Ready for another shock-and-awe panic-cut by the Fed? Last time the Fed panic-cut was in 2007/2008, and look what happened to stocks.

By Wolf Richter for WOLF STREET.

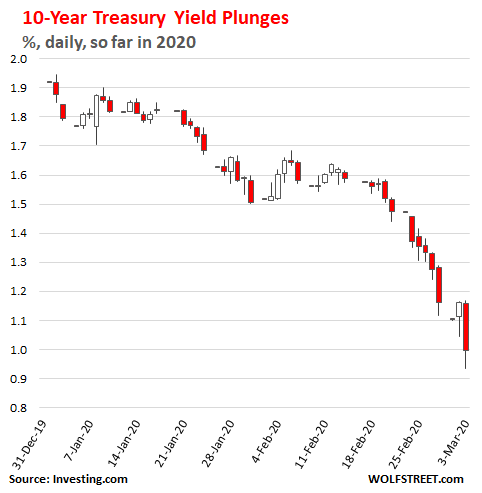

Spooked by the Fed’s shock-and-awe surprise 50-basis-point rate cut, the already frazzled markets did a job today. Gold surged nearly 3%. The three major stock indices all swooned nearly 3%. And Treasury yields plunged across the board.

The 10-year Treasury yield plunged from 1.13% pre-announcement to an intraday low of 0.935%, and closed officially at 1.02%. When the yield drops, it means that bond prices rise. In late trading the yield fell below 1% again, and is currently at 0.997% reflected in the chart (data via Investing.com):

The one-month yield – in a sign that this was a surprise act – plunged 34 basis points, most of it instantly, from 1.45% just before the shock-and-awe rate-cut announcement to 1.11% at the close, which put it in the middle of the Fed’s new federal-funds target range between 1.0% and 1.25%.

The three-month Treasury yield plunged from 1.20% just before the announcement to 0.95%, already pricing in another rate cut well before its maturity in 90 days.

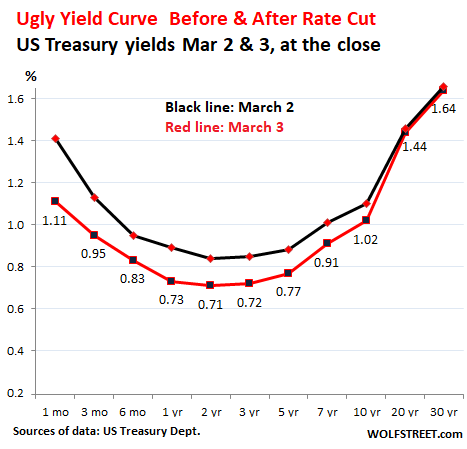

The two-year yield plunged to 0.72%, the lowest point on today’s yield curve. The 30-year yield ticked down 2 basis points to 1.64%, a record low.

The chart below shows the increasingly ugly yield curve yesterday at the close (black line) and today at the close (red line), for each maturity, from the one-month yield on the left, to the 30-year yield on the right:

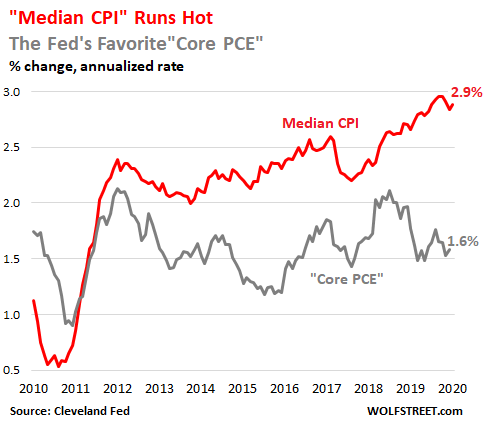

At this point, nearly the entire yield curve is below our most doctored and repressed US inflation gauge, the Fed’s preferred “core PCE,” which languishes at 1.6%. And the entire yield curve is far below the Cleveland Fed’s median CPI, which has surged to 2.9%.

The Median CPI is based on the data from the Consumer Price Index (CPI) but removes the extremes of price increases and price decreases, that are often temporary, to reveal underlying inflation trends:

Generally speaking, plunging Treasury yields, while inflation is rising, are not a sign of confidence, other than confidence in yields falling even further due to fears of more mayhem coming at the markets which would make the Fed react even more vigorously by cutting rates even further.

Investors who bought Treasuries before the rate cut and sold afterwards made a very quick buck, especially if it was a leveraged bet.

But lower yields are bad news for fixed-income investors of all kinds that have to replace maturing securities with new low-yielding securities. These fixed-income products amount to over $40 trillion in the US, including Treasury securities, bank savings products, investment-grade corporate bonds, municipal bonds, asset-backed securities, and the like.

Much of this stuff now yields below the rate of inflation as measured by median CPI, meaning that interest income doesn’t even compensate investors for the loss of purchasing power of their principal due to inflation. New buyers of these securities get their cash flows from interest payments confiscated by the Fed’s monetary policy.

So they can invest in the still immensely overpriced stock market, and count on meager and fragile dividend yields, or they can stand on the edge of a cliff and look down and see if they have enough of a death wish to buy Ford shares for their 8% dividend yield. Dividends can get cut any time, no sweat. And those fixed-income investors chasing yield among dividends have a good chance of losing a lot of principal a lot more quickly than the damage inflation might do.

By the stock market’s reaction today to the Fed’s shock-and-awe surprise 50-basis point rate cut – it should have caused stocks to soar, but caused them to plunge nearly 3% instead – it would seem that another such shock-and-awe event signals even more panic inside the Fed, and who knows how the stock market might react when it sees the Fed panicking.

There is historic precedent: Most recently, the Fed started cutting its policy rates in late 2007 and was slashing them wholesale in big panic-cuts in 2008, seeing whatever it saw. Then Lehman blew up, and by then, all heck had broken lose in the stock market.

Were they disappointed the Fed didn’t print antibodies? Read…. Stocks Sag as Fed Cures Coronavirus by Cutting Rates ½ Percentage Point

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Because the Fed rate cut was a surprise, the market said, OMG!

The Fed must know something we don’t!

Things must be worst than we thought!

SELL! Sell! sell! sell. buy. Buy! BUY!

A large gaggle of very vocal people, led by the present White House tenant, had been clamoring for more rate cuts since Jerome Powell had his ‘read my lips: no new rate cuts’ moment. This was happening before Covid-19 became a worldwide issue, when the manufacturing slump had already struck China, Japan and Europe but still wasn’t much of a problem in the US.

Just like the folks here are always clamoring for more subsidies and tax breaks, Wall Street and real estate speculators are always clamoring for rate cuts, no matter how things are going.

