Amazon Prime.

The wife had such a hearty laugh after that. It went over the edge of orgasmic. Such a simple trip for a visit cemented our marriage and draining any hate to the renters.