And very much like the child who threw a tantrum to get chocolate ice cream and threw it against the wall without even tasting it, Wall Street threw the rate cut against the wall. They’ve done this before, and they’ll do it again.

I am no expert in children, but in adults the only cure for such behavior is tough love of the monetary and fiscal kind.

Love it.

None of this will work because the sky is very dark with chickens coming home to roost. War, injustice, exploitation of workers and poverty wages, hypocrisy, filthy pollution, and above all, indifference to all of them.

I like to read the historical justifications for these, especially the slave trade in the US. Nothing new under the sun….

US has become a huge plantation and we the people aren’t living in the “Big House”………

What a mess!

This rate cut will further devastate retirees, retirees’ pensions…..

US financial system needs a good dose of Castor Oil……..and it’s shape-shifting politicians and financial moguls.

I must be doing something wrong; two bags of groceries I paid maybe $50-$60 year ago now cost me $100. Just basic groceries no frills…….

Stay healthy and safe out there!

This is fine.

For now.

NEGATIVE RATES ARE APPROACHING!!!!!

Good luck, retiring on negative interest yields and broken pension funds!

good luck retiring, period. at least on your own terms…

I respectfully disagree. I do not see the “Fed” taking any steps that might hurt its little banksters, like allowing negative interest rates, unless it can figure out ways to funnel huge sums to offset the loss of interest payments to the banks resulting from negative interest rates.

That can only be done in countries or the EU, in which the central bank truly is relatively independent of private control or the banksters are protected by easier direct or indirect governmental bailouts (like the EU.) Remember that the “Fed” is a bank cartel that looks out first for the interest of its banksters, who own it. It is not a federal agency.

At any rate, do not expect any persons below the level of the government/banksters to be able to get negative interest rate loans. The leading, “moderate” candidates of both parties now have close ties to the banksters, so expect more bailouts because the banks are going to get burned sooner or later in their derivatives gambling: a black swan like the coronavirus might already have burned them for all I know.

I cite to Zerohedge and unfamiliar websites, because the OCC has now pulled its page listing the banks’ 222 trillion dollars in derivatives exposure. See…

mike,

“I cite to Zerohedge and unfamiliar websites, because the OCC has now pulled its page listing the banks’ 222 trillion dollars in derivatives exposure.”

Good lordy. There is so much BS in this sentence that it gives me a headache. So I deleted the links. But here are the quarterly reports by the OCC about derivatives, including the December 2019 report, that you said the OCC had “pulled.” Making up conspiracy theories as we go, no?

https://www.occ.gov/publications-and-resources/publications/quarterly-report-on-bank-trading-and-derivatives-activities/index-quarterly-report-on-bank-trading-and-derivatives-activities.html

Sorry. Another page link that I had did not work. I jumped to conclusions. Reading about the 2008 bailouts, etc., and dealing personally with certain persons as an attorney has made me a little over-suspicious. :-)

‘based on information from the Reports of Condition and Income (call reports) filed by all insured U.S. commercial banks and trust companies as well as other published financial data, the Office of the Comptroller of the Currency prepares a report.’

The KEY words: Based on information ””filed by banks-trust companies.

The question who is going to verify their reports? Has any one audited them by independant 3rd party? Does any one knows the QUALITY of assets on the Fed’s balance sheet?

Watch, money will leave this country, in due time.

Can’t wait to see the next TICDATA.

Japanese and Europeons will keep buying unhedged, as long as its above their 0 coupons at equivalent maturities (or until they get wiped when the leveraged spreaders who need to keep borrowing rehypothicated collateral are forced to unwind lol)

I feel like everyone is failing economics 101.

The name of the game is pushing up productivity by getting people to work. Money printings does that by providing an incentive to borrow money and take a chance on giving that unemployed dude a job.

But if people can’t go to work because it’s too dangerous and your business can’t make money because your consumers think it’s too dangerous then interest rates don’t work. In this case supply and demand are constrained.

If supply and demand is constrained, then printing money does one and only one thing – cause inflation.

This is what happened in the late 70s when there wasn’t enough oil to go around. Printing money didn’t make more oil magically appear, it just caused inflation. Printing money now won’t make the virus disappear.

Sorry, but your interpretation of the Fed’s policy is mistaken.

Go back and carefully re-read your Economics 101 textbook!

One thing the Fed wants is more inflation.

They hope it gets more people to take risks/create more economy activity.

That’s the hope anyway.

It’s running out of ammo.

The Stable Prices mandate…..yet they promote inflation at a rate (2%-2.5%) that rips 22% to 28% off the dollar in just ten years.

File this with the “promote moderate long term rates”, moderate meaning ‘not extreme’. Flat yield curves and record low rates are extreme, NOT moderate.

So the Fed ignores TWO of their three mandates.

The name of the game is…

Central Bankers are engaged in a concerted effort to drive the cost of governmental borrowing to zero.

(to the delight of the governments that empower them)

I wonder if this is just signaling with all talk without massive money printing.

What does it take per 25 basis points lower? 500 billion or so?

How much has money supply or base money have to grow or expand to make 0.5% stick? 1 trillion? With the expected supply disruption, the Fed may get the inflation that they are looking for.

My mind is spinning.

The Fed doesn’t have to do anything. The 10 tear dropped below the Fed’s overnight rate yesterday. That’s Mr. Price Discovery telling the Fed they have far too rosy an outlook.

Price Discovery? You jest.

How is there fair unmanaged free market price discovery when the Fed creates FAKE demand for Treasuries with their $60 Billion a month non QE and over accommodative REPO antics?

Prices are dictated, managed, supervised….no discovery here.

Maybe this is a setup for a necessary MMT liquidity injection coupled with a necessary freedom reduction while expanding the exit door.

I’m glad I have a modest rental paid for with sweat equity. Far better return than stocks.

Treasuries below inflation rate? People must be absolutely terrified to buy such a product. Ten years?

And now with such a rate drop will housing prices regroup? Personally, I don’t think so. This is the slide, imho. Prices drop until a buyer is found, but what happens when the buyers don’t show up? It looks very very desperate. Plus, all happening in an election year.

. . . sweat equity . . .

Exactly.

Ultimately, investing in financial markets amounts to seeking to profit from the labour of others to avoid having to do the work personally. That’s capitalism.

It becomes predatory when it maximises profit by cheating the people who do the actual work. The markets don’t collapse because workers aren’t working and aren’t producing. The markets collapse when the games of greed backfire on the predators, and lately they’ve been backfiring bigly.

The alternative is to avoid the games, do the work yourself, and keep the profit for yourself.

Unamused-a succinct observation on the transparent garments of the predators. Would that the scales on the eyes of so many have the same transparency. TANSTAAFL, all-too-often in a long eventuality…

May we all find that better day.

Speaking of ‘cliffs’, by cutting rates this deeply, with so little room left before they are zero, the FED is literally PUSHING people over and OFF the cliff. Stocks have been over valued for years, so now when China is basically frozen over like a glacier with no production, and no ships moving, affecting the entire planet and every supply chain imaginable, the FED is saying ‘screw you’ mr. investor or joe/jane ‘saver’, and force everyone into holding their noses and ‘plunge’ already into a declining stock market.

Many reitrees are crowding into alphabet soups like BDCs, CEFs and MLPs, with no idea of what is under those hoods.

That is what happens when a 30-year T-bill is now equivalent to a 60 P/E stock with zero growth.

The Economy is primarily tuned to the needs of the 2% who holds all of the assets. Some gig-services are also provided to serve the needs of their salaried servants, the 10% so technical/managerial segment of the population, so these can work harder and more efficiently for their masters!

The 2% now really need to dump their stocks without taking a loss so of course their FED will force the rest of the population to buy their junky assets at full price!

Their indentured 10%’ers can get to use an app to order Sushi in at 2 AM while slaving with the practical details of making ‘Joe & Jane’ ‘Buy Stawks for Prosperity’.

What breaks with the Covid-19 is that the Zero-hour muppets preparing that sushi and the Uber-Eat delivery staff can’t afford to be off sick and they will cough all over the food to get revenge.

The 2%’ers support structure is under direct threat from the virus. This was not supposed to happen.

Serves them right for not pricing in risk.

I prefer my system, where risk is priced in automatically, can’t be avoided or evaded, and has to be dealt with up front. The downside is that it limits our ROI to 6-8%.

Mike R…

Right you are.

Central bankers, preventing cycles that naturally flush excesses, has allowed excesses to be pent up, and thus the eventual flush becomes a systemic risking event.

Thank goodness the Fed is wisely saving it’s amunition so it doesn’t have do NIRP, which of course all the mostest wisest amongst us say can’t happen here.

Wolf,

Aye, it’s ugly out there. 3-month LIBOR was briefly inverted with 30-year U.S. Treasuries last week. That didn’t last long. LIBOR has plunged over 40 basis points since. Now 1-month and 3-month LIBOR are the inverted pair.

Here’s a question for all: Does anyone here honestly believe that our feral leaders didn’t see this all coming over two years ago? Remember how much criticism Treasury was getting for funding government operations via huge T-bill issuance? Looks like a shrewd move now though. In 2018, 30-year Treasuries were yielding as much as 3.20% and 10-year was as high as 3.00%. Looks as if Treasury can now safely kick the can for a few more decades. That is if we can make it a few more decades in one piece.

Sounds like the Treasury is using the coronavirus as an excuse. They look desperate.

Out on a limb here, the money is out of their hands. In 2007 new private credit (MBS, et al) was outstripping Fed’s monetary controls. (IMO they crashed the market to regain control). Now the global fiat machine is far more insidious. Fed is the ultimate backstop, no longer the coach, just the team manager. This is the new reality Fed, president tweets “drop rates”, you drop rates. Congress monetizes your balance sheet, everyone monetizes you. Powell is accommodative in the broad sense of the term, with just enough troll in his remarks to project the image of a proud servant. When he begins to lapse into sycophancy, he becomes indignant. (ditto the AG). Bush brought Bernanke into cabinet meetings, and the Fed chief has been there ever since. Dollar policy, Fiscal policy? This Fed is an empty vessel.

A tsunami of cash, pouring into the markets,

is pricing people out of the rental market.

On the bright side:

— Oil is cheap.

— Asia still has a great work ethic.

— Singapore is a duplicatable success story.

Not sure work ethic applies to starvation wages in firetraps. Did you hear about the suicide in a phone plant this week?

Yes, let’s see some video of these laborers while we buy the product.

i have no need to see any videos. nor do i have any need to buy the lion’s share of “products.” food, gas, something to put in my wolf street mug yes. the rest of it? not so much. i try to produce as much of the food and mug filler as i can in house.

A million dollars used to be a large fortune. It will not buy a two bedroom apartment in the world’s most expensive neighborhoods. Trump was asking for tax cuts with spending increases. America left the gold standard during the Nixon years. We are in uncharted territory.

A couple of years before I retired, my big-city bank called me up and asked me to come in for a chat with a financial planner. We met, he ran a spreadsheet, and told me that $600,000 would set me up nicely for a comfortable retirement. After my burst of maniacal laughter we settled down. Turned out he wasn’t just a spreadsheet runner, he knew finance, so we spent n interesting quarter hour talking about Wolf Street, and markets with no fundamentals, and fun stuff.

So yeah, with retirement-for-one at $600,000 a million is not very much.

What’s fascinating is that stocks are being bought.

So you have to wonder who’s smarter. The buyers getting rid of their dollars or the sellers getting rid of their stocks for dollars.

I have a feeling and hunch you won’t want to own dollars as a primary investment in the coming years due to historically low interest rates. You then have to wonder where all these sellers will park their cash???!

Some say metals and mining stocks. Others think rental real estate.

There will be a winning trade in hindsight, but one thing is clear holding cash in this environment for too long is not looking like a smart decision. In the short maybe as markets correct to fair value but in the long run the markets will be inflated with 5-10x as much Fiat.

Dow was 1k in 1980. Now it’s 29k. The economy did not increase 29x in 40years. SP500 similar.

If you held your 1980 dollars you’d have little to show for it.

If you bought the SP500 before the 1987 crash you’d be up 10x, which is roughly what real inflation was. Buying gold in 1987 would’ve netted you a 3x return roughly. Bonds did something in the middle or better if you bought 30yTs at 10%

Shows you that stocks seem to do well in inflationary environments. And sometimes much better than historical inflation hedges.

Kissing the bottom of a stock market correction can produce 20-30x returns if you’re good at timing.

IMHO the SP500 will be at 12k by 2030. Dow will be 65-80k. Gold at 4K.

Pay off your house first before taking these long term views. Of course!

Yup, lets cherrypick lookbacks and liquidity preferences overtime and hope SP500 doesn’t end up like the from 1989 n225 30 years later, despite following everything the BOJ has done/tried many times over thus far.

10 year results are especially difficult to predict or time. The last ten years were great, especially from January 2010 to January 2020.

Had you pick January 2000 to January 2010, ugh, you would be down quite a bit on your principle. The ten year period of the 1970s were bad. Any ten year period before October 1929 to 1939 would have seen you in a severe loss.

It’s far more likely that all the failed policies of the Fed and the world central bankers will come to roost, and all the low inflation fakery will finally be stripped bare and exposed within the next ten years and the SP 500 will be lucky to be at break even by 2030 from this massive bubble of a peak in January 2020.

If you have time to buy and hold for 40-50 years, almost any period that long looks great for stocks. Few people have that luxury of time and patience and discipline.

when you have time, and more importantly the means, to buy and hold for generations, and have been doing so for, say, a few centuries, the results tend to be good. try and catch up. then you can start making the rules.

>>Shows you that stocks seem to do well in inflationary environments.<<

Evidently, you were not an active investor in the 1970's.

In nominal terms stocks can “do well” during inflation. In real terms (inflation adjusted) not so well.

@Pedro – Why should I put totally liquid cash into my house when in these crazy times I can stay liquid for a few hundred bucks a month? I’m not chasing yield into an illiquid asset that can take months maybe years to sell, perhaps even at a loss. YMMV

Pedro,

In tough times I figure people always need a place to live, water to drink and food to eat, healthcare, and things repaired/built. Mining stocks and PM for those who cannot do any of the above, I guess.

There is just a lot of unnecessary services that seems to be the cream in this economy. In tough times, who is more valuable? A plumber or investment banker?

The plumber, but people’s pipes won’t be bursting any more often, so if more people become plumbers you just have more people competing for a limited amount of work. Supply and demand would drive down plumber wages. Those unnecessary services are a byproduct of a modern economy that can already produce necessities for most people using very few people. Most people need a paycheck though, so they have to do what the labor market demands which is increasingly whatever random services become the fad du jour.

Your assumptions are correct during “normal times”

But if the Fed goes all and Federal spending starts to zoom we could move closer to a “Weimar inflation” where wages go up hourly and people are paid twice a day as the dollar rapidly loses value

Paulo:

Recalling my family during the Great D. we neither had the money (like millions of others) to pay a plumber or money for an “investment banker”.

There was no money for too many.

There was product to sell but no money in circulation to buy.

Paulo, we live in a different neighborhood but it’s fun watching the gymnastics on the other side of the tracks, isn’t it?

I would say diversify into good quality stocks, metals and rental real estate with 10% cash in various currencies

The problem with rental real estate is rents are already so high in many areas of the country that people can not afford any increases in rents. I do not know the maximum % of income that people overall can pay in rents , but with rents consuming over %50 of incomes in many parts of NYC and SF , it is not far from this limit.

with enough credit (cards), rent can easily eclipse 100% of income. for a while.

I agree. London is the same, and I hear it’s almost as bad in Paris. Rent levels are such that for many working couples they could drop an income, move somewhere else and have more disposable/savings. Unless you really love your job this defeats the economic benefits of the mega city conglomeration effect. Essentially, you are paying to be able to have two careers.

As rents rise this premium gets worse and the numbers stop working for more households. The net effect is that all this rent seeking drives down real economic activity. But who cares right, they can just print more to make up for it.

I’m convinced the central bankers don’t have a clue what is going on. That is what’s really scary.

The general population can choke down the loss of value of our currency due to inflation, without a specific target to blame it on. But the closer the FED comes to the zero rate, the bigger the bullseye will become, and a much clearer focus on who to blame it on. Welcome to the zero sum game, and our part in it has been deemed nil.

Re – the Fed as bad actor behind the scenes

With the internet and the greatly enhanced access to historical data and data in general, I think it gets much harder for the Fed/DC to shift the blame for inflation to others…it isn’t like people don’t know what ZIRP has done to their bank accts for 17 yrs…it isn’t a coincidence that contempt of gvt is also probably at an all time high.

I think you’re overestimating the ability of most people to research and apply facts. Most people today get their “information” from their social media echochamber of choice.

and thus, we find ourselves in the current predicament.

Old dead white guy Mr Smith from Edinburg would tell you the silent invisible hand of the market place clutches only money. Only gold is money. Every thing else is debt in the form of fiat paper.Old dead white guy from France named Voltaire would tell you that all paper fiat eventually returns to its intrinsic value of zero. The Feds only product is fiat based leveraged debt , simple to comprehend. N’cest pas?

Old dead white guy Mr. J.P. Morgan testified before Congress in 1912 – which, of course, was before the Federal Reserve Act was signed into law – “Gold is money. Everything else is credit.”

Old dead white guy who signed that Act into law, Mr. President Wilson, had this to say:

“Some of the biggest men in the United States, in the field of commerce and manufacture, are afraid of something. They know there is a power somewhere, so organized, so subtle, so watchful, so interlocked, so complete, so pervasive that they had better not speak above their breath in condemnation of it.”

Now an old living white guy who resides in the White House uses Twitter to speak in condemnation of this power.

Yesterday’s action was anything but subtle.

The old white guy in the White House is at least as beholden to any “mysterious” financial entities as any other highly leveraged rich guy. They let him get away with his Twitter tantrums because he’s giving them what they want.

Personally I don’t buy into the conspiracy stuff. The only real mystery is collective confidence/fear.

thanks for that W.W. quote. going to have to read up on him, i always thought he was a patsy of the banksters of his day. perhaps he was something different than an early 20th century version of the guy standing between the bankers and the pitchforks.

Nice story! I’m not so sure of the details, but it made me laugh.

The Fed is there to try to make the guy from France’s insight to happen very slowly.

So far, so good.

I’ll gladly lose 2% to inflation the next few years to avoid hazards in the stock market. I have a feeling many layoffs will be announced shortly. The negative feedback cycle has begun. The Fed is shooting blanks and everybody understands that now. Nothing stands in the way of a significant stock price drop.

@Bobber – that’s exactly what I have been thinking is that layoffs are just around the bend, but hardly mentioned by anyone.

IMO – the Fed made a frantic .50% cut because they are looking out 6 months and see some VERY ugly things coming down the pipeline that we are just speculating about, – I think they are rolling the dice to head of disaster.

I don’t think it will work, however they must be seen as trying to do something.

With all the slowdowns/weaknesses that Wolf keenly pointed out prior to the coronavirus panic many weeks ago, plus this virus today, plus all the bubbles, plus the Fed panic, will lead to a recession, or a complete disaster, the Fed has little ammo left.

Maybe gold/silver, maybe muni funds, I dunno – the worst is yet to manifest itself.

Any investment suggestions are welcome!

In the end, it does not matter much. You can’t take it when you die.

When you save wealth, you’re really saving for those you leave on earth.

I was the receiver recently. Looks like I will be the giver next.

Like most , I save primarily because I don’t want charity. I have been a receipient of hard manual work long done but not by me. I have added that past to my own in the present. My job is to remember and pass on the hard learned lessons of the past that these resources are damn precious and hard to replace . I cannot spend them on me . I am a fear filled creature , it is my nature. I have watched the Fed harvest our pensions , time value of money and still it wants more.Robert Burns poem “To A Mouse” sums it up proper on the fear of loss of our “nest” , financial or otherwise .”Backward I cast my eyes on prospects dreary and forward I cannot see, I guess and fear”

Exactly, they are doing “something”

Diversify with gold and silver and don’t take any loss at all

i agree with you to a point. how does one diversify against the breakdown of rules and laws? we are already there, when one considers the penalties applied to “elite” lawbreakers. is your pedigree proof against confiscation of your prudently saved PMs by the above the law types? asking for a friend…

If it all happens as you say then those with short positions should make windfalls. That ain’t the way reality usually works. As you said, things definitely look like they are about to hit the brick wall of reality, however I remember the old saying: “the market can remain irrational longer than you can remain solvent”. Maybe those that are (obviously) “shooting blanks” are hoping for that irrationality to continue so that no-one notices that the Emperor has no potency. So what type of prick will it finally take to pop the everything bubble? :-)

2% -2.5% rips 22% to 28% off the dollar in ten years.

Why is that a necessity, a wise strategy, for anyone but the borrower of large sums?

It is terrible for the working man who attempts to create wealth but has it stripped by dictates of unelected central bankers.

Real yields

5 year=(-.57)

7 year=(-.52)

10 year=(-.43)

And these numbers reflect the doctored inflation numbers of US government stats.

On the one hand lower interest rates used to discount future cash flows raise the P/E s of stocks ; on the other hand such low rates mean very low expected growth rates. Low future growth rates mean that GDP will expand slower than the current growth of US government debt. This is a recipe for sure depreciation of the dollar, which in turn will lead to sharp inflation of imported goods.

Just IMHO, I suspect many are parking their funds in T-bills not so much for yield–which, as you pointed out, doesn’t exist–but because they don’t trust banks. TBTF or not, the hoi polloi will be pretty angry if the bankers get a pass. Again.

I agree… that’s pretty much what I am doing now.

Last YOY Core inflation 2.5%.

Ten year under 1%. And the Fed cuts.

Stealing wealth via central banking decisions.

The Fed is being exposed as King Canute.

There’s no stopping the tide.

We are in full mode Japanification.

After a run up from 8,000 to 39,000 in 7 years ending in 1989,only to decline to 10,000 on the next 10. Huge Central bank

Intervention with little effect on the markets and on the economy . Look for 10,000 during the current decade

The Fed seems to be in a liquidity trap.

They will probably EXTEND the repo operations.

They will probably increase the $60 Billion per month T Bill purchase and longer.

They 2 above are steepeners of the yield curve.

They will probably do another Operation Twist when the bulk of the T bills the purchased start maturing later in the Spring.

And lastly, if they need more money, I would not count out another round or rounds of Q.E.

1) AAPL had a minus 3.2% day in the red. Burnie was checked. The Fed rates were pinned down to the ground by the coronavirus and Europe negative rates.

2) If u expect a green Mandelbrot day, buy a bag of apples.

3) US 10Y < 1%, Ford dividend @ 8.6%, Repo is down, signaled election submission, so both u and your broker can make good money.

4) If u earn 60K and spend 100K, no problems. Finance the gap with higher debt, because eveything is a bargain.

5) The trend is up. The trend is strong. You are the smart money. Take more debt, surf on the next bull run and enjoy your Das Kapital.

Such are the misbehavior(s) of the market.

My son came and told me he bought Ford at 7 and he’s writing covered calls. That’s how he is learning to play.

Things are always changing. One thing is constant: you can only invest in a few things. Real estate, businesses, commodities, and your own skills. Bonds are debt instruments and cash and gold are stores of value, although fiat currency is rather variable.

The first objective is day to day living. Second is paying off your own debt. Then you can save some extra cash, you might investing in the rest according to your stomach. Hope you beat inflation. Give some to charity every year to help your neighbour.

Well, there is one other unfortunate constant: the noise of financial talk. That is best ignored ‘though.

Thank you for a reasoned, intelligent contribution to the conversation.

Wolf,

You need to do an article about investing in gold.

All these gold bugs crawling out on your website extolling the virtues of gold…

OMG, just google “gold price historical” and you will instantly see that everything these goldbugs say about gold being a great investment, that it always keeps its value, is simply total and complete BS.

Gold prices have ALWAYS fluctuated up and down, with huge peaks, and huge troughs worse than the stock market. Had an investor panic bought at any of those peaks, he/she would have needed well over a decade or more to break even on their investment. They would have been much better off buying and holding US Treasuries, despite all the bias against it being a fiat currency.

Gold is WORSE than a fiat currency – it is simply a semi-rare metals commodity, not really a true hedge against inflation and disaster, simply because inflation and disasters usually get resolved. BUT, because these prices cause increasingly difficult gold mining technology to develop, more gold mines open up, produce more gold, and the price of gold plummets, because of the increased supply, and the fact that the fears of inflation and disaster have been fixed. Yes, it sometimes takes a decade or more for inflation and disasters to get fixed, but they usually do get fixed, throughout modern history.

And if you think that gold will be any use when an extinction level asteroid hits the Earth, or some other unrecoverable disaster happens to life on Earth …..

@Gandalf –

The disgust evident in your second sentence reveals a strong bias that helps to explain the numerous misunderstandings littering your post.

Your “OMG” sentence is deeply ignorant. Why? Well, here are the FACTS:

– the vast majority of “gold bugs” do not view the metal as an investment, but rather insurance, or a store of value

– ALL fiat currencies are degraded by governments, lose value in the process, and eventually die

– gold has retained value over thousands of years, and is a reliable store of value during currency crises

– inflation of fiat currencies doesn’t get “resolved”, it degrades their value and ultimately kills them

– the USD has declined over 90% in value due to inflation since the FED was created; at that time, gold had a “fixed” value of $20.67 per ounce; 20 1914 dollars now buys roughly $2 worth of goods and services, while an ounce of gold is worth ~$1600

– most “gold bugs” have appeared since around 2000, after the tech bubble bursts, and the FED began its obviously flawed, serial bubble blowing policies, and the metal has increased in value over 7x since then

– gold is at or around all-time highs vs. most currencies right now, and for reasons that were predicted by most “gold bugs”

– viewing gold only through a USD lens is misleading at best; there are many individual examples, but holding gold in Argentina rather than pesos would have yielded MASSIVE benefits (it is up over 800% over the past few years alone!)

– comparing gold to stock or bond markets is an exercise in futility, as the timelines chosen will produce radically different results

Etc.

I am still holding my gold and silver PM’s. However, I did get stopped out of my metal miners. Gave them a short fuse given the virus news and people not going to work either scared or being in a confined area. Some have come back a little so I might dip my toe in again and see how it goes.

I agree with your assessment of gold and believe it stands the test of time unlike fiat and other paper.

Time will tell whether this is all overblown or we’re witnessing the ‘black swan’ that was being discussed over and over but not known.

Disagree with both of you.

Arable land with a water source, woodlot, tools, skills, community, etc, located in a country that respects property rights and rule of law, are all more valuable than gold. Pick your country and location. It exists.

Magic angle investors gravitate to gold and trinkets, civilizations value the above. Stocks and bonds remain hope and bets, not even printed on paper these days.

As an aside, tomorrow I head down island to buy the last of my new greenhouse materials. For cash, about 3K worth. Installed, this new 500 sq ft greenhouse is worth 25K as a purchased kit, installation extra. Cost for me to build? 5K all in for an old growth yellow cedar structure on concrete foundation, using recycled glass panels. Time to build? 2-3 weeks dodging snow and rain events, working only mornings, (max 4 hours per day). 5X investment gain in 3 weeks. Lifelong return in grown produce keeping family healthy and fit. I have yet to see any investment return at such levels, ever.

If I lived in a city I would rehab property and offer affordable small rentals to select tenants. Or, do renos on the side for cash. Once you are established it is all done by word of mouth. I know builders booked up for several years working from this position. I know a retired GP in the States who fancies herself a ‘developer’. She buys up junk with potential, has a stable of trades she calls on to do the actual work, and does the scut work she is capable of like painting and cleaning, staging, etc. She’s rich. She prefers renovating over doctoring mostly due to the nightmare of dealing with insurance companies and the private business model.

Don’t use glass on the roof if you have hail in your area; instead, use some of the newer plastics that will last 10-20 years and not be shattered by the hail.

Been there done that with both, and good luck on the savings, etc., from having the seeds started a month or more in greenhouse before planting time, etc.

Saves a ton of money and effort.

Amish do it with a wood heater for the greenhouse to have no petro fuels involved at all after construction.

You’re actually not disagreeing with anything that I said. I never suggested that the choice was binary, nor that holding gold was preferable to productive land, etc. I Also agree that investing in properties can be a very attractive alternative.

Tinky,

Your knowledge of the history of gold prices clearly goes back to only the year 2004 (not 2000, see below), and you refuse to actually learn anything more about it.

For much of its history, the US was on a gold standard, in which the price of gold in dollars was set by the US Treasury. In 1792 gold was set at $19.75 an ounce, $20.67 in 1834, and $35 in 1934. Americans were also banned by Federal law in 1934 from owning gold bullion or coins and needed special Federal licenses to buy gold for manufacturing purposes. This was FDR’s Lite Version of “going off the gold standard”.

In 1944, the Bretton Woods treaty made the USD the world reserve currency by allowing signatories to the treaty to exchange their reserves of dollars for gold at the fixed price of $35.

By 1971, as Europe recovered and their currencies strengthened and the perpetual US trade deficit ballooned, a number of European countries either went off the Bretton Woods treaty or challenged it by redeeming ALL their dollar holdings for US gold. This was obviously going to deplete the US holdings of gold very quickly, so in 1971, Nixon, at the advice of Treasury Secretary John Connelly, also abrogated Bretton Woods, which effectively ended the gold standard in the United States.

That’s not the full story though. In 1975, Ford and Congress made it legal for ordinary Americans to own gold coins and bullion again which is when gold became possible as an investment again.

A combination of factors, the Arab Oil Embargo, the Fed dropping interest rates in response to what was a SUPPLY economic shock, and the devaluation of the USD due to the changing world economy (Germany and other European countries and Japan’s economies and currencies were growing stronger) led to the high inflation of the 1970s.

And THAT was when gold bugs first appeared in the US. Gold shot up to a peak of $843 in 1980 when Carter was President and inflation was sky high. I remember gold bugs everywhere screaming BUY GOLD! BUY GOLD!

I did buy gold, but not at then, and not at those prices. In 1986 I bought 33 one ounce gold coins for $354 each.

You see, the price of gold dropped like a rock after 1980, and pretty much hovered at or under $400 an ounce from 1982-2004, hitting a low of $252.90 in 1999.

Had anybody bought gold at the peak of the gold hysteria in 1980, they would have had to wait until 2008, some TWENTY EIGHT YEARS to break even or make a tiny profit selling their gold.

That’s actually WORSE than if you had bought the SP 500 at the peak in 1929 right before the Crash. You would have had to wait only until 1954-1955 (25-26 years) to break even or make a small profit

So you see, my rant about buying gold was directed against those people advising people to buy gold AS AN INVESTMENT in times of uncertainty, like right now. Because that’s when gold will be at its highest price, and it’s a lousy investment unless you intend to hold it forever, or…. until you need it to pay for the last seat on the last refugee boat out of Dothan, Alabama, or wherever you live

Yes, gold can be useful for getting a seat on those refugee boats

I used to work with a Vietnamese woman. She was the same age as me. One day we were eating and chit chatting in the lunch room. I started asking her about when she left Vietnam. She started getting very serious and a little emotional and remarked how nobody had ever asked her about her experience of leaving Vietnam. She was 12 years old in 1975. She told me about all the horrors that were happening as the North Vietnamese were closing in on Saigon. She said the only reason why she got out was that her dad had some gold and was able to pay someone to get them on a boat and out of Vietnam. All of the paper money that her dad had was worthless, just the gold had value.

I’m not a gold bug, but I get why people are. I don’t have any physical gold but I probably should.

Did she end up in HK harbor? When did she make it stateside? Did she spend time at Camp Pendleton? We fought a terrible war and then we welcomed these people. The only part of it that makes me feel proud.

She might have told me but I don’t remember those details. The conversation took place back in early 2011. Another Viet girl I worked with was also on a refugee boat after the fall of South Vietnam. She told me the boat broke down out in the ocean and they drifted with the currents for weeks before being rescued. She told me they ran out of food and she went for 3 weeks without eating. Several people on the boat died and had to be tossed over board. You get the point. Stories like that really put things into perspective. My youth was spent in sunny Southern California. I lived in one of the safest cities in the USA. Always had a lot to eat. Had all kinds of opportunities. In my youth I never knew just how lucky I was.

Folks. Happenings like Coronous virus nothing new in the civilisation of China. Before there were no exporting then because China itself was huge and rather inward looking. Then China decided to look out to the world and export export export. Goods, her people and of course contagious diseases goes along. The world welcome her with open arms because of money. Inevitably contagious diseases are bundled with it. Payback time can be anytime.

Ancient Chinese people knew and prepared well for catastrophic events. They used precious metals of silver and gold for livelihood and insurance.

Many older civilisations have similiar practices.

They knew.

If the only the Fed, led by the chairman I appointed, would stop being so scared and useless, interest rates need to be so far into negative that payments on mortgages are reversed and homeowners get a monthly check just for owning a home. Think of how great that would make America! Greater than ever!

Have been long gold for 18 years but sold half at $1895 when it peaked at $1900+ in mid 2000’s. May sell another half at $1700 (if it gets there). Thinking a commodity fund like BCI may be a buy with China, the biggest commodity buyer in the world, on it’s knees. Plus the dollar cost of commodities should rise with even more money printing.

Be careful with commodities in an inflationary environment.

Lithium carbonate peaked back in December 2017 at about CNY 171,000/ton. Yup, lithium is priced in yuan. Since then it has been steadily thumbling down: in June 2019 it was already down at CNY 73,700/ton in the midst of the now depressingly familiar barrage of stimulus. Right now? A miserable CNY 48,000/ton. It will bounce back, but I doubt Lithium carbonate will get to more than CNY 80,000 any time soon, and I am being generous with inflation.

The reasons for these drops are two. The first is the worldwide slump in manufacturing, which is not going to get better anytime soon and is completely unrelated to Covid-19. The second is large lithium producers such as IQM have used some of all that free money to add a ton of capacity in Australia, Argentina and Chile, capacity which is coming on line right now.

Right now everybody is piling into noble metals, especially palladium and rhodium. Rhodium is up 330% year on year or something like that.

Wait for prices to crater as the prospect of easy profits in a world where yield is a mirage drives a ton of money into what is effectively a niche metal: rhodium is mostly recovered from anode slimes, meaning what’s left over from copper smelting and refining.

There’s already what I can only call a booming trade in anode slimes worlwide. With “Dr Copper” (Doctor in what exactly?) down 17% year on year anode slimes are possibly worth more than copper itself.

I suspect somebody will attempt recovering rhodium from spent nuclear fuel on industrial scale: while costs may be astronomical and yields nothing to write home about I invite readers to look up the Swedish startup “Cangoroo”. If that can find seed money, anything can.

If only my mother knew she sent me to the Uni to study chemistry so I can write nonsense like this… :-D

Agriculture commodities are also interesting to look at.

Now, spring wheat is worth about $5.30 a bushel.

Twelve years ago, it was $17.30.

A lot of the growers in eastern North Dakota and northwest Minnesota, who were sitting on large inventories from the 2007 harvest did not sell. They figured the price would be in the low $20 range soon.

No sir. Those high March 2008 prices soon evaporated down to $9.81 in July, $7.71 in September, and after harvest the December price was $6.04.

All commodities follow that course these days: the search for any scrap of yield is having money flow into absolutely everything.

If there’s a disruption that sends prices soaring higher (IE the recent outbreak of African swine fever in China), money immediately pours into the segment and ends up creating oversupply, which in some cases can be massive.

In turn this leads to crazy stuff to artificially prop up prices such the ethanol mandate, which becomes even crazier when one considers under the EU CAP (Common Agricultural Policy) ethanol-grade corn prices are “negotiated” by governments, not set by supply and demand (which would 0 for ethanol grade fuel in a world of $50-70 oil).

In turn this has led to whole areas being given over to corn monoculture with a laundry list of issues, running from water mismanagement (120-day corn uses 25″ of water on average) to the spread of pesticide-resistant Western corn weevil… it’s a classic case of cure being far worse than the disease.

Selling at 1700 would be foolish Gold is heading above 2k very soon I predict

Frederick, Hope so, but I will still have enough as wealth insurance.

Supporting what I said earlier.

https://www.bloomberg.com/amp/news/articles/2020-03-04/credit-suisse-sees-funding-strain-risk-without-fed-liquidity

Are we going to see a $1T QE or notQE to make this 50 point rate cut stick? How long can words-only rate cuts last?

Iamafan,

“Funding strain? BS. They’re eager to borrow at 1.11% from the Fed to invest in MBS at 3% or so. That’s all. Cheapest money around, the Fed hands it out, and there is always demand for the cheapest money, and you get to earn the spread. And this money via the repo market is 50 basis points cheaper than two days ago.

The owners of the Fed are clutching pearls crying wolf pinky pointing upwards saying the sky is falling.

If it wasn’t so ridiculous I would laugh.

One would think a 50 bps cut would goose the markets. that the opposite happened tells us something bad is out there. And now the FED has wasted the last of its remaining bullets. Close to Trump directing monetary “policy” of printing to fund all of the gov’s “needs”.

This morning’s repo oversubscribed again.

Overnight repo is $100 billion just like yesterday’s.

Low rate = 1.10%. High rate =1.18%.

Yesterday’s FICC repo Treasury weighted average rate was 1.72%.

It was actually creeping up since Monday. The MBS repo rate was actually lower than Treasuries.

This worried the Fed.

Yes, 1.1%, cheapest money out there. Who wouldn’t try to get as much as possible, if the Fed hands it out. The Fed needs to raise offering rates on repos — and it had done that a tiny bit a few weeks ago, and repos dropped. Now it cut rates by a bunch.

Btw, the Fed repo number for tomorrow’s h.4.1. should be around $195 billion. It was an increase last seen since January 16th.

A reversal of Wolf’s liquidity theory.

Repos are not funding the phantom misnomer of “liquidity,” they are funding short term trades for the big banks. Some of those trades are flipping treasuries to fund the national debt, some are the ongoing flipping of legacy MBS, the rest is pure speculation funded with nearly free money, but only for the privileged bros. Now go back to work!

If the Fed offered 0% repos, there would be unlimited demand. Offering rates plunged 50 basis points to 1.1% … I’d love to borrow at those rates and invest in MBS at 3%. That’s what this is all about. SUDDENLY money got a lot cheaper.

Wolf can you kindly estimate the size of this carry trade? How much T’s are repoed to finance MREITs? Thanks. How big is this?

Iamafan,

I’m not going to guess about the size of it. But here is an example. In November, I looked up just one publicly traded MREIT — easy to do since it has to file with the SEC. There are plenty of other MREITS out there, and there are also many hedge funds in this business that are not publicly traded and that therefore I cannot get any data on. So this example MREIT is AGNC. This is what I said:

Now let’s think this through. If AGNC last week figured that sooner or later — maybe over the weekend, as it was rumored — the Fed would cut rates and bring down the 10-year yield along with the yield of MBS (and therefore push up their prices), if would make sense to buy for example $5 billion in MBS last week at the lower prices still available then.

AGNC would then fund these MBS in the repo market with overnight repos (selling MBS and taking the cash as a daily in and out) for a few days at the old rate (ca. 1.65%), and then when rates dropped to 1.1%, it would fund them in the repo market at the new low rates.

The MBS that it bought last week have now jumped in price, as yields have dropped over the past two days. But AGNC locked in the higher yield at the time of acquisition. So now AGNC has these MBS that pay AGNC the yield of last week (given the price AGNC paid), but the cost of funding them in the repo market has dropped by 50 basis points, and therefore the spread (AGNC’s profit margin) has jumped by 50 basis points.

Thing is, if it had waited till today to buy this MBS, it would have missed out on the higher yields that those MBS were paying last week, and on the capital gains. It locked those yield in for itself by having bought the MBS at that price.

It will now continue to fund them in the repo market, and eventually, when the dust of this rate cut settles, banks will become more competitive in the repo market at these new low rates to where the Fed isn’t the lender of first resort, which is what the Fed set itself up to be as of yesterday.

Question:

Is the REPO rate for a term REPO fixed, or did the rate drop when the Fed cut?

Why is there no penalty for constant use of the REPO market?

The Discount window had a wisdom to it……abuse it and you pay.

This seems to have disappeared since 2008…it should be reinstated IMO.

All the Fed has to do is soak up a few more trillions in toxic financial waste and hide them away with all the other crap. The markets aren’t based on fundamentals and are disconnected from the Real Economy anyway.

Problem solved.

It doesn’t have to be true. All you have to do is believe it.

Default rates are a lagging indicator. They don’t peak until after a recession. Leading economic indicators peak before a recession.

Go figure.

Lost in discussion, the IORR is now 1.1%.

Ahh, where will the banks’ profits come from?

Banks’ average cost of funding was below 1% even before this rate cut. And now it will be even lower. The bank can deposit at the Fed the cash in your zero-interest-bearing account and earn the spread of 1.1% risk free.

Wolf, would this deposit count towards the banks minimum required reserve, and if not, would they be skirting any rules? This has the smell of a misrepresentation scam!

DawnsEarlyLight,

No, the bank is not skirting any rules.

Your $100 deposit is two things for the bank, according to modern double-entry accounting where each transaction is booked with at least two entries, one credit and one debit:

1. An amount it owes you, so a liability for the bank, and the bank retains the liability.

2. The cash that you deposited is an asset for the bank. And this asset is what we’re talking about here, not the liability (deposit).

A bank can do all kinds of things with cash to make money. But first this cash goes into its huge bucket of “cash” that the bank has, and then portions of that bucket are put to work in various ways to earn interest. Part of it is used for loans, part of it is used to buy Treasuries, etc…

And part of this cash the bank MUST send to the Fed as required reserves against the bank’s deposit liabilities (so that the bank can draw on this cash at the Fed if there is a run on the bank).

What those reserve requirements are depends on the size of the bank. For all larger banks in the US, this reserve requirement is 10% of the bank’s total deposit liabilities.

So if a bank has $1 billion in deposit liabilities, it also got $1 billion cash from those deposits. It puts much of that $1 billion of cash to work by making loans, etc. But the bank has to send $100 million (10%) of it to the Fed as required reserves.

In addition, the bank can, if it so chooses, send more cash to the Fed, which become the excess reserves. The Fed pays interest on both types of reserves.

Ahh, where will the banks’ profits come from?

Predatory loans. Same as their losses.

Six minutes in and the DJIA is already down 200 pts from it’s high for the day.

I like watching re-runs. If they are good. The plot never changes, but the actors do. And if the plot is and works, can just change the details and use if over and over again.

On to the next existential “crises” that “forces” the Fed to cut rates/launch QE/launch NIRP/whatever.

Free ice cream!

For all my friends!!

All my frieenns./

https://www.calculatedriskblog.com/2009/01/tarp-free-ice-cream.html?m=1

The YC has no significance at historically low rates. The issue is the disconnect between banking and the economy. Powell said, “business isn’t concerned with interest rates, [but we are dropping rates anyway]..” Banking is where the auto industry was twenty years ago (or more) dying and irrelevant, requiring massive bailouts, and impossible to ignore. Musk to replace Dimon, makes perfect sense.

“HELOCs have been slowly falling in popularity, and over time the amount of HELOC debt has been gradually falling as people pay down their debts and fewer people take up the slack by borrowing them,” Lewis said. “This seems time for that trend to possibly reverse. The rates on HELOCs are going to be so tempting, especially for people who want to fix up their homes.”

Ugly for everyone, excepts governments. Guess what, they don’t care.

I wonder if the Fed is just making room for a large sale of Treasuries by a country like China?

Or other long term securities by affected Asians. Lower rates now to cushion the effects of selling.

Lower yields mean that demand for bonds is increasing (and bond prices are therefore increasing).

The increasing demand for bonds is a decision to opt for safety by investors.

This increasing demand for bonds suggests that investors are more wary of investing in other categories such as equities, property, etc.

If the economy is as robust as some claim it is, why are investors suing for safety instead? (rhetorical question).

My concern is, that when the central banks exhaust all of their machinations, the distinct possibility that the liabilities of the central banks become nationalised.

The financial/economic system is broken utterly.

Yeah but you missed a very important point or ignored it

which is that long-term rates and short term rates the spread between those

got wider not narrower or negative which would be an increasing sign of recession

all the rates went down yesterday what’s the spread got Wider

so I think you missed the most important point

3) joe’s bros are a potentially bigger liability than bernie’s bros.

hunter is but a part of the iceberg.

Trivia question:

What is the Fed’s THIRD mandate?

Answer: “promote moderate long term rates”.

“It is the Federal Reserve’s actions, as a central bank, to achieve three goals specified by Congress: maximum employment, stable prices, and moderate long-term interest rates in the United States””

The definition of “moderate” is “not extreme”. The Fed has promoted extremely low long term interest rates. Some will say that the Fed can only control short rates, but that is a dodge. With a 4.5 Trillion balance sheet, and other gimmickery, they certainly could sway long rates.

What is the wisdom behind “moderate long rates”? Savers tend to save, there is a second avenue for placing your money other than the stock market, and there is a balance between lenders and borrowers. Debt creation is moderated, costs being weighed against benefit.

Curious that the mantra is always the “dual mandate”. Why is the third ignored?

Lowering interest is the Feds desperate attempt to prevent a mass default of bank debt. It is not designed to improve the economy or boost the Stock Market. The fact is that debt is out of control and the thought of a portion of that debt going into default is what keeps the Fed up at night. The deflation that will follow this pandemic will make much of the debt now carried on books of the banking and bond industries simply not worth paying. People worldwide are about to learn a new lesson about debt